South Africa Fantasy Sports Market Size, Share, Trends and Forecast by Sports Type, Platform, Demographics, and Region, 2026-2034

South Africa Fantasy Sports Market Size, Share, Trends & Forecast (2026-2034)

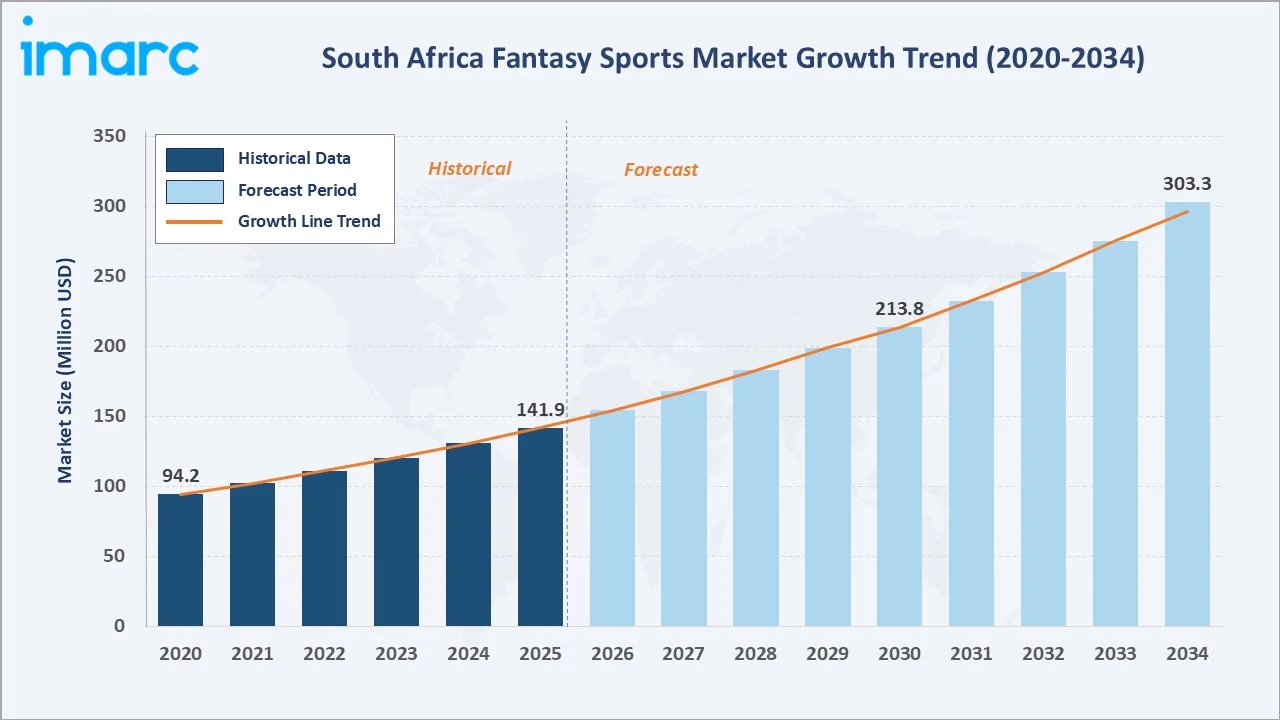

The South Africa fantasy sports market reached USD 141.9 Million in 2025 and is projected to reach USD 303.3 Million by 2034, growing at a CAGR of 8.54% during 2026-2034. Rising smartphone and mobile internet penetration, deepening football and cricket fan engagement culture, and the growing appeal of social gaming and real-money contest formats are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 141.9 Million |

