Singapore Energy Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Singapore Energy Market Size, Share, Trends & Forecast (2026-2034)

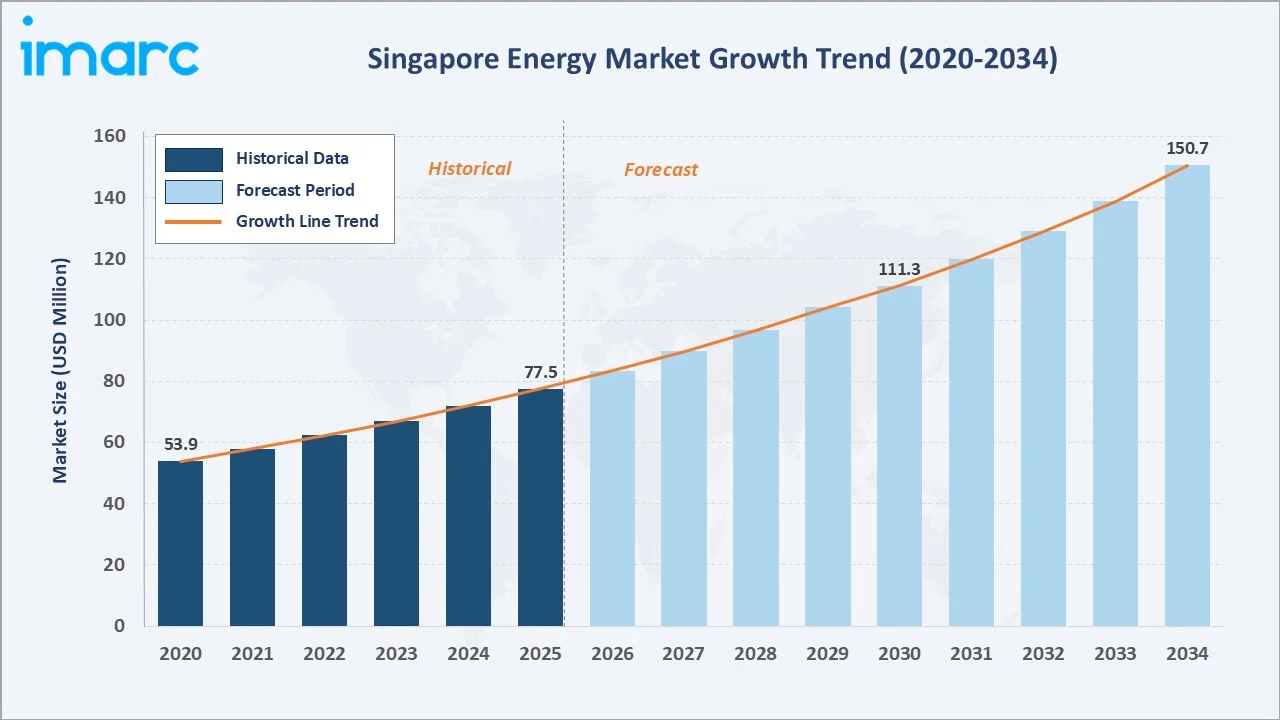

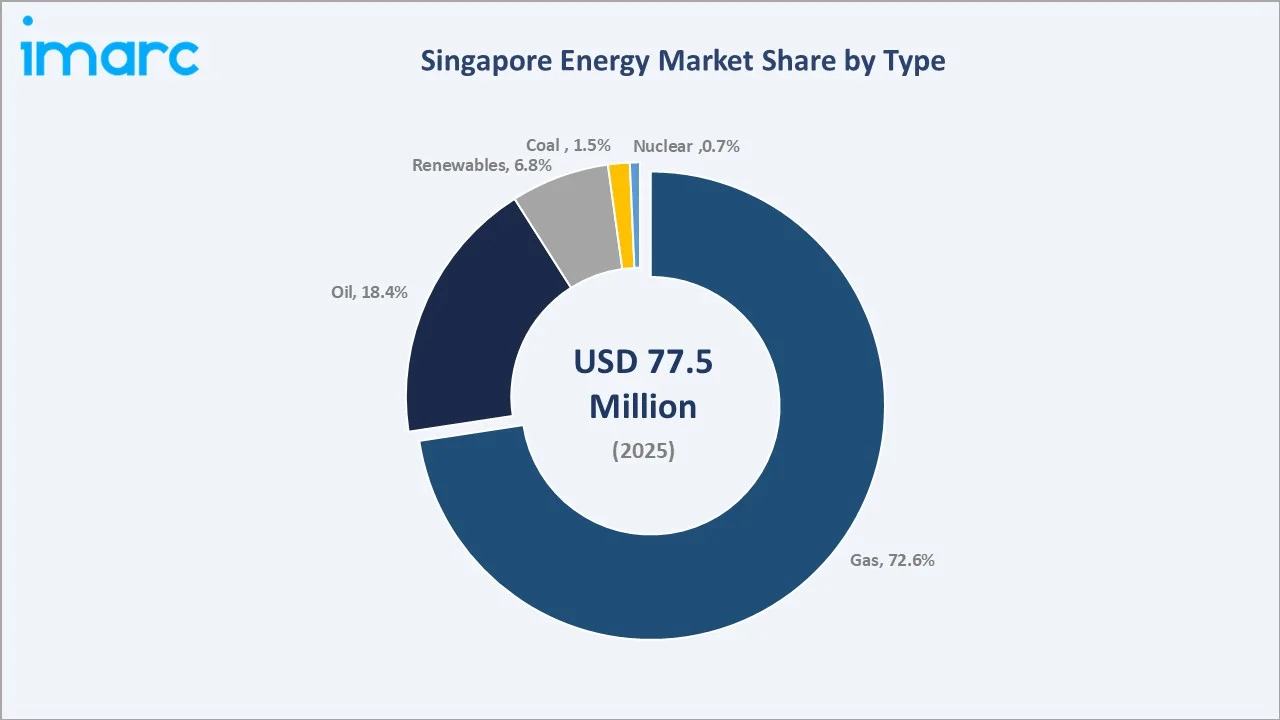

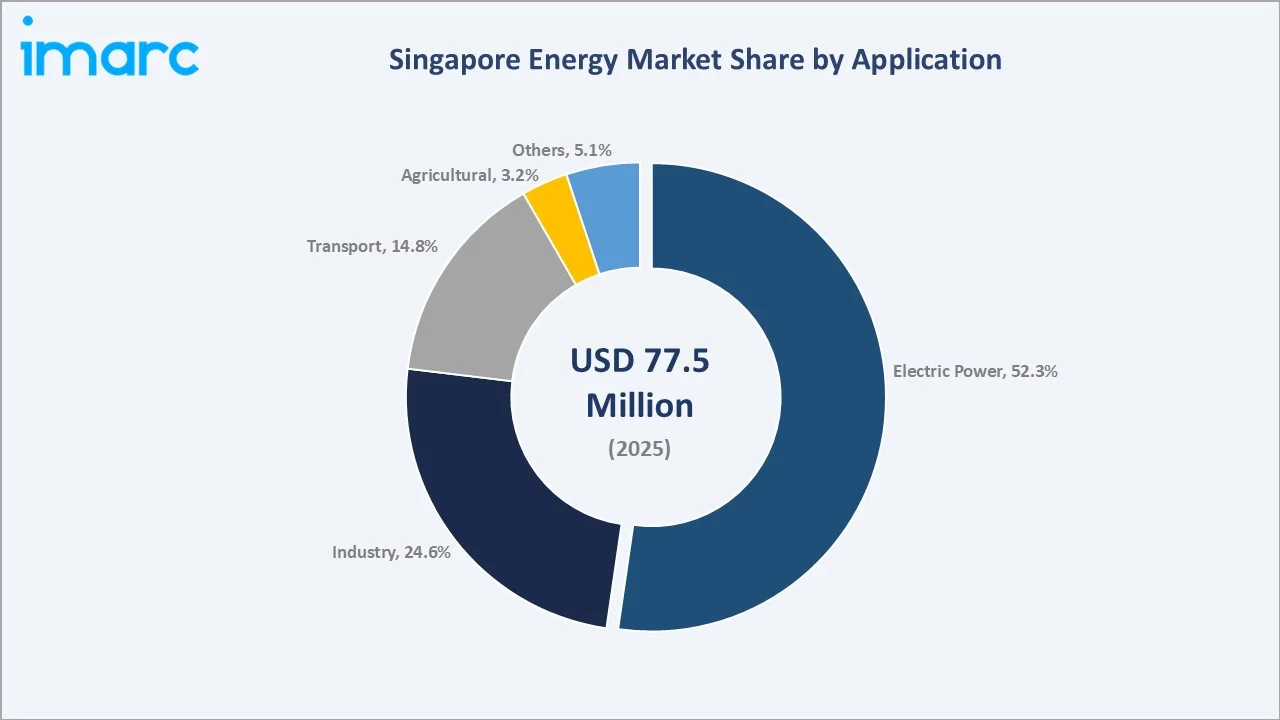

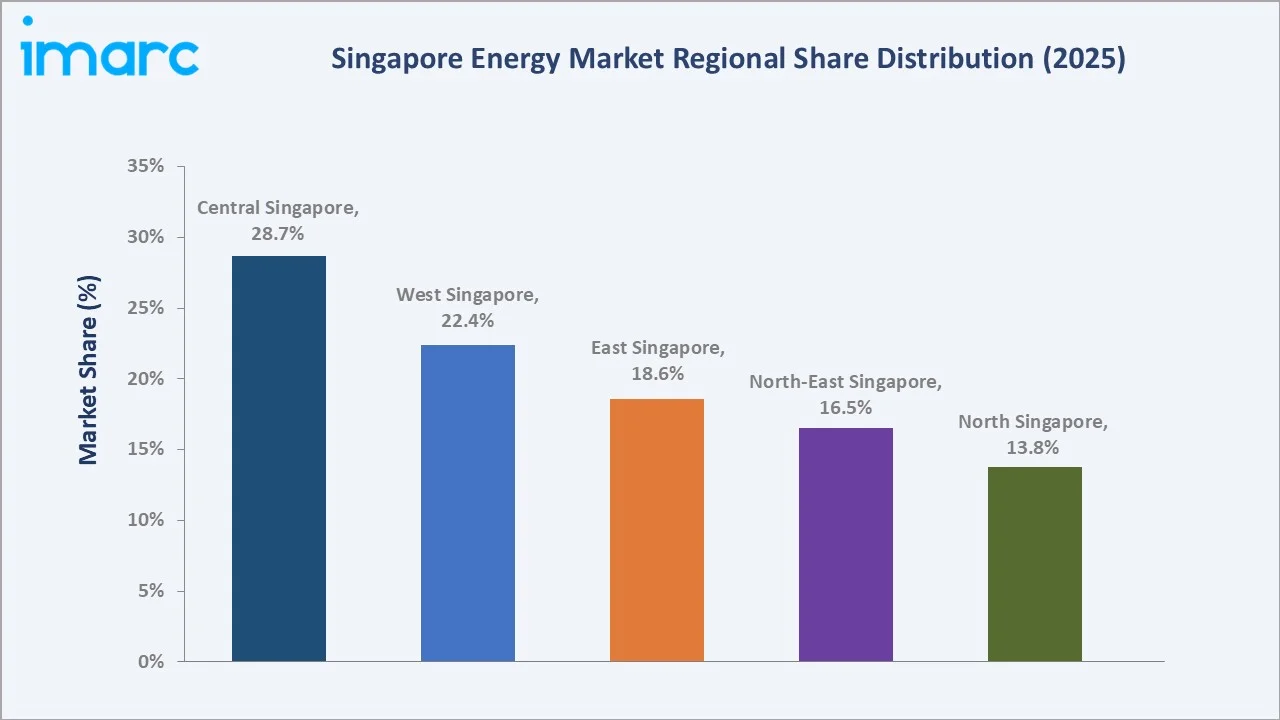

The Singapore energy market reached USD 77.5 Million in 2025 and is projected to reach USD 150.7 Million by 2034, growing at a CAGR of 7.52% during 2026-2034. Singapore’s per capita energy consumption reached around 6.4 toe in 2024, nearly 4 times higher than the Asian average, while electricity consumption stood at approximately 9,822 kWh per person, around 3 times the Asian average. This high energy consumption is driving Singapore’s energy market through rising demand for power generation, grid modernization, energy efficiency solutions, and sustainable energy infrastructure. Gas dominates at 72.6% energy type share. Electric power leads the application at 52.3%. Central Singapore commands 28.7% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 77.5 Million |

|

Forecast Market Size (2034) |

USD 150.7 Million |

|

CAGR (2026-2034) |

7.52% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Gas (72.6%, 2025) |

|

Dominant Application |

Electric Power (52.3%, 2025) |

|

Leading Region |

Central Singapore (28.7%, 2025) |

The market expanded from USD 53.9 Million in 2020 to USD 77.5 Million in 2025, anchored at USD 111.3 Million in 2030, and forecast to reach USD 150.7 Million by 2034. Singapore's energy market is uniquely characterized by near-total import dependence, making energy security, price competitiveness, and supply diversification the market's defining strategic concerns alongside decarbonization.

