Saudi Arabia Seafood Market Size, Share, Trends and Forecast by Type, Form, Distribution Channel, and Region 2026-2034

Saudi Arabia Seafood Market Size, Share, Trends & Forecast (2026-2034)

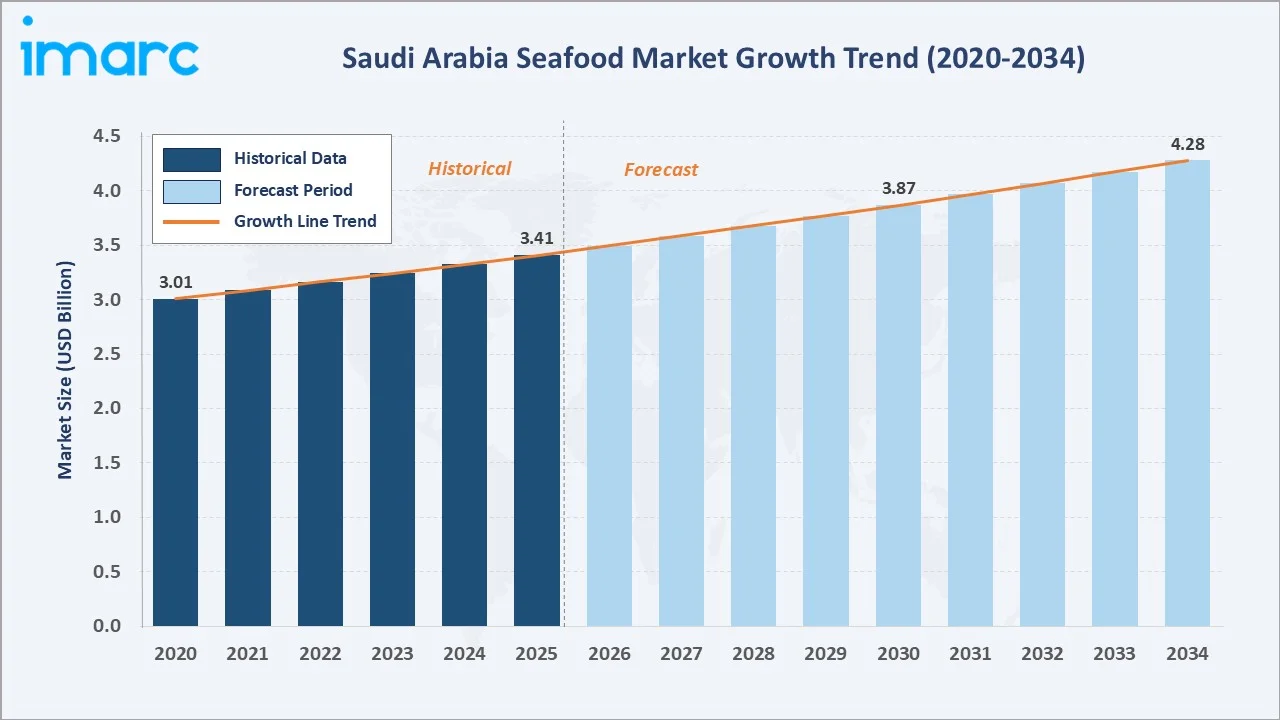

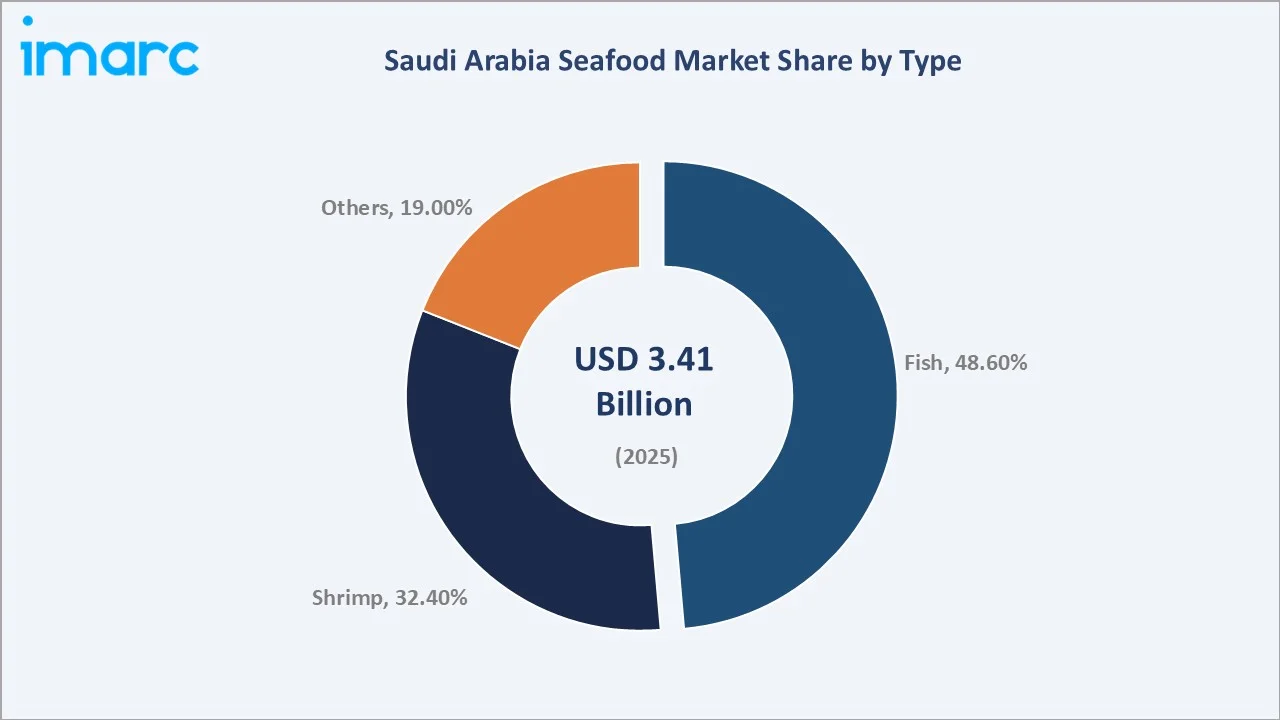

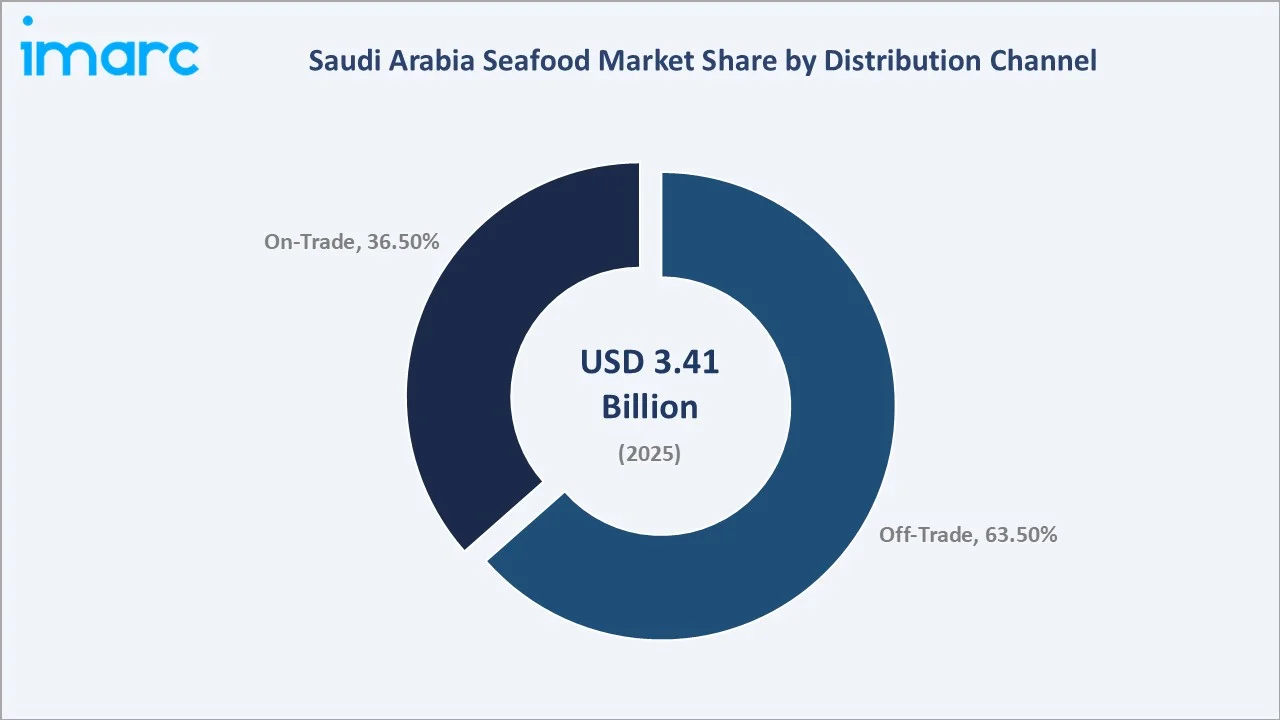

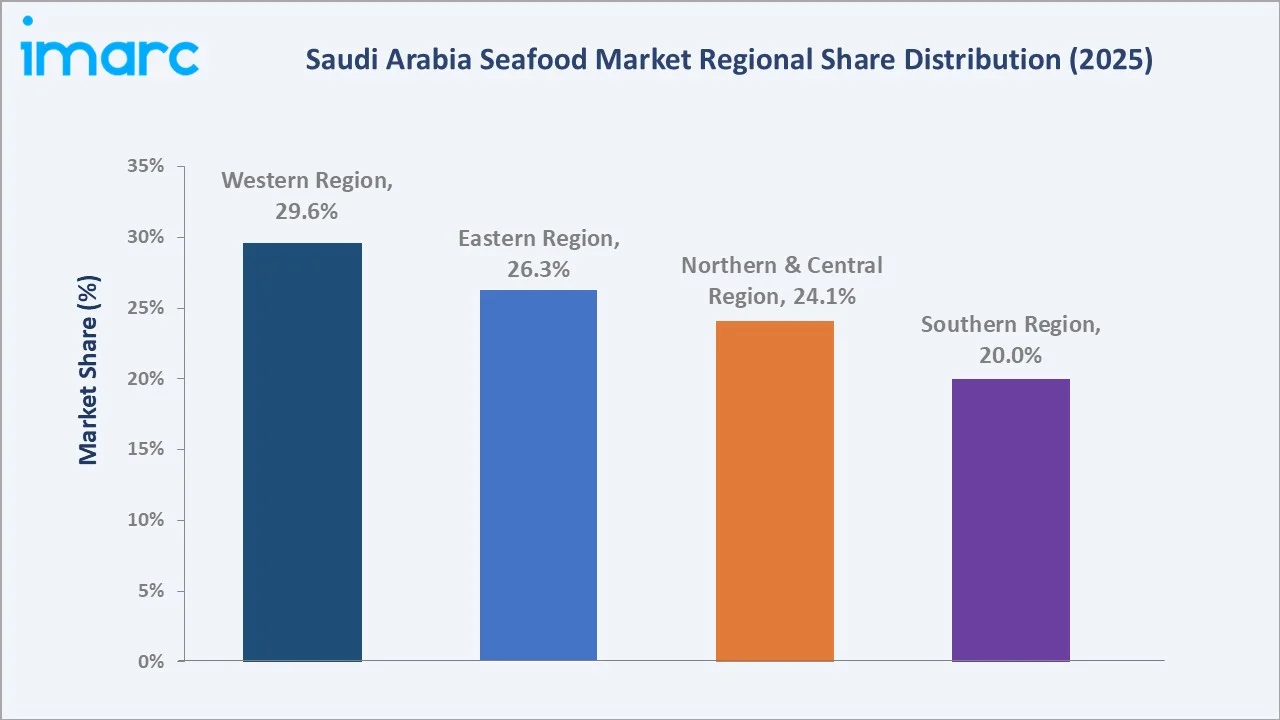

The Saudi Arabia seafood market was valued at USD 3.41 Billion in 2025 and is projected to reach USD 4.28 Billion by 2034, expanding at a CAGR of 2.54% during the forecast period (2026-2034). Growth is driven by Vision 2030’s food security investments, rising health consciousness among the Saudi population, expanding domestic aquaculture capacity, and the rapid growth of tourism and hospitality sectors. Of Saudi Arabia's 7,572 km coastline, approximately 2,400 km is suitable for aquaculture development, spanning the Red Sea to the west and the Arabian Gulf to the east. Fish dominates at 48.6% of market share (2025), while off-trade channels lead distribution at 63.5%. The Western Region holds the largest regional share at 29.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.41 Billion |