|

Forecast Market Size (2034) |

USD 303.3 Million |

|

CAGR (2026-2034) |

8.54% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

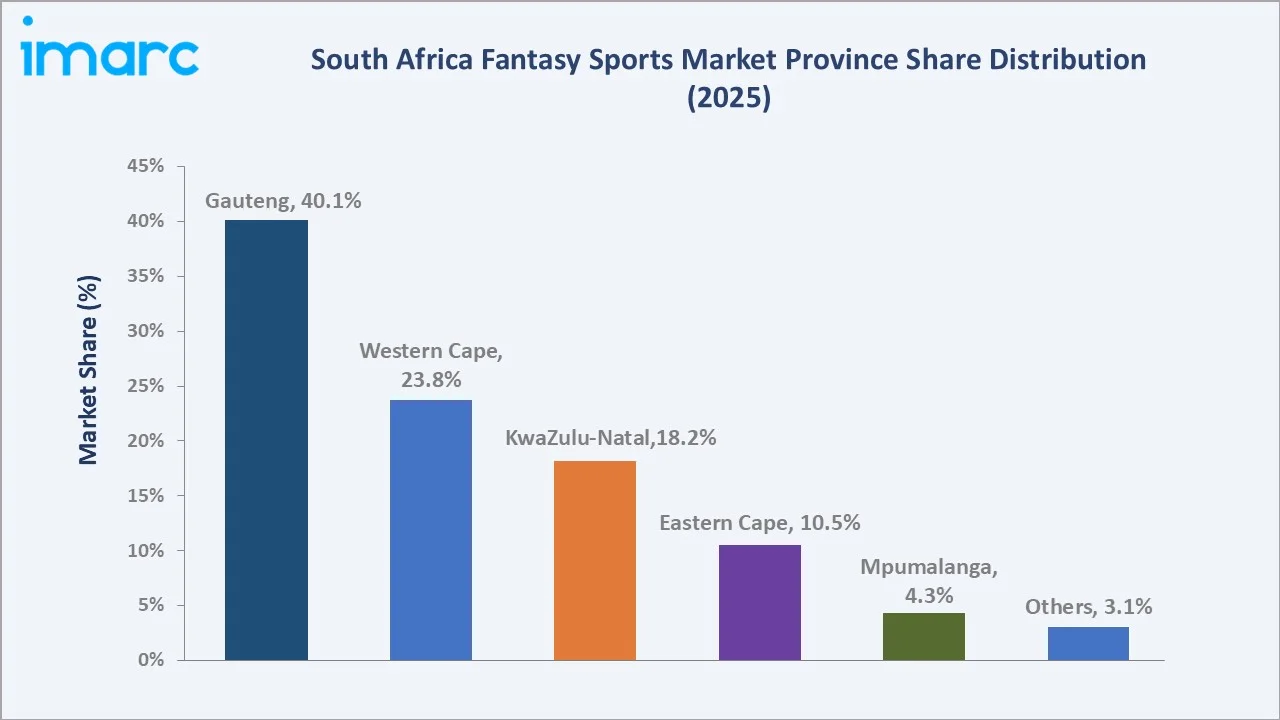

Gauteng leads regionally with a 40.1% market share in 2025, anchored by Johannesburg and Pretoria’s status as South Africa’s most densely populated and digitally connected urban centers, hosting the country’s highest smartphone penetration and digital payment adoption rates. Football commands the largest sports-type share at 46.8%, reflecting South Africa’s position as the continent’s most football-passionate market, supported by Premier Soccer League (PSL) fan engagement and the broader continental and global football following across South African sports culture.

To get more information on this market, Request Sample

South Africa’s fantasy sports market is underpinned by three structural forces: the country’s rapidly expanding smartphone and mobile internet user base that is bringing fantasy sports platforms within reach of a growing digital consumer population, deep-rooted football and cricket fan culture that creates natural engagement hooks for fantasy contest participation, and the broader social gaming trend that is normalizing skill-based real-money contests as a mainstream entertainment category among South Africa’s sports-following youth and working-age population.

Executive Summary

The South Africa fantasy sports market is experiencing robust expansion, driven by the convergence of rapid mobile internet adoption, deepening sports fan engagement culture, and the maturation of digital payment infrastructure that enables seamless real-money contest participation. The market was valued at USD 141.9 Million in 2025 and is forecast to reach USD 303.3 Million by 2034, growing at a CAGR of 8.54%.

Football dominates the sports-type segment with a 46.8% share in 2025, reflecting South Africa’s status as the continent’s most football-obsessed market, with fan engagement spanning the domestic Premier Soccer League (PSL), continental competitions, and major European leagues that South African audiences follow closely. Cricket at 21.7% benefits from South Africa’s strong cricketing heritage and the growing popularity of T20 league formats including the SA20, while basketball, hockey, and baseball collectively represent emerging fantasy sports categories with smaller but growing participation bases.

Mobile application is the dominant platform at 64.3%, reflecting South Africa’s mobile-first internet usage patterns where smartphone penetration significantly exceeds traditional desktop and laptop computer ownership across the broader population. Website-based platforms at 35.7% continue to serve a meaningful user base, particularly among desktop-first users and those accessing fantasy sports platforms through web browsers on shared or family devices.

