South Africa Forage Market Size, Share, Trends and Forecast by Crop Type, Product Type, Animal Type, and Province, 2026-2034

South Africa Forage Market Summary:

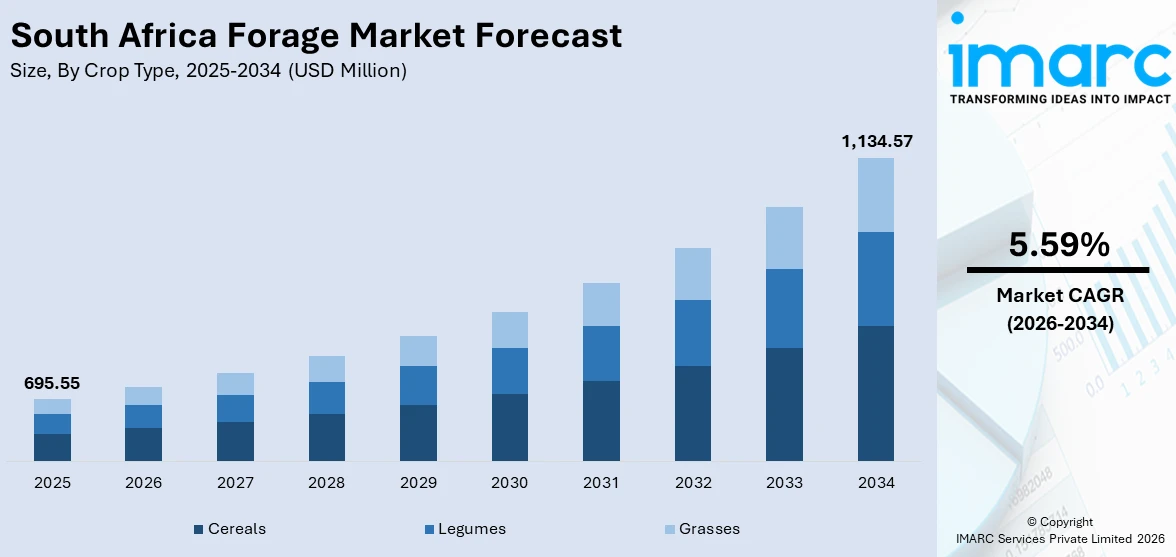

The South Africa forage market size was valued at USD 695.55 Million in 2025 and is projected to reach USD 1,134.57 Million by 2034, growing at a compound annual growth rate of 5.59% from 2026-2034.

The South Africa forage market is driven by expanding livestock production, increasing demand for quality animal nutrition, and rising focus on sustainable feeding practices. Growing dairy and beef sectors require reliable forage supplies, while farmers increasingly adopt improved forage varieties to enhance productivity. The market benefits from favorable agricultural conditions in key provinces and modernizing farming operations across the country.

Key Takeaways and Insights:

- By Crop Type: Cereals dominate the market with a share of 46% in 2025, owing to their adaptability across diverse climatic zones, established cultivation practices, and high nutritional value for livestock. Growing demand from feedlots and dairy operations continues to fuel cereal forage expansion.

