Saudi Arabia Snacks Market Size, Share, Trends and Forecast by Product, Packaging, Distribution Channel, and Region, 2026-2034

Saudi Arabia Snacks Market Size, Share, Trends & Forecast (2026-2034)

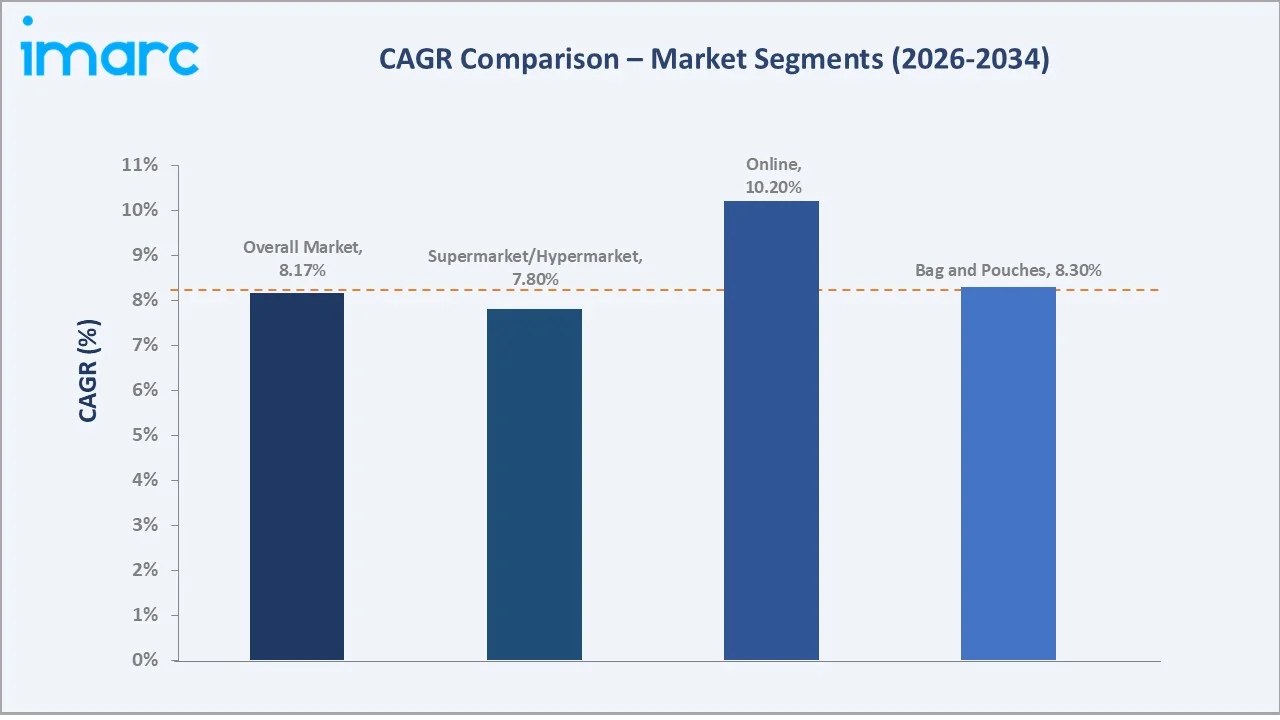

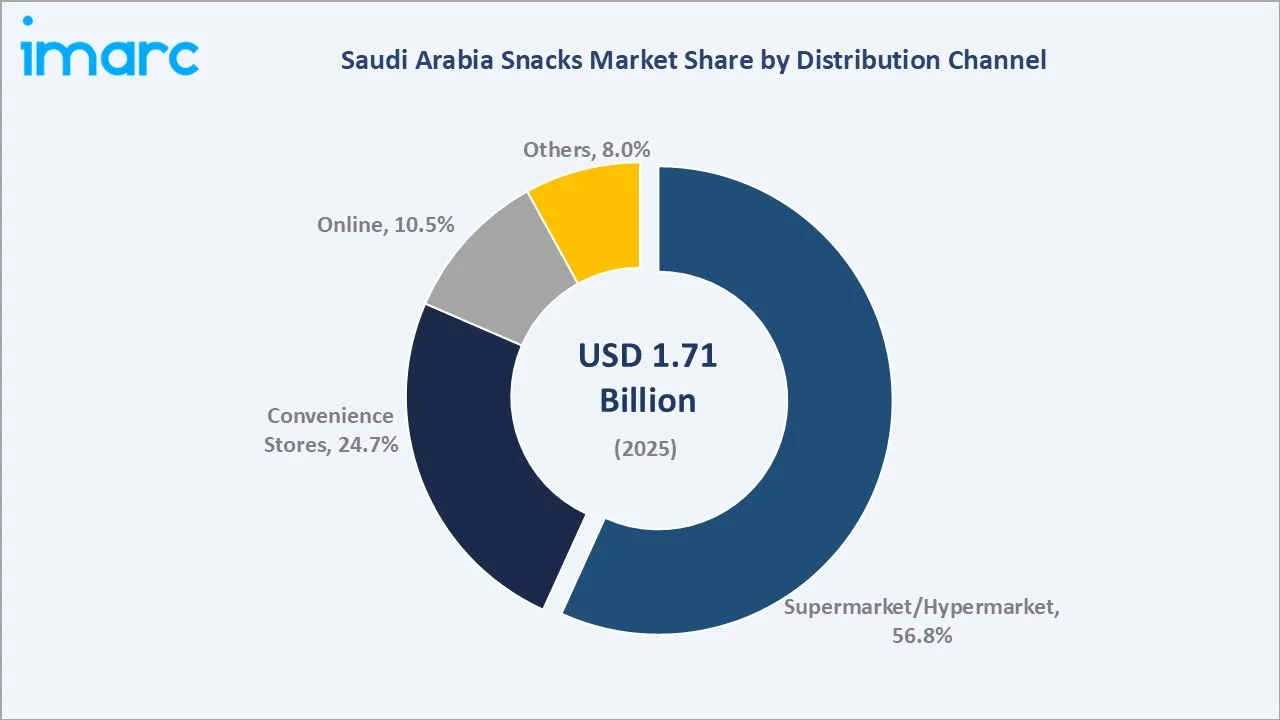

The Saudi Arabia snacks market reached USD 1.71 Billion in 2025 and is projected to reach USD 3.47 Billion by 2034, exhibiting a CAGR of 8.17% during 2026-2034. The market is fueled by a youthful, urbanized population, rising disposable incomes, and growing demand for convenient food options. E-commerce expansion and health-conscious snacking further accelerate growth. Supermarket/hypermarket dominate at 56.8% distribution share, while bag and pouch packaging leads at 49.3%. The Northern and Central Region commands the largest regional share at 37.9%, driven by high population density and economic activity in Riyadh.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.71 Billion |

|

Forecast Market Size (2034) |

USD 3.47 Billion |

|

CAGR (2026-2034) |

8.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Distribution Channel |

Supermarket/Hypermarket (56.8%, 2025) |

|

Largest Packaging Type |

Bag and Pouches (49.3%, 2025) |

|

Dominant Region |

Northern & Central Region (37.9%, 2025) |

The market expanded from USD 1.16 Billion in 2020 to USD 1.71 Billion in 2025. It is anchored at USD 2.54 Billion in 2030, before reaching USD 3.47 Billion by 2034. Growth is supported by Vision 2030 economic diversification, rising youth population, and digital retail expansion.

.webp)

To get more information on this market, Request Sample

Online distribution channels grow fastest at approximately 10.2% CAGR (2026-2034), driven by rising smartphone penetration and e-commerce platforms offering diverse snack selections. Bag and pouches packaging grows at 8.3% CAGR, reflecting consumer preference for resealable, on-the-go formats.

Executive Summary

