Smart Connected Pet Collar Market Size, Share, Trends and Forecast by Pet Type, Application, Sales Channel, and Region, 2026-2034

Smart Connected Pet Collar Market Size, Share, Trends & Forecast (2026-2034)

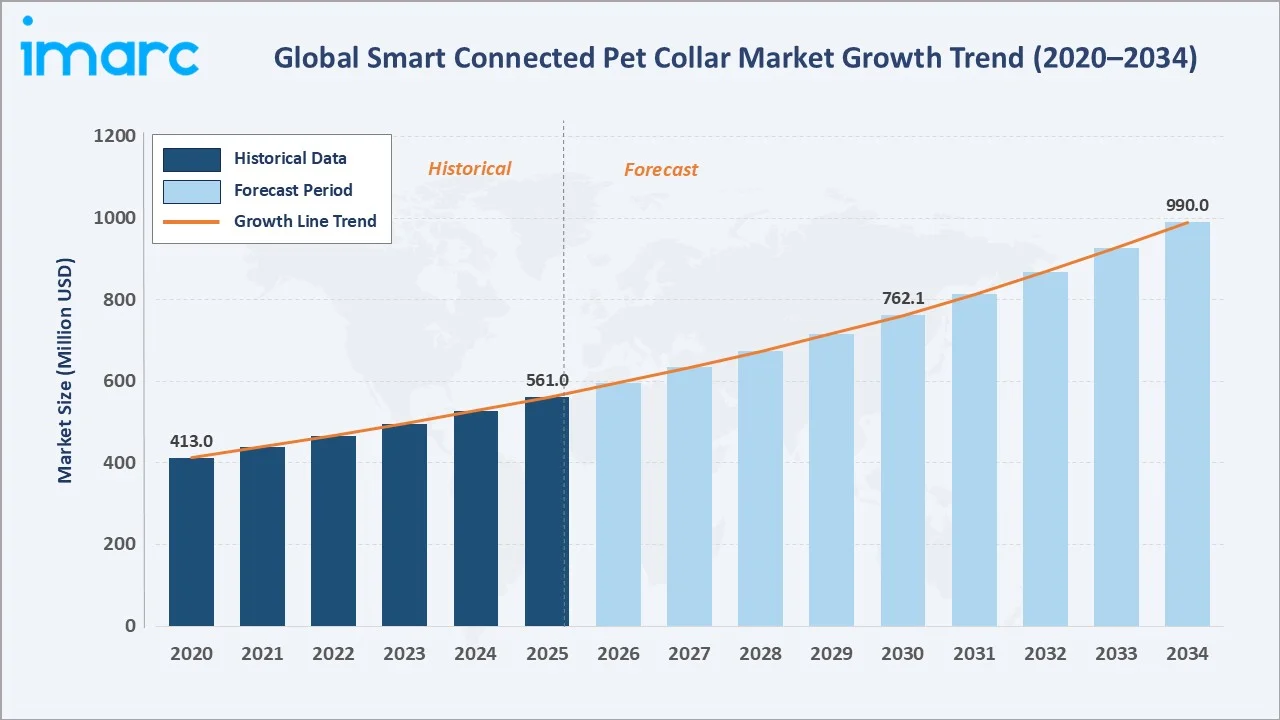

The global smart connected pet collar market reached USD 561.0 Million in 2025 and is projected to reach USD 990.0 Million by 2034, growing at a CAGR of 6.32% during 2026-2034. Rising pet ownership rates, growing concern for pet health and safety, and rapid technological advancements in IoT, GPS, and AI-driven health analytics are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 561.0 Million |

|

Forecast Market Size (2034) |

USD 990.0 Million |

|

CAGR (2026-2034) |

6.32% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.6% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

