South Africa Gluten-Free Beer Market Size, Share, Trends and Forecast by Ingredient Type, Product Type, Packaging Type, Distribution Channel, and Region, 2026-2034

South Africa Gluten-Free Beer Market Summary:

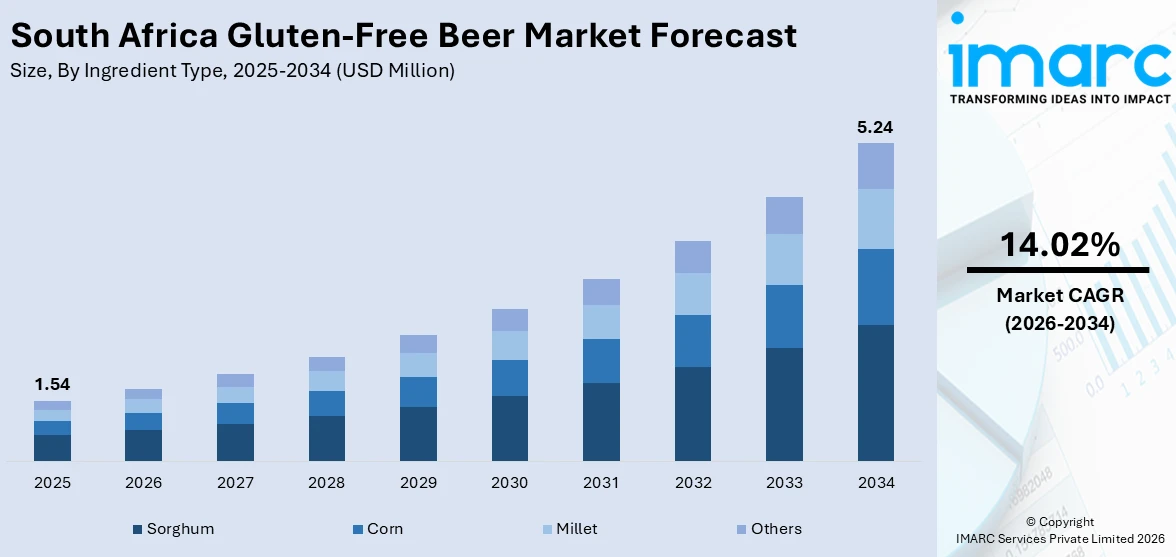

The South Africa gluten-free beer market size was valued at USD 1.54 Million in 2025 and is projected to reach USD 5.24 Million by 2034, growing at a compound annual growth rate of 14.02% from 2026-2034.

The market is gaining momentum as health-conscious consumers increasingly seek dietary alternatives that align with evolving wellness trends. Rising awareness of celiac disease and gluten sensitivity, coupled with growing interest in premium craft beverages, is broadening the consumer base beyond those with medical dietary needs. The proliferation of craft breweries experimenting with indigenous grains such as sorghum and millet, alongside expanding distribution networks and improving product accessibility, is expanding South Africa gluten-free beer market share.

Key Takeaways and Insights:

- By Ingredient Type: Sorghum dominates the market with approximately 36.5% revenue share in 2025, driven by the grain’s deep cultural significance in traditional African brewing and its natural gluten-free properties that support authentic, heritage-inspired production.

- By Product Type: Lager leads the market with a share of 67.8% in 2025, reflecting strong consumer preference for crisp, refreshing gluten-free options that closely replicate the taste profile of conventional mainstream beers.

- By Packaging Type: Bottles hold the largest share at 54.3% in 2025, supported by established ties with on-premise venues, consumer preference for premium glass presentation, and sustainability-driven returnable bottle initiatives.

