Siding Market Size, Share, Trends and Forecast by Material, End Use, Application, and Region 2026-2034

Global Siding Market Size, Share, Trends & Forecast (2026-2034)

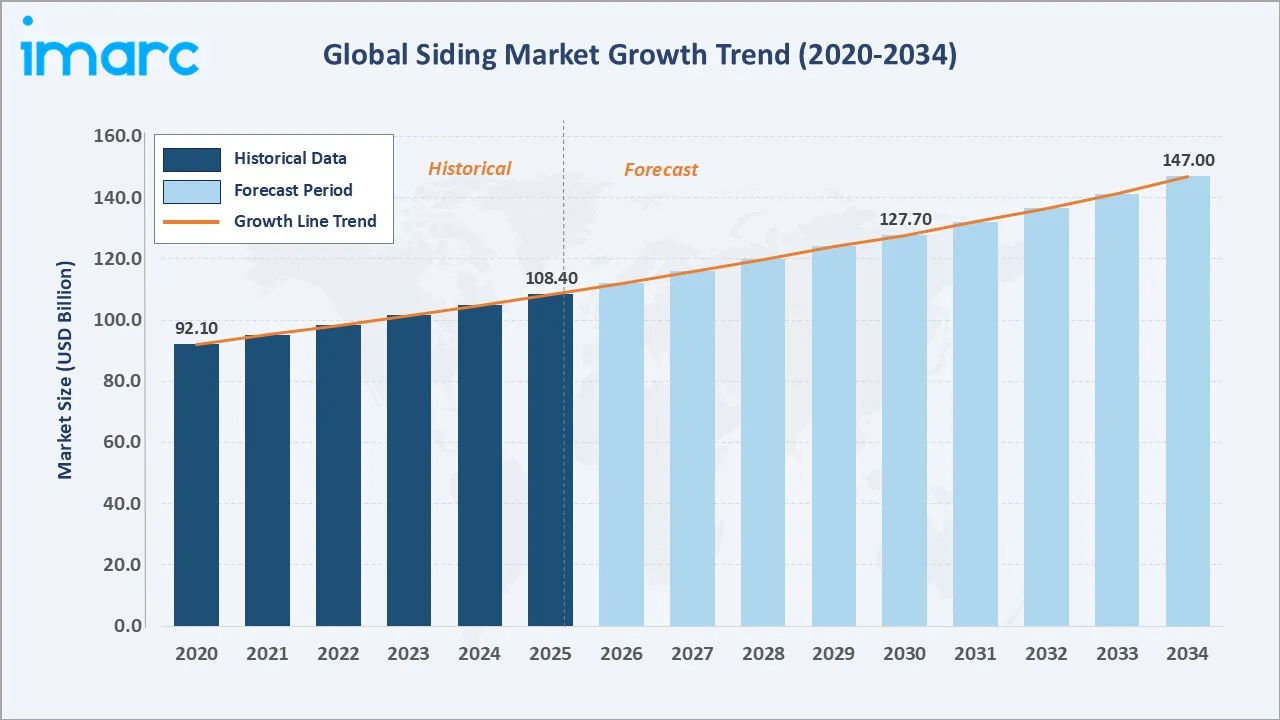

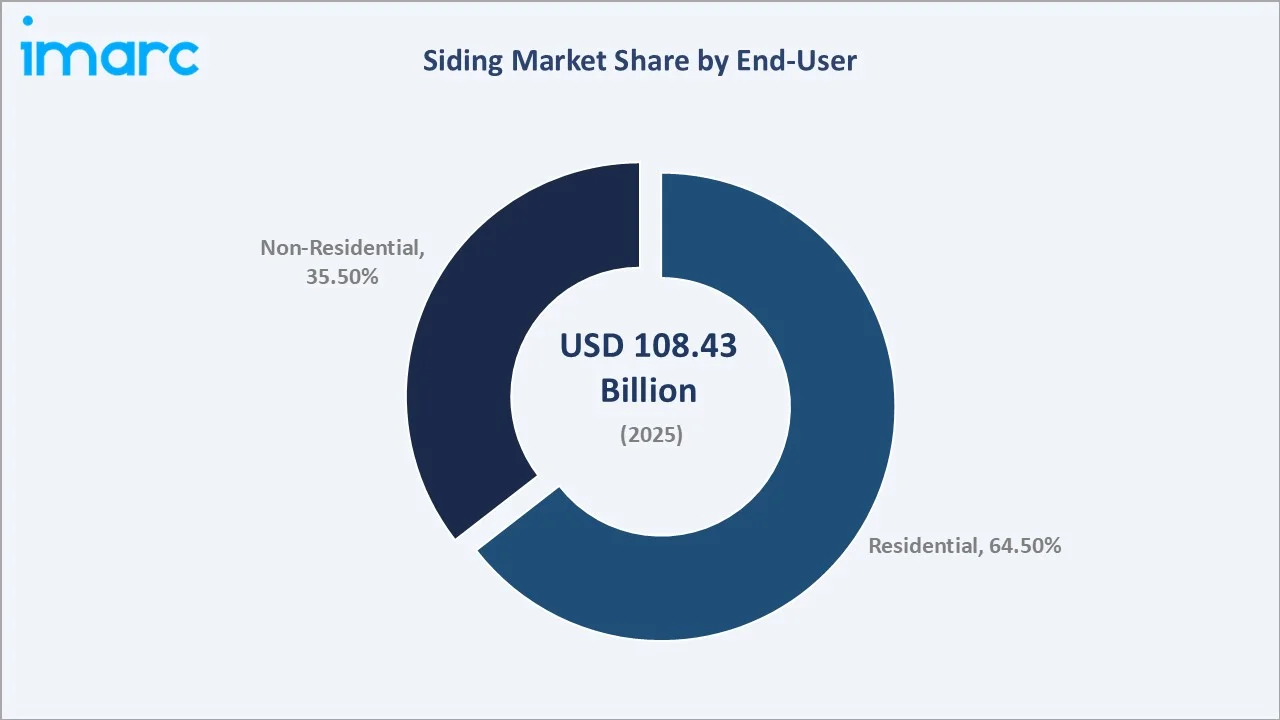

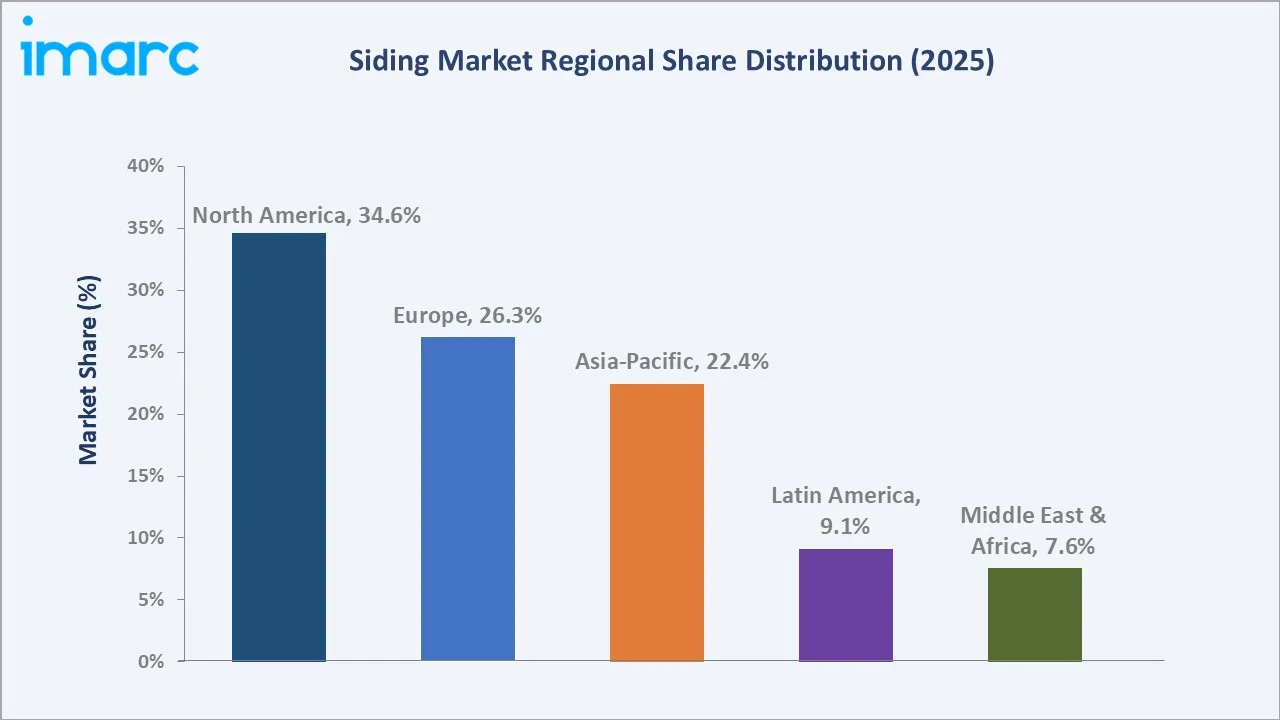

The global siding market size reached USD 108.43 Billion in 2025 and is projected to reach USD 147.03 Billion by 2034, at a CAGR of 3.32% during 2026-2034. Rising global construction activity with an average annual growth in construction of 3.6% per annum over the decade to 2030, energy efficiency mandates across building codes, surging repair and remodeling spending, and growing aesthetic preferences for durable, low-maintenance exteriors are the primary growth drivers. Fiber cement leads the material segment at 26.8%, residential dominates end-use at 64.5%, and North America holds a 34.6% regional share in 2025, anchored by robust single-family housing starts and a mature renovation market.

Market Snapshot

|

Metric |

Value |

|

Market Size 2025 |

USD 108.43 Billion |

|

Forecast Market Size (2034) |

USD 147.03 Billion |

|

CAGR 2026-2034 |

3.32% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.6%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~4.4% CAGR, 2026-2034) |

|

Leading Material |

Fiber Cement (26.8%, 2025) |

|

Leading End-User |

Residential (64.5%, 2025) |

The siding market trajectory from 2020 to 2034, grew from USD 92.1 Billion in 2020 to USD 108.43 Billion in 2025 anchored at USD 127.7 Billion in 2030 before reaching USD 147.03 Billion by 2034. This steady expansion reflects the inelastic demand nature of exterior cladding as a mandatory building component tied directly to global construction output.