To get more information on this market, Request Sample

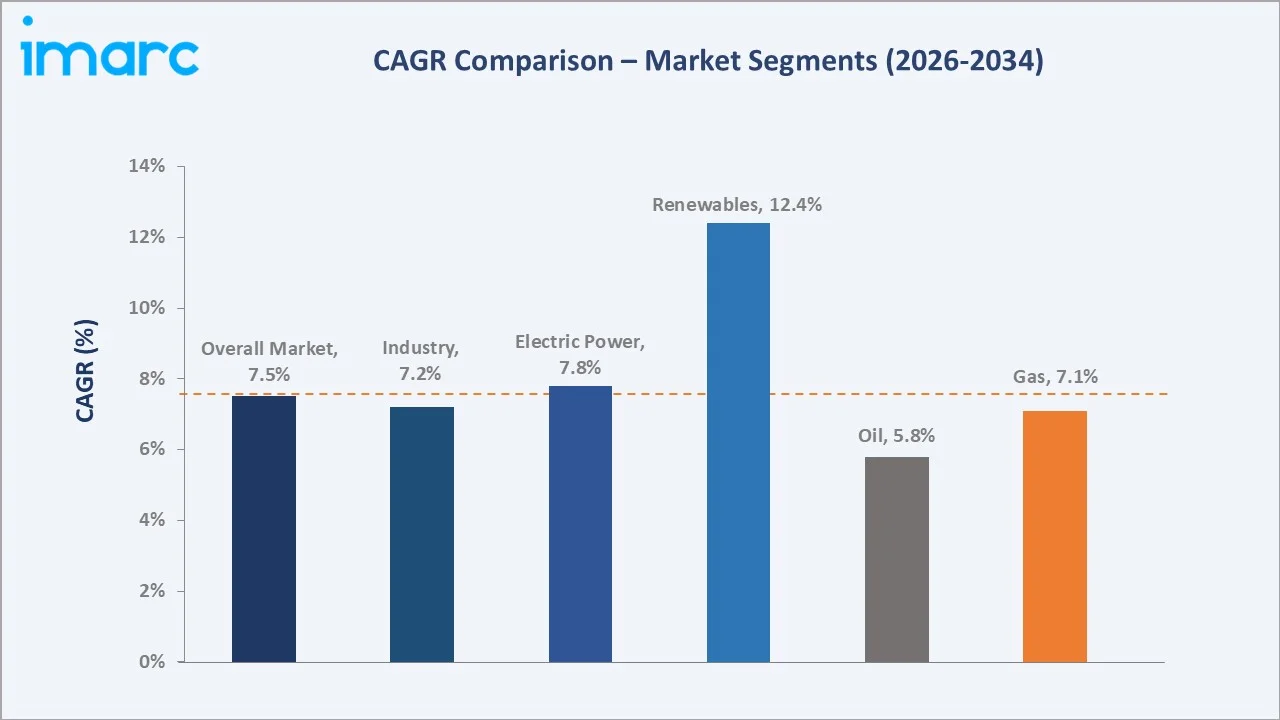

Renewables grow fastest at ~12.4% CAGR (2026-2034) as Singapore's Green Plan 2030 targets 2 GWp solar deployment, ASEAN cross-border renewable power import, offshore floating solar platforms, and green hydrogen imports from Australia, Chile, and the Middle East as Singapore develops its hydrogen supply chain. Electric power application grows at ~7.8% CAGR driven by Singapore's data center sector and EV charging infrastructure expansion.

Executive Summary

The Singapore energy market reached USD 77.5 Million in 2025, reflecting the city-state's position as Southeast Asia's most sophisticated energy hub, simultaneously serving as ASEAN's primary LNG trading center, one of the world's largest oil trading hubs, a global petrochemical manufacturing cluster, and increasingly as the region's green energy transition laboratory. The market is projected to reach USD 150.7 Million by 2034 at 7.52% CAGR.

Gas at 72.6% dominates Singapore's energy mix as the nation's near-exclusive power generation fuel. The electric power application segment at 52.3% growing rapidly. Central Singapore at 28.7% leads through the CBD's commercial and data center energy intensity.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Gas - 72.6% share (2025) |

|

Dominant Application |

Electric Power - 52.3% market share (2025) |

|

Leading Region |

Central Singapore - 28.7% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Gas is the dominant segment at 72.6%: Gas is the primary fuel used for electricity generation due to its reliability, efficiency, and lower carbon emissions compared to other fossil fuels. Strong LNG infrastructure, long-term gas import agreements, and Singapore’s focus on energy security and cleaner power generation continue to support the segment’s dominance.

- Electric Power at 52.3% driven by data center growth and EV infrastructure as new demand frontiers: Singapore's data center moratorium has resumed approvals for new green data centers, creating distributed new demand nodes across all Singapore regions.

- Central Singapore at 28.7% through the CBD's commercial and data center concentration: Singapore's commercial buildings are among Asia's most energy managed, Building and Construction Authority (BCA) Green Mark Platinum certification is standard for new CBD developments, integrating chilled beam air distribution, variable frequency drives, and building energy management systems (BEMS) that achieve below Singapore's median commercial building energy intensity. .

Singapore Energy Market Overview

Singapore's energy market operates within one of the world's most unique national energy contexts. The market encompasses natural gas procurement and distribution, petroleum products, electricity generation and distribution through the National Electricity Market of Singapore (NEMS), renewable energy development, and energy services.

The ecosystem integrates international fuel suppliers, the Singapore LNG Terminal, power generators, the National Electricity Market of Singapore (NEMS), retail electricity licensees, industrial consumers, and regulatory bodies. Macroeconomic factors include strong economic activity, industrialization, urban infrastructure development, rising electricity demand, and the expansion of data centers, manufacturing, and commercial sectors.

