Sodium Ion Battery Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Sodium Ion Battery Market Size, Share, Trends & Forecast (2026-2034)

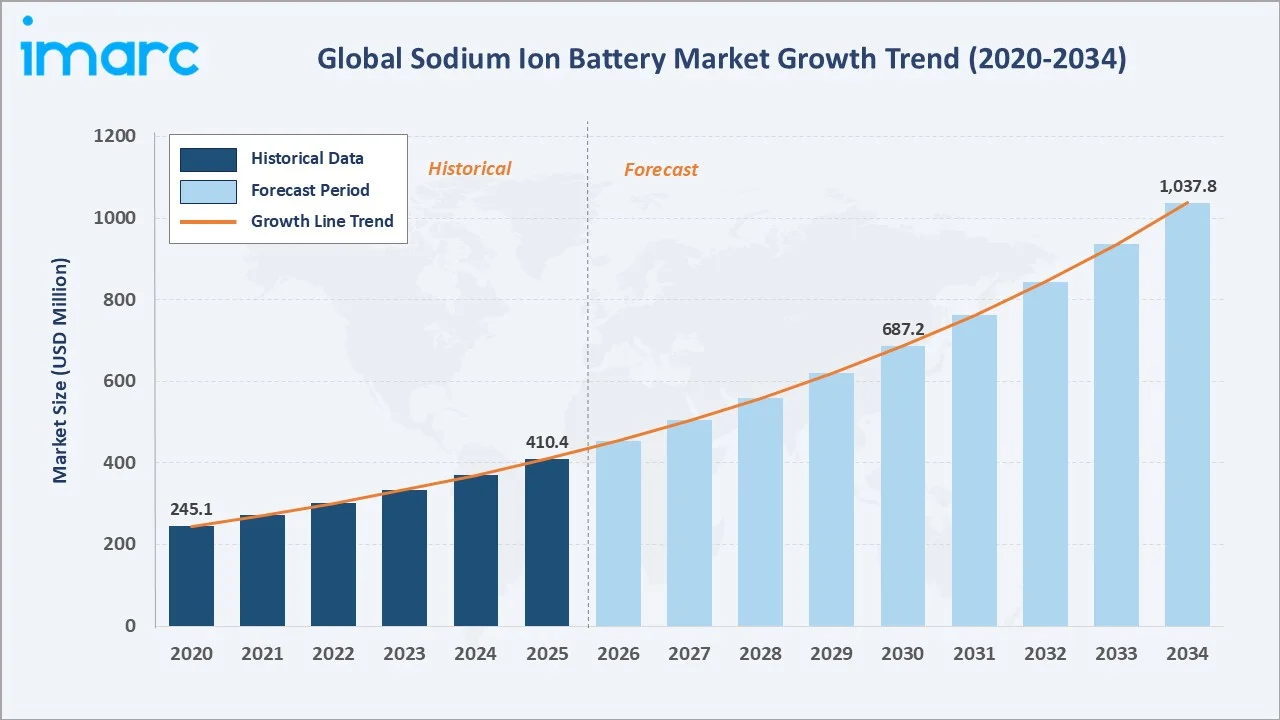

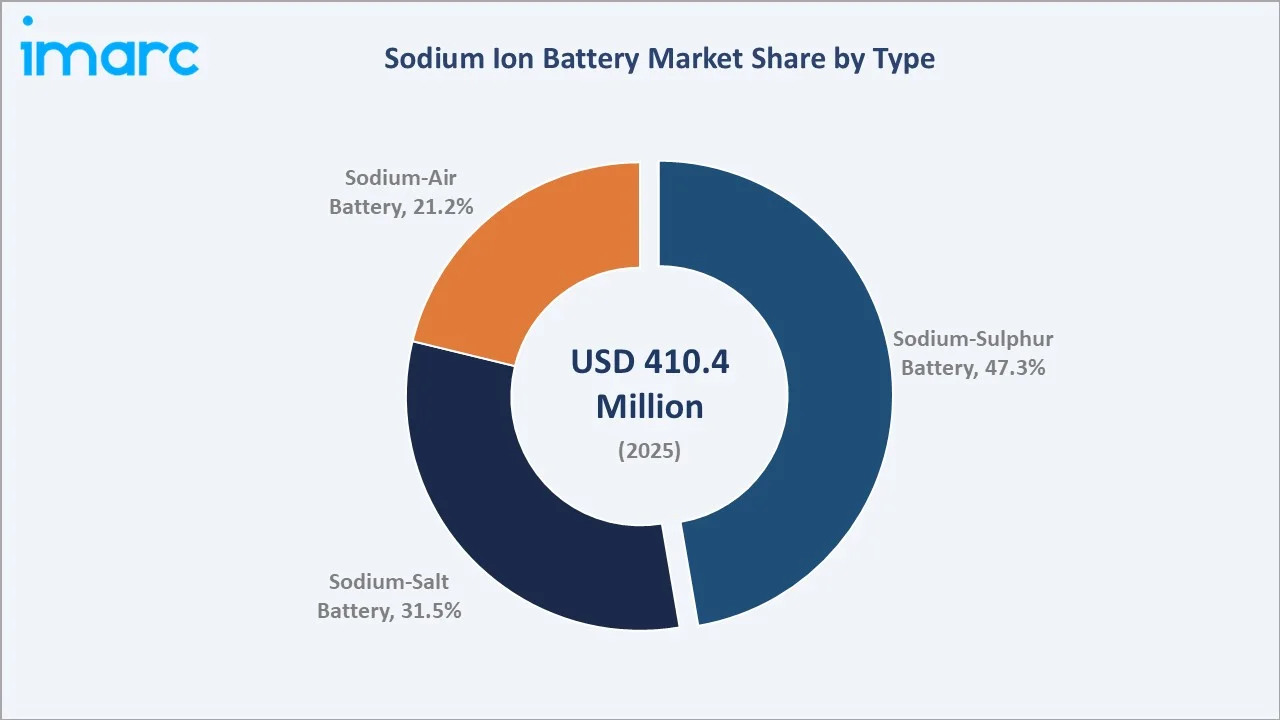

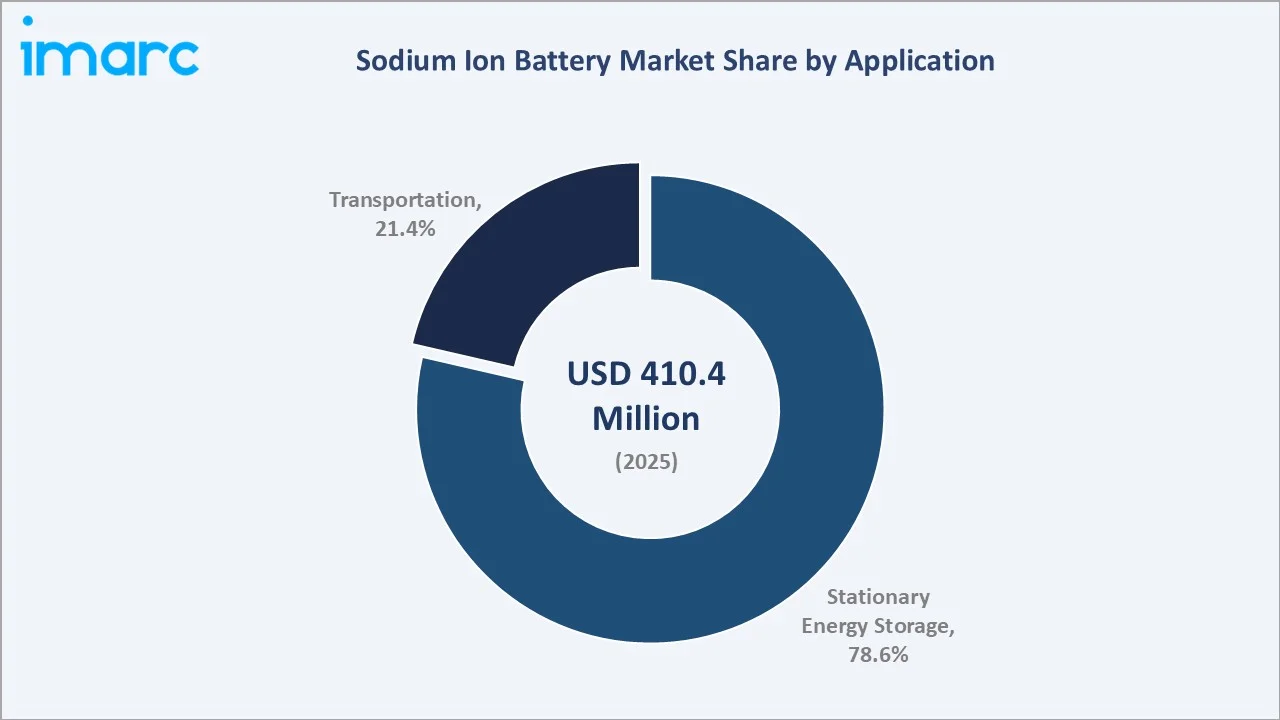

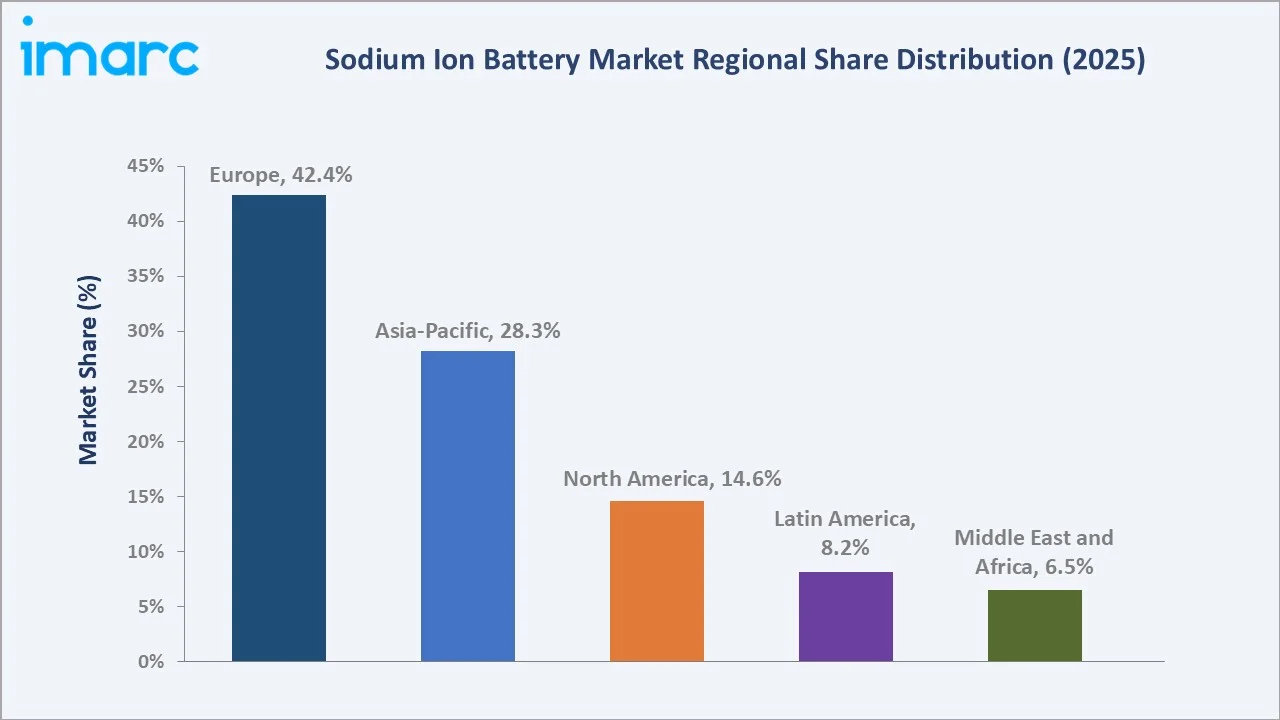

The global sodium ion battery market reached USD 410.4 Million in 2025 and is projected to reach USD 1,037.8 Million by 2034, growing at a CAGR of 10.86% during 2026-2034. Growing adoption in grid-scale energy storage, electric mobility, and renewable energy integration is further accelerating market expansion due to sodium’s abundant availability and improved safety profile. Sodium-ion batteries (SIBs) demonstrate up to 21.8% lower costs per km compared to nickel manganese cobalt (NMC) batteries, making them an economically attractive alternative for energy storage and electric mobility applications. Sodium-sulphur batteries dominate at 47.3%. Stationary energy storage leads at 78.6%. Europe commands 42.4% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 410.4 Million |

|

Forecast Market Size (2034) |

USD 1,037.8 Million |

|

CAGR (2026-2034) |

10.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Sodium-Sulphur Battery (47.3%, 2025) |

|

Dominant Application |

Stationary Energy Storage (78.6%, 2025) |

|

Leading Region |

Europe (42.4%, 2025) |

The market expanded from USD 245.1 Million in 2020 to USD 410.4 Million in 2025, anchored at USD 687.2 Million in 2030, and forecast to reach USD 1,037.8 Million by 2034. The 2020-2025 phase was dominated by commercial NaS grid storage deployments, while 2022-2025 saw the emergence of room-temperature sodium-ion battery technology as a commercially viable proposition, signaling mainstream industry and investor confidence in the sodium-ion battery technology.