The Saudi Arabia snacks market reached USD 1.71 Billion in 2025, underpinned by a rapidly urbanizing population, rising household incomes, and evolving snack consumption patterns across the Kingdom. Saudi Arabia's population of over 36 million - over 80% urban - creates a sizeable consumer base for convenience foods and packaged snacks. The market is forecast to reach USD 3.47 Billion by 2034, at a 8.17% CAGR, as health-conscious, premium, and globally-inspired snack options gain traction.

Supermarket/hypermarket dominate distribution at 56.8% share (2025), anchored by extensive modern retail infrastructure in Riyadh, Jeddah, and Dammam. Online channels at 10.5% are the fastest-growing, driven by food delivery apps and grocery e-commerce adoption. Bag and pouches packaging holds 49.3% segment share, favored for portability and freshness retention.

The Northern and Central Region commands 37.9% regional share, driven by Riyadh's concentration of retail outlets and high consumer purchasing power. Government health initiatives under Vision 2030's Quality of Life Program are influencing shifts toward functional and better-for-you snack categories, driving innovation across the competitive landscape.

Key Market Insights

|

Insight |

Data |

|

Largest Distribution Channel |

Supermarket/Hypermarket - 56.8% share (2025) |

|

Largest Packaging Type |

Bag and Pouches - 49.3% share (2025) |

|

Fastest Growing Channel |

Online - ~10.2% CAGR (2026-2034) |

|

Dominant Region |

Northern & Central Region - 37.9% share (2025) |

|

Major Players |

PepsiCo, Inc., Mondelēz International, Nestlé S.A., Almarai Company, and Bahlsen GmbH & Co. KG |

|

Key Trend |

Premiumization and global flavor adoption |

Key Analytical Observations Supporting The Above Data:

- Supermarket/Hypermarket at 56.8% share (2025) reflects strong modern retail infrastructure - Saudi Arabia's top retailers such as Panda Retail, Lulu Hypermarket, and Carrefour KSA cover major urban centers, providing broad snack shelf space and promotional platforms for leading brands.

- Bag and Pouches at 49.3% packaging share (2025) aligns with consumer preference for resealable, portable formats suitable for on-the-go snacking - a behavior reinforced by Saudi Arabia's high vehicle usage rates and active outdoor lifestyles.