Market Dynamics

To evaluate market opportunities, Request Sample

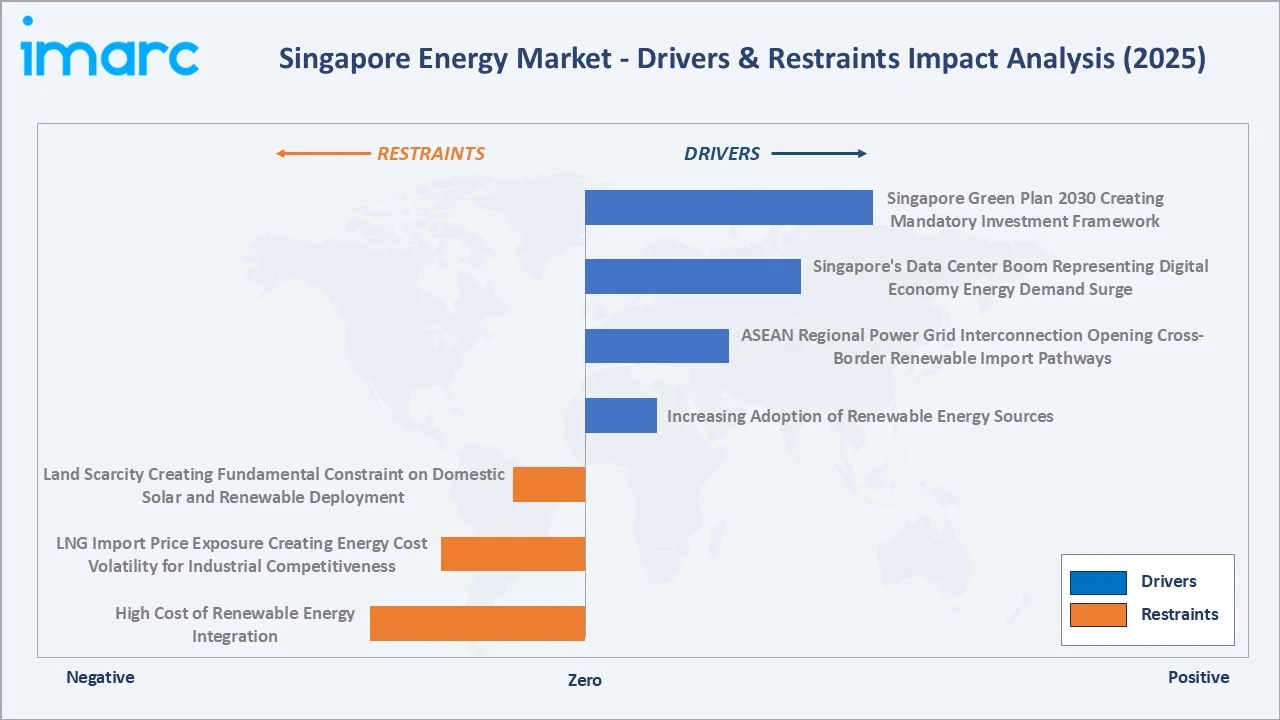

Market Drivers

- Singapore Green Plan 2030 Creating Mandatory Investment Framework: Under the Singapore Green Plan 2030, the country aims to expand solar energy deployment to at least 2 GWp, enabling solar power to meet a portion of projected electricity demand while supporting the annual energy needs of hundreds of thousands of households. This initiative is driving Singapore’s energy market by accelerating investments in renewable energy infrastructure, solar integration, grid modernization, and clean energy transition projects.

- Singapore's Data Center Boom Representing Digital Economy Energy Demand Surge: Singapore’s data center boom is rapidly rising electricity demand from cloud computing, AI workloads, digital services, colocation facilities, and hyperscale infrastructure expansion. The growth of the digital economy is increasing investments in power generation, grid reliability, energy-efficient cooling systems, renewable energy integration, and sustainable energy solutions to support high-density data center operations.

- ASEAN Regional Power Grid Interconnection Opening Cross-Border Renewable Import Pathways: ASEAN regional power grid interconnection initiatives enabling cross-border electricity imports and improving access to low-carbon renewable energy from neighboring countries. These interconnection projects support Singapore’s energy diversification strategy, strengthen energy security, and accelerate investments in transmission infrastructure, clean energy trading, and regional renewable power partnerships.

Market Restraints

- Land Scarcity Creating Fundamental Constraint on Domestic Solar and Renewable Deployment: Singapore's 728 sq.km. land area leaves buildable area that competes with housing, industrial, commercial, and military uses for solar deployment. This constraint makes Singapore structurally dependent on energy imports and drives the ASEAN power grid interconnection priority as the only economically viable pathway to large-scale renewable integration.

- LNG Import Price Exposure Creating Energy Cost Volatility for Industrial Competitiveness: Singapore's dependence on LNG imports exposes its electricity system to global LNG spot price volatility. Oil price volatility similarly affects Singapore's petrochemical industry and transportation fuel prices.

Market Opportunities

- Offshore Floating Solar and Agrivoltaic Deployment Beyond Conventional Land Constraints: Singapore's exclusive economic zone (EEZ) extends nautical miles offshore, representing orders of magnitude more area than Singapore's land territory. International technology providers are actively pursuing Singapore EEZ deployment partnerships.

- Singapore's Low-Carbon Hydrogen Import Infrastructure as Next-Generation Energy Commodity: Singapore introduced its national hydrogen strategy in 2022, identifying hydrogen as a key low-carbon fuel that could potentially supply up to half of the country’s power demand by 2050. As hydrogen supply chains mature and achieve delivered cost, Singapore's unique position as ASEAN's energy trading hub positions it to become the region's hydrogen distribution center, generating new energy infrastructure investment and market activity that will be captured in the 2026-2034 forecast period.

Market Challenges

- Balancing Energy Security, Economic Competitiveness, and Decarbonization Simultaneously: Singapore's energy trilemma is particularly acute given the city-state's zero domestic resources, high-cost living environment, and economy dependent on energy-intensive industries. Every energy transition investment that improves sustainability adds cost versus incumbent gas generation, creating tension between Singapore's energy market's competitiveness and decarbonization goals.

- Energy Transition Job Displacement in Traditional Energy Sector: Singapore's refining and petrochemical sector employs a high number of workers whose skills are aligned with fossil fuel processing rather than renewable energy. EDB's (Economic Development Board) Energy Industry Plan retraining programs address this challenge, but the pace of skill transition must accelerate to match the market's green transition CAGR.

