Smart Bed Market Size, Share, Trends and Forecast by Type, End Use, Distribution Channel, and Region, 2026-2034

Global Smart Bed Market Size, Share, Trends & Forecast (2026-2034)

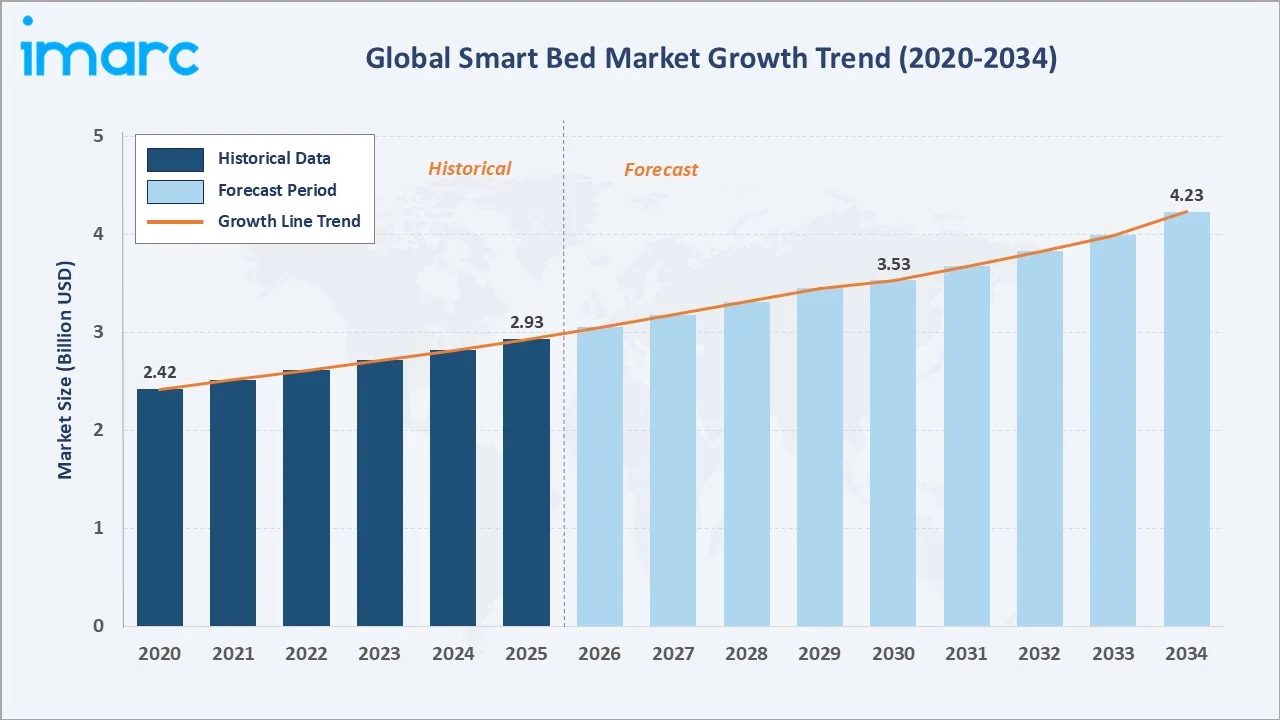

The global smart bed market size reached USD 2.93 Billion in 2025 and is projected to reach USD 4.23 Billion by 2034, exhibiting a CAGR of 3.83% during 2026-2034. Rising prevalence of sleep disorders, growing IoT and AI integration in healthcare and residential beds, and increasing demand from aging populations are the primary forces driving market growth.

