Silicon Fertilizer Market Size, Share, Trends and Forecast by Type, Form, Application, and Region, 2026-2034

Silicon Fertilizer Market Size, Share, Trends & Forecast (2026-2034)

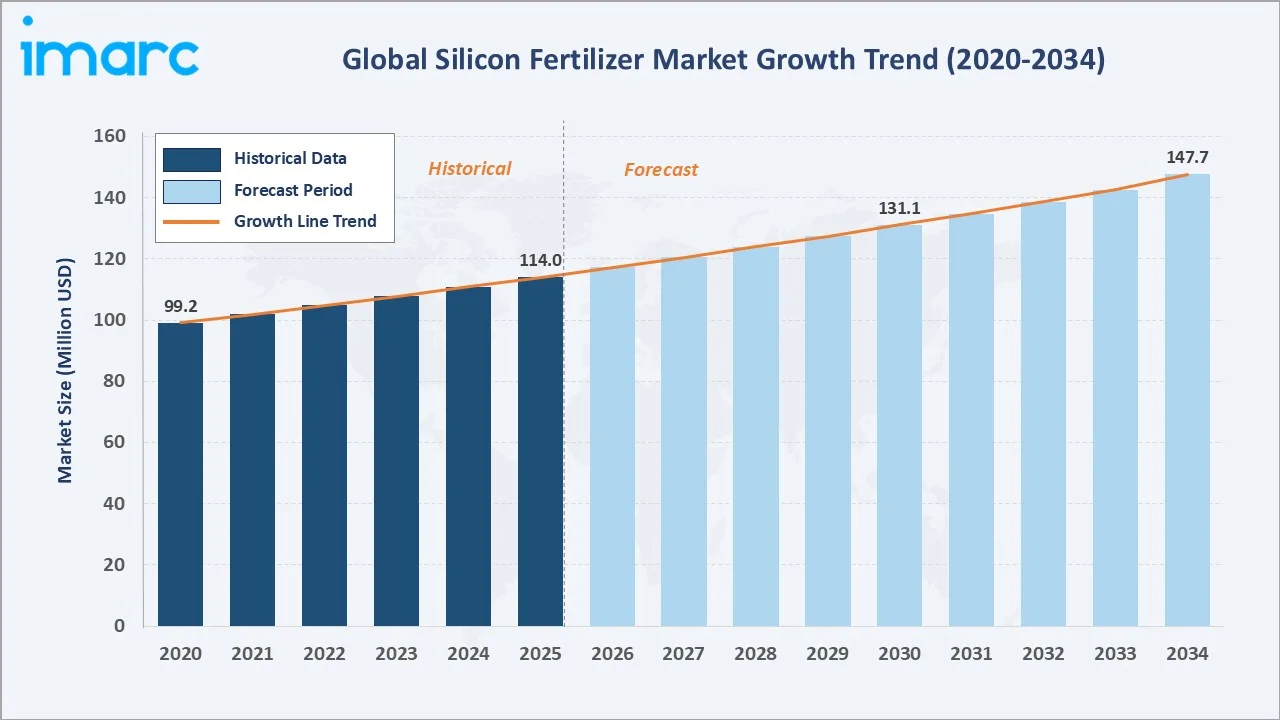

The global silicon fertilizer market reached USD 114.0 Million in 2025 and is projected to reach USD 147.7 Million by 2034, growing at a CAGR of 2.83% during 2026-2034. Market growth is driven by rising demand from silicon-accumulating crops such as rice, sugarcane, and wheat, growing recognition of silicon's role in mitigating abiotic and biotic crop stresses, soil degradation concerns, and expanding adoption of precision agriculture practices.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 114.0 Million |