|

Forecast Market Size (2034) |

USD 4.28 Billion |

|

CAGR (2026-2034) |

2.54% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Western Region (29.6%, 2025) |

|

Fastest Growing Region |

Eastern Region (CAGR ~2.9%, 2026-2034) |

To get more information on this market, Request Sample

The Saudi Arabia’s seafood market from 2020 through 2034, expanded from USD 3.01 Billion in 2020 to USD 3.41 Billion in 2025, supported by post-COVID recovery, Vision 2030 aquaculture investments, and rising protein consumption. The market is forecast to pass USD 3.87 Billion in 2030 before reaching USD 4.28 Billion by 2034.

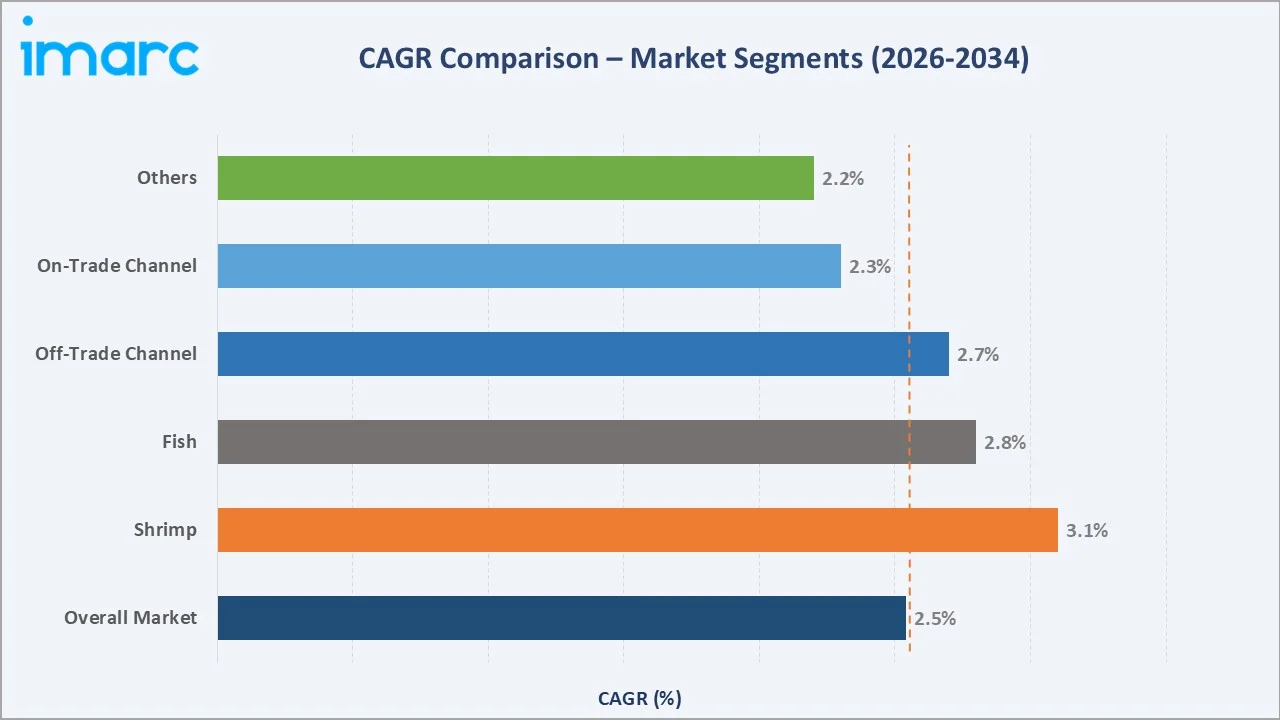

The CAGR across key market segments. Shrimp leads at ~3.1% CAGR, reflecting premium consumer preferences and NAQUA’s expanding shrimp aquaculture capacity. Fish follows at ~2.8% CAGR, while off-trade channels at ~2.7% CAGR outpace on-trade growth, driven by supermarket and online retail expansion across the Kingdom’s major urban centers.

Executive Summary

The Saudi Arabia seafood market occupies a unique position as one of the GCC’s largest and most structurally diverse food categories, combining deep cultural traditions of seafood consumption with Vision 2030’s ambitious food security transformation agenda. From USD 3.01 billion in 2020, the market grew to USD 3.41 billion in 2025, recovering strongly from COVID-19 impacts on the hospitality and food service sectors. The forecast trajectory to USD 4.28 billion by 2034 reflects sustained demographic and tourism demand growth, supported by the government’s Ministry of Environment, Water and Agriculture, which reached up to 100 thousand tons of fisheries products by 2020, and committed to reach 600 thousand tons by 2030..

Fish dominates the type segment at 48.6% (2025), reflecting the deep-rooted cultural significance of fish in Saudi Arabian coastal communities and the increasing availability of premium imported species, including Norwegian salmon, Omani hamour, and Indian tilapia. Shrimp at 32.4% is the fastest-growing type at ~3.1% CAGR, driven by the National Aquaculture Group’s Red Sea shrimp farming expansion and rising demand from the restaurant and hospitality sectors. Off-trade channels dominate at 63.5% as modern supermarket penetration deepens across all Saudi cities.

The Western Region’s 29.6% leadership (2025) reflects Jeddah’s status as Saudi Arabia’s seafood capital, home to the kingdom’s largest commercial fishing port and the primary entry point for imported seafood. The Eastern Region at 26.3% is driven by its large expatriate community and industrial workforce. Northern & Central Region at 24.1% includes Riyadh’s 8+ million metropolitan population, while Southern Region at 20.0% benefits from the Jizan coastal fishing tradition and emerging agri-food investment in the Jizan Economic City.