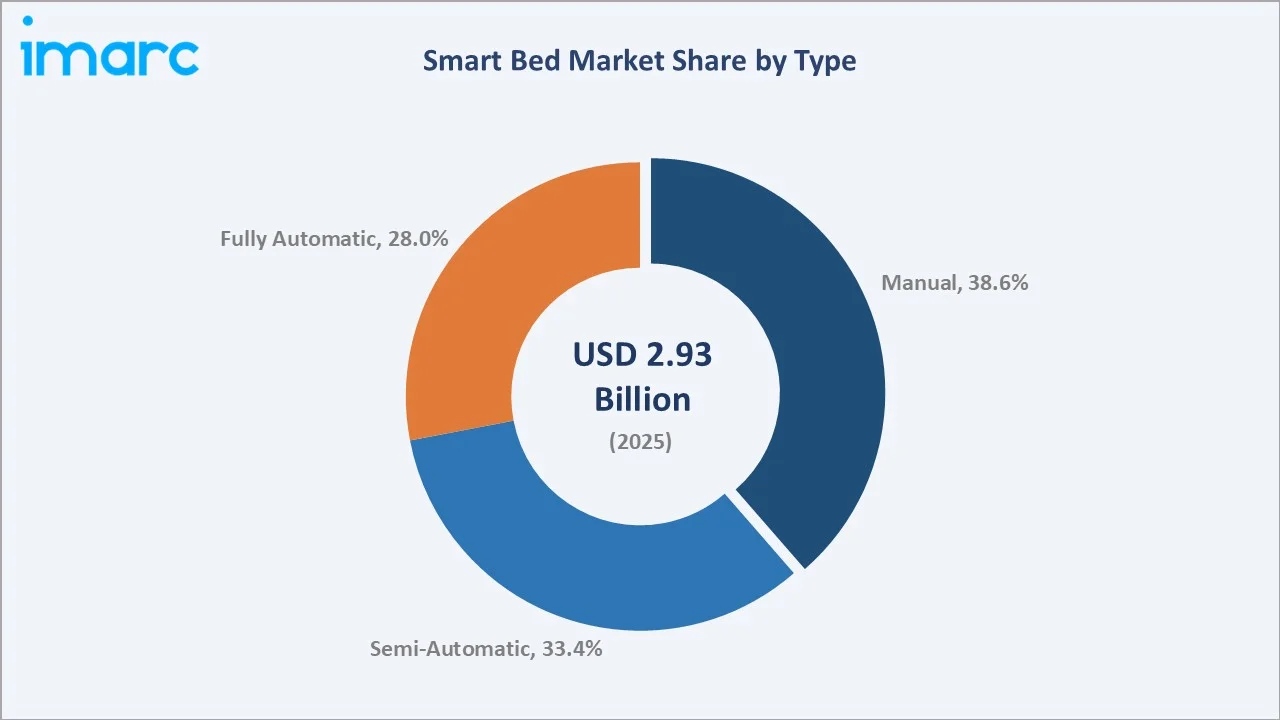

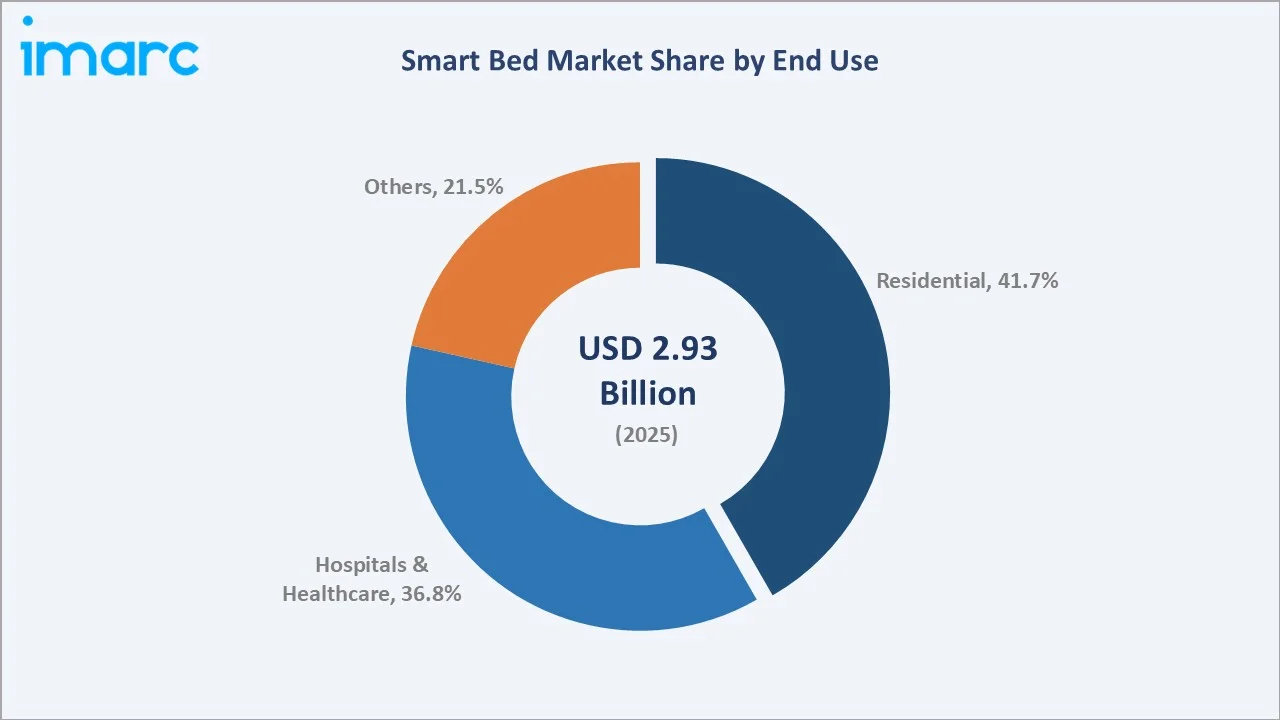

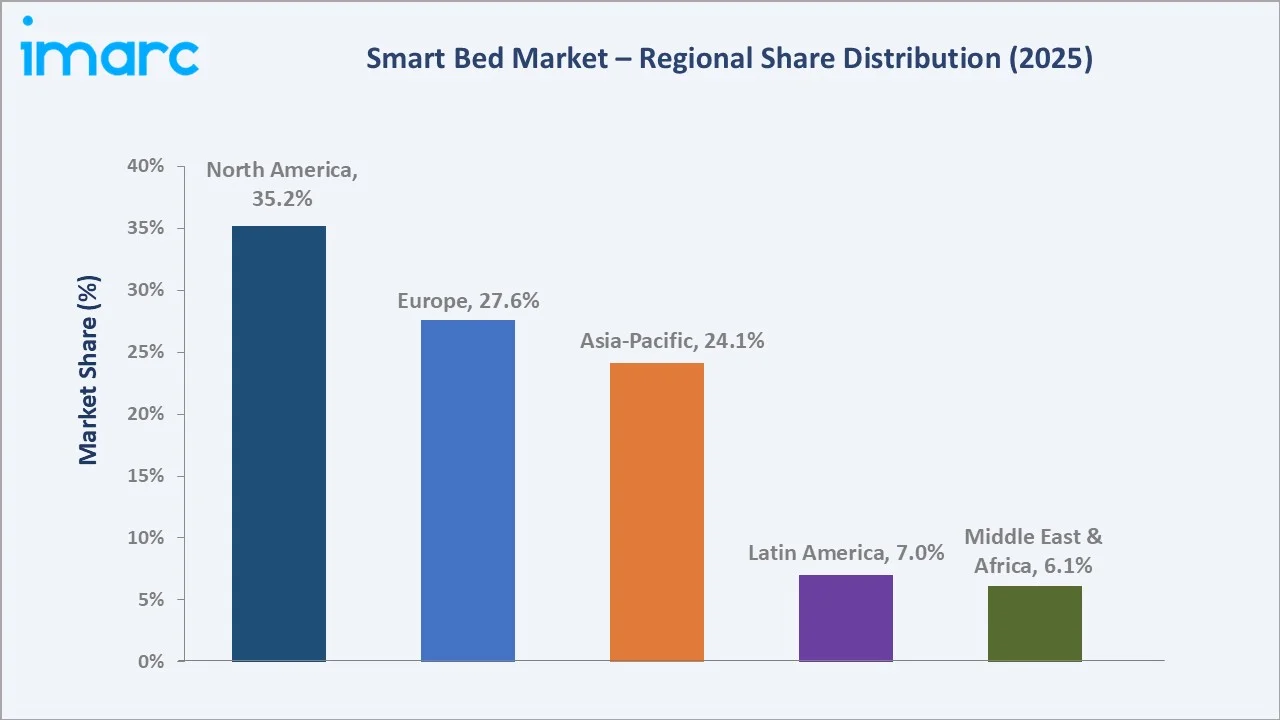

Manual beds dominate the type mix at 38.6% in 2025, while residential end use leads at 41.7%. North America commands a dominant 35.2% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.93 Billion |

|

Forecast Market Size (2034) |

USD 4.23 Billion |

|

CAGR (2026-2034) |

3.83% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (35.2% share, 2025) |

|

Second Largest Region |

Europe (27.6% share, 2025) |

|

Leading Type Segment |

Manual (38.6%, 2025) |

|

Leading End Use |

Residential (41.7%, 2025) |

The global smart bed market growth trajectory from 2020 through 2034, with the historical expansion to USD 2.93 Billion in 2025, reflects consistent demand driven by healthcare infrastructure investment and residential wellness adoption, while the forecast to USD 4.23 Billion captures accelerating technology integration and aging population dynamics.

