Smart Thermostat Market Size, Share, Trends and Forecast by Product, Component, Technology, Application, and Region, 2026-2034

Global Smart Thermostat Market Size, Share, Trends & Forecast (2026-2034)

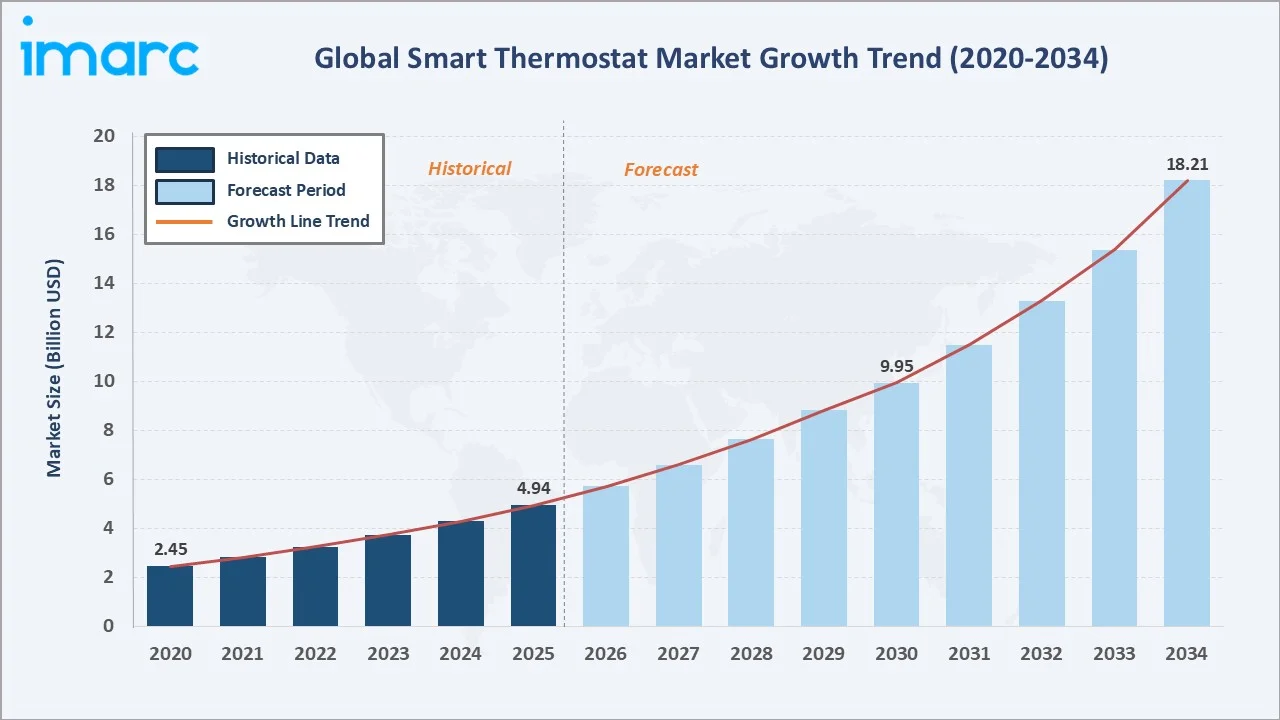

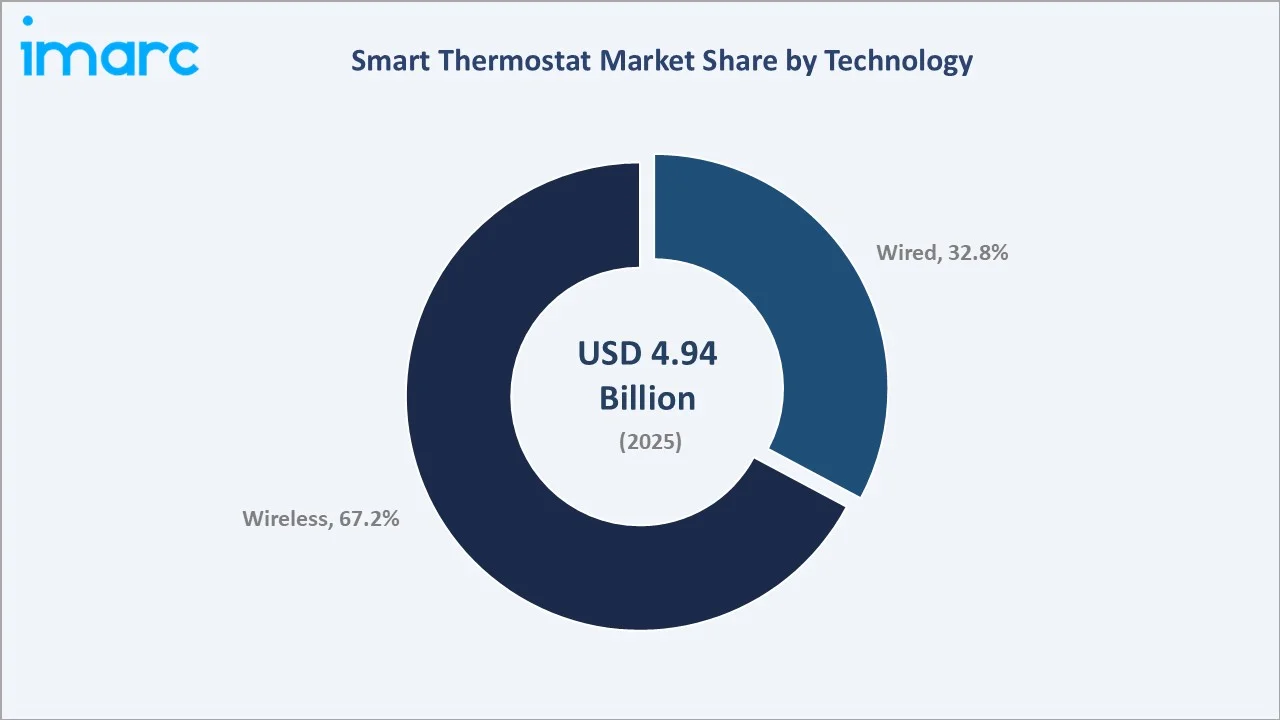

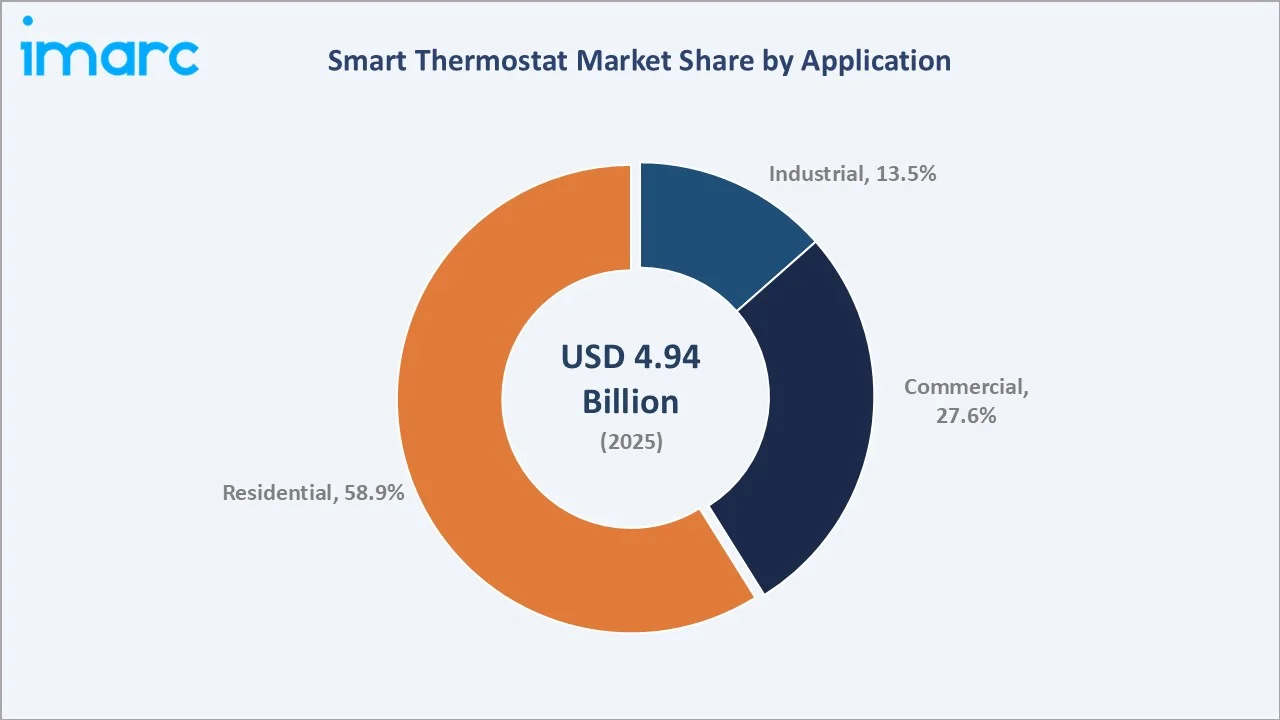

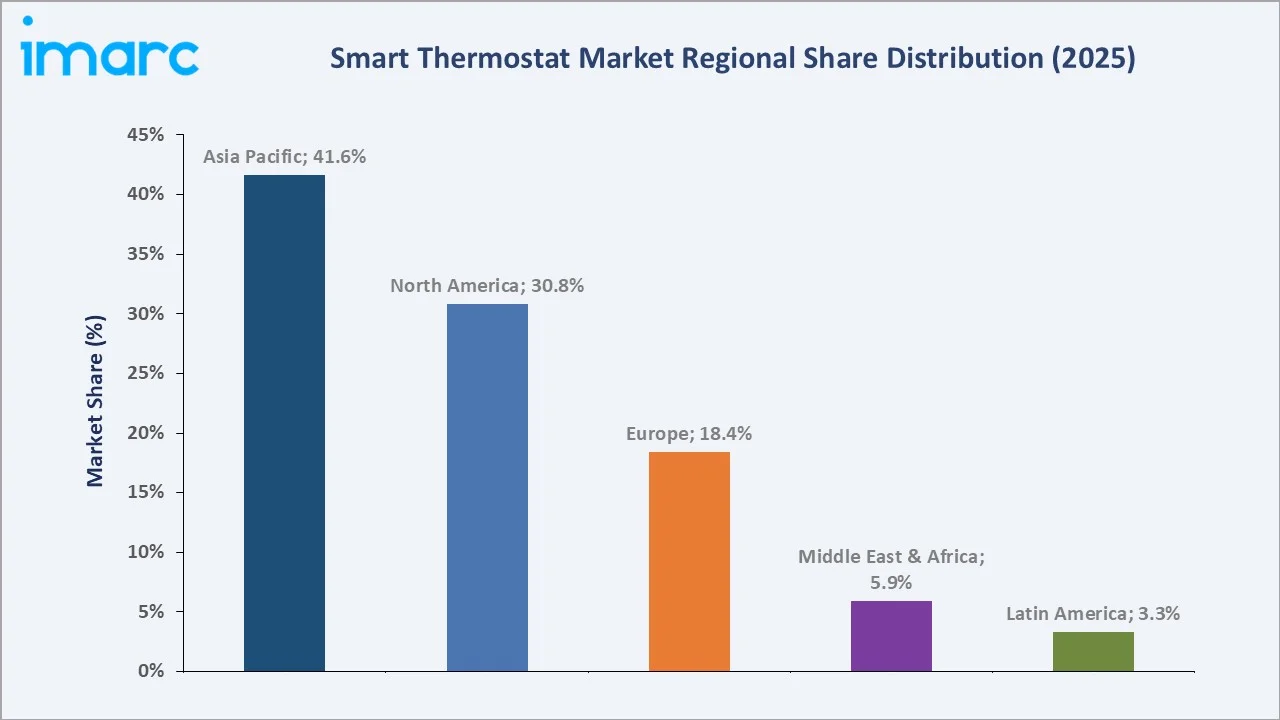

The global smart thermostat market size was valued at USD 4.94 Billion in 2025 and is projected to reach USD 18.21 Billion by 2034, exhibiting a CAGR of 15.05% during the forecast period 2026-2034. Accelerating smart-home penetration, rising HVAC energy efficiency mandates, and expanding voice-assistant ecosystems are driving the smart thermostat market growth. Residential applications lead at 58.9% share in 2025, while wireless technology accounts for 67.2% of global installations. Asia Pacific dominates with 41.6% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.94 Billion |

|

Forecast Market Size (2034) |

USD 18.21 Billion |

|

CAGR (2026-2034) |

15.05% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (41.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~16.1%) |

|

Leading Technology |

Wireless (67.2%, 2025) |

|

Leading Application |

Residential (58.9%, 2025) |

The global smart thermostat market growth trajectory from 2020 through 2034 contrasts historical expansion against a sustained forecast curve powered by AI-led energy management, voice control adoption, and tightening building efficiency codes across residential and commercial segments.

