Singapore E-commerce Market Size, Share, Trends and Forecast by Type, Transaction, and Region, 2026-2034

Singapore E-commerce Market Size, Share, Trends & Forecast (2026-2034)

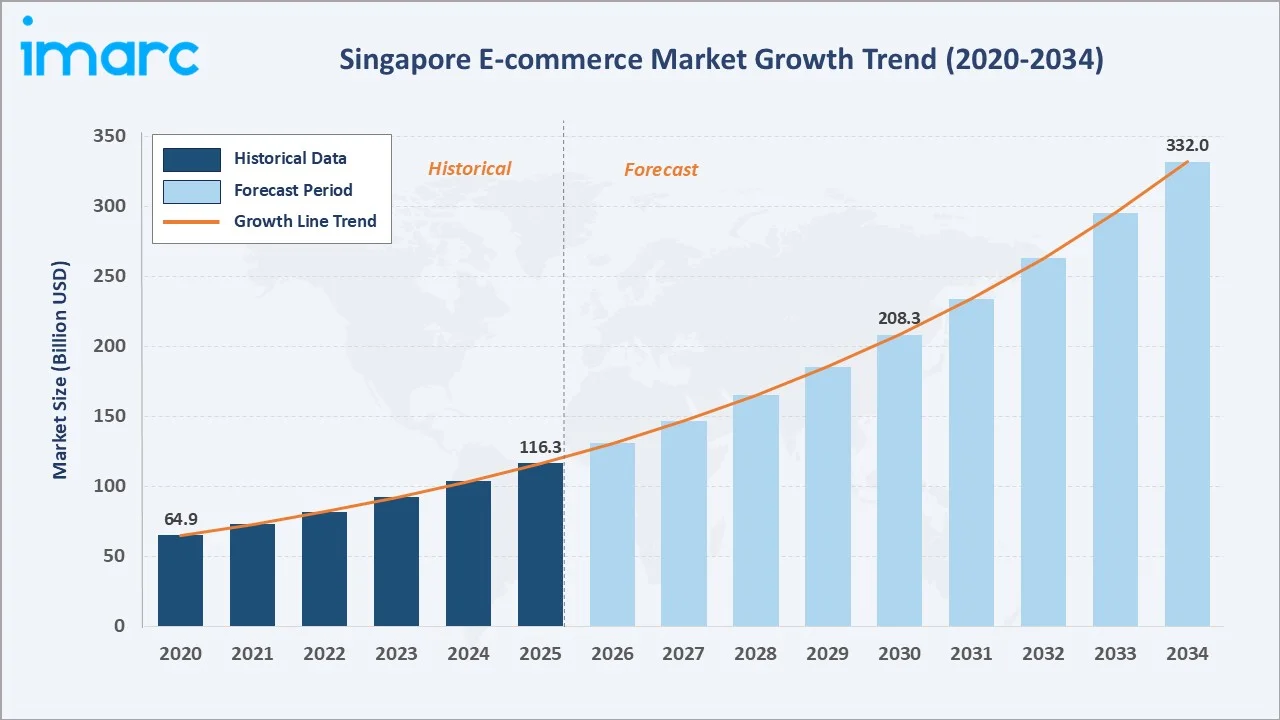

The Singapore e-commerce market size reached USD 116.3 Billion in 2025 and is projected to reach USD 332.0 Billion by 2034, exhibiting a CAGR of 12.36% during 2026-2034. High internet penetration, rapid smartphone adoption, and advanced logistics infrastructure are primary drivers of Singapore e-commerce market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 116.3 Billion |

