Smart Electric Meter Market Size, Share, Trends and Forecast by Type, Phase, End User, and Region, 2026-2034

Global Smart Electric Meter Market Size, Share, Trends & Forecast (2026-2034)

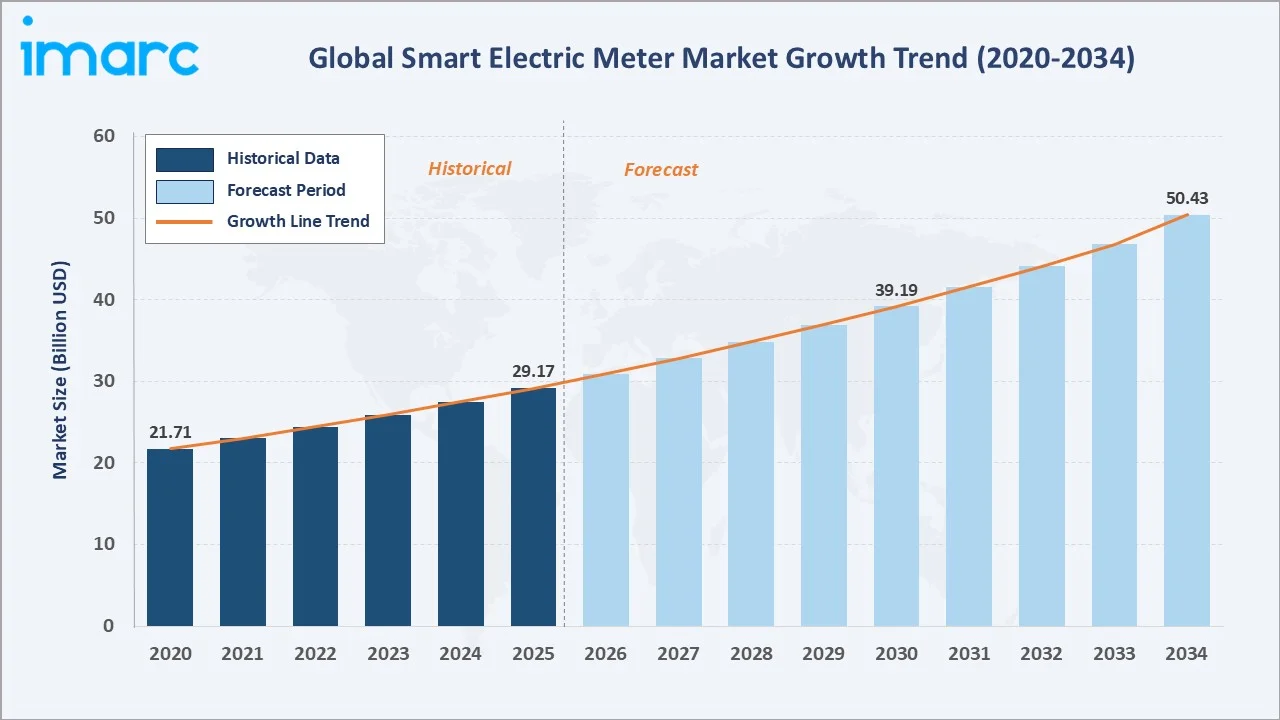

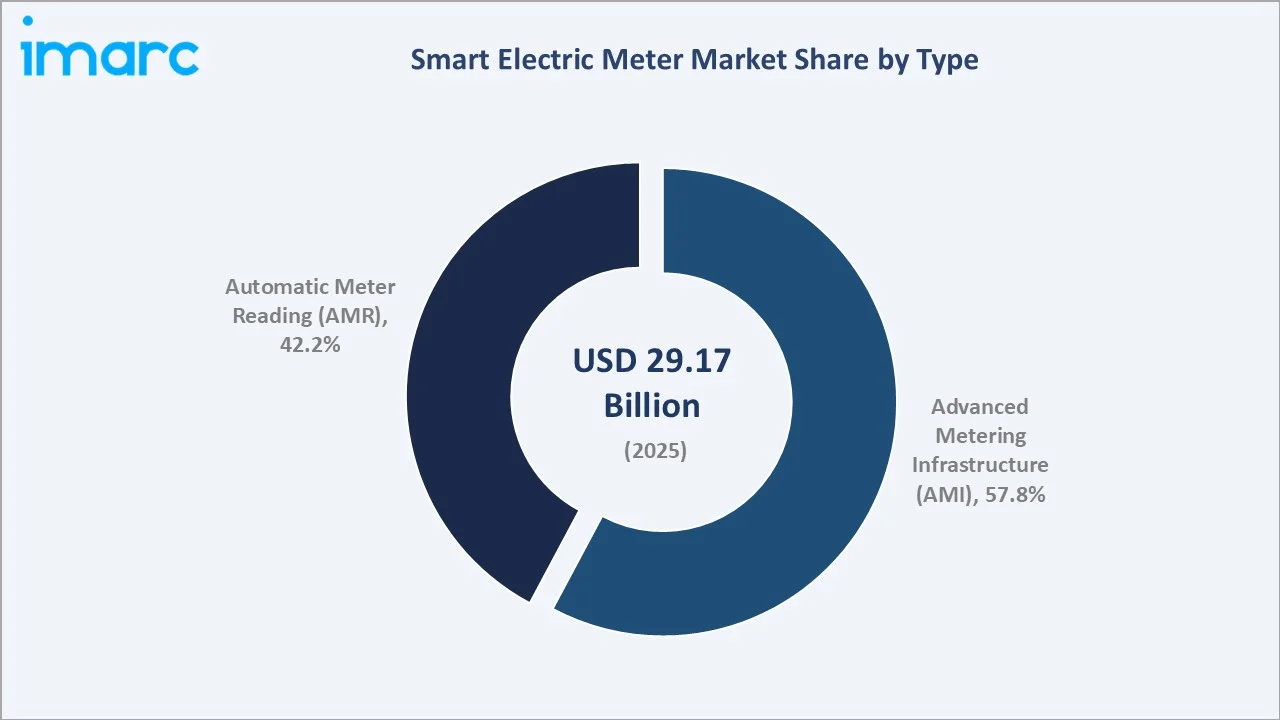

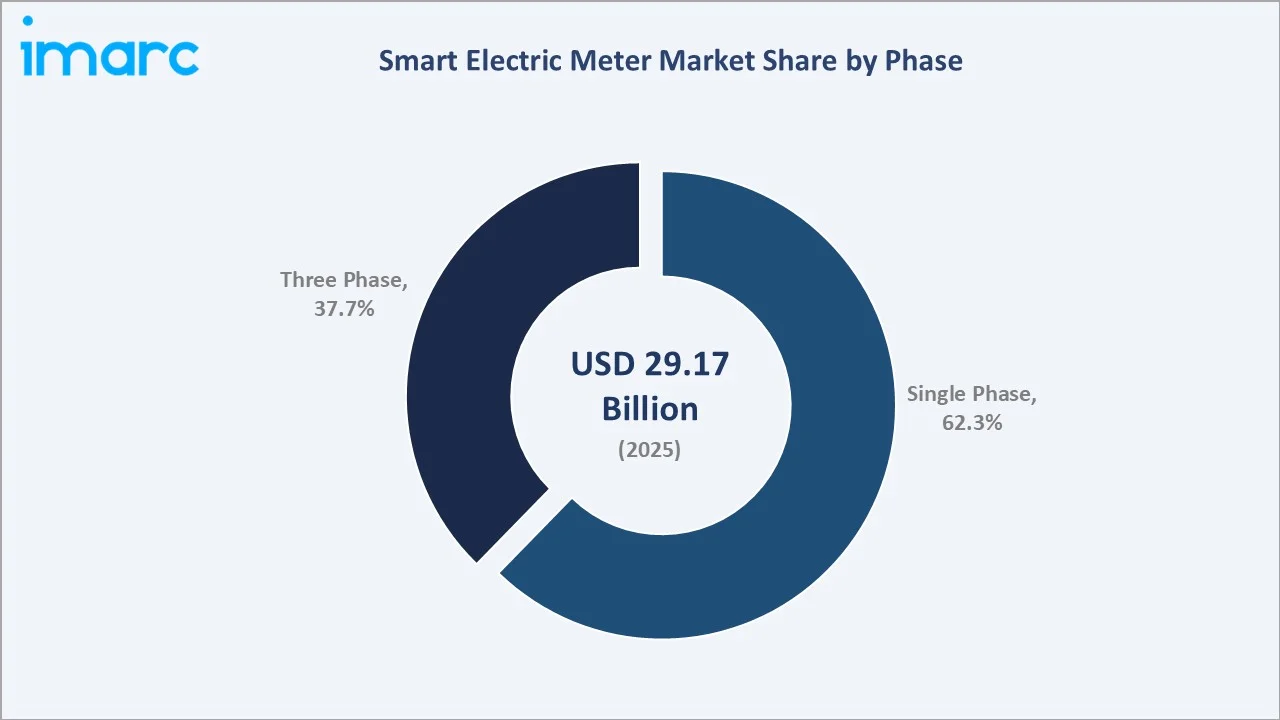

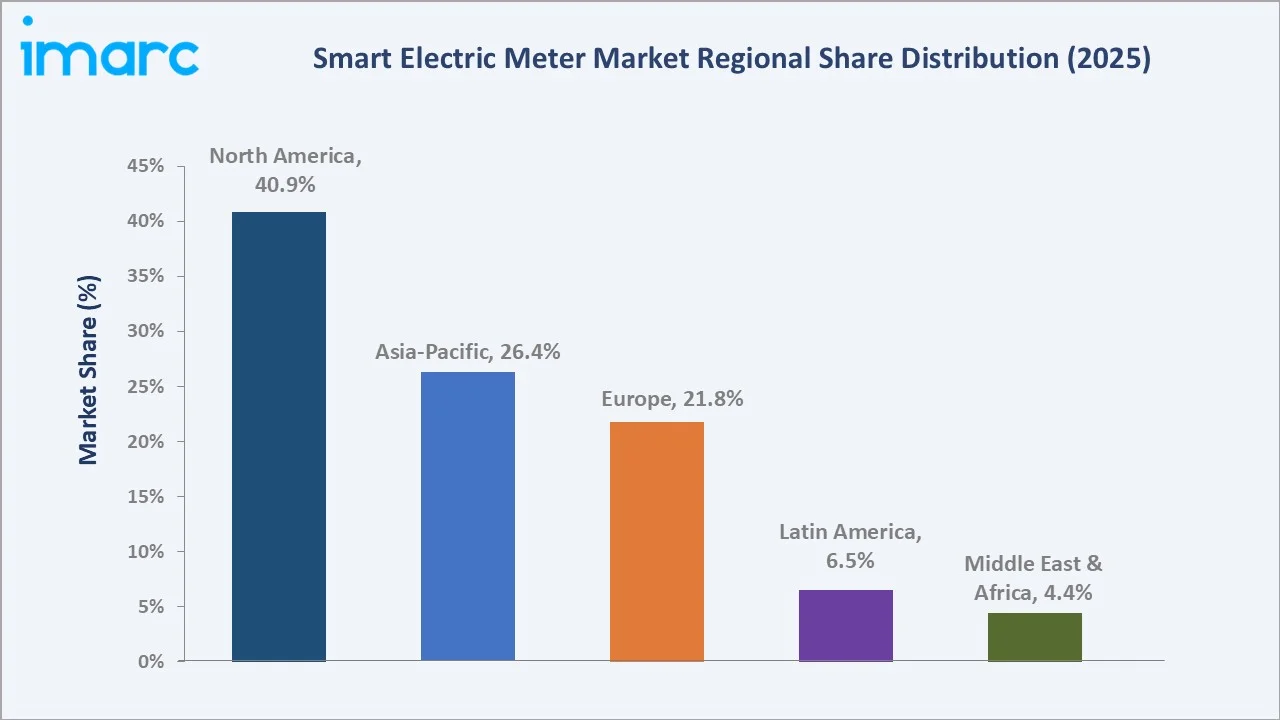

The global smart electric meter market size was valued at USD 29.17 Billion in 2025 and is projected to reach USD 50.43 Billion by 2034, expanding at a CAGR of 6.09% during 2026-2034. Accelerating utility digitalization, large-scale advanced metering infrastructure (AMI) rollouts, rising renewable energy integration, and stringent grid modernization mandates are collectively driving smart electric meter market growth. Advanced Metering Infrastructure (AMI) leads the market with a 57.8% share in 2025, while Single Phase meters account for 62.3% of global demand. North America dominates regional revenue with a 40.9% share, supported by mature smart grid investment and federal funding programs.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 29.17 Billion |

|

Forecast Market Size (2034) |

USD 50.43 Billion |

|

CAGR (2026-2034) |

6.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (40.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Type Segment |

Advanced Metering Infrastructure (AMI) - 57.8%, 2025 |

|

Leading Phase Segment |

Single Phase - 62.3%, 2025 |

The chart below illustrates smart electric meter market growth from 2020 to 2034, with disciplined historical adoption transitioning into a sharper forecast trajectory driven by AMI scale-up.