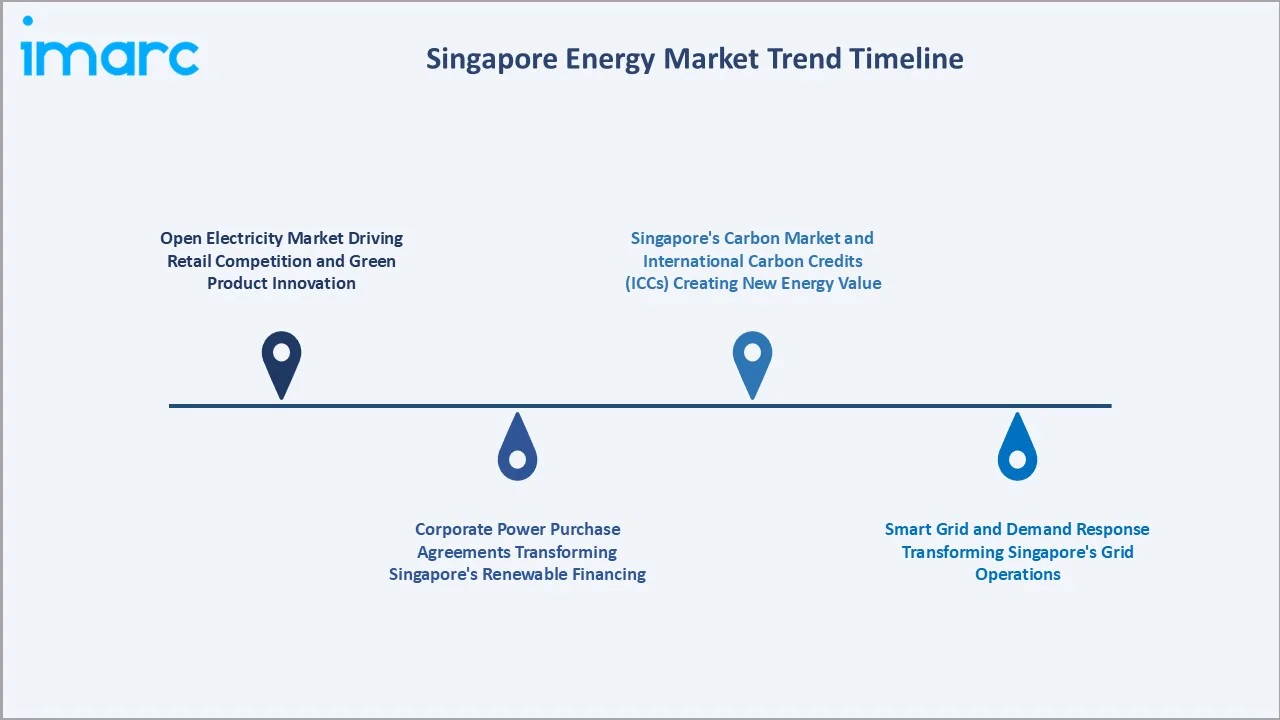

Emerging Market Trends

1. Open Electricity Market Driving Retail Competition and Green Product Innovation

The open electricity market is increasing retail competition and encouraging electricity providers to offer differentiated pricing models, flexible contracts, and green energy plans. Retailers are increasingly introducing renewable energy packages, carbon-neutral electricity plans, and digital energy management solutions to attract environmentally conscious residential and commercial consumers. The trend is further supported by growing adoption of solar-linked energy plans, smart metering systems, and sustainability-focused electricity products aligned with Singapore’s low-carbon transition goals.

2. Corporate Power Purchase Agreements Transforming Singapore's Renewable Financing

Corporate Power Purchase Agreements (PPAs) enable businesses to secure long-term renewable electricity supply while supporting clean energy project financing. Large corporations, data center operators, technology firms, and industrial players are increasingly entering renewable PPAs to meet ESG commitments, manage energy costs, and reduce carbon emissions. The trend is encouraging investments in regional solar and renewable energy projects, including cross-border clean power imports and virtual PPAs linked to Singapore’s decarbonization strategy.

3. Smart Grid and Demand Response Transforming Singapore's Grid Operations

Smart grid and demand response technologies are enabling real-time monitoring, intelligent load balancing, and more efficient electricity distribution across the national grid. Utilities and energy providers are increasingly deploying smart meters, AI-driven grid analytics, automated demand management systems, and dynamic pricing mechanisms to optimize power consumption and improve grid stability. The trend is further supported by Singapore’s growing renewable integration, electric vehicle adoption, and rising energy demand from data centers and advanced industrial infrastructure.

4. Singapore's Carbon Market and International Carbon Credits (ICCs) Creating New Energy Value

Singapore's International Carbon Credits (ICCs) framework, enabling companies to offset up to 5% of their carbon tax liability using eligible carbon credits from qualifying international projects, has connected Singapore's energy market to global carbon markets. The carbon price signal is directly driving energy efficiency investments across Singapore's industry and commercial sectors.

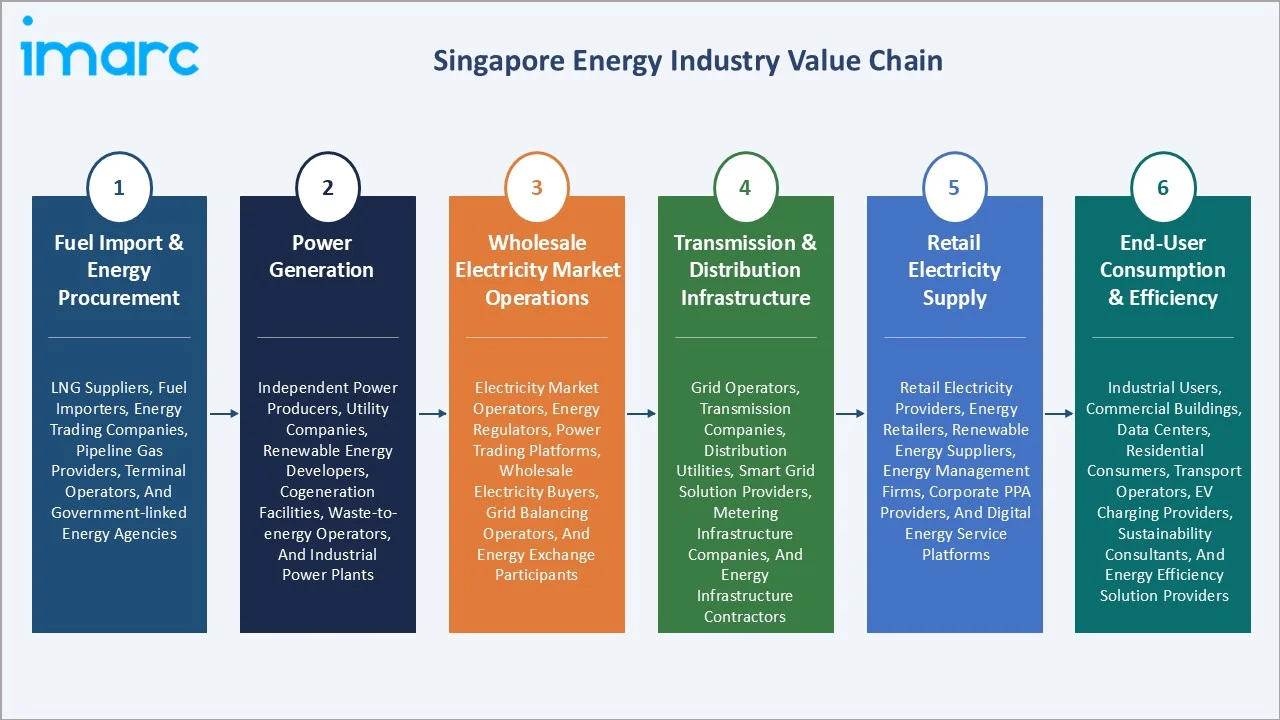

Industry Value Chain Analysis

Singapore's energy value chain integrates international fuel procurement, power generation through the NEMS wholesale market, transmission and distribution via a regulated network, and retail supply to customers. Industrial energy users on Jurong Island operate outside the retail market, with direct bilateral contracts for gas and electricity supply from pipeline operators.