| Forecast Market Size (2034) | USD 147.7 Million |

| CAGR (2026-2034) | 2.83% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

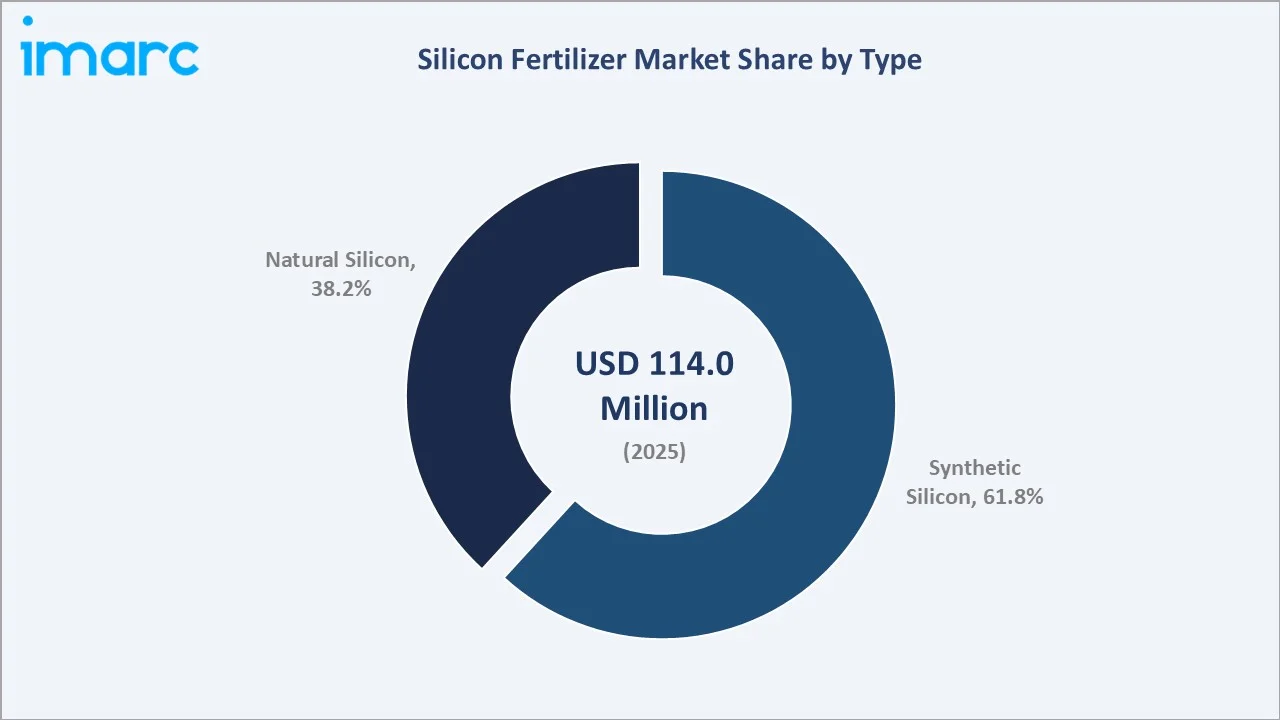

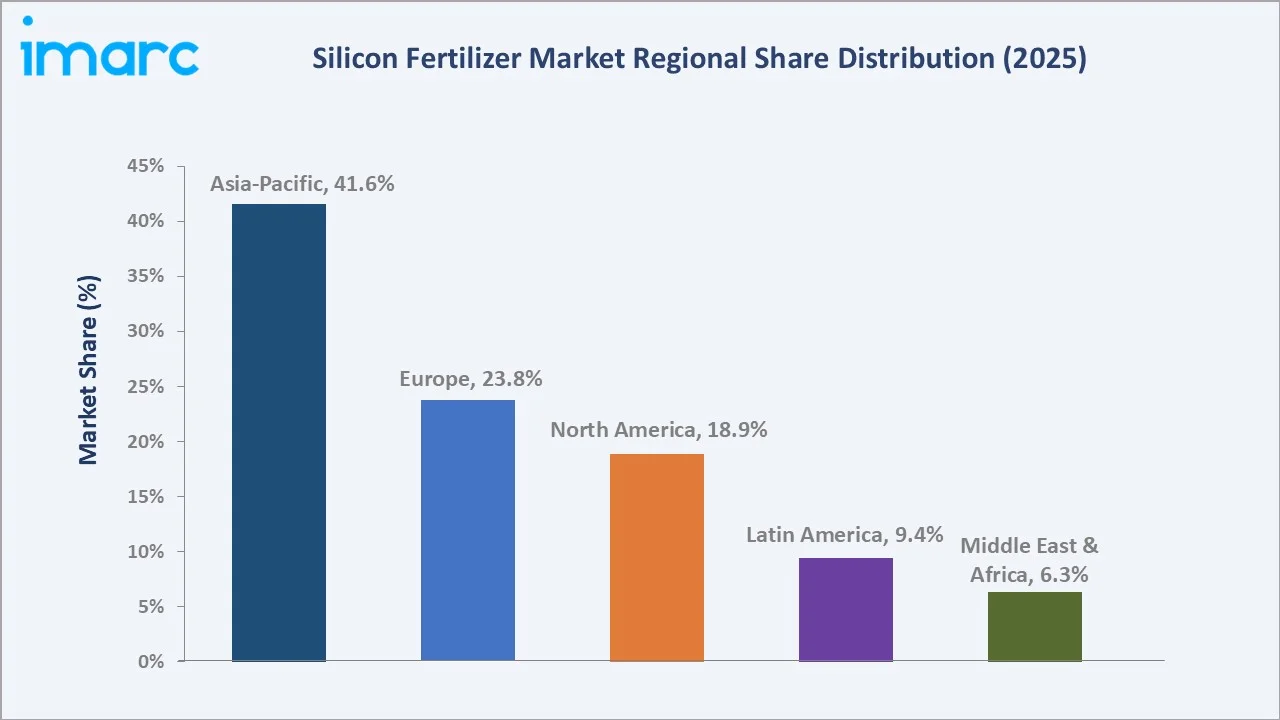

Asia-Pacific's 41.6% dominance reflects the region's concentration of rice paddy cultivation, the crop category most responsive to silicon fertilization, across China, Japan, South Korea, India, and Southeast Asia. Synthetic silicon fertilizers' 61.8% share reflects their consistent nutrient specification, water solubility control, and bioavailability standardization advantages over natural silica sources.