To get more information on this market, Request Sample

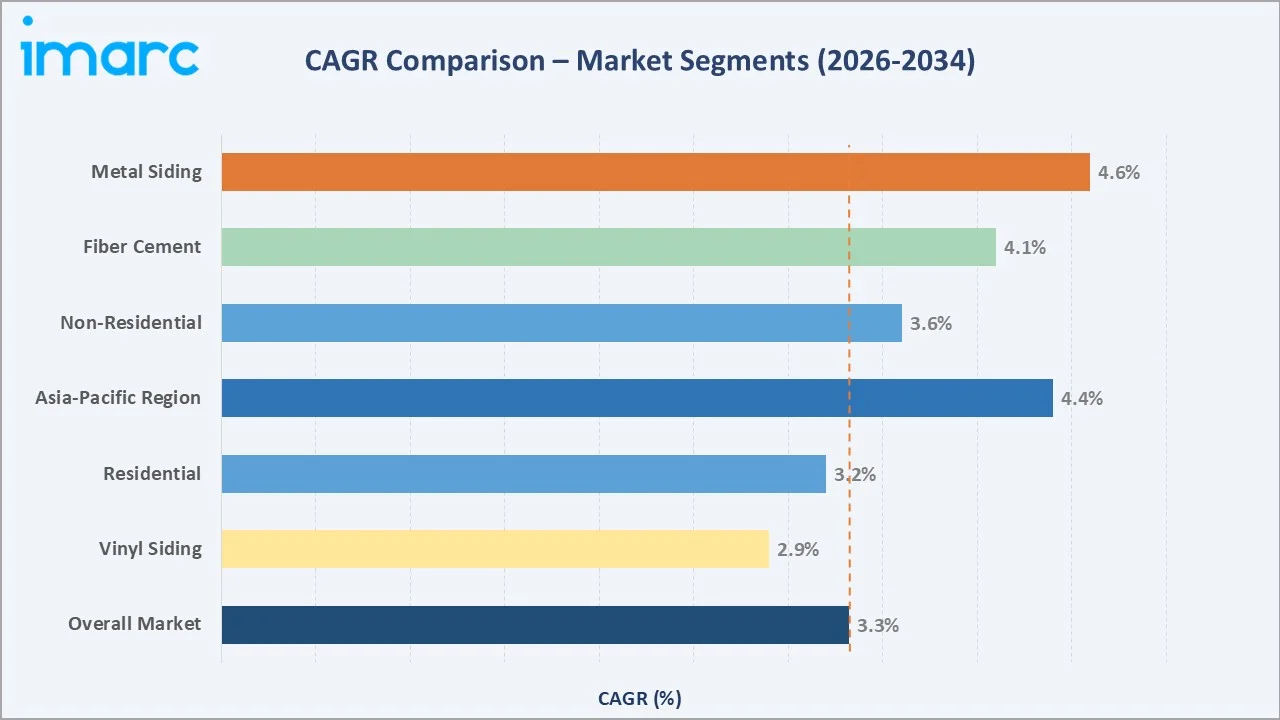

The CAGR across key segments, metal siding leads at ~4.6% CAGR and Asia-Pacific at ~4.4%, both outpacing the overall 3.32% market rate. These above-average growth pockets reflect steel cladding’s rise in commercial construction and Asia-Pacific’s urbanization-driven new build activity through 2034.

Executive Summary

The global siding market is growing at a 3.32% CAGR from USD 108.43 Billion in 2025 to USD 147.03 Billion by 2034. Siding, also known as wall cladding or exterior casing, is the protective and decorative material applied to the exterior walls of buildings, providing weather resistance, thermal insulation, and aesthetic value. The market serves both new construction and repair and maintenance applications across residential and non-residential building segments globally.

Fiber cement leads the material segment at 26.8% in 2025, reflecting its superior durability, resisting rot, termites, fire, and moisture, and its ability to mimic wood, brick, and stone aesthetics at lower long-term cost. Residential end-use commands 64.5%, driven by single-family housing starts and the US renovation market, where siding replacement ranks among the highest-ROI exterior improvement projects.

North America leads regionally at 34.6% in 2025, with the US accounting for the majority of regional revenue through its high housing turnover rate, aggressive renovation spending, and building code-driven material upgrades. Europe at 26.3% reflects strong demand from Central and Eastern European housing modernization programs. Asia-Pacific at 22.4% is growing fastest at ~4.4% CAGR, driven by China’s and India’s residential construction boom.

Key Market Insights

|

Insight |

Data / Finding |

|

Largest Material |

Fiber Cement – 26.8% (2025) |

|

Leading End-User |

Residential – 64.5% (2025) |

|

Leading Region |

North America – 34.6% (2025) |

|

Fastest Region |

Asia-Pacific – ~4.4% CAGR |

Key Analytical Observations Supporting the Above Data:

- Fiber cement at 26.8% in 2025, commands the largest material share due to a compelling combination of functional performance and aesthetic versatility. James Hardie’s HardiePlank, available in 21 color options,has become the default specification for premium residential construction in North America, Australia, and Northern Europe.

- Residential end-use at 64.5% in 2025is anchored by two concurrent demand streams: new single-family construction and repair and remodeling.

- North America’s 34.6% regional dominance reflects structural market advantages. The US siding market is reinforced by the Insurance Institute for Business & Home Safety (IBHS) Fortified Home program, which specifies impact-resistant siding standards that drive premium material upgrades.

- Asia-Pacific at 22.4% in 2025, growing at ~4.4% CAGR, is driven by China’s 14th Five-Year Plan and India’s Pradhan Mantri Awas Yojana (PMAY) housing scheme targeting 2 crore affordable homes.

Global Siding Market Overview

Siding refers to all exterior wall cladding materials applied to the outside of a building structure for weather protection, thermal performance, moisture management, and visual enhancement. Material categories span fiber cement (portland cement, wood pulp, sand composite), vinyl (PVC extrusion), engineered wood (LP SmartSide, zinc borate-treated strand board), natural wood, brick and stone veneer, metal panels (steel, aluminum), stucco (acrylic and traditional lime), and concrete composites. Each material category occupies a distinct price-performance niche across new construction and repair and maintenance applications.

The ecosystem encompasses raw material suppliers (cement producers, PVC resin manufacturers, timber mills, steel mills), siding manufacturers and OEMs, quality testing laboratories, wholesale distributors, contractors and installers, and end-users across residential and non-residential building sectors. Key macroeconomic drivers include global construction output, US renovation market, energy efficiency building code upgrades mandated across EU, North America, and Australia, and urbanization adding 2.5 Billion new urban residents globally through 2050.