To get more information on this market, Request Sample

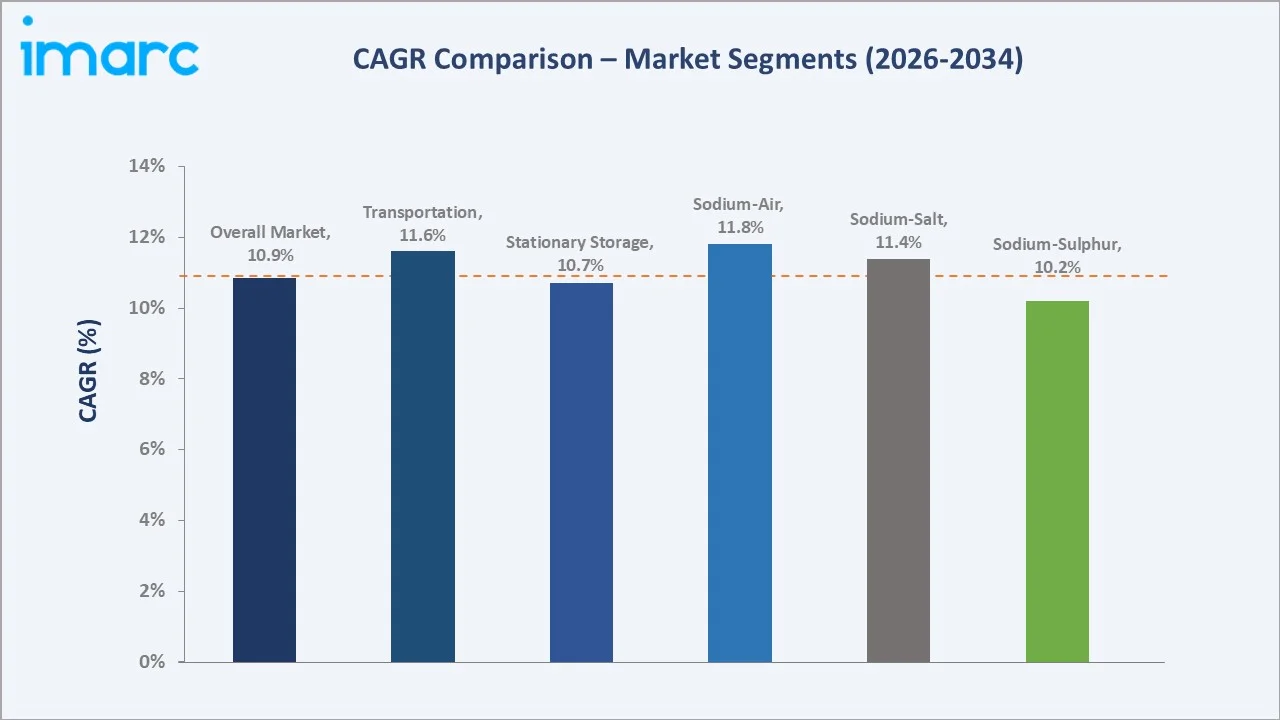

Sodium-air batteries grow fastest at ~11.8% CAGR, driven by significant R&D investment in rechargeable sodium-oxygen electrochemistry as a theoretical ultra-high energy density chemistry that could outcompete lithium-air as a long-duration storage technology. Transportation grows fastest among applications at ~11.6% CAGR as advanced SIB cell performance toward the 160-200 Wh/kg threshold, making room-temperature SIB viable for entry-level electric vehicles and electric two-wheelers.

Executive Summary

The global sodium ion battery market reached USD 410.4 Million in 2025, a figure that belies the technology's extraordinary long-term potential. Sodium-ion batteries are positioned as the electrochemical storage technology best aligned with the world's need for truly low-cost, geopolitically secure, sustainable grid storage for the energy transition. Sodium's abundance creates a theoretical battery input cost floor that no lithium chemistry can approach, and the room-temperature sodium-ion battery's operational safety, wide temperature operating range, and environmental compatibility position it as the 'green battery' for large-scale stationary storage. The market is projected to reach USD 1,037.8 Million by 2034 at 10.86% CAGR.

Sodium-sulphur (NaS) batteries at 47.3% dominate through high-capacity long-duration grid battery storage technology. Stationary energy storage at 78.6% dominates application because sodium's theoretical cost advantage is most commercially significant in large-format stationary applications where energy density (Wh/kg) is less critical than cost per kWh, cycle life, and service life, creating a natural application fit for grid storage, commercial backup, and microgrid energy management. Europe, at 42.4%, leads through its grid decarbonization policy framework.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Sodium-Sulphur (NaS) - 47.3% share (2025) |

|

Dominant Application |

Stationary Energy Storage - 78.6% market share (2025) |

|

Leading Region |

Europe - 42.4% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Sodium-sulphur at 47.3%: The sodium-sulphur segment dominates due to its high energy density, long cycle life, and strong suitability for large-scale grid energy storage applications. Its ability to operate efficiently in renewable energy integration and utility-scale power backup systems is further strengthening segment growth.

- Stationary energy storage at 78.6%: The stationary energy storage segment dominates due to the growing need for cost-effective and safe energy storage solutions for renewable energy integration and grid stabilization. Sodium-ion batteries are highly suitable for stationary applications because of their lower material costs, abundant raw material availability, and long operational lifespan.

- Europe at 42.4%: Europe dominates the market due to strong investments in renewable energy infrastructure, grid-scale energy storage projects, and sustainable battery manufacturing initiatives. Supportive government policies promoting energy transition and reducing dependence on critical raw materials such as lithium and cobalt are further accelerating regional market growth.

Sodium Ion Battery Market Overview

The global sodium ion battery market encompasses three distinct battery chemistries unified by their use of sodium ions (Na+) as the charge carrier: sodium-sulfur (NaS) high-temperature batteries for utility-scale grid storage; sodium-salt intermediate-temperature batteries for transportation and stationary; and room-temperature sodium-ion batteries that directly parallelize the lithium-ion battery architecture with sodium substitution. The market's common characteristic across all three types is sodium's elemental abundance. Sodium is the sixth most abundant element in Earth's crust, found in seawater, natural brines, and mineral deposits globally, at virtually zero resource scarcity risk versus lithium's concentrated deposits and geopolitically sensitive supply chains.

The ecosystem integrates sodium raw material suppliers, cathode material manufacturers, hard carbon anode suppliers, cell manufacturers, battery system integrators, utility and grid operators, and regulatory bodies. Macroeconomic factors include rising global investments in renewable energy infrastructure, increasing electrification across transportation and industrial sectors, and growing demand for affordable energy storage solutions.