To get more information on this market, Request Sample

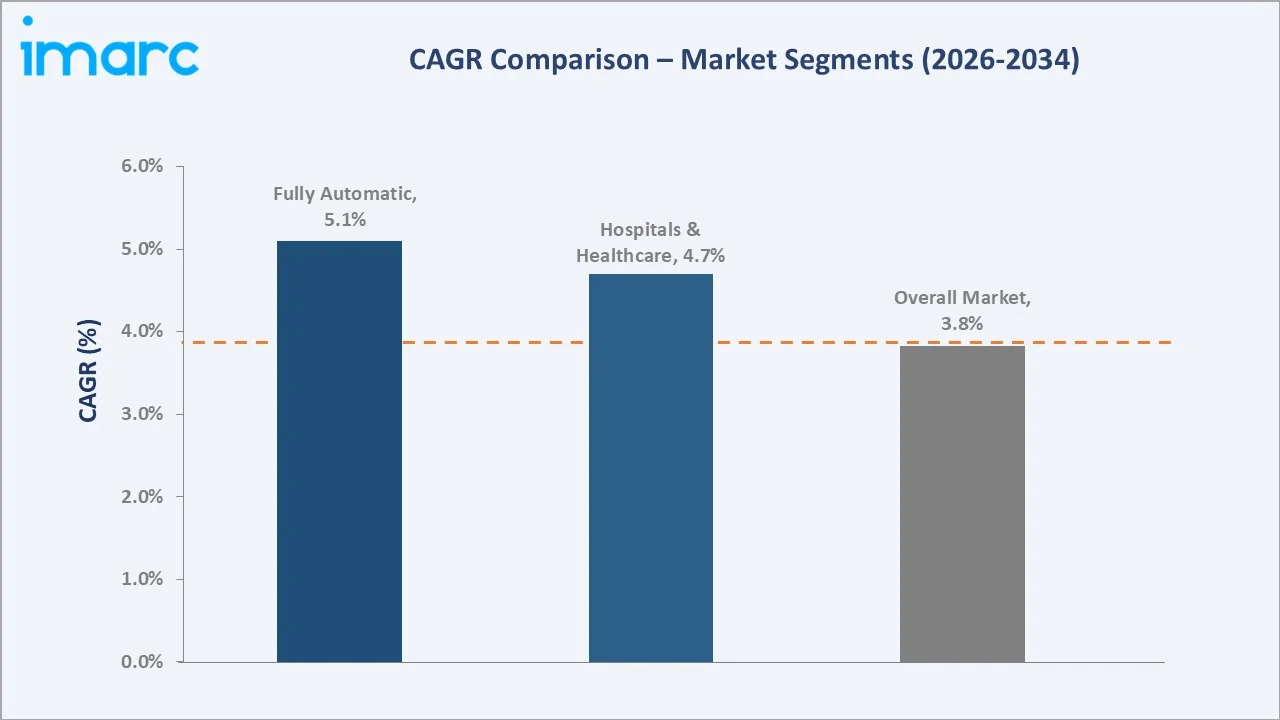

The CAGR trajectories across key type and end-use sub-segments, with Fully Automatic beds at ~5.1% CAGR and Hospitals & Healthcare end use at ~4.7% CAGR, are the fastest-growing categories within the global smart bed industry analysis through 2034.

Executive Summary

The global smart bed market is on a sustained growth trajectory from USD 2.93 Billion in 2025 to USD 4.23 Billion by 2034. Smart beds integrating adjustable positioning, sleep-tracking sensors, pressure management, and IoT connectivity address non-discretionary needs across clinical and residential settings, benefiting from aging demographics and rising sleep health awareness.

Manual smart beds dominate the type mix at 38.6% in 2025, benefiting from affordability and broad hospital specification requirements. Semi-Automatic beds (33.4%) are gaining traction in long-term care and premium residential segments. Fully Automatic smart beds (28.0%) command the highest ASP and fastest CAGR, driven by ICU technology upgrades and smart home integration.

North America leads at 35.2% in 2025, reflecting high healthcare expenditure and early adoption of connected wellness devices. Europe (27.6%) follows, driven by hospital modernization and aging population investment. Asia-Pacific (24.1%) is the fastest-growing region, fueled by expanding hospital infrastructure in China, Japan, and Southeast Asia.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Manual – 38.6% share (2025) |

|

Leading End Use |

Residential – 41.7% share (2025) |

|

Leading Region |

North America – 35.2% share (2025) |

|

Second Largest Region |

Europe – 27.6% share (2025) |

|

Top Companies |

Arjo, Reverie Sleep, IOF srl, Baxter, Invacare International Holdings Corp., Paramount Bed Co. Ltd., Sleep Number Corporation, Stryker |

- Manual beds, at 38.6% in 2025, dominate because of established hospital procurement preference and cost-effective positioning for large-volume institutional purchasing cycles.

- Residential end use, at 41.7% in 2025, leads as consumer awareness of sleep health rises and smart home ecosystems enable seamless integration of adjustable, sensor-equipped sleep platforms.

- North America's 35.2% dominance reflects the world's highest per-capita healthcare spending, strong sleep technology consumer adoption, and a robust network of acute care and home healthcare facilities upgrading to connected bed solutions.

- Europe at 27.6% benefits from government-funded hospital infrastructure renewal and robust reimbursement frameworks for assistive medical equipment and high elderly care facility density.

Global Smart Bed Market Overview

Smart beds are advanced sleep and care platforms integrating mechanical, electronic, and software systems to provide adjustable positioning, biometric monitoring, pressure redistribution, and connectivity to clinical information or smart home systems. Product configurations range from basic electrically adjustable frames to fully AI-driven platforms with continuous vital sign monitoring and automated comfort adjustment.