Key Market Insights

|

Insight |

Data |

|

Largest Sports Type |

Football – 46.8% share (2025) |

|

Fastest Growing Sports Type |

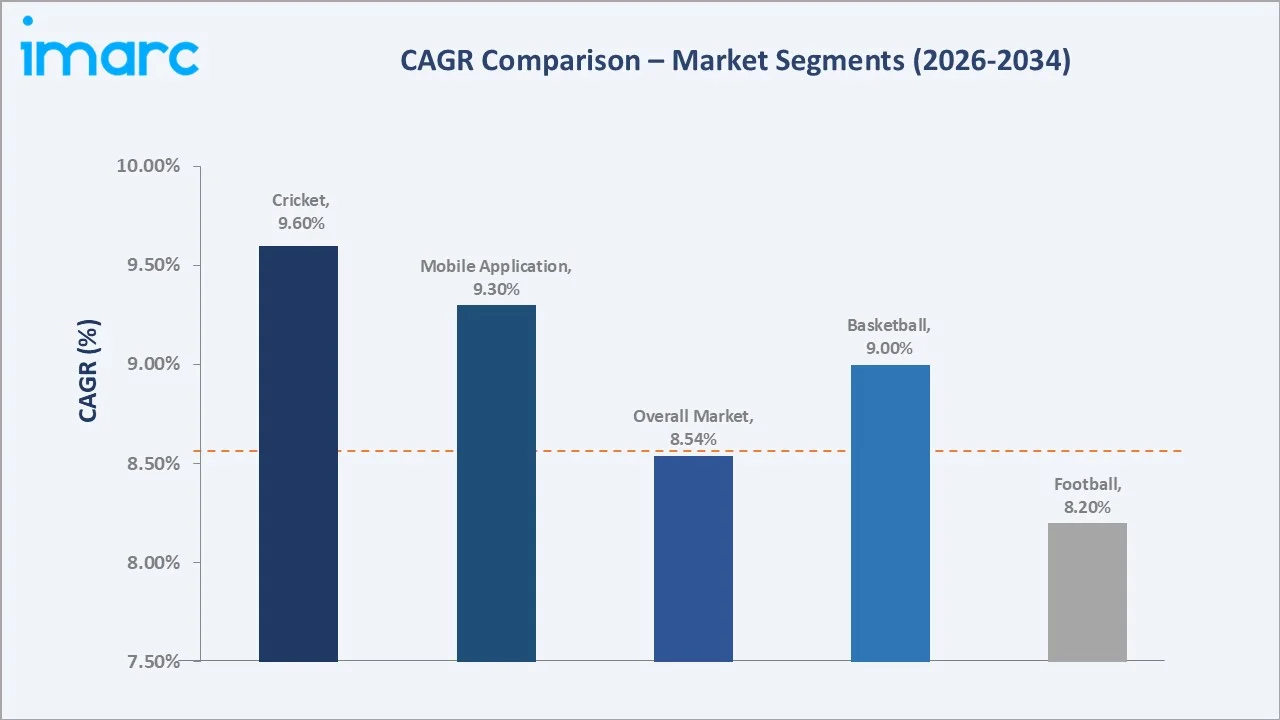

Cricket – ~9.6% CAGR (2026-2034) |

|

Largest Platform |

Mobile Application – 64.3% share (2025) |

|

Fastest Growing Platform |

Mobile Application – ~9.3% CAGR (2026-2034) |

|

Leading Province |

Gauteng – 40.1% share (2025) |

|

Top Companies |

Scout Gaming Group, Super Group (SGHC) Limited, MultiChoice Group |

Key Analytical Observations Supporting The Above Data:

- Football accounts for 46.8% of South Africa’s fantasy sports market in 2025, reflecting the sport’s unmatched cultural penetration across the country. South African fans engage not only with the domestic Premier Soccer League (PSL) but also extensively follow European leagues including the English Premier League, creating year-round football fantasy participation opportunities.

- Cricket at 21.7% share (2025) is expected to be the fastest-growing sports-type segment at approximately 9.6% CAGR, propelled by South Africa’s deep cricketing heritage and the rising popularity of fast-paced T20 league formats including the domestic SA20 league launched in 2023.

- Mobile application at 64.3% share (2025) reflects South Africa’s mobile-first digital consumption patterns, where smartphone penetration has significantly outpaced fixed broadband and desktop computer adoption, particularly among younger and lower-income demographics who represent core fantasy sports participants.

- Gauteng’s 40.1% share (2025) regional dominance reflects Johannesburg and Pretoria’s status as South Africa’s most urbanized and digitally connected metropolitan centers, combining the country’s highest population density, strongest smartphone and mobile data infrastructure, and greatest concentration of disposable income available for discretionary entertainment and gaming spending.

South Africa Fantasy Sports Market Overview

Fantasy sports platforms enable participants to assemble virtual teams of real-world athletes and earn points based on those athletes’ actual statistical performance in live matches, with contests ranging from free-to-play engagement formats to real-money skill-based competitions offering cash prizes. South Africa’s fantasy sports market spans football, cricket, basketball, hockey, baseball, and other sports categories, delivered through both native mobile applications and browser-based website platforms that serve the country’s growing base of digitally engaged sports fans.

South Africa’s fantasy sports market operates within a regulatory environment where skill-based fantasy sports contests are generally distinguished from traditional gambling, though the precise regulatory classification continues to evolve across South Africa’s provincial gambling authorities. The market’s growth is closely tied to the broader expansion of South Africa’s digital economy, including rising smartphone affordability, expanding 4G and 5G mobile network coverage, and the proliferation of digital payment methods that have collectively lowered the barriers to fantasy sports platform adoption across an increasingly broad consumer base.