|

Forecast Market Size (2034) |

USD 332.0 Billion |

|

CAGR (2026-2034) |

12.36% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

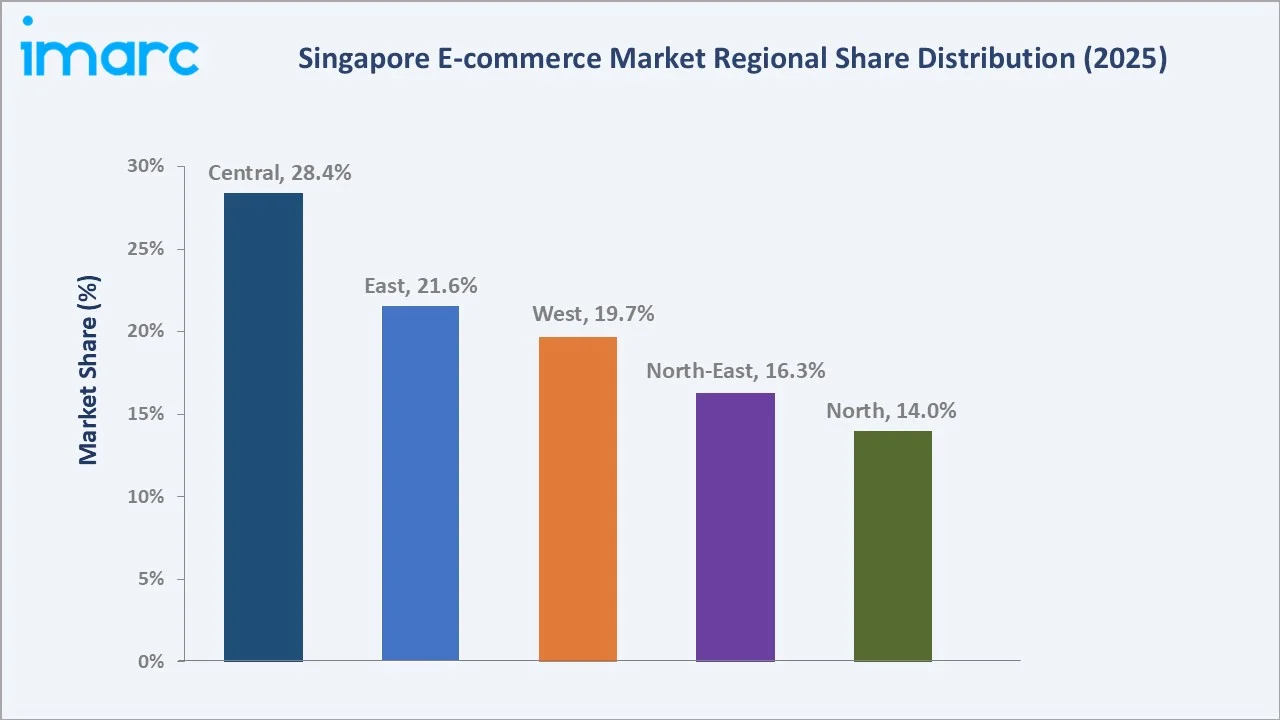

Central (28.4% share, 2025) |

|

Fastest Growing Region |

North-East (CAGR ~13.5%) |

|

Leading Type |

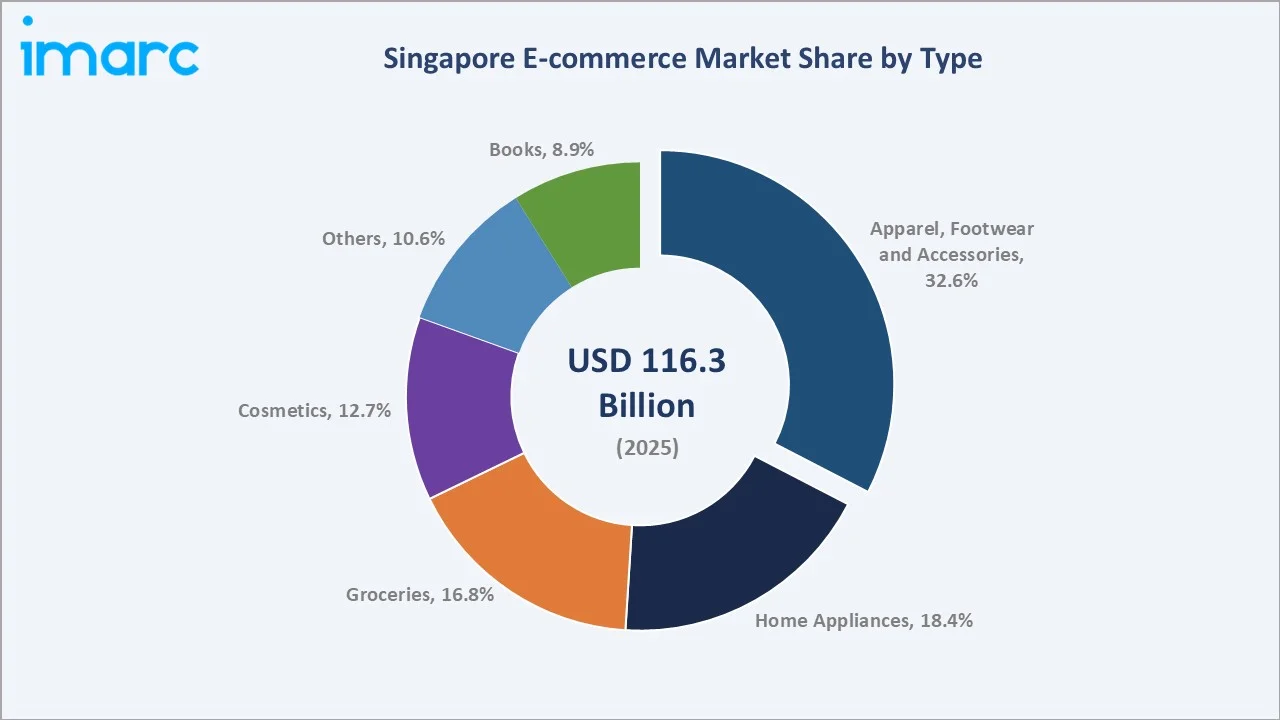

Apparel, Footwear and Accessories (32.6%, 2025) |

|

Leading Transaction |

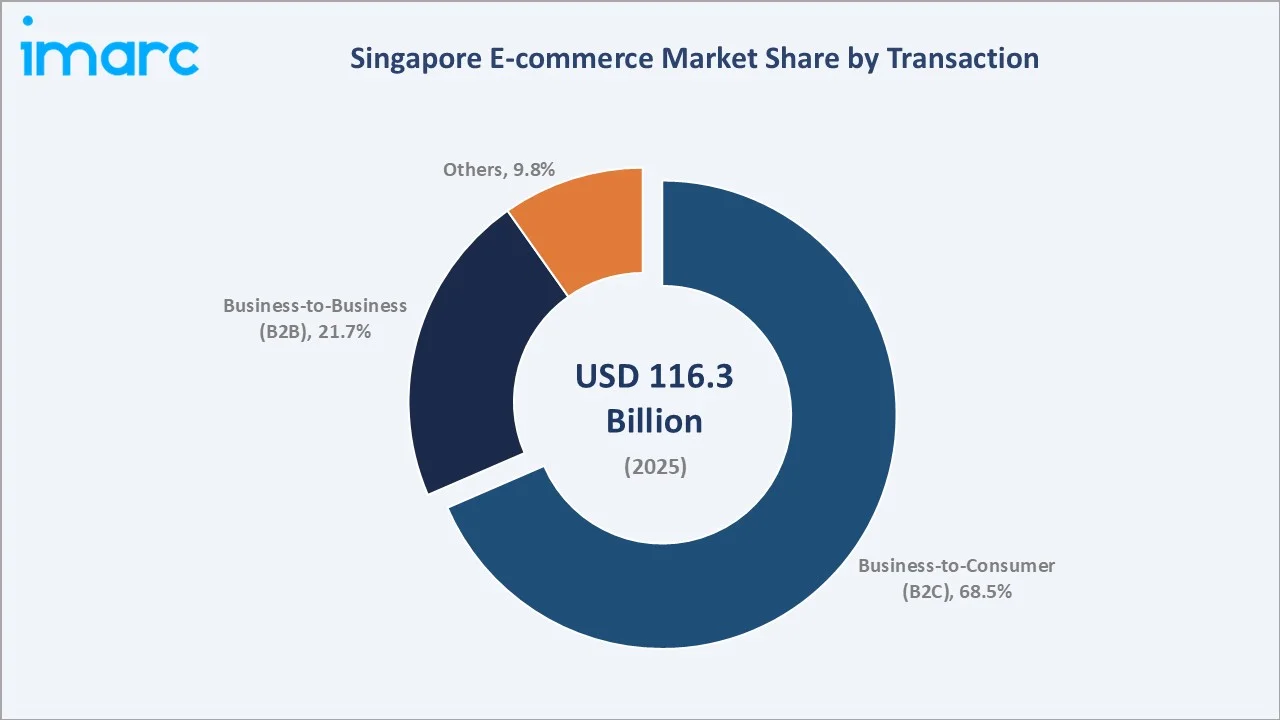

Business-to-Consumer (68.5%, 2025) |

The chart below illustrates the Singapore e-commerce market growth trajectory from 2020 through 2034. It contrasts historical expansion against the sustained forecast curve powered by digital adoption, mobile commerce penetration, and cross-border trade expansion across Southeast Asian and global markets.

To get more information on this market, Request Sample

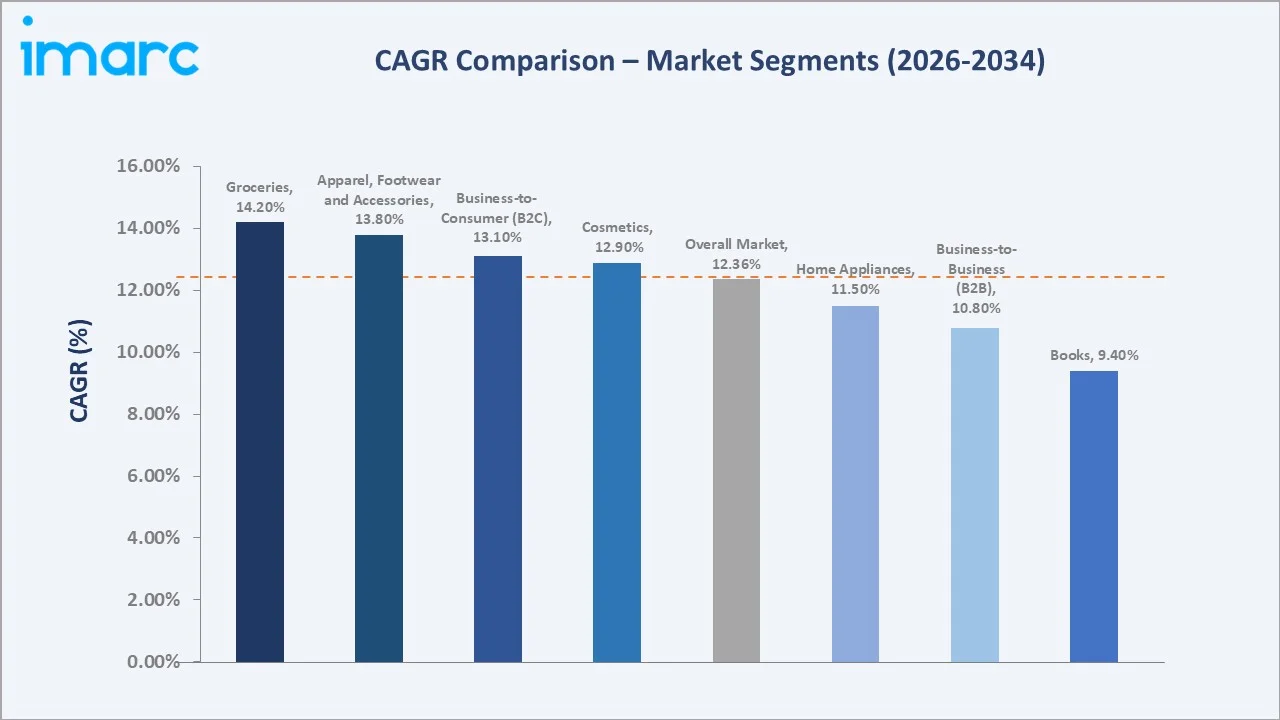

Segment-level CAGR comparisons highlight the Groceries sub-segment and Apparel as the fastest-growing categories within the Singapore e-commerce market forecast through 2034.

Executive Summary

The Singapore e-commerce market is undergoing a powerful structural transformation. It is propelled by near-universal internet connectivity, rising consumer confidence in digital transactions, and a government-backed Smart Nation initiative that continues to accelerate digital commerce adoption. Valued at USD 116.3 Billion in 2025, the market is forecast to reach USD 332.0 Billion by 2034 at a CAGR of 12.36%. Singapore's strategically positioned role as a regional trade hub amplifies its influence across Southeast Asian e-commerce corridors.

Apparel, Footwear, and Accessories commands a 32.6% share in 2025, anchored by youth-driven fashion consumption and the rapid growth of social commerce platforms. The Groceries sub-segment is the fastest-growing type, driven by post-pandemic behavioral shifts toward online food procurement. B2C transactions account for 68.5% of total market volume, while B2B e-commerce is expanding steadily at approximately 10.8% CAGR, fueled by SME digital procurement adoption.

The Central region leads with a 28.4% geographic revenue share, supported by Singapore's dense population centers and business districts. The Singapore e-commerce market outlook remains strongly positive as mobile wallet penetration, AI-driven personalization, and live commerce formats continue to reshape consumer engagement and purchasing patterns through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Apparel, Footwear and Accessories – 32.6% share (2025) |