To get more information on this market, Request Sample

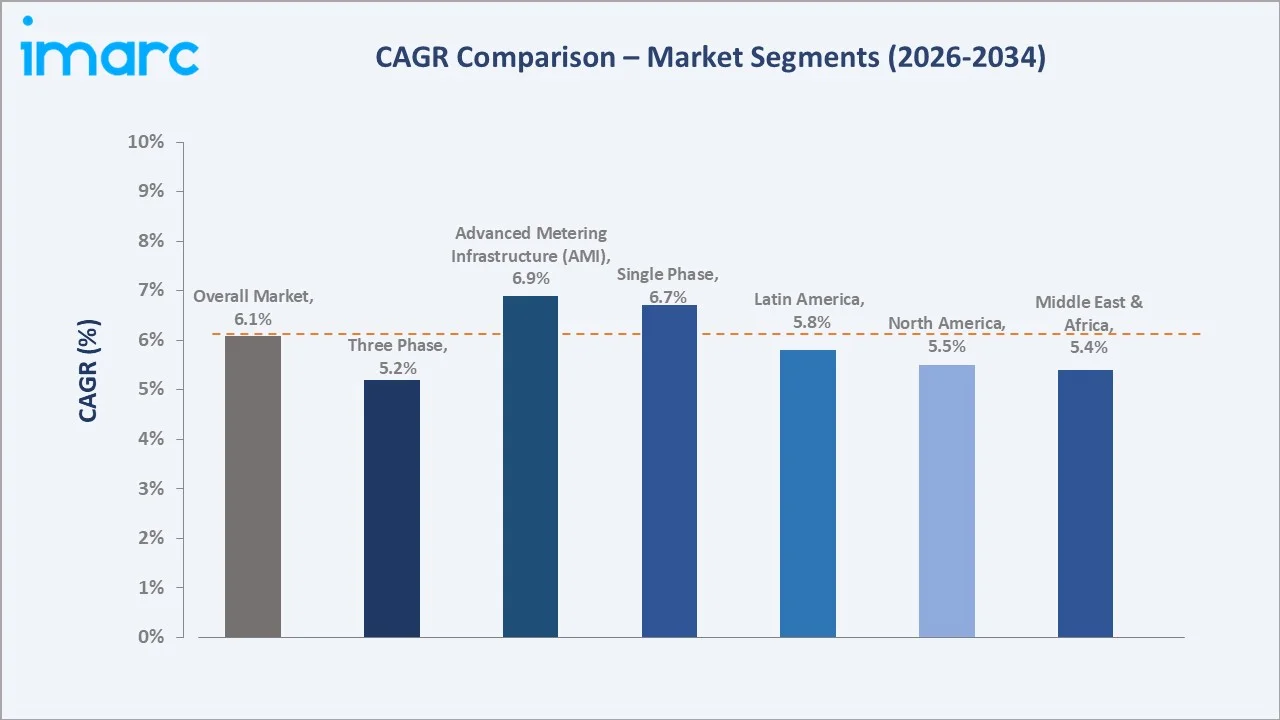

CAGR analysis identifies Asia-Pacific and the AMI segment as the fastest-growing pockets within the global smart electric meter market through 2034.

Executive Summary

The global smart electric meter market is undergoing structural transformation driven by grid digitalization, renewable energy integration, and utility-led modernization programs. Valued at USD 29.17 Billion in 2025, the market is projected to expand to USD 50.43 Billion by 2034, registering a CAGR of 6.09% during 2026-2034. Rising power consumption, distribution loss reduction targets, and policy-led smart grid mandates are collectively fueling adoption across mature and emerging utility markets.

Advanced Metering Infrastructure (AMI) leads the market with a 57.8% share in 2025, supported by two-way communication capability and demand response readiness. Automatic Meter Reading (AMR) holds 42.2% and continues to serve cost-sensitive utility upgrades. Single Phase meters represent 62.3% of global volume in 2025, reflecting residential dominance. Key trends include AI-driven load forecasting, edge analytics, cellular IoT meters, and cyber-resilient firmware design accelerating utility procurement priorities.

North America commands a 40.9% in 2025, anchored by U.S. Inflation Reduction Act funding and DOE grid programs. Asia-Pacific holds 26.4% and is the fastest-growing region, propelled by China's State Grid AMI expansion and India's Revamped Distribution Sector Scheme covering more than 250 million planned smart meters. Europe accounts for 21.8%, supported by EU energy efficiency directives and the UK SMETS2 rollout, reinforcing strong global outlook through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Advanced Metering Infrastructure (AMI) - 57.8% share (2025) |

|

Second Type Segment |

Automatic Meter Reading (AMR) - 42.2% share (2025) |

|

Leading Phase Segment |

Single Phase - 62.3% share (2025) |

|

Leading Region |

North America - 40.9% (2025) |

|

Second Region |

Asia-Pacific - 26.4% (2025) |

|

Top Companies |

Itron Inc., Landis+Gyr, Honeywell International Inc., Siemens, Schneider Electric and Xylem |

Key Analytical Observations Supporting the Above Data:

- AMI's 57.8% dominance in 2025 reflects utility preference for two-way communication, real-time outage detection, and demand response capabilities that AMR systems cannot deliver at the same operational depth.

- AMR at 42.2% in 2025 continues to serve cost-conscious deployments, particularly across emerging markets where utilities prioritize meter replacement over full-stack head-end system overhauls.

- Single Phase meters' 62.3% share in 2025 mirrors the residential weighting of global power demand, with three phase meters concentrated in commercial and industrial accounts that contribute disproportionate revenue per unit.

- North America's 40.9% global in 2025 is anchored by the U.S. installed base of more than 135 million smart meters and active deployment programs across investor-owned utilities including Florida Power & Light and Pacific Gas & Electric.

- Asia-Pacific's position as the fastest-growing region, with a 26.4% share in 2025, is reinforced by India's target of installing approximately 250 million smart meters under the Revamped Distribution Sector Scheme by the end of the decade.

- Itron, Landis+Gyr, and Honeywell collectively serve a substantial portion of global utility AMI procurement, with Itron reporting USD 2.4 Billion in revenue for FY2024, underscoring the consolidation at the top tier.