To get more information on this market, Request Sample

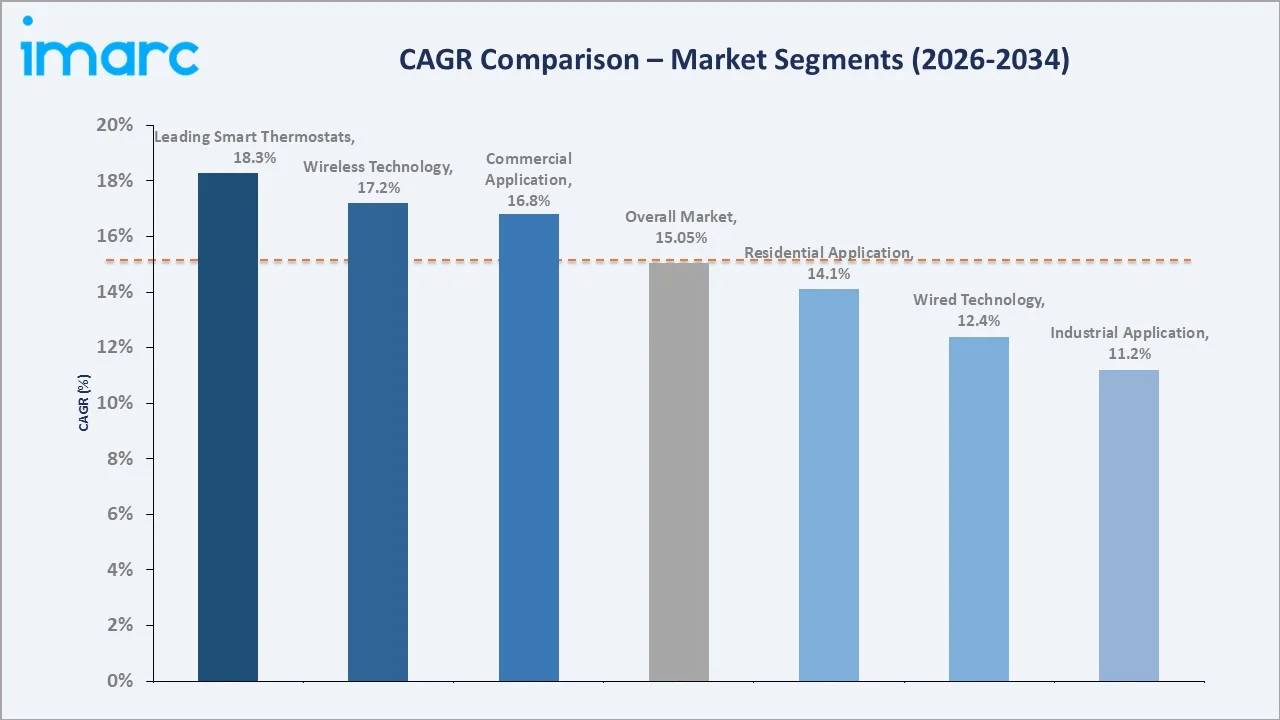

Segment-level CAGR comparisons highlight learning thermostat adoption and wireless technology expansion as the fastest-growing sub-categories within the global smart thermostat market forecast through 2034.

Executive Summary

The global smart thermostat market is undergoing a rapid transformation. It is propelled by smart-home ecosystem maturity, tightening energy efficiency codes, and consumer demand for connected climate control. Valued at USD 4.94 Billion in 2025, the market is forecast to reach USD 18.21 Billion by 2034 at a CAGR of 15.05%.

Wireless technology commands 67.2% share in 2025, driven by Wi-Fi and ZigBee adoption across retrofit and new-build installations. Residential applications account for 58.9% of global demand, while commercial is the fastest-growing end-user category at an estimated CAGR of 16.8% through 2030. Learning smart thermostats represent the premium growth tier with AI-led behavioral algorithms.

Asia Pacific leads with 41.6% global revenue share in 2025. North America holds 30.8% and Europe 18.4%. The smart thermostat market outlook remains positive as utility rebate programs, rooftop solar pairing, and Matter protocol standardization converge across major markets.

Key Market Insights

|

Insight |

Data |

|

Largest Technology |

Wireless – 67.2% share (2025) |

|

Second Technology |

Wired – 32.8% share (2025) |

|

Largest Application |

Residential – 58.9% share (2025) |

|

Fastest Growing Application |

Commercial – ~16.8% CAGR (2025-2030) |

|

Leading Region |

Asia Pacific – 41.6% revenue share (2025) |

|

Top Companies |

Alphabet Inc, Resideo Technologies Inc, Ecobee, Emerson, Carrier, Schneider Electric |

|

Connected Device Demand |

42 million units (2025) |

Key Analytical Observations Supporting the Above Data:

- Wireless' 67.2% dominance in 2025 reflects mainstream Wi-Fi adoption and the shift toward app-controlled HVAC systems in retrofit installations, where conduit-free deployment is a decisive advantage.

- Wired's 32.8% share remains anchored by commercial buildings and new-built residential projects, where structured cabling supports deep integration with building management systems.

- Residential applications' 58.9% majority is underpinned by global smart-home unit sales crossing 870 million devices in 2025, with thermostats ranking among the top five connected categories alongside speakers and cameras.

- Asia Pacific's 41.6% global dominance reflects China's district heating modernization push and India's accelerating air-conditioning penetration, which reached 26 units per 100 households in urban centers by 2024.

- Around 19 Million Connected smart thermostat were installed in the US in 2025, driven by utility demand-response incentives, Matter protocol rollout, and tightening EU Energy Performance of Buildings Directive (EPBD) requirements.

- Learning thermostats represent the highest-growth product tier at an estimated 18.3% CAGR through 2030, driven by AI-led behavioral algorithms that can cut heating costs by 10-12% per household annually.

Global Smart Thermostat Market Overview

Smart thermostats are internet-connected climate control devices that regulate heating, ventilation, and air conditioning (HVAC) systems through Wi-Fi, ZigBee, Z-Wave, or proprietary wireless protocols. The global market covers standalone, connected, and learning variants equipped with temperature, humidity, motion, and occupancy sensors. These products integrate with leading smart-home ecosystems such as Google Home, Amazon Alexa, and Apple HomeKit.

The industry operates at the intersection of IoT maturity, utility demand-response programs, building energy codes, and rising consumer climate-cost awareness. Growth is anchored by macro drivers such as Matter protocol standardization, heat-pump adoption accelerated by decarbonization policy, and the rapid expansion of smart-city infrastructure in Asia Pacific and the Middle East.