Market Dynamics

To evaluate market opportunities, Request Sample

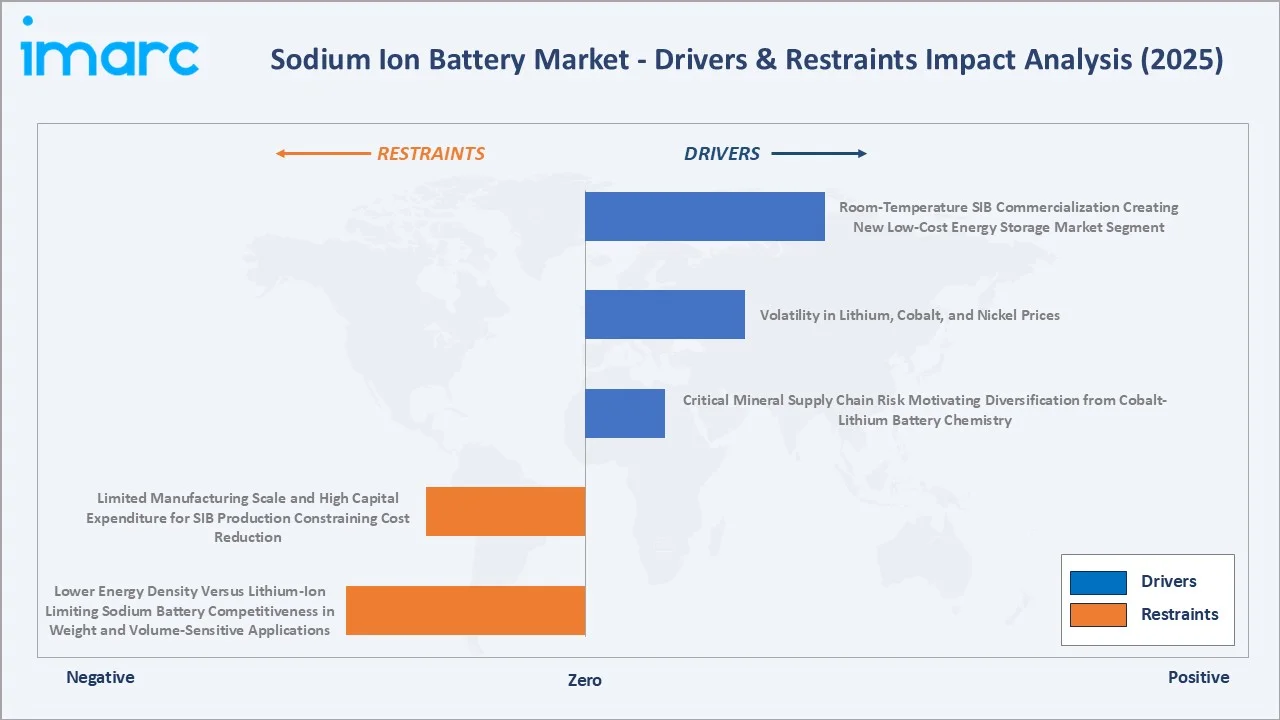

Market Drivers

- Critical Mineral Supply Chain Risk Motivating Diversification from Cobalt-Lithium Battery Chemistry: The strategic vulnerabilities of lithium-ion battery supply chains have motivated government energy security strategies to actively fund and support sodium-ion battery development as a domestic-resource-compatible alternative.

- Volatility in Lithium, Cobalt, and Nickel Prices: Volatility in lithium, cobalt, and nickel prices is encouraging battery manufacturers and end users to explore alternative chemistries with more stable and affordable raw material costs. Lithium carbonate prices in China surged by 78.3% within slightly more than a month, reaching their peak levels since the end of 2023. Sodium-ion batteries utilize abundantly available sodium resources, reducing dependence on expensive and supply-constrained critical minerals. This cost stability is improving the commercial attractiveness of sodium-ion technology for electric vehicles, grid-scale storage, and stationary energy storage applications. Additionally, manufacturers are increasingly investing in sodium-ion battery development to minimize supply chain risks and improve long-term profitability.

- Room-Temperature SIB Commercialization Creating New Low-Cost Energy Storage Market Segment: The commercialization of room-temperature sodium-ion batteries eliminates the need for complex thermal management systems. These batteries offer improved safety, lower operational costs, and easier scalability for stationary storage and entry-level electric mobility applications. Their affordability and compatibility with existing battery manufacturing infrastructure are encouraging wider adoption across residential, commercial, and utility-scale energy storage projects. Additionally, ongoing technological advancements are improving energy density and cycle performance, further strengthening market demand.

Market Restraints

- Lower Energy Density Versus Lithium-Ion Limiting Sodium Battery Competitiveness in Weight and Volume-Sensitive Applications: Sodium's larger ionic radius and heavier atomic mass inherently limit sodium battery energy density relative to lithium equivalents. Room-temperature SIB currently achieves 120-160 Wh/kg versus LFP at 150-180 Wh/kg and NMC at 200-250 Wh/kg. This energy density penalty is manageable in stationary applications and short-range urban EVs but eliminates SIB competitiveness for long-range premium EVs where battery pack weight directly impacts vehicle performance, handling, and range.

- Limited Manufacturing Scale and High Capital Expenditure for SIB Production Constraining Cost Reduction: Room-temperature SIB production scale remains orders of magnitude below lithium-ion manufacturing. The hard carbon anode supply chain creates a critical supply chain bottleneck that limits SIB manufacturing ramp-up speed.

Market Opportunities

- Second-Generation NaS Battery Technology at Reduced Operating Temperature Expanding Application Scope: Second-generation sodium-sulphur (NaS) battery technology operating at reduced temperatures improves safety, reducing energy consumption, and lowering maintenance requirements compared to conventional high-temperature NaS systems. These advancements are expanding the application scope of sodium-ion batteries across grid-scale storage, renewable energy integration, industrial backup power, and commercial energy management systems.

- Integration with Renewable Energy Projects Creating Co-Located SIB and NaS Procurement Opportunities: Large-scale renewable energy projects increasingly require co-located battery storage for grid compliance, merchant revenue optimization, and capacity payment qualification, creating battery storage procurement alongside renewable energy equipment procurement from single contractors. Sodium battery technologies that can demonstrate competitive cost and grid compliance certification for co-located storage alongside solar and wind PV inverters position for procurement in the global pipeline of 50+ GW of solar-plus-storage and wind-plus-storage projects.

Market Challenges

- Room-Temperature SIB Manufacturing Readiness and Quality Consistency at Commercial Scale: The transition from laboratory and pilot production of room-temperature SIB cells to reliable commercial manufacturing at GWh scale requires solving manufacturing process challenges that lithium-ion manufacturers spent 20+ years optimizing.