- Online channels at 10.5% (2025) growing fastest at ~10.2% CAGR - Saudi Arabia ranked among MENA's leading e-commerce markets with smartphone penetration above 95%, enabling food-delivery apps and online grocers to capture a growing share of snack purchases.

- Northern and Central Region at 37.9% dominance anchored by Riyadh - Saudi Arabia's capital city houses the highest concentration of modern retail formats, food courts, and entertainment venues driving premium snack consumption.

Saudi Arabia Snacks Market Overview

Saudi Arabia's snacks market encompasses all packaged and processed snack categories sold through retail, foodservice, and digital channels within the Kingdom. Product categories include savory snacks, confectionery, bakery snacks, fruit snacks, dairy snacks, and frozen/refrigerated snack items. The market operates within Saudi Arabia's Food and Drug Authority (SFDA) regulatory framework, responsible for setting mandatory food safety, labeling, and quality standards for all food products sold in the Kingdom.

.webp)

Macroeconomic tailwinds include Vision 2030's economic diversification, rising non-oil GDP growth, expanding middle class, and government-backed entertainment and tourism initiatives that elevate snack consumption occasions. Saudi Arabia's young demographic profile, over 40% of the population below 25 years, creates a structurally favorable consumer base for diverse and innovative snack formats.

Market Dynamics

.webp)

To evaluate market opportunities, Request Sample

Market Drivers

- Young, Urbanized Population Driving Convenience Food Demand: Saudi Arabia's population exceeds 36 million (2025), with over 80% living in urban areas and more than 40% below the age of 25. This demographic profile creates inherent demand for convenient, portable snack formats. Young Saudi consumers actively seek variety, global flavors, and innovative snack experiences, consistently driving product launch activity across the snack segment.

- Rising Disposable Incomes Enabling Premium Snack Spending: Saudi per capita GDP reached approximately USD 35,122 in 2024, supporting discretionary food spending. The expanding Saudi middle class is trading up to premium snack brands, gourmet flavors, and imported specialty products, lifting average selling prices and revenue per unit across the market.

- E-Commerce and Food Delivery App Expansion: Saudi Arabia's e-commerce sector grew at double-digit rates through 2024-2025, with food and grocery delivery platforms such as Noon Food and Jahez expanding snack product selections significantly. Online snack discovery and purchase is increasing, particularly among younger, digitally-native consumers in Riyadh and Jeddah.

- Vision 2030 Entertainment and Tourism Expansion Creating New Snack Occasions: Giga-projects including NEOM, Diriyah Gate, Qiddiya Entertainment City, and Red Sea Global tourism destinations are creating new high-frequency snack consumption environments. Stadiums, theme parks, cinemas, and outdoor event venues drive impulse snack purchase volumes.

Market Restraints

- Import Dependency and Supply Chain Vulnerability: Saudi Arabia imports a significant share of its packaged snack products. Global supply chain disruptions, freight cost volatility, and USD-SAR currency linkage create margin pressures for importers and price volatility for consumers in the budget snack segment.

- Health Regulatory Pressure on High-Sugar and High-Fat Snacks: Saudi Arabia's SFDA enforces front-of-pack nutrition labeling requirements, while ZATCA administers excise taxes on carbonated beverages, with similar measures under discussion for confectionery and high-fat snack categories. These regulatory measures constrain volume growth in traditional confectionery and fried snack categories.

- Price Sensitivity in Budget Segment Limiting Premium Penetration: While premium snack demand is growing, a large portion of Saudi Arabia's expatriate population - which accounts for over 40% of the total population - remains highly price-sensitive, constraining volume growth in premium segments and sustaining intense competition in the value-tier snack category.

Market Opportunities

- Health and Functional Snacking Innovation: Saudi Arabia's government Quality of Life Program and rising health awareness among Saudi consumers create a substantial opportunity for protein bars, organic snacks, low-sugar confectionery, and functional snacks enriched with vitamins and minerals. The functional snack segment is in early growth stages, offering high-margin product development pathways.

- Local Flavor Innovation and Saudi Brand Development: Growing Saudi consumer pride and demand for locally-inspired flavors, including za'atar, saffron-spiced nuts, and date-based confectionery, create opportunities for local snack manufacturers to develop distinct product lines that resonate with national identity while meeting SFDA quality standards.

- D2C and Subscription Snack Box Models: Saudi Arabia's high digital adoption rates and young population support direct-to-consumer snack subscription services delivering curated snack selections monthly. This model enables emerging snack brands to acquire customers cost-effectively while building recurring revenue streams.

Market Challenges

- Intense Competition from Multinational Snack Brands: Global majors including PepsiCo (Lay's, Cheetos), Mondelēz International (Oreo, Cadbury), and Nestlé maintain strong Saudi market positions through established distribution networks, high marketing investment, and loyal consumer bases - creating significant barriers for emerging local and regional snack brands.