The global ecosystem spans component manufacturers, bed assembly specialists, software developers, distribution networks, and end-use sectors including acute hospitals, long-term care, rehabilitation centers, and premium residential consumers. Clinical-grade smart beds address patient safety, fall prevention, and workflow efficiency, while residential variants focus on personalized comfort, sleep quality, and health monitoring.

Market Dynamics

To evaluate market opportunities, Request Sample

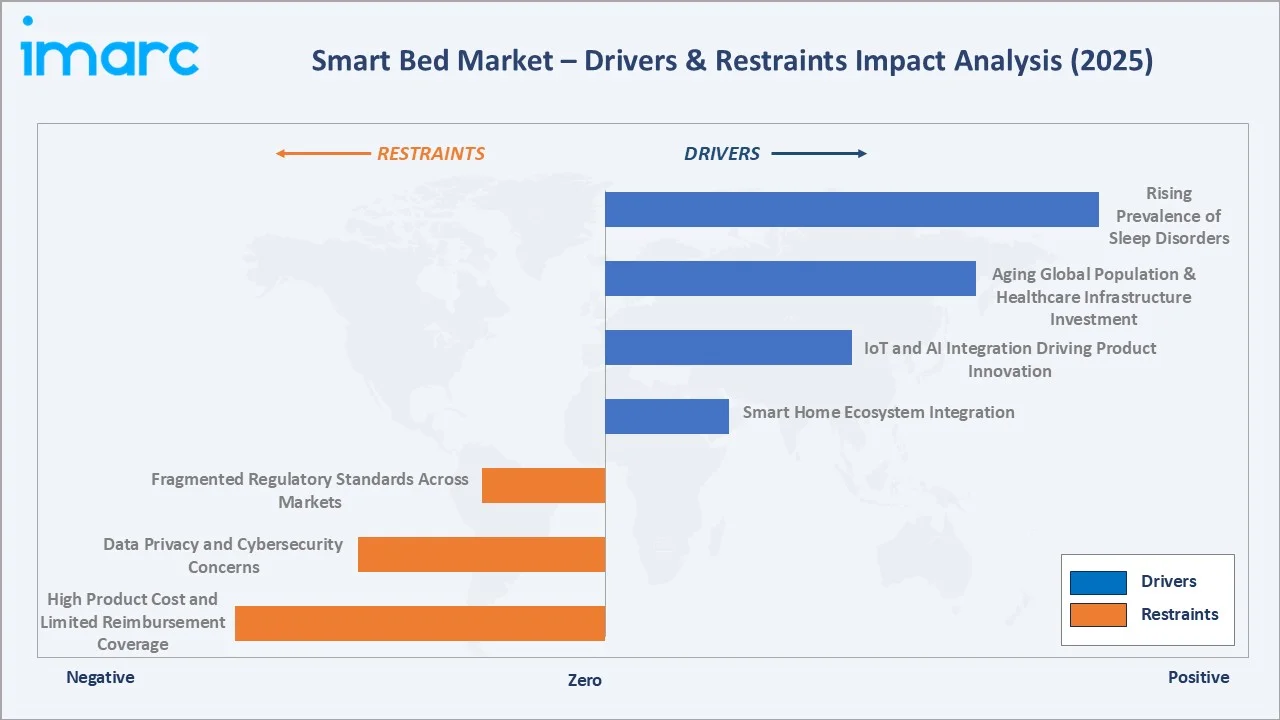

Market Drivers

- Rising Prevalence of Sleep Disorders: The American Sleep Association estimates 50–70 million US adults suffer from sleep disorders. Smart beds with biometric feedback and automated adjustments directly address insomnia, sleep apnea, and restless leg syndrome across consumer and clinical populations.

- Aging Global Population and Healthcare Infrastructure Investment: The global population aged 65+ is projected to reach 1.6 billion by 2050, increasing demand for advanced healthcare solutions and long-term care services. Healthcare providers are increasingly adopting smart and connected equipment to improve patient monitoring, safety, and overall care quality. This shift is also driving investments in modernizing healthcare infrastructure and integrating technology-enabled solutions to enhance operational efficiency and patient outcomes.

- IoT and AI Integration Driving Product Innovation: Falling sensor costs and mature wireless connectivity protocols enable feature-rich smart beds at accessible price points, expanding the addressable market beyond premium tiers into mid-range residential and care home segments.

Market Restraints

- High Product Cost and Limited Reimbursement Coverage: Advanced smart beds and technology-enabled care solutions often involve significant upfront investment, which can limit adoption among cost-sensitive healthcare providers and individual consumers. Limited or inconsistent reimbursement policies further restrict accessibility, making it challenging for facilities to justify large-scale deployment. As a result, cost considerations and funding constraints remain key barriers to wider market penetration.

- Data Privacy and Cybersecurity Concerns: Continuous biometric data collection through connected smart beds raises significant GDPR, HIPAA, and consumer privacy concerns, requiring costly compliance frameworks and regulatory certifications from manufacturers globally.

Market Opportunities

- Smart Home Ecosystem Integration: Growing penetration of smart home platforms creates pull-through demand for compatible smart beds capable of automating lighting, temperature, and alarms based on sleep-stage detection, expanding addressable market to tech-forward consumers. In 2024, 69.91 million of U.S. households were actively using smart home devices. This number is projected to rise to 103 million by 2028, thereby increasing the demand of smart beds across the world.

- Emerging Market Hospital Modernization: Government-funded hospital construction across India, Southeast Asia, and the GCC region represents a large greenfield opportunity for clinical-grade smart bed suppliers targeting first-time infrastructure investment cycles.

Market Challenges

- Fragmented Regulatory Standards Across Markets: Divergent medical device classification requirements across FDA, EU MDR, and PMDA increase compliance costs and time-to-market for international expansion, particularly for fully integrated biometric monitoring platforms.

- Consumer Education Gap and Technology Skepticism: A significant share of target residential consumers remains unfamiliar with smart bed capabilities, requiring substantial marketing investment to demonstrate ROI versus conventional premium mattresses and adjustable bases.