Market Dynamics

To evaluate market opportunities, Request Sample

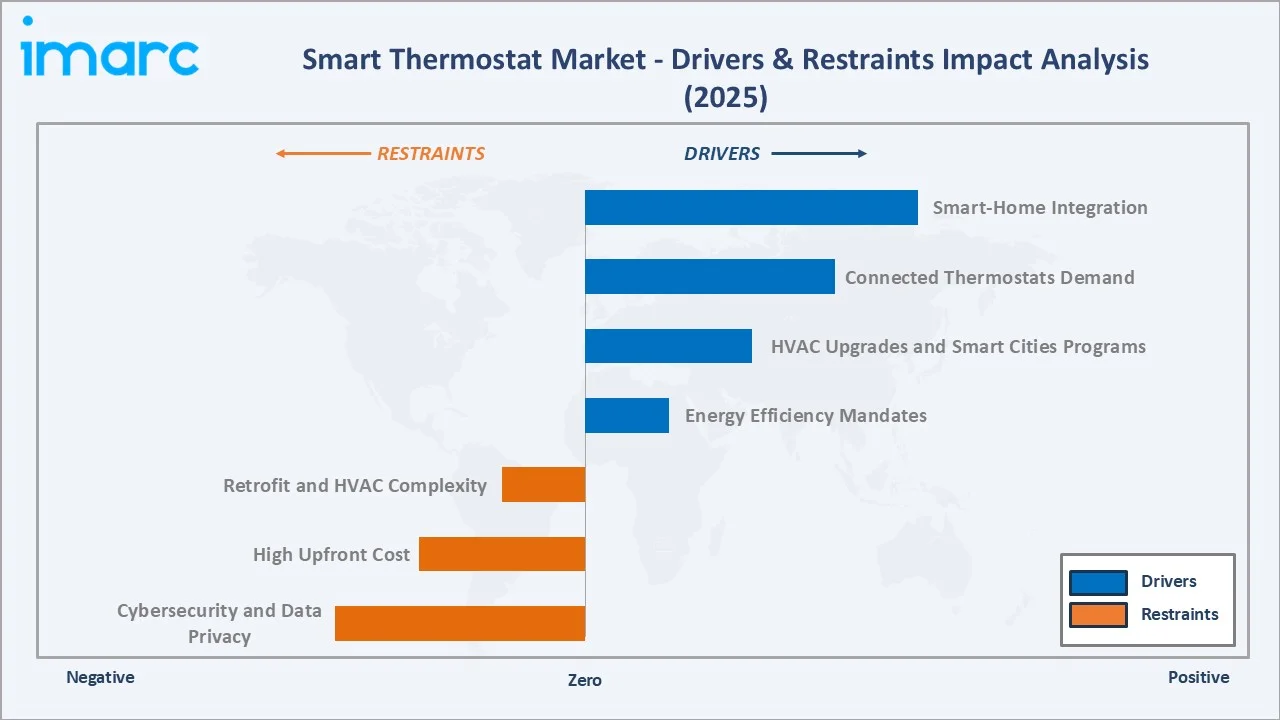

Market Drivers

- HVAC Upgrades and Smart Cities Programs: Global decarbonization commitments and smart-city investment pipelines are driving HVAC modernization. The U.S. Inflation Reduction Act represents approximately USD 430 billion in total climate and economic incentives, including targeted funding for building energy efficiency, while China’s 14th Five-Year Plan emphasizes large-scale building retrofits and green construction through regulatory targets rather than a consolidated investment figure.

- Energy Efficiency Mandates: Regulatory frameworks are reshaping thermostat specifications worldwide. The EU’s revised Energy Performance of Buildings Directive (EPBD), effective from 2024, mandates the adoption of building automation and control systems in non-residential buildings, with capacity thresholds progressively reduced to around 70 kW by 2030. In the U.S., ENERGY STAR-certified smart thermostats deliver average energy savings of approximately 8% on heating and cooling, supporting increased adoption of connected HVAC control solutions.

- Connected Thermostats Demand: Smart-home ecosystem penetration crossed 22% of global households in 2024 and is projected to reach 38% by 2030. The rapid expansion of voice assistants, Matter-certified devices, and interoperable climate platforms is converting the thermostat from a passive appliance into a central node in the connected home.

- Smart-Home Integration: Deep integration with ecosystems such as Google Home, Amazon Alexa, Apple HomeKit, and Samsung SmartThings is driving cross-category bundling. Utility partnerships with Nest, Ecobee, and Honeywell deliver thermostats to subscribers at reduced cost, lowering purchase friction for mass-market consumers.

Market Restraints

- High Upfront Cost: Premium learning thermostats retail between USD 180 and USD 280, limiting adoption in price-sensitive developing markets where standard manual thermostats cost under USD 30.

- Cybersecurity and Data Privacy: Connected thermostats collect occupancy, temperature, and behavioral data, creating privacy and breach concerns that slow procurement in enterprise and healthcare settings.

- Retrofit and HVAC Complexity: Compatibility issues with older HVAC systems, C-wire requirements, and multi-zone configurations add installation friction, particularly for DIY consumers and aging building stock.

Market Opportunities

- AI-Led Energy Optimization: Learning algorithms that integrate weather data, occupancy patterns, and real-time utility pricing can reduce household HVAC costs by 10% annually. This creates a high-margin product tier with strong consumer willingness to pay.

- Utility Demand-Response Programs: Utility-led demand-response programs and rebate schemes across North America and Europe continue to incentivize smart thermostat adoption, with incentive spending forming a key component of a multi-billion-dollar demand-response ecosystem, creating a structurally funded channel for OEMs to scale connected device installations.

Market Challenges

- Interoperability Fragmentation: Competing protocols including Wi-Fi, ZigBee, Z-Wave, Thread, and proprietary radios create compatibility headaches for consumers and integrators, slowing adoption until Matter standardization matures fully through 2026-2027.

- Distribution Channel Complexity: Serving HVAC contractors, big-box retail, utility partnerships, and direct-to-consumer e-commerce simultaneously requires differentiated pricing, SKUs, and after-sales support that strain smaller manufacturers.