|

Second Type Segment |

Home Appliances – 18.4% share (2025) |

|

Largest Transaction Mode |

B2C – 68.5% share (2025) |

|

Fastest Growing Transaction |

B2B – ~10.8% CAGR (2026-2034) |

|

Leading Region |

Central – 28.4% revenue share (2025) |

|

Top Companies |

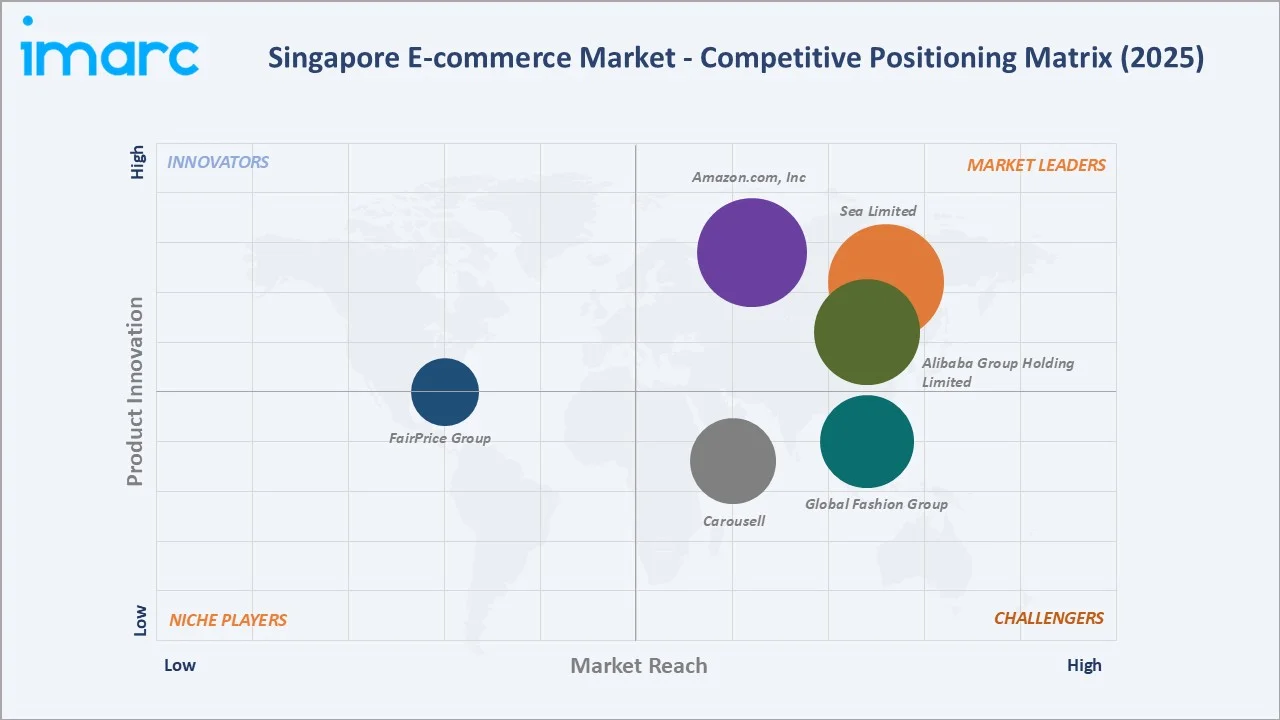

Sea Limited, Alibaba Group Holding Limited, Amazon.com, Inc, Global Fashion Group, Carousell, FairPrice Group |

|

Market Opportunity |

Cross-border e-commerce and live commerce expansion |

Key Analytical Observations Supporting the Above Data:

- Apparel's 32.6% dominance in 2025 reflects Singapore's fashion-forward consumer culture, high smartphone penetration at 89%, and the surge of social media commerce platforms such as TikTok Shop and Instagram Shopping.

- Home Appliances' 18.4% share is driven by rising renovation activity, increasing dual-income household formation, and the replacement cycle accelerated by post-COVID home improvement trends in Singapore.

- B2C's commanding 68.5% majority is underpinned by Singapore's 5.78 million internet users (2025) and one of Asia's highest per-capita digital payment adoption rates.

- The Central region's 28.4% dominance reflects the concentration of high-income households, corporate offices driving B2B procurement, and the dense logistics infrastructure of Singapore's central districts.

- Groceries is the fastest-growing type at approximately 14.2% CAGR through 2034, driven by services like RedMart, and FairPrice Online capturing the post-pandemic shift to online food procurement.

Singapore E-commerce Market Overview

E-commerce in Singapore encompasses digital retail, marketplace platforms, and B2B procurement channels operating through internet-enabled platforms. The market spans product categories from fashion and electronics to groceries and financial services. Key ecosystem participants include marketplace platforms, payment gateways, logistics providers, and technology enablers.

The industry operates at the convergence of high consumer digital literacy, world-class logistics infrastructure, and a regulatory framework that balances innovation with consumer protection. Macroeconomic influences include Singapore's role as ASEAN's financial hub, a per-capita GDP exceeding USD 90,674.1 in 2024, and government initiatives such as the Digital Economy Framework for Action, which targets e-commerce as a strategic growth pillar through 2030.