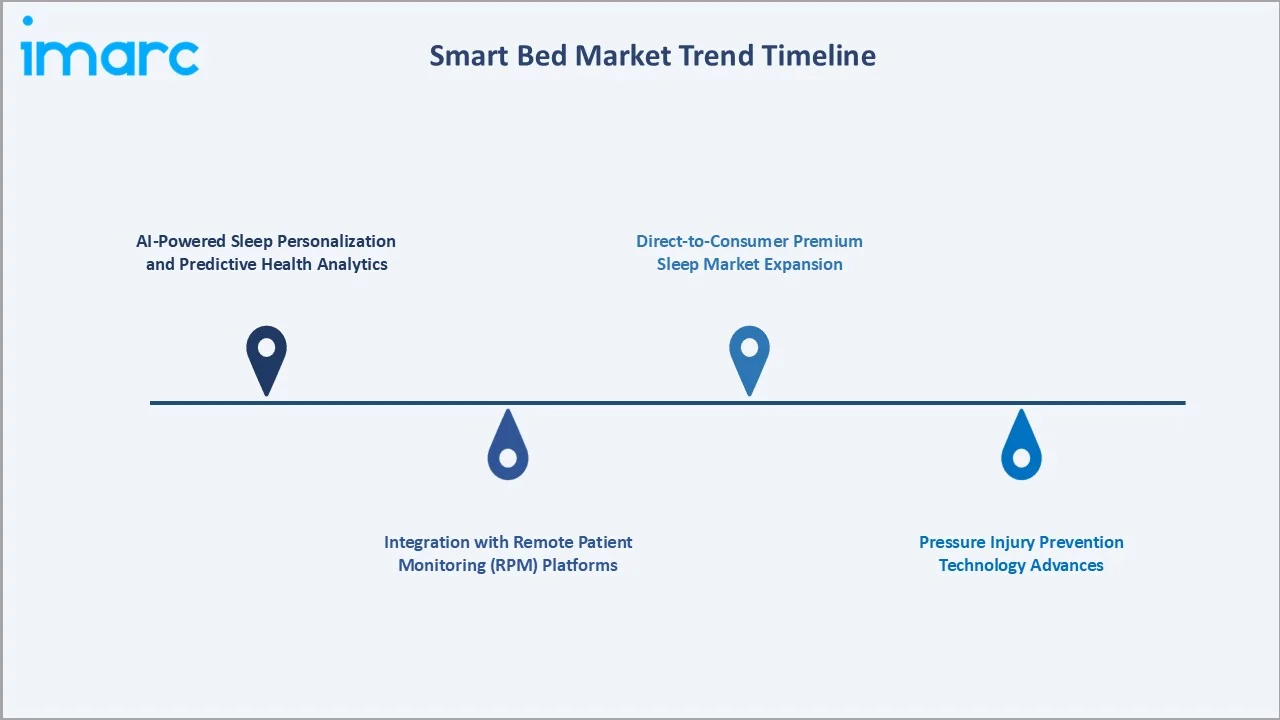

Emerging Market Trends

1. AI-Powered Sleep Personalization and Predictive Health Analytics

Machine learning algorithms processing continuous biometric data from bed sensors are enabling predictive health insights, detecting early cardiovascular and respiratory anomalies, and providing personalized sleep coaching that transforms smart beds from comfort devices into preventive health platforms.

2. Integration with Remote Patient Monitoring (RPM) Platforms

Clinical smart beds are evolving into integrated RPM nodes, transmitting real-time patient data to EHR systems and nursing stations, reducing manual observation rounds and enabling earlier clinical intervention in hospital and long-term care settings.

3. Pressure Injury Prevention Technology Advances

Advanced alternating pressure and microclimate management systems embedded in smart bed mattresses are demonstrating measurable reductions in hospital-acquired pressure injury (HAPI) rates, generating strong clinical evidence that supports procurement justification in acute and post-acute care settings.

4. Direct-to-Consumer Premium Sleep Market Expansion

Celebrity endorsements, sleep influencer marketing, and clinical validation partnerships are driving mass-market awareness of residential smart bed benefits, with DTC brands leveraging subscription coaching models to build recurring revenue streams alongside hardware sales.