Key Market Insights

|

Insight |

Data |

|

Largest Seafood Type |

Fish - 48.6% revenue share (2025) |

|

Dominant Distribution Channel |

Off-Trade - 63.5% revenue share (2025) |

|

Leading Region |

Western Region - 29.6% revenue share (2025) |

|

Fastest Growing Region |

Eastern Region (CAGR ~2.9%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Fish dominates at 48.6% (2025): By 2023, aquaculture output surged to 139,949 tons in Saudi Arabia, while fisheries contributed 74,700 tons. Fish consumption per capita in Saudi Arabia stands high, reflecting the kingdom’s dual Red Sea and Arabian Gulf coastline heritage.

- Off-Trade dominates at 63.5% (2025): Modern grocery retail penetration in Saudi Arabia is rising. Dedicated fresh fish counters are now standard in hypermarkets, while frozen seafood aisles have expanded in shelf space.

- Western Region leads at 29.6% (2025): Jeddah’s Islamic Port processes approximately 65% of Saudi Arabia’s seaborne imports. The annual Hajj pilgrimage and Umrah drive extraordinary seasonal seafood demand spikes in the Makkah region.

Saudi Arabia Seafood Market Overview

The Saudi Arabia seafood market encompasses the production, import, processing, distribution, and retail sale of fish, shrimp, and other seafood products across the kingdom’s four geographic regions. Saudi Arabia’s unique position, bordered by both the Red Sea and the Arabian Gulf, provides access to two distinct marine ecosystems supporting artisanal and commercial fishing alongside rapidly expanding aquaculture operations.

Applications span household fresh and frozen seafood consumption, restaurant and hospitality food service, government institutional catering (military, hospitals, schools), and the rapidly growing food delivery and quick-service restaurant channels. Macroeconomic influences include Saudi Arabia’s GDP, the Vision 2030 food security investment program, the kingdom’s growing tourism economy, and the global seafood commodity price cycles driven by fishing quotas, climate change impacts on stocks, and freight cost volatility.

Market Dynamics

To evaluate market opportunities, Request Sample

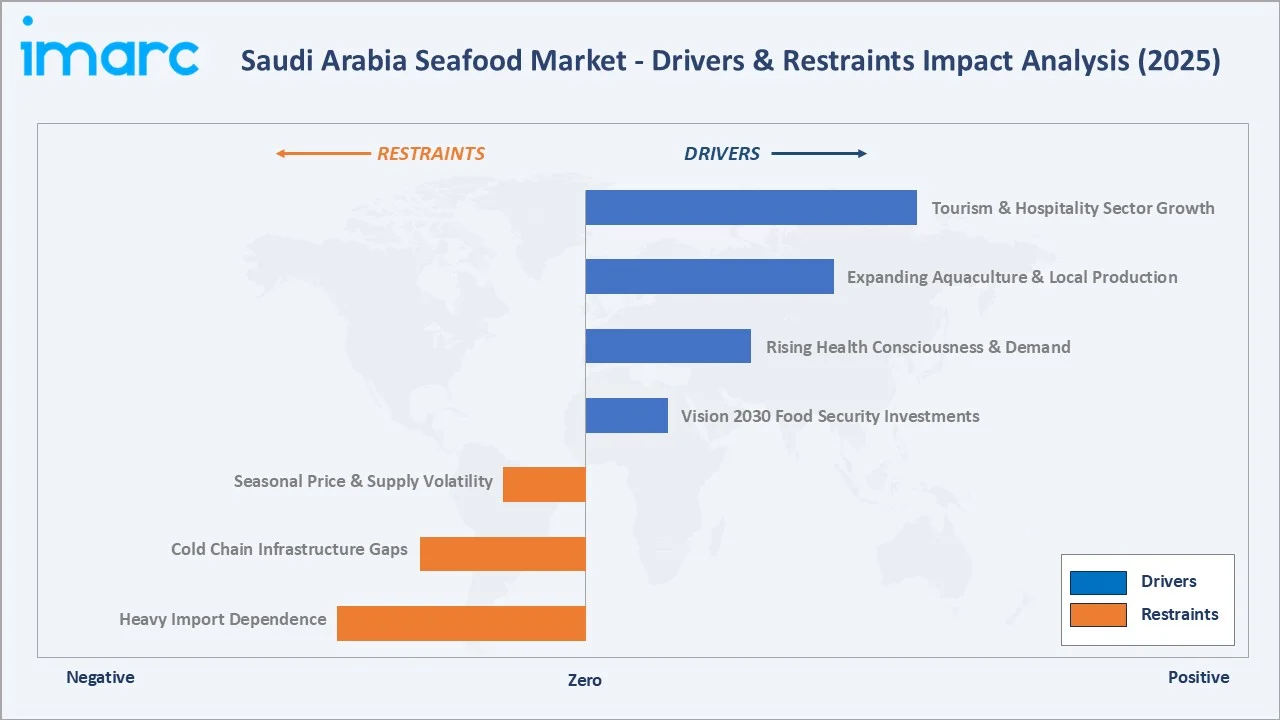

Market Drivers

- Vision 2030 Food Security Strategy and Aquaculture Investment: Saudi Arabia’s projects aim to expand production from 80,000 tons in 2018 to a target of 600,000 tons by 2030. Saudi Arabia's seafood consumption is projected to increase by 7.4% annually until 2030, with rising local demand driven by population growth and higher per capita consumption, leading to an additional 500,000 tons of demand by 2030.

- Rising Health Consciousness and Protein Diversification: Saudi Arabia’s obesity rate reached 35.5%, triggering widespread dietary shift toward lean protein sources, including seafood.

- Tourism and Hospitality Sector Expansion: Saudi Arabia welcomed 116 million domestic and inbound tourists in 2024, on track toward the Vision 2030 target. The tourism sector’s expansion is driving commensurate growth in hotel and restaurant seafood procurement.

- Population Growth and Demographic Dividend: Saudi Arabia’s population reached 35.3 million in 2024. The large and growing Saudi expatriate community brings diverse global seafood consumption traditions that expand the total addressable market.

Market Restraints

- Heavy Import Dependence and Supply Chain Vulnerability: Saudi Arabia imports a high amount of seafood, creating exposure to global commodity price cycles, freight cost volatility, and geopolitical disruptions.