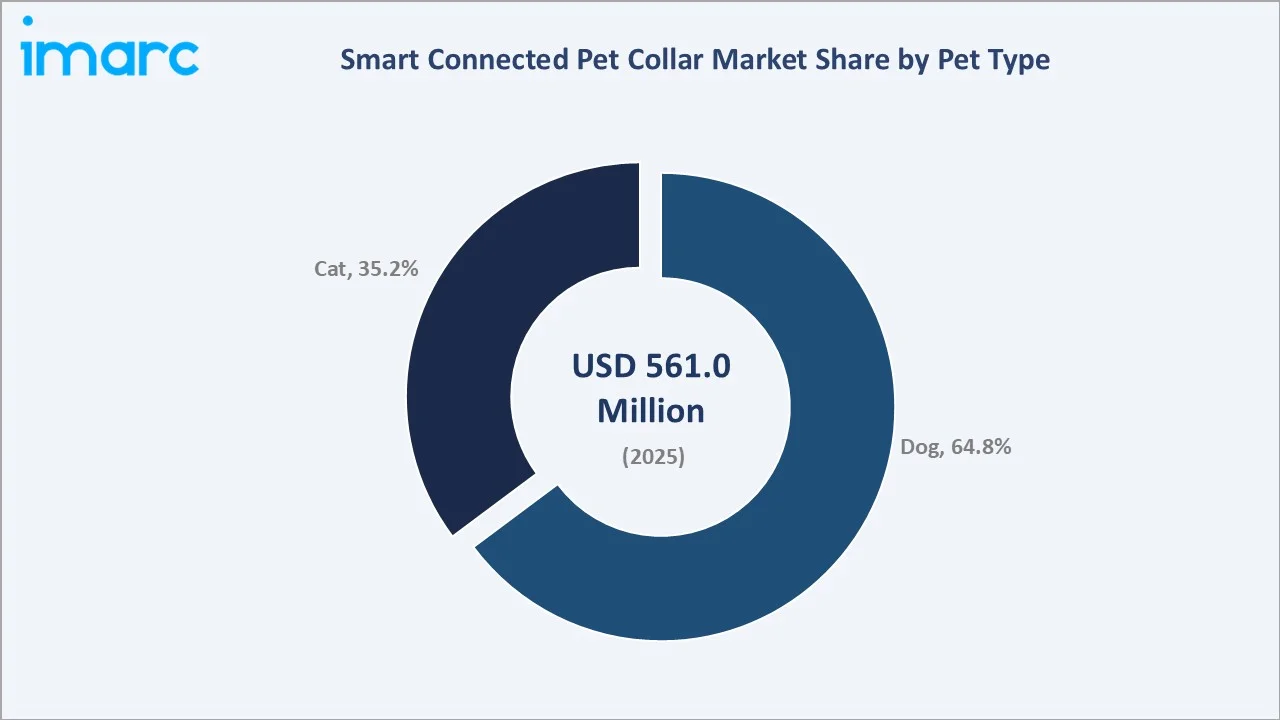

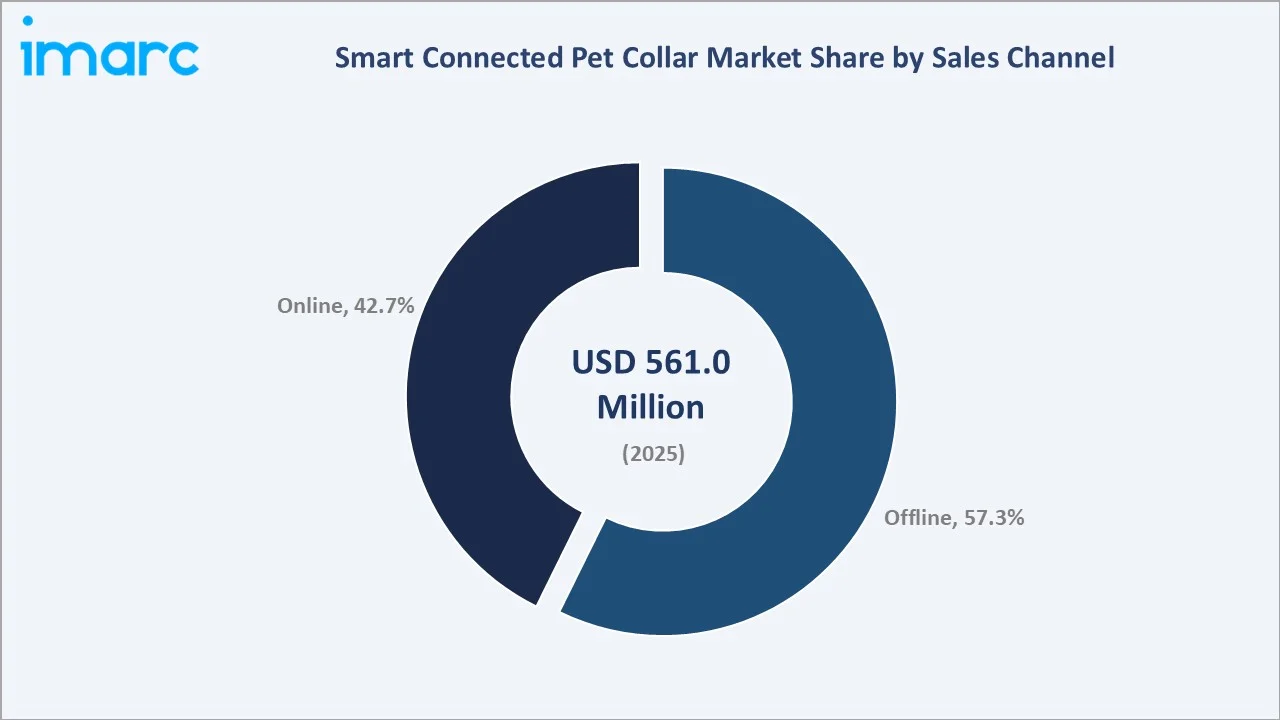

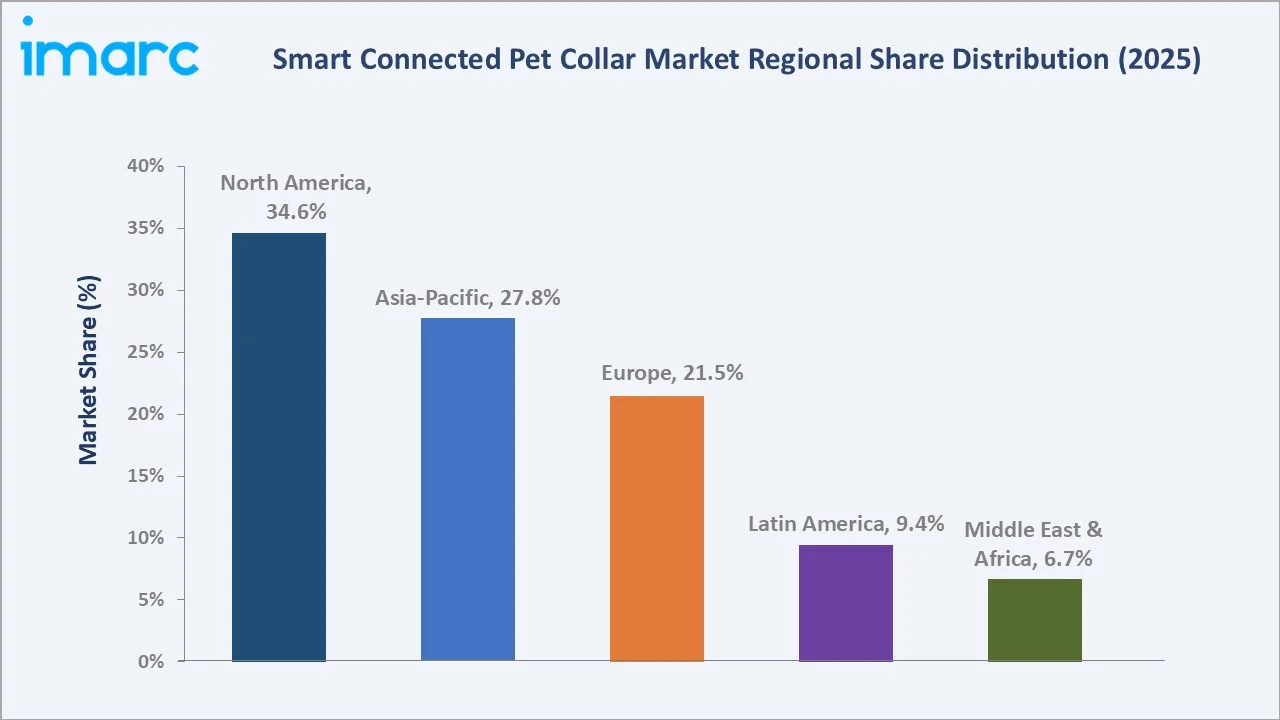

North America dominates, holding a 34.6% market share in 2025, while dogs represent the largest pet-type segment at 64.8%. Offline channels retain a 57.3% sales share. Smart connected pet collars integrate GPS location tracking, real-time activity monitoring, and biometric health sensors, making them indispensable tools for modern pet owners who regard their companions as family members.

To get more information on this market, Request Sample

With applications spanning GPS location monitoring, activity and health tracking, and multi-purpose monitoring, the market is expected to continue expanding, supported by innovations in AI-powered diagnostics, subscription-based service models, and increasing adoption in emerging markets with rising disposable incomes.