To get more information on this market, Request Sample

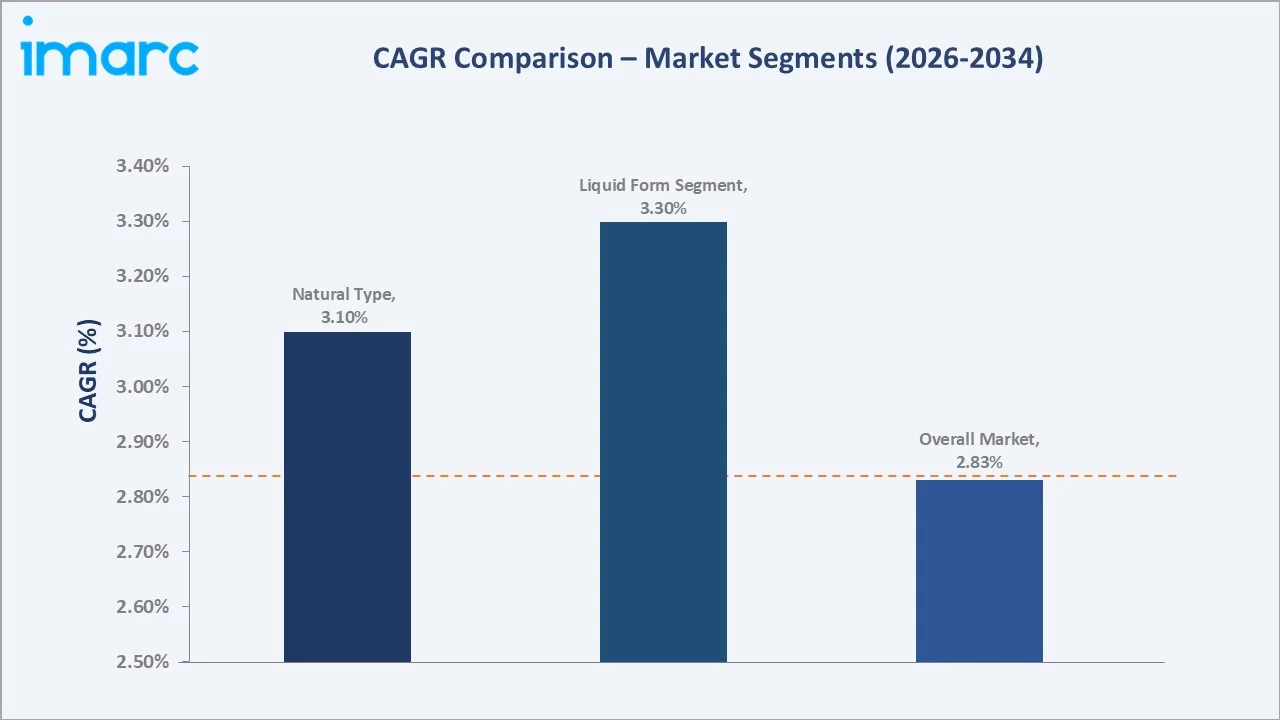

The market's 2.83% CAGR reflects steady adoption growth constrained by the niche status of silicon as a plant nutrient; it is not yet universally recognized as an essential element under most national agricultural extension systems, limiting the pace of mainstream farmer adoption beyond specialist rice, sugarcane, and horticultural grower segments where silicon's yield and quality benefits are best documented.

Executive Summary

The global silicon fertilizer market is on a gradual but accelerating growth trajectory as silicon's agronomic benefits gain mainstream recognition among farmers, agronomists, and agricultural policy makers. From USD 114.0 Million in 2025, the market will reach USD 147.7 Million by 2034, generating USD 33.7 Million in incremental value at a 2.83% CAGR.

Synthetic silicon fertilizers lead at 61.8% in 2025, with calcium silicate being the most widely applied synthetic form across rice paddy and sugarcane applications. Natural silicon fertilizers at 38.2%, including diatomite, rice husk ash, and amorphous silica from volcanic deposits, are growing in organic farming and sustainability-certified agricultural programs.

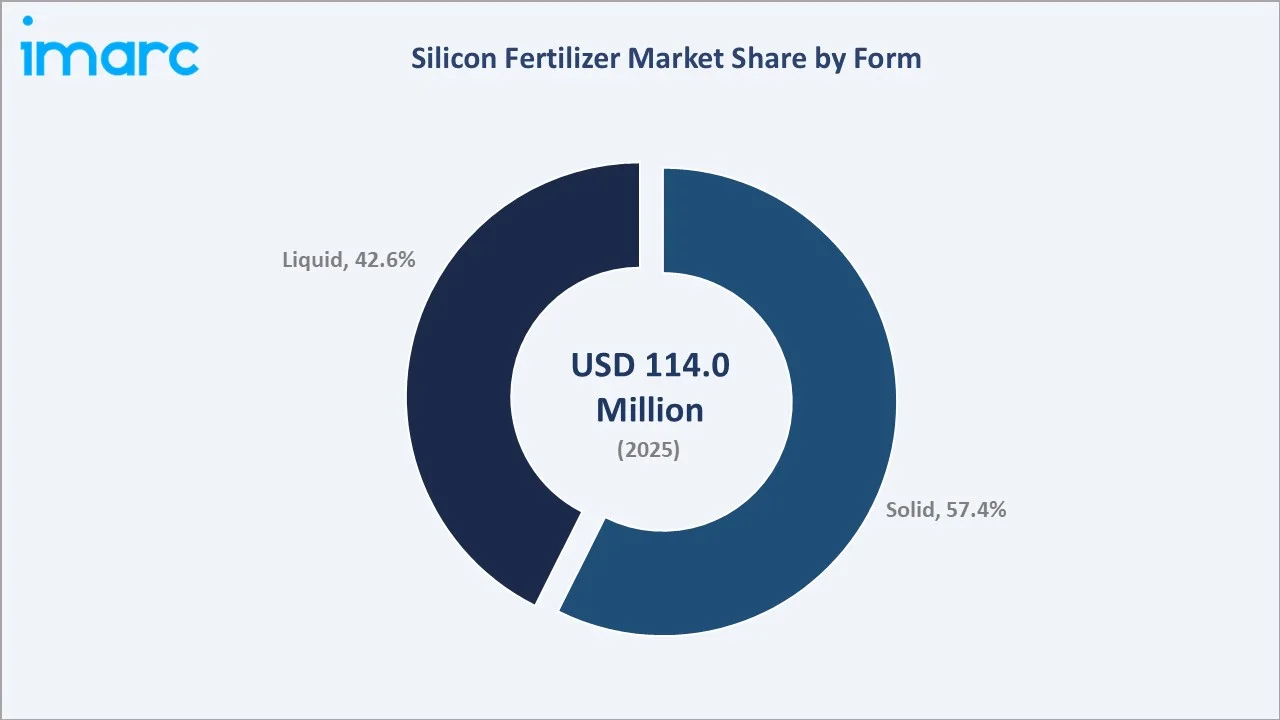

Solid form products dominate at 57.4%, while liquid silicon fertilizers at 42.6% are growing fastest, driven by fertigation and foliar application adoption in horticultural and precision farming systems. Key players, including Denka Company Limited, Agripower Australia Ltd, MaxSil Pty Ltd., and Edw. C. Levy Co., compete through product bioavailability, application form versatility, and crop-specific formulation expertise.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Type Segment | Synthetic – 61.8% share (2025) |