Global Smart Electric Meter Market Overview

Smart electric meters are digital devices that measure electricity consumption with high temporal granularity and communicate usage data bidirectionally between utilities and end users. They support remote reading, time-of-use billing, outage detection, prepayment, and demand response through cellular, RF mesh, or power-line communication networks.

The ecosystem includes silicon and component suppliers, meter manufacturers, communication module vendors, software and meter data management providers, system integrators, and electric utilities. Macroeconomic forces such as decarbonization commitments, electrification of transport, and aging grid infrastructure replacement cycles continue to expand the addressable opportunity through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

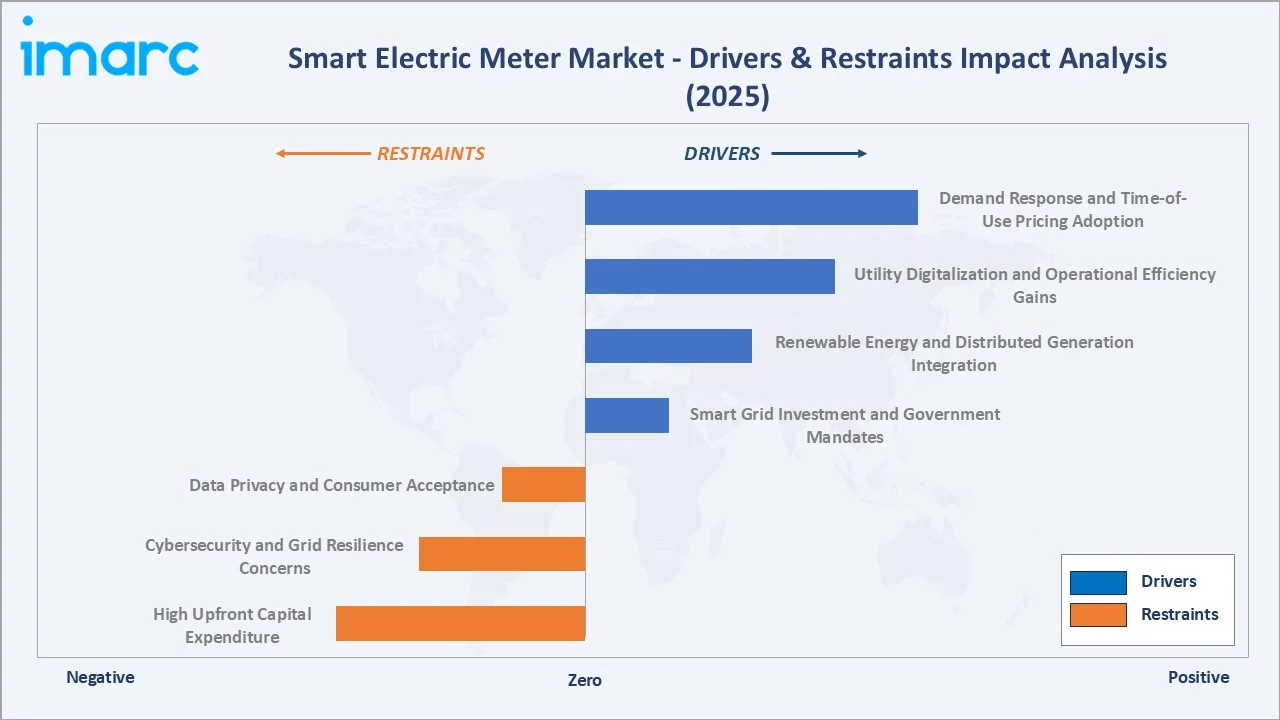

Market Drivers

- Smart Grid Investment and Government Mandates: Government grid modernization programs are accelerating smart meter adoption. U.S. funding under the Infrastructure Investment and Jobs Act and initiatives by the U.S. Department of Energy support grid resilience and digital technologies, indirectly enabling advanced metering infrastructure deployment..

- Renewable Energy and Distributed Generation Integration: Rising rooftop solar and EV adoption require granular consumption data. Global solar PV capacity exceeded 1.6 TW by end-2023, driving structural demand for prosumer-ready smart meters.

- Utility Digitalization and Operational Efficiency Gains: Smart meters help utilities reduce manual meter reading costs and improve billing accuracy. They also assist in lowering non-technical losses, which remain high in several developing regions, thereby improving operational efficiency and revenue realization.

- Demand Response and Time-of-Use Pricing Adoption: Dynamic tariffs in California, the UK, and Australia rely on smart meter granularity, reinforcing meter replacement cycles in advanced regulatory regimes.

Market Restraints

- High Upfront Capital Expenditure: Smart meter deployment involves high upfront costs, including devices, communication networks, and IT systems. Studies by the International Energy Agency and World Bank indicate utilities face long payback periods, especially in price-sensitive and emerging markets.

- Cybersecurity and Grid Resilience Concerns: Smart meters increase grid digitalization risks, requiring stronger cybersecurity frameworks. Agencies like European Union Agency for Cybersecurity and North American Electric Reliability Corporation highlight rising cyber threats, prompting stricter compliance requirements that can delay smart meter deployments.

- Data Privacy and Consumer Acceptance: Detailed energy usage data raises privacy concerns under regulations such as General Data Protection Regulation and California Consumer Privacy Act, requiring utilities to implement data protection, consent mechanisms, and secure data handling practices.

Market Opportunities

- Asia-Pacific AMI Acceleration: India's Revamped Distribution Sector Scheme targets approximately 250 million smart meters this decade. China's State Grid has already deployed over 500 million meters, with replacement cycles offering recurring revenue.

- Edge Analytics and AI-Driven Insights: Next-generation meters embed processing capability for fault detection, theft analytics, and predictive load management, opening high-margin software and services upsell.

- EV Charging and Vehicle-to-Grid Integration: Global EV stock surpassed 45 million units in 2023 Smart meters with V2G compatibility support bidirectional energy flow, creating new metering categories.

Market Challenges

- Interoperability and Standardization Gaps: Multiple competing standards (DLMS/COSEM, IEEE 2030.5, IEC 62056) and proprietary head-end systems complicate multi-vendor utility procurement and slow open-architecture adoption.

- Skilled Workforce Shortages: Utilities face shortages of skilled technicians, engineers, and data specialists required for smart grid deployment. Reports from the International Energy Agency and European Commission highlight workforce gaps impacting digital energy infrastructure rollout timelines.