Executive Summary

The global smart connected pet collar market is on a sustained growth path, underpinned by rising pet humanization trends, escalating demand for real-time pet safety solutions, and the rapid integration of IoT and AI technologies into wearable pet accessories. The market reached USD 561.0 Million in 2025 and is forecast to surpass USD 990.0 Million by 2034, reflecting a healthy CAGR of 6.32% over the forecast period.

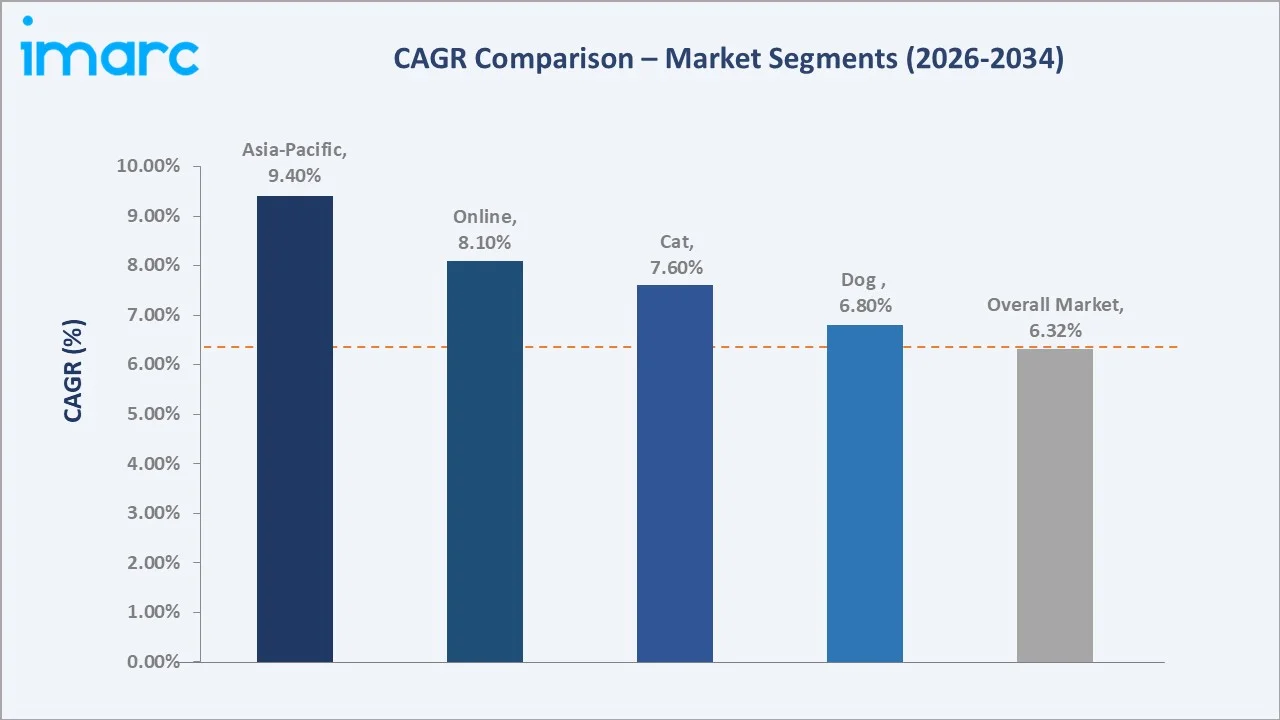

North America leads globally with a 34.6% share in 2025, driven by high pet ownership rates, high disposable incomes, and a well-established pet care industry. Asia-Pacific, at 27.8%, represents the fastest-growing opportunity, with China, Japan, South Korea, and Australia accelerating adoption through rising middle-class pet ownership and expanding e-commerce infrastructure. Dogs account for 64.8% of the pet-type segment, reflecting a broader application range and owner willingness to invest in advanced tracking and health monitoring solutions.

Offline sales channels command a 57.3% share, anchored by pet specialty retailers such as PetSmart and Petco, though online channels at 42.7% are growing rapidly, driven by DTC brand strategies, Amazon/Chewy distribution, and subscription bundling. Leading players, including Garmin Ltd., Tractive, FitBark Inc., and PetPace, continue to invest in AI-powered health analytics, longer battery life, and veterinary integration to strengthen platform loyalty and premium pricing power.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Pet Type) |

Dog – 64.8% share (2025) |

|

Second Largest (Pet Type) |

Cat – 35.2% share (2025) |

|

Dominant Sales Channel |

Offline – 57.3% share (2025) |

|

Leading Region |

North America – 34.6% share (2025) |

|

Fastest Growing Region |

Asia-Pacific (rising pet ownership + IoT adoption) |

|

Top Companies |

Garmin Ltd., Tractive, FitBark Inc., PetPace |

Key Analytical Observations Supporting the Above Data:

- Dog collars account for 64.8% of the smart connected pet collar market in 2025, driven by the higher volume of dog ownership globally, greater average spending per dog owner, and the wider range of use cases, from GPS tracking for outdoor excursions to clinical health monitoring for ageing dogs.

- Cat collars represent 35.2% of the market (2025), with growth accelerating as manufacturers develop lighter, more comfortable form factors and cat-specific health monitoring algorithms. The cat segment is projected to grow at a higher CAGR than dogs through 2034.

- Offline channels retain a 57.3% share, supported by the tactile purchasing preference for wearable pet accessories and the importance of in-store veterinary endorsements. However, online channels at 42.7% are expanding at approximately 8.1% CAGR, driven by subscription-linked collar purchases.

- North America holds 34.6% of the global market in 2025, with approximately 66% of U.S. households owning a pet (APPA 2023–2024), generating robust addressable demand for premium smart collar solutions.

Global Smart Connected Pet Collar Market Overview

The global smart connected pet collar market encompasses technologically enhanced collar devices that integrate GPS modules, IoT connectivity, biometric sensors, and mobile application ecosystems to enable continuous pet location tracking, health monitoring, and behavioral analytics. Originally limited to basic radio-frequency tracking, the product category has evolved into sophisticated multi-sensor platforms capable of monitoring heart rate, respiratory rate, temperature, activity levels, calorie expenditure, and sleep quality in real time.

Macroeconomic factors, including rising disposable incomes globally, the cultural trend of pet humanization, and the growing integration of connected health technologies into everyday consumer life, are primary growth catalysts. Smart connected pet collars offer pet owners the ability to respond proactively to health anomalies, locate lost pets instantly, and access veterinarian-shared health insights, creating compelling value propositions that sustain premium pricing and recurring subscription revenue.