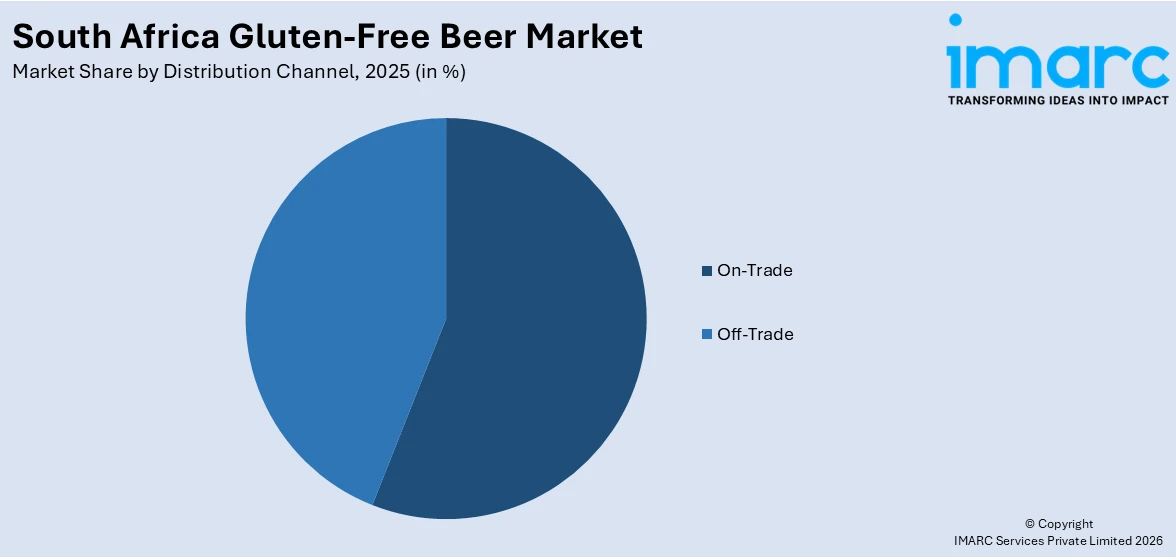

- By Distribution Channel: On-trade commands for the highest revenue share of 55.9% in 2025, benefiting from South Africa’s vibrant hospitality culture, growing craft beer taproom experiences, and increasing gluten-free menu offerings across bars and restaurants.

- By Region: Gauteng represents the largest segment with a market share of 34.2% in 2025, anchored by its status as the country’s economic hub with the highest concentration of affluent, health-conscious consumers and premium hospitality establishments.

- Key Players: The market features a mix of established craft breweries and emerging producers competing through product innovation, flavor diversification, sustainability commitments, and strategic distribution partnerships to capture growing consumer demand.

To get more information on this market Request Sample

The gluten-free beer market in South Africa is moving forward because of the growing awareness of dietary needs, innovation in brewing, and the trend of premiumization, which is changing the face of the beverage industry in the country. One of the key drivers that are helping the market move forward is the increasing use of local ingredients like sorghum in modern brewing methods, which is connecting the country’s heritage with the modern needs of consumers. For example, at the 2025 African Beer Cup, Soul Barrel Brewing took home the award for Best Beer in Africa with Wild African Soul, which is a collaboration with Johannesburg-based Tolokazi Beer that combines traditional sorghum umqombothi with a farmhouse ale aged in wine barrels, defeating 260 entries from 14 African countries. Increasing retail presence, engagement with the hospitality industry, and consumer willingness to pay a premium for specialty dietary products are also helping to create a positive environment for the adoption of gluten-free beer in the country.

South Africa Gluten-Free Beer Market Trends:

Integration of Traditional Sorghum Brewing with Modern Craft Techniques

The South African gluten-free beer market is experiencing a unique blend of traditional umqombothi beer production techniques with modern craft beer production standards. This blend honors traditional fermentation techniques while adopting quality control practices that enhance shelf life. In 2024, United National Breweries, the South African subsidiary of Zimbabwe's Delta Corporation, will open its new sorghum beer brewery by the end of its financial year, which ends on 31st March 2024. The opening of the new brewery has been delayed because of equipment hold-ups. Additionally, the initiative is encouraged by the government's efforts via the Sorghum Cluster Initiative, which encourages the growth of indigenous grains, providing an opportunity for breweries to utilize locally derived, naturally gluten-free ingredients while appreciating the rich beer heritage of South Africa.