Market Dynamics

To evaluate market opportunities, Request Sample

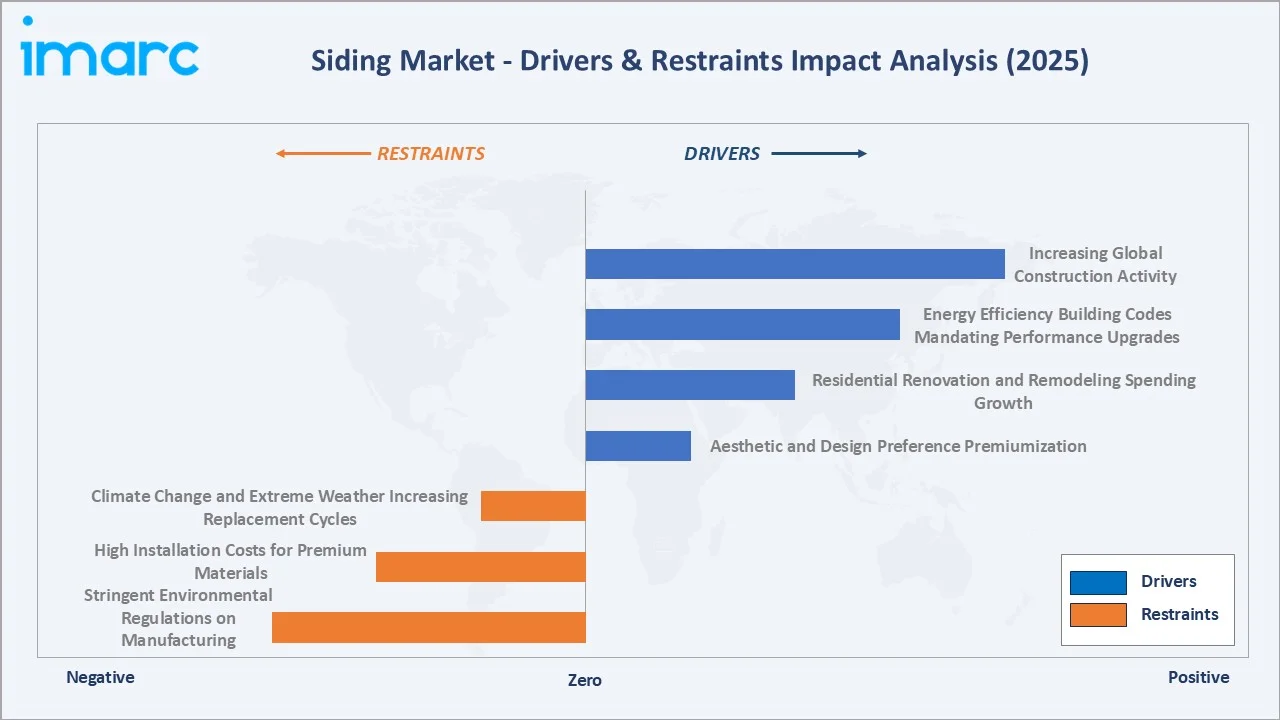

Market Drivers

- Increasing Global Construction Activity: The US construction output grew at approximately 4.5% in 2024, with residential construction the dominant driver. In the US, housing starts reached 1.36 million in 2024. Each new residential unit requires 1,200–2,500 square feet of siding material, creating an irreplaceable baseline demand that grows in direct proportion to global construction activity.

- Energy Efficiency Building Codes Mandating Performance Upgrades: The EU’s Energy Performance of Buildings Directive requires all new buildings to be zero-emission from 2028.

- Residential Renovation and Remodeling Spending Growth: US homeowner equity reached USD 32 Trillion in 2024, providing the financial capacity for premium siding upgrade decisions that are driving the market.

- Aesthetic and Design Preference Premiumization: The rise of architectural social media platforms is accelerating trend adoption for board-and-batten vertical siding, dark color schemes, and mixed-material facades that require premium siding products.

Market Restraints

- Stringent Environmental Regulations on Manufacturing: The EU’s Construction Products Regulation (CPR) recast imposes new chemical substance restrictions on siding products, particularly targeting flame retardants in vinyl and biocide treatments in fiber cement.

- High Installation Costs for Premium Materials: Fiber cement siding installation requires specialized contractor training and certification. Installation labor costs for fiber cement average USD 4–6 per square foot versus USD 2–3 for vinyl, creating a total installed cost gap of USD 6–10 per square foot that limits premium penetration in cost-sensitive new construction and affordable housing segments.

Market Opportunities

- Insulated Siding for Energy Code Compliance: The IECC 2021 mandate for continuous insulation (ci) in climatic zones 4–8, covering approximately 65% of US housing units, creates structural demand for insulated siding products.

- Asia-Pacific Urbanization Creating Mass-Market Demand: India’s PMAY-U (Urban) housing mission successfully sanctioned 4.21 crore houses, and ASEAN’s infrastructure buildout collectively represent the world’s largest single growth opportunity for fiber cement and metal siding manufacturers.

Market Challenges

- Climate Change and Extreme Weather Increasing Replacement Cycles: Increased frequency of extreme weather events, hurricanes (Southeastern US), wildfires (Western US, Australia), and severe hailstorms (Midwest US), is simultaneously a demand driver (insurance-funded replacement) and a challenge (product specification complexity).

- Digital Visualization and Homeowner Expectation Gap: 72% of homeowners now use digital visualization tools before purchase, creating elevated aesthetic expectations that on-site installation quality sometimes fails to meet.