- Rapid Trend Cycles Requiring Frequent Product Reformulation: Saudi consumers - highly exposed to global food trends via social media platforms including TikTok and Instagram - drive rapid flavor and format trend cycles. Snack manufacturers must invest continuously in product development and limited-edition launches to remain relevant, increasing R&D costs and inventory complexity.

Emerging Market Trends

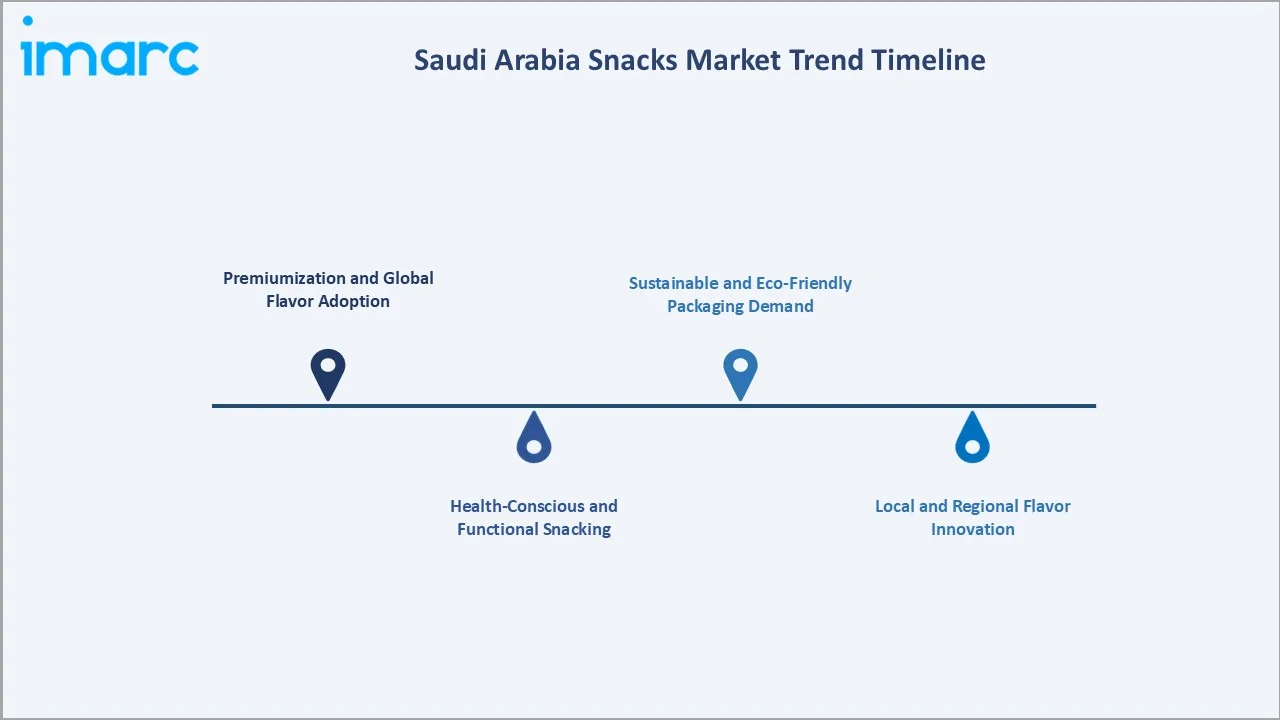

1. Premiumization and Global Flavor Adoption

Saudi consumers increasingly seek premium snack products with international flavor profiles, including South Korean spicy chips, American cheese puffs, and Japanese matcha confectionery. Specialty retailers and online platforms are expanding imported snack ranges, while domestic brands launch premium lines targeting the quality-seeking middle class. The premium snack segment is growing above the overall market CAGR, reflecting sustained trade-up behavior.

2. Health-Conscious and Functional Snacking

Demand for low-calorie, high-protein, gluten-free, and organic snacks is accelerating as Saudi consumers respond to rising diabetes and obesity concerns. The Saudi Ministry of Health's Quality of Life Program targets a 10% reduction in diabetes cases by 2030, directly influencing consumer behavior. Protein bars, roasted nuts, dried fruits, and baked (non-fried) snack alternatives are outperforming traditional fried snack categories in growth rate.

3. Digital Commerce and Social Media-Driven Discovery

Online grocery platforms and food delivery apps are becoming primary snack discovery and purchase channels for Saudi Arabia's digitally connected youth. Social media influencers on Instagram, TikTok, and Snapchat generate viral trends around specific snack products, creating demand spikes for previously niche items. Brands are increasingly leveraging Saudi social media personalities to drive trial and brand awareness.

4. Sustainable and Eco-Friendly Packaging Demand

Growing environmental awareness among Saudi consumers, particularly the young urban demographic, is driving preference for snacks packaged in recyclable or reduced-plastic materials. Saudi Arabia's Vision 2030 environmental pillar supports circular economy principles, and SFDA is developing packaging sustainability guidelines. Brands offering compostable or recycled packaging materials are gaining positioning advantage in premium retail channels.