Premiumization and Craft Beer Portfolio Expansion

The strategies of premium positioning are transforming the gluten-free beer market as breweries begin to create specialized product lines to cater to the demands of premium consumers who are willing to pay a higher price for quality and innovation. Darling Brew enhanced its Break Free gluten-free beer product line with a new Red Ale made from naturally gluten-free ingredients, aside from its successful gluten-free lager product. The strategy of premium positioning is not only focused on the product itself but also on the packaging design, sustainability, and marketing through brewery tasting rooms. Craft breweries focus on artisanal brewing processes, unique product flavors, and limited edition products to build brand loyalty among specific consumer markets. The strategy is in line with the overall consumer shift towards authenticity and provenance, where the heritage of brewing, ingredient disclosure, and sustainability become major drivers of purchasing decisions aside from the gluten-free functionality, making it possible to justify the premium price points that can support smaller-scale production.

Digital Commerce and Direct-to-Consumer Distribution Models

E-commerce platforms are revolutionizing the accessibility of markets for gluten-free beer brands, especially for craft breweries, to reach consumers without the need for distribution channel intermediaries. The online market trend is fueled by the penetration of smartphones in the market and the development of logistics infrastructure, while social media marketing enables breweries to build communities and create brand stories for product discovery by health-conscious groups searching for specialized products for their dietary needs. According to IMARC Group, the South Africa e-commerce market is projected to reach USD 2,199.27 Billion by 2033.

Market Outlook 2026-2034:

South Africa’s gluten-free beer market is poised for sustained advancement, supported by growing health awareness, expanding craft brewery capabilities, and increasing consumer demand for premium specialty beverages. The market generated a revenue of USD 1.54 Million in 2025 and is projected to reach a revenue of USD 5.24 Million by 2034, growing at a compound annual growth rate of 14.02% from 2026-2034. The commercialization of traditional sorghum beer through modern production standards presents unique growth opportunities, particularly as heritage-based products gain traction among both local and international consumers seeking authentic African culinary experiences. Enhanced distribution infrastructure, including digital commerce platforms and expanded retail presence, will facilitate wider product availability while premium craft offerings cultivate higher-value market segments through differentiated positioning.

South Africa Gluten-Free Beer Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Ingredient Type |

Sorghum-based |

36.5% |

|

Product Type |

Lager |

67.8% |

|

Packaging Type |

Bottles |

54.3% |

|

Distribution Channel |

On-Trade |

55.9% |

|

Region |

Gauteng |

34.2% |

Ingredient Type Insights:

- Corn

- Sorghum

- Millet

- Others

Sorghum dominates with a market share of 36.5% of the total South Africa gluten-free beer market in 2025.

Sorghum-based gluten-free beer benefits from South Africa's extensive agricultural heritage in indigenous grain cultivation and traditional brewing practices rooted in umqombothi production. The naturally gluten-free grain provides favorable malting characteristics and distinctive flavor profiles that resonate with consumers seeking authentic African beverage experiences. Recent commercialization efforts by major breweries have elevated sorghum beer from informal traditional contexts into formal retail channels, expanding accessibility while maintaining cultural authenticity. The segment's growth trajectory reflects successful integration of traditional knowledge with modern brewing science, creating market opportunities that balance cultural authenticity with contemporary consumer expectations for consistency, safety, and premium quality across gluten-free beer categories.

The ingredient's versatility enables diverse product formulations ranging from traditional opaque beers to contemporary clear lagers, facilitating market segmentation across premium and value price points. Brewers leverage sorghum's complex flavor characteristics to create differentiated products that compete effectively against imported gluten-free beers while celebrating indigenous brewing heritage. Growing consumer interest in heritage grains and ancient agricultural practices further strengthens market positioning for sorghum-based offerings. However, challenges including inconsistent grain quality from smallholder farmers and shorter shelf life compared to enzyme-treated barley beers require ongoing innovation in production processes and quality control standards.