- Aging Communication Infrastructure: The phase-out of legacy 2G and 3G networks is disrupting older AMR and early smart meter systems. According to the GSMA, global network sunsets are forcing utilities to upgrade communication modules and accelerate meter replacement programs.

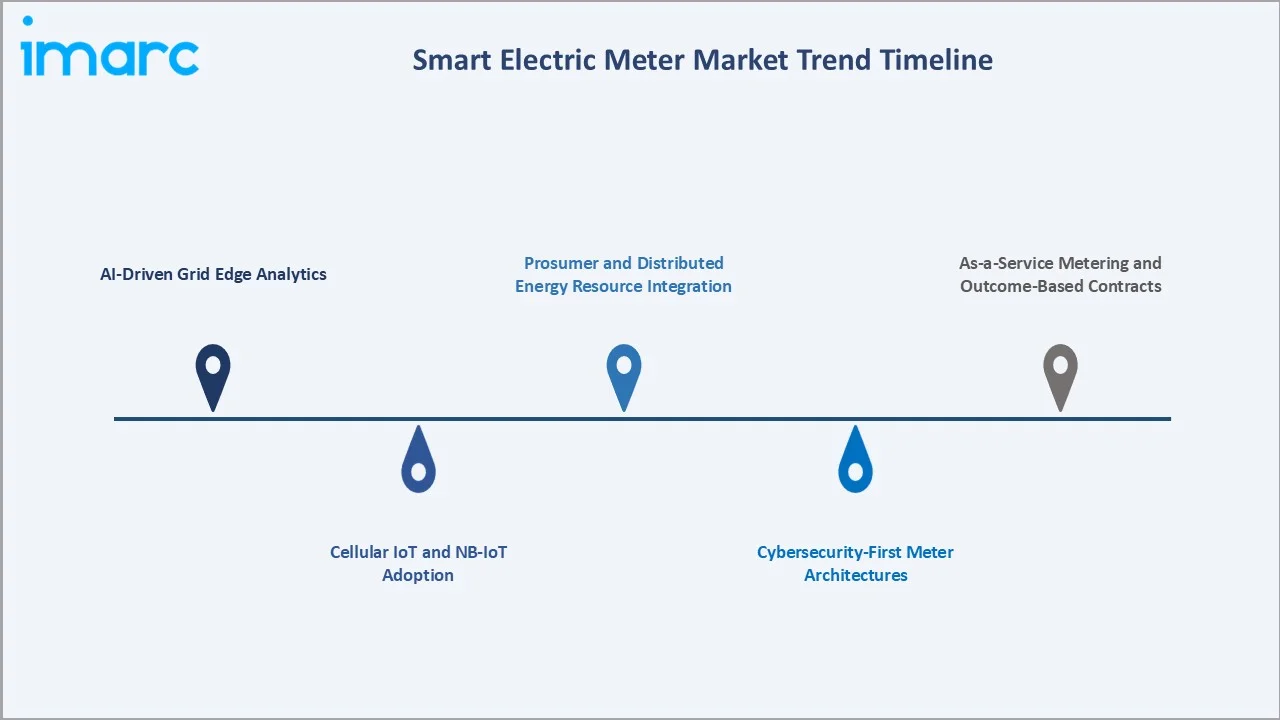

Emerging Market Trends

1. AI-Driven Grid Edge Analytics

Smart meters are increasingly embedding machine learning capability for theft detection, voltage event diagnosis, and predictive maintenance. Itron's Riva platform and Landis+Gyr's edge intelligence offerings are reducing utility analytics latency from days to minutes, accelerating fault response.

2. Cellular IoT and NB-IoT Adoption

Utilities are transitioning from legacy 2G/3G to NB-IoT and LTE-M for smart metering connectivity. According to the GSMA, low-power wide-area technologies enable better coverage, scalability, and cost efficiency for large-scale AMI deployments.

3. Cybersecurity-First Meter Architectures

Smart meter vendors are embedding advanced security features such as secure boot and encrypted communication. Standards from National Institute of Standards and Technology and IEC 62443 guide utilities toward adopting secure, resilient metering infrastructure.

4. Prosumer and Distributed Energy Resource Integration

Rising rooftop solar penetration is driving demand for bidirectional meters that capture export and import flows. Australia, and China report household solar penetration exceeding 30%, making prosumer-ready meters a baseline procurement requirement.

5. As-a-Service Metering and Outcome-Based Contracts

Utilities are adopting Meter-as-a-Service models to convert capital expense into operating expense. Honeywell, Itron, and Sensus offer managed AMI subscriptions, including hardware, networks, software, and analytics under multi-year service contracts.