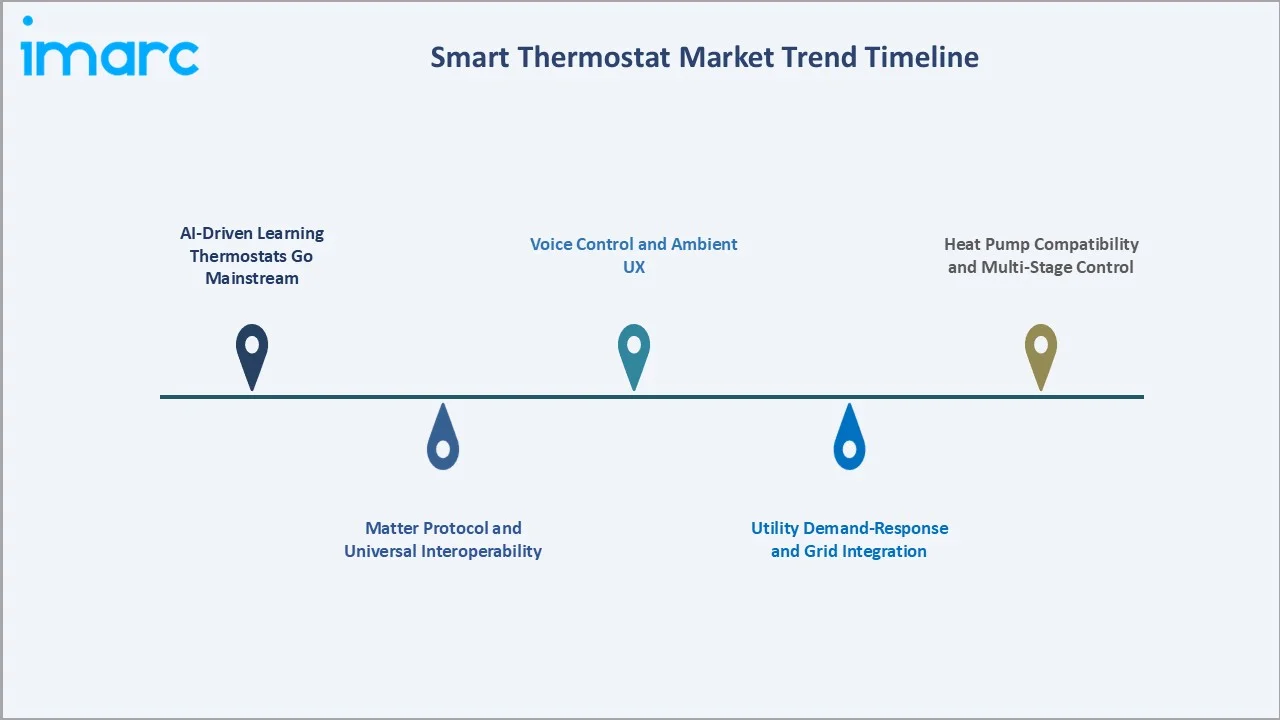

Emerging Market Trends

1. AI-Driven Learning Thermostats Go Mainstream

Machine learning-enabled smart thermostats that automatically adapt to occupant schedules are increasingly defining the premium segment, with global shipments projected to reach 67.2 million units cumulatively by 2030, reflecting rapid scaling from mid-decade volumes. Brands such as Google Nest and Ecobee are embedding on-device AI models that reduce cloud dependency and improve response latency.

2. Matter Protocol and Universal Interoperability

The Matter 1.3 specification, released in May 2024, mandates cross-ecosystem compatibility for connected thermostats. Mainstream adoption is expected to accelerate installed-base growth by eliminating the vendor lock-in that deterred many household buyers through 2023.

3. Utility Demand-Response and Grid Integration

Smart thermostats are evolving into grid-interactive assets capable of modulating heating and cooling loads in response to real-time electricity prices, with demand-response programs in the United States enrolling over 10 million customers across utility and ISO/RTO markets, a category expected to double by 2028.

4. Voice Control and Ambient UX

Voice-first operation through Alexa, Google Assistant, and Siri is becoming the primary interaction mode in smart homes. Manufacturers are reducing physical button counts and emphasizing e-ink displays and ambient sensors for context-aware temperature control.

5. Heat Pump Compatibility and Multi-Stage Control

The accelerated shift to heat pumps in Europe and North America requires thermostats that can manage multi-stage heating, cooling, and auxiliary electric elements. Purpose-built thermostats optimized for heat pump systems are emerging as one of the fastest-growing product segments, supported by accelerating global heat pump adoption and electrification trends.

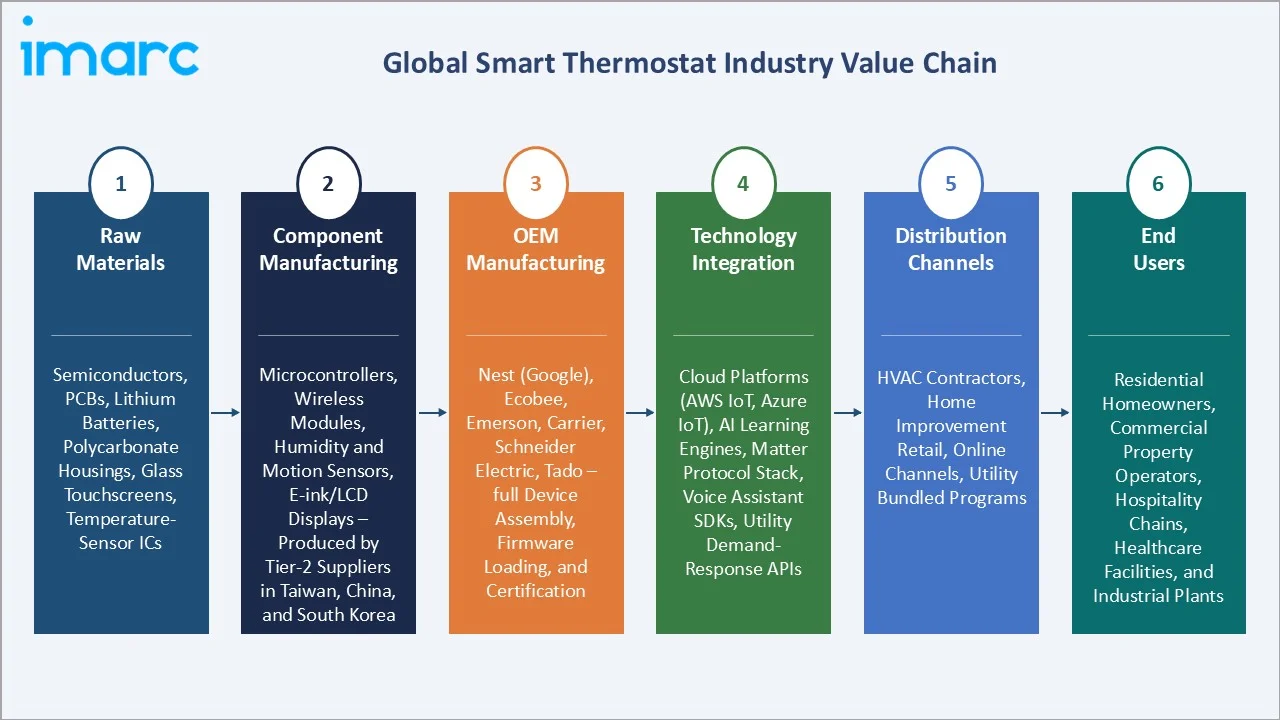

Industry Value Chain Analysis

The global smart thermostat industry value chain spans six integrated stages from raw material supply through end-consumer installation. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall smart thermostat market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Semiconductors, PCBs, lithium batteries, polycarbonate housings, glass touchscreens, temperature-sensor ICs |

|

Component Manufacturing |

Microcontrollers, wireless modules (Wi-Fi, ZigBee, Thread), humidity and motion sensors, e-ink/LCD displays – produced by Tier-2 suppliers in Taiwan, China, and South Korea |

|

OEM Manufacturing |

Google Nest, Ecobee, Emerson, Carrier, Schneider Electric, Tado – full device assembly, firmware loading, and certification |

|

Technology Integration |

Cloud platforms (AWS IoT, Azure IoT), AI learning engines, Matter protocol stack, voice assistant SDKs, utility demand-response APIs |

|

Distribution Channels |

HVAC contractors (35.2% share), home improvement retail (28.4%), online channels (~21.8% CAGR), utility bundled programs |

|

End Users |

Residential homeowners, commercial property operators, hospitality chains, healthcare facilities, and industrial plants |