- Competition from Rapidly Improving LFP Battery Economics Pressuring SIB Cost Advantage Timeline: The sodium-ion battery's primary commercial value proposition is facing a narrowing window as LFP (lithium iron phosphate) battery prices have fallen and are projected to fall further.

Emerging Market Trends

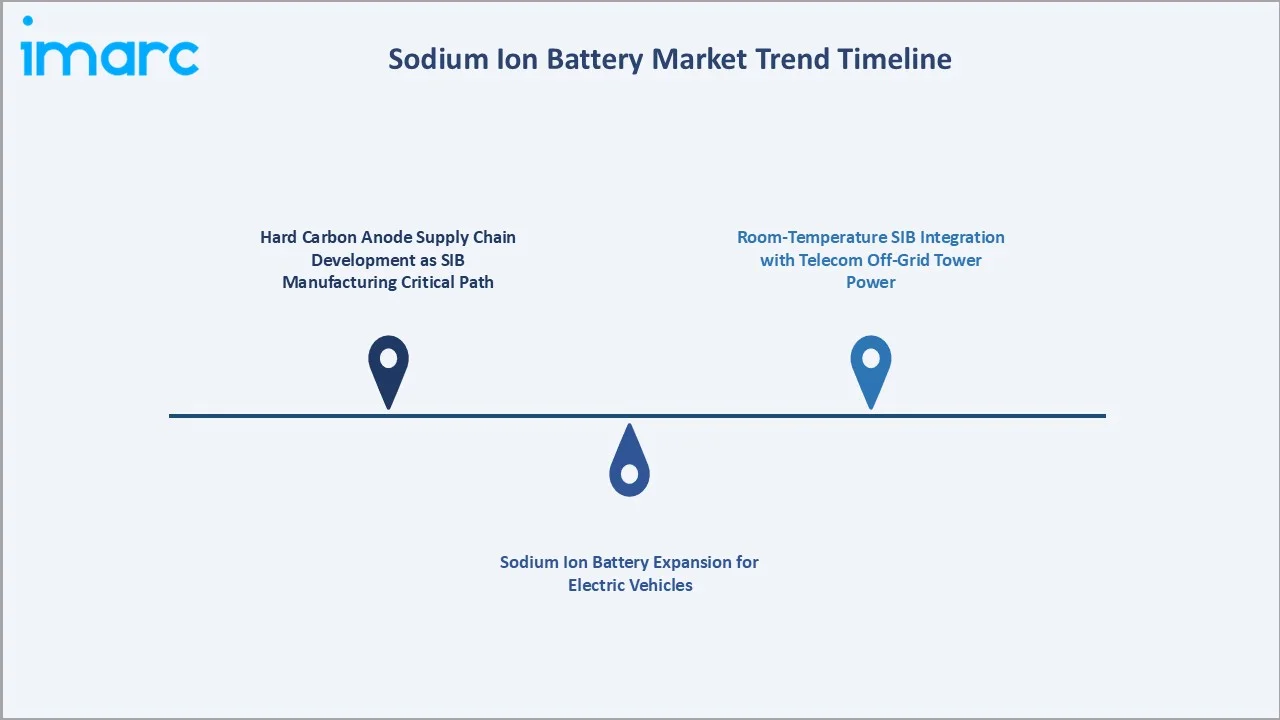

1. Hard Carbon Anode Supply Chain Development as SIB Manufacturing Critical Path

The development of hard carbon anode supply chains is emerging as manufacturers focus on securing stable and scalable raw material availability for commercial production. Companies are increasingly investing in biomass-derived and synthetic hard carbon materials to improve battery performance, energy density, and charging efficiency. This trend is also encouraging localization of battery material supply chains to reduce dependence on imported graphite and strengthen production resilience. As sodium-ion battery commercialization accelerates, demand for high-quality hard carbon anodes is expected to grow significantly.

2. Sodium Ion Battery Expansion for Electric Vehicles

The expansion of sodium-ion batteries for electric vehicles is emerging due to their lower material costs, improved thermal stability, and reduced dependence on critical minerals such as lithium and cobalt. Automakers are increasingly exploring sodium-ion technology for entry-level electric vehicles, two-wheelers, and commercial fleets where affordability is a key purchasing factor. In February 2026, CHANGAN Automobile collaborated with CATL to introduce the world’s first mass-produced passenger vehicle powered by sodium-ion batteries during the “CHANGAN SDA Intelligence Milestone Release & Sodium-Ion Battery Global Strategy Launch” event.

3. Room-Temperature SIB Integration with Telecom Off-Grid Tower Power

The integration of room-temperature sodium-ion batteries with telecom off-grid tower power systems is emerging due to the growing need for reliable, low-cost, and thermally stable energy storage solutions in remote areas. Sodium-ion batteries offer improved safety and better performance under varying environmental conditions, making them suitable for telecom infrastructure with limited maintenance access. Their lower dependence on critical raw materials also helps telecom operators reduce energy storage costs and supply chain risks. The increasing expansion of rural connectivity and telecom networks is further supporting adoption in off-grid applications.

