Saudi Arabia Pathology Lab Services Market Size, Share, Trends and Forecast by Type, Testing Service, End Use, and Region, 2026-2034

Saudi Arabia Pathology Lab Services Market Overview:

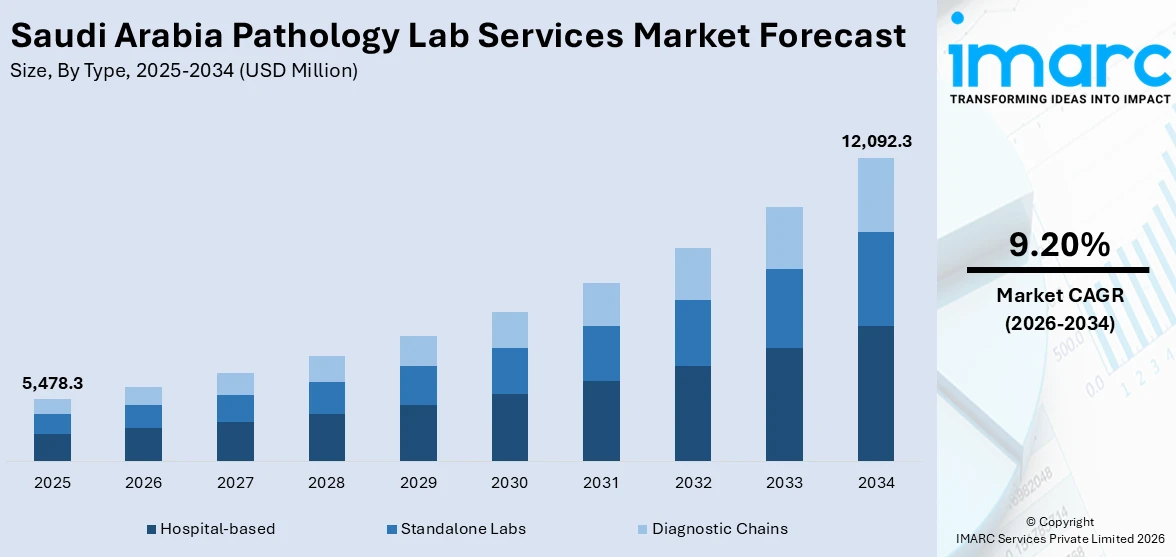

The Saudi Arabia pathology lab services market size reached USD 5,478.3 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 12,092.3 Million by 2034, exhibiting a growth rate (CAGR) of 9.20% during 2026-2034. The market is driven by the rising prevalence of chronic diseases, such as diabetes and cancer, increasing the need for early and accurate diagnostics through advanced technologies. Government initiatives, including Saudi Vision 2030, and private sector investments are accelerating lab modernization, enhancing efficiency and service offerings. Additionally, growing healthcare privatization, outsourcing trends, and expanded insurance coverage are further augmenting the Saudi Arabia pathology lab services market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 5,478.3 Million |

| Market Forecast in 2034 | USD 12,092.3 Million |

| Market Growth Rate 2026-2034 | 9.20% |

Saudi Arabia Pathology Lab Services Market Trends:

Increasing Demand for Advanced Diagnostic Technologies

The market is witnessing an increase in demand for sophisticated diagnostic technologies, propelled by the growing incidences of chronic illnesses and the necessity for early disease identification. According to a recent study, Saudi Arabia shows a prevalence of diabetes at 27.19%, with a significant burden on females (26%) and the young adult population (19%), which has raised public health concerns to a great extent. An increase in diabetes mainly results from inactive lifestyles and improper diets. Additionally, the sudden equal prevalence of Type 1 and Type 2 diabetes could be due to genetic causes, highlighting the need for pathology lab services and tailored prevention methods. Since the rates of diabetes in Saudi Arabia are significantly higher than the international average, the Saudi pathology lab services industry could be vital for early detection and targeted measures to reduce this growing health emergency. With conditions such as diabetes, cardiovascular diseases, and cancer on the rise, healthcare providers are adopting automated histopathology, molecular diagnostics, and digital pathology solutions to enhance accuracy and efficiency. Government initiatives, such as Saudi Vision 2030, are also promoting healthcare modernization, encouraging labs to integrate AI-powered tools and next-generation sequencing (NGS) for precision medicine. Private sector investments are further accelerating the adoption of high-throughput analyzers and telepathology, enabling faster and more reliable test results. As a result, pathology labs are expanding their service portfolios to include genetic testing and personalized diagnostics, catering to a more informed patient population seeking proactive healthcare solutions.

To get more information on this market Request Sample

Growth of Private Pathology Labs and Outsourcing Trends

The significant growth in private-sector labs is also supporting the Saudi Arabia pathology lab services market growth, fueled by increasing healthcare privatization and outsourcing by hospitals. Due to the growing patient load and the need for cost-effective diagnostics, many healthcare facilities are partnering with private labs to manage high testing volumes. This trend is supported by favorable government policies encouraging private investments in healthcare infrastructure. Saudi Arabia has invested over USD 8 Billion in healthcare, of which USD 6.47 Billion went directly towards domestic programs to increase hospital capacity, diagnostics, and laboratory services as part of Vision 2030. To reduce reliance on public health systems, over 110 domestic healthcare agreements have been established, involving investments in diagnostic networks and digital health, which encourages the growth of pathology laboratories. Additionally, corporate wellness programs and insurance coverage expansions are driving demand for routine and specialized lab tests. Private labs are also leveraging partnerships with international diagnostic chains to introduce advanced testing methodologies, improving service quality and turnaround times. As a result, the market is becoming more competitive, with private labs focusing on customer-centric services, home sample collection, and digital reporting to enhance patient convenience and satisfaction.