Emerging Market Trends

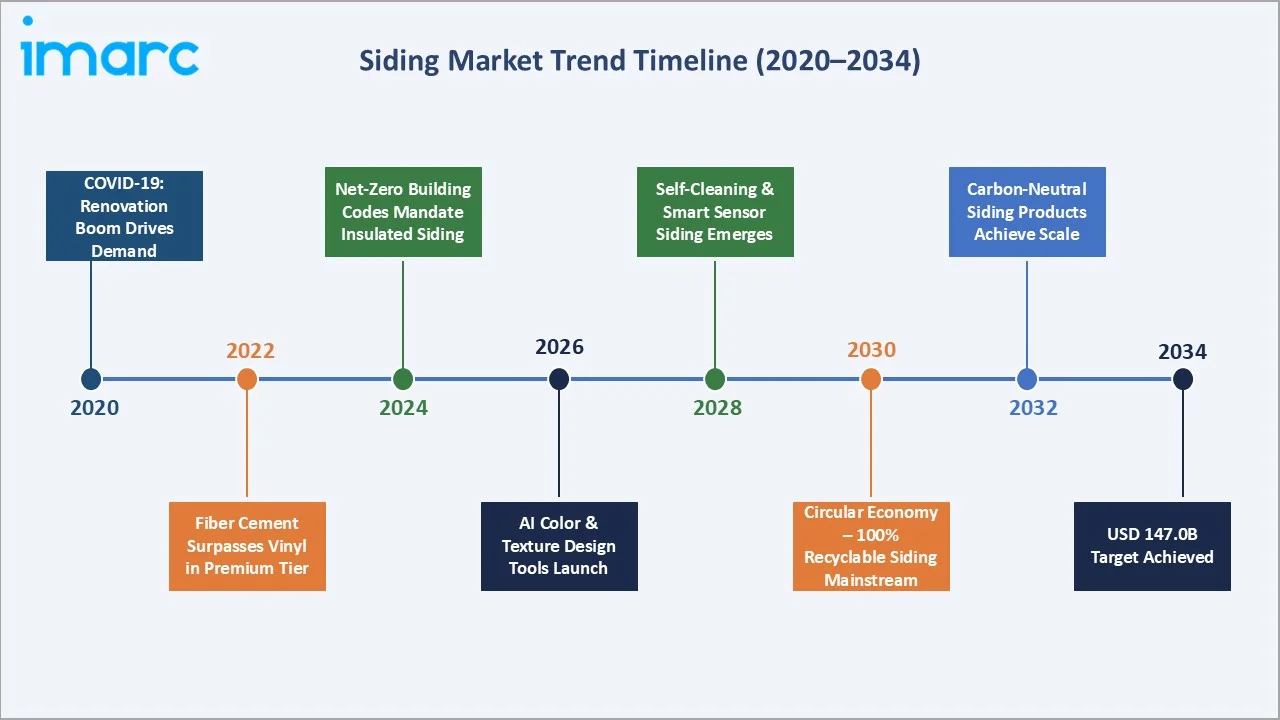

1. Engineered Wood Siding Capturing Mid-Price Natural-Aesthetic Demand

LP Building Solutions’ SmartSide, strand-based engineered wood with zinc borate treatment for insect and rot resistance, is growing rapidly as a mid-price alternative between vinyl and premium fiber cement. LP Building Solutions’ dedicated SmartSide expansion represented a manufacturing capacity investment, signaling long-term commitment to this growing segment.

2. Metal Siding Gaining Share in Commercial and Multifamily Construction

Metal siding, particularly steel and aluminum panel systems, is growing at ~4.6% CAGR as the fastest-rising material category in the commercial construction segment. The shift toward modern architectural aesthetics in commercial and multifamily buildings is driving the specification of concealed-fastener metal panel systems that provide clean-line facades previously achievable only with expensive precast concrete.

3. Sustainability and Circular Economy Driving Green Building Certification

The US Green Building Council reports more than 7,500 LEED-certified commercial projects in 2025, each requiring cladding materials with Environmental Product Declarations (EPDs) and recycled content documentation.

4. Digital Design Tools Elevating Consumer Specification Sophistication

Digital design tools reduce post-installation dissatisfaction while simultaneously increasing average project value. Digital visualizer users are more likely to choose premium material options when they can see the result before commitment. AI-powered style recommendation engines integrated into contractor sales tools are expected to increase average siding project values.

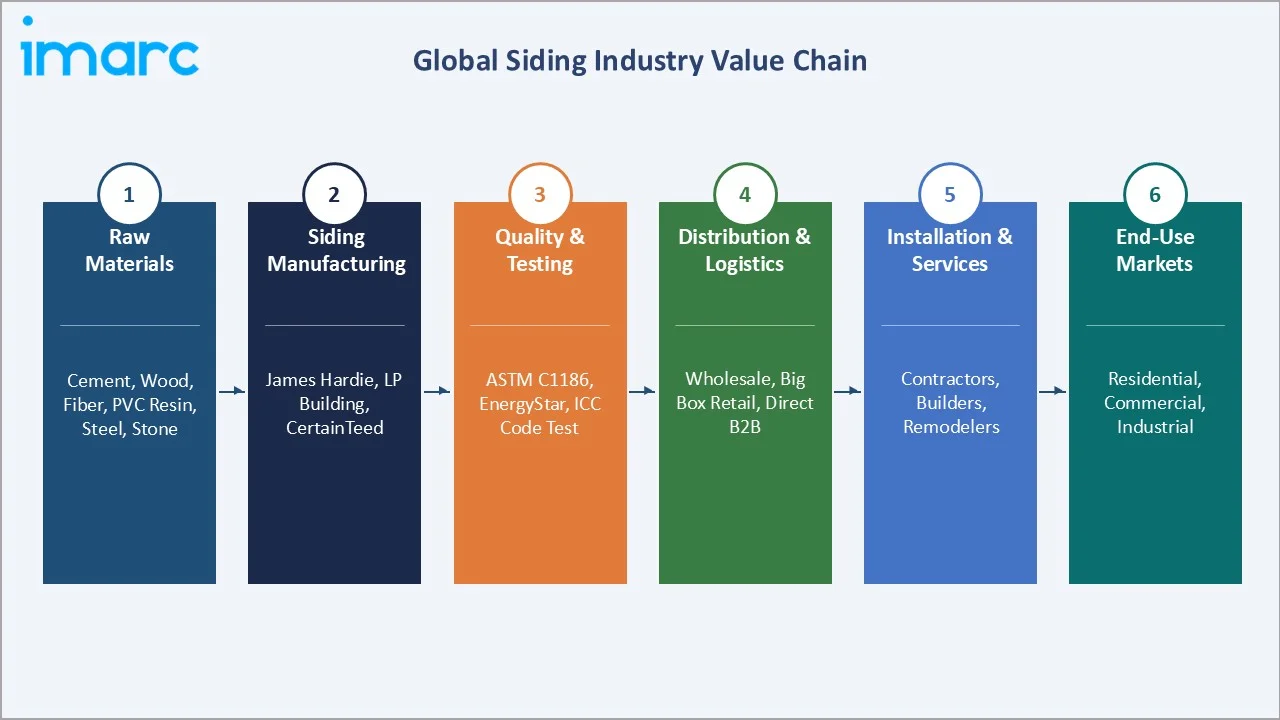

Industry Value Chain Analysis

The siding value chain creates highest margin at the branded manufacturing stage, where James Hardie commands EBIT margins of 25–28% on fiber cement production, versus 8–12% for commodity vinyl manufacturers, through product IP, contractor certification programs, and factory-applied ColorPlus finish premiums.