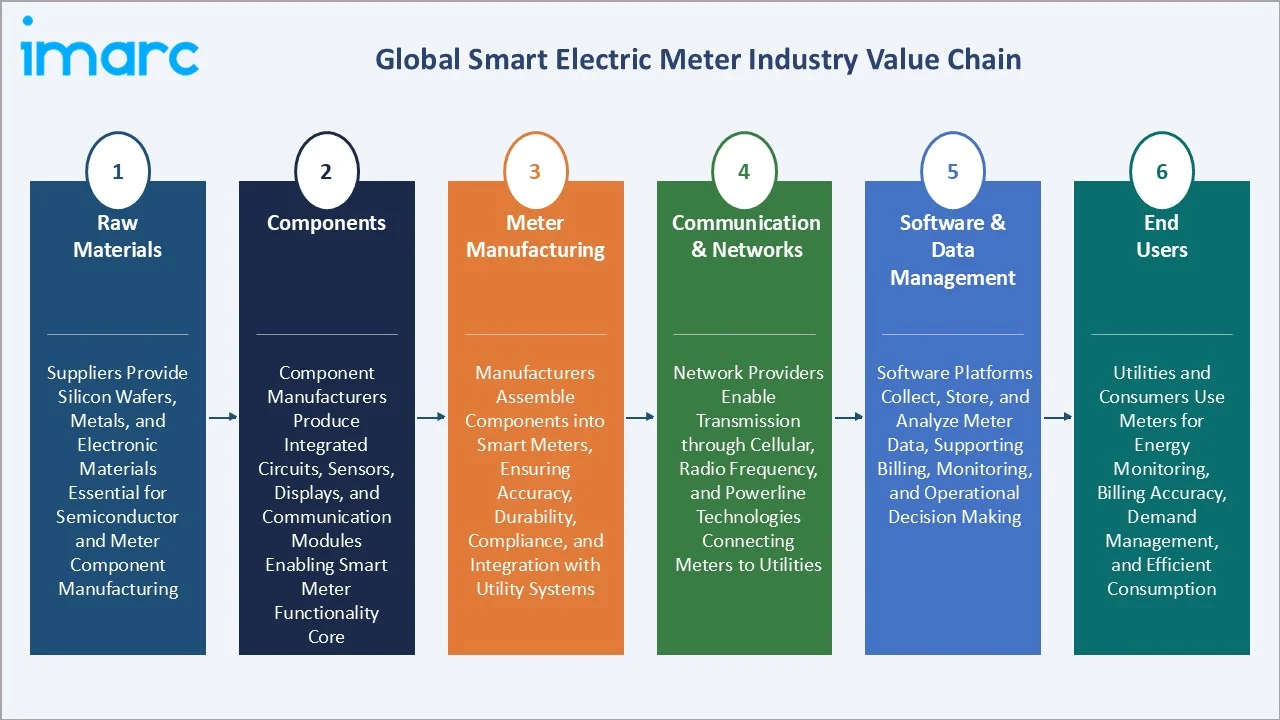

Industry Value Chain Analysis

The smart electric meter value chain spans six stages, from raw silicon to utility deployment, with each stage carrying distinctive margin dynamics, supplier concentration, and competitive intensity.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Suppliers provide silicon wafers, metals, and electronic materials essential for semiconductor and meter component manufacturing |

|

Components |

Component manufacturers produce integrated circuits, sensors, displays, and communication modules enabling smart meter functionality core |

|

Meter Manufacturing |

Manufacturers assemble components into smart meters, ensuring accuracy, durability, compliance, and integration with utility systems |

|

Communication & Networks |

Network providers enable transmission through cellular, radio frequency, and powerline technologies connecting meters to utilities |

|

Software & Data Management |

Software platforms collect, store, and analyze meter data, supporting billing, monitoring, and operational decision making |

|

End Users |

Utilities and consumers use meters for energy monitoring, billing accuracy, demand management, and efficient consumption |

Tier-1 manufacturers including Itron, Landis+Gyr, and Honeywell capture the highest value share by integrating hardware, communications, and software services into bundled offerings. Their scale enables direct utility procurement relationships, multi-year service contracts, and recurring software revenue streams that smaller component-only suppliers cannot replicate.

Technology Landscape in the Smart Electric Meter Industry

Battery and Power Management Technology

Smart meters increasingly use long-life lithium batteries, often designed to last over 10–15 years depending on usage and communication frequency. Industry insights from the International Energy Agency highlight improved power management reducing maintenance and operational costs.

Materials Innovation and Sensor Design

Modern smart meters utilize solid-state electronic sensing technologies that improve measurement accuracy and reliability. Standards such as IEC 62053 define accuracy classes, while durable materials enhance performance in varied environmental conditions.

Smart Connectivity and Communication Protocols

Cellular IoT (NB-IoT, LTE-M), RF mesh networks (Wi-SUN), and power-line communication (G3-PLC, PRIME) dominate global deployments. The GSMA and Wi-SUN Alliance highlight growing adoption of interoperable, scalable connectivity solutions.

Automation, AI, and Edge Computing

Edge processing in next-generation meters enables real-time anomaly detection, theft analytics, and predictive load forecasting. Itron's Gen5 and Landis+Gyr's E360 platforms incorporate ARM Cortex-class processors that bring utility-grade analytics directly to the meter endpoint.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Advanced Metering Infrastructure (AMI) | 57.8% | 2025 |

| Phase | Single Phase | 62.3% | 2025 |

| End User | Residential | 86.7% | 2025 |

| Region | North America | 40.9% | 2025 |

By Type

Advanced Metering Infrastructure (AMI) holds a commanding 57.8% share in 2025, driven by two-way communication, demand response readiness, and outage management capability. AMI is the default architecture for new utility procurements across North America, Europe, and large parts of Asia-Pacific.

To access detailed market analysis, Request Sample

Automatic Meter Reading (AMR) accounts for 42.2% in 2025, primarily serving cost-sensitive deployments and brownfield meter replacements where utilities prioritize lower upfront cost over advanced functionality. AMR-to-AMI transitions remain a key market growth lever through 2034, particularly across emerging markets.

By Phase

Single Phase smart meters dominate with a 62.3% share in 2025, reflecting their use across residential and small commercial accounts that represent the largest meter volume globally. Lower unit cost and simpler installation requirements support continued single-phase preference.

Three Phase meters hold 37.7% in 2025, concentrated in commercial, industrial, and large institutional accounts. They generate higher revenue per unit due to enhanced measurement capability, demand recording, and power quality features required by C&I customers under time-of-use tariffs.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

40.9% |

Mature AMI deployments across the U.S. and Canada; FERC and DOE grid modernization funding; investor-owned utility programs |

|

Asia-Pacific |

26.4% |

Large-scale rollouts in China and India; State Grid smart meter procurement; Bharat Smart Meter National Programme |

|

Europe |

21.8% |

EU energy efficiency directives; UK SMETS2 rollout; Germany and France digital grid investment |

|

Latin America |

6.5% |

Brazil and Mexico utility modernization; ANEEL regulatory mandates; non-technical loss reduction targets |

|

Middle East & Africa |

4.4% |

GCC smart city programs; Saudi Vision 2030 utility upgrades; African pre-paid metering expansion |

North America commands a 40.9% global in 2025, reflecting its leadership in AMI deployment maturity. The U.S. has installed more than 135 million smart electric meters, with deployments led by major investor-owned utilities. Federal stimulus through the IRA and DOE programs is funding next-generation AMI 2.0 upgrades, accelerating replacement cycles through the forecast period.

Asia-Pacific, with 26.4% in 2025, is the fastest-growing region, fueled by India's Revamped Distribution Sector Scheme targeting roughly 250 million smart meters and China's State Grid completing more than 500 million installations to date. Europe at 21.8% benefits from the UK's SMETS2 rollout and EU directives mandating member-state smart meter coverage targets above 80%, anchoring stable procurement demand through 2034.