Market Dynamics

To evaluate market opportunities, Request Sample

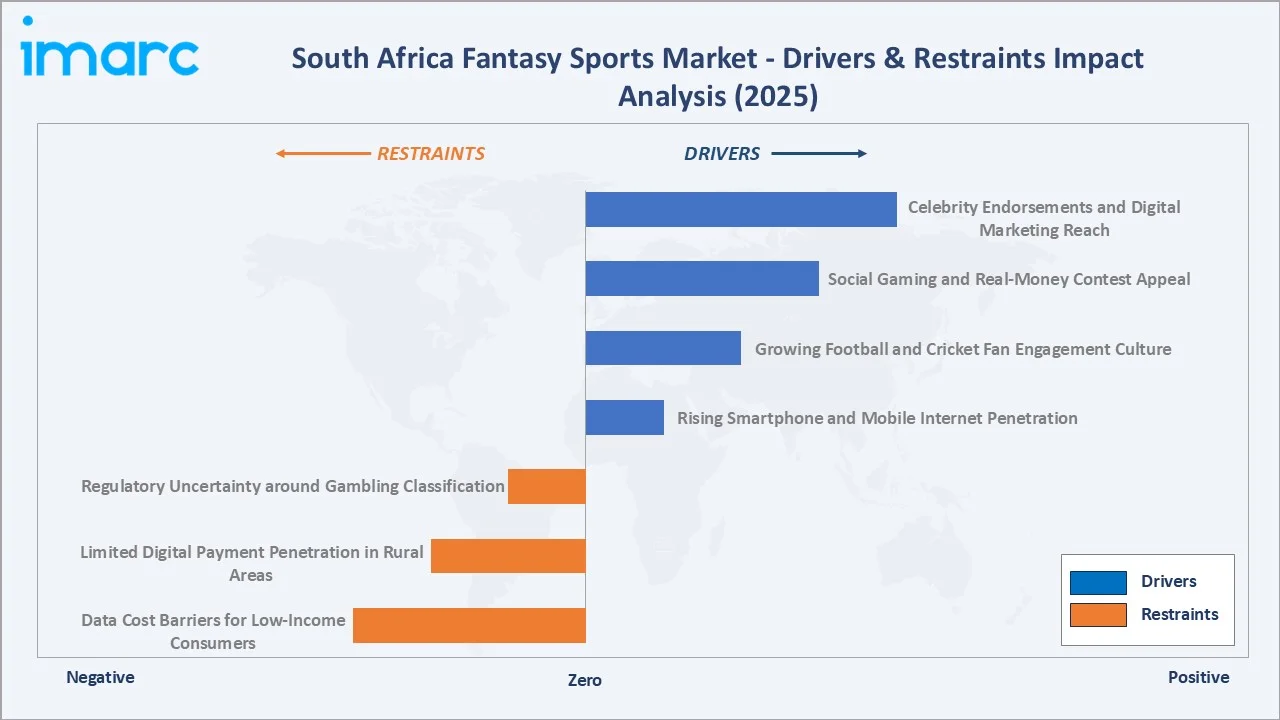

Market Drivers

- Rising Smartphone and Mobile Internet Penetration: In early 2025, South Africa had 124 million active cellular mobile connections, equivalent to 193% of the country’s total population, driven by declining device costs, competitive mobile data pricing, and continued network infrastructure investment by leading telecom operators. This expanding digital access foundation directly enables fantasy sports platform adoption, particularly among younger demographics who represent the core fantasy sports user base and increasingly access entertainment, social, and gaming content.

- Growing Football and Cricket Fan Engagement Culture: South Africa’s deeply embedded football and cricket fan culture provides fantasy sports operators with an exceptionally engaged and passionate user base. The Premier Soccer League’s growing production quality and broadcast reach, combined with cricket’s elevated profile through the SA20 T20 league and national team performances, are sustaining and expanding the pool of sports-engaged consumers.

- Social Gaming and Real-Money Contest Appeal: The broader global normalization of skill-based real-money gaming and social prediction contests is resonating strongly with South African consumers, particularly younger demographics seeking entertainment experiences that combine sports knowledge, social competition with friends, and the potential for cash prize rewards. Fantasy sports platforms are successfully positioning themselves at the intersection of sports fandom, social gaming, and skill-based competition.

- Celebrity Endorsements and Digital Marketing Reach: Fantasy sports operators are increasingly leveraging partnerships with prominent South African athletes, sports commentators, and social media personalities to drive platform awareness and user acquisition. Targeted digital marketing campaigns across social media platforms, combined with influencer partnerships and football and cricket player endorsements, are proving highly effective in reaching South Africa’s sports-engaged, digitally native consumer base.

Market Restraints

- Regulatory Uncertainty around Gambling Classification: South Africa’s fragmented provincial gambling regulatory framework creates ongoing uncertainty regarding the precise classification and licensing requirements for real-money fantasy sports contests, with different provincial gambling boards potentially applying varying interpretations of whether specific fantasy sports formats constitute games of skill or fall under traditional gambling regulation.

- Limited Digital Payment Penetration in Rural Areas: While South Africa’s major metropolitan centers benefit from well-developed digital payment infrastructure, rural and peri-urban areas continue to face limitations in banking access, digital wallet adoption, and reliable internet connectivity that constrain fantasy sports platform usage and real-money contest participation outside the country’s primary urban centers.

- Data Cost Barriers for Low-Income Consumers: Despite improvements in mobile data affordability, the cost of sustained mobile data consumption required for regular fantasy sports platform engagement, including live match updates and in-app notifications, remains a meaningful barrier for South Africa’s lower-income consumer segments, limiting the addressable market for fantasy sports platforms relative to the country’s total smartphone-owning population.

Market Opportunities

- Cricket and T20 League Fantasy Product Expansion: The continued growth and international profile-raising of South Africa’s SA20 T20 league, combined with the broader global expansion of franchise T20 cricket leagues, presents a significant opportunity for fantasy sports operators to develop deeper, more sophisticated cricket-specific fantasy products that capture the format’s fast-paced, high-engagement viewing experience.

- Localized Football Fantasy Products for PSL Engagement: Developing fantasy sports products specifically optimized for Premier Soccer League engagement, including localized statistical models, South African football personality partnerships, and PSL-specific contest formats, represents an opportunity to deepen domestic football fan engagement beyond the European league-focused fantasy products that currently dominate much of the football fantasy sports category.