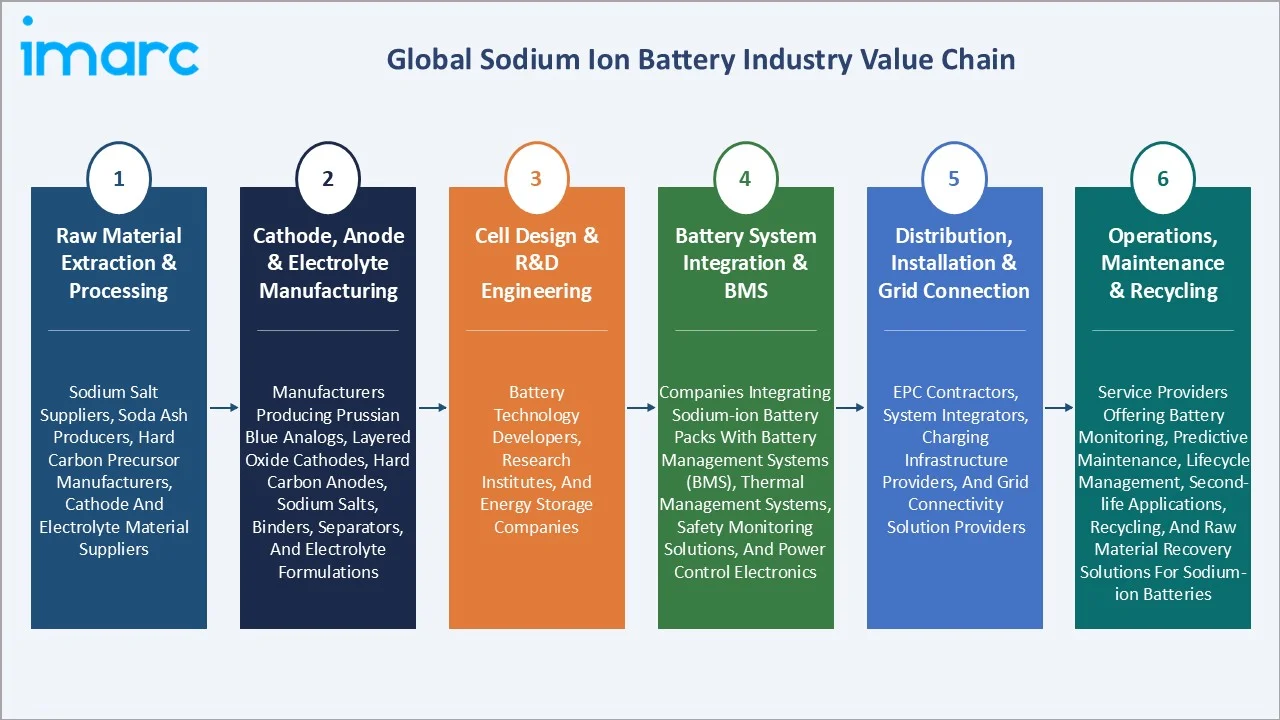

Industry Value Chain Analysis

The sodium ion battery value chain integrates sodium source and cathode material synthesis, cell design and R&D engineering, cell and module manufacturing and testing, battery system integration and BMS, project deployment and grid connection, and operations, maintenance, data analytics, and recycling. Value is primarily created in cathode and anode material synthesis, cell manufacturing, and system integration.

|

Stage |

Key Participants |

|

Raw Material Extraction & Processing |

Sodium salt suppliers, soda ash producers, hard carbon precursor manufacturers, cathode and electrolyte material suppliers. |

|

Cathode, Anode & Electrolyte Material Manufacturing |

Manufacturers producing Prussian blue analogs, layered oxide cathodes, hard carbon anodes, sodium salts, binders, separators, and electrolyte formulations. |

|

Cell Design & R&D Engineering |

Battery technology developers, research institutes, and energy storage companies |

|

Battery System Integration & BMS |

Companies integrating sodium-ion battery packs with battery management systems (BMS), thermal management systems, safety monitoring solutions, and power control electronics. |

|

Distribution, Installation & Grid Connection |

EPC contractors, system integrators, charging infrastructure providers, and grid connectivity solution providers. |

|

Operations, Maintenance & Recycling |

Service providers offering battery monitoring, predictive maintenance, lifecycle management, second-life applications, recycling, and raw material recovery solutions for sodium-ion batteries |

Room-temperature SIB recycling will develop commercial value from hard carbon anode recovery, PBA cathode material recovery, and cathode recovery. The battery regulation's end-of-life collection and recycling requirements apply to SIB as to all battery chemistries, creating both compliance obligations and commercial recycling business development opportunities from growing SIB installed base.

Technology Landscape in the Sodium Ion Battery Industry

Sodium-Sulfur (NaS) High-Temperature Battery Technology

Sodium-sulfur (NaS) high-temperature battery technology has the ability to deliver high energy density, long-duration storage, and stable performance for grid-scale applications. The technology is widely adopted in renewable energy integration, peak load management, and utility-scale backup systems due to its long operational life and high discharge efficiency. Continuous advancements focused on reducing operating temperatures, improving thermal insulation, and enhancing safety systems are further expanding its commercial viability. These innovations are encouraging broader deployment of NaS batteries across industrial and large-scale energy storage applications.

Room-Temperature Sodium-Ion Battery Cathode Technologies

Room-temperature sodium-ion battery cathode technologies are improving battery safety, operational stability, and manufacturing flexibility. In April 2026, SEVB introduced the “Xin Na Qing” sodium-ion battery full-scenario solution targeting both electric vehicle power systems and grid energy storage applications, alongside its AI-plus-battery strategy. The company also unveiled a 388Ah large-capacity sodium-ion battery cell for energy storage applications, offering more than 20,000 charge cycles with 70% capacity retention, over 85% low-temperature discharge retention at -40°C, and energy efficiency at room temperature that is 7% higher than LFP batteries. These innovations are accelerating the commercialization of sodium-ion batteries for electric vehicles, stationary energy storage, and telecom backup systems.

Hard Carbon Anode Optimization

Hard carbon anode optimization improves energy density, charging efficiency, and cycle stability of sodium-ion cells. Manufacturers are increasingly developing biomass-derived and engineered hard carbon materials to enhance sodium-ion storage capacity and reduce irreversible capacity loss during charging cycles. These advancements are enabling better low-temperature performance and longer battery lifespan, making sodium-ion batteries more competitive for electric vehicles and stationary energy storage applications. Ongoing research is also supporting scalable and cost-effective commercial production of advanced hard carbon anodes.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Sodium-Sulphur Battery |

47.3% |

2025 |

|

Application |

Stationary Energy Storage |

78.6% |

2025 |

|

Region |

Europe |

42.4% |

2025 |

By Type

Sodium-sulphur (NaS) leads at 47.3% market share (2025). The segment dominates due to its high energy density, long cycle life, and strong efficiency in large-scale stationary energy storage applications. NaS batteries are widely used for renewable energy integration, grid stabilization, and peak load management because they can deliver reliable long-duration power storage at a utility scale.

To access detailed market analysis, Request Sample

Sodium-salt batteries at 31.5% serve transportation and stationary applications. Sodium-air at 21.2% primarily represents research funding flows rather than commercial product revenue.

By Application

Stationary energy storage leads at 78.6% market share (2025). This category encompasses utility-scale grid storage, commercial and industrial backup power, and off-grid rural electrification storage. The application category benefits from the fastest-growing global energy storage procurement as renewable energy integration drives battery storage demand at the utility scale globally.

Transportation at 21.4% represents EV pilot programs, electric bus deployments, and early-stage SIB two-wheeler and three-wheeler vehicle programs. Transportation grows fastest at ~11.6% CAGR.

Regional Market Insights

Europe's 42.4% market leadership reflects the unique combination of European utility partnerships generating current commercial revenue, EU battery policy creating structural procurement advantage for non-lithium-cobalt chemistries, and Europe's exceptionally dense concentration of SIB R&D and startup activity relative to market size.