Market Dynamics

To evaluate market opportunities, Request Sample

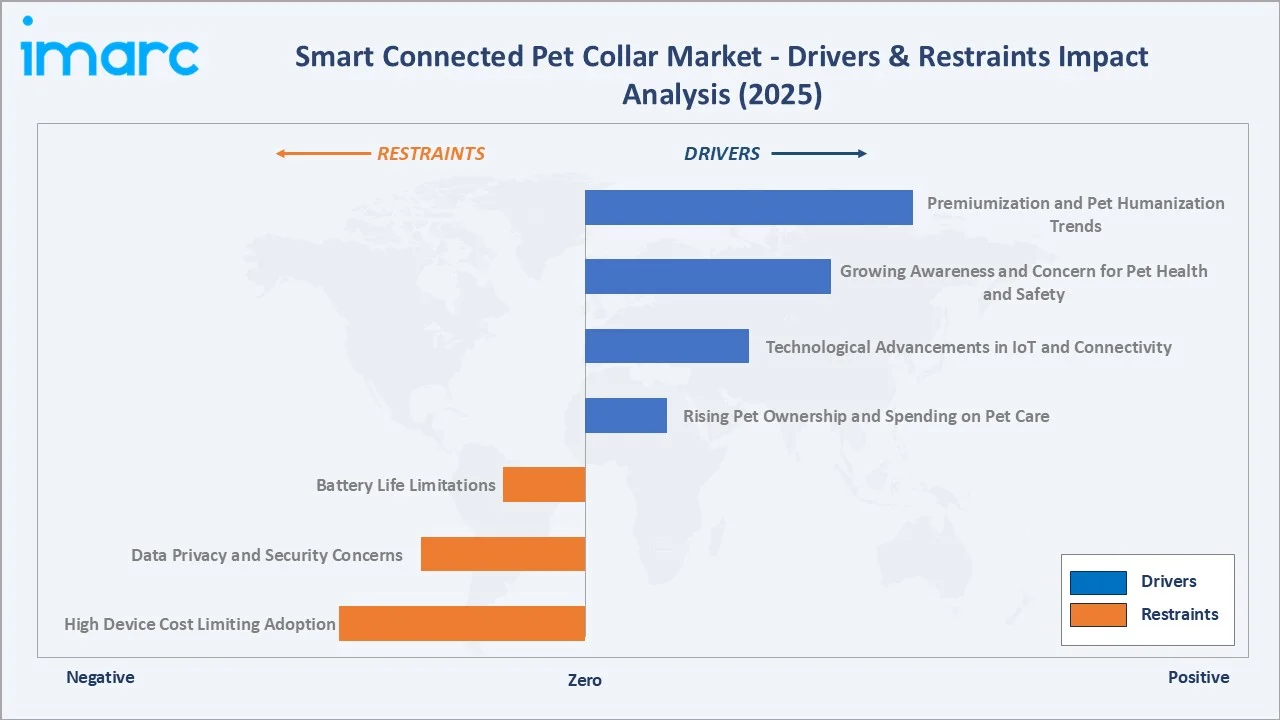

Market Drivers

- Rising Pet Ownership and Spending on Pet Care: The 2025 National Pet Owners Survey, referenced in the APPA's 2026 State of the Industry Report, reveals that 95 million U.S. households have a pet. Actual sales in the U.S. market in 2024 amounted to USD 158 billion spent on pets, with projected sales of USD 165 billion in 2026.

- Technological Advancements in IoT and Connectivity: The integration of IoT technologies enables continuous monitoring, real-time alerts, and data insights about a pet's activity, health, and location. Features such as geofencing, AI-powered anomaly detection, and live GPS tracking have become increasingly sophisticated and reliable, propelling market demand. The global pet wearables market is projected to reach USD 7.2 Billion by 2034, underpinning the smart collar sub-segment trajectory.

- Growing Awareness and Concern for Pet Health and Safety: An increasing proportion of pet owners invest in health-monitoring technologies. According to the American Veterinary Medical Association (AVMA), 88% of pet owners believe the best care involves regular veterinary consultation, creating strong demand for remote health devices that generate shareable health data for veterinary review.

- Premiumization and Pet Humanization Trends: The anthropomorphic treatment of pets as family members is driving expenditure on premium, feature-rich accessories. Smart collar average selling prices of USD 100–300+ are increasingly accepted by high-income pet owners in North America, Europe, and Asia-Pacific, supporting robust revenue growth even in a moderately sized unit volume market.

Market Restraints

- High Device Cost Limiting Adoption: Premium smart connected pet collars range from USD 100 to over USD 400, presenting a significant adoption barrier in price-sensitive emerging markets. The additional monthly subscription cost for GPS and health data services further elevates the total cost of ownership.

- Data Privacy and Security Concerns: Smart collars collect continuous location and biometric data, raising concerns about data storage, third-party sharing, and potential hacking vulnerabilities. Regulatory scrutiny under GDPR (Europe) and state-level privacy laws (U.S.) creates compliance complexity for manufacturers operating across jurisdictions.

- Battery Life Limitations: Standard Tractive dog and cat GPS trackers typically last 5–14 days. This operational inconvenience reduces adoption among owners of highly active dogs and represents a persistent product development challenge requiring trade-offs between functionality and longevity.

Market Opportunities

- AI and Predictive Health Analytics: In January 2024, Invoxia introduced its Minitailz Smart Pet Tracker at CES 2024, featuring AI-powered technology to track pet health, activity, and location with an emphasis on preventive monitoring. AI models capable of early disease detection, breed-specific health benchmarking, and behavior pattern analysis represent a high-margin, recurring revenue opportunity for platform-oriented companies.

- Emerging Market Adoption: Asia-Pacific and Latin America collectively represent an incremental USD 180 Million smart pet collar opportunity by 2030. Rising smartphone penetration, expanding pet care retail infrastructure, and growing middle-class pet ownership create favorable adoption conditions. Entry via affordable subscription-linked hardware and localized app ecosystems is the preferred strategy.

- Veterinary Integration and Clinical Health Monitoring: In November 2023, PetPace partnered with Veterinary Health Research Centers (VHRC) for the "DOGMA" initiative, using biometric collar data to study cognitive decline in ageing dogs. Such clinical partnerships validate the health monitoring category and open pathways to insurance reimbursement and prescription-level device classification.

Market Challenges

- Platform Interoperability: The absence of universal standards for smart pet collar connectivity, data formats, and third-party integrations creates fragmented user experiences. Consumers with multi-brand smart home ecosystems (Apple HomeKit, Google Home, Amazon Alexa) expect seamless integration that most pet collar platforms do not yet fully support.