|

Stage |

Key Participants |

|

Fuel Import & Energy Procurement |

LNG suppliers, fuel importers, energy trading companies, pipeline gas providers, terminal operators, and government-linked energy agencies. |

|

Power Generation |

Independent power producers, utility companies, renewable energy developers, cogeneration facilities, waste-to-energy operators, and industrial power plants. |

|

Wholesale Electricity Market Operations |

Electricity market operators, energy regulators, power trading platforms, wholesale electricity buyers, grid balancing operators, and energy exchange participants. |

|

Transmission & Distribution Infrastructure |

Grid operators, transmission companies, distribution utilities, smart grid solution providers, metering infrastructure companies, and energy infrastructure contractors. |

|

Retail Electricity Supply |

Retail electricity providers, energy retailers, renewable energy suppliers, energy management firms, corporate PPA providers, and digital energy service platforms. |

|

End-User Consumption & Efficiency |

Industrial users, commercial buildings, data centers, residential consumers, transport operators, EV charging providers, sustainability consultants, and energy efficiency solution providers. |

The wholesale electricity market (NEMS) tier is Singapore's most dynamic energy value chain element, processing electricity supply through a competitive pool market where registered market participants submit half-hourly bids.

Technology Landscape in the Singapore Energy Industry

Combined Cycle Gas Turbine (CCGT) Efficiency Leadership

Combined Cycle Gas Turbine (CCGT) technology is enabling highly efficient and reliable natural gas-based power generation with lower carbon emissions compared to conventional thermal plants. Energy companies are increasingly deploying advanced CCGT systems with improved thermal efficiency, digital monitoring, predictive maintenance, and optimized fuel utilization to support Singapore’s growing electricity demand. The technology plays a critical role in maintaining grid stability, supporting industrial and data center power requirements, and facilitating Singapore’s transition toward a lower-carbon energy mix.

Floating Solar PV Technology for Land-Constrained Deployment

Floating solar PV technology enables large-scale renewable energy deployment despite the country’s limited land availability. Solar panels installed on reservoirs and water bodies help optimize unused space, improve energy generation efficiency through natural cooling effects, and support Singapore’s clean energy transition goals. The technology is encouraging investments in innovative renewable infrastructure, smart grid integration, and sustainable power generation projects to strengthen long-term energy security and decarbonization efforts.

Battery Energy Storage Systems (BESS) for Island Grid Stability

Battery Energy Storage Systems (BESS) are enhancing grid stability, managing peak electricity demand, and supporting the integration of intermittent renewable energy sources. As an island-based power system with limited interconnection flexibility, Singapore is increasingly deploying advanced battery storage solutions for frequency regulation, backup power, and rapid-response energy balancing. The technology is also supporting smart grid development, energy resilience, electric vehicle infrastructure, and the country’s broader transition toward a low-carbon and digitally managed energy ecosystem.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Gas |

72.6% |

2025 |

|

Application |

Electric Power |

52.3% |

2025 |

|

Region |

Central Singapore |

28.7% |

2025 |

By Type

Gas dominates at 72.6% market share (2025). Singapore's natural gas market serves two distinct demand streams: pipeline gas imported from Malaysia and Indonesia for Genco power generation and industrial use; and LNG imported at the Singapore LNG Terminal for power generation top-up and industrial consumers requiring flexible supply.

To access detailed market analysis, Request Sample

Oil at 18.4% serves Singapore's refining industry, marine fuels, and aviation fuels. Renewables at 6.8% is growing fastest at ~12.4% CAGR through solar, offshore wind feasibility, and cross-border renewable imports. Coal at 1.5% is used minimally in older industrial boilers, being phased out under Singapore's carbon tax. Nuclear at 0.7% represents research and feasibility investment rather than operational nuclear power generation.

By Application

Electric power leads at 52.3% market share (2025). Singapore generated 60 TWh of electricity in 2024. Of these, 91.6% (or 55 TWh) was generated by main power producers. The electricity sector's CAGR of ~7.8% reflects both demand growth and energy market value appreciation from renewable energy premiums that increase the revenue intensity per unit of energy delivered.

Industry at 24.6% encompasses Jurong Island petrochemical process energy, manufacturing plant utilities, and cold chain facilities. Transport at 14.8% covers aviation fuel, marine bunkers, and land transport fuels, with EV charging as the fast-growing new component. The agricultural segment at 3.2% serves Singapore's indoor vertical farming industry. Others at 5.1% covers government facilities, educational institutions, and healthcare.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Central Singapore |

28.7% |

High commercial activity, dense urban infrastructure, and strong electricity demand from offices, retail establishments, hospitality facilities, and mixed-use developments. The region also benefits from advanced grid infrastructure and growing adoption of smart energy management systems. |

|

West Singapore |

22.4% |

Supported by manufacturing activities, industrial infrastructure, logistics operations, and large-scale commercial facilities. Strong demand for reliable power supply and energy efficiency solutions continues to support market growth in the region. |

|

East Singapore |

18.6% |

Driven by transportation infrastructure, commercial developments, residential expansion, and rising electricity consumption from urban infrastructure projects. The region is also witnessing increasing adoption of sustainable and energy-efficient technologies. |

|

North-East Singapore |

16.5% |

Expanding residential communities, commercial projects, and digital infrastructure development. Investments in smart city initiatives and energy-efficient urban planning are further supporting regional market expansion. |

|

North Singapore |

13.8% |

Supported by infrastructure development, industrial activities, residential growth, and improved connectivity. The region is gradually adopting renewable energy systems and smart energy technologies to support sustainable urban development. |

Central Singapore's 28.7% lead reflects the CBD's energy intensity premium. The Central Region's forthcoming Greater Southern Waterfront (GSW) development will significantly expand Central Singapore's energy demand when built out through 2030-2040.

West Singapore's 22.4% reflects Jurong Island's industrial dominance, demonstrating the petrochemical complex's extreme energy. North-East Singapore, at 16.5%, is growing fastest as Punggol Digital District, new HDB smart towns, and the Seletar Aerospace Park expansion create new energy demand patterns distinct from the CBD and industrial concentrations. East Singapore's 18.6% growth is driven by Changi Airport Terminal 5 development, data center cluster expansion in the East, and Tampines Regional Centre commercial growth.