Asia-Pacific at 28.3% is the SIB innovation leader, with China's positioning the most advanced room-temperature SIB commercial production, and Japan's maintaining NaS manufacturing supremacy. North America, at 14.6%, is developing its SIB ecosystem through DOE funding, US national laboratory research leadership, and domestic manufacturing investment. Latin America, at 8.2%, and the Middle East and Africa, at 6.5%, represent developing markets where NaS grid stability installations and emerging SIB interest from energy access and decarbonization programs create growing demand.

|

Region |

Share (2025) |

Key Sodium Ion Battery Market Drivers & Characteristics |

|

Europe |

42.4% |

Driven by strong renewable energy deployment, grid-scale energy storage investments, and government initiatives supporting sustainable battery technologies and localized supply chains. |

|

Asia-Pacific |

28.3% |

Supported by rapid battery manufacturing expansion, strong research activities, and growing adoption of low-cost energy storage and electric mobility solutions. |

|

North America |

14.6% |

Characterized by increasing investments in next-generation battery startups, grid modernization projects, and a rising focus on reducing dependence on critical battery minerals. |

|

Latin America |

8.2% |

Gradually expanding due to rising renewable energy integration, increasing demand for affordable stationary energy storage, and improving rural electrification infrastructure. |

|

Middle East and Africa |

6.5% |

Witnessing growth from expanding renewable energy projects, off-grid power applications, and increasing demand for cost-effective energy storage solutions in remote locations. |

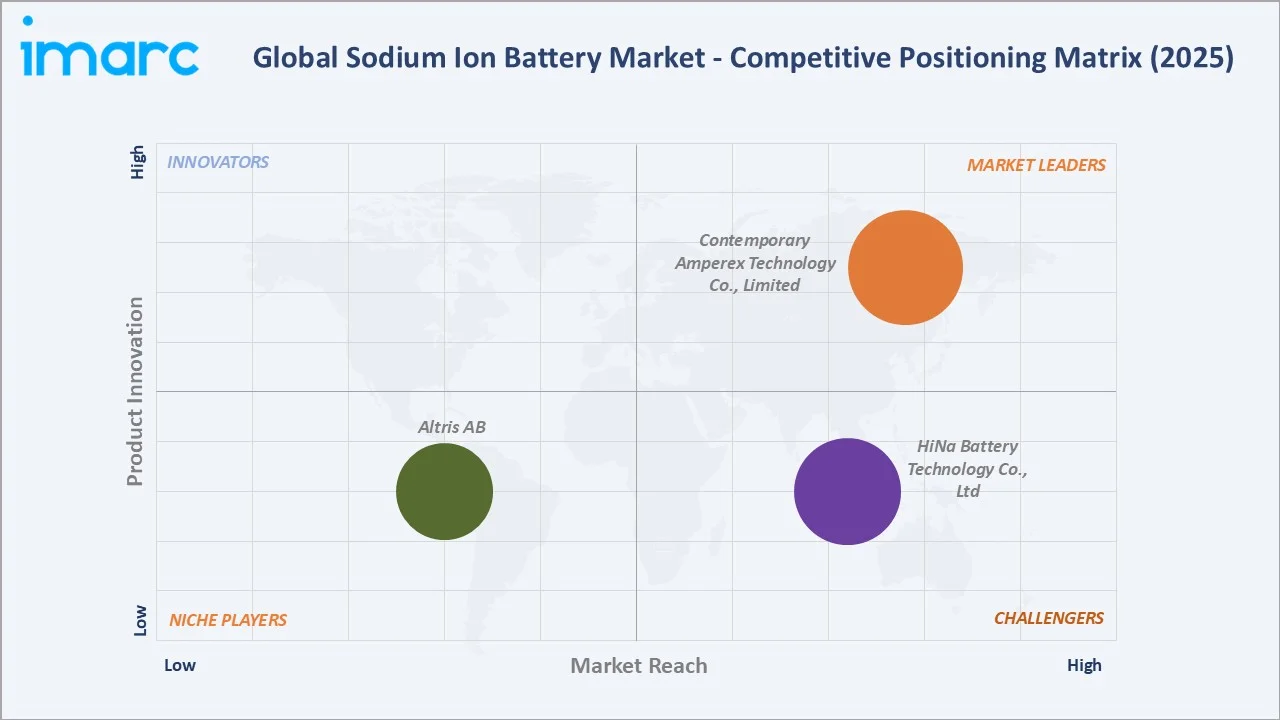

Competitive Landscape

The global sodium ion battery competitive landscape is divided between the established NaS market and the emerging room-temperature SIB market. The room-temperature SIB market is much more competitive, with parallel development across multiple chemistries and multiple geographies that creates competitive intensity despite the market's small current scale.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Contemporary Amperex Technology Co., Limited |

Naxtra sodium-ion battery |

Market Leader |

Naxtra is among the world's prominent mass-producible sodium-ion battery, which breaks resource constraints and strengthens the foundation of the new energy industry. |

|

HiNa Battery Technology Co., Ltd |

NaCP08/80/138, NaCR26650, NaCR32138 Na-ion batteries |

Strong Challenger |

HiNa Battery Technology Co., Ltd is a new high-tech enterprise, focusing on the R&D and manufacturing of the new generation Na-ion batteries. |

|

Altris AB |

Prussian White sodium ion batteries |

Niche Player |

Altris focuses on advancing energy independence and sustainability through the development and commercialization of affordable Prussian White sodium-ion battery technology. |

The competitive landscape's most significant development is CATL's SIB market entry, the world's largest battery manufacturer's commitment to SIB production provides the commercial credibility, manufacturing scale pathway, and supply chain development that accelerates the entire room-temperature SIB market's development timeline.

Key Company Profiles

Contemporary Amperex Technology Co., Limited

CATL is a global leader in zero-carbon new energy technology, committed to providing first-class solutions and services for global new energy applications. Naxtra, a world's prominent mass-producible sodium-ion battery, breaks resource constraints and strengthens the foundation of the new energy industry.

- Key Products: Naxtra sodium-ion battery.

- Recent Developments: In February 2026, CHANGAN Automobile, in collaboration with CATL, revealed the world’s first mass-produced passenger vehicle powered by sodium-ion batteries during the “CHANGAN SDA Intelligence Milestone Release & Sodium-Ion Battery Global Strategy Launch” event.

- Strategic Focus: Focused on accelerating mass commercialization of sodium-ion batteries for electric vehicles and energy storage applications through advanced battery innovation, large-scale manufacturing, and diversified battery platform development.

HiNa Battery Technology Co., Ltd

HiNa Battery Technology Co., Ltd is located in Zhongguancun, Liyang, Jiangsu Province. It is a new high-tech enterprise, focusing on the R&D and manufacture of the new generation Na-ion batteries.

- Key Products: NaCP08/80/138, NaCR26650, NaCR32138 Na-ion batteries.