Market Challenges

- Competition from International Platforms: South Africa’s fantasy sports market faces competitive pressure from well-capitalized international platforms, particularly those with a strong presence in cricket-playing nations, that bring substantial marketing budgets and established product sophistication that can challenge the growth trajectory of smaller domestic and regional operators.

- User Retention and Engagement Sustainability: Fantasy sports platforms face inherent challenges in sustaining user engagement and retention beyond initial sign-up and trial participation, requiring continuous investment in product innovation, contest variety, and engagement features to prevent user churn, particularly during off-season periods for major sports leagues when natural engagement triggers are reduced.

Emerging Market Trends

1. AI-Driven Fantasy Team Builder Tools

Fantasy sports platforms operating in South Africa are increasingly integrating artificial intelligence-powered team-building assistance tools that analyze player statistics, historical performance trends, and matchup data to provide users with data-driven team selection recommendations. These AI-assisted features are particularly appealing to casual fantasy sports participants who may lack the time or statistical expertise to conduct manual player analysis, broadening the addressable market beyond hardcore sports statistics enthusiasts to a wider base of casual sports fans seeking simplified, guided contest participation.

2. SA20 and T20 League Fantasy Engagement Surge

The continued success and growing international broadcast reach of South Africa’s SA20 T20 cricket league is generating substantial fantasy sports engagement during the league’s January-February annual window, with fantasy platforms reporting significant user activity spikes correlated with SA20 match days. This trend is encouraging fantasy sports operators to develop increasingly sophisticated, league-specific product features and marketing campaigns timed to the SA20 calendar, recognizing the league’s growing role as a major annual fantasy sports engagement driver alongside traditional football season engagement.

3. Social and Community-Based Fantasy Contest Formats

Fantasy sports operators are increasingly emphasizing social and community-based contest formats that enable users to create private leagues with friends, colleagues, and social media communities, shifting platform positioning from purely transactional real-money gaming toward social entertainment experiences built around shared sports fandom. This trend reflects broader South African social media usage patterns and is proving effective in driving organic user acquisition through friend referrals and private league invitations.

4. Mobile Payment Integration and Frictionless Onboarding

Fantasy sports platforms are progressively integrating with South Africa’s expanding mobile payment ecosystem, including bank-linked instant EFT payment methods and mobile wallet services, to reduce friction in deposit and withdrawal processes that have historically represented a meaningful barrier to real-money fantasy sports participation. Streamlined KYC verification processes and instant payment processing are becoming key competitive differentiators as operators compete for user acquisition and retention in an increasingly crowded market.

Industry Value Chain Analysis

South Africa’s fantasy sports value chain spans sports data acquisition through end-user contest participation, with each stage involving specialized participants whose capabilities directly influence platform reliability, user experience, and overall market competitiveness.

|

Stage |

Key Players / Examples |

|

Sports Data Providers |

Live sports data and statistics aggregators providing real-time scores, player performance data, and fixture information |

|

Platform Developers |

Mobile app and web platform development teams, UX/UI designers, cloud infrastructure and hosting providers |

|

Fantasy Sports Operators |

Fantasy sports platform operators managing contest creation and prize structures |

|

Payment & Prize Processing |

Payment gateway providers, digital wallet integrations, KYC verification services, prize disbursement and withdrawal processing |

|

Marketing & User Acquisition |

Digital advertising agencies, athlete and celebrity endorsement partnerships, social media marketing |

|

End User Participants |

Casual sports fans, dedicated fantasy league enthusiasts, social gaming participants, sports communities |

Technology Landscape in the South Africa Fantasy Sports Industry

Real-Time Data and Live Scoring Technology

Fantasy sports platforms operating in South Africa depend on robust real-time sports data integration to deliver live scoring updates, player performance statistics, and instant point calculations during active matches. Platforms partner with sports data providers to access live football and cricket feeds, ensuring that fantasy contest standings update in near real-time as on-field events unfold, a critical technical capability for maintaining user engagement during live match periods when fantasy sports participation peaks.

Mobile Application Architecture and User Experience

Given mobile applications’ 64.3% platform dominance in South Africa’s fantasy sports market, operators are investing heavily in native mobile app performance optimization, including efficient data usage design suited to South Africa’s variable mobile data cost environment, offline-capable team management features, and push notification systems that drive re-engagement around match start times and contest deadlines.

AI and Machine Learning for Player Analytics

Artificial intelligence and machine learning technologies are increasingly embedded within South Africa’s fantasy sports platforms to power player recommendation engines, injury risk assessment models, and predictive performance analytics that help users make more informed team selection decisions. These AI-driven features are particularly valuable in democratizing access to sophisticated statistical analysis for casual fantasy sports participants who lack the time or expertise to conduct manual player research, broadening platform appeal beyond dedicated sports statistics enthusiasts.