| Fastest Growing Type | Natural – ~3.10% CAGR (organic farming & sustainability demand) |

| Largest Form Segment | Solid – 57.4% share (2025) |

| Fastest Growing Form | Liquid – ~3.30% CAGR (fertigation and foliar application growth) |

| Leading Region | Asia-Pacific – 41.6% share (2025) |

| Top Companies | Denka Company Limited, Agripower Australia Ltd, MaxSil Pty Ltd., and Edw. C. Levy Co. |

Key Analytical Observations:

- Synthetic silicon fertilizers at 61.8% dominate due to their consistent nutrient specification, calcium silicate (CaSiO3) granules, and potassium silicate liquids, which provide defined silicon content that enables accurate application rate calculation.

- Natural silicon fertilizers at 38.2% (2025) include diatomite, rice husk ash, volcanic rock dusts, and naturally occurring silica sands. These products are valued for their OMRI-listed and certification-compatible status, where cost-competitive silicon sources from agricultural by-products provide an accessible supply for smallholder farmers.

- Solid form products at 57.4% (2025) dominate through granular and powder formulations applied via broadcast spreading or incorporation into irrigation channels in paddy rice systems. Powder forms are used in hydroponics and substrate growing media, where silicon pre-blending with growing mix is the application method.

- Liquid silicon fertilizers at 42.6% (2025) are growing fastest at approximately 3.30% CAGR, driven by adoption in modern greenhouse horticulture, precision fertigation systems, and foliar application programs for high-value vegetable and fruit crops.

Silicon Fertilizer Market Overview

Silicon fertilizers are products that supply plant-available silicon to crops through soil or foliar application, improving crop growth, yield, quality, and resistance to biotic and abiotic stresses. Silicon is classified as a "beneficial element" by the International Plant Nutrition Institute (before its programs were wound down and assets transferred in 2019) rather than an essential nutrient.

The silicon fertilizer market distinguishes itself from macronutrient fertilizers (NPK) through its relatively small volume requirements, premium pricing per ton, and the niche agronomic expertise required for effective sales and agronomic advisory support. The market is characterized by a strong technical selling environment where field demonstration data, peer-reviewed crop response research, and agronomist relationships are critical to commercial adoption.

Market Dynamics

To evaluate market opportunities, Request Sample

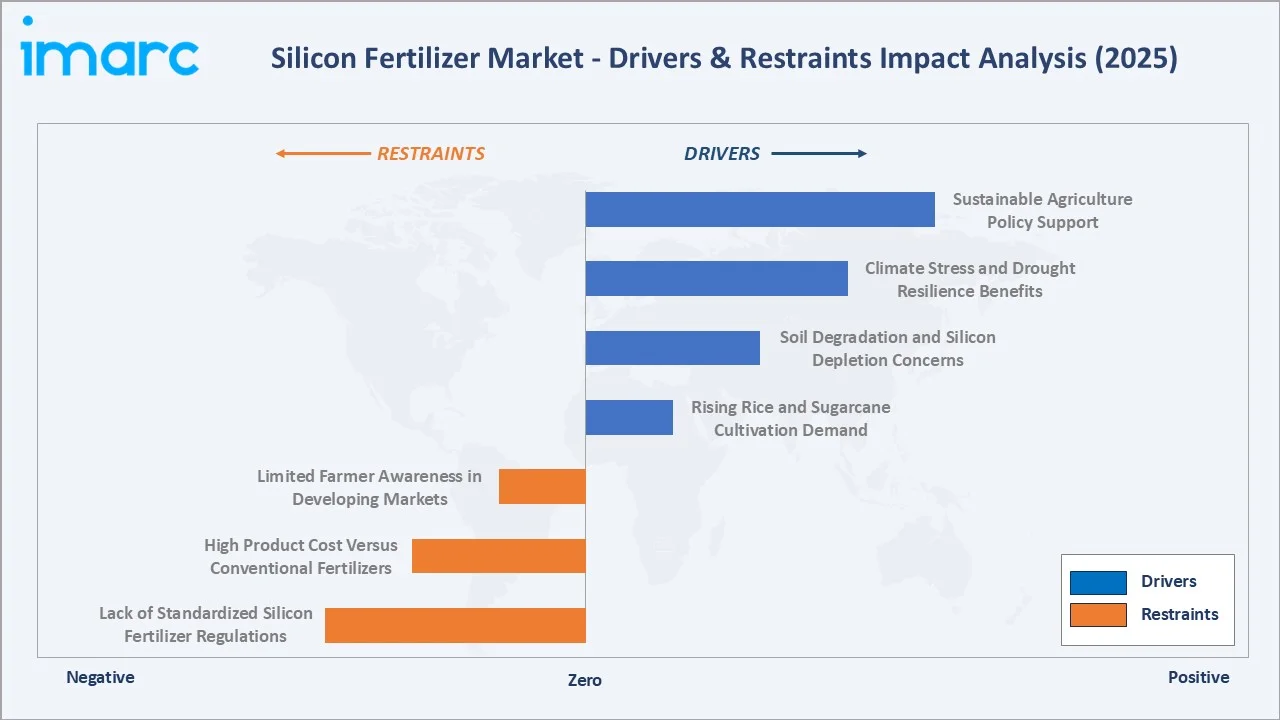

Market Drivers

- Rising Rice and Sugarcane Cultivation Demand: Rice and sugarcane are the two highest silicon-accumulating crop species and collectively represent the primary demand driver for silicon fertilizers. Global rice paddy cultivation covers approximately 165 million hectares, with silicon depletion occurring at rates of 100–200 kg SiO2 per hectare per crop cycle as harvested grain removes silicon from the soil system.