- Cold Chain Infrastructure Gaps in Secondary Cities: While Jeddah, Riyadh, and Dammam have well-developed cold chain logistics for seafood, secondary cities face significant gaps in refrigerated transport, cold storage capacity, and fish handling hygiene standards.

- Seasonal Price and Supply Volatility: Saudi seafood markets experience significant seasonal price volatility, with fresh fish prices rising during Ramadan and Hajj seasons due to demand spikes that import logistics cannot fully smooth.

Market Opportunities

- National Aquaculture Strategy and Domestic Production Scale-Up: Saudi Arabia’s Ministry of Industry and Mineral Resources issued 158 industrial licenses in October 2023, covering shrimp, fish, oyster, and pearl oyster operations.

- Processed and Value-Added Seafood Product Development: Marinated, ready-to-cook, and ready-to-eat (RTE) seafood products represent a growing opportunity aligned with the lifestyle needs of dual-income Saudi households and young professional consumers.

Market Challenges

- SFDA Regulatory Compliance Complexity: The Saudi Food and Drug Authority’s increasingly stringent seafood import, labeling, and food safety regulations, including Halal certification requirements, country-of-origin labeling, and cold chain documentation, create compliance complexity that smaller importers struggle to manage.

- Skilled Labor Scarcity in Aquaculture Operations: Saudi Arabia’s Vision 2030 aquaculture scale-up requires more skilled aquaculture technicians, feed specialists, and cold chain operations staff that the current Saudi labor market cannot supply. Saudization requirements limiting expatriate worker percentages create additional recruitment challenges.

Emerging Market Trends

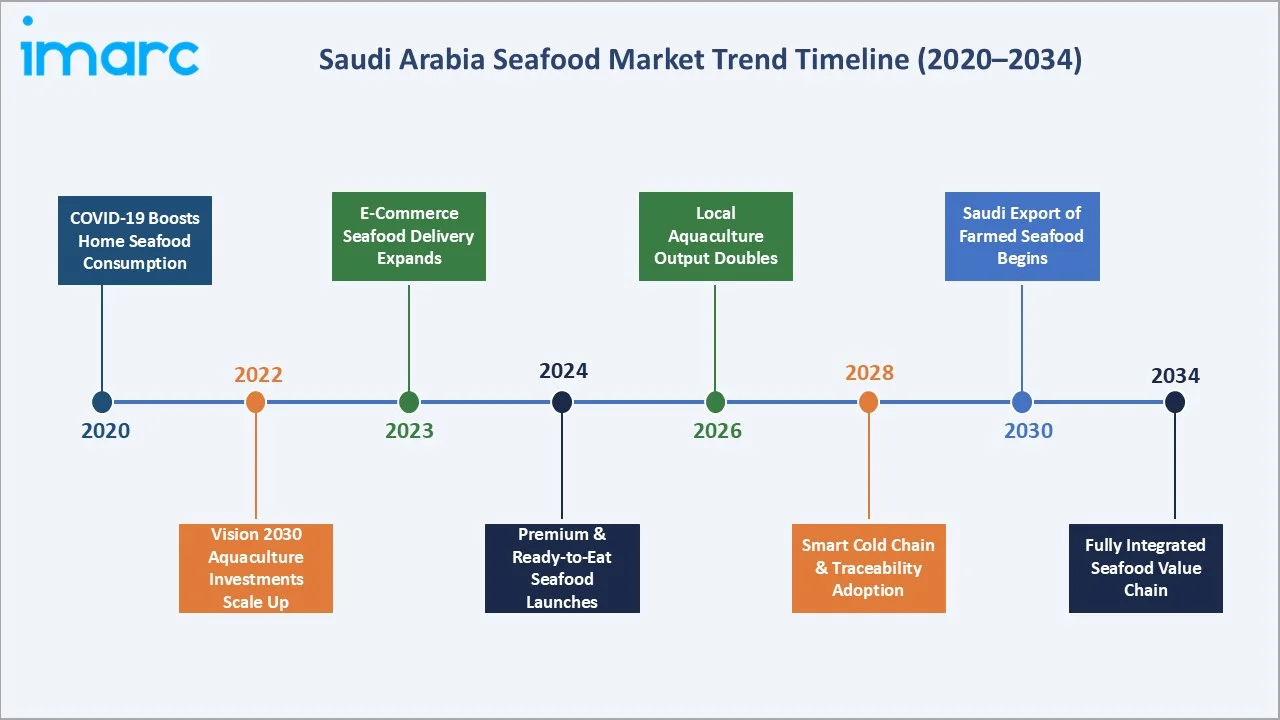

1. Premium and Sustainable Seafood Gaining Market Share

Saudi consumers’ rising disposable incomes and health awareness are driving a premiumization trend. Certified sustainable seafood is now stocked, with premium consumers in Riyadh and Jeddah demonstrating price premium acceptance for sustainability-certified products.

2. Online and Dark Kitchen Seafood Delivery Mainstreaming

Ghost kitchens and dark kitchens dedicated to seafood preparation are serving the rapidly growing online food delivery market.

3. Processed and Ready-to-Cook Seafood Growth

Saudi Arabia’s working women population, which jumped from 17% in 2015 to 36.2% in Q3 2024 under Vision 2030, is driving demand for convenience food solutions. Marinated, portion-cut, and ready-to-grill seafood products are growing in supermarket categories.

4. NEOM and Giga-Project Hospitality Demand Creation

Saudi Arabia’s giga-projects, such as NEOM (USD 500 Billion), are developing additional annual visitors by 2030 with seafood-intensive resort and hospitality environments.