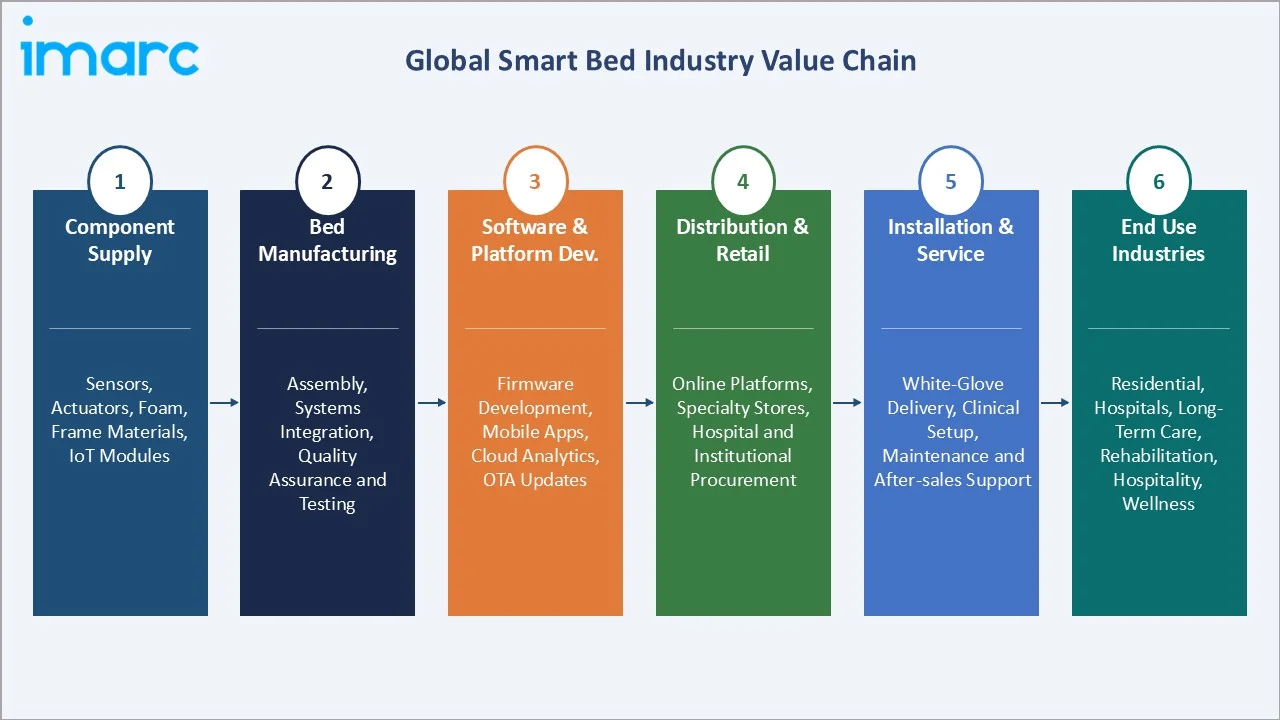

Industry Value Chain Analysis

The smart bed value chain spans six stages from component sourcing through end-use deployment. Technology integration and software development capture the highest value-add margins, while distribution and clinical installation generate significant service revenue in institutional segments. Integrated manufacturers with in-house sensor development and cloud platform capabilities achieve stronger competitive positioning than pure hardware assemblers.

|

Stage |

Key Examples |

|

Component Supply |

Sensors, actuators, foam, frame materials, IoT modules |

|

Bed Manufacturing |

Assembly, systems integration, quality assurance and testing |

|

Software & Platform Dev. |

Firmware development, mobile apps, cloud analytics, OTA updates |

|

Distribution & Retail |

Online platforms, specialty stores, hospital and institutional procurement |

|

Installation & Service |

White-glove delivery, clinical setup, maintenance and after-sales support |

|

End Use Industries |

Residential, hospitals, long-term care, rehabilitation, hospitality, wellness |

Manufacturers that vertically integrate sensor development, firmware, and cloud analytics alongside physical bed assembly achieve significant competitive advantages over pure hardware assemblers reliant on third-party platforms. Distribution and clinical installation represent the fastest-evolving value chain stages, with online DTC channels disrupting traditional specialty retail in the residential segment while hospital group purchasing organizations continue to consolidate procurement leverage in the clinical channel.

Technology Landscape in the Smart Bed Industry

Sensor and Biometric Monitoring Technology

Piezoelectric pressure sensors, ballistocardiography (BCG) sensors, and capacitive mat arrays embedded in smart bed surfaces enable contactless vital sign monitoring with clinical-grade accuracy. BCG-based heart rate measurement achieves accuracy comparable to wrist-worn consumer wearables, enabling non-contact nightly health screening for both residential and clinical applications.

Actuator Systems: Linear and Pneumatic Adjustment Mechanisms

Precision linear actuators in adjustable bed bases enable programmable head, foot, and lumbar positioning with sub-degree angular precision. Dual-zone pneumatic air chamber systems enable independent partner comfort adjustment, one of the most commercially successful residential smart bed differentiators globally, driving significant volume in the premium residential segment.

Cloud Platform and Data Analytics Infrastructure

HIPAA-compliant cloud platforms aggregating multi-night sleep data enable longitudinal trend analysis, population health benchmarking, and machine learning model training for next-generation predictive health features. OTA firmware updates continuously improve product capabilities post-purchase, extending product lifecycle value and deepening customer engagement over time.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | Manual | 38.6% |

2025 |

| End Use | Residential |

41.7% |

2025 |

| Distribution Channel | Specialty Stores |

🔒 |

2025 |

|

Region |

North America |

35.2% |

2025 |

By Type

Manual smart beds command a 38.6% majority share in 2025, reflecting their established position in hospital procurement and home healthcare settings where ease of operation and cost-efficiency are prioritized. Manual adjustability via wired remotes satisfies core clinical and budget-conscious residential requirements effectively across diverse institutional and consumer applications.

To access detailed market analysis, Request Sample

Semi-Automatic smart beds at 33.4% in 2025 are gaining share through motorized positioning capabilities that improve caregiver ergonomics and patient comfort in long-term care settings. Fully Automatic smart beds (28.0%) command the highest ASP and fastest CAGR, integrating continuous monitoring, automated adjustment, and app connectivity for premium applications.

By End Use

Residential end use leads at 41.7% in 2025, driven by rising consumer awareness of sleep health, growing smart home ecosystem adoption, and increased willingness to invest in premium wellness products. DTC brands and established furniture retailers are expanding smart bed assortments to meet demand across multiple price tiers in North America and Europe.

Hospitals and healthcare at 36.8% in 2025 represents the highest value-per-unit segment, with clinical smart beds priced at USD 5,000–USD 20,000 and specified for patient safety, pressure injury prevention, and nurse workflow optimization. The Others segment (21.5%) includes long-term care, rehabilitation, hospitality, and specialty wellness applications globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

35.2% |

High healthcare expenditure; aging demographics; strong consumer wellness adoption |

|

Europe |

27.6% |

Aging population; hospital modernization; robust reimbursement frameworks |

|

Asia-Pacific |

24.1% |

Expanding hospital infrastructure; rising middle class; growing sleep awareness |

|

Latin America |

7.0% |

Growing healthcare investment; urban hospital construction; wellness spending |

|

Middle East & Africa |

6.1% |

Hospital infrastructure development; medical tourism; increasing healthcare budgets |

North America's 35.2% dominance in 2025 is underpinned by the world's highest healthcare expenditure per capita, strong consumer spending on sleep health and wellness, and a mature acute care infrastructure requiring continuous technology refreshment. Sleep Number Corporation leads in the residential segment while Stryker and Hill-Rom dominate the clinical channel.

Europe, with 27.6% in 2025, benefits from robust public healthcare funding, comprehensive medical device reimbursement frameworks, and a large elderly population generating persistent demand for smart pressure-care beds.