- Subscription Churn and Monetization Sustainability: Hardware-embedded subscription models generate recurring revenue but face high churn rates when consumers perceive insufficient value. Maintaining engagement through software updates, new health features, and veterinary integrations is critical to long-term revenue sustainability for subscription-dependent business models.

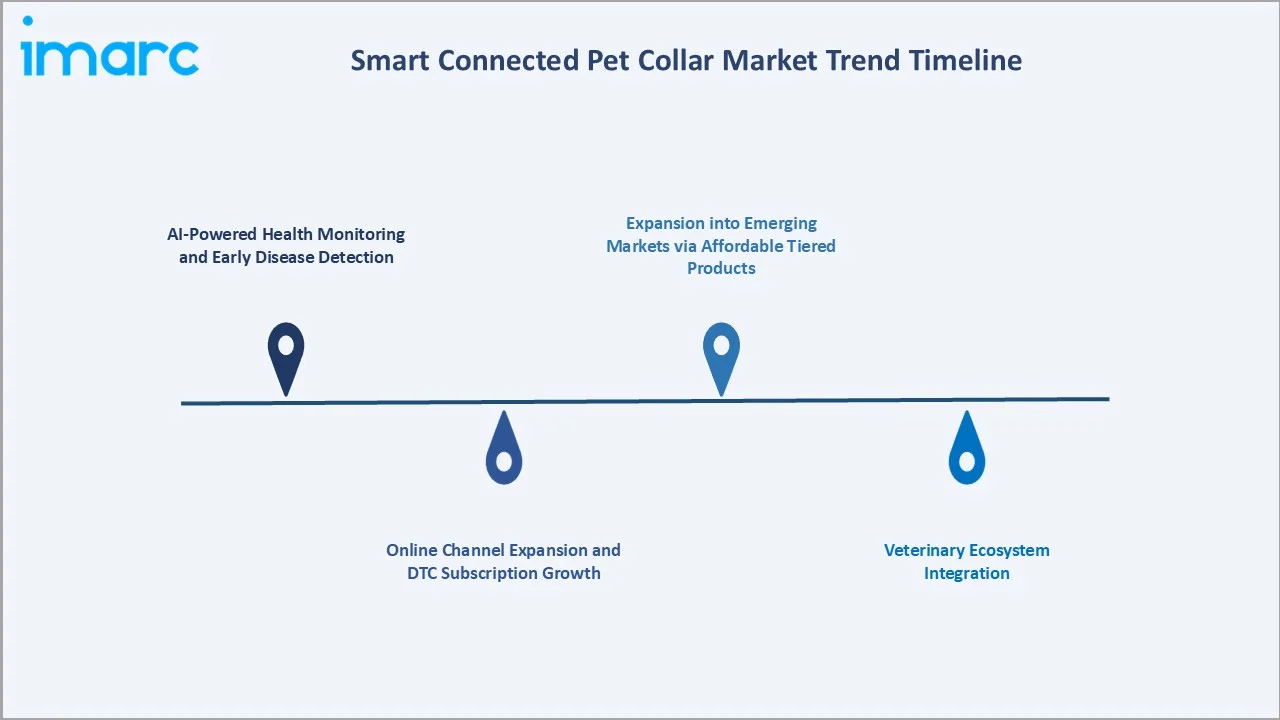

Emerging Market Trends

1. AI-Powered Health Monitoring and Early Disease Detection

In March 2024, PetPace launched PetPace 2.0, an AI-powered smart collar providing continuous real-time monitoring of canine vital signs, including heart rate, respiratory rate, temperature, and posture. Machine learning models trained on millions of pet health data points enable early detection of cardiac anomalies, respiratory distress, and anxiety episodes.

2. Online Channel Expansion and DTC Subscription Growth

Online and direct-to-consumer smart pet collar sales channels grew from approximately 32% of total distribution in 2020 to 42.7% in 2025. In March 2026, PingPong announced a strategic partnership with Chewy Inc. to become one of Chewy’s first official cross‑border payments partners and support international merchant expansion into the North American pet market. Under the agreement, PingPong will provide a full suite of services, giving sellers a streamlined pathway to register, list products, and collect orders on Chewy’s platform.

3. Veterinary Ecosystem Integration

Leading smart collar brands are building structured veterinary integration capabilities, enabling pet owners to share continuous biometric data directly with veterinary electronic medical record (EMR) systems. This trend reduces the diagnostic information gap between annual check-ups, enables data-driven preventive care recommendations, and creates powerful clinical positioning for premium collar platforms.

4. Expansion into Emerging Markets via Affordable Tiered Products

Mass-market and economy-tier smart collars are gaining traction in Asia-Pacific and Latin America, with products like the FitBark GPS Dog Tracker offering basic tracking at sub-USD 100 price points. Brands are deploying modular software models where entry-level hardware can unlock premium health and GPS features incrementally via subscription upgrades. This tiered strategy dramatically expands the addressable market beyond high-income pet owners, with India, Brazil, and Indonesia emerging as key targets.