Industry Value Chain Analysis

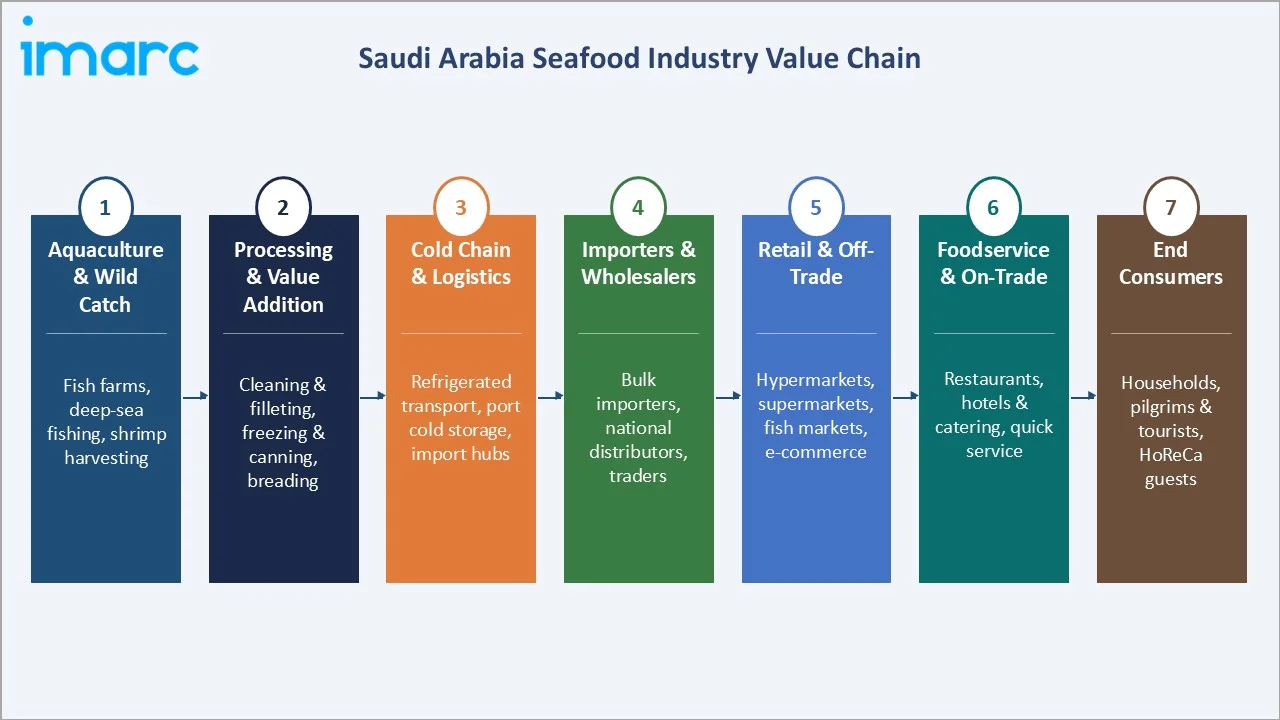

The Saudi Arabia seafood value chain spans wild capture fishing and aquaculture production through international import, domestic processing, cold chain logistics, and final consumer delivery across four distinct regional markets.

|

Stage |

Key Players & Examples |

|

Fishing & Aquaculture |

Wild-catch: Red Sea and Arabian Gulf traditional fishing fleets; Aquaculture: NAQUA (shrimp, fish), Saudi Fisheries Company, Tabuk Fisheries, Arabian Shrimp Company |

|

Processing & Quality Control |

Fish packing, processing, export, and SFDA halal certification are mandatory for all facilities |

|

Cold Chain & Storage |

Cold storage network, frozen distribution, refrigerated transport |

|

Retail & Foodservice |

Off-trade: Panda Retail, LuLu Group, online, On-trade: restaurants, hotel foodservice, Hajj/Umrah catering |

|

End Consumers |

Saudi national households, expatriate population, Hajj/Umrah pilgrims, hotel & resort guests, institutional buyers (hospitals, schools, military) |

The processing and distribution stages capture the highest margin layers in the Saudi seafood value chain. Premium importers achieve gross margins on Norwegian salmon through direct sourcing relationships and cold chain ownership. Traditional fish souk operators at the retail end operate on 10–18% margins, while modern supermarket seafood counters command 25–35% gross margins on fresh fish through value-added services including filleting, marinating, and portioning.

Technology Landscape in the Saudi Arabia Seafood Industry

Recirculating Aquaculture Systems (RAS) for Desert Conditions

Saudi Arabia’s Vision 2030 aquaculture expansion is uniquely dependent on Recirculating Aquaculture Systems (RAS), closed-loop water management technology that enables fish farming in the kingdom’s arid climate with water recycling efficiency.

Cold Chain Technology and IoT-Enabled Freshness Monitoring

The Saudi Arabis aims to boost domestic aquaculture production from 280,000 tons in 2024 to 530,000 tons annually by 2030. The cold chain technology and freshness monitoring are highly crucial with the rising aquaculture production. Saudi Arabia’s seafood cold chain is being modernized through IoT temperature monitoring sensors, blockchain-based provenance tracking, and smart refrigeration systems that maintain 0–2°C throughout the supply chain.

E-Commerce and Last-Mile Seafood Delivery Technology

Saudi seafood e-commerce is leveraging GPS-tracked refrigerated motorcycle delivery, AI-driven demand forecasting for fish souk digital integration, and customer-facing freshness scoring apps that display catch date, origin, and storage time for online purchased seafood.

Halal-Certified Processing and Traceability Systems

Saudi Arabia’s mandatory Halal certification for all processed seafood (SFDA Regulation) requires end-to-end documentation from catch or farm to consumer. RFID-tagged fish crates, electronic catch certificates, and blockchain-based supply chain verification systems are being piloted by MEWA and major importers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | Fish | 48.6% |

2025 |

| Form | 🔒 | 🔒 |

2025 |

| Distribution Channel | Off-Trade | 63.5% |

2025 |

| Region | Western Region | 29.6% |

2025 |

By Type

To access detailed market analysis, Request Sample

Fish dominates with 48.6% market share (2025). The fish category spans an extraordinary diversity of species, from the culturally revered hamour to affordable tilapia. The Saudi Arabian Ministry of Environment, Water and Agriculture has reached up to 100 thousand tons of fisheries products by 2020 and is committed to reach 600 thousand tons by 2030.

Shrimp at 32.4% is the fastest-growing segment at ~3.1% CAGR through 2034. Others at 19.0% include crab, squid, octopus, lobster, and shellfish, predominantly served in premium restaurants and hotels.

By Distribution Channel

Off-trade channels dominate with 63.5% market share (2025). This encompasses supermarkets and hypermarkets, traditional fish markets and souks, online delivery, and convenience stores. Panda Retail’s with the highest consideration score (of 32.3) have all invested heavily in fresh seafood counter expansion, seafood processing in-store, and premium frozen seafood aisle development.

