Seed Coating Market Size, Share, Trends and Forecast by Additive Type, Process, Crop Type, and Region, 2026-2034

Global Seed Coating Market Size, Share, Trends & Forecast (2026-2034)

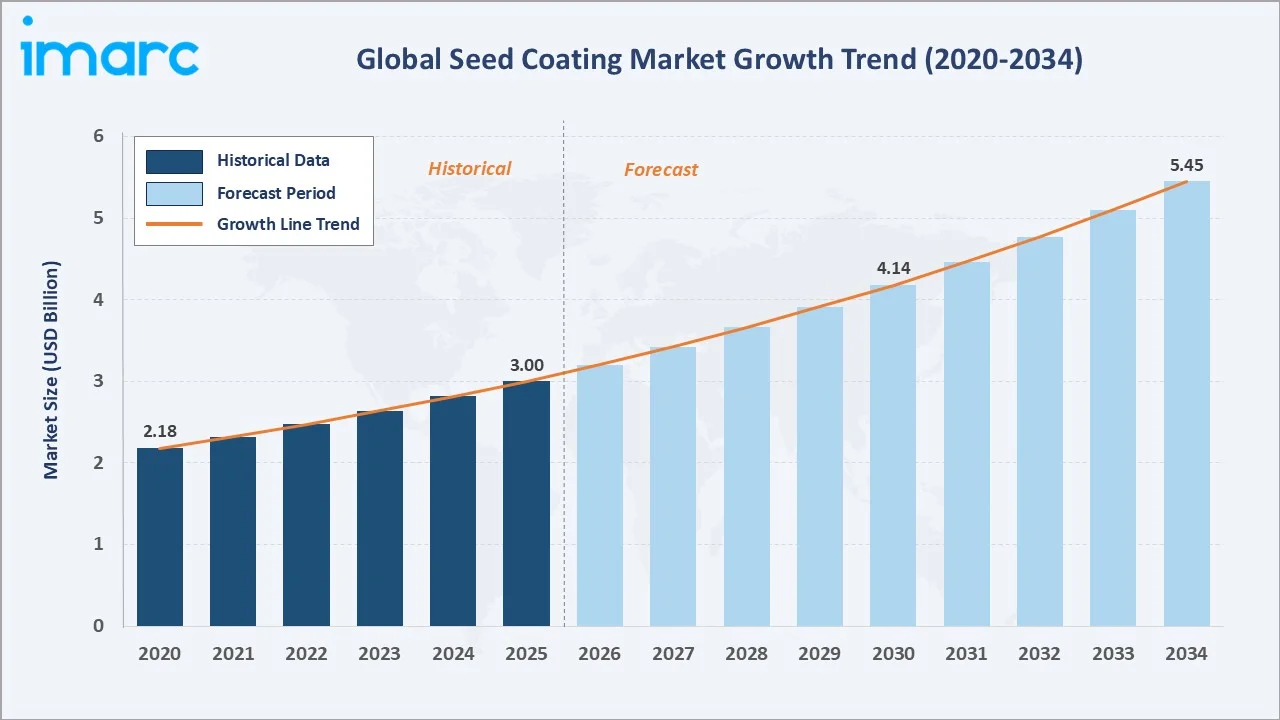

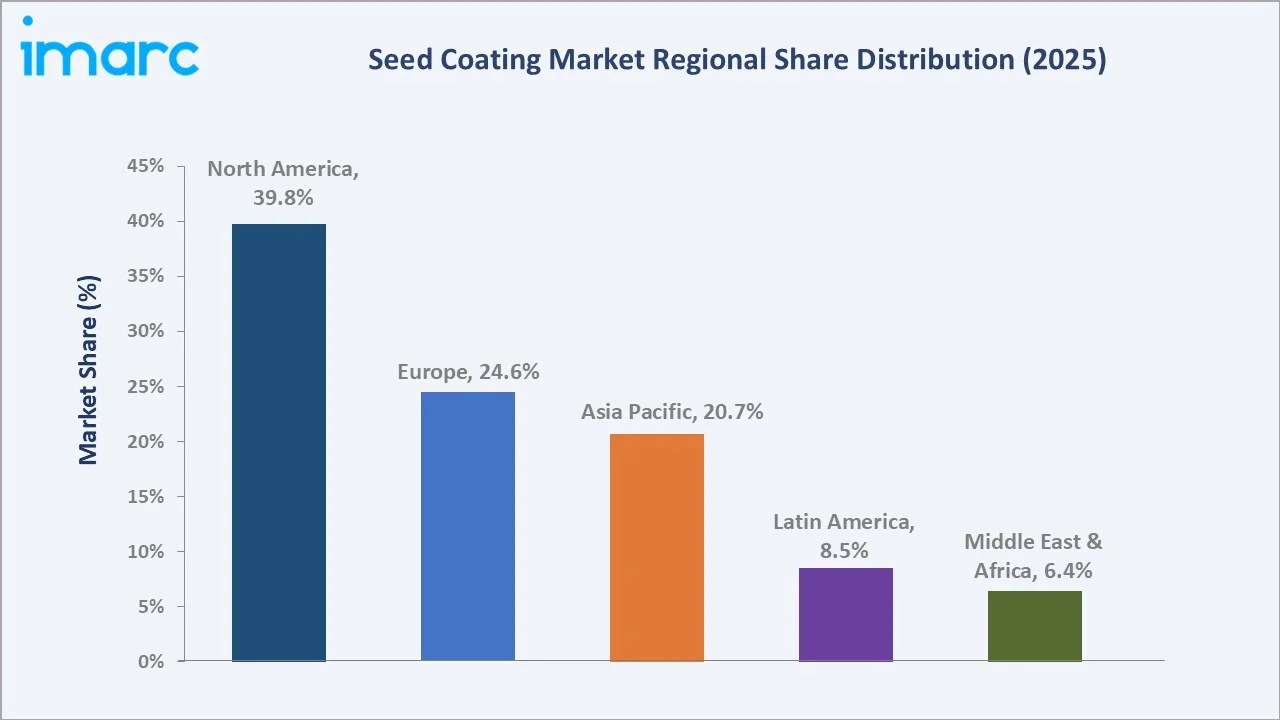

The global seed coating market size was valued at USD 3.0 Billion in 2025 and is projected to reach USD 5.45 Billion by 2034, registering a CAGR of 6.63% during 2026-2034. North America dominates with a 39.8% share in 2025, driven by advanced farming technologies and strong R&D investment.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.0 Billion |

|

Forecast Market Size (2034) |

USD 5.45 Billion |

|

CAGR (2026-2034) |

6.63% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (39.8%, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Process |