- Soil Degradation and Silicon Depletion Concerns: Continuous intensive cropping removes silicon from soil systems faster than natural weathering replenishes it. Studies across Asian rice-producing regions indicate that silicon availability in intensively farmed paddy soils has declined 20–40% over the past 50 years of continuous cultivation.

- Climate Stress and Drought Resilience Benefits: Silicon is deposited in plant epidermal cells, improving structural rigidity, reducing water loss through transpiration, and increasing tolerance of heat stress, drought, and waterlogging, all increasing in frequency due to climate change.

- Sustainable Agriculture Policy Support: Multiple national governments, including Japan, South Korea, Taiwan, China, and increasingly India and Brazil, provide subsidies, extension support, or mandated minimum application requirements for silicon fertilizers in rice cultivation.

Market Restraints

- Limited Farmer Awareness in Developing Markets: Despite growing research evidence, silicon fertilizers remain unfamiliar to the majority of smallholder farmers across South and Southeast Asia, Sub-Saharan Africa, and Latin America.

- High Product Cost Versus Conventional Fertilizers: Soluble silicon fertilizers, particularly potassium silicate liquid products, command prices of USD 1,500–3,000 per ton, significantly higher than calcium silicate slag at USD 80–200 per ton or standard NPK fertilizers.

- Lack of Standardized Silicon Fertilizer Regulations: In many markets, silicon fertilizers do not have a defined regulatory category separate from soil amendments or lime products, creating labelling, registration, and market access complexity. The absence of internationally harmonized standards for silicon fertilizer product specification limits consumer confidence and creates trade barriers for cross-border product movement.

Market Opportunities

- Slow-Release and Controlled-Release Silicon Formulations: New polymer-coated silicon fertilizer granules and zeolite-matrix silicon products enable extended silicon release over crop growth periods, improving silicon use efficiency and reducing application frequency.

- Biostimulant and Silicon Combination Products: The combination of silicon with biostimulants and with micronutrients creates multi-functional crop enhancement products that broaden the value proposition beyond silicon nutrition alone.

Market Challenges

- Agronomic Complexity of Silicon Fertilizer Recommendations: Optimal silicon fertilizer application rate depends on soil pH, clay mineral composition, organic matter content, plant silicon uptake capacity, and existing soil silicon reserves, factors that vary significantly across field conditions.

- Competition from Natural Silicon Sources and Industrial By-Products: In regions with silicon-rich parent rock geology, natural soil silicon levels may be adequate without supplementation. Additionally, industrial by-products from steel slag and phosphoric acid production provide low-cost calcium silicate that competes with commercial silicon fertilizer products.

Emerging Market Trends

1. Nano-Silicon Fertilizer Technology Development

Nano-silicon fertilizers, colloidal silicon nanoparticles in the 20–200 nm size range, are demonstrating significantly enhanced silicon uptake efficiency versus conventional silicic acid forms in controlled studies. Silicon nanoparticles can penetrate plant cell walls directly, delivering silicon to intracellular locations inaccessible to conventional silicate ions.

2. Silicon-Based Fertilizer for Enhanced Crop Growth

Godrej Agrovet’s Agrisilica is a granular, silicon-based fertilizer categorized under fertilizers and organic manures, designed to provide plant-available silicon. The product is suitable for crops including sugarcane, grapes, banana, tomato, chilli, maize, onion, pomegranate, potato, and other vegetables.

3. Silicon Fertilizer Inclusion in Integrated Soil Health Programs

National soil health improvement programs in India, China, and Brazil are increasingly incorporating silicon management into their soil health assessment and improvement frameworks. India's ICAR and state agricultural universities have published updated rice and sugarcane fertilizer management recommendations that include silicon as a beneficial element, creating institutional demand and extending service-driven adoption channels.

4. Water-Soluble Silicon Fertigation System Integration

Potassium silicate and monosilicic acid liquid silicon fertilizers are gaining adoption in modern drip irrigation and fertigation systems across greenhouse vegetable and berry production. The integration of liquid silicon into automated fertigation injection programs enables precise ppm-level silicon delivery with minimal labor, creating a scalable adoption pathway for premium horticultural growers seeking to improve disease resistance, fruit quality, and shelf life without adding manual application steps.