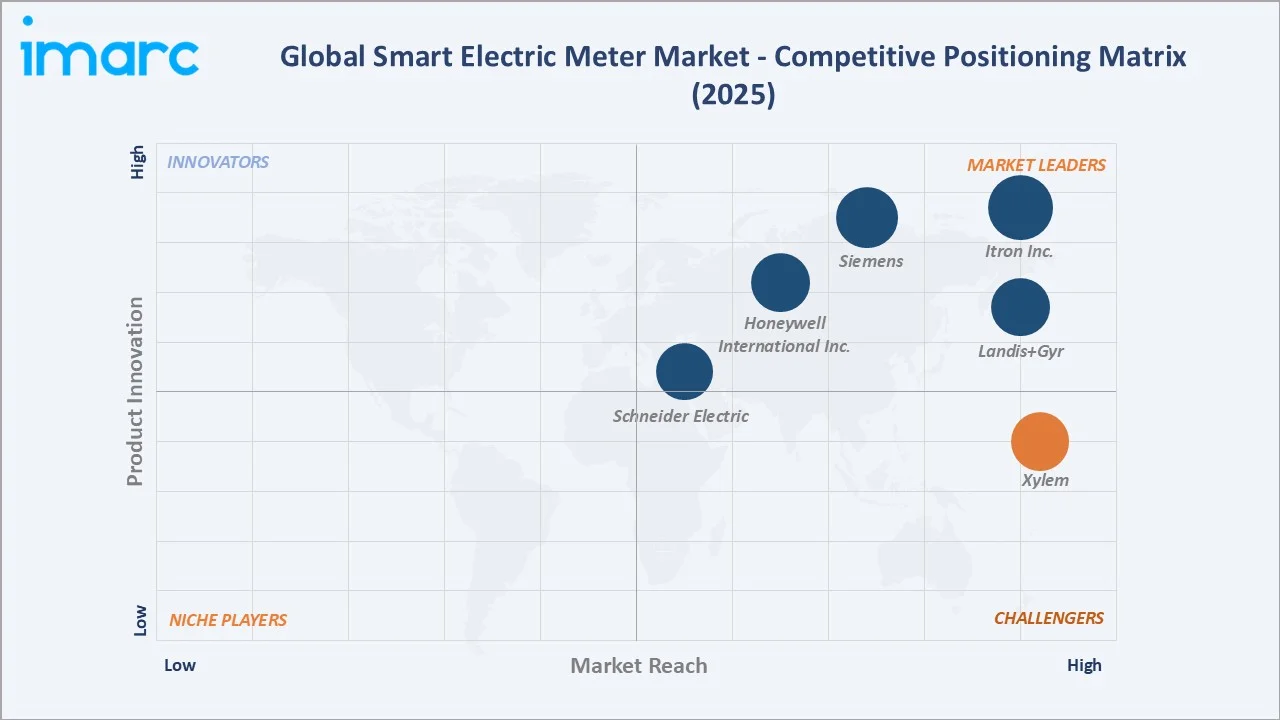

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Itron Inc. |

OpenWay Riva / CENTRON |

Leader |

Global AMI scale, IoT meter platforms, edge analytics |

|

Landis+Gyr |

Revelo®, E360 |

Leader |

End-to-end smart grid solutions, European utility base |

|

Honeywell International Inc. |

EnergyAxis, REX2 |

Leader |

Multi-utility metering, gas/electric integration |

|

Siemens |

SICAM P Series |

Leader |

Industrial-grade meters, grid automation integration |

|

Schneider Electric |

EcoStruxure |

Leader |

Smart grid software, C&I metering portfolio |

|

Xylem |

Stratus IQ+ |

Challenger |

RF mesh communications, water-electric AMI |

The smart electric meter market is led by a small group of global players competing alongside regional specialists and emerging Asian manufacturers. Itron Inc. reported FY2024 revenue of approximately USD 2.4 Billion, while Landis+Gyr generated USD 1,729.3 million in FY2024. Together with Honeywell's Elster business and Siemens' metering operations, the top tier accounts for a meaningful share of global AMI procurement.

Key Company Profiles

Itron Inc.

Itron Inc., based in Liberty Lake, USA, provides smart metering, grid edge intelligence, and energy management solutions. Operating globally, it delivers devices, networking platforms, software, and services, with FY2024 revenue of about USD 2.4 billion.

- Product & Service Portfolio: OpenWay Riva smart meters, Gen5/GenX IoT network platforms, Itron Enterprise Edition (MDM), Distributed Intelligence (DI) applications, grid edge analytics, and Outcomes-as-a-Service solutions for utilities.

- Recent Developments: In 2024, Itron Inc. introduced ATLM/ATVM applications enabling real-time transformer load and voltage monitoring. These DI-enabled solutions improve low-voltage grid visibility, support DER integration (EVs, solar), reduce outages, and extend transformer life through predictive insights and API-driven analytics.

- Strategic Focus: Itron focuses on advancing grid edge intelligence through cellular IoT, distributed analytics, and software-driven recurring revenue models while expanding managed services across global utility networks.

Landis+Gyr

Landis+Gyr, headquartered in Cham, Switzerland, is a global provider of smart metering and grid management solutions. Operating across multiple regions, the company has deployed over 300 million devices and reported FY2024 revenue of about USD 1,729.3 million.

- Product & Service Portfolio: E360 and E660 smart meters, Revelo grid edge meters, Gridstream IoT/AMI platform, AIM (Advanced Information Management) software, and managed services for utility analytics and operations.

- Recent Developments: In 2025, Landis+Gyr and Sense announced the introduction of 1MHz sampling for the Revelo® platform at DISTRIBUTECH 2025, enabling ultra-high-resolution data and on-meter AI. The upgrade supports arc-fault detection, real-time grid monitoring, DER integration, and improved reliability, transforming AMI 2.0 meters into advanced sensing and analytics platforms for modern utilities.

- Strategic Focus: Landis+Gyr prioritizes grid edge intelligence, AMI 2.0 leadership, and software-led recurring revenue, supported by partnerships with hyperscale cloud providers for utility data analytics.

Honeywell International Inc.

Honeywell International Inc., headquartered in Charlotte, USA, operates a global smart metering business through its Elster solutions. The company provides electricity, gas, and water metering technologies, supporting utilities worldwide with large-scale deployments and advanced energy management systems.

- Product & Service Portfolio: Honeywell offers EnergyAxis AMI systems, A3 ALPHA and REX2 electric meters, A1140 smart meters, and integrated multi-utility metering and analytics solutions across electricity, gas, and water networks.

- Recent Developments: In 2024, Honeywell International Inc. launched Honeywell Forge Performance+ for Utilities, integrating AI, machine learning, and digital twin technologies. The platform delivers real-time analytics, predictive asset management, and supports DER and demand response, improving grid reliability, operational efficiency, and utility decision-making capabilities.