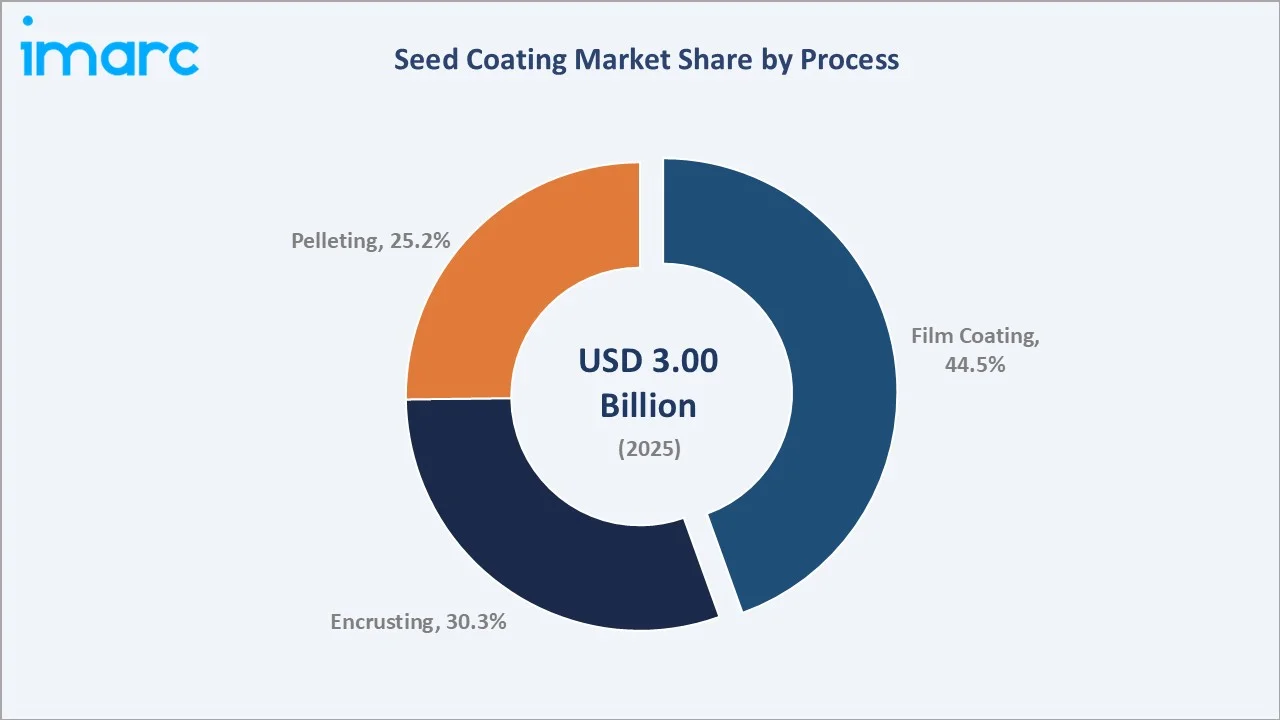

Film Coating (44.5%, 2025) |

|

Leading Additive Type |

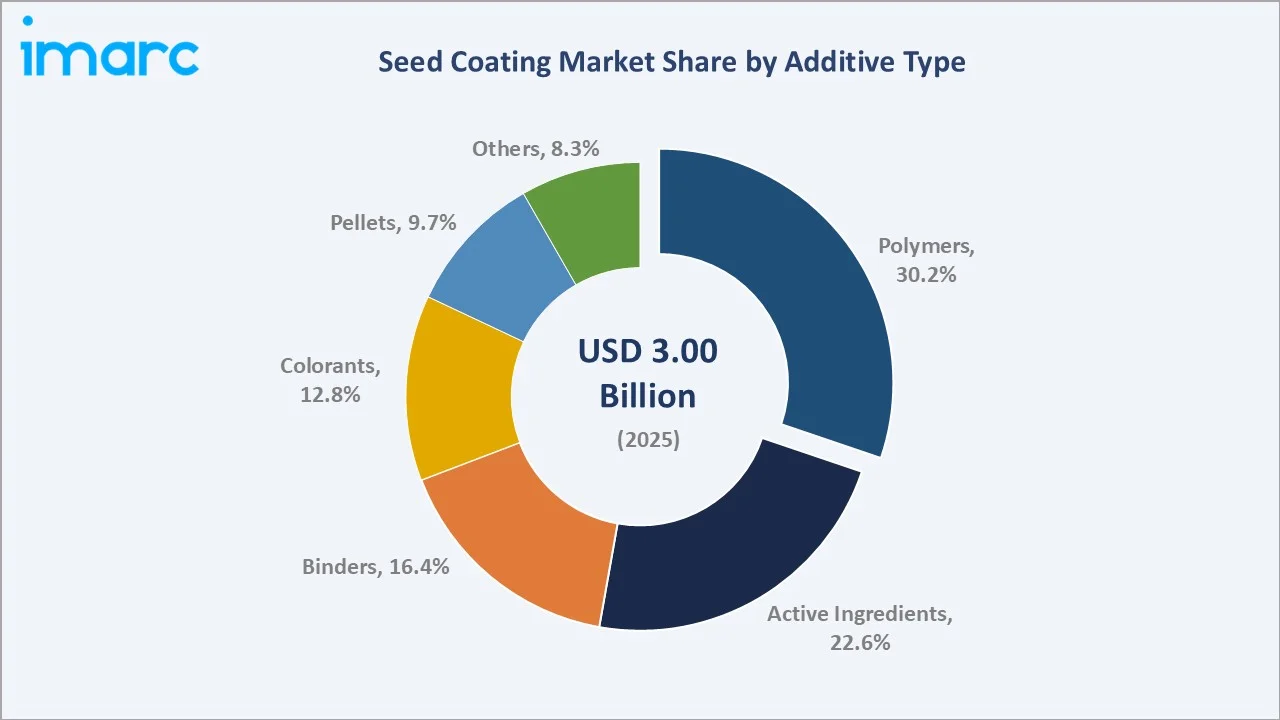

Polymers (30.2%, 2025) |

The market expanded steadily from USD 2.18 Billion in 2020 to USD 3.0 Billion in 2025. Growth momentum is expected to strengthen further through the forecast period, underpinned by biodegradable polymer innovation, increasing precision agriculture deployment, and proactive government food security investments across North America, Europe, and Asia Pacific.

To get more information on this market, Request Sample

Asia Pacific leads regional growth. Film coating and active ingredients deliver above-average returns, validating investment prioritization in these segments.

Executive Summary

The global seed coating market, valued at USD 3.0 Billion in 2025, is forecast to reach USD 5.45 Billion by 2034 at a CAGR of 6.63%. Key drivers include escalating food security demands driven by shrinking arable land is accelerating demand for uniformly sized coated seeds compatible with GPS-guided planters.

Film Coating leads process segmentation at 44.5% share in 2025, prized for its thin, uniform protective layers that preserve seed dimensions and enable active ingredient integration. Polymers dominate additive types at 30.2%, owing to their versatility, controlled-release capabilities, and compatibility with diverse crop and climate conditions. The encrusting process accounts for 30.3% while pelleting (25.2%) is the fastest-growing process, driven by vegetable and specialty crop requirements for standardized seed shapes.

North America holds 39.8% of global market share in 2025, with the United States leading through precision agriculture investment and new product launches. Europe (24.6%) is driven by EU Farm-to-Fork mandates promoting bio-based coatings. Asia Pacific (20.7%), the fastest-growing region, is propelled by India's IIOR biopolymer technology delivering 25-30% yield improvements in 2024, and China's extensive cereal and grain production base. Latin America (8.5%) and Middle East & Africa (6.4%) represent nascent but growing markets aligned with food security programs.

Key Market Insights

|

Insight |

Data |

|

Market Size (2025) |

USD 3.0 Billion |

|

Market Forecast (2034) |

USD 5.45 Billion |

|

CAGR (2026-2034) |

6.63% |

|

Largest Process |

Film Coating - 44.5% share (2025) |

|

Largest Additive Type |

Polymers - 30.2% share (2025) |

|

Leading Region |

North America - 39.8% revenue share (2025) |

|

Top Companies |

Bayer AG, Syngenta, BASF, Croda International Plc, Clariant, Sensient Technologies Corporation, UPL |

|

Market Opportunity |

Biodegradable polymer coatings |

Key Analytical Observations:

- Film Coating's 44.5% dominance (2025) reflects its precision in mechanical sowing compatibility, low dust-off profile, and ability to carry fungicide, insecticide, and micronutrient payloads in a single uniform application layer.

- Polymers' 30.2% additive type leadership stems from their versatility in encapsulating active ingredients such as fungicides, insecticides, and micronutrients, enabling targeted controlled-release seed protection across diverse crop types and climates.

- North America's 39.8% regional share is underpinned by the United States' advanced precision agriculture infrastructure; Lallemand Plant Care's 2024 LALRISE SHINE DS dry seed treatment launch exemplifies the active commercial innovation pipeline.

- Asia Pacific is the fastest-growing region, supported by India's IIOR biopolymer technology , and China's large-scale cereal production requiring advanced seed protection at scale.

- Encrusting (30.3%) and Pelleting (25.2%) processes are gaining momentum for crops with irregular seed morphology including vegetables, flowers, and oilseeds, enabling uniform mechanical planting in automated greenhouse and field environments.

Global Seed Coating Market Overview

Seed coating refers to the application of functional materials - polymers, colorants, binders, active ingredients, and other additives - to seeds, modifying surface properties to enhance germination, protection, and planting efficiency.

The global market encompasses film coating, encrusting, and pelleting processes, each serving distinct crop types and agricultural conditions. Major crop applications include cereals and grains, fruits and vegetables, oilseeds and pulses, and ornamentals.

The industry intersects agrochemicals, specialty chemicals, advanced materials, and precision agriculture technologies. Growth is influenced by macroeconomic factors including shrinking global arable land, expanding global food demand, escalating government food security investments, and accelerating adoption of sustainable farming practices across all major agricultural economies.

The ecosystem is anchored by specialty chemical and polymer suppliers at the upstream end, followed by seed coating manufacturers - including integrated agrochemical majors such as Bayer AG, Syngenta, and BASF - who apply coatings via film, encrusting, or pelleting processes. Distribution occurs through agri-dealer networks and direct-to-farm platforms, with end-user demand concentrated among commercial and smallholder farmers globally.