OEMs capture the highest strategic value by integrating components, cloud services, and ecosystem certification into turnkey propositions. At the same time, utility partnerships and direct-to-consumer digital channels are bypassing traditional HVAC distributors, allowing manufacturers to own customer data and strengthen recurring service revenue.

Technology Landscape in the Smart Thermostat Industry

Wireless Connectivity and Protocols

Wi-Fi continues to dominate connectivity for residential smart thermostats due to its ubiquitous home coverage and direct cloud access. ZigBee and Thread are gaining share in mesh-based smart homes, while the Matter protocol is rapidly emerging as the cross-ecosystem standard. Leading manufacturers are shipping dual-radio models to hedge against fragmentation during the 2025-2027 transition period.

AI Learning and Behavioral Algorithms

Learning thermostats employ on-device and cloud-based machine learning to model household schedules, occupancy patterns, and thermal lag. Nest Labs' auto-schedule feature, refined across more than a decade of production data, and Ecobee's SmartSensor occupancy logic exemplify algorithmic differentiation. Edge AI adoption is rising to reduce latency and address data privacy concerns.

Sensor Integration and Materials Innovation

Modern smart thermostats integrate temperature, humidity, motion, ambient light, and air quality sensors in compact housings. Touch-capacitive glass interfaces, low-power e-ink displays, and PVD-coated metallic finishes are elevating the category from utilitarian to design-led. Lead-free solder and recycled polymer enclosures are becoming standard to meet RoHS and EU Ecodesign mandates.

Smart-Home and Grid Automation

Integration with leading smart-home hubs and voice platforms is table stakes. The frontier is grid-interactive buildings, where thermostats coordinate with solar inverters, EV chargers, and battery storage to optimize self-consumption and participate in demand-response markets. U.S. and European utilities are actively subsidizing these grid-ready devices through 2030.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global smart thermostat market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on technology and application.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Learning Smart Thermostats | 🔒 | 2025 |

| Component | 🔒 | 🔒 | 2025 |

| Technology | Wireless | 67.2% | 2025 |

| Application | Residential | 58.9% | 2025 |

| Region | Asia Pacific | 41.6% | 2025 |

By Technology

Wireless smart thermostats lead the global market with a 67.2% share in 2025. Demand is driven by retrofit-friendly Wi-Fi installation, voice-assistant compatibility, and the rapid proliferation of smart-home ecosystems. The global wireless sub-segment was valued at approximately USD 3.32 Billion in 2025 and is projected to grow at 17.2% CAGR through 2030. Wi-Fi remains the dominant protocol, while ZigBee and Thread adoption is accelerating for mesh-network deployments.

To access detailed market analysis, Request Sample

Wired smart thermostats account for 32.8% of global technology demand. This segment anchors commercial installations and new residential construction, where structured cabling and C-wire availability simplify integration with multi-stage HVAC and building management systems. Consumer preference for reliability in mission-critical commercial sites such as data centers and hospitals sustains wired demand despite wireless growth.

By Application

Residential leads the global smart thermostat market with a 58.9% share in 2025. U.S. single-family housing starts reached 1.01 million units in 2024, a 6.5% year-over-year increase per the U.S. Census Bureau. Utility rebate programs in North America and Europe are accelerating home-owner replacement cycles. Premium residential consumers in the U.S. and Germany are the primary adopters of learning thermostats.

Commercial users represent 27.6% of global demand and are the fastest-growing segment, expanding at an estimated CAGR of 16.8% from 2025 to 2030. Office modernization, hotel chain renovations, and retail store rollouts drive demand. The EU's EPBD mandate for building automation in large non-residential facilities will structurally lift commercial adoption through 2030. Industrial users (13.5%) serve manufacturing, cold chain, and laboratory facilities with specification-grade multi-zone thermostats.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

41.6% |

China HVAC modernization, India Smart Cities Mission, Japan heat-pump subsidies, ASEAN AC penetration |

|

North America |

30.8% |

U.S. utility rebate programs, IRA funding, ENERGY STAR specifications, smart-home adoption |

|

Europe |

18.4% |

EU EPBD 2024 revision, heat-pump rollout, Germany BEG subsidies, UK Boiler Upgrade Scheme |

|

Middle East & Africa |

5.9% |

GCC smart-city projects (NEOM, Masdar), Dubai Green Building regulation, hotel chain expansion |

|

Latin America |

3.3% |

Brazil and Mexico middle-class AC adoption, hospitality investments, solar self-consumption pairing |

Asia Pacific commands 41.6% global revenue share in 2025. China is the single largest national market, combining district heating modernization with rapid air-conditioning penetration and aggressive smart-home rollouts by Xiaomi, Haier, and Midea. India’s Smart Cities Mission encompasses investments exceeding ₹1.6 lakh crore across urban infrastructure projects, creating a structured pipeline for the deployment of connected building and smart city technologies. Asia Pacific is expected to be the fastest-growing regional market, driven by rapid urbanization, smart city initiatives, and increasing adoption of connected home technologies.

North America holds 30.8% of global revenue, anchored by U.S. utilities which offer widespread rebate and demand-response incentive programs for smart thermostats, with millions of devices enrolled and incentive values typically ranging from $50 to $200 per unit, forming part of broader multi-billion-dollar energy efficiency program spending.

Europe holds 18.4%, characterized by strict building codes, aggressive heat-pump deployment, and renovation activity in Germany, France, and the UK. The EU's EPBD revision entered into force in May 2024, reinforcing automation mandates in commercial buildings. The Middle East and Africa represent 5.9%, driven by GCC mega-projects and Dubai's Green Building regulation expansion in 2025. Latin America accounts for 3.3%, led by Brazil, Mexico, and Chile through middle-class air-conditioning adoption and rooftop solar pairing.