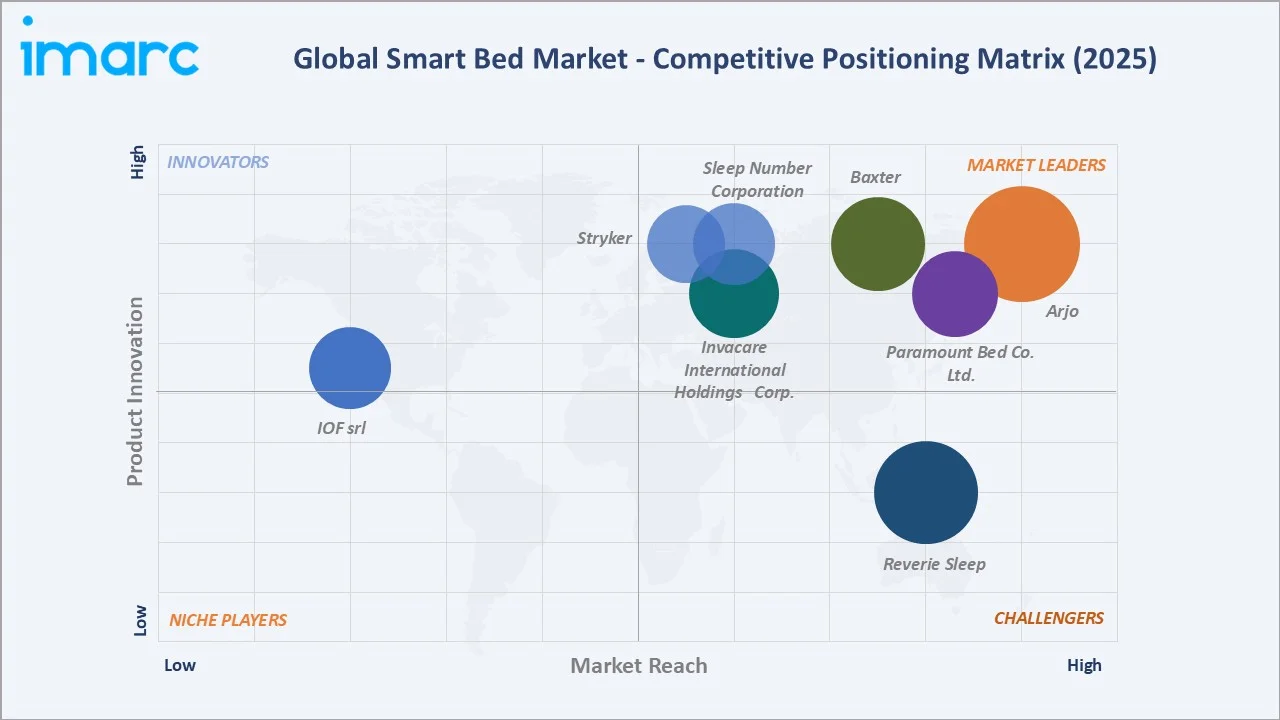

Competitive Landscape

The global smart bed market is moderately fragmented, with distinct competitive ecosystems in the clinical and residential segments. Clinical smart beds are dominated by large medical device companies with established hospital relationships, while residential smart beds feature both specialist sleep technology companies and consumer electronics-adjacent challengers.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Arjo |

Hospital beds, patient handling systems |

Leader |

EMEA & global; clinical patient care |

|

Reverie Sleep |

Adjustable bed bases, lifestyle beds |

Challenger |

North America; residential premium |

|

IOF srl |

HiAm, IoT sleep monitoring |

Emerging |

Europe; hospitality & premium residential |

|

Baxter |

Smart hospital beds, nurse-call integration |

Leader |

North America & global; acute care |

|

Invacare International Holdings Corp. |

Home care beds, medical beds |

Leader |

North America & Europe; home healthcare |

|

Paramount Bed Co. Ltd. |

Electric nursing beds, ICU smart beds |

Leader |

Asia-Pacific; hospital & care market |

|

Sleep Number Corporation |

Sleep Number beds, SleepIQ technology |

Leader |

North America; residential smart beds |

|

Stryker |

ProCuity ICU bed, hospital smart beds |

Leader |

North America & global; acute hospital |

Key players include Arjo, Reverie Sleep, IOF srl, Baxter, Invacare International Holdings Corp., Paramount Bed Co. Ltd., Sleep Number Corporation, Stryker, and others.

Key Company Profiles

Sleep Number Corporation

Sleep Number Corporation is the leading US residential smart bed company headquartered in Minneapolis, Minnesota. Its SleepIQ technology platform continuously tracks sleep biometrics and adjusts air chamber firmness to maintain optimal sleep conditions for each partner.

- Product Portfolio: Sleep Number 360 smart beds, SleepIQ platform, smart adjustable bases, sleep accessories.

- Recent Developments: In October 2024, Sleep Number Corporation introduced its new ClimateCool smart bed, designed to actively regulate temperature and automatically adjust to individual sleep preferences for improved comfort. The bed uses advanced airflow technology to draw heat away from the body, helping maintain an optimal sleeping environment throughout the night.

- Strategic Focus: Sleep Number's strategy deepens the recurring revenue model through SleepIQ subscription coaching services alongside hardware sales, while expanding product range downward in price to capture broader consumer demographics across the premium and mid-market segments.

Stryker

Stryker is one of the world's largest medical technology companies, with its Patient Handling division producing leading clinical smart beds for acute care hospitals. Its InTouch Critical Care bed integrates vital sign monitoring with EHR connectivity.

- Product Portfolio: ProCuity wireless bed, Secure II Medical-Surgical Bed, Zoom Drive mobility system.

- Recent Developments: In October 2020, Stryker Corporation introduced a smart hospital bed, ProCuity, designed to enhance patient safety, improve caregiver efficiency, and reduce operational costs. The bed integrates wireless connectivity and advanced monitoring features, allowing healthcare staff to track patient movement and bed status in real time without relying on manual checks.

- Strategic Focus: Stryker's smart bed strategy centers on deepening EHR integration and expanding clinical workflow optimization capabilities, positioning beds as connected nodes within hospital digital infrastructure rather than standalone products in the acute care setting.

Baxter

Baxter is a global leader in connected hospital infrastructure, including smart beds, patient lifts, and clinical communication systems. Its Centrella Smart+ bed is widely specified in US acute care facilities.

- Product Portfolio: Centrella Smart+ Bed, Progressa+ TRUE ICU Hospital Bed, TotalCare Bed, VersaCare bed system.

- Recent Developments: In December 2021, Baxter International completed its acquisition of Hillrom, creating a leading global medtech company with a significantly expanded portfolio across connected care and medical technologies. From a smart bed perspective, the deal is particularly strategic, as Hillrom is a key provider of smart hospital beds equipped with sensors and connectivity features that support real-time patient monitoring and safety.

- Strategic Focus: Hill-Rom's strategy leverages Baxter's global distribution to expand smart bed penetration in international hospital markets, particularly in Asia-Pacific and the Middle East where hospital infrastructure investment is accelerating across government-funded programmes.