- Recent Developments: In October 2025, HiNa Battery Technology Co., Ltd. organized a mass-production launch event under the theme “Evolution & Leap: From the Product Era to the Commercial Era,” marking the transition of sodium-ion batteries into large-scale commercial deployment. The company announced plans to supply high-performance and cost-efficient sodium-ion battery products to support the growth of the global new energy sector.

- Strategic Focus: Focusing on scaling mass production of sodium-ion battery technologies while strengthening partnerships across electric vehicle and grid energy storage ecosystems.

Market Concentration Analysis

The global sodium ion battery market exhibits extreme concentration in the NaS segment and emerging fragmentation in the room-temperature SIB segment, and others are developing parallel commercial offerings. The market's total USD 410.4 Million scale (2025) is too small to support the number of SIB developers currently active, and industry consolidation is expected from 2027-2030 as commercial production scale separates viable manufacturers from undercapitalized technology developers. The NaS segment's extreme concentration is structurally durable, creating an impenetrable manufacturing moat that no competitor has breached despite the technology's high commercial value.

Investment & Growth Opportunities

Highest Growth Segments

Sodium-air battery R&D investment (~11.8% CAGR from R&D funding), transportation SIB applications (~11.6% CAGR), sodium-salt ZEBRA batteries in electric bus applications (~11.4% CAGR), room-temperature SIB for grid storage (~10.5% CAGR), and European SIB manufacturing ecosystem development (~12-15% CAGR from EU policy tailwinds) represent the market's highest-growth investment vectors through 2034.

Emerging Investment Opportunities

The off-grid telecom SIB replacement market in Sub-Saharan Africa and South Asia represents an emerging commercial opportunity where room-temperature SIB's temperature tolerance, potential low cost, and improved cycle life versus lead acid create compelling replacement economics for diesel and lead acid-powered telecom towers.

Investment Themes

- Room-temperature SIB GWh manufacturing scale-up investment for grid storage market development: CATL and HiNa's SIB production scale-up growth requires high cumulative capital investment, creating equipment supply, materials supply, and system integration opportunities across the SIB manufacturing supply chain.

- Second-generation NaS technology investment for intermediate-temperature operation, enabling new applications: Development capital for NaS battery operation at 150-200 degrees Celsius would open industrial, commercial, and transportation applications currently unsuitable for high-temperature NaS.

Future Market Outlook (2026-2034)

The global sodium ion battery market is projected to grow from USD 410.4 Million in 2025 to USD 1,037.8 Million by 2034, delivering a 10.86% CAGR over the forecast period. The market's anchor value of USD 687.2 Million in 2030 represents a sodium battery industry at a pivotal commercialization inflection point. The market's USD 687.2 Million 2030 value, while modest in absolute terms, represents the foundation of a technology that could reach USD 50-100 Billion annual market value by 2040-2045 if room-temperature SIB achieves its theoretical cost targets and displaces lithium in large-format stationary applications globally.

Three structural forces sustain the sodium battery market growth through 2034 with high confidence. First, the fundamental sodium abundance advantage creates a permanent theoretical cost floor below lithium that motivates manufacturing investment when scale is achieved; no amount of lithium mining expansion can eliminate sodium's inherent cost advantage at identical production scale. Second, battery regulation and critical mineral supply chain policy create structural regulatory preferences for sodium batteries that grow in commercial weight with each tightening of sustainability requirements. Third, the global energy transition's need for truly affordable, long-duration grid storage creates a structural application fit for NaS batteries that no lithium chemistry matches at equivalent cost for the long-duration class.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including Head of NAS Battery Business; Product Directors; Chief Technology Officers; grid storage procurement managers; battery materials research directors; venture capital partners; and regulatory specialists.

Secondary Research

Secondary research encompassed IEA World Energy Outlook 2025 critical mineral and battery storage data; Company Annual Reports; Battery Regulation requirements; European Battery Alliance (EBA) Strategic Research and Innovation Agenda 2023; US Vehicle Technologies Office Annual Report 2025; Academic publications in Journal of Power Sources, Nature Energy, ACS Energy Letters on SIB materials research (2020-2025 period); standard technical committee documents for electrochemical energy storage. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up battery type and application models calibrated against annual shipment data, SIB production disclosures, government R&D funding flows, and venture capital investment in sodium battery companies. Key forecast inputs include SIB production ramp timeline, manufacturing schedule, grid storage tender volumes, hard carbon supply chain scale-up trajectory, and SIB cost reduction learning curve rate.

Sodium Ion Battery Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Sodium-Sulphur Battery, Sodium-Salt Battery, Sodium-Air Battery |

| Applications Covered | Stationary Energy Storage, Transportation |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Contemporary Amperex Technology Co., Limited, HiNa Battery Technology Co., Ltd, Altris AB, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the sodium ion battery market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global sodium ion battery market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the sodium ion battery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Sodium Ion Battery Market Report

The global sodium ion battery market reached USD 410.4 Million in 2025, primarily driven by NaS (sodium-sulfur) commercial grid storage deployments, room-temperature SIB commercialization by CATL and HiNa Battery Technology, grid decarbonization procurement, and growing R&D investment in sodium-air battery technology from government and corporate research programs.

The market grows at 10.86% CAGR during 2026-2034, reaching USD 1,037.8 Million by 2034, among the highest CAGRs of any battery technology market. Growth is driven by CATL's SIB EV commercial deployment, grid storage procurement favoring non-lithium-cobalt chemistries, and the global energy transition's demand for long-duration, affordable grid storage.

Sodium-sulphur (NaS) leads at 47.3% through proven utility-scale grid storage.

Stationary energy storage leads at 78.6% through NaS and SIB grid storage deployments, commercial backup power, and microgrid storage, where sodium's cost-per-kWh advantage and service life superiority are most commercially relevant.

Europe leads at 42.4% through European utility NaS partnerships, the EU Green Deal and Battery Regulation, creating structural procurement advantages for non-lithium-cobalt chemistries, and Europe's dense SIB startup ecosystem.

Leading companies include Contemporary Amperex Technology Co., Limited, HiNa Battery Technology Co., Ltd, and Altris AB, among others.

The market is projected to reach approximately USD 687.2 Million by 2030, with CATL achieving SIB production and EV deployment scale, EU grid storage tenders creating structural SIB procurement, and hard carbon supply chain scaling to enable room-temperature SIB manufacturing ramp at multiple manufacturers simultaneously.

Three primary technical challenges constrain room-temperature SIB commercialization: hard carbon anode performance and supply chain; cathode material energy density improvement; and manufacturing quality consistency.

Three priority opportunities: CATL and HiNa SIB manufacturing supply chain; European SIB manufacturing ecosystem investment for EU Battery Regulation compliance positioning; and supply chain development for the Indian market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)