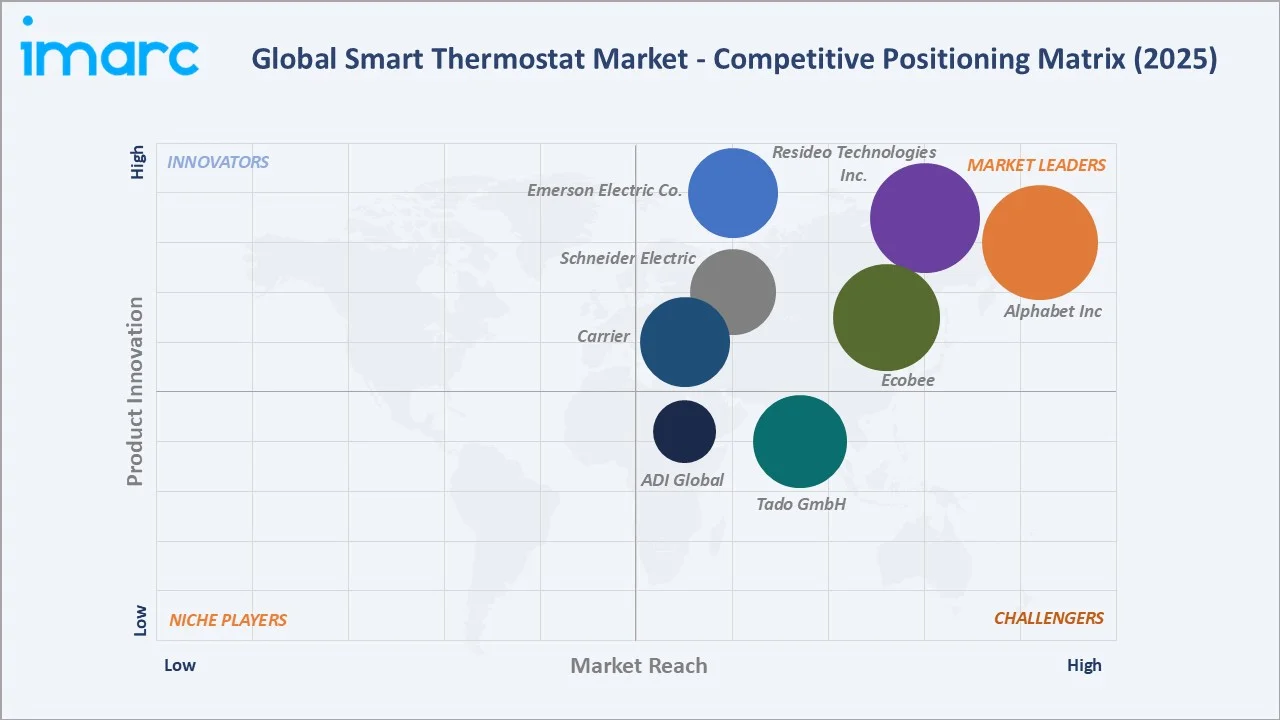

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Alphabet Inc |

Google Nest |

Leader |

AI-led learning, Google Home integration, design leadership |

|

Resideo Technologies Inc. |

Resideo, Resideo Pro |

Leader |

HVAC contractor network, global scale, commercial strength |

|

Ecobee |

Ecobee |

Leader |

Occupancy sensing, premium positioning, HomeKit leadership |

|

Emerson Electric Co. |

Sensi |

Leader |

Professional HVAC channel, Copeland heat-pump integration |

|

Schneider Electric |

Schneider Electric |

Leader |

Building automation, European commercial presence |

|

Carrier |

Carrier |

Leader |

HVAC OEM integration, heat-pump specification leadership |

|

Tado GmbH |

Tado |

Challenger |

European energy management, multi-room control |

|

ADI Global |

Control4 |

Challenger |

Luxury home automation, dealer-installed premium systems |

The global smart thermostat market's competitive landscape is moderately consolidated. Global powerhouses with deep cloud and AI capabilities compete alongside HVAC-native OEMs and regional specialists. Leading players compete on ecosystem integration, algorithm sophistication, utility partnership depth, and design differentiation. Strategic acquisitions are a key tool - Resideo acquired Snap One in June 2024 for USD 1.4 Billion to deepen its professional installer channel.

Key Company Profiles

Alphabet Inc.

Alphabet Inc. is a global technology conglomerate headquartered in Mountain View, California. Formed in October 2015 as the restructured parent of Google, Alphabet operates across internet services, hardware, cloud computing, and emerging technologies through subsidiaries including Google, Google Nest, Waymo, Verily, and DeepMind, with presence in more than 100 countries.

- Product & Platform Portfolio: Alphabet's diversified portfolio spans internet services through Google Search, YouTube, Gmail, Google Maps, and Android; hardware through Pixel smartphones, Pixel Watch, and the Google Nest smart-home line; cloud infrastructure through Google Cloud Platform and Workspace; and AI services powered by Gemini models, alongside emerging bets in autonomous driving (Waymo) and life sciences (Verily).

- Recent Developments: In August 2024, Alphabet's Google Nest division launched the 4th-generation Nest Learning Thermostat featuring a redesigned display, expanded Matter support, and improved heat-pump compatibility.

- Strategic Focus: Alphabet's strategy centres on AI-led innovation through Gemini model development, expansion of Google Cloud to compete with AWS and Azure, sustained leadership in digital advertising via Search and YouTube, and long-horizon investment in autonomous vehicles, quantum computing, and life sciences through its Other Bets portfolio.

Resideo Technologies Inc.

Resideo Technologies Inc. through its spin-off and Honeywell Building Technologies unit, is a global leader in connected thermostats and building automation. Headquartered in Charlotte, North Carolina, the company serves residential and commercial markets in more than 100 countries.

- Product & Platform Portfolio: Honeywell's portfolio spans the Honeywell Home T-series, Resideo T9 and T10 Pro, VisionPRO, and integrated building automation platforms through Honeywell Forge.

- Recent Developments: In June 2024, Resideo completed the acquisition of Snap One for approximately USD 1.4 Billion, strengthening its professional installer and custom-integration channel. Honeywell also expanded Matter certification across its consumer lineup in 2025.

- Strategic Focus: Honeywell's focus is on leveraging its unmatched HVAC contractor network, expanding cloud-based building automation through Forge, and deepening penetration in commercial and light-industrial markets globally.

Ecobee

Ecobee, Inc., a wholly owned subsidiary of Generac Holdings since 2021, is a Canadian smart home pioneer headquartered in Toronto. Ecobee launched the world's first Wi-Fi-enabled smart thermostat in 2009 and remains a premium-tier leader with particular strength in the Apple HomeKit ecosystem.