Invacare International Holdings Corp.

Invacare is a leading global manufacturer of home medical equipment, including home care smart beds for the post-acute and long-term care markets, serving both institutional and individual consumer segments across more than 80 countries worldwide.

- Product Portfolio: Invacare Full-Electric Hospital Bed, Semi-Electric Series, Threshold mattress systems.

- Recent Developments: In September 2025, Invacare launched its new Accent medical profiling bed, designed to enhance comfort, independence, and daily care for users in both homecare and long-term care environments. The bed focuses on delivering a balance of affordability, safety, and functionality, making it accessible without compromising on quality.

- Strategic Focus: Invacare's strategy targets the high-volume home healthcare segment with reliable, cost-effective smart bed platforms and growing IoT connectivity for remote monitoring by home health agencies and family caregivers managing post-acute and chronic care patients at home.

Market Concentration Analysis

The global smart bed market exhibits moderate fragmentation at the global level, with distinct concentration patterns across clinical and residential sub-markets. No single company holds more than 12–15% of total global market revenue, reflecting the market's bifurcated structure across healthcare and consumer distribution channels globally.

Clinical-segment concentration is higher, with Stryker, Hill-Rom (Baxter), and Invacare collectively commanding an estimated 45–50% of hospital and long-term care smart bed revenue in North America and Europe. Residential-segment fragmentation is greater, with Sleep Number leading in the US but competing against numerous adjustable base and smart mattress brands.

Investment & Growth Opportunities

Fastest-Growing Segments

Fully Automatic smart beds at ~5.1% CAGR through 2034 represent the highest-growth type segment, driven by ICU technology refresh cycles and residential premium wellness adoption. Hospitals and Healthcare end use at ~4.7% CAGR captures the most valuable growth opportunity given clinical-grade ASPs exceeding USD 10,000 per unit across acute care procurement cycles.

Emerging Markets

Asia-Pacific at ~4.8% CAGR is the fastest-growing region through 2034. China's hospital construction program, India's Ayushman Bharat health infrastructure expansion, and Southeast Asia's rapidly expanding private hospital sector create large-scale procurement opportunities for both clinical and long-term care smart bed suppliers with localized product strategies.

Venture & Investment Trends

Digital health investment flowing into sleep technology startups is accelerating smart bed software innovation, with AI sleep coaching, continuous health monitoring, and RPM integration attracting venture capital. Strategic acquisition of biometric analytics companies by smart bed OEMs is an emerging consolidation trend defining next-generation product platforms.

Future Market Outlook (2026-2034)

The global smart bed market is forecast to expand from USD 2.93 Billion in 2025 to USD 4.23 Billion by 2034 at a CAGR of 3.83%, adding USD 1.30 Billion in incremental annual market value over the forecast period. This consistent growth reflects the market's healthcare-linked, non-discretionary demand characteristics combined with accelerating consumer wellness adoption.

Three technological forces will most significantly shape the smart bed industry through 2034. AI-powered predictive health analytics will transition smart beds from comfort devices to preventive health platforms. Seamless EHR integration will make clinical smart beds indispensable nodes in hospital digital infrastructure, strengthening installed base retention and switching costs.

The residential market will continue bifurcating between value-oriented DTC adjustable base brands and technology-forward premium platforms with comprehensive health monitoring capabilities. Subscription revenue models will become standard among leading residential brands, improving revenue visibility and deepening customer relationships beyond the initial hardware purchase.

Research Methodology

Primary Research

Primary research encompassed structured interviews with smart bed industry stakeholders including clinical procurement specialists, hospital facilities managers, sleep technology R&D leaders, home healthcare agency buyers, and retail category managers at leading mattress and furniture retailers. Primary data validated market sizing, segment shares, and technology adoption timelines across key regional markets.

Secondary Research

Key secondary sources include WHO Global Health Observatory sleep disorder data, American Sleep Association epidemiological studies, CMS hospital capital expenditure data, Consumer Electronics Association smart home adoption surveys, EUROSTAT elderly care facility statistics, and trade publications including Sleep Review, Medical Product Outsourcing, and Furniture Today.

Forecasting Models

Market size estimations and projections were derived using combined top-down and bottom-up forecasting models incorporating GDP growth rates, aging population indices, healthcare expenditure trajectories, technology adoption curves, and historical market evolution patterns. Scenario analysis was performed to account for macroeconomic uncertainty and regulatory changes.

Smart Bed Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Manual, Semi-Automatic, Fully Automatic |

| End Uses Covered | Hospitals and Healthcare, Residential, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Arjo, Reverie Sleep, IOF srl, Baxter, Invacare International Holdings Corp., Paramount Bed Co. Ltd., Sleep Number Corporation, Stryker, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the smart bed market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global smart bed market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the smart bed industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Smart Bed Market Report

The global smart bed market reached USD 2.93 Billion in 2025, reflecting consistent demand from healthcare infrastructure investment, aging population demographics, and growing residential sleep health awareness globally.

The market is projected to reach USD 4.23 Billion by 2034, growing at a CAGR of 3.83% during 2026-2034, driven by AI integration, aging population dynamics, hospital modernization, and smart home ecosystem adoption across residential and clinical segments.

Manual smart beds lead with 38.6% in 2025, valued for their established clinical procurement position, operational simplicity, and cost-effective pricing across hospital and home care settings.

Residential dominates at 41.7% in 2025, driven by consumer sleep health awareness, smart home integration, and DTC brand expansion across premium and mid-range price tiers globally.

North America commands 35.2% market share in 2025, driven by high healthcare expenditure, aging demographics, strong consumer wellness spending, and leadership positions of Sleep Number in residential and Stryker and Hill-Rom in the clinical bed segment.

Fully Automatic smart beds are the fastest-growing at ~5.1% CAGR through 2034, driven by ICU technology refresh demand and residential premium wellness adoption with AI-powered monitoring.

Leading companies include Arjo, Reverie Sleep, IOF srl, Baxter, Invacare International Holdings Corp., Paramount Bed Co. Ltd., Sleep Number Corporation, Stryker, and others.

Key applications include hospital acute care, intensive care units, long-term care and nursing homes, post-acute rehabilitation, home healthcare, and premium residential sleep health and wellness.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)