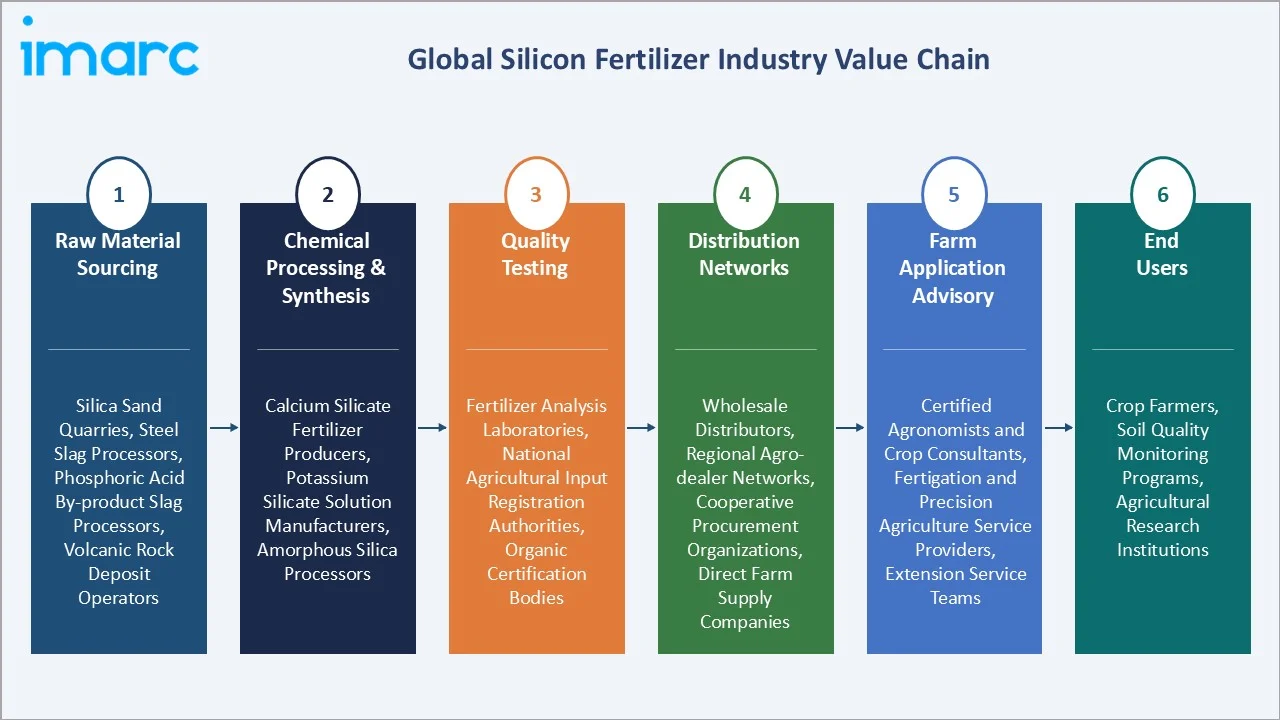

Industry Value Chain Analysis

The silicon fertilizer value chain spans raw material sourcing through chemical processing, quality certification, distribution, and farm application, with each stage requiring technical expertise in silicon chemistry and crop agronomy.

| Stage | Key Players / Examples |

|---|---|

| Raw Material Sourcing | Silica sand quarries, steel slag processors, phosphoric acid by-product slag processors, volcanic rock deposit operators |

| Chemical Processing & Synthesis | Calcium silicate fertilizer producers, potassium silicate solution manufacturers, amorphous silica processors |

| Quality Testing | Fertilizer analysis laboratories, national agricultural input registration authorities, organic certification bodies |

| Distribution Networks | Wholesale distributors, regional agro-dealer networks, cooperative procurement organizations, direct farm supply companies |

| Farm Application Advisory | Certified agronomists and crop consultants, fertigation and precision agriculture service providers, extension service teams |

| End Users | Crop farmers, soil quality monitoring programs, agricultural research institutions |

Technology Landscape in the Silicon Fertilizer Industry

Calcium Silicate Technology

Calcium silicate is the dominant synthetic silicon fertilizer globally, produced from steel slag or direct silica-calcium carbonate synthesis. Denka's calcium silicate line for Japanese rice cultivation represents the industry benchmark for consistent silicon content specification.

Potassium Silicate Technology

Potassium silicate solutions manufactured through high-temperature fusion of silica with potassium carbonate are the primary liquid silicon fertilizer. At 25–35% SiO2 concentration, they are diluted for fertigation or foliar application. Their water solubility and fertigation compatibility make them the preferred silicon source for greenhouse horticulture.

Bioavailability Enhancement Technology

Stabilized orthosilicic acid (OSA), the monomeric, directly plant-available silicon form, is maintained in non-condensed form using propylene glycol or humic acid carriers, delivering silicon at just 1–5 kg Si/ha versus 100–500 kg for conventional products.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Synthetic | 61.8% | 2025 |

| Form | Solid | 57.4% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Region | Asia-Pacific | 41.6% | 2025 |

By Type

Synthetic silicon fertilizers lead at 61.8% in 2025. Their dominance reflects the established industrial infrastructure for calcium silicate slag production as a by-product of steel and phosphoric acid manufacturing, providing cost-competitive silicon supply at scale. Japan's institutionalized calcium silicate application program for rice represents the world's most established silicon fertilizer market, underpinning synthetic silicon's volume leadership.

To access detailed market analysis, Request Sample

Natural silicon fertilizers at 38.2% serve the organic and biostimulant-adjacent market segments where OMRI-certified natural silicon sources are mandated. Diatomite, rice husk ash, and amorphous volcanic silica products from Agripower and similar suppliers are growing as sustainable agriculture programs create structured demand for non-synthetic soil health inputs.

By Form

Solid form products lead at 57.4% in 2025, dominated by granular calcium silicate applied to rice paddies and sugarcane fields at high rates. Powder forms serve hydroponics and growing media applications. The solid segment's leadership reflects the dominance of rice paddy silicon fertilization, where broadcast granular application is the standard agronomic practice.

Liquid silicon fertilizers at 42.6% are growing fastest (~3.30% CAGR), driven by fertigation adoption in modern greenhouses and the growth of high-value horticultural markets where liquid silicon enables precision delivery at low application rates. Liquid products are progressively capturing market share from solid forms in markets where modern irrigation infrastructure enables fertigation-based crop nutrition.