|

Stage |

Key Players & Examples |

|

Raw Materials |

Portland cement, PVC resin, wood fiber, steel coils |

|

Siding Manufacturing |

James Hardie Industries, LP Building Solutions, Saint-Gobain |

|

Quality & Testing |

ASTM C1186, ASTM D3679, EnergyStar certification, IBHS Fortified Home, GREENGUARD Gold, ISO 9001 plant certification |

|

Distribution |

Two-step distribution (manufacturers to distributors to contractors): Builders FirstSource, ABC Supply, Big box retail: Home Depot, Lowe’s, Menards |

|

Installation |

James Hardie ALLIANCE, LP BuildSmart Preferred Contractor Program referral network, independent siding contractors, national remodeling chains |

|

End-Use Markets |

Residential (single-family, multifamily, mobile homes), Non-residential (commercial office, retail, industrial, institutional healthcare/education) |

Two-step distribution, where manufacturers sell to regional wholesale distributors who sell to contractor installers, remains the dominant channel.

Technology Landscape in the Siding Industry

Advanced Fiber Cement Formulation

James Hardie’s HZ10 technology, a proprietary formulation adjusting the portland cement, silica, and cellulose fiber ratios for specific climate zones, delivers improvement in moisture resistance and freeze-thaw durability over standard fiber cement formulations.

LP SmartSide SmartGuard Process

LP Building Solutions’ SmartGuard manufacturing process infuses engineered wood fiber with zinc borate, a borate salt with proven termite, fungal, and moisture resistance, throughout the strand mat before resin binder application and press forming. This through-body treatment versus surface-applied coatings that can wear or be compromised during installation provides a limited warranty performance against rot, insects, and moisture damage.

Digital Manufacturing and Mass Customization

CNC cutting, digital texture embossing, and automated color line changeover capabilities are enabling siding manufacturers to offer wider product customization at mass production economics.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material |

Fiber Cement |

26.8% |

2025 |

|

End Use |

Residential |

64.5% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

North America |

34.6% |

2025 |

By Material

Fiber cement commands 26.8% in 2025, having overtaken vinyl in the premium residential segment in North America by 2023. Fiber cement’s Class A fire rating, warranty, and zero-rot performance make it the mandatory specification in California wildfire zones, where 1.2 million homes need to build in California.

To access detailed market analysis, Request Sample

Vinyl at 22.4% remains the volume champion in repair and remodeling. Wood at 14.2% reflects natural wood’s strong position in premium architectural markets, where cedar and pine shingle siding is installed. Metal at 9.3% is the fastest-growing material at ~4.6% CAGR, gaining share in commercial and multifamily construction. Brick at 10.6% maintains strong institutional demand, where masonry construction traditions persist.

By End-User

Residential end-use at 64.5% in 2025, is driven by two concurrent demand streams. New single-family construction, 1.36 million US housing starts in 2024, generates irreplaceable baseline siding demand. US homeowner equity at USD 32 Trillion provides financial capacity for premium siding selections that are elevating average residential project values.

Non-residential end-use at 35.5% in 2025, encompasses commercial offices, retail centers, warehouses, data centers, schools, hospitals, and industrial facilities. Data center construction, driven by AI infrastructure investment, represents an emerging high-value non-residential siding application where insulated metal panel systems provide combined exterior cladding and thermal performance in a single product.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Data |

|

North America |

34.6% |

US 1.36M housing starts (2024), renovation market, insulated siding mandates |

|

Europe |

26.3% |

EU EPBD zero-emission buildings from 2028, Eastern European housing modernization, natural wood and brick tradition in the UK, Germany, Nordic markets |

|

Asia-Pacific |

22.4% |

China 40M urban housing units; India PMAY homes under construction; ASEAN SHERA expansion, Japan commercial retrofit |

|

Latin America |

9.1% |

Brazil housing deficit 5,97 million units, Mexico urbanization, Colombia/Chile commercial construction growth, fiber cement adoption growing from low base |

|

Middle East & Africa |

7.6% |

Saudi NEOM, UAE construction growth, South Africa affordable housing, climate-appropriate metal and stucco siding demand in hot arid regions |

North America’s 34.6% dominance in 2025 reflects the region’s uniquely favorable siding market conditions. The US has the world’s highest per-capita siding renovation spend, driven by aging housing stock, high housing turnover stimulating pre-sale renovation, and progressive building energy codes mandating insulated exterior cladding upgrades.

Asia-Pacific (22.4%, 2025), growing fastest at ~4.4% CAGR, represents the market’s most dynamic opportunity, with China’s 14th Five-Year Plan, India’s PMAY scheme, and ASEAN construction boom collectively adding more new siding-requiring building floor area annually than North America and Europe combined. Europe at 26.3% in 2025, reflects a mixed demand picture. Western European mature markets, the UK, Germany, and France, show moderate renovation-driven growth as energy efficiency retrofits replace aging brick and stucco cladding. Eastern European markets, Poland, Czech Republic, Romania, and Hungary, are growing as post-Soviet housing stock undergoes comprehensive thermal envelope upgrades under EU Cohesion Funding programs.