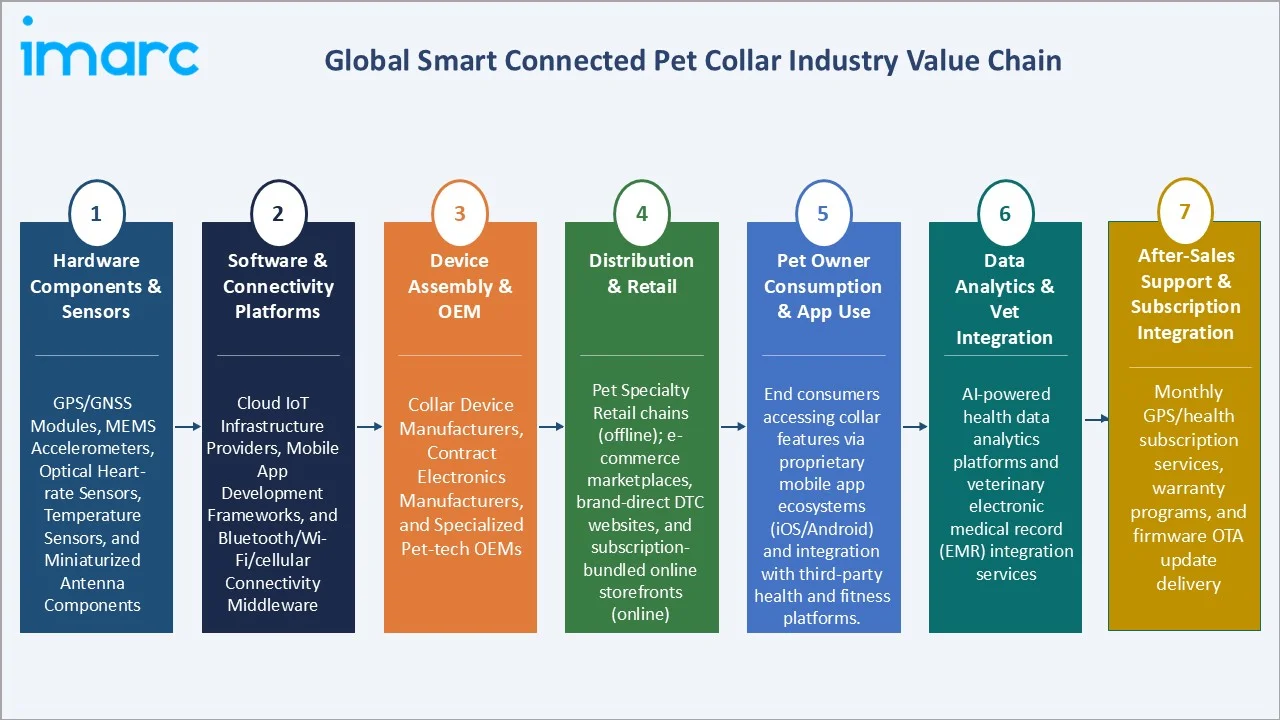

Industry Value Chain Analysis

The smart connected pet collar value chain spans semiconductor component manufacturing through subscription service delivery, with each stage populated by specialized operators whose performance directly influences device accuracy, connectivity reliability, and user experience quality.

|

Stage |

Key Players / Examples |

|

Hardware Components & Sensors |

GPS/GNSS modules, MEMS accelerometers, optical heart-rate sensors, temperature sensors, and miniaturized antenna components |

|

Software & Connectivity Platforms |

Cloud IoT infrastructure providers, mobile app development frameworks, and Bluetooth/Wi-Fi/cellular connectivity middleware. |

|

Device Assembly & OEM |

Collar device manufacturers, contract electronics manufacturers, and specialized pet-tech OEMs. |

|

Distribution & Retail |

Pet specialty retail chains (offline); e-commerce marketplaces, brand-direct DTC websites, and subscription-bundled online storefronts (online) |

|

Pet Owner Consumption & App Use |

End consumers accessing collar features via proprietary mobile app ecosystems (iOS/Android) and integration with third-party health and fitness platforms. |

|

Data Analytics & Vet Integration |

AI-powered health data analytics platforms and veterinary electronic medical record (EMR) integration services |

|

After-Sales Support & Subscription |

Monthly GPS/health subscription services, warranty programs, and firmware OTA update delivery |

Technology Landscape in the Smart Connected Pet Collar Industry

GPS and GNSS Tracking Technology

Modern smart pet collars integrate multi-constellation GNSS receivers (GPS, GLONASS, Galileo), enabling location accuracy of 2–5 meters under optimal conditions. In May 2023, Garmin introduced its all‑new Alpha Series handheld and dog collars featuring advanced GPS tracking with multi‑band technology, improved range, and enhanced durability, designed for outdoor and hunting use.

Biometric Sensing and Health Monitoring Technology

Clinical-grade biometric sensors measuring heart rate, respiratory rate, skin temperature, and activity acceleration are being embedded into consumer pet collar platforms. MEMS accelerometers, optical heart-rate sensors, and piezoelectric respiration monitors enable continuous multi-parameter health data capture. AI algorithms process this data to generate wellness scores, detect anomalies, and issue owner alerts.

IoT Connectivity and Cloud Platform Architecture

Smart pet collars operate across cellular (LTE-M/NB-IoT), Wi-Fi, Bluetooth 5.0, and LoRaWAN connectivity protocols, enabling persistent cloud synchronization of location and health data. Cloud-based data platforms, built on AWS IoT, Google Cloud IoT Core, and proprietary infrastructure, process streaming collar telemetry, support over-the-air firmware updates, and power mobile app experiences.

Battery Technology and Energy Optimization

Manufacturers are deploying adaptive duty-cycling algorithms that dynamically balance GPS polling frequency with location update urgency, extending battery life by 30–40%. Emerging solid-state battery chemistries and energy-harvesting approaches incorporating kinetic and solar charging are at early development stages, with commercial deployment expected to extend standby times to 14+ days in next-generation platforms by 2027–2028.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Pet Type | Dog |

64.8% |

2025 |

| Application | GPS Location Monitoring |

🔒 |

2025 |

| Sales Channel | Offline |

57.3% |

2025 |

| Region | North America |

34.6% |

2025 |

By Pet Type

Dogs dominate the pet type segment with a 64.8% share in 2025. This dominance reflects the higher global volume of dog ownership, the broader range of smart collar use cases for dogs, spanning GPS tracking for off-leash outdoor activities, training collar integration, and clinical health monitoring for senior dogs, and significantly higher average selling prices supported by dog owners' premium spending disposition.

To access detailed market analysis, Request Sample

Cats account for 35.2% of the market, with growth accelerating as manufacturers develop lighter, more ergonomic form factors and deploy cat-specific health algorithms. The cat segment is the fastest-growing pet type, driven by growing urban cat ownership in Europe and Asia-Pacific, and increasing owner willingness to invest in safety solutions for indoor-outdoor cats.

By Sales Channel

Offline channels command a 57.3% share of the smart connected pet collar market in 2025. Pet specialty retailers, including PetSmart and Petco, alongside veterinary clinics and electronics retailers, remain the dominant distribution touchpoint, benefiting from consumers' preference to physically evaluate wearable devices before purchase and the influential role of in-store veterinary endorsements in driving premium collar adoption.

Online channels represent 42.7% of the market, growing at approximately 8.1% CAGR as DTC brand strategies, Amazon, and Chewy.com distribution partnerships, and subscription-bundled hardware models accelerate digital purchasing. Social media marketing, influencer-driven pet care content, and trial-period subscription offers are proving highly effective in converting digital traffic to online collar purchases.

Regional Market Insights

North America's market leadership (34.6%, 2025) reflects the world's most developed pet care industry and the highest per-household pet spending levels. Approximately 66% of U.S. households own at least one pet, generating a robust addressable market for premium smart collar platforms. The region benefits from the strong brand presence of Garmin Ltd., alongside a well-developed e-commerce infrastructure.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.6% |

High pet ownership, premium health monitoring demand, and established e-commerce |

|

Asia-Pacific |

27.8% |

Rising middle class, growing pet humanization, and China & Australia urbanization |

|

Europe |

21.5% |

High disposable incomes, pet wellness culture, and GDPR-compliant data platforms |

|

Latin America |

9.4% |

Rising pet adoption, growing smartphone penetration, and expanding e-commerce |

|

Middle East & Africa |

6.7% |

Urbanization, high-income pet ownership in GCC, and tourism-driven pet services |

Asia-Pacific is the highest-growth region, projected at approximately 9.4% CAGR through 2034, driven by China's rapidly expanding urban pet population, South Korea's technology-forward consumer culture, and Australia's high pet ownership combined with outdoor lifestyle demand for GPS tracking solutions.