Market Dynamics

To evaluate market opportunities, Request Sample

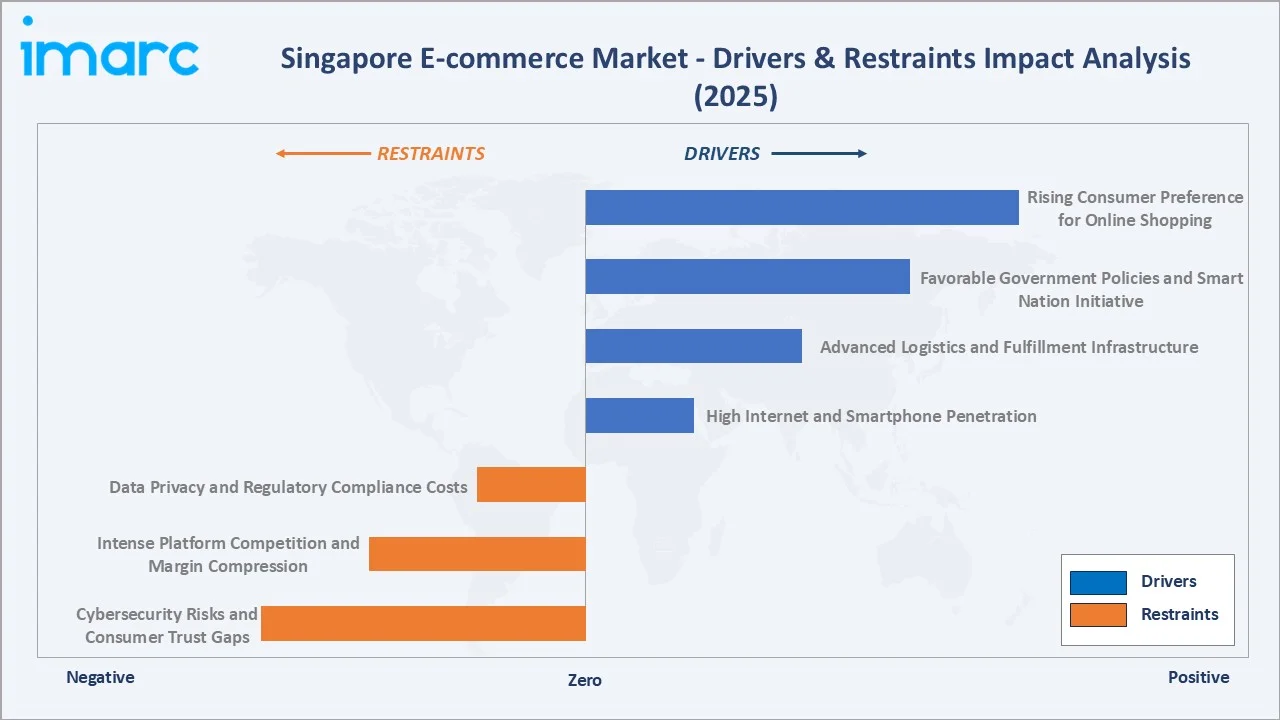

Market Drivers

- High Internet and Smartphone Penetration: Singapore recorded 5.78 million internet users in 2025, . Widespread smartphone usage creates the foundation for seamless mobile commerce. This near-universal connectivity directly facilitates online purchasing, digital payment adoption, and multi-channel retail engagement across all consumer demographics.

- Advanced Logistics and Fulfillment Infrastructure: The country’s highly developed warehousing networks, automated fulfillment centers, and strong last-mile capabilities support same-day and next-day delivery expectations. Integration of AI-driven route optimization, real-time tracking, and inventory management systems improves operational efficiency and reduces delivery times.

- Favorable Government Policies and Smart Nation Initiative: Singapore's IMDA-led digitalization grants, SME Go Digital programme, and Startup SG ecosystem actively support e-commerce adoption. The Digital Economy Framework for Action targets e-commerce as a priority sector. PayNow's interoperability with regional payment rails is accelerating cross-border digital commerce.

- Rising Consumer Preference for Online Shopping: Behavioral shifts post-COVID have structurally increased digital purchase frequency. Recent consumer trends indicate that a significant share of Singapore consumers shop online at least weekly. Live commerce formats, influencer marketing, and social media integration are sustaining high engagement rates.

Market Restraints

- Cybersecurity Risks and Consumer Trust Gaps: Rising incidents of digital fraud and phishing attacks undermine consumer confidence in online payments. Authorities have reported a year-on-year increase in e-commerce scams, representing a structural restraint on market expansion, particularly among older demographics.

- Intense Platform Competition and Margin Compression: The market is characterized by aggressive discounting, high customer acquisition costs, and subsidy-driven growth by well-capitalized players such as Shopee and Lazada. This creates structural profitability challenges for emerging platforms and niche retailers.

- Data Privacy and Regulatory Compliance Costs: Singapore's Personal Data Protection Act (PDPA) and its 2021 amendments impose data handling obligations that increase compliance costs. New mandatory data breach notification requirements add operational complexity for smaller e-commerce operators.

Market Opportunities

- Cross-Border E-commerce Expansion: Singapore's strategic position as an ASEAN gateway creates significant cross-border trade opportunities. The ASEAN e-commerce market is projected to reach USD 230 Billion by 2026. Singapore-based platforms are well-positioned to capture regional demand, particularly from Indonesia, Malaysia, Thailand, and Vietnam.

- Live Commerce and Social Media Integration: TikTok Shop's rapid growth in Singapore signals a significant structural opportunity for brands integrating shoppable video content. Live commerce is projected to represent a notable share of total e-commerce GMV by the end of the decade.

- B2B E-commerce Digitalization: SME procurement digitalization, driven by IMDA's Nationwide E-Invoicing Network and enterprise resource planning integrations, is expanding the addressable B2B e-commerce market. B2B platforms targeting wholesale food, industrial supply, and professional services represent high-growth niches.

Market Challenges

- Last-Mile Delivery Cost Escalation: Rising labor costs, fuel price volatility, and growing consumer expectations for free and same-day delivery create structural cost pressures. Delivery expenses represent a significant share of total operational expenditure for mid-tier e-commerce operators.

- Platform Saturation and Customer Retention: High competition between Shopee, Lazada, and Amazon SG creates customer switching behavior and loyalty challenges. Customer acquisition costs have risen over recent years, compressing unit economics for new entrants.

Emerging Market Trends

1. Live Commerce and Shoppable Video Acceleration

Live commerce has emerged as one of the fastest-growing e-commerce formats in Singapore, driven by TikTok Shop and Instagram Live integrations. Livestream e-commerce Gross Merchandise Value (GMV) in Southeast Asia is projected to grow at a strong pace through the forecast period. Singapore brands are actively integrating real-time interactive selling into their digital strategies, particularly in Fashion, Beauty, and Consumer Electronics categories.

2. AI-Powered Personalization and Recommendation Engines

Leading platforms are deploying machine learning models to deliver hyper-personalized product recommendations, dynamic pricing, and predictive inventory management. AI-driven recommendation engines contribute significantly to overall platform GMV. AI adoption is accelerating across customer service (chatbots), fraud detection, and demand forecasting functions, structurally improving platform economics.

3. Sustainable and Ethical E-commerce

Consumer awareness of environmental impact is shaping purchasing decisions, with a significant share of Singapore consumers expressing preference for sustainable packaging options. Platforms are responding by introducing green delivery slots, carbon offset programs, and eco-friendly packaging mandates for seller partners. This trend is particularly pronounced in Apparel and Groceries categories.