Competitive Landscape

The global siding market has a moderately fragmented structure. The top 5 players, James Hardie, Cornerstone Building Brands, LP Building Solutions, Saint-Gobain, and Etex Group, collectively account for an estimated 35–45% of total global siding market revenue in 2025.

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

James Hardie Industries PLC |

HardiePlank / HardiePanel |

Leader |

Fiber cement global leader, 20,000+ certified contractors, 30-yr warranty |

|

Cornerstone Building Brands |

Ply Gem / Mastic / Variform |

Leader |

Largest North American siding manufacturer; vinyl + metal + trim |

|

LP Building Solutions |

LP SmartSide |

Leader |

Engineered wood strand siding; zinc borate SmartGuard; 50-yr warranty; 12%/year segment growth |

|

Compagnie de Saint-Gobain S.A. |

CertainTeed |

Leader |

Multi-material portfolio, 100+ year building materials heritage, global reach |

|

Etex Group SA |

Equitone / Cedral |

Leader |

Belgian global fiber cement producer; architectural panel innovation; strong European/APAC presence |

|

Nichiha Corporation |

Nichiha Architectural Panels |

Challenger |

Premium large-format fiber cement panels; commercial/multifamily specialist; Japan + US presence |

|

SHERA Public Company |

SHERA Fiber Cement |

Emerging |

Thailand-based ASEAN leader; 30% capacity expansion 2024; affordable fiber cement for ASEAN markets |

|

Kaycan Ltd. |

Kaycan Vinyl / Aluminium |

Emerging |

Canada-based; vinyl and aluminum siding; Canadian/Northeastern US contractor channel specialist |

The market bifurcates between globally present diversified building materials groups and regionally focused specialty siding manufacturers.

Key Company Profiles

James Hardie Industries PLC

James Hardie Industries PLC headquartered in Dublin, Ireland, is the world’s largest manufacturer of fiber cement building products.

- Product Portfolio: HardiePlank Lap Siding, HardiePanel Vertical Siding, HardieTrim Boards, HardieShingle, HardieSoffit panels, HardieBacker cement board, and HardieLapSD.

- Recent Developments: In September 2025, James Hardie Building Products Inc. renewed its partnership with Green Brick Partners, Inc., signing a new three-year agreement that designates Hardie siding and trim as the exclusive products for Green Brick’s new developments through 2028.

- Strategic Focus: James Hardie’s strategy centers on converting vinyl siding market share to fiber cement through the ‘Grow the Addressable Market’ (GAM) initiative, targeting 20 million vinyl-sided US homes as fiber cement upgrade candidates.

LP Building Solutions

Louisiana-Pacific Corporation is headquartered in Nashville, Tennessee. LP Building Solutions is the company’s dedicated siding and trim division, manufacturing LP SmartSide engineered wood siding across its manufacturing plants in North and South America.

- Product Portfolio: LP SmartSide Lap Siding, LP SmartSide Trim & Fascia, LP SmartSide Strand Panel Siding, LP SmartSide Cedar Shakes, LP SmartSide Nickel Gap Siding.

- Recent Developments: In February 2024, LP Building Solutions launched its newest siding solution, LP SmartSide Nickel Gap Siding.

- Strategic Focus: LP’s SmartSide strategy targets the home market where natural wood aesthetics are desired, but fiber cement budgets are not available, positioning SmartSide as the ‘right-price premium alternative’ that delivers 85% of fiber cement’s aesthetic appeal at 70% of its total installed cost.

Etex Group SA

Etex Group SA, headquartered in Belgium, is a privately-held global building materials group. Etex operates two primary siding brands: Equitone (large-format fiber cement facade panels for commercial architecture) and Cedral (fiber cement lap siding for residential applications in Europe and Asia-Pacific).

- Product Portfolio: Equitone architectural fiber cement panels, Cedral lap siding

- Recent Developments: In December 2023, Etex signed an agreement with BGC to acquire its plasterboard and fibre cement businesses.

- Strategic Focus: Etex’s strategy positions Equitone as the architect’s premium large-format fiber cement panel brand in European commercial architecture, where specification decisions are made by design firms rather than contractors, while growing Cedral’s residential market share in Central/Eastern Europe through EPBD-compliant insulated siding innovation that addresses regulatory compliance and aesthetic upgrade demand simultaneously.

Nichiha Corporation

Nichiha Corporation, headquartered in Japan, is a leading manufacturer of fiber cement architectural panels for commercial and residential building applications.

- Product Portfolio: Nichiha Illumination Series, Nichiha Vintage Wood Series, Nichiha AWP panels, Nichiha Fiber Cement Lap Siding, and Nichiha ArtPanel.

- Recent Developments: In September 2025, Nichiha USA launched the industry’s first in-house two-piece metal trim system, designed to match a wide range of fiber cement textures and colors for a seamless finish through single-source supply .

- Strategic Focus: Nichiha’s US strategy targets the design-led commercial and premium multifamily segment where architect specification of distinctive facade aesthetics, rather than contractor familiarity or builder price preferences, drives material selection, creating a niche where Nichiha’s architectural panel design library and large-format installation speed advantage build sustainable differentiation from both James Hardie’s residential-focused product line and metal panel competitors.

Market Concentration Analysis

The global siding market exhibits moderate fragmentation overall but high concentration within specific material categories. James Hardie holds an estimated 80–85% of the North American fiber cement market and is the global fiber cement category leader with 14–18% of total global siding market revenue. The vinyl siding segment is more fragmented and 30+ regional manufacturers competing for the remainder. Regional manufacturers, particularly in China, India, Brazil, and Eastern Europe, collectively serve their domestic markets with cost-competitive products that represent the fragmented global revenue not captured by the top 5 players.

Consolidation has been significant in North America over the past decade. The Asia-Pacific segment, currently served by numerous small regional manufacturers, is expected to see consolidation as small companies expand production capacity to serve the rapidly growing ASEAN and Indian markets.