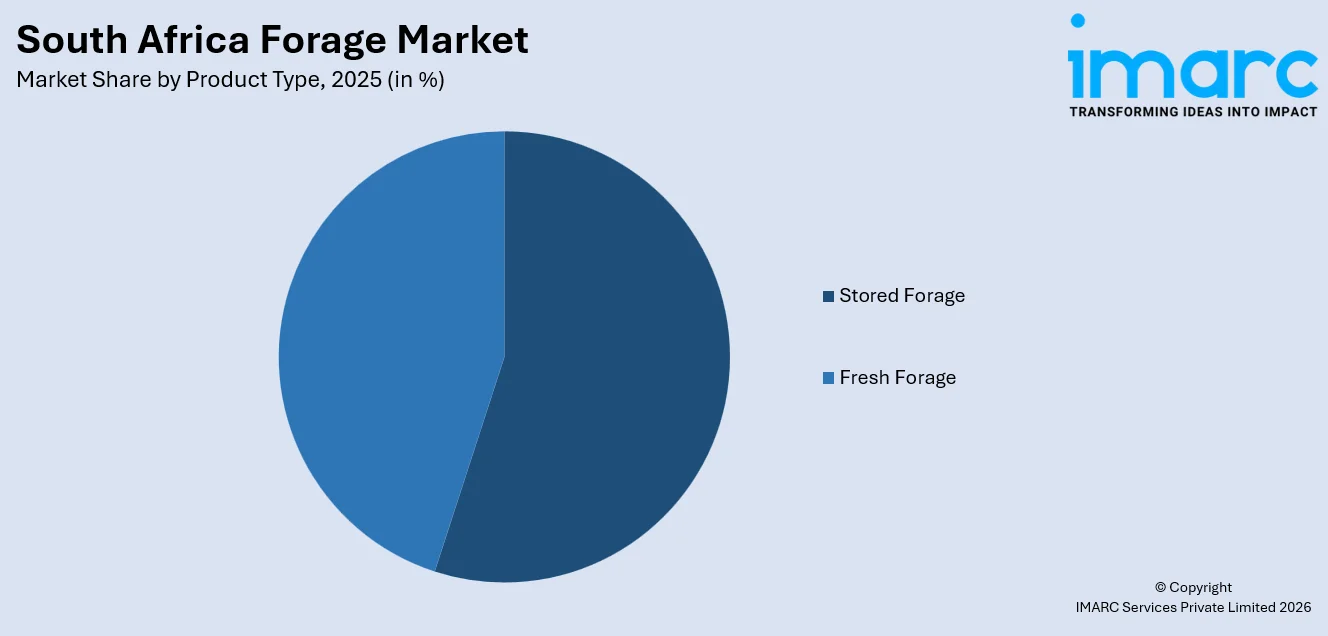

- By Product Type: Stored forage leads the market with a share of 55% in 2025. This dominance is driven by the need for year-round feed availability, reduced wastage through proper preservation techniques, and consistent nutritional quality maintenance throughout dry seasons.

- By Animal Type: Ruminants comprise the largest segment with a market share of 50% in 2025, reflecting the significant cattle and sheep population requiring high-fiber diets for optimal digestive function, milk production, and meat quality across commercial farming operations.

- By Province: Gauteng represents the largest province with 22% share in 2025, driven by concentrated livestock operations, proximity to major processing facilities, established distribution networks, and higher demand from commercial dairy and feedlot enterprises serving urban markets.

- Key Players: Key players drive the South Africa forage market by expanding product portfolios, introducing improved seed varieties, investing in research for drought-resistant cultivars, and strengthening distribution networks. Their focus on precision nutrition and sustainable farming practices accelerates market development across diverse agricultural segments.

To get more information on this market Request Sample

The South Africa forage market demonstrates robust growth potential, driven by the expanding livestock sector and increasing commercialization of animal farming operations. As of September 2024, animal production represented the largest segment of agriculture in South Africa, accounting for roughly 42% of the overall agricultural output in terms of value. Farmers increasingly recognize forage as a cost-effective feed source compared to commercial compound feeds, driving adoption across both commercial and emerging farming sectors. The feedlot industry relies heavily on consistent forage supplies for fattening operations. Government initiatives promoting agricultural development, combined with private sector investments in improved seed varieties and precision agriculture technologies, position the market for continued expansion throughout the forecast period. Rising focus on improving livestock productivity and feed efficiency is further encouraging farmers to invest in high-quality forage solutions that support sustainable and profitable animal husbandry practices.

South Africa Forage Market Trends:

Growing Adoption of Drought-Resistant Forage Varieties

South African farmers are increasingly adopting drought-tolerant forage varieties to address climate change challenges and water scarcity concerns. Improved seed technologies offering enhanced resilience during dry periods are gaining traction across major producing provinces. Research organizations partner with seed firms to develop cultivars adapted to regional environments, fostering sustainable forage production. This trend supports the South Africa forage market growth as producers seek reliable yields despite variable rainfall patterns affecting traditional cultivation areas.