5. Local and Regional Flavor Innovation

A rising wave of Saudi national pride and cultural identity is driving demand for snacks incorporating local flavors and ingredients - including dates, Arabic spices, saffron, and za'atar. Local snack startups are capitalizing on this trend, creating premium packaged snacks that combine traditional Saudi tastes with modern formats. Saudi Vision 2030's cultural tourism programs are also amplifying interest in authentically Saudi food products.

Industry Value Chain Analysis

Saudi Arabia's snacks market value chain spans agricultural raw material production, industrial ingredient processing, snack manufacturing, multi-tier Saudi import and distribution networks, retail and digital sales channels, and end consumers across residential, foodservice, and institutional settings.

|

Stage |

Key Participants |

|

Raw Materials |

Agricultural producers of grains, corn, potatoes, oils, and sugar; dairy and nut commodity suppliers; flavoring and additive manufacturers |

|

Food Ingredient Processing |

Industrial ingredient processors supplying starches, seasonings, flavorings, and stabilizers to snack manufacturers |

|

Snack Manufacturing |

Global snack manufacturers with production facilities outside Saudi Arabia; regional manufacturers in GCC countries |

|

Import & Regional Distribution |

Licensed Saudi importers and SFDA-registered agents; regional distributors managing bonded warehouses and city-level distribution logistics |

|

Retail & Digital Channels |

Supermarket/hypermarket (Panda, Lulu, Carrefour); convenience stores; online grocery platforms; food delivery apps |

|

End Users |

Individual consumers; foodservice operators; institutional buyers including hospitality, entertainment, and education sector clients |

Saudi Arabia's snack distribution follows a two-tier model: global and regional manufacturers supply licensed Saudi importers/distributors, who in turn supply retail chains and sub-distributors. SFDA product registration and halal certification are mandatory import requirements. Online channels are increasingly enabling brand-direct consumer relationships, applying pressure on traditional distributor margin structures.

Technology Landscape in the Saudi Arabia Snacks Industry

Advanced Snack Production and Ingredient Technology

Modern snack manufacturing leverages extrusion technology, vacuum frying, and air-popping processes that reduce oil content by 30-70% versus traditional frying, enabling the production of healthier snack variants. Microencapsulation technology allows precise delivery of vitamins, minerals, and functional ingredients within snack matrices without compromising taste or texture.

Smart Packaging and Extended Shelf-Life Innovation

Modified atmosphere packaging (MAP) and oxygen-absorber technologies are extending snack shelf life by 25-40%, reducing waste during Saudi Arabia's long-distance distribution logistics. Active packaging with moisture control is particularly relevant for the Kingdom's humid coastal regions. QR code-enabled packaging is allowing consumers to access product origin, nutrition, and sustainability information digitally.

E-Commerce Technology and Personalization Platforms

AI-driven product recommendation engines on Saudi grocery platforms are enabling personalized snack discovery, increasing average basket size and brand trial rates. Subscription algorithm platforms curate individualized monthly snack boxes based on purchase history and dietary preferences. In August 2024, Heinz unveiled the "Hum Hum" robotic snack dipper at the Esports World Cup in Saudi Arabia - a device using a mechanical hand to dip snacks into sauces, controlled by foot pedals and designed for gamers, signaling growing technology integration in snack consumption experiences.

Halal Certification Technology and Traceability

Blockchain-based halal traceability systems are gaining adoption among premium snack importers seeking to verify end-to-end ingredient sourcing and production compliance. Digital SFDA certification platforms reduce import clearance times. These technologies address Saudi consumer demand for verified halal integrity throughout the supply chain.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

🔒 |

🔒 |

2025 |

|

Packaging |

Bag and Pouches |

49.3% |

2025 |

|

Distribution Channel |

Supermarket/Hypermarket |

56.8% |

2025 |

|

Region |

Northern & Central Region |

37.9% |

2025 |

By Distribution Channel

Supermarket/hypermarket lead with 56.8% market share in 2025, anchored by Panda Retail Company, Saudi Arabia's largest food retailer operating over 200 stores, alongside Lulu Hypermarket and Carrefour KSA. These channels provide extensive shelf space, chilled snack sections, and organized promotional programs that benefit major multinational snack brands. Convenience stores at 24.7% serve impulse purchase occasions, growing through Saudi Arabia's expanding petrol station retail, such as SASCO-affiliated outlets, and urban mini-market format expansion. Online channels at 10.5% are the fastest-growing segment, driven by Noon Food, Jahez, and HungerStation expanding grocery delivery services to cover more Saudi cities.

To access detailed market analysis, Request Sample

Others category at 8.0% includes vending machines, foodservice operators, institutional buyers, and specialty food stores. Vending machine deployments in Saudi Arabia's expanding entertainment and sporting venue network are creating a growing indirect distribution sub-channel for snack brands targeting captive audiences.

By Packaging

Bag and pouches dominate at 49.3% share (2025), reflecting consumer preference for lightweight, resealable packaging that maintains freshness in Saudi Arabia's high-temperature environment. Stand-up pouches with zip-lock closures are particularly popular for nuts, dried fruits, and premium snack mixes. Boxes at 22.1% serve structured confectionery and gift snack segments. Cans at 12.4% are used predominantly for premium nuts and puffed snack products offering superior product protection and premium shelf presentation. Jars at 9.2% serve spread-based and specialty snack categories.

.webp)

Others at 7.0% encompass flexible films, wrappers, and multi-pack formats. Sustainable packaging variants, including paper-based pouches and reduced-plastic formats, are gaining traction in premium retail channels as SFDA develops environmental packaging guidelines under Vision 2030's sustainability objectives.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Northern & Central Region |

37.9% |

Highest vehicle density and population concentration centered around Riyadh; broad modern retail presence; Vision 2030 mega-events and entertainment driving snack occasion growth |

|

Western Region |

29.1% |

High tourist and religious traveler traffic in Makkah and Madinah driving foodservice and convenience snack demand; Jeddah's port logistics enable faster snack import distribution |

|

Eastern Region |

22.0% |

Concentration of oil, gas, and petrochemical workforce driving institutional and convenience snack demand; Al-Khobar and Dammam's expanding retail landscape supporting market growth |

|

Southern Region |

11.0% |

Emerging infrastructure development; growing domestic tourism to Asir region; government programs developing regional connectivity and hospitality supporting gradual snack market growth |

The Northern and Central Region's 37.9% dominance reflects Riyadh's position as Saudi Arabia's economic capital and the Kingdom's most populous metropolitan area. The region hosts the highest density of modern trade retail formats, premium hypermarkets, and entertainment venues - all high-frequency snack purchase environments. Riyadh's expanding subway network and entertainment venues under Vision 2030's Quality of Life Program are creating new snack consumption touchpoints.

.webp)

The Western Region at 29.1% benefits from Jeddah's status as Saudi Arabia's commercial gateway and largest port. Makkah and Madinah's year-round religious tourism, hosting tens of millions of pilgrims and Umrah visitors annually, generates substantial demand for portable, halal-certified snack products in a diverse, international consumer environment.

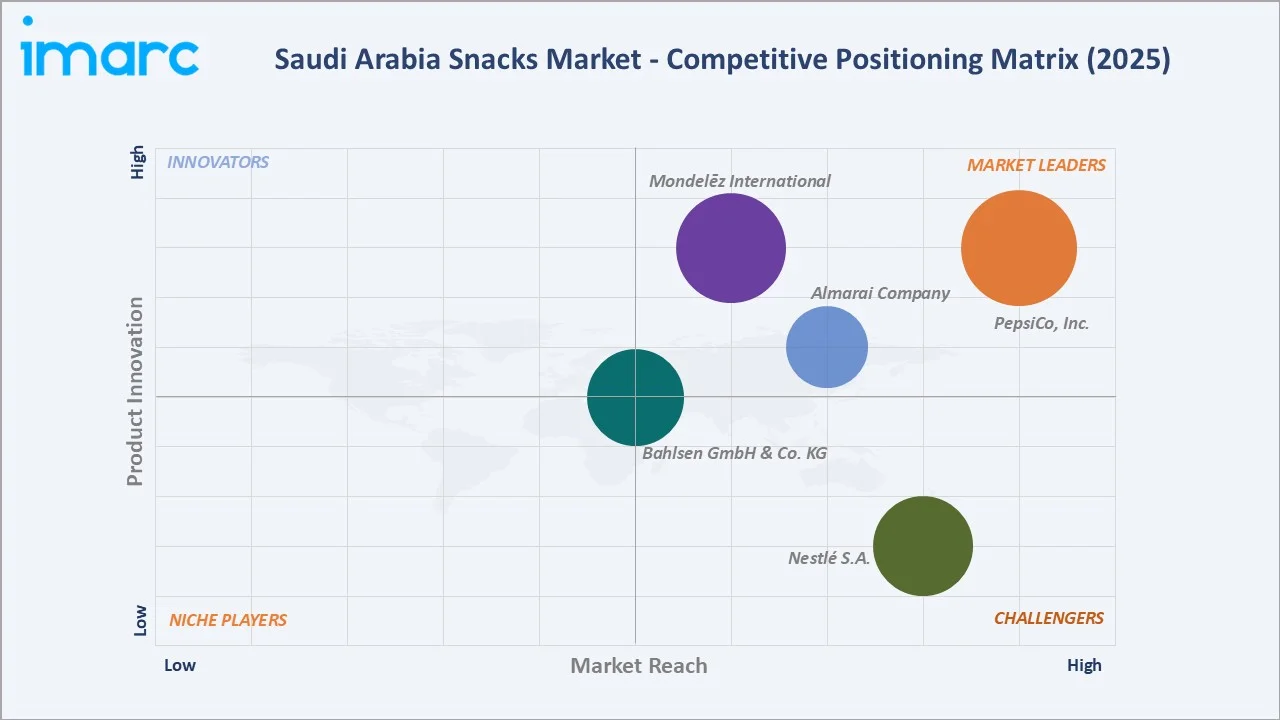

Competitive Landscape

Saudi Arabia's snacks market is moderately concentrated among multinational food majors at the premium and mass-market tiers, with intensifying competition from regional GCC brands and growing local Saudi snack startups.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

PepsiCo, Inc. |

Lay's, Cheetos, Doritos, Tasali, Quaker |

Market Leader |

Largest global snack portfolio; strong Saudi retail presence across all trade channels |

|

Mondelēz International |

Oreo, Cadbury, Milka, Barni, Ritz, BelVita |

Market Leader |

Leading confectionery and biscuit brand in MENA; halal-certified production serving GCC markets |

|

Nestlé S.A. |

KitKat, Aero, Smarties |

Strong Challenger |

Broad product range across confectionery, dairy snacks, and savory; established Saudi distribution |

|

Almarai Company |

L'usine, Almira, 7DAYS |

Market Leader |

Saudi Arabia's largest food and beverage company; strong local dairy snack and bakery positioning |

|

Bahlsen GmbH & Co. KG |

Bahlsen, Leibniz, PiCK UP!, Hit, Waffeletten |

Established Player |

European biscuit specialist with growing MENA presence through premium retail channels in KSA |

Key Company Profiles

PepsiCo, Inc.

PepsiCo, Inc., which is largely operational through Saudi Snack Foods Company Ltd. (SSFL), is Saudi Arabia's leading snack brand by volume, with Lay's commanding dominant shelf presence across supermarkets, convenience stores, and online channels. SSFL is mostly involved in the production and distribution of the company’s snack brands.

- Product Portfolio: Lay's, Cheetos, Doritos, Quaker, Tasali, and others.

- Strategic Focus: Premiumization through limited-edition flavor launches, health-focused product line expansion, and digital marketing campaigns targeting Saudi youth demographics.

Mondelēz International

Mondelēz International maintains leading positions across biscuit, confectionery, and chocolate snack categories in Saudi Arabia, with products sold through all major retail channels and extensive convenience store distribution.

- Product Portfolio: Oreo, Barni, Ritz, BelVita, Cadbury, Milka, and others.

- Strategic Focus: Occasion-led marketing, seasonal product innovation, and expansion of health-positioned snack variants in Saudi retail.

Almarai Company

Almarai is Saudi Arabia's largest integrated food and beverage company, with annual revenues exceeding SAR 20 Billion. Almarai's bakery division produces a range of packaged bakery snacks distributed through its own extensive direct-delivery network covering all Saudi regions.

- Product Portfolio: L'usine, Almira, 7DAYS (co-produced with MFI), and others.

- Strategic Focus: Leveraging direct distribution network; expanding bakery snack portfolio addressing health and convenience trends among Saudi families.

Market Concentration Analysis

Saudi Arabia's snacks market exhibits moderate-to-high concentration at the mass-market branded level, with the top five multinational players holding an estimated 40-50% of organized retail value (2025). Market fragmentation increases significantly in the budget, specialty, and artisan snack segments, where dozens of regional GCC brands, emerging Saudi startups, and imported Asian budget brands compete for shelf space.

The organized snack market's concentration ratio reflects the scale advantages of multinationals in Saudi SFDA registration, halal certification, and trade marketing investment. Local Saudi snack brands have grown their collective market share from approximately 8% in 2020 to an estimated 12-15% in 2025, driven by Vision 2030-backed Saudi content programs encouraging domestic food manufacturing.

Consolidation trends include Saudi food conglomerates, such as Almarai and Savola Group, actively expanding their snack product portfolios through internal development and selective acquisitions of local snack brands with established regional distribution networks.

Investment & Growth Opportunities

Fastest Growing Segments

Online distribution (~10.2% CAGR), premium and artisan snack categories (~10-12% CAGR), and locally-inspired flavor innovation represent Saudi Arabia's highest-growth snack investment vectors through 2034.

Emerging Market Opportunities

- Health Snack Manufacturing Localization: Saudi Arabia's Vision 2030 industrial strategy supports domestic food production investment. Establishing halal-certified, SFDA-compliant snack manufacturing facilities in industrial zones such as Riyadh's or Jeddah's industrial areas provides access to Vision 2030 investment incentives and government procurement programs.

- D2C Digital Snack Platforms: Saudi Arabia's 95%+ smartphone penetration and young population support subscription snack box business models. Monthly curated snack discovery services leveraging personalization algorithms represent a high-margin, low-capital-intensity entry point for snack brand development.

- Premium Nut and Date-Based Snack Export Hub: Saudi Arabia's world-class date production, over 1.9 million tons annually per the Saudi Ministry of Environment, Water, and Agriculture, creates a raw material advantage for developing premium date-based confectionery and snack products targeting export markets.

Investment Themes

- Functional snack portfolio development targeting Saudi Arabia's health-conscious demographic, aligned with Ministry of Health's Vision 2030 wellness programs.

- Sustainable packaging investment - brands adopting eco-friendly packaging solutions gain positioning advantage in premium retail channels as SFDA develops environmental guidelines.

- Sports and entertainment venue snack concession expansion - Vision 2030 sports infrastructure investment, including Formula 1 hosting, football stadiums, and entertainment parks, creates captive high-frequency snack purchase environments.

Future Market Outlook (2026-2034)

The Saudi Arabia snacks market is projected to grow from USD 1.71 Billion in 2025 to USD 3.47 Billion by 2034, at an 8.17% CAGR. By 2030, the market is expected to reach USD 2.54 Billion, reflecting compounding growth from Vision 2030's economic transformation, rising snack consumption occasions, and increasing penetration of premium and health-focused products.

Three structural forces anchor Saudi Arabia's snacks market growth through 2034: demographic demand driven by a young, digitally-connected population with strong appetite for snack variety and global trends; Vision 2030's entertainment and tourism expansion multiplying high-frequency snack consumption occasions; and the e-commerce revolution enabling new brand discovery and purchase channels that democratize premium snack access across all Saudi regions.

Technological disruption will reshape the competitive landscape through 2034. AI-powered personalization platforms, D2C subscription models, and functional ingredient innovation will enable nimble snack brands to compete effectively with established multinationals. Regulatory evolution under SFDA mandatory nutrition labeling updates, will accelerate health snack reformulation and create structural headwinds for traditional high-sugar and high-fat confectionery segments.

Research Methodology

Primary Research

Primary research comprised structured interviews with 60+ Saudi Arabia snack industry stakeholders (2025), including regional snack importers and distributors, retail category managers from major Saudi hypermarkets, foodservice operators, SFDA regulatory specialists, and consumer research panels across Riyadh, Jeddah, and Dammam demographics.

Secondary Research

Secondary research encompassed Saudi Food and Drug Authority (SFDA) product registration data, Saudi General Authority for Statistics (GASTAT) household expenditure surveys, Saudi Ministry of Environment, Water, and Agriculture agricultural production data, Saudi Ministry of Commerce trade statistics, and company annual reports for major snack brands operating in Saudi Arabia. Saudi Vision 2030 program documentation and CST e-commerce market data were key secondary inputs. Over 100 secondary sources were reviewed.

Forecasting Models

Market size forecasts were developed using bottom-up consumption per capita x population growth models segmented by snack category, distribution channel, and region. Validated against SFDA import registration data and GASTAT consumer expenditure surveys. Key inputs include Saudi population growth projections, Vision 2030 tourism and entertainment visitor forecasts, e-commerce penetration rate curves, and health-trend-adjusted category demand models.

Saudi Arabia Snacks Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Frozen & Refrigerated, Fruit, Bakery, Savory, Confectionery, Dairy, Others |

| Packagings Covered | Bag and Pouches, Boxes, Cans, Jars, Others |

| Distribution Channels Covered | Supermarket/Hypermarket, Convenience Stores, Online, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Companies Covered | PepsiCo, Inc., Mondelēz International, Nestlé S.A., Almarai Company, Bahlsen GmbH & Co. KG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Saudi Arabia snacks market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Saudi Arabia snacks market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Saudi Arabia snacks industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Saudi Arabia Snacks Market Report

The Saudi Arabia snacks market reached USD 1.71 Billion in 2025. This growth is driven by rising disposable incomes, urbanization, and strong demand for convenience and premium snack products.

The market is forecast to grow at a CAGR of 8.17% during 2026-2034, reaching USD 3.47 Billion by 2034. Growth is supported by Vision 2030, e-commerce expansion, and premiumization trends.

Supermarket/hypermarket lead with 56.8% share (2025), anchored by Panda, Lulu, and Carrefour KSA's extensive retail footprints in major Saudi cities.

Bag and pouches hold the largest share at 49.3% (2025), preferred for their lightweight, resealable design suited to Saudi Arabia's on-the-go consumption patterns.

The Northern and Central Region leads with 37.9% share (2025), driven by Riyadh's high population density, extensive modern retail infrastructure, and strong consumer purchasing power.

The Saudi Arabia snacks market was valued at USD 1.16 Billion in 2020. The market has expanded consistently from 2020 to 2025 at a CAGR of approximately 8%, reaching USD 1.71 Billion in 2025.

Online distribution is growing fastest at approximately 10.2% CAGR (2026-2034). Health and functional snack categories are also growing at above-average rates, driven by rising health awareness.

Key players include PepsiCo, Inc., Mondelēz International, Nestlé S.A., Almarai Company, and Bahlsen GmbH & Co. KG. These companies collectively hold approximately 40-50% of the organized snack market.

Key drivers include a young, urbanized population, rising disposable incomes, e-commerce expansion, Vision 2030 entertainment and tourism mega-projects, and growing demand for health-conscious snack options.

The Saudi Arabia snacks market is forecast to reach USD 2.54 Billion in 2030. This milestone reflects consistent growth driven by demographic expansion, premium snack adoption, and digital retail channel penetration.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)