On-trade channels at 36.5% are growing at ~2.3% CAGR through 2034. Large-scale catering for NEOM and giga-project construction camps feeds a huge number of workers daily, a segment with significant and growing seafood requirements.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Western Region |

29.6% |

Jeddah port access, Hajj/Umrah tourism surge, Makkah hospitality sector, Red Sea coastal fishing tradition |

|

Eastern Region |

26.3% |

Dammam petrochemical industry worker demand, expat community in Khobar/Dhahran, Al-Ahsa agri-food development, industrial aquaculture |

|

Northern & Central Region |

24.1% |

Riyadh capital city population, Vision 2030 NEOM project Tabuk demand, Al-Ula tourism development, government employee spending |

|

Southern Region |

20.0% |

Asir and Jizan coastal fishing communities, traditional seafood culture, Jizan Economic City agri-food investment, tourism development |

The Western region’s 29.6% market share (2025) is structurally supported by Jeddah’s Islamic Port, Saudi Arabia’s primary seafood import gateway, processing seafood imports. The region’s Red Sea coastline also supports the most active artisanal and commercial fishing fleet in the kingdom. Makkah and Madinah’s extraordinary annual visitor flows create demand spikes that make the Western Region the highest-peak-demand market for both premium and commodity seafood formats.

The Eastern region at 26.3% (2025) hosts Saudi Arabia’s largest expatriate community, predominantly South Asian and Southeast Asian workers with strong cultural seafood traditions. Northern & Central region at 24.1% (2025) represents the inland market centered on Riyadh, which, despite having no coastline is Saudi Arabia’s largest city by population.

Competitive Landscape

The Saudi Arabia seafood market is moderately fragmented. The top five players, Almunajem Foods, National Aquaculture Group, Arab Fisheries, IZAFCO, and Shell Fisheries, collectively account for approximately 40–45% of market revenue, with the remainder shared among dozens of regional importers, distributors, and souk operators.

|

Company Name |

Product Line |

Market Position |

Core Strength |

|

Almunajem Foods |

Shrimps, Fish FPP |

Market Leader |

Saudi Arabia’s one of the largest integrated food import and distribution company |

|

National Aquaculture Group (NAQUA) |

Red Sea Shrimp, Red Sea Barramundi |

Market Leader |

Largest domestic aquaculture producer; Vision 2030 strategic partner; Red Sea shrimp farms |

|

Arab Fisheries CO. |

Fish, Molluscs, and Crustaceans |

Strong Challenger |

Pioneer of Saudi commercial fishing; strong government supply relationships |

|

IZAFCO LLC |

Frozen and Fresh Fishes |

Strong Challenger |

Leading frozen seafood importer and distributor, strong hypermarket and restaurant channel penetration across all regions |

|

Shell Fisheries |

Shell and Maydar (2 Seafood Brands), Frozen Fillet, Frozen Steaked Fish, Frozen Crustacean, Frozen Mollusc, Breaded Seafood |

Specialist |

Specialty shellfish and crustacean importer; upscale restaurant and hotel supply focus |

Competitive differentiation is driven by cold chain infrastructure ownership, import supplier relationships, government panel contracts, and brand recognition in modern retail channels.

Key Company Profiles

Almunajem Foods

Almunajem Foods is one of the Saudi Arabia’s largest integrated food import, distribution, and retail companies, with seafood representing a significant revenue pillar within its diversified food portfolio.

- Product Portfolio: Shrimps, Fish FPP, Tuna.

- Recent Developments: In May 2025, Almunajem Foods Co. receives the necessary approvals from the relevant authorities to commence operations of its previously approved limited liability subsidiary, Optimal Solution for Logistics Services Co. (Loadly), under Commercial Registration No. 1009107581.

- Strategic Focus: Premium import and brand-building for Norwegian and Scottish salmon; national cold chain infrastructure expansion to capture Vision 2030 tourism growth; corporate catering and HORECA channel deepening; digital ordering platform for B2B institutional clients.

National Aquaculture Group (NAQUA)

NAQUA is Saudi Arabia’s premier domestic aquaculture company and a strategic partner of the Ministry of Environment, Water and Agriculture in the Vision 2030 aquaculture scale-up program. The company operates Red Sea shrimp farming facilities.

- Product Portfolio: Red Sea Shrimp, Red Sea Barramundi.

- Recent Developments: In November 2023, National Aquaculture Group (NAQUA) planned to increase its seafood output by more than 400% over the next seven years.

- Strategic Focus: Domestic shrimp production leadership targeting 40,000 MT/year by 2028; NAQUA brand development as premium domestic origin alternative to imports; partnership with MEWA on aquaculture technology transfer and Saudization of technical workforce; potential Red Sea export program to GCC countries.

Arab Fisheries CO.

Arab Fisheries CO. is one of Saudi Arabia’s oldest commercial fishing companies, operating a fleet of fishing vessels in both the Red Sea and Arabian Gulf alongside onshore processing and distribution capabilities.

- Product Portfolio: Fishes, Molluscs, and Crustaceans.

- Recent Developments: Expanded fishing fleet with 8 new vessels under Saudi Aramco Build-Saudi-Build initiative.

- Strategic Focus: Fleet modernization for higher catch efficiency and reduced bycatch for sustainability certification; processing capacity expansion for value-added fish products; institutional B2B supply growth for government entities and hospital catering; potential MSC certification for Red Sea fisheries.

IZAFCO LLC

IZAFCO LLC is a leading frozen and processed seafood importer and distributor serving the Saudi Arabian market with an extensive portfolio of frozen fish, shrimp, squid, and shellfish products.

- Product Portfolio: Frozen and Fresh Fishes.

- Recent Developments: Expanded private-label frozen seafood range and established new cold storage facility.

- Strategic Focus: Private label brand development as margin improvement strategy versus commodity import; Central Region (Riyadh) market share growth through improved logistics; halal-certified processing partnerships in source countries; value-added product range expansion for the convenience-oriented Saudi consumer segment.