Market Dynamics

To evaluate market opportunities, Request Sample

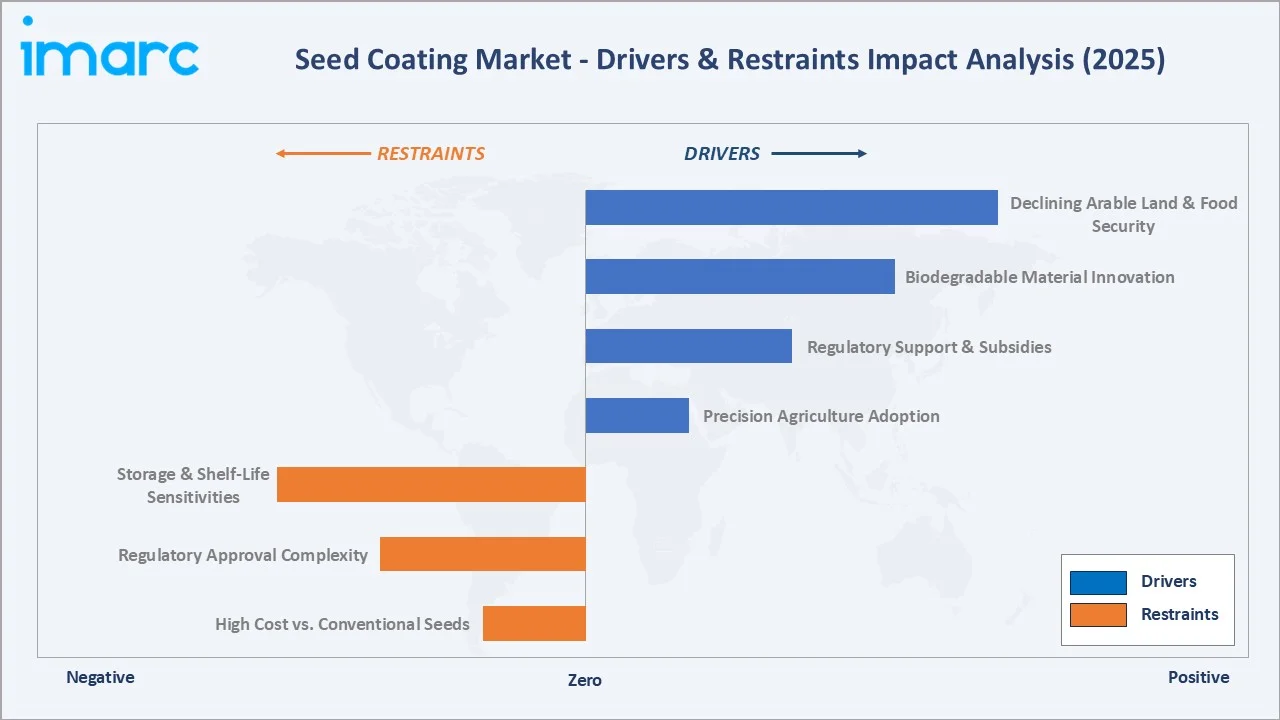

Market Drivers

- Declining Arable Land and Rising Food Demand: Ongoing loss of productive farmland is intensifying pressure on agricultural systems. This scarcity is driving demand for yield-enhancing seed technologies, with coated seeds offering significantly improved germination performance in stressed field environments, supporting higher crop establishment rates and more resilient agricultural output under challenging growing conditions.

- Innovations in Biodegradable Coating Materials: India's IIOR unveiled patented biopolymer coating technology in 2024. These biodegradable alternatives align with ESG mandates and reduce reliance on synthetic chemicals, broadening market addressability.

- Regulatory Support and Subsidies: Governments across North America, Europe, and Asia Pacific are funding seed treatment research and offering agricultural subsidies that incentivize adoption of advanced coated seed technologies, particularly for food staple cereals, oilseeds, and vegetables.

- Precision Agriculture Adoption: The global precision agriculture market is witnessing strong growth momentum. Pelleted and film-coated seeds with standardized dimensions are critical for GPS-guided vacuum planters, reducing seed wastage and improving field uniformity, thereby enhancing operational efficiency and planting accuracy in large-scale commercial farming systems.

Market Restraints

- High Cost vs. Conventional Seeds: Premium coating technologies increase per-unit seed costs significantly, creating affordability barriers in low-income farming regions of Sub-Saharan Africa and South Asia, where subsistence farming is prevalent and access to premium agri-inputs is limited.

- Regulatory Approval Complexity: Integration of pesticides and fungicides into seed coatings requires complex multi-regional regulatory clearances from EPA, EFSA, and national agencies, extending commercialization timelines and increasing compliance costs for new market entrants.

- Storage and Shelf-Life Sensitivities: Coated seeds incorporating biological active ingredients such as microbial inoculants face shortened shelf-life and require specialized cold-chain storage, adding logistical costs and limiting accessibility in rural distribution networks across emerging markets.

Market Opportunities

- Biologicals and Microbial Seed Coatings: Rising demand for organic and sustainable agriculture is creating a high-growth niche for bio-stimulant and microbial seed coatings. The biologicals segment within seed coatings is projected to grow at substantial growth rate, outpacing the broader market. Lallemand Plant Care's 2024 LALRISE SHINE DS launch demonstrates commercial viability.

- Asia Pacific and Latin America Expansion: Asia Pacific (20.7% share, fastest growing) and Latin America (8.5%) represent under-penetrated markets. Increasing government food security investments and growing precision agriculture adoption position these regions as primary long-term growth engines through 2034.

- Next-Generation Nano-Coating Integration: Nano-enabled platforms with IoT-connected soil sensors are enabling adaptive coating formulations triggered by real-time field conditions, representing a premium market segment.

Market Challenges

- Climate-Induced Coating Efficacy Variability: Unpredictable rainfall patterns and temperature extremes challenge the efficacy of certain coating formulations across different agro-climatic zones, requiring continuous R&D investment in climate-adaptive coating technologies.

- Supply Chain Fragmentation for Specialty Polymers: Dependence on specialty biodegradable polymers from limited global suppliers creates vulnerability to raw material price volatility and supply disruptions, particularly affecting SME coating manufacturers in emerging markets.