4. Super-App Integration and Embedded Commerce

Singapore's fintech and super-app ecosystem, led by Grab and Singtel Dash, is embedding e-commerce capabilities within broader lifestyle and financial platforms. Embedded commerce reduces friction in the purchase journey by integrating payment, loyalty rewards, and product discovery within single-app environments. This trend is expected to channel a significant share of mobile GMV through super-app ecosystems over the coming years.

5. Cross-Border E-commerce and ASEAN Market Integration

Singapore-based merchants are leveraging the country's free-trade agreements with over 25 countries to enable efficient cross-border commerce. Platforms such as Lazada and Shopee provide cross-border fulfillment services connecting Singapore sellers with over 670 million ASEAN consumers. Cross-border e-commerce revenue from Singapore is projected to grow at approximately 16% CAGR through 2034.

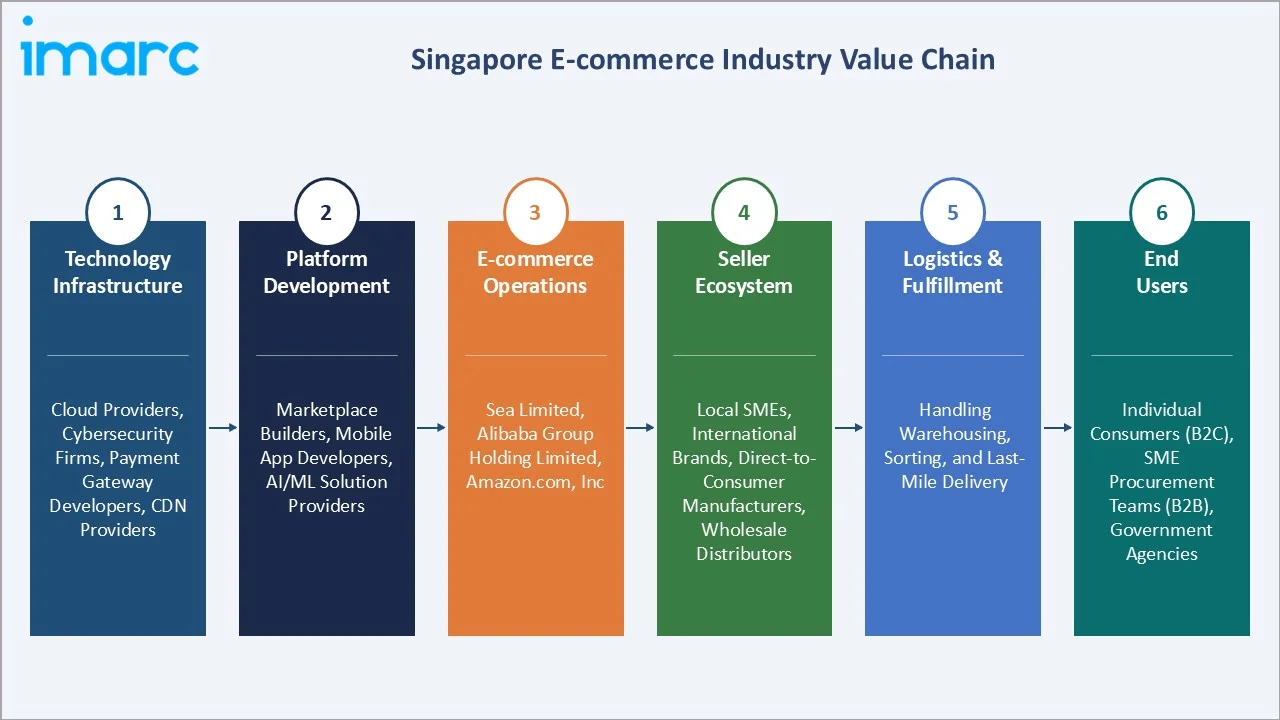

Industry Value Chain Analysis

The Singapore e-commerce industry value chain spans six integrated stages from technology infrastructure supply through end-consumer delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Value Chain Stage |

Key Participants / Description |

|

Technology Infrastructure |

Cloud providers, cybersecurity firms, payment gateway developers, CDN providers |

|

Platform Development |

Marketplace builders, mobile app developers, AI/ML solution providers |

|

E-commerce Operations |

Sea Limited, Alibaba Group Holding Limited, Amazon.com, Inc |

|

Seller Ecosystem |

Local SMEs, international brands, direct-to-consumer manufacturers, wholesale distributors adopting e-commerce channels |

|

Logistics & Fulfillment |

Handling warehousing, sorting, and last-mile delivery |

|

End Users |

Individual consumers (B2C), SME procurement teams (B2B), government agencies, institutional buyers |

Marketplace platforms hold the highest strategic value by integrating seller ecosystems, consumer data analytics, and logistics coordination into turnkey commerce solutions. Meanwhile, social commerce and embedded payment ecosystems are reshaping the value chain, enabling direct-to-consumer brands to bypass traditional marketplace intermediaries.

Technology Landscape in the Singapore E-commerce Industry

Artificial Intelligence and Machine Learning

AI-powered recommendation engines, dynamic pricing algorithms, and predictive inventory management systems are becoming standard infrastructure for leading platforms. Shopee and Lazada deploy deep learning models to analyze user behavior and drive conversion rates.

Mobile Commerce and Super-App Technology

Mobile-first platforms now account for a dominant share of Singapore's total e-commerce transactions. Progressive web apps, one-click checkout, and biometric authentication are reducing cart abandonment rates. Integration with digital wallets including PayNow, GrabPay, and Apple Pay is enabling frictionless transactions across devices.

Logistics Technology and Automation

Automated fulfillment centers, route optimization algorithms, and real-time tracking systems are transforming delivery efficiency. Companies such as J&T Express and Ninja Van employ AI-powered route planning that reduces delivery costs. Drone delivery pilots are underway for specific residential zones, with commercial viability expected in the coming years.