Payment Gateway and Digital Wallet Integration

Fantasy sports platforms in South Africa integrate with multiple payment gateway providers and digital wallet services to enable convenient deposit and withdrawal processing for real-money contests. Integration with South Africa’s instant EFT payment infrastructure, alongside card payment processing and emerging mobile wallet services, is critical for reducing transaction friction and supporting the rapid, low-friction payment experience that users increasingly expect from digital gaming and entertainment platforms.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Sports Type |

Football |

46.8% |

2025 |

|

Platform |

Mobile Application |

64.3% |

2025 |

|

Demographics |

🔒 |

🔒 |

2025 |

|

Province |

Gauteng |

40.1% |

2025 |

By Sports Type

Football dominates with a 46.8% share in 2025. This segment encompasses fantasy contests built around domestic Premier Soccer League (PSL) matches, continental competitions, and major European football leagues that South African audiences follow extensively. Football’s unmatched cultural penetration across South Africa sustains its position as the foundational sports-type category driving fantasy sports market participation.

To access detailed market analysis, Request Sample

Cricket at 21.7% represents the second-largest sports-type segment and is projected to grow at the fastest rate at approximately 9.6% CAGR, propelled by South Africa’s deep cricketing heritage and the rising popularity of the SA20 T20 league format. Basketball at 12.4%, hockey at 9.6%, and baseball at 4.8% collectively represent smaller but growing fantasy sports categories, reflecting the gradual diversification of South Africa’s sports fan engagement beyond the traditionally dominant football and cricket categories, particularly among younger urban demographics.

By Platform

Mobile application leads with a 64.3% share in 2025, reflecting South Africa’s mobile-first digital consumption patterns where smartphone penetration substantially exceeds fixed broadband and desktop computer access across the broader population. Mobile apps deliver a superior user experience for the time-sensitive, notification-driven engagement model that defines fantasy sports participation, including live match score updates, contest deadline alerts, and frictionless in-app payment processing.

Website platforms at 35.7% continue to serve a meaningful user segment, particularly users accessing fantasy sports contests through desktop or laptop computers in workplace or home settings, as well as users who prefer browser-based access over downloading dedicated mobile applications. While mobile applications are growing faster as smartphone penetration deepens, website platforms remain an important complementary access channel that some operators continue to invest in alongside their primary mobile application offerings.

Regional Market Insights

Gauteng’s market leadership (40.1%, 2025) reflects its status as South Africa’s most populous and economically dynamic province. Johannesburg and Pretoria together host the country’s densest urban population, highest smartphone and mobile data penetration, and greatest concentration of disposable income available for discretionary digital entertainment spending, creating the optimal environment for fantasy sports platform adoption and sustained engagement.

Western Cape at 23.8% represents the country’s second-largest market, anchored by Cape Town’s affluent and digitally engaged consumer base that combines strong football and cricket fan culture with high smartphone penetration and disposable income availability. KwaZulu-Natal at 18.2% benefits from Durban’s strong cricket heritage and growing engagement with the SA20 T20 league.

|

Province |

Share (2025) |

Key Growth Drivers |

|

Gauteng |

40.1% |

Johannesburg and Pretoria’s dense urban population; highest smartphone and mobile data penetration; strongest digital payment infrastructure; concentration of disposable income for discretionary gaming spend |

|

Western Cape |

23.8% |

Cape Town’s affluent, digitally engaged consumer base; strong cricket and football fan culture; growing tech-savvy youth demographic |

|

KwaZulu-Natal |

18.2% |

Durban’s strong cricket heritage and SA20 league fan base; growing urban smartphone penetration; expanding digital payment adoption |

|

Eastern Cape |

10.5% |

Growing urban centers in Gqeberha and East London; rising youth smartphone adoption; improving mobile network infrastructure |

|

Mpumalanga |

4.3% |

Emerging digital infrastructure development; growing football fan engagement; expanding mobile data access in regional towns |

|

Others |

3.1% |

Smaller provinces with developing digital infrastructure and gradually expanding fantasy sports platform awareness and adoption |