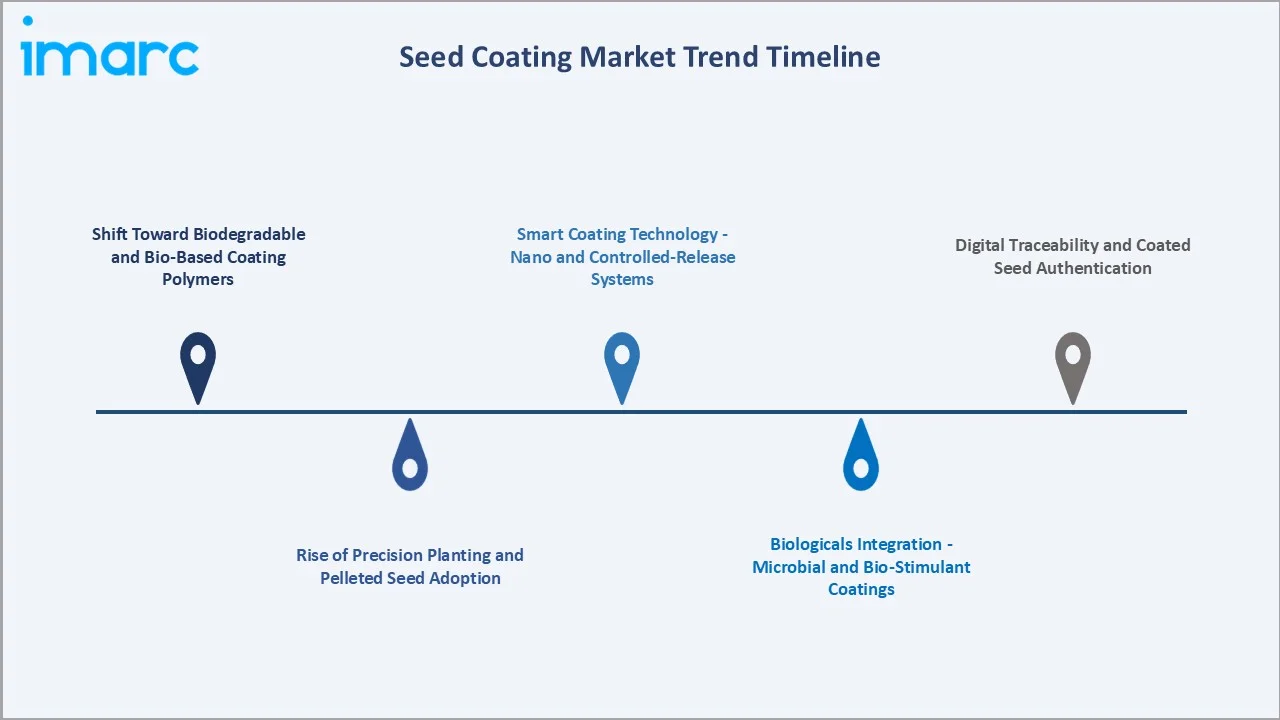

Emerging Market Trends

1. Shift Toward Biodegradable and Bio-Based Coating Polymers

Environmental regulations and ESG-aligned corporate strategies are accelerating the transition from synthetic to biodegradable seed coating materials. Indian Institute of Oilseeds Research (IIOR) patented biopolymer technology is demonstrating strong commercial yield improvements.

2. Rise of Precision Planting and Pelleted Seed Adoption

Pelleting (25.2% share, 2025) is growing in sync with precision agriculture. Pelleted seeds deliver standardized spherical shapes essential for GPS-guided vacuum planters. This trend is most pronounced in vegetable and flower seed production targeting commercial greenhouse and controlled-environment agriculture operators globally.

3. Biologicals Integration - Microbial and Bio-Stimulant Coatings

Microbial seed coatings incorporating rhizobacteria, mycorrhizal fungi, and biostimulants are gaining commercial traction. Lallemand Plant Care's LALRISE SHINE DS (USA, 2024) demonstrated enhanced phosphorus uptake and root vigor in corn and dry beans.

4. Smart Coating Technology - Nano and Controlled-Release Systems

Next-generation nano-coating platforms enable precise controlled release of embedded nutrients, fungicides, and plant growth regulators in response to soil moisture and temperature triggers. This technology reduces chemical runoff versus conventional soil applications, addressing environmental impact concerns while improving agronomic outcomes and farmer economics simultaneously.

5. Digital Traceability and Coated Seed Authentication

Leading seed companies are embedding QR-coded colorants and digital markers within seed coatings to enable supply chain traceability, anti-counterfeiting compliance, and regulatory reporting. This trend is particularly relevant in Brazil and India, where seed authentication is increasingly mandated under national agricultural reform legislation enacted between 2022 and 2025.