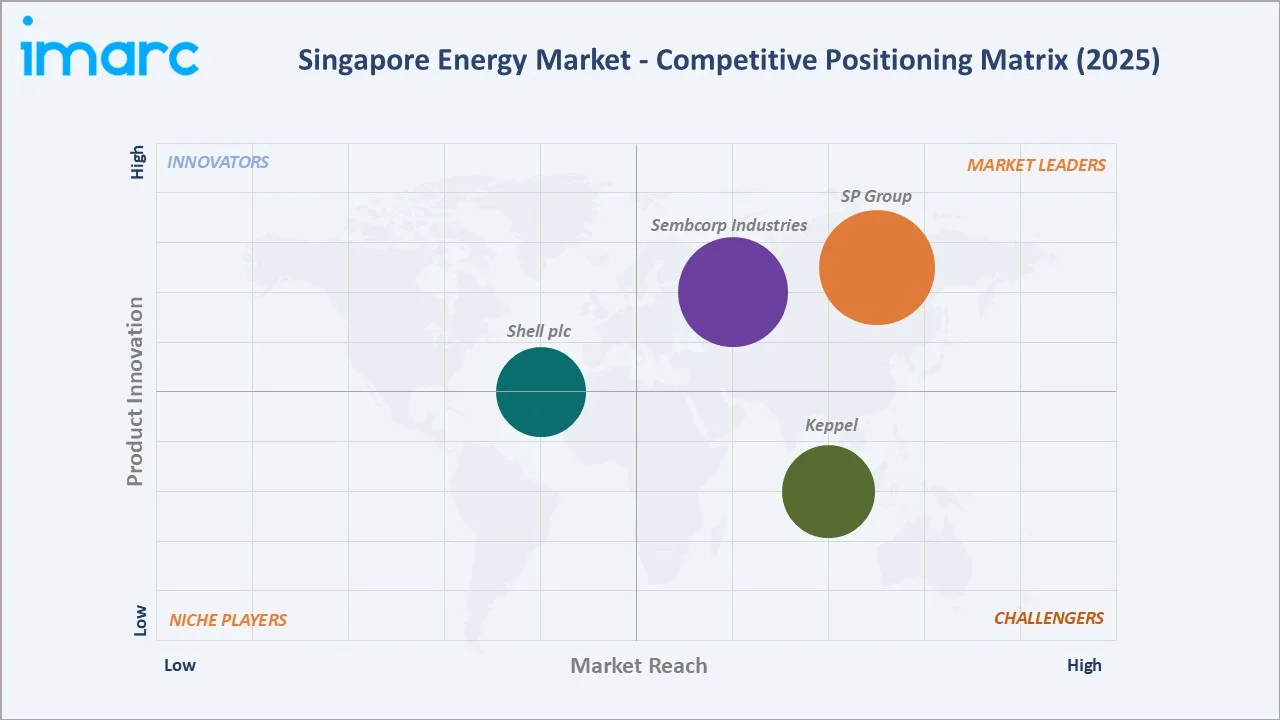

Competitive Landscape

Singapore's energy market operates with a distinctive competitive structure: a regulated transmission and distribution monopoly, a competitive wholesale electricity market (NEMS) with major Gencos, a liberalized retail electricity market, and free competition in renewable energy development and energy services.

|

Company Name |

Key Solutions |

Market Position |

Core Strength |

|

SP Group |

District cooling and heating systems, Electric Vehicle Solutions, Renewable Energy |

Market Leader |

SP Group is committed to delivering reliable and efficient energy utility services to its customers and enabling a low-carbon, smart energy future with the company’s sustainable solutions. |

|

Sembcorp Industries |

Wind, Solar, Hydro, Energy Storage Systems |

Market Leader |

As a leading renewables player, Sembcorp are driving the global energy transition with a diversified portfolio, spanning wind, solar, hydro and energy storage. |

|

Keppel |

District Cooling, EV Charging |

Strong Challenger |

Keppel is the first and largest developer and service provider of district cooling systems (DCS) in Singapore. |

|

Shell plc |

Natural gas, LNG for transport |

Established Player |

Shell Energy Singapore is a supplier of energy solutions, including gas, power, and Renewable Energy Credits (RECs), to Singapore’s domestic market. |

The competitive landscape is being reshaped by three forces: SP Group's extension from grid monopoly to EV charging infrastructure deployment gives it first-mover structural advantage in the EV energy services market; Sembcorp Industries' transformation from fossil fuel Genco to clean energy company positions it as Singapore's clean energy champion ahead of the energy transition; and international energy majors operating Singapore's largest industrial energy facilities are making structural decisions about Singapore's long-term role in their low-carbon portfolios that will determine whether Jurong Island's energy demand sustains or contracts through 2034.

Key Company Profiles

SP Group

SP Group is a leading utilities provider in the Asia Pacific, empowering the future of energy through low-carbon, smart solutions. As Singapore’s national grid operator, SP Group serves industrial, commercial, and residential customers with world-class transmission, distribution, and market support services.

- Portfolio: District cooling and heating systems, Electric Vehicle Solutions, Renewable Energy.

- Strategic Focus: Smart grid modernization, sustainable energy solutions, electric vehicle charging infrastructure, and digital energy management to support the country’s low-carbon transition.

Sembcorp Industries

Sembcorp Industries is Singapore's most strategically important listed energy company. As a leading renewables player, Sembcorp are driving the global energy transition with a diversified portfolio, spanning wind, solar, hydro and energy storage.

- Portfolio: Wind, Solar, Hydro, Energy Storage Systems

- Recent Developments: In October 2025, Sembcorp Industries launched two clean energy projects on Jurong Island.

- Strategic Focus: Accelerating renewable energy capacity, expanding low-carbon and gas-based power solutions, and driving the country’s energy transition through sustainable infrastructure, smart energy systems, and regional clean energy investments.

Market Concentration Analysis

Singapore's energy market exhibits structural concentration by design in the natural monopoly transmission and distribution segment, alongside competitive dynamics in power generation and fragmented retail competition. The Genco concentration reflects the high capital barriers to CCGT entry rather than anti-competitive behavior, as EMA's vesting contract and competitive bidding systems ensure generation price competition despite high concentration.

Renewable energy concentration is lower but rapidly shifting, and new entrants are competing aggressively for new corporate mandates. EV charging concentration is similarly concentrated, with SP Mobility holding 40-50% of the public charging market share. Market concentration will evolve through 2034 as the renewable energy and EV charging segments grow faster than the mature Genco market, projected renewable concentration reducing to 40-50% for the top 2 players as international developers establish Singapore renewable portfolios, while Genco market share distribution remains stable absent major new plant construction.