Product Type Insights:

- Ale

- Lager

- Others

Lager leads with a share of 67.8% of the total South Africa gluten-free beer market in 2025.

Lager dominates the South Africa gluten-free beer market through consumer familiarity, refreshing taste profiles, and successful product innovations from craft breweries that maintain authentic lager characteristics despite gluten-free constraints. The product type benefits from established consumer preferences within South Africa's broader beer market, where lagers account for significant consumption volumes across demographic segments. Gluten-free lagers successfully replicate the crisp, clean finishing profiles that define traditional lager styles, minimizing taste compromises that historically challenged gluten-free beer acceptance.

Lager's dominance extends across both on-trade and off-trade channels, with the product type's versatility supporting diverse consumption occasions from casual social drinking to premium dining experiences. Light body and moderate alcohol content align with contemporary health-conscious consumption patterns favoring sessionability over high-alcohol alternatives. The segment benefits from established distribution relationships and brand recognition, as lager's mainstream appeal facilitates retail placement and consumer trial compared to specialized ale or stout offerings. Marketing strategies emphasize lifestyle compatibility and inclusive social participation, positioning gluten-free lagers as enabling products that remove dietary barriers without sacrificing taste satisfaction or social integration. Innovation opportunities include flavored lager variants and seasonal limited editions that build on core product equity while introducing novelty elements to sustain repeat purchases.

Packaging Type Insights:

- Bottles

- Cans

- Others

Bottles exhibit a clear dominance with a 54.3% share of the total South Africa gluten-free beer market in 2025.

Bottle packaging dominates the South Africa gluten-free beer market through established premium positioning, consumer perceptions of quality associated with glass containers, and strong ties with on-premise venues that favor bottled presentations for table service and visual appeal. Glass bottles convey craftsmanship and artisanal values that align with premium gluten-free product positioning, supporting higher price points through packaging-driven quality cues. The format's transparency enables visual product inspection, showcasing beer clarity and color characteristics that communicate brewing quality and ingredient purity to discerning consumers.

Traditional associations between glass packaging and premium beer categories reinforce purchasing decisions within gift-giving contexts and special occasion consumption, where packaging aesthetics influence brand perceptions and willingness to pay. Environmental sustainability narratives further support glass adoption, as bottles offer infinite recyclability without material degradation, appealing to environmentally conscious consumers who integrate sustainability criteria into purchasing decisions. The segment benefits from established retail display infrastructure optimized for bottled beer merchandising, ensuring favorable shelf placement and visibility compared to emerging packaging formats. However, convenience limitations relative to canned alternatives may constrain growth within outdoor consumption occasions and younger demographic segments prioritizing portability and casual drinking contexts over traditional premium positioning.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- On-Trade

- Off-Trade

On-trade leads with a share of 55.9% of the total South Africa gluten-free beer market in 2025.

On-trade distribution maintains dominant positioning within the South Africa gluten-free beer market through experiential consumption contexts, product discovery facilitation, and service-oriented environments that support premium pricing and brand engagement. Restaurants, bars, and brewery tasting rooms provide curated beverage selections that introduce consumers to specialized gluten-free offerings through staff recommendations, tasting menus, and pairing programs that educate purchases and build brand loyalty. The channel's role in social consumption rituals and celebratory occasions drives trial among consumers exploring dietary alternatives within familiar hospitality settings.

Professional service standards ensure optimal product presentation through proper glassware, serving temperatures, and food pairings that maximize taste experiences, addressing historical quality concerns that challenged gluten-free beer category acceptance. The segment benefits from craft beer culture's emphasis on brewery visits, guided tastings, and immersive brand narratives that transform product purchases into lifestyle experiences resonating with health-conscious consumers seeking meaningful consumption connections beyond functional dietary compliance. On-trade venues function as marketing platforms enabling direct consumer engagement