Blockchain and Supply Chain Transparency

Blockchain-based product authentication and supply chain tracking are gaining traction in Luxury Goods and Food Safety categories. Singapore's regulatory sandbox environment supports blockchain commerce pilots. These technologies address counterfeiting concerns, which represent a key barrier to premium product adoption online.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Apparel, Footwear and Accessories | 32.6% | 2025 |

| Transaction | Business-to-Consumer | 68.5% | 2025 |

| Region | Central | 28.4% | 2025 |

By Type

To access detailed market analysis, Request Sample

Apparel, Footwear, and Accessories leads the Singapore e-commerce market by type with a 32.6% share in 2025. Demand is driven by Singapore's fashion-forward consumer base, influencer marketing adoption, and the rapid growth of fast-fashion and luxury resale platforms. The segment is projected to sustain a CAGR of approximately 13.8% through 2034, supported by TikTok Shop's commerce integration and the expansion of international fashion brands' direct digital presence in Singapore.

By Transaction

Business-to-Consumer (B2C) is the dominant transaction mode at 68.5% of total market volume in 2025. High credit card and digital wallet penetration, and consumer trust in established marketplace platforms underpin B2C dominance.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Central |

28.4% |

Dense commercial districts, high-income households, corporate B2B procurement |

|

East |

21.6% |

Residential growth corridors, Changi Airport logistics hub, Tampines commercial nodes |

|

West |

19.7% |

Jurong industrial zone, NTU student population, Tuas logistics corridor |

|

North-East |

16.3% |

Rapidly growing residential zones (Punggol, Sengkang), young family demographics, fastest-growing CAGR |

|

North |

14.0% |

Woodlands cross-border commerce corridor, JB connectivity, industrial procurement |

Central region commands 28.4% of Singapore e-commerce revenue in 2025. The region encompasses Singapore's Central Business District (CBD), Orchard Road retail corridor, and Marina Bay. High-density commercial and residential activity, combined with the concentration of Singapore's highest-income households, drives premium e-commerce purchasing. Corporate B2B procurement from companies headquartered in the CBD further amplifies the Central region's revenue share.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Sea Limited |

Shopee |

Leader |

Largest GMV, live commerce, logistics network (SLS) |

|

Alibaba Group Holding Limited |

Lazada |

Leader |

Chinese supply chain access, regional ASEAN scale |

|

Amazon.com, Inc |

Amazon SG |

Leader |

Prime ecosystem, AWS logistics, global brand trust |

|

Global Fashion Group |

Zalora |

Challenger |

Fashion vertical specialization, regional presence |

|

Carousell |

Carousell |

Challenger |

C2C marketplace dominance, community-led growth |

|

FairPrice Group |

FairPrice Online |

Emerging |

Grocery anchor, Singapore-centric, omnichannel |

The Singapore e-commerce competitive landscape is moderately concentrated. Regional specialists and vertical-focused platforms compete in niche categories. Strategic investments in logistics infrastructure, AI capabilities, and live commerce technology are the primary competitive battlegrounds.

Key Company Profiles

Sea Limited

Sea Limited is the parent company of Shopee, the dominant e-commerce marketplace in Singapore and Southeast Asia. Headquartered in Singapore, The company operates across e-commerce (Shopee), digital financial services (SeaMoney), and digital entertainment (Garena).

- Product & Platform Portfolio: Shopee offers a comprehensive marketplace spanning fashion, electronics, groceries, and home goods. The ShopeePay digital wallet, ShopeeFood delivery, and Shopee Live commerce format are key platform extensions. Shopee Logistics Service (SLS) provides end-to-end fulfillment.

- Recent Developments: In 2026, Sea Limited announced an expanded strategic partnership with Google to develop AI-powered innovations across its ecosystem, including e-commerce, digital finance, and gaming. The collaboration includes building advanced AI-driven shopping experiences on Shopee, such as “agentic commerce” tools to enhance product discovery and transactions.

- Strategic Focus: Shopee's strategy centers on deepening live commerce integration, expanding SeaMoney financial services, and leveraging its Singapore base to scale across Southeast Asia's 670 million consumer market.

Alibaba Group Holding Limited

Alibaba Group Holding Limited is a leading global technology conglomerate focused on e-commerce, digital payments, cloud computing, and logistics. Founded in 1999 and headquartered in Hangzhou, China, the company has built one of the world’s largest digital commerce ecosystems.

- Product & Platform Portfolio: Lazada, a subsidiary of Alibaba Group, offers marketplace commerce, LazMall for branded goods, LazLive for live commerce, and LEO (Lazada Ecosystem Optimization) AI tools for sellers. LazMall hosts thousands of official brand stores in Singapore.

- Recent Developments: In 2026, Alibaba Group Holding Limited announced that its AI-powered platform Accio Work has rapidly scaled to support over 230,000 online stores globally within a month of launch. The tool functions as an “agentic AI workforce,” enabling businesses to automate end-to-end e-commerce operations such as store management, product listing optimization, and performance tracking through simple commands.

- Strategic Focus: Alibaba Group is focused on improving profitability through seller monetization, premium brand partnerships via LazMall, and leveraging Alibaba's Cainiao logistics network for cross-border commerce efficiency.

Amazon.com, Inc

Amazon.com, Inc. is a global leader in e-commerce, cloud computing, digital streaming, and artificial intelligence. Founded in 1994 by Jeff Bezos and headquartered in Seattle, USA, Amazon has evolved from an online bookstore into one of the world’s most influential digital ecosystems.

- Product & Platform Portfolio: Amazon.com, Inc offers over 50 million products across all major categories. Prime membership provides free same-day delivery on eligible orders, exclusive deals, and streaming content. Amazon Business serves B2B procurement needs of Singapore's SME and enterprise segments.

- Recent Developments: In 2023, Amazon.com, Inc launched its first cross-border e-commerce Brand Launchpad in Singapore in partnership with Enterprise Singapore and the Singapore Business Federation. The initiative aims to help over 100 local SMEs expand internationally—particularly into the U.S.—through training, account management, and access to global marketplaces.

- Strategic Focus: Amazon's Singapore strategy focuses on deepening Prime ecosystem engagement, expanding Amazon Business for B2B procurement, and leveraging AWS cloud leadership to offer integrated commerce and technology solutions.

Market Concentration Analysis

The Singapore e-commerce market exhibits moderate concentration at the platform level. The top three players, Sea Limited, Alibaba Group Holding Limited, Amazon.com, Inc, collectively account for an estimated 55-62% of total market in 2025.