Expansion of Silage Production for Dairy Operations

The dairy industry increasingly favors silage production for maintaining consistent year-round feed quality and nutritional value. Fermented high-moisture fodder preserves nutrients effectively while offering better palatability for dairy cattle compared to traditional dry hay methods. Modern silage techniques, including improved inoculants and storage systems, enhance fermentation quality and aerobic stability. Dairy farmers recognize silage as essential for total mixed rations supporting optimal milk production across seasonal variations.

Integration of Precision Agriculture in Forage Management

Precision agriculture technologies are transforming forage production across South Africa, enabling farmers to optimize irrigation, fertilization, and harvesting operations. Advanced monitoring systems provide real-time data on soil moisture, crop health, and yield potential, supporting informed decision-making. Variable-rate irrigation systems curb water use significantly while maintaining productivity levels. These technological advancements improve resource efficiency, reduce operational costs, and enhance overall South Africa forage market share competitiveness. The integration of drones and global positioning system (GPS)-enabled equipment is further improving yield predictability and helping farmers manage climate variability more effectively across different forage-growing regions. As per IMARC Group, the South Africa drones market is expected to attain USD 336.27 Million by 2033.

Market Outlook 2026-2034:

The South Africa forage market demonstrates promising growth prospects, driven by expanding livestock operations, rising meat consumption, and increasing focus on quality animal nutrition. The market generated a revenue of USD 695.55 Million in 2025 and is projected to reach a revenue of USD 1,134.57 Million by 2034, growing at a compound annual growth rate of 5.59% from 2026-2034. Growing dairy sector requirements, feedlot industry expansion, and increasing adoption of improved forage varieties support market development. Government initiatives promoting agricultural productivity, combined with private sector investments in seed technology and sustainable farming practices, create favorable conditions for continued market expansion across South Africa's diverse agricultural regions.

South Africa Forage Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Crop Type |

Cereals |

46% |

|

Product Type |

Stored Forage |

55% |

|

Animal Type |

Ruminants |

50% |

|

Province |

Gauteng |

22% |

Crop Type Insights:

- Cereals

- Legumes

- Grasses

Cereals dominate with a market share of 46% of the total South Africa forage market in 2025.

Cereals, including maize, oats, sorghum, and wheat varieties, form the foundation of livestock nutrition across South Africa's diverse agricultural regions. Cereal forages are crucial for intensive livestock operations because of their high calorie content, superior digestibility, and consistent yields under ideal management. Major agricultural provinces, such as the Free State, North West, Mpumalanga, and KwaZulu-Natal, cultivate cereal fodder crops. As a staple food and the principal source of feed for livestock operations, maize continues to be one of the most significant grain crops.

With silage and hay production methods, cereal forages are essential to ensuring year-round feed supply. To increase biomass yields and forage quality, farmers are increasingly using better hybrid seeds and balanced nutrient management techniques. These crops integrate well into crop rotation systems, helping maintain soil fertility and reduce pest pressure. Cereals are emerging as a reliable and scalable forage option in South Africa's changing animal agricultural landscape because of their tolerance to mechanical harvesting and storage, which also supports large-scale livestock and feedlot operations.

Product Type Insights:

Access the comprehensive market breakdown Request Sample

- Stored Forage

- Fresh Forage

Stored forage leads with a share of 55% of the total South Africa forage market in 2025.

Stored forage, encompassing hay and silage products, provides essential feed security throughout seasonal variations when fresh grazing becomes limited. Hay production, particularly lucerne, offers excellent protein content and digestibility for high-producing dairy cows and performance livestock. The Northern Cape provinces, including Jankempdorp, Hopetown, Jacobsdal, and Douglas, serve as major lucerne hay-producing regions benefiting from favorable environmental conditions and irrigation infrastructure. Growing adoption of mechanized baling and storage practices is further improving hay quality consistency and reducing post-harvest losses for producers.