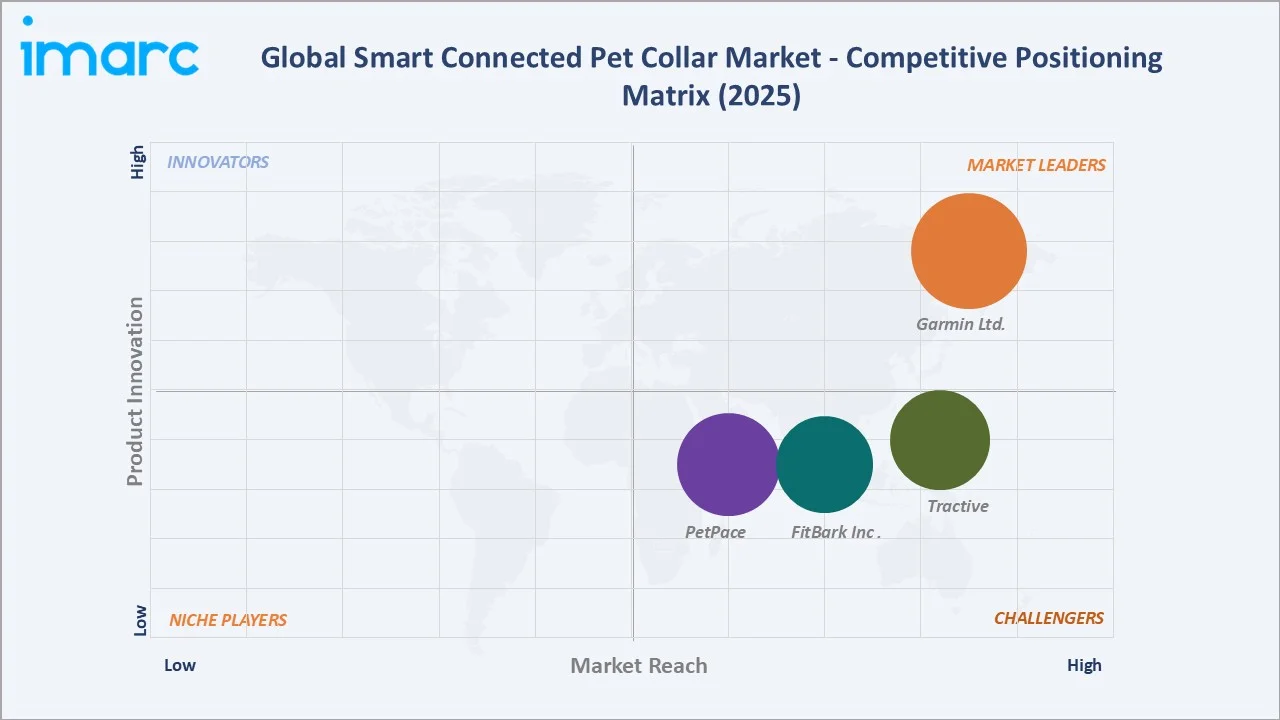

Competitive Landscape

The global smart connected pet collar market exhibits a moderately fragmented structure. The top manufacturers, Garmin Ltd., Tractive, FitBark Inc., and PetPace, collectively hold approximately 30–35% of global market revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Garmin Ltd. |

Alpha, Delta, PRO

|

Market Leader |

Global GPS expertise; precision outdoor tracking; rugged design for sporting dogs |

|

Tractive |

Tractive |

Strong Challenger |

Europe's leading GPS tracker; affordable live tracking; geo-fencing; multilingual app |

|

FitBark Inc. |

FitBark GPS, FitBark 2 |

Strong Challenger |

Health & fitness monitoring; research partnerships; sub-USD 100 price accessibility |

|

PetPace |

PetPace V3.0 |

Challenger |

AI-powered clinical health monitoring; vital signs tracking; veterinary integration |

A significant long tail of regional and niche platform providers ensures substantial competitive dynamism, particularly in the Asia-Pacific and Latin American markets, where localized products and distribution are key competitive advantages.

Key Company Profiles

Garmin Ltd.

Garmin Ltd., headquartered in Olathe, Kansas, with legal incorporation in Schaffhausen, Switzerland, is a global leader in GPS and navigation technology with a well-established presence in the smart pet collar market through its Alpha and Astro product series, primarily targeting hunting dog tracking and outdoor adventure use cases.

- Product Portfolio: Alpha, Delta, and PRO.

- Recent Developments: For the full fiscal year 2025, Garmin achieved record consolidated revenue of USD 7.25 billion (+15%), shipped over 20 million units (including smart connected pet collars), and posted operating income of USD 1.88 billion, both marking substantial annual growth.

- Strategic Focus: Expanding from the sporting/hunting dog niche to mainstream pet wellness; leveraging GPS hardware expertise for next-generation multi-GNSS precision tracking; veterinary data integration development.

Tractive

Tractive, headquartered in Pasching, Austria, is Europe's leading GPS pet tracker manufacturer, offering subscription-based live GPS tracking and activity monitoring solutions for dogs and cats. Tractive operates an LTE-connected collar platform with coverage in 175+ countries through global cellular roaming partnerships.

- Product Portfolio: CAT Mini, CAT 6 Mini, DOG 6, DOG 6 XL, DOG XL Adventure (upcoming).

- Recent Developments: In April 2026, Tractive launched the DOG 6 XL tracker for large breeds, featuring enhanced durability, battery life, and a new scratch monitoring system, while also debuting the CAT 6 Mini with heart rate and respiratory tracking for cats.

- Strategic Focus: Subscription model scaling across North America and Asia-Pacific; hardware miniaturization for cat collars; AI-powered health alert development.

FitBark Inc.

FitBark Inc., headquartered in Missouri, U.S., specializes in dog health and activity monitoring wearables, offering sub-USD 100 price-point devices that provide wellness scoring, sleep analysis, and activity benchmarking against breed-specific health norms.

- Product Portfolio: FitBark 2 and FitBark GPS.