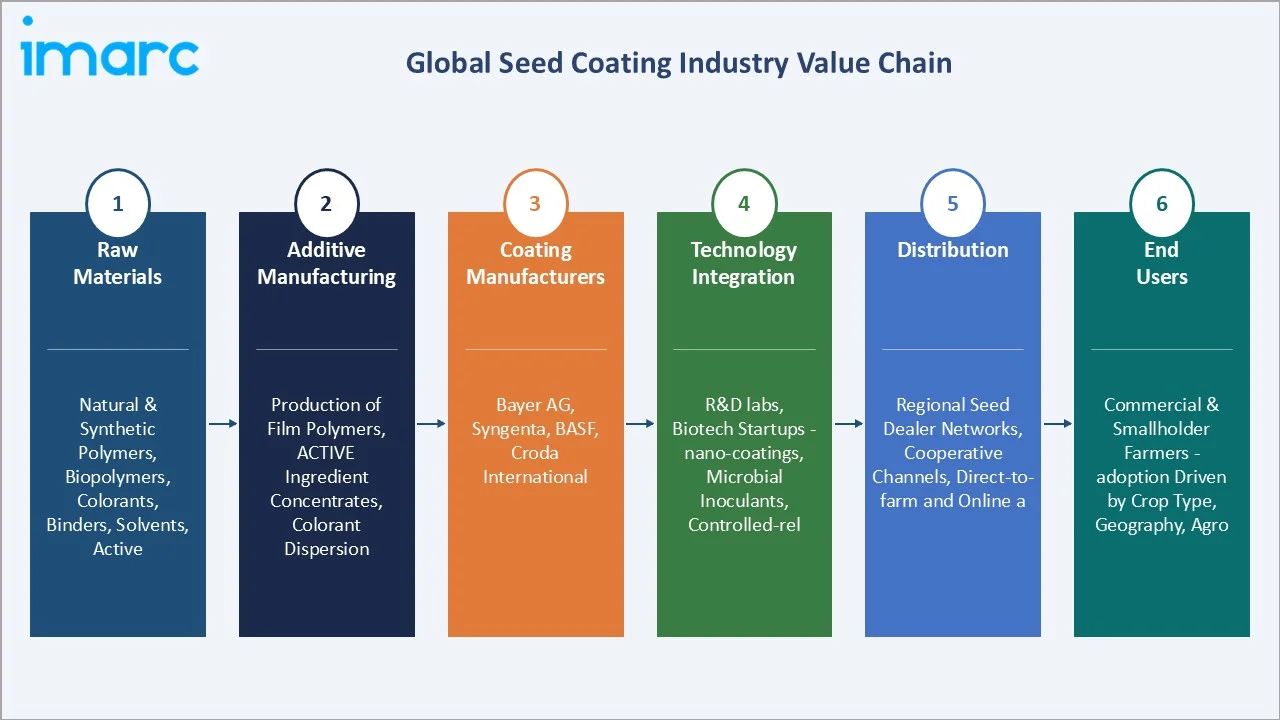

Industry Value Chain Analysis

The global seed coating industry value chain spans six integrated stages, from raw material supply through end-user crop cultivation. Each stage presents distinct margin profiles and competitive dynamics critical to the overall seed coating market analysis.

|

Stage |

Key Participants |

Description |

|

Raw Materials |

Chemical suppliers, Polymer producers |

Natural & synthetic polymers, biopolymers, colorants, binders, solvents, active ingredient precursors |

|

Additives Manufacturing |

Specialty chemical |

Production of film polymers, active ingredient concentrates, colorant dispersions, binders |

|

Coating Manufacturers / OEMs |

Bayer AG, Syngenta, BASF, Croda International Plc |

Full seed coating application via film, encrusting, or pelleting processes with QA validation |

|

Technology Integration |

R&D labs, biotech start-ups |

Nano-coatings, microbial inoculants, controlled-release systems, biopolymer development |

|

Distribution |

Seed distributors, agri-retailers |

Regional seed dealer networks, cooperative channels, direct-to-farm and online agri-platforms |

|

End Users |

Commercial & smallholder farmers |

Adoption driven by crop type, geography, agronomic objectives, and product access |

Coating manufacturers and OEMs hold the highest strategic value by integrating specialty chemicals, active ingredients, and polymer technologies into value-added seed solutions. Distribution channels are evolving with the rise of direct-to-farm digital seed purchasing platforms in North America and Western Europe, allowing manufacturers to capture higher margins while improving traceability.

Technology Landscape in the Seed Coating Industry

Polymer and Film Technology

Film coating polymers remain the dominant technology at 44.5% process share in 2025. Water-soluble and biodegradable polymer matrices - including hydroxypropyl methylcellulose (HPMC), polyvinyl alcohol (PVA), and cellulose acetate phthalate (CAP) - are replacing conventional synthetic options. These materials enable precise active ingredient loading and controlled-release profiles while meeting environmental compliance mandates across the EU and North America.

Biopolymer Innovation and Sustainable Coatings

The 2024 IIOR biopolymer patent in India represents a landmark in sustainable seed coating, demonstrating commercial viability of bio-based materials for crop yield enhancement. Chitosan, starch-based coatings, and alginate-derived polymers are under accelerated R&D, targeting both environmental performance and antifungal efficacy across wheat, rice, and soybean seed applications.

Controlled-Release Active Ingredient Systems

Advanced microencapsulation using melamine-formaldehyde and polyurea shells reduces early leaching of active compounds, improving agronomic performance and environmental safety. Temperature- and moisture-triggered release systems are critical for high-value specialty crop markets in Europe and North America, where regulatory scrutiny of pesticide runoff is intensifying.

Nano-Coating and Smart Agriculture Integration

Nano-silica and nano-clay composites improve moisture retention, pathogen resistance, and nutrient delivery at sub-micron precision. Integration with IoT-connected soil sensors enables adaptive coating formulations triggered by real-time field conditions, aligning with precision agriculture investments. This frontier technology is projected to reach commercial scale adoption by 2028.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Additive Type | Polymers | 30.2% |

2025 |

| Process | Film Coating |

🔒 |

2025 |

| Crop Type | Cereals and Grains |

26.8% |

2025 |

|

Region |

North America |

39.8% |

2025 |

By Process

To access detailed market analysis, Request Sample

Film Coating leads with 44.5% market share in 2025, preferred for its thin, uniform protective layer that preserves seed dimensions - essential for mechanical planting equipment calibration. Encrusting (30.3%) is gaining momentum for oilseed and vegetable crops with irregular morphology. Pelleting (25.2%) is growing fastest, driven by precision agriculture requirements for standardized seed shapes compatible with high-speed vacuum planters across commercial greenhouse and field operations.

By Additive Type

Polymers command 30.2% of additive type share in 2025, driven by their chemical compatibility with diverse active ingredients and ability to form durable, uniform seed films. Active Ingredients (22.6%) represent a high-value category, integrating crop protection chemistries directly into the seed coating layer. Binders (16.4%) ensure structural cohesion of the coating matrix. Colorants (12.8%) serve regulatory traceability and brand authentication purposes, increasingly incorporating digital markers. Pellets (9.7%) and Others (8.3%) represent emerging high-growth niches.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

North America |

39.8% |

Precision agriculture, high-yield crop demand, R&D investment |

EPA regulations, USDA seed quality programs |

|

Europe |

24.6% |

Sustainable farming mandates, biodegradable coating demand |

EU Green Deal, Farm-to-Fork Strategy |

|

Asia Pacific |

20.7% |

Population growth, food security programs, biopolymer R&D |

India IIOR regulation, China seed quality standards |

|

Latin America |

8.5% |

Soy, corn, sugarcane seed treatment expansion in Brazil |

Brazil MAPA certification, Argentina rules |

|

Middle East & Africa |

6.4% |

Food security initiatives, semi-arid crop protection needs |

FAO-backed programs, national seed policies |

North America

North America dominates with 39.8% share in 2025. The United States drives demand through large-scale commercial farming and significant R&D in seed treatment technologies. Lallemand Plant Care's 2024 LALRISE SHINE DS dry seed treatment - combining microbes with a seed finisher for corn and dry beans - exemplifies the active innovation pipeline. EPA-aligned sustainable chemistry mandates and USDA research grants are structural growth drivers through 2034.