Investment & Growth Opportunities

Fastest Growing Segments

Renewables (~12.4% CAGR), electric power application (~7.8% CAGR), hydrogen import infrastructure (~30%+ CAGR from zero base post-2027), offshore floating solar (~25%+ CAGR from small base), and EV charging energy services (~20%+ CAGR embedded within transport application) represent Singapore's highest-growth energy market investment vectors through 2034. Cross-border renewable power import represents the single most transformational market development, potentially tripling Singapore's effective renewable capacity and creating new energy trading and transmission infrastructure markets.

Emerging Market Opportunities

Singapore's energy storage market represents the most structurally underserved segment relative to the market's requirements. The gap between the current 300 MWh deployed and the 2,000-4,000 MWh required by 2030 represents a storage infrastructure investment opportunity for BESS developers and project financiers seeking Singapore's EMA-backed deployment program incentives.

Investment Themes

- Singapore as ASEAN hydrogen import and distribution hub: Singapore's unique combination of LNG terminal infrastructure, chemical port handling capabilities at Jurong Island, and regional shipping network positions it as the natural hydrogen import hub for Southeast Asia.

- Singapore Building Energy Management as a Service: Singapore's smart meters, 4G/LTE IoT coverage, and BCA Green Mark mandatory upgrade requirements create a high-demand market for energy management SaaS, demand response aggregation, and Building Energy Management Systems (BEMS) services.

Future Market Outlook (2026-2034)

The Singapore energy market is projected to grow from USD 77.5 Million in 2025 to USD 150.7 Million by 2034, delivering a 7.52% CAGR over the forecast period. The market's anchor value of USD 111.3 Million in 2030 represents a Singapore energy landscape at a pivotal transition point, where the proportion of renewable energy in Singapore's grid has grown through the combination of domestic solar (2 GWp target), cross-border ASEAN renewable imports, and demand response resources reducing peak demand growth, fundamentally beginning to alter the gas-dominated energy mix that has characterized Singapore since the 1980s.

Three structural forces define Singapore's energy market growth through 2034 with high confidence: Singapore's digital economy expansion creates technology-driven demand growth that is decoupled from GDP growth and insensitive to economic cycles; Singapore's energy transition capital investment sustains 7-8% CAGR market growth through capital expenditure multiplier effects; and Singapore's hydrogen economy commercialization entering its active investment phase (2027-2030) as import supply chains from Australia, Chile, and the Middle East establish commercial viability, creating new energy infrastructure markets in import terminal, storage, distribution, and hydrogen-blended generation.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including senior executives from SP Group (Corporate Planning and Innovation divisions), Sembcorp Industries (Singapore Utilities and Renewable Energy teams), EMA (Licensing and Market Development divisions), EDB (Energy and Chemicals cluster), JTC Corporation (Jurong Island Management), and key Genco operational directors; Singapore energy management heads; IMDA data center sustainability team; and enterprise energy managers from major Singapore commercial real estate operators and industrial facilities.

Secondary Research

Secondary research encompassed EMA's Singapore Energy Statistics 2025 Annual Edition, EMA's Energy Transition Masterplan 2022, Singapore Green Plan 2030 official documents and progress reports, BCA Green Building Masterplan 2030, SP Group Annual Report FY2025, Sembcorp Industries Annual Report FY2024, EMA's National Electricity Market of Singapore (NEMS) monthly market reports, SLNG Corporation annual capacity reports, Ministry of Sustainability and the Environment (MSE) carbon tax implementation reports, Singapore's Long-Term Low-Emissions Development Strategy (LEDS), UNFCCC Singapore NDC update documents, and ASEAN Centre for Energy cross-border power grid reports. Over 80 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up energy type and application models calibrated against EMA's Singapore Energy Statistics volume data (2020-2025), Singapore electricity tariff evolution projections based on LNG price forecasts, renewable energy premium pricing trajectories, carbon tax escalation schedule, data center energy demand projections from IMDA's Data Center Sustainability Roadmap, and EV energy demand from LTA's Electric Vehicle Growth projections. Key inputs include EMA's 2 GWp solar target timeline, LTMS cross-border power import commissioning schedule, SMR feasibility study outcome scenarios, and natural gas pipeline renewal negotiations with Malaysia and Indonesia.

Singapore Energy Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Coal, Oil, Gas, Renewables, Nuclear |

| Applications Covered | Industry, Transport, Electric Power, Agricultural, Others |

| Regions Covered | North-East, Central, West, East, North |

| Companies Covered | SP Group, Sembcorp Industries, Keppel, Shell plc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Singapore energy market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Singapore energy market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Singapore energy industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Singapore Energy Market Report

The Singapore energy market reached USD 77.5 Million in 2025, driven by Singapore's Green Plan 2030 investment requirements, data center digital economy power surge, LNG hub expansion at the Singapore LNG Terminal, Open Electricity Market competition generating retail electricity innovation, and Singapore's position as ASEAN's energy transition laboratory and financial hub.

The market grows at 7.52% CAGR during 2026-2034, reaching USD 150.7 Million by 2034, driven by cross-border renewable power import activation, hydrogen economy commercialization, data center demand growth, EV charging infrastructure expansion, and Singapore's energy transition capital investment program through 2030.

Gas leads at 72.6% as Singapore's near-exclusive power generation fuel through CCGT plants at SLNG Terminal-supplied combined cycle generators.

Electric power leads at 52.3%, growing at ~7.8% CAGR from data center power demand, EV charging, and Singapore's premium electricity tariff structure.

Central Singapore leads at 28.7%, anchored by Marina Bay Financial Centre, CBD Grade A offices consuming 250-400 kWh/sq.m./year, and data center clusters in the Queenstown-Alexandra area.

Leading companies include SP Group, Sembcorp Industries, Keppel, and Shell plc, among others.

The market is projected to reach approximately USD 111.3 Million by 2030, with renewables reaching 15-20% of Singapore's electricity mix, cross-border ASEAN power imports activating, hydrogen pilot power generation, data centers growth, EV fleet, and Singapore achieving its Green Plan 2030 energy targets.

Singapore's 728 sq.km. restricts solar to a maximum 4 GWp technical potential (rooftops, water bodies, offshore) against 8 GW peak demand. This forces Singapore's EMA to pursue the Four Switches strategy, maximizing domestic solar, pursuing ASEAN cross-border power imports, researching SMR nuclear, and developing hydrogen import supply chains, creating a diversified investment program that sustains 7.52% energy market CAGR.

Three priority opportunities: cross-border renewable HVDC cable financing; building energy management as a service; and hydrogen import terminal infrastructure, capitalizing on Singapore's natural hub position as ASEAN's first commercial hydrogen import center.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)