Silage production continues to gain prominence among dairy operations seeking consistent nutrient preservation and improved palatability for livestock. The anaerobic fermentation process retains more nutrients compared to traditional haymaking, reducing leaf loss and maintaining higher feeding value. As of January 2026, South Africa shipped approximately 160,000 to 240,000 Tons of lucerne hay each year, primarily to nearby nations and the Middle East, demonstrating the quality and competitive positioning of locally produced stored forage. Investments in modern storage facilities, improved harvesting equipment, and advanced inoculation technologies support the expansion of stored forage production across commercial farming operations.

Animal Type Insights:

- Ruminants

- Swine

- Poultry

- Others

Ruminants exhibit a clear dominance with a 50% share of the total South Africa forage market in 2025.

Ruminants, comprising cattle, sheep, and goats, represent the primary consumer of forage products across South Africa's agricultural landscape. In 2024, cattle production contributed R48 Billion to the agricultural economy, making it the second-largest livestock sector after poultry. Ruminant animals require high-fiber diets for optimal rumen function, making forage an essential dietary component rather than a supplementary feed source. The beef and dairy industries drive substantial forage consumption through feedlot operations and commercial dairy farming.

Ruminant-based agricultural systems are being encouraged to concentrate more on nutrition optimization due to the growing demand for premium meat and dairy products. Better feed conversion, consistent productivity in cattle, sheep, and goats, and effective rumen function are supported by improved forage rations. To fulfill the unique dietary requirements of ruminants at various stages of production, commercial ranches and smallholder operations are using diverse forage regimens. In order to ensure that ruminants maintain consistent development, health, and reproductive performance throughout the year, seasonal grazing limits further increase reliance on conserved fodder.

Province Insights:

- Gauteng

- KwaZulu-Natal

- Western Cape

- Mpumalanga

- Eastern Cape

- Others

Gauteng represents the leading province with a 22% share of the total South Africa forage market in 2025.

Gauteng leads the South Africa forage market, driven by concentrated livestock operations, established distribution networks, and proximity to major processing facilities serving urban consumer markets. Large commercial farming operations that depend on steady forage supplies for dairy and feedlot operations are located in the province. The geographical location of Gauteng facilitates effective logistics that link producers with manufacturers of animal feed and final customers throughout the whole agricultural value chain. For intensive livestock operations, this link enables dependable fodder availability and quicker turnaround times.

Well-established agricultural infrastructure that supports intensive livestock production systems helps the growth of the market in the province. The demand for meat and dairy products is fueled by higher disposable incomes and urban population density, which propel forage consumption across commercial farming operations. Gauteng is positioned as a major hub for the South Africa forage industry because of investments in feed manufacturing facilities, storage infrastructure, and distribution capabilities that link farmers with expanding consumer markets.

Market Dynamics:

Growth Drivers:

Why is the South Africa Forage Market Growing?

Expanding Livestock Sector and Rising Meat Consumption

South Africa’s livestock sector continues to show strong momentum, supported by rising domestic demand for meat and the steady expansion of commercial farming operations. Animal production has grown steadily over the years and forms the backbone of the country’s agricultural economy. Poultry and cattle farming play a central role, with producers increasingly relying on quality forage to support animal health and productivity. Changing dietary preferences and higher purchasing power are driving greater meat consumption, which is strengthening demand for reliable feed systems built around forage-based nutrition. As livestock operations become more commercialized, farmers are focusing on feed efficiency, where balanced forage rations help control costs and improve performance. The expansion of feedlot operations has further increased year-round forage requirements, as intensive production systems depend on consistent and nutritious feed inputs. Collectively, these dynamics reinforce the importance of forage as a critical component of sustainable and profitable livestock production in South Africa.

Growing Dairy Industry Requirements for Quality Nutrition

The dairy industry's ongoing development creates substantial demand for high-quality forage products essential for milk production optimization. As dairy farming becomes more commercialized, producers are placing greater emphasis on nutrition strategies that support higher milk yields, improved animal health, and longer lactation cycles. Quality forage forms the foundation of dairy rations, supplying the fiber and energy needed for efficient rumen function and consistent milk output. Farmers are increasingly adopting silage, lucerne hay, and improved pasture varieties to ensure reliable feed availability throughout the year, especially during dry seasons. Rising awareness about the link between forage quality and milk composition is also influencing feeding decisions, as better nutrition translates into higher butterfat and protein levels. Larger dairy operations are investing in improved storage, harvesting, and feed management practices to preserve forage quality and reduce wastage. These trends are steadily increasing demand for premium forage products.