- Product & Platform Portfolio: Ecobee's portfolio includes the ecobee SmartThermostat Premium (with air quality monitor and built-in speaker), ecobee Smart Thermostat Enhanced, and SmartSensor occupancy devices for multi-room climate control.

- Recent Developments: In early 2025, Ecobee expanded its SmartSensor platform and rolled out deeper integration with Generac's home standby generator and solar ecosystem, positioning itself in the grid-interactive building category.

- Strategic Focus: Ecobee's strategy emphasizes premium design, occupancy-sensor-led energy savings, and integration with Generac's whole-home energy ecosystem for a differentiated grid-ready proposition.

Market Concentration Analysis

The global smart thermostat market exhibits moderate concentration. The top five players – Alphabet, Resideo, Ecobee, Emerson (Sensi), and Carrier - collectively account for 48-55% of global market revenue in 2025. The remaining market share is distributed across Schneider Electric, Tado, Control4 and a long tail of regional specialists including Xiaomi and Haier in China.

The market is experiencing a bifurcated dynamic. At the premium tier, consolidation is occurring around ecosystem integration, AI capability, and utility-partnership depth. Simultaneously, Chinese smart-home players such as Xiaomi, Aqara, and Haier are generating low-cost competitive pressure that is reshaping entry-level pricing in Asia Pacific and, increasingly, European retail channels. This dual dynamic is intensifying competition across price tiers through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Online channel sales are the highest-growth distribution sub-segment at an estimated 21.8% CAGR through 2030. Commercial applications are the fastest-growing end-user tier at 16.8% CAGR. Learning-enabled smart thermostats represent a key premium growth segment, supported by increasing adoption of AI-driven control features and interoperability standards such as Matter, with shipments scaling into the tens of millions annually as the market matures.

Emerging Market Expansion

India represents a high-potential emerging market, supported by low air-conditioning penetration (below 10% of households) and large-scale urban infrastructure investments under the Smart Cities Mission, with approved funding of 1.64 Lakh Crore, and Latin America's middle-class electrification collectively represent significant volume opportunities for manufacturers with localized distribution and multi-language voice support.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the competitive landscape. Resideo acquired Snap One in June 2024 for USD 1.4 Billion to deepen its professional installer channel. Venture investment continues to flow into AI energy management platforms, grid-interactive building software, and Matter-native start-ups. These are the primary focus areas for corporate and venture capital in the smart thermostat industry through 2034.

Future Market Outlook (2026-2034)

The global smart thermostat market forecast projects accelerated value expansion from USD 4.94 Billion in 2025 to USD 18.21 Billion by 2034 at a CAGR of 15.05%. Asia Pacific will retain regional leadership while accelerating structurally. North America and Europe will sustain premium value growth through utility rebate programs and EPBD-driven compliance cycles.

Three shifts will reshape the smart thermostat market through 2034. Matter protocol maturation will eliminate ecosystem lock-in and unlock mass-market adoption, making connected climate control standard in new builds by 2028-2030. Grid-interactive buildings will turn thermostats into monetizable demand-response assets. Meanwhile, Chinese smart-home players will continue to compress entry-level pricing, intensifying global competition across price tiers.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with smart thermostat industry stakeholders, including product directors at OEM manufacturers, procurement managers at commercial property developers, HVAC contractors, utility demand-response program managers, and institutional investors in building technology. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include U.S. Census Bureau housing data, ENERGY STAR program reports, International Energy Agency (IEA) building-energy publications, EU EPBD documentation, company annual reports, industry publications including ACHR News, Smart Home Magazine, and Energy Manager Today, and regional construction and utility databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, HVAC shipment data, smart-home penetration curves, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic and regulatory uncertainty.

Smart Thermostat Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Standalone Smart Thermostats, Connected Smart Thermostats, Learning Smart Thermostats |

| Components Covered | Display, Temperature Sensors, Humidity Sensors, Motion Sensors, Others |

| Technologies Covered |

|

| Applications Covered | Residential, Commercial, Industrial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Alphabet Inc, Resideo Technologies Inc., Ecobee, Emerson Electric Co., Schneider Electric, Carrier, Tado GmbH, ADI Global, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the smart thermostat market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global smart thermostat market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the smart thermostat industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Smart Thermostat Market Report

The global smart thermostat market was valued at USD 4.94 Billion in 2025, driven by smart-home adoption, HVAC modernization, and rising demand for connected, energy-efficient climate control across residential and commercial buildings worldwide.

The market is projected to reach USD 18.21 Billion by 2034, growing at a CAGR of 15.05% during 2026-2034, supported by AI learning algorithms, Matter protocol standardization, and aggressive utility demand-response incentives.

Wireless technology leads with a 67.2% share in 2025, driven by Wi-Fi ubiquity, voice-assistant integration, and retrofit-friendly installation that eliminates the need for structured cabling in existing homes.

The commercial segment is the fastest-growing application category, expanding at an estimated CAGR of 16.8% through 2030, driven by office modernization, EU EPBD mandates, and hospitality chain energy-efficiency rollouts.

Asia Pacific dominates with a 41.6% share in 2025. China's HVAC modernization push, India's Smart Cities Mission, and Japan's heat-pump subsidy programs underpin its regional leadership position globally.

Key drivers include rising smart-home penetration, EU EPBD and ENERGY STAR energy mandates, utility demand-response rebates exceeding USD 1.2 Billion in 2024, voice-assistant adoption, and accelerating heat-pump electrification across developed markets.

Major players include Alphabet Inc, Resideo Technologies Inc., Ecobee, Emerson Electric Co., Schneider Electric, Carrier, Tado GmbH, and ADI Global among other regional specialists and HVAC-native OEMs.

Learning smart thermostats are the fastest-growing product tier, advancing at approximately 18.3% CAGR from 2025 to 2030, driven by on-device AI, personalized scheduling, and measurable household energy savings of 10-12% annually.

Key opportunities include AI-led energy optimization platforms, grid-interactive building software, India and Southeast Asia market expansion, heat-pump-optimized SKUs, and direct-to-consumer online channel development targeting Matter-native consumers.

The Matter 1.3 specification, released in May 2024, mandates cross-ecosystem compatibility, eliminating vendor lock-in and accelerating mainstream adoption. It is expected to structurally lift installed-base growth from 2026 onward across all major regions.

North American and European utilities disbursed over USD 1.2 Billion in thermostat rebates and demand-response incentives in 2024, effectively subsidizing consumer adoption and creating a structurally funded channel for OEMs to scale distribution.

Key challenges include high upfront cost versus basic thermostats, cybersecurity and data-privacy concerns, retrofit complexity around C-wire and multi-zone HVAC systems, and fragmented wireless protocols still consolidating around Matter interoperability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)