Investment & Growth Opportunities

Fastest-Growing Segments

Metal siding at ~4.6% CAGR is the highest-growth material segment, driven by commercial and data center construction. Data center construction growth globally creates premium demand for insulated metal panel systems. The insulated siding segment, growing at 5–6% above overall market rates, is creating premium pricing opportunities as IECC 2021 continuous insulation mandates expand across North American climatic zones. Investment in insulated siding manufacturing capacity is generating returns justified by regulatory-driven demand certainty through 2030.

Emerging Markets

India’s fiber cement siding market is the most underpenetrated high-growth opportunity globally. India’s 1.4 Billion population, with a rising urbanization trend, and PMAY housing mission collectively create a structural siding demand pipeline that domestic manufacturers are currently addressing primarily with low-cost cement board products. The first major global fiber cement brand to establish India-based manufacturing and a certified contractor network in India’s tier-1 and tier-2 cities will capture first-mover pricing advantages in a market.

Venture and Investment Trends

Private equity investment in regional siding distributors and specialty contractors is creating consolidation opportunities in the highly fragmented installation services channel. Building envelope systems integrators, companies bundling siding, insulation, air barrier, and window installation under a single contractor relationship, are attracting 8–12x EBITDA private equity valuations as the building performance market matures and building owners seek accountable single-source performance guarantors for their envelope investments.

Future Market Outlook (2026-2034)

The global siding market is positioned for sustained, construction-cycle-resilient growth through 2034, driven by the inelastic demand nature of exterior cladding as a mandatory building component. From USD 108.43 Billion in 2025, the market is forecast to reach USD 127.7 Billion by 2030 and USD 147.03 Billion by 2034, representing USD 38.6 Billion in absolute incremental value over the nine-year forecast horizon at a steady 3.32% CAGR.

Technological disruptions, including self-cleaning photocatalytic coatings that eliminate washing maintenance by 2028–2030, integrated photovoltaic siding (building-integrated PV) enabling siding panels to generate electricity, and smart sensor-embedded siding that monitors wall moisture and thermal performance in real time, are expected to redefine the siding product’s value proposition from passive exterior cladding to active building performance infrastructure.

Research Methodology

Primary Research

Primary research encompassed over 60 structured interviews in 2024–2025 with siding market participants, including VP-level product management, residential and commercial siding contractors and installers, national home builders procurement managers, building materials distributors, and building code officials specializing in IECC implementation.

Secondary Research

Key secondary sources include US Census Bureau New Residential Construction (2024), Harvard Joint Center for Housing Studies Improving America’s Housing (2024), NAHB Builder Practice Report – Siding Product Usage (2024), James Hardie Industries FY2024 Annual Report, Louisiana-Pacific Corporation FY2023 Annual Report, Remodeling Magazine 2024 Cost vs. Value Report, ASTM International fiber cement standards, and EU Energy Performance of Buildings Directive revised text.

Forecasting Models

IMARC’s Bottom-Up and Top-Down estimation models were applied in parallel. Bottom-Up aggregates siding demand by material category across new construction and repair and maintenance application channels in each regional market. Top-Down calibrates against global construction output growth projections, US housing start forecasts, and European housing renovation pipeline data.

Siding Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | Fiber Cement, Vinyl, Metal, Stucco, Concrete and Stone, Brick, Wood, Others |

| End Uses Covered |

|

| Applications Covered | New Construction, Repair and Maintenance |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | James Hardie Industries PLC, Cornerstone Building Brands, LP Building Solutions, Compagnie de Saint-Gobain S.A., Etex Group SA, Nichiha Corporation, SHERA Public Company, Kaycan Ltd. etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the siding market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global siding market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the siding industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Siding Market Report

The global siding market reached USD 108.43 Billion in 2025, growing from USD 92.1 Billion in 2020. Growth is driven by rising global construction activity, energy efficiency building codes, and US renovation market spending.

The market is projected to reach USD 147.03 Billion by 2034 at a CAGR of 3.32%, passing through USD 127.7 Billion in 2030. Net-zero building mandates, premiumization toward fiber cement, and Asia-Pacific urbanization are key drivers.

Fiber cement leads with 26.8% in 2025, driven by James Hardie’s HardiePlank dominance. It surpassed vinyl in premium residential specification, offering Class A fire rating, warranty, and color options through ColorPlus Technology.

Residential dominates at 64.5% in 2025, anchored by US 1.36M housing starts (2024) and renovation market growth. Siding replacement delivers 81.6-86.3% cost recoup at home sale, sustaining R&R spending.

North America leads at 34.6% in 2025, driven by US housing construction, a renovation market, and insulated siding mandates. James Hardie’s HardiePro certified contractors support premium fiber cement adoption.

Asia-Pacific at 22.4% (2025) is fastest-growing at ~4.4% CAGR. China’s 14th FYP targets urban housing units; India’s PMAY homes under construction; SHERA expanded ASEAN production in 2024.

Key players include James Hardie Industries PLC, Cornerstone Building Brands, LP Building Solutions, Compagnie de Saint-Gobain S.A., Etex Group SA, Nichiha Corporation, SHERA Public Company, and Kaycan Ltd.

Key drivers include global construction growth at 4.5% in 2024, US 1.36M housing starts, IECC 2021 insulated siding mandates, US renovation market, and EU EPBD zero-emission buildings mandate effective 2028.

IECC 2021 mandates continuous insulation in US climatic zones 4-8 (65% of US homes), driving insulated siding adoption. EnergyStar certified insulated siding reduces heating costs up to 20%. EU EPBD requires zero-emission new buildings from 2028, driving European renovation demand.

Fiber cement outperforms vinyl on fire resistance (Class A rating), termite immunity, moisture resistance, and aesthetic longevity. Vinyl offers lower upfront cost and zero maintenance.

Key challenges include PVC resin price volatility, Portland cement cost increases of 18-22% (2022-2023), EU CPR chemical substance restrictions on siding formulations, and 250,000+ unfilled US construction jobs creating installation labor shortages.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)