Competitive Landscape

|

Company Name |

Key Brand / Division |

Market Position |

Specialization |

|

Bayer AG |

Bayer CropScience Seed Treatment |

Market Leader |

Fungicide & insecticide coatings |

|

Syngenta |

Syngenta Seedcare |

Market Leader |

Integrated seed treatment systems |

|

BASF |

BASF Agricultural Solutions |

Strong Challenger |

Polymer & active ingredient coatings |

|

Croda International Plc |

Croda Agriculture |

Challenger |

Bio-based coating polymers |

|

Clariant |

Clariant Crop Solutions |

Challenger |

Colorants and polymer binders |

|

Sensient Technologies Corporation |

Sensient Industrial Colors |

Niche Leader |

Colorant and tracer systems |

|

UPL |

Arysta LifeScience (UPL) |

Emerging |

Emerging market seed treatments |

The global seed coating market is moderately consolidated, with Bayer AG, Syngenta, BASF, Croda International Plc, Clariant collectively commanding significant market influence through integrated crop science platforms.

Key Company Profiles

Bayer AG

Bayer AG is German multinational life sciences company with a leading position in crop science through its CropScience division. Its seed treatment portfolio covers fungicides, insecticides, and biologicals for corn, soybeans, wheat, and canola globally, with operations in over 80 countries.

- Product Portfolio: Film coating fungicide/insecticide seed treatments for major cereals and grains. Brands include Gaucho and Poncho seed treatment product lines, which are among the most widely recognized in the global commercial seeds market, serving commercial seed producers across every major growing region worldwide.

- Recent Developments: In 2025, Bayer AG is advancing next-generation seed technologies by focusing on innovative seed-applied solutions and new seed varieties. The company is strengthening its SeedGrowth portfolio with advanced fungicidal treatments and coating technologies designed to enhance early-stage crop protection, improve germination, and support higher yield potential.

- Strategic Focus: Integration of biologicals with chemical actives in seed coatings, sustainability compliance, and precision agronomy partnerships with global commercial seed companies.

BASF

BASF is the world’s largest chemical producer, headquartered in Ludwigshafen, Germany. The company operates as a diversified chemicals and materials leader, serving industries such as agriculture, automotive, construction, consumer goods, and energy.

- Product Portfolio: Xemium (fluxapyroxad), Systiva, and F500 fungicide-based seed treatments combined with BASF polymer coating adjuvants for cereal and soybean markets.

- Recent Developments: In 2023, BASF introduced its Flo Rite Pro 02 plantability polymer, an advanced seed coating solution designed to enhance seed flow, optimize singulation, and improve spacing during planting. The technology supports better plant population and yield potential, while maintaining compatibility with multiple seed treatment inputs and reducing dust levels for improved application efficiency.

- Strategic Focus: R&D in sustainable active ingredient systems, bio-fungicide development, and strategic partnerships with regional seed treatment applicators across Europe and North America.

Croda International Plc

Croda International Plc is a UK-based specialty chemicals company. Headquartered in Snaith, UK. Founded in 1925, the company focuses on developing high-value, sustainable ingredients used across consumer, life sciences, and industrial applications.

- Product Portfolio: Bio-based film polymers, seed flow agents, colorant dispersants, and controlled-release adjuvant systems. The Ecosphere product line leads Croda's sustainable seed coating portfolio.

- Recent Developments: In 2025, Croda International Plc, through its seed enhancement brand Incotec, is set to showcase advanced seed coating technologies at the Asian Seed Congress 2025. The company is highlighting microplastic-free coatings, biological seed applications, and enhanced film-coating solutions designed to improve germination, crop protection, and early plant development.

- Strategic Focus: Sustainability-led innovation in bio-based seed coating polymers, regulatory compliance with REACH and EU Green Deal, and technical partnerships with seed coating manufacturers globally.

Market Concentration Analysis

The global seed coating market exhibits a moderately consolidated structure. The top five companies - Bayer AG, Syngenta, BASF, Croda International Plc, Clariant - collectively hold an estimated 45-55% combined market share in 2025. This concentration is highest in the active ingredient and integrated crop protection seed treatment segment, where regulatory barriers and proprietary chemistry portfolios create significant moats.

The polymer coating materials and adjuvant sub-segments are comparatively more fragmented, with regional specialty chemical companies competing alongside global majors. Entry barriers include complex regulatory approval processes, capital-intensive R&D for active ingredient development, and long-term commercial relationships with seed companies. Medium-term consolidation is expected to continue as companies seek to bundle seed genetics with seed coating treatment portfolios, particularly in biologicals and precision agriculture enablement.

Investment & Growth Opportunities

Fastest Growing Segments

- Biologicals & Microbial Seed Coatings: The biological seed treatment segment is projected to witness strong growth, outpacing overall market expansion. Investments in microbial fermentation infrastructure and bio-polymer coating R&D present high-ROI opportunities for agri-biotech companies targeting the sustainability transition, driven by increasing demand for eco-friendly and performance-enhancing agricultural inputs.

- Pelleting and Precision Seeding Technology: Pelleting is the fastest-growing process segment. Companies offering pelleting technology solutions for vegetable, flower, and specialty crop seed producers are well-positioned for above-market growth through the forecast period.