Regional Market Insights

Asia-Pacific leads the global silicon fertilizer market with a 41.6% share in 2025. Japan, South Korea, Taiwan, and China collectively account for the region's dominance through their extensive rice cultivation and institutionalized silicon fertilizer application programs. Japan represents the world's most mature silicon fertilizer market, with Denka's calcium silicate product dominating government-subsidized paddy rice application programs.

Europe's 23.8% share reflects the continent's sophisticated horticulture sector, particularly the Netherlands' world-leading greenhouse industry, where liquid potassium silicate is incorporated as a standard component of fertigation nutrient programs for tomato, cucumber, and pepper crops.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| Asia-Pacific | 41.6% | Institutionalized calcium silicate rice programs, China's expanding silicon fertilizer awareness, India's growing rice silicon deficit, Southeast Asia's increasing crop productivity focus |

| Europe | 23.8% | Premium horticultural crop adoption, EU sustainable agriculture policy support, growing organic silicon fertilizer demand, climate stress mitigation applications |

| North America | 18.9% | US sugarcane silicon fertilization, greenhouse horticulture liquid silicon adoption, growing specialty crop silicon response research, regulated organic market demand |

| Latin America | 9.4% | Brazil's large sugarcane sector, expanding awareness, growing research on silicon benefits for tropical crop stress management |

| Middle East & Africa | 6.3% | Water stress management in greenhouse horticulture, rice cultivation silicon programs, growing awareness of silicon's drought resilience benefits |

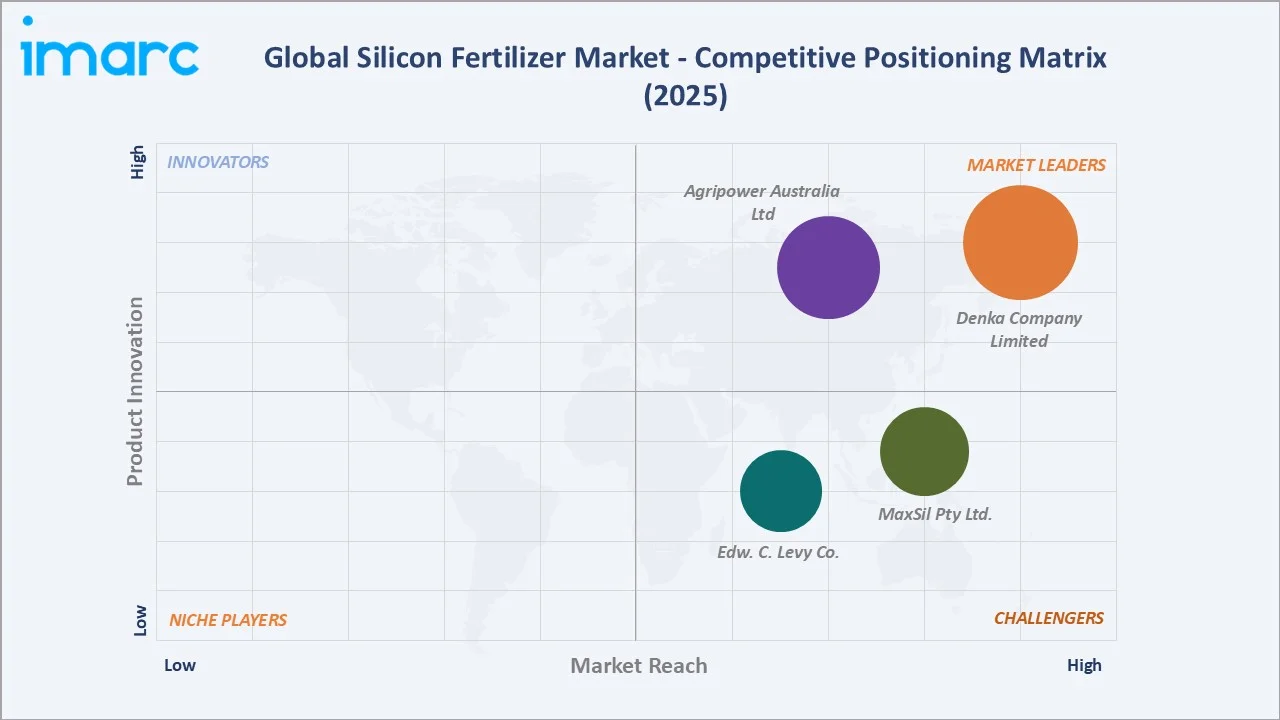

Competitive Landscape

The silicon fertilizer market is fragmented, with no single global player dominating across all geographies and product categories. Denka Company Limited leads in the Japanese and Asian calcium silicate market, while Agripower Australia Ltd and MaxSil Pty Ltd. compete in the Asia-Pacific and Australian premium silicon segment.

| Company | Brand / Division | Market Position | Key Strength |

|---|---|---|---|

| Denka Company Limited | Denka | Market Leader | Calcium silicate rice fertilizer leadership, government program supply, high-purity slag processing, established distribution network |

| Agripower Australia Ltd | Agrisilica | Market Leader | Amorphous silica soil conditioner, low-processing-energy natural silicon source, cost-competitive natural product |

| MaxSil Pty Ltd. | MaxSil | Strong Challenger | Offers granules and powder form of silicon fertilizer, horticultural market focus, export market supply, turf & specialty crop expertise |

| Edw. C. Levy Co. | Plant Tuff | Challenger | Offers a unique three-in-one silicon fertilizer that delivers silicon and micronutrients while helping regulate soil pH |

Edw. C. Levy Co. serves the high-bioavailability potassium silicate and OSA market niches globally from its technology platform.

Key Company Profiles

Denka Company Limited

Denka Company Limited is the global market leader in calcium silicate fertilizers for rice cultivation. The company supplies the majority of Japan's government-program calcium silicate rice fertilizer.