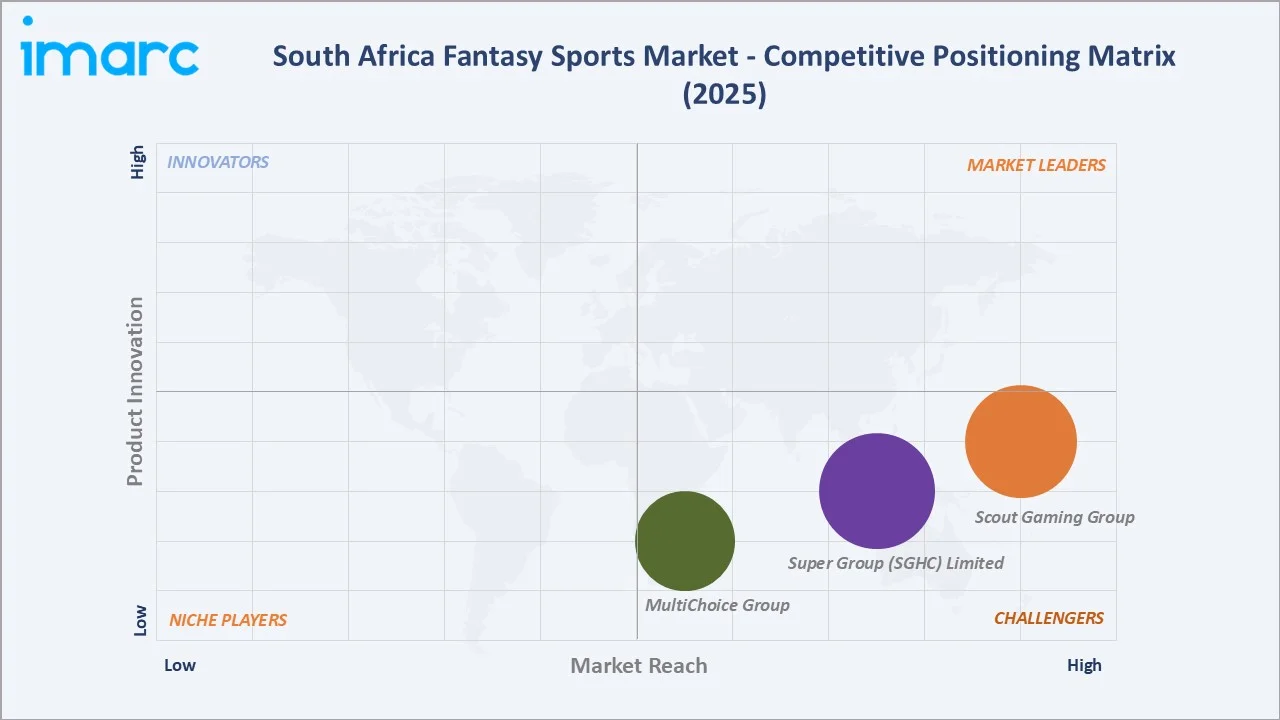

Competitive Landscape

South Africa’s fantasy sports market features a competitive landscape combining established international platforms with strong global brand recognition alongside regional and domestic operators that have built localized product offerings tailored to South African sports fan preferences.

|

Company Name |

Key Sports Focus |

Market Position |

Core Strength |

|

Scout Gaming Group |

FanTeam Fantasy Football, Basketball, Hockey, Am.Football, Tennis, Baseball, Motor Racing, UFC |

Strong Challenger |

European football league fantasy product strength; daily fantasy contest variety; international platform credibility |

|

Super Group (SGHC) Limited |

Betway Fantasy Football, Cricket, among others |

Strong Challenger |

Strong South African brand presence; integrated sports betting and fantasy ecosystem; local marketing investment |

|

MultiChoice Group |

SuperSport Fantasy Football, Rugby, Cricket, Golf, among others |

Challenger |

Deep integration with SuperSport broadcast content; strong PSL and local football fan engagement; broadcast cross-promotion |

International platforms compete through global brand recognition, sophisticated technology platforms, and substantial marketing budgets, while South African-focused operators differentiate through localized product features, broadcast partnerships, and deeper integration with domestic sports leagues including the PSL and SA20 that resonate strongly with local fan bases.

Key Company Profiles

Super Group (SGHC) Limited

Super Group (SGHC) Limited operates Betway Fantasy as part of the broader Betway sports betting and gaming brand, which maintains substantial visibility and brand recognition in South Africa through extensive sports sponsorship activity, including partnerships with South African football and cricket properties.

- Product Portfolio: Football, basketball, hockey, am.football, tennis, baseball, motor racing, and UFC fantasy sports contests integrated with Betway’s broader sports betting platform.

- Recent Developments: In January 2024, Betway SA20 signed Zoho as its Official Business Technology Partner to strengthen the league’s digital capabilities and operational efficiency.

- Strategic Focus: Integrated fantasy sports and sports betting ecosystem; brand visibility through sports sponsorship; South African market localization; cross-platform user acquisition synergies.

MultiChoice Group

MultiChoice Group operates SuperSport Fantasy with the distinct advantage of direct integration with SuperSport, South Africa’s dominant sports broadcasting network, enabling powerful cross-promotional opportunities during live football and cricket broadcasts that few competing fantasy sports platforms can match.

- Product Portfolio: Football fantasy contests aligned with PSL and European league broadcasts, multi-sport fantasy formats covering football, rugby, cricket, and golf among others.

- Recent Developments: In January 2024, MultiChoice Group partnered with KingMakers to launch SuperSportBet, a sports and casino betting platform for fans in South Africa. The platform combines SuperSport’s sports brand with KingMakers’ betting technology, offering global sports markets, bonus bets, and responsible gambling tools.

- Strategic Focus: Broadcast cross-promotion leverage; PSL and domestic football fan engagement depth; multi-sport platform expansion; viewer-to-participant conversion optimization.

Market Concentration Analysis

South Africa’s fantasy sports market exhibits moderate concentration, with international platforms including Dream11 and FanTeam holding significant share alongside strong domestic and regional competitors including Betway Fantasy and SuperSport Fantasy that have built differentiated positioning through local broadcast partnerships and sports betting ecosystem integration. The market remains sufficiently fragmented to support continued competitive entry, particularly in emerging sports categories beyond football and cricket.

Competitive dynamics are increasingly shaped by the depth of localized product features, including South African league-specific statistical models, local payment method integration, and broadcast or sponsorship partnerships that create differentiated user acquisition channels beyond generic digital marketing approaches available to all competing platforms.