Government Support and Agricultural Development Initiatives

Government initiatives supporting agricultural productivity and rural development create favorable conditions for forage market expansion across South Africa. The Agriculture and Agro-processing Master Plan provides policy continuity that helps unlock private capital investment in agricultural operations, including forage production. The proclamation of the Climate Change Act, 2024 in March 2025 steers investment towards climate-resilient cultivars, including drought-tolerant forage varieties suited to variable rainfall conditions. These policy measures encourage farmers to adopt sustainable production practices that improve long-term productivity while reducing environmental risks. Support for research, extension services, and farmer training is helping accelerate the adoption of improved forage seeds and modern cultivation techniques. Public–private partnerships (PPPs) are also strengthening input supply chains and market access, enabling both commercial and emerging farmers to participate more actively in forage production.

Market Restraints:

What Challenges the South Africa Forage Market is Facing?

Water Scarcity and Drought Vulnerability

Climate variability and recurring drought conditions pose significant challenges for forage production across South Africa. Water scarcity affects irrigation-dependent cultivation, particularly lucerne production requiring consistent moisture for optimal yields. Extended dry periods reduce forage availability, forcing farmers to rely on costly alternatives while constraining overall market supply. The dependency on favorable rainfall patterns creates production uncertainty affecting both commercial and emerging farming operations.

Rising Input Costs and Electricity Tariffs

Escalating input costs, including electricity tariffs for irrigation pumps, fertilizers, and fuel, squeeze profit margins for forage producers. Frequent load-shedding forces growers to resort to diesel generators or invest in solar backup systems, adding operational expenses. High capital requirements for haymaking equipment, irrigation infrastructure, and storage facilities create barriers, particularly for smaller-scale operations seeking market entry or expansion.

Limited Domestic Forage Seed Production Capacity

South Africa remains a net importer of forage seeds due to insufficient domestic production capacity, creating supply chain vulnerabilities. Import dependency exposes producers to exchange rate fluctuations and international supply disruptions affecting seed availability and pricing. Limited local seed multiplication programs constrain access to improved varieties, while quality control requirements for imported seeds add administrative complexity and costs throughout the forage production value chain.

Competitive Landscape:

The South Africa forage market features a fragmented competitive landscape with multiple domestic and international players, serving diverse agricultural segments. Companies focus on expanding product portfolios, introducing improved seed varieties, and strengthening distribution networks across major farming regions. Investments in research and development (R&D) activities for drought-resistant cultivars and high-yielding forage varieties drive innovations throughout the market. Strategic partnerships between international seed companies and local distributors enhance market penetration while ensuring technical support availability for farmers. Players increasingly adopt sustainable practices and precision agriculture technologies to differentiate offerings and capture market share among environmentally conscious commercial farming operations.

South Africa Forage Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Crop Types Covered | Cereals, Legumes, Grasses |

| Product Types Covered | Stored Forage, Fresh Forage |

| Animal Types Covered | Ruminants, Swine, Poultry, Others |

| Provoinces Covered | Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South Africa Forage Market Report

The South Africa forage market size was valued at USD 695.55 Million in 2025.

The South Africa forage market is expected to grow at a compound annual growth rate of 5.59% from 2026-2034 to reach USD 1,134.57 Million by 2034.

Cereals dominated the market with a share of 46%, owing to their adaptability across diverse climatic zones, established cultivation practices, high nutritional value for livestock, and consistent demand from feedlot and dairy operations.

Key factors driving the South Africa forage market include expanding livestock sector, rising meat consumption, growing dairy industry requirements, government agricultural support programs, and increasing adoption of improved forage varieties.

Major challenges include water scarcity and drought vulnerability affecting production, rising input costs and electricity tariffs impacting profitability, limited domestic forage seed production capacity, and climate variability creating production uncertainty.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)