- Recent Developments: In January 2026, FitBark announced that its FitBark GPS tracker is now available in the UK, expanding the pet health and location tracking product beyond its existing markets. The move allows UK pet owners to use real‑time GPS tracking and activity monitoring features to better manage their dogs’ health and safety.

- Strategic Focus: Democratizing pet health monitoring through affordable hardware; research-backed health data credibility; integration with Apple Health and Google Fit for cross-platform owner engagement.

Market Concentration Analysis

The smart connected pet collar market exhibits moderate concentration at the brand level, with the top five global suppliers holding approximately 30–35% of total revenue in 2025. However, a long tail of 50+ regional manufacturers and platform providers, particularly in China, India, and Latin America, ensures substantial market fragmentation below the top tier.

Consolidation activity is accelerating, including Tractive's acquisition of Whistle from Mars Petcare (July 2025), gaining access to Whistle's U.S. subscriber base. Private equity interest remains elevated, targeting mid-tier smart collar platforms with validated health data capabilities and established subscription user bases. The subscription-linked recurring revenue model and proprietary health data assets represent the primary sources of value in M&A transactions, creating incentives for platform-oriented consolidation rather than pure hardware integration.

Investment & Growth Opportunities

Fastest Growing Segments

AI-powered health analytics platforms (estimated CAGR 12%+), veterinary-integrated smart collar ecosystems (10% CAGR), and cat-specific smart collar solutions (8.5% CAGR) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable market of approximately USD 280 Million by 2030, with disproportionate margin potential versus commoditized GPS-only hardware.

Emerging Market Expansion

Asia-Pacific and Latin America collectively represent an incremental USD 180 Million smart pet collar opportunity by 2030. Entry via affordable subscription-linked hardware models, partnerships with regional e-commerce platforms (Lazada, Mercado Libre, Flipkart), and alignment with local pet care retail chains is the preferred investment modality. Products designed for multi-pet household economics and optimized for local cellular network standards (NB-IoT, LTE-M) are prioritized for emerging market deployment.

Venture and Institutional Investment Trends

- Key investment themes include AI-driven early disease detection algorithms, breed-specific health benchmark development, and veterinary-grade biometric sensor miniaturization. The convergence of pet care and human health technology is attracting crossover investment from digital health venture funds.

- Family offices and PE firms are targeting vertical integration opportunities, consolidating sensor manufacturing, cloud platform development, subscription management, and veterinary data partnerships into single platform companies capable of commanding premium EBITDA multiples from strategic acquirers in the broader pet care or health technology ecosystems.

Future Market Outlook (2026-2034)

The global smart connected pet collar market is positioned for sustained, broad-based growth through 2034. From a base of USD 561.0 Million in 2025, the market is projected to reach USD 990.0 Million by 2034, representing total incremental value creation of USD 429.0 Million over the forecast decade. The smart connected pet collar market forecast remains consistently positive, anchored by structural demand tailwinds that are demographic, technological, and cultural in nature.

Technological evolution, particularly the transition from GPS-only tracking devices to AI-powered multi-sensor health companions capable of generating clinically actionable pet health insights, will redefine how value is captured in the ecosystem. Platforms that successfully integrate autonomous health monitoring, veterinary data sharing, insurance partnerships, and personalized wellness recommendations will command sustainable competitive advantages and superior subscriber retention metrics.

Long-term, the market's trajectory is tied to three structural macro-themes: the sustained rise of pet humanization globally (driving willingness to pay for premium health and safety solutions), the democratization of health monitoring technology through sensor miniaturization and cost reduction, and the maturation of subscription-based pet care ecosystems. Smart connected pet collars sit at the intersection of all three, ensuring resilient demand growth well beyond the 2034 forecast horizon.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including smart pet collar manufacturers, pet specialty retailers, veterinary professionals, IoT technology providers, and a consumer panel of 1,800 pet owners across North America, Europe, and Asia-Pacific. Insights were gathered on device usage patterns, purchase decision drivers, subscription renewal behaviors, and unmet product needs across all major market segments.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, investor presentations, FDA and CE device regulatory submissions, industry databases (Euromonitor, Statista, IBISWorld), trade publications (Pet Business Magazine, Pet Product News), and publicly available financial and subscriber data. Over 200 secondary sources were reviewed and triangulated to validate market size and growth assumptions.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating pet population growth data, household pet spending indices, average selling price trajectories, and subscription penetration rate modelling. A base-case CAGR of 6.32% reflects consensus analyst estimates validated against reported manufacturer revenue growth rates and regional pet wearables market performance data from 2020 to 2024.

Smart Connected Pet Collar Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Pet Types Covered | Cat, Dog |

| Applications Covered | GPS Location Monitoring, Activity and Health Monitoring, Multi-purpose Monitoring, Others |

| Sales Channels Covered | Offline, Online |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Garmin Ltd., Tractive, FitBark Inc., PetPace, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the smart connected pet collar market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global smart connected pet collar market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the smart connected pet collar industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Smart Connected Pet Collar Market Report

The global smart connected pet collar market reached USD 561.0 Million in 2025. It is projected to reach USD 990.0 Million by 2034.

The smart connected pet collar market is expected to grow at a CAGR of 6.32% during the forecast period from 2026 to 2034, supported by consistent demand from pet safety, health monitoring, and IoT-enabled tracking applications.

North America leads the market with a 34.6% share in 2025, driven by high pet ownership rates, high disposable incomes, well-established pet specialty retail infrastructure, and early adoption of premium IoT-enabled pet accessories.

The dog segment dominates with a 64.8% share in 2025, valued at approximately USD 363.5 Million. Its dominance reflects higher dog ownership volumes globally, broader GPS and health tracking use cases, and significantly higher average spending per dog owner.

The offline sales channel holds the largest share at 57.3% in 2025, anchored by pet specialty retailers, electronics stores, and veterinary clinics. However, Online channels at 42.7% are growing at approximately 8.1% CAGR and are expected to gain further share through 2034.

Key players include Garmin Ltd., Tractive, FitBark Inc., and PetPace, among others.

Online channels are increasingly preferred for smart pet collar purchasing, particularly for subscription-bundled hardware products. DTC brand strategies and social media marketing are accelerating online adoption. E-commerce sales are growing at approximately 8.1% CAGR, outpacing the overall market rate.

Key challenges include high device costs limiting adoption in price-sensitive markets, data privacy and security concerns under GDPR and state-level regulations, battery life limitations of GPS-active modes, and platform interoperability issues across smart home ecosystems.

Significant opportunities exist in AI-powered pet health analytics platforms, veterinary-integrated smart collar ecosystems, affordable tiered products targeting Asia-Pacific and Latin American markets, and corporate B2B pet care benefit programs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)