Investment & Growth Opportunities

Fastest Growing Segments

Cricket sports type (~9.6% CAGR) and mobile application platform (~9.3% CAGR) represent the highest-growth investment vectors through 2034. Cricket’s growth is directly linked to the continued international profile-raising of the SA20 T20 league, while mobile application growth reflects the structural shift toward mobile-first digital engagement across South Africa’s expanding smartphone user base.

Emerging Market Expansion

Eastern Cape and Mpumalanga, currently representing a combined 14.8% of national market share, offer meaningful underpenetrated growth potential as mobile network infrastructure investment and smartphone affordability improvements progressively extend fantasy sports platform access beyond South Africa’s primary metropolitan centers of Gauteng and Western Cape.

Venture and Institutional Investment Trends

- Growing international investor interest in African digital gaming and sports technology markets is creating potential capital availability for South African fantasy sports platforms seeking to scale product development and marketing investment to compete more effectively against well-capitalized global platforms.

- Strategic partnerships between fantasy sports operators and South African sports broadcasting and sponsorship properties represent a structurally valuable growth lever, as demonstrated by SuperSport Fantasy’s broadcast integration model, creating replicable partnership opportunities with other domestic sports media and league properties.

- The continued international expansion and broadcast reach growth of the SA20 T20 cricket league creates a structural multi-year tailwind for cricket-focused fantasy sports investment, as the league’s growing global visibility progressively attracts both domestic and international fantasy sports participation.

Future Market Outlook (2026-2034)

South Africa’s fantasy sports market is positioned for sustained, above-average digital entertainment sector growth through 2034. From a base of USD 141.9 Million in 2025, the market is projected to reach USD 303.3 Million by 2034, representing total incremental value creation of USD 161.4 Million at a CAGR of 8.54%.

This growth reflects the compound effect of continued smartphone and mobile internet penetration deepening, sustained football and cricket fan engagement culture, and the progressive maturation of South Africa’s digital payment infrastructure that increasingly supports frictionless real-money contest participation.

The market composition is expected to evolve through 2034, with cricket’s share of sports-type revenue growing from 21.7% as the SA20 league’s international profile continues to rise, while mobile applications’ platform dominance is projected to extend further beyond its current 64.3% share as desktop and website-based access continues to decline in relative importance.

Gauteng is expected to maintain its regional leadership position, while Eastern Cape and Mpumalanga are projected to grow at above-average rates as digital infrastructure investment progressively extends market access beyond South Africa’s established metropolitan centers.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 65 industry participants in 2024–2025, including fantasy sports platform executives, sports data providers, digital marketing specialists, payment processing partners, and sports industry analysts across South Africa’s major digital entertainment and gaming markets.

Secondary Research

Secondary research encompassed operator platform data and public disclosures, South African telecommunications and digital infrastructure reports, provincial gambling and gaming regulatory publications, sports broadcasting viewership data, and industry publications covering South Africa’s digital gaming and sports entertainment sectors.

Forecasting Models

Market size estimations were derived from top-down and bottom-up forecasting incorporating smartphone and mobile internet penetration trends, sports fan engagement data, platform user growth metrics, and operator revenue intelligence. A base-case CAGR of 8.54% reflects consensus estimates validated against digital entertainment sector growth trends and IMARC market tracking from 2020 to 2025.

South Africa Fantasy Sports Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sports Types Covered | Football, Baseball, Basketball, Hockey, Cricket, Others |

| Platforms Covered | Website, Mobile Application |

| Demographics Covered | Under 25 Years, 25-40 Years, Above 40 Years |

| Regions Covered | Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, Others |

| Companies Covered | Scout Gaming Group, Super Group (SGHC) Limited, MultiChoice Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the South Africa fantasy sports market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the South Africa fantasy sports market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the South Africa fantasy sports industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the South Africa Fantasy Sports Market Report

The South Africa fantasy sports market reached USD 141.9 Million in 2025 and is projected to reach USD 303.3 Million by 2034, growing at a CAGR of 8.54% during 2026-2034.

Football leads with a 46.8% market share in 2025, reflecting South Africa’s unmatched football fan culture spanning domestic Premier Soccer League engagement and extensive following of major European football leagues across all demographic segments.

Mobile application leads with a 64.3% market share in 2025, reflecting South Africa’s mobile-first digital consumption patterns where smartphone penetration significantly exceeds desktop and fixed broadband access across the broader population.

Gauteng leads with a 40.1% share in 2025, anchored by Johannesburg and Pretoria’s dense urban population, highest smartphone and digital payment penetration, and greatest concentration of disposable income for discretionary gaming spend.

Some of the leading companies include Scout Gaming Group, Super Group (SGHC) Limited, and MultiChoice Group. These platforms compete through differentiated product offerings spanning international platform sophistication, sports betting ecosystem integration, and South African broadcast and sponsorship partnerships.

Cricket fantasy sports growth (~9.6% CAGR) is driven by South Africa’s deep cricketing heritage combined with the rising popularity and international profile of the SA20 T20 league, which has successfully attracted younger audiences and significantly boosted cricket fantasy contest participation beyond traditional format followers.

Key challenges include regulatory uncertainty around the gambling classification of real-money fantasy sports contests across South Africa’s fragmented provincial gambling regulatory framework, competition from well-capitalized international platforms, and the challenge of sustaining user engagement during off-season periods for major sports leagues.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)