- Product Portfolio: Fused silicic acid phosphate fertilizer for high-quality rice cultivation.

- Recent Developments: In May 2026, Denka Company Limited reported FY2025 net sales of JPY 384.2 billion, down 4.0% year-on-year, while operating profit rose 82.0% to JPY 26.2 billion. For FY2026, the company forecasts net sales of JPY 450.0 billion and operating profit of JPY 30.0 billion.

- Strategic Focus: Calcium silicate rice fertilizer global market leadership, supply reliability for Japanese government procurement programs, and new formulation development for improved silicon bioavailability in challenging soil conditions.

Agripower Australia Ltd

Agripower Australia Ltd is a leading natural silicon fertilizer producer and innovator specializing in amorphous silica products derived from naturally occurring volcanic silica deposits.

- Product Portfolio: Agrisilica granules, agrisilica chip, agrisilica liquid, and agrisilica powder.

- Strategic Focus: Asian rice and sugarcane market expansion, natural and organic market positioning, low-carbon silicon source differentiation, and agronomic trial program development for Asian market customer adoption.

Market Concentration Analysis

The silicon fertilizer market is moderately fragmented. Denka Company Limited and Agripower Australia Ltd collectively represent an estimated 25–30% of global revenue, with no single company holding dominant market power across all product categories and geographies.

The market bifurcates between the high-volume, low-margin calcium silicate slag segment (dominated by Japanese and Korean industrial by-product producers) and the premium-priced, lower-volume potassium silicate and OSA product categories.

Investment & Growth Opportunities

Fastest Growing Segments

Liquid silicon fertilizers (~3.30% CAGR), nano-silicon formulations (~8% commercial development CAGR), natural silicon for organic markets, and silicon biostimulant combination products represent the highest-growth investment vectors through 2034, collectively targeting a combined incremental market of approximately USD 20 Million by 2034.

Emerging Market Expansion

India's 44 million hectare rice cultivation area represents the largest untapped silicon fertilizer market globally. ICAR field research has confirmed widespread silicon deficiency across Indian paddy soils, particularly in continuously cultivated Kharif rice states. Government inclusion of silicon in the Soil Health Card program recommendations would create a transformative market development catalyst.

Venture and Institutional Investment Trends

- AgTech venture capital investment in silicon fertilizer startups, focusing on nano-silicon formulations, stabilized orthosilicic acid platforms, and biostimulant-silicon combinations, is growing, with companies in India, China, and Europe attracting seed and Series A funding for novel silicon delivery technology development.

- Steel industry investment in slag valorization programs, converting basic oxygen furnace and electric arc furnace slags into certified fertilizer-grade calcium silicate products, is creating new supply pipelines and market development investment from steel companies seeking to monetize by-product streams.

Future Market Outlook (2026-2034)

The global silicon fertilizer market will reach USD 147.7 Million by 2034 from USD 114.0 Million in 2025, adding USD 33.7 Million at a 2.83% CAGR. The outlook will be shaped by India's potential transition from awareness to adoption in rice silicon fertilization, the ongoing premium horticulture liquid silicon market expansion in Europe and North America, and accelerating nano-silicon commercial development.

Liquid silicon fertilizers will gradually gain market share from solid forms as precision irrigation infrastructure expands and fertigation adoption grows across Asia-Pacific and Latin America. Natural silicon fertilizers will grow their share within the broader silicon fertilizer market as organic and sustainability-certified agricultural programs expand globally.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 70 industry participants in 2024–2025, including silicon fertilizer manufacturers, agri-input distributors, agronomists, crop research institutes, and farmers across Asia-Pacific, Europe, and North America. Expert input validated market sizing, product adoption trends, and regional development dynamics.

Secondary Research

Secondary research encompassed manufacturer annual reports, FAO fertilizer statistics, ICAR and national agricultural research institute publications, peer-reviewed crop response research, and trade publications including Fertilizer Focus, International Fertilizer Association reports, and CropLife.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting, incorporating global silicon-accumulating crop area, silicon depletion rates, adoption penetration assumptions by crop type and region, average silicon fertilizer product price trajectories, and government program procurement data.

Silicon Fertilizer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Synthetic, Natural |

| Forms Covered | Liquid, Solid |

| Applications Covered | Field Crops, Horticultural Crops, Hydroponics, Floriculture |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Denka Company Limited, Agripower Australia Ltd, MaxSil Pty Ltd., Edw. C. Levy Co., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Silicon Fertilizer Market Report

The market reached USD 114.0 Million in 2025 and is projected to reach USD 147.7 Million by 2034 at a 2.83% CAGR.

Asia-Pacific leads with a 41.6% share in 2025, anchored by Japan's institutionalized calcium silicate rice programs, South Korea, China, and India's large rice cultivation area.

Synthetic silicon fertilizers lead at 61.8% in 2025, primarily calcium silicate slag products applied to rice paddies and sugarcane fields at scale.

Solid form products lead at 57.4% in 2025, dominated by granular calcium silicate applied to rice paddies at rates of 1–3 tons per hectare.

Denka Company Limited, Agripower Australia Ltd, MaxSil Pty Ltd., and Edw. C. Levy Co. are some of the leading players in the market.

Rising rice and sugarcane cultivation demand, soil silicon depletion, climate stress resilience benefits, and sustainable agriculture policy support are primary drivers.

Limited farmer awareness, high product cost versus conventional fertilizers, lack of standardized regulations, and competition from natural silicon sources are key challenges.

Liquid silicon fertilizers are growing fastest at approximately 3.30% CAGR, driven by fertigation adoption in modern greenhouse horticulture and precision farming.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)