- Asia Pacific Expansion: Asia Pacific's 20.7% market share and fastest growth trajectory present compelling expansion opportunities. India's biopolymer innovation ecosystem and China's production scale provide dual investment pathways across R&D and commercial manufacturing infrastructure.

Emerging Markets

- Sub-Saharan Africa: FAO and World Bank-backed food security programs are creating nascent but growing demand for seed treatment adoption. First-mover advantages are available for companies establishing regional distribution and farmer education infrastructure across Nigeria, Ethiopia, and Kenya.

- Southeast Asia: Vietnam, Indonesia, and Thailand represent emerging precision agriculture markets with growing seed coating adoption for rice, corn, and tropical vegetable crops aligned with national food self-sufficiency programs.

Venture & Corporate Investment Trends

- Venture capital investment in agri-biotech seed treatment start-ups has seen significant growth in recent years, with biological-focused ventures attracting the majority of funding rounds across North America and Europe, reflecting strong investor confidence in sustainable agricultural innovation and next-generation crop input technologies.

- Corporate R&D spending by leading companies in the seed coating space remains substantial, with a strong focus on bio-actives, nano-coatings, and controlled-release polymer systems, aligned with evolving regulatory transition timelines and increasing demand for sustainable and high-performance agricultural inputs.

- Strategic alliances between seed genetics companies and coating technology providers are accelerating, with integrated seed-treatment bundles emerging as the preferred commercial model for large-scale cereal seed producers, enabling improved performance consistency, streamlined procurement, and enhanced value delivery across global agricultural markets.

Future Market Outlook (2026-2034)

The global seed coating market is projected to expand from USD 3.0 Billion in 2025 to USD 5.45 Billion by 2034, registering a CAGR of 6.63% over the forecast period. North America will retain its dominant position while Asia Pacific emerges as the primary growth leader. Biological and sustainable coating technologies will increasingly displace conventional synthetic-polymer systems, particularly in regulatory-progressive markets across Europe and North America post-2026.

Technological disruptions in nano-coatings, IoT-integrated seed systems, and AI-driven coating formulation optimization are expected to create premium market segments growing. Controlled-release active ingredient coatings will become standard in commercial cereal and oilseed production by 2030, reducing environmental chemical load while improving farm-level economics and farmer return on input investment.

The industry is undergoing structural transformation as seed companies vertically integrate coating capabilities, blurring traditional boundaries between seed genetics providers and agrochemical coating specialists. Companies investing in biodegradable polymer platforms, biologicals integration, and digital traceability systems today are well-positioned to capture disproportionate value as the global seed coating market reaches USD 5.45 Billion by 2034.

Research Methodology

Primary Research

IMARC Group's primary research involves direct engagement with industry stakeholders including seed coating manufacturers, agrochemical companies, seed distributors, agricultural cooperatives, and regulatory experts. Structured interviews and expert consultations were conducted with over 50 industry professionals across North America, Europe, and Asia Pacific through 2024-2025.

Secondary Research

Secondary data sources include industry association databases (ISF, ESTA, CropLife), government agricultural publications (USDA, FAO, EU Commission, ICAR), company annual reports, patent filings, trade journals (Seed World, Agrow, CropLife International), and proprietary IMARC databases covering crop protection and specialty chemical markets globally.

Forecasting Models

Market forecasts utilize a bottom-up and top-down hybrid approach. Bottom-up estimation builds from individual segment demand drivers across crop types and process technologies. Top-down validation is applied against macro-level agricultural production data, GDP growth indices for key markets, and historical market penetration rates. CAGR calculations reflect compound annual growth validated through regression analysis of 2020-2025 historical data.

Seed Coating Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Additive Types Covered | Polymers, Colorants, Pellets, Binders, Active Ingredients, Others |

| Processes Covered | Film Coating, Encrusting, Pelleting |

| Crop Types Covered | Cereals and Grains, Fruits and Vegetables, Flowers and Ornamentals, Oilseeds and Pulses, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bayer AG, Syngenta, BASF, Croda International Plc, Clariant, Sensient Technologies Corporation, UPL, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the seed coating market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global seed coating market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the seed coating industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Seed Coating Market Report

The global seed coating market was valued at USD 3.0 Billion in 2025 and is projected to reach USD 5.45 Billion by 2034, growing at a CAGR of 6.63% from 2026 to 2034.

The market is projected to register a CAGR of 6.63% from 2026 to 2034, driven by precision agriculture adoption, biodegradable polymer innovation, and expanding government support for sustainable seed treatment practices.

North America leads with a 39.8% market share in 2025, driven by precision agriculture adoption, advanced R&D infrastructure, and high-yield commercial crop demand across the United States and Canada.

Film Coating is the leading process segment, holding 44.5% share in 2025, preferred for its uniform thin-layer protection and excellent compatibility with mechanical planting systems for commercial cereal and oilseed production.

Polymers dominate additive types with 30.2% share in 2025, owing to their versatility in controlled-release systems and strong compatibility with diverse active crop protection and biostimulant ingredients.

Primary drivers include declining arable land, precision agriculture growth, biodegradable material innovation, government food security subsidies, and rising demand for sustainable crop protection globally.

Leading companies include Bayer AG, Syngenta, BASF, Croda International Plc, Clariant, Sensient Technologies Corporation, and UPL.

Asia Pacific is the fastest-growing region. Pelleting is the fastest-growing process, and biodegradable polymers are the fastest-growing additive sub-segment, all driven by precision agriculture integration and sustainability demands.

Sustainability mandates under the EU Farm-to-Fork Strategy and EPA guidelines are accelerating adoption of biodegradable polymers and bio-based active ingredients, fundamentally reshaping coating material formulations

Asia Pacific holds a 20.7% share of the global seed coating market in 2025 and is growing fastest, supported by India's biopolymer breakthroughs and China's large-scale cereal production base.

Seed coatings enhance germination rates, protect against pests and diseases, enable controlled-release nutrient delivery, and improve seed flowability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)