The market is experiencing bifurcated competitive dynamics. At the platform tier, consolidation is occurring around GMV scale, logistics ownership, and AI technology differentiation. Simultaneously, niche vertical platforms in groceries, fashion, and home goods are capturing loyal customer segments through category expertise.

Consolidation trends through 2034 are expected to be driven by platform mergers, logistics network acquisitions, and super-app integrations that absorb standalone commerce functionalities. Carousell's acquisition strategy and Grab's embedded commerce expansion are examples of consolidation dynamics already reshaping the competitive landscape.

Investment & Growth Opportunities

Fastest-Growing Segments

Grocery e-commerce is the highest-growth type sub-segment at approximately 14.2% CAGR through 2034, driven by post-pandemic behavioral permanence, cold-chain logistics maturity, and subscription meal kit adoption. Live commerce technology and social commerce integration represent the premium growth opportunity. B2B e-commerce platforms targeting SME procurement are expanding at approximately 10.8% CAGR.

Emerging Market Expansion

Singapore-based platforms have unique access to the broader ASEAN e-commerce market, projected to reach USD 230 Billion by 2026. The North-East region of Singapore presents the highest domestic growth opportunity, with new Smart Town developments in Punggol Digital District creating digital-native commerce corridors. Cross-border commerce corridors with Malaysia (Johor Bahru) and Indonesia (Batam) represent emerging hyper-local opportunities.

Venture and Strategic Investment Trends

Singapore's e-commerce ecosystem attracted significant venture investment during the recent period, according to Crunchbase data. Key investment themes include logistics automation, AI personalization engines, embedded finance for commerce, and sustainability-focused supply chain platforms. The government's SGInnovate initiative and Enterprise Singapore's Scale-Up SG programme provide co-investment support for e-commerce infrastructure start-ups.

Future Market Outlook (2026-2034)

The Singapore e-commerce market forecast projects steady value expansion from USD 116.3 Billion in 2025 to USD 332.0 Billion by 2034 at a CAGR of 12.36%. This trajectory positions Singapore as one of the highest per-capita e-commerce markets globally by 2034, reflecting the maturity and sophistication of its digital commerce ecosystem.

Technological disruptions expected to shape the market through 2034 include ambient commerce (voice and IoT-enabled purchasing), augmented reality (AR) virtual try-on capabilities for fashion and home goods, and autonomous last-mile delivery. Regulatory evolution under Singapore's Digital Economy Agreements with partner countries will expand cross-border trade frameworks, creating new revenue corridors for Singapore-based merchants.

Industry transformation will be characterized by deeper super-app convergence, where e-commerce, financial services, food delivery, and entertainment merge within single platforms. The Groceries and Cosmetics segments are projected to experience the most significant structural shifts.

Research Methodology

Primary Research

IMARC Group's primary research encompasses structured interviews with industry stakeholders, including e-commerce platform executives, logistics operators, payment gateway providers, retail brands, and regulatory authorities. These interviews validate quantitative data, surface emerging trends, and provide qualitative context not available through secondary sources.

Secondary Research

Secondary research draws from Singapore's IMDA annual reports, Enterprise Singapore publications, Monetary Authority of Singapore (MAS) digital payment statistics, DataReportal digital economy reports, company annual reports, trade association publications (e-Commerce Association of Singapore), and investment transaction databases (Crunchbase, PitchBook). All secondary data is cross-validated across a minimum of two independent sources.

Forecasting Models

Market forecasts are generated using a hybrid methodology combining time-series regression analysis, bottom-up segment aggregation, and scenario-based modeling. The bottom-up approach aggregates type-level, transaction-level, and regional-level market estimates to validate top-down macro projections. Three scenarios (base, optimistic, conservative) are modeled; the base case is presented in this report, representing the most probable market trajectory given current market conditions as of Q1 2025.

Singapore E-commerce Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Home Appliances, Apparel, Footwear and Accessories, Books, Cosmetics, Groceries, Others |

| Transactions Covered | Business-to-Consumer, Business-to-Business, Others |

| Regions Covered | North-East, Central, West, East, North |

| Companies Covered | Sea Limited, Alibaba Group Holding Limited, Amazon.com, Inc, Global Fashion Group, Carousell, FairPrice Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Singapore e-commerce market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Singapore e-commerce market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Singapore e-commerce industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Singapore E-commerce Market Report

The Singapore e-commerce market size reached USD 116.3 Billion in 2025 and is projected to reach USD 332.0 Billion by 2034 at a 12.36% CAGR.

The market is growing at a CAGR of 12.36% during 2026-2034, supported by high digital adoption, smartphone penetration, and advanced logistics infrastructure.

Key drivers include 97.1% internet penetration, smartphone adoption exceeding 89%, government Smart Nation initiatives, and advanced logistics infrastructure.

Apparel, Footwear, and Accessories is the largest segment, holding 32.6% of market share in 2025, driven by fashion-forward consumer behavior and social commerce growth.

Groceries is the fastest-growing type segment at approximately 14.2% CAGR, driven by online food procurement platforms.

Business-to-Consumer (B2C) transactions dominate at 68.5% of total market volume in 2025. B2B is the fastest-growing transaction type at approximately 10.8% CAGR.

The Central region leads with a 28.4% revenue share in 2025, driven by high-income households, corporate procurement, and Singapore's dense commercial districts.

Leading companies include Sea Limited, Alibaba Group Holding Limited, Amazon.com, Inc, Global Fashion Group, Carousell, and FairPrice Group.

Key trends include live commerce acceleration, AI-powered personalization, sustainable e-commerce, super-app integration, and cross-border ASEAN commerce expansion.

The Singapore e-commerce market is projected to reach USD 208.3 Billion by 2030, reflecting continued strong growth at a 12.36% CAGR from the 2025 base of USD 116.3 Billion.

The Singapore government actively supports e-commerce through the Smart Nation initiative, IMDA digitalization grants, SME Go Digital programme, and Digital Economy Agreements with partner countries.

Key challenges include rising cybersecurity risks and scam incidents, intense platform competition compressing margins, data privacy regulatory compliance costs, and last-mile delivery cost escalation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)