Saudi Arabia Pathology Lab Services Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on type, testing service, and end use.

Type Insights:

- Hospital-based

- Standalone Labs

- Diagnostic Chains

The report has provided a detailed breakup and analysis of the market based on the type. This includes hospital-based, standalone labs, and diagnostic chains.

Testing Service Insights:

- General Physiological and Clinical Tests

- Imaging and Radiology Tests

- Esoteric Tests

- COVID-19 Tests

A detailed breakup and analysis of the market based on the testing service have also been provided in the report. This includes general physiological and clinical tests, imaging and radiology tests, esoteric tests, and COVID-19 tests.

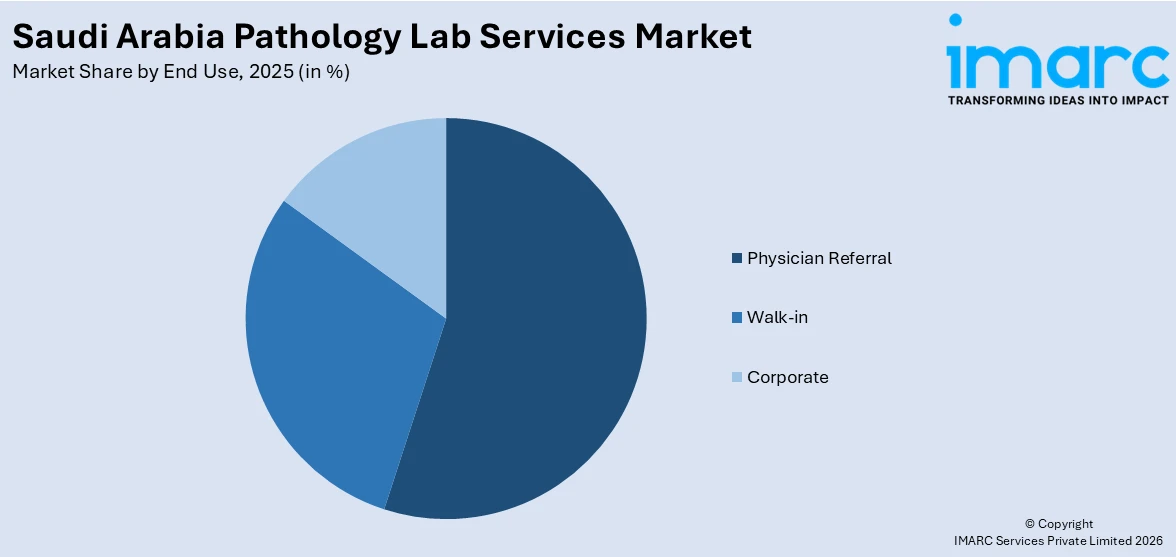

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Physician Referral

- Walk-in

- Corporate

The report has provided a detailed breakup and analysis of the market based on the end use. This includes physician referral, walk-in, and corporate.

Regional Insights:

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

The report has also provided a comprehensive analysis of all the major regional markets, which include Northern and Central Region, Western Region, Eastern Region, and Southern Region.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Saudi Arabia Pathology Lab Services Market News:

- May 19, 2025: King Faisal Specialist Hospital & Research Centre (KFSHRC) launched the MENA region's leading-edge advanced hematology diagnostics laboratory, featuring the region's largest automated hematology track and AI-based image analysis for faster and more precise diagnostics. The center, which features Saudi Arabia's largest clinical flow cytometry facility, performs approximately 9,000 tests annually, offering cutting-edge diagnostics for hematolymphoid and immunological diseases. This state-of-the-art lab sets a new benchmark for pathology services within the Kingdom, enabling clinical research and education alongside encouraging innovation in precision diagnosis.

Saudi Arabia Pathology Lab Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Hospital-based, Standalone Labs, Diagnostic Chains |

| Testing Services Covered | General Physiological and Clinical Tests, Imaging and Radiology Tests, Esoteric Tests, COVID-19 Tests |

| End Uses Covered | Physician Referrals, Walk-in, Corporate |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Saudi Arabia pathology lab services market performed so far and how will it perform in the coming years?

- What is the breakup of the Saudi Arabia pathology lab services market on the basis of type?

- What is the breakup of the Saudi Arabia pathology lab services market on the basis of testing service?

- What is the breakup of the Saudi Arabia pathology lab services market on the basis of end use?

- What is the breakup of the Saudi Arabia pathology lab services market on the basis of region?

- What are the various stages in the value chain of the Saudi Arabia pathology lab services market?

- What are the key driving factors and challenges in the Saudi Arabia pathology lab services market?

- What is the structure of the Saudi Arabia pathology lab services market and who are the key players?

- What is the degree of competition in the Saudi Arabia pathology lab services market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia pathology lab services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia pathology lab services market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia pathology lab services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)