- Strategic Focus: Honeywell focuses on software-driven, cybersecurity-enabled multi-utility metering and energy management platforms, aligned with digital transformation, grid modernization, and portfolio optimization across its automation and smart infrastructure businesses.

Market Concentration Analysis

The global smart electric meter market is moderately concentrated at the top, with Itron Inc., Landis+Gyr, Honeywell International Inc., Siemens, Schneider Electric collectively accounting for approximately 50 to 55% of global revenue in 2025, supported by deep utility relationships, large installed bases, and end-to-end solution capability.

Fragmentation increases substantially in regional and emerging markets, where players such as Wasion, Holley Technology, Hexing Electric, and Iskraemeco compete actively in cost-sensitive deployments. China hosts dozens of domestic smart meter manufacturers, many of which participate in large-scale procurement programs led by State Grid Corporation of China and China Southern Power Grid, making it the world’s largest smart meter supply base.

Consolidation continues through M&A and portfolio repositioning. Itron acquired Elpis Squared in March 2024 for approximately USD 35 million to strengthen its grid edge intelligence portfolio, while cybersecurity, software depth, and AMI 2.0 capability requirements are accelerating consolidation pressure on smaller, hardware-only manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

Advanced Metering Infrastructure (AMI) remains the fastest-growing type segment through 2034, supported by utility AMI 2.0 upgrade cycles in mature markets and greenfield rollouts in emerging economies. Three phase commercial and industrial meters offer above-average revenue per endpoint, making them attractive premium opportunities.

Emerging Market Expansion

Asia-Pacific, accounting for 26.4% in 2025, represents the largest forward-looking opportunity. India's USD 36+ Billion Revamped Distribution Sector Scheme, combined with Vietnam, Indonesia, and the Philippines AMI initiatives, will drive multi-year procurement demand. Latin America, especially Brazil and Mexico, offers similar growth tailwinds anchored by ANEEL and CRE regulatory mandates.

Venture & Strategic Investment Trends

Investment in adjacent grid edge, cybersecurity, and meter analytics technology is intensifying. Major venture capital and strategic capital flowed into companies including Bidgely, AutoGrid, Sense, and Utilidata in recent funding rounds. Established meter OEMs are also pursuing tuck-in acquisitions in software and analytics to defend against pure-software competitors targeting utility wallet share.

Future Market Outlook (2026-2034)

The global smart electric meter market forecast projects sustained value expansion from USD 29.17 Billion in 2025 to USD 50.43 Billion by 2034 at a CAGR of 6.09%, representing an incremental value addition of more than USD 21 Billion over the forecast period. Growth will be anchored by AMI 2.0 upgrade cycles in North America, sustained EU directive-led replacement, and accelerating Asia-Pacific deployment under national distribution reform programs.

Three transformational shifts will reshape the market through 2034. First, AI-driven edge analytics will turn meters into intelligent grid sensors capable of theft detection and predictive maintenance. Second, prosumer-ready bidirectional metering will become standard as solar PV and EV adoption expand. Third, Meter-as-a-Service contracting will accelerate, shifting utility spending toward multi-year managed agreements with integrated software and analytics.

By 2034, the smart electric meter is expected to evolve from a metering endpoint into a programmable, secure, software-defined grid edge node. Vendors investing in cellular IoT, edge AI, and cybersecurity-hardened architectures are positioned to capture disproportionate value as the market transitions from hardware-led procurement toward software-driven, outcome-based utility contracting models.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024 and 2025 with smart electric meter industry stakeholders, including utility procurement officers at investor-owned utilities, OEM product management leaders at top-tier manufacturers, regulatory affairs specialists, AMI deployment engineers, and energy regulators across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary sources include company annual reports (Itron, Landis+Gyr, Honeywell, Siemens, Schneider Electric), regulatory publications (FERC, ENISA, NERC, CERC, ANEEL), industry association data (EEI, EURELECTRIC, IEEE), government publications (DOE, EU Commission energy directives), and trade media including Smart Energy International and T&D World.

Forecasting Models

Market sizing and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating utility CAPEX data, regulatory deployment targets, regional installed-base analysis, meter replacement cycle modeling, and scenario analysis under base, optimistic, and conservative macroeconomic assumptions.

Smart Electric Meter Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Advanced Metering Infrastructure (AMI), Automatic Meter Reading (AMR) |

| Phases Covered | Single Phase, Three Phase |

| End Users Covered | Industrial, Commercial, Residential |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Itron Inc., Landis+Gyr, Honeywell International Inc., Siemens, Schneider Electric, Xylem, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the smart electric meter market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global smart electric meter market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the smart electric meter industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Smart Electric Meter Market Report

The global smart electric meter market was valued at USD 29.17 Billion in 2025, driven by utility digitalization, AMI rollouts, renewable integration, and grid modernization investment programs.

The market is projected to reach USD 50.43 Billion by 2034, growing at a CAGR of 6.09% during 2026-2034, supported by AMI 2.0 upgrades, Asia-Pacific deployments, and edge analytics.

Advanced Metering Infrastructure (AMI) leads with a 57.8% share in 2025, supported by two-way communication, demand response readiness, and superior outage management versus AMR systems.

Single Phase meters command a 62.3% share in 2025, anchored by residential and small commercial accounts, which represent the largest meter volume across global utility deployments.

North America leads with a 40.9% share in 2025, supported by mature AMI deployments, IRA and DOE grid funding, and AMI 2.0 upgrade cycles across major U.S. utilities.

Key drivers include grid modernization mandates, renewable integration, utility cost reduction, demand response programs, time-of-use tariffs, and government funding for smart grid infrastructure.

Asia-Pacific is fastest-growing, driven by India's target of 250 million smart meters under the Revamped Distribution Sector Scheme and China's State Grid deployment exceeding 500 million units.

Leading companies include Itron Inc., Landis+Gyr, Honeywell International Inc., Siemens, Schneider Electric, and Xylem, among others.

Automatic Meter Reading (AMR) holds a 42.2% share in 2025, primarily serving cost-sensitive deployments and brownfield meter replacements where lower upfront cost outweighs advanced AMI functionality.

AMI growth is driven by demand response capability, real-time outage management, distributed energy integration, and regulatory mandates for two-way communication and time-of-use billing.

AI-driven edge analytics, NB-IoT, Wi-SUN mesh networks, and cybersecurity-hardened firmware are improving meter intelligence, reducing operational costs, and enabling outcome-based service contracting.

Residential users represent the largest end-user segment, driven by single phase meter dominance, while commercial and industrial users contribute disproportionate revenue per endpoint via three phase pricing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)