Market Concentration Analysis

The Saudi Arabia seafood market exhibits moderate fragmentation at the distribution level and low-to-moderate concentration at the top-tier operator level. The top five companies, Almunajem Foods, National Aquaculture Group, Arab Fisheries, IZAFCO, and Shell Fisheries, collectively account for an estimated 38–42% of total market revenue. The next tier of 10–15 mid-size importers and distributors captures approximately 25–30%, with the remaining 28–35% distributed among hundreds of small regional importers, souk operators, and artisanal fishing cooperatives.

The traditional fish souk sector is effectively outside the formal concentration analysis, operating as a highly fragmented network of individual traders. This informal sector is a structural feature of Saudi seafood retail that will gradually formalize as Vision 2030 initiatives modernize seafood market infrastructure, but full formalization is a 15–20 year horizon rather than a near-term probability.

Investment & Growth Opportunities

Fastest Growing Segments

Shrimp (CAGR ~3.1%), off-trade channels (CAGR ~2.7%), and premium processed/value-added seafood represent the three highest-growth investment vectors through 2034. Domestic aquaculture production investment represents the single largest capital allocation opportunity in the Saudi food sector, with MEWA aquaculture licensing applications growth.

Emerging Growth Markets

NEOM’s aquaculture campus in the Gulf of Aqaba and The Red Sea Project create geographically distinct premium seafood demand and supply infrastructure that requires dedicated investment. The Jizan Economic City (JEC)’s food processing zone is attracting seafood processing investment from Indian and Thai operators seeking to establish Saudi-based halal-certified processing for GCC distribution, potentially creating a new export-oriented seafood processing hub.

Venture Investment Trends

Saudi Arabia’s seafood sector is attracting growing venture and institutional investment through MEWA’s Agricultural Development Fund (ADF). The Saudi Agricultural and Livestock Investment Company (SALIC) is actively evaluating upstream aquaculture partnerships. Digital seafood startup activity is nascent but growing.

- Key investment themes: RAS aquaculture technology for premium species, branded domestic seafood, e-commerce fresh seafood delivery, halal-certified processing for export, and luxury resort seafood supply chains.

- International partnership interest: Norwegian salmon companies, Dutch aquaculture engineering firms, Thai seafood processors, and Indian shrimp farmers are all actively evaluating Saudi Arabia partnership or investment opportunities enabled by Vision 2030 aquaculture incentives.

Future Market Outlook (2026-2034)

The Saudi Arabia seafood market is positioned for steady, multi-driver growth through 2034. From USD 3.41 Billion in 2025, the market is forecast to reach USD 4.28 Billion by 2034, an absolute value addition of USD 870 million at a 2.54% CAGR. This growth narrative is fundamentally different from most other Saudi food categories because it operates on two distinct tracks simultaneously: a domestic consumption demand track driven by population growth, health trends, and rising incomes; and a structural supply-side transformation track driven by Vision 2030’s aquaculture program that will fundamentally reshape the origin mix of seafood available in Saudi markets.

Between 2026 and 2030, the most significant market development will be the first major scale-up of domestic aquaculture production, reducing Saudi Arabia’s seafood import dependence. This is not merely a supply chain story, it will reshape brand, quality, and pricing dynamics across all seafood categories. Saudi-branded domestic shrimp and fish will command price premiums over imported equivalents, improving industry revenue per ton metrics even as volumes grow modestly.

Research Methodology

Primary Research

Primary research for this report included structured interviews with 110+ industry stakeholders in 2025, comprising Saudi seafood importers, MEWA aquaculture officers, supermarket seafood category managers, restaurant procurement directors, food service distributors, and market analysts covering the Saudi food sector. All primary interviews were conducted in Saudi Arabia and key exporting countries. Primary insights validated market sizing, regional share estimates, and aquaculture production capacity projections.

Secondary Research

Secondary research encompassed MEWA fisheries and aquaculture statistics, SFDA food import records, FAO global seafood production and trade data, Saudi General Authority of Statistics household expenditure surveys, Tourism Authority visitor data, Vision 2030 investment documentation, company annual reports, and trade publications. Over 220 secondary sources were reviewed and cross-validated.

Forecasting Models

Market size forecasts were developed using a bottom-up demand modeling approach validated against top-down import trade value data and domestic production volume estimates. Key inputs include Saudi population projections, tourist arrival forecasts, Vision 2030 aquaculture production timelines, and GCC seafood price indices. Three-scenario modelling was applied across 2026-2034.

Saudi Arabia Seafood Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fish, Shrimp, Others |

| Forms Covered | Fresh / Chilled, Frozen / Canned, Processed |

| Distribution Channels Covered |

|

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | Almunajem Foods, National Aquaculture Group (NAQUA), Arab Fisheries CO., IZAFCO LLC, Shell Fisheries, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia seafood market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia seafood market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia seafood industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Seafood Market Report

The Saudi Arabia seafood market was valued at USD 3.41 Billion in 2025 and is projected to reach USD 4.28 Billion by 2034, growing at a CAGR of 2.54%.

The Western Region leads with 29.6% revenue share (2025), driven by Jeddah port seafood imports, Red Sea fishing tradition, and Hajj/Umrah tourism demand spikes.

Fish leads with 48.6% market share (2025), driven by cultural preference for hamour and other Red Sea species, combined with growing imported salmon consumption.

Shrimp is the fastest growing type at ~3.1% CAGR, driven by National Aquaculture Group’s Red Sea shrimp farming expansion and rising hospitality sector demand.

Off-trade channels dominate with 63.5% share (2025), led by hypermarkets and supermarkets, including Panda, Al-Raya, Carrefour, and Lulu across all regions.

Key players include Almunajem Foods, National Aquaculture Group (NAQUA), Arab Fisheries CO., IZAFCO LLC, and Shell Fisheries.

Vision 2030’s aquaculture strategy targets 600,000 MT domestic production by 2030, backed by investment incentives, significantly reducing the current import dependence.

Key trends include premium seafood premiumization, Saudi-branded domestic aquaculture products, e-commerce delivery growth, NEOM giga-project demand, and processed seafood convenience expansion.

Key challenges include import dependence, cold chain gaps in secondary cities, SFDA regulatory compliance complexity, traditional souk informality, and skilled aquaculture workforce shortages.

Top opportunities include RAS aquaculture technology investment, Vision 2030 domestic production partnerships, e-commerce seafood delivery platforms, NEOM luxury resort supply chains, and halal-certified export processing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)