Semiconductor Materials Market Report by Material (Silicon Carbide, Gallium Manganese Arsenide, Copper Indium Gallium Selenide, Molybdenum Disulfide, Bismuth Telluride), Application (Fabrication, Packaging), End Use Industry (Consumer Electronics, Manufacturing, Automotive, Energy and Utility, and Others), and Region 2026-2034

Global Semiconductor Materials Market:

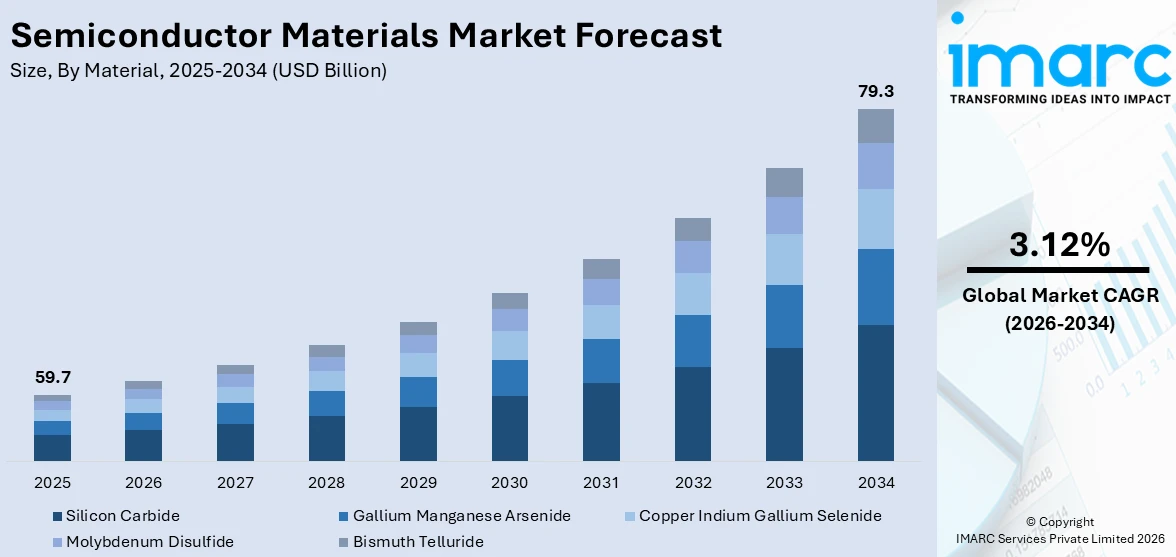

The global semiconductor materials market size reached USD 59.7 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 79.3 Billion by 2034, exhibiting a growth rate (CAGR) of 3.12% during 2026-2034. The increasing demand for electronics, continuous technological advancements in semiconductor manufacturing, and growth in emerging applications like 5G and electric vehicles are some of the key factors driving the growth of the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 59.7 Billion |

| Market Forecast in 2034 | USD 79.3 Billion |

| Market Growth Rate (2026-2034) | 3.12% |

Semiconductor Materials Market Analysis:

- Major Market Drivers: The proliferation of smartphones, tablets, wearable devices, and smart home appliances is primarily driving the growth of the market. Furthermore, the deployment of 5G networks that require semiconductor materials capable of handling higher frequencies and faster data rates is also contributing to the market growth.

- Key Market Trends: Demand for semiconductor materials in renewable energy technologies like solar photovoltaics and energy storage systems (batteries) is creating a positive outlook for the overall market. Besides this, constant innovations in semiconductor materials driven by the demand for smaller, faster, and more efficient electronic devices are further propelling the semiconductor materials market industry growth.

- Competitive Landscape: Some of the leading players in the global semiconductor materials market include BASF SE, Air Liquide Electronics, Avantor Inc., DuPont de Nemours, Inc., Entegris, Inc., Hemlock Semiconductor Operations LLC, Henkel Adhesive, JSR Corporation, LG Chem Ltd., Sumco Corporation, and Tokyo Ohka Kogyo Co., Ltd., among others.

- Geographical Landscape: According to the report, Asia Pacific currently dominates the global market. The growth of the region can be attributed to the growing demand for semiconductor chips and increasing investment in manufacturing facilities and equipment across the region.

- Challenges and Opportunities: Challenges in the semiconductor materials market include navigating supply chain disruptions, geopolitical uncertainties, and meeting increasingly stringent environmental regulations. However, opportunities lie in the growing demand for advanced materials to support technologies like 5G, electric vehicles, and renewable energy, as well as the potential for innovation in sustainable materials and manufacturing processes to address these challenges.

To get more information on this market Request Sample

Semiconductor Materials Market Trends:

Expanding Consumer Electronics Sector

Significant growth in the consumer electronics sector is primarily driving the growth of the global semiconductor materials market. Semiconductors are integral to the consumer electronics market, powering devices ranging from smartphones and tablets to laptops, TVs, and smart home appliances. They enable the processing, memory storage, and transmission of data essential for these devices’ functionality. In 2024, the revenue generated in the consumer electronics market worldwide amounted to a staggering US$ 1,046.0 Billion. Moreover, by 2028, the volume of the consumer electronics market is expected to reach 9,014.0 million pieces. Besides this, the consumer share of the total devices, including fixed and mobile devices, reached to 74%, in 2023. Furthermore, the smartphone market is the major consumer of semiconductors in the consumer electronics segment. The smartphone market has been very competitive in recent years. The increasing usage of cell phones is anticipated to propel the semiconductor materials market share in the coming years. For instance, according to Ericsson, smartphone subscriptions are expected to reach 7.8 billion by 2027, from 6.3 billion in 2021. Such a rapid growth in the adoption of smartphones and other consumer electronics like smart TVs, laptops, refrigerators, etc., is likely to create a positive outlook for the overall market.

Increasing Shift Towards 5G Technology

The shift towards 5G technology is significantly impacting the semiconductor industry by driving demand for advanced semiconductor materials and components. 5G networks require semiconductors capable of handling higher frequencies, faster data speeds, and lower latency. Moreover, the escalating proliferation of IoT applications from the industrial sector is significantly catalyzing the market for 5G services, which is eventually offering lucrative growth opportunities to the semiconductor materials market. For instance, semiconductor materials market statistics by IMARC indicate that the global 5G services market size reached US$ 128.1 Billion in 2023. Looking forward, IMARC Group expects the market to reach US$ 3,431.8 Billion by 2032, exhibiting a growth rate (CAGR) of 44.1% during 2024-2032. Besides this, the growing interest of telecom operators to invest and launch in 5G technology is expected to fuel the demand for 5G capable devices, where consumers and industries are expected to opt for 5G devices. For instance, according to a report by Ericsson, 5G mobile subscriptions, which grew from 273.96 million in 2020 to 664.18 million in 2021, are expected to reach 4,389.77 million globally by 2027, thereby driving the demand for semiconductor chips and semiconductor materials.

Growing Product Applications in Automotives

Semiconductor materials are crucial in the automotive industry for enhancing vehicle performance, safety, and efficiency. They power advanced driver assistance systems (ADAS) like collision avoidance, adaptive cruise control, and lane departure warning systems. Moreover, the expanding automotive industry and the escalating sales of autonomous vehicles are creating a positive outlook for the semiconductor materials market. For instance, in 2019, there were around 31 million cars with at least some level of automation in operation worldwide. It is expected that their number will surpass 54 million in 2024. Additionally, according to IMARC, the global autonomous vehicle market size reached US$ 81.0 Billion in 2023. Looking forward, IMARC Group expects the market to reach US$ 1,171.6 Billion by 2032, exhibiting a growth rate (CAGR) of 33.5% during 2024-2032. Furthermore, various automotive manufacturers are increasingly developing highly autonomous cars, which is bolstering the employment of semiconductors. For instance, in March 2024, Pony.ai, a leading global autonomous mobility company, signed a Memorandum of Understanding (MoU) with the Government of the Grand Duchy of Luxembourg (“The Government”) to advance the development of autonomous mobility in Luxembourg. Such a significant expansion in the autonomous cars market is anticipated to positively impact the semiconductor market outlook in the coming years.

Global Semiconductor Materials Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global semiconductor materials market report, along with forecasts at the global and regional levels from 2026-2034. Our report has categorized the market based on material, application, and end use industry.

Breakup by Material:

- Silicon Carbide

- Gallium Manganese Arsenide

- Copper Indium Gallium Selenide

- Molybdenum Disulfide

- Bismuth Telluride

Silicon carbide holds the majority of the total market share

The report has provided a detailed breakup and analysis of the market based on the material. This includes silicon carbide, gallium manganese arsenide, copper indium gallium selenide, molybdenum disulfide, and bismuth telluride. According to the report, silicon carbide holds the majority of the total market share.

Silicon carbide (SiC) is a wide-bandgap semiconductor material known for its exceptional electrical properties, such as high breakdown electric field strength and thermal conductivity. Its applications span power electronics, where it enables more efficient energy conversion in electric vehicles, renewable energy systems like solar inverters, and industrial motor drives. SiC devices operate at higher temperatures and voltages than traditional silicon counterparts, offering reduced energy losses and smaller sizes, crucial for compact and efficient power modules. Overall, SiC's benefits include enhanced system performance, reduced cooling requirements, and increased reliability, making it a key enabler for next-generation high-power electronic applications.

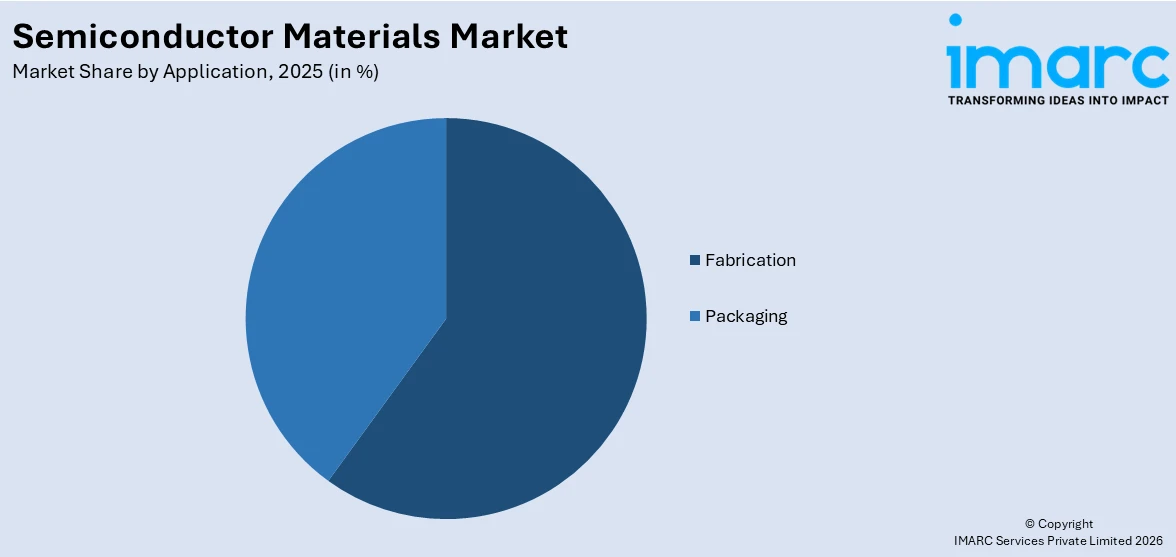

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Fabrication

- Silicon Wafers

- Electronic gases

- Photomasks

- Photoresist ancillaries

- CMP Materials

- Photoresists

- Wet chemicals

- Others

- Packaging

- Leadframes

- Organic Substrates

- Ceramic Packages

- Encapsulation Resins

- Bonding Wires

- Die-Attach Materials

- Others

Fabrication currently exhibits a clear dominance in the market

The report has provided a detailed breakup and analysis of the market based on the application. This includes fabrication (Silicon Wafers, Electronic gases, Photomasks, Photoresist ancillaries, CMP Materials, Photoresists, Wet chemicals, Others) and packaging (Leadframes, Organic Substrates, Ceramic Packages, Encapsulation Resins, Bonding Wires, Die-Attach Materials, Others). According to the report, fabrication currently exhibits a clear dominance in the market.

Semiconductor materials play a critical role in fabrication processes, particularly in the production of integrated circuits (ICs). Silicon is the most commonly used semiconductor material due to its abundant supply and excellent electrical properties. Through photolithography, etching, and doping processes, semiconductor materials are patterned and modified to create intricate structures on silicon wafers. Semiconductor silicon wafer remains the core component of many microelectronic devices and forms the cornerstone of the electronics industry. These structures form transistors, diodes, and other components essential for electronic devices. Additionally, the rising adoption of consumer electronics and wearable technology like smartwatches is also bolstering the market growth. According to Zebra Technologies Corporation, 40-50% of manufacturers globally adopted wearables in 2022. Also, the demand for small-sized gadgets has raised the need for more functionalities from a single device. This indicates that an IC chip should now house more transistors to support more functionalities, thereby bolstering the market for semiconductor materials.

Breakup by End Use Industry:

- Consumer Electronics

- Manufacturing

- Automotive

- Energy and Utility

- Others

The consumer electronics industry currently accounts for the largest market share

The report has provided a detailed breakup and analysis of the market based on the end use industry. This includes consumer electronics, manufacturing, automotive, energy and utility, and others. According to the report, the consumer electronics industry currently accounts for the largest market share.

The global semiconductor materials market is experiencing substantial growth, largely fueled by the expansion in consumer electronics. These semiconductors are essential components in a wide array of devices, including smartphones, tablets, laptops, TVs, and smart home appliances. According to the Consumer Technology Association's (CTA) 'US Consumer Technology Sales and Forecast' study, CTA stated that 5G-enabled smartphone devices reached 2.1 million units and crossed US$ 1.9 Billion in revenue in 2021. Furthermore, in 2023, Apple announced a contribution of US$ 350 Billion to the US economy and promised 2.4 million jobs over the next five years, which comprises new investments and its existing spending with domestic companies for supply and manufacturing. The company is a prominent player in the consumer electronics industry. Hence, the announcement is expected to propel the demand for semiconductor materials in the coming years.

Breakup by Region:

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

Asia Pacific currently dominates the global market

The semiconductor materials market has also provided a comprehensive analysis of all the major regional markets, which include North America, Asia Pacific, Europe, Latin America, and Middle East and Africa. According to the report, Asia Pacific currently dominates the global market.

The growth of the region can be attributed to the rising demand for semiconductor chips and increasing investment in manufacturing facilities and equipment across the region. Moreover, the Chinese government's national strategic plan, Made in China 2025, has become a key factor in the growth of the country's semiconductor industry. A central goal of this plan is the growth of the semiconductor industry. Furthermore, the growth in wearable electronic devices has also been leading to the adoption of new miniaturized chips, propelling the semiconductor's growth and increasing the demand for wafers, further driving the market growth. As per Cisco Systems, the number of connected wearable devices in China reached nearly 439 million in 2022 from 378.8 million in 2021. Additionally, according to Ericsson, the number of smartphone mobile network subscriptions reached approximately 6.6 billion worldwide in 2022 and is expected to exceed 7.8 billion by 2028. This will further propel the growth of the semiconductor materials market in the region.

Competitive Landscape:

The report provides a comprehensive analysis of the competitive landscape in the global semiconductor materials market with detailed profiles of all major companies, including:

- BASF SE

- Air Liquide Electronics

- Avantor Inc.

- DuPont de Nemours, Inc.

- Entegris, Inc.

- Hemlock Semiconductor Operations LLC

- Henkel Adhesive

- JSR Corporation

- LG Chem Ltd.

- Sumco Corporation

- Tokyo Ohka Kogyo Co., Ltd.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Semiconductor Materials Market News:

- June 2024: G-7 leaders announced plans for a semiconductor supply chain coordination group. The group will help G-7 leaders focus on subsea cable connectivity for Internet security and resilience, amid global chip shortage challenges.

- February 2024: Researchers from the Indian Institute of Technology Guwahati, Department of Electronics and Electrical Engineering and Centre for Nanotechnology, in collaboration with IIT Mandi and Institute of Sensor and Actuator Systems, Technical University Wien, developed a cost-effective method to grow a special semiconductor. The new semiconductor holds the potential to significantly enhance the efficiency of power electronics used in high-power applications such as electric vehicles, high-voltage transmission, traction, and industry automation, among others.

Global Semiconductor Materials Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | Silicon Carbide, Gallium Manganese Arsenide, Copper Indium Gallium Selenide, Molybdenum Disulfide, Bismuth Telluride |

| Applications Covered |

|

| End Use Industries Covered | Consumer Electronics, Manufacturing, Automotive, Energy and Utility, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | BASF SE, Air Liquide Electronics, Avantor Inc., DuPont de Nemours, Inc., Entegris, Inc., Hemlock Semiconductor Operations LLC, Henkel Adhesive, JSR Corporation, LG Chem Ltd., Sumco Corporation, Tokyo Ohka Kogyo Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the semiconductor materials market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global semiconductor materials market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the semiconductor materials industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Semiconductor Materials Market Report

We expect the global semiconductor materials market to exhibit a CAGR of 3.12% during 2026-2034.

The growing application of semiconductor materials in the manufacturing of different electronic components is one of the key factors catalyzing the global semiconductor materials market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations resulting in temporary shutdown of numerous manufacturing units of semiconductor materials.

Based on the material, the global semiconductor materials market can be segmented into silicon carbide, gallium manganese arsenide, copper indium gallium selenide, molybdenum disulfide, and bismuth telluride. According to semiconductor materials market insights silicon carbide holds the majority of the total market share

Based on the application, the global semiconductor materials market has been divided into fabrication and packaging, where fabrication currently exhibits a clear dominance in the market.

Based on the end use industry, the global semiconductor materials market can be categorized into consumer electronics, manufacturing, automotive, energy and utility, and others. Among these, the consumer electronics industry currently accounts for the largest market share.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa. According to the semiconductor materials market forecast by IMARC, Asia Pacific currently dominates the global market.

Some of the major players in the global semiconductor materials market include BASF SE, Air Liquide Electronics, Avantor Inc., DuPont de Nemours, Inc., Entegris, Inc., Hemlock Semiconductor Operations LLC, Henkel Adhesive, JSR Corporation, LG Chem Ltd., Sumco Corporation, Tokyo Ohka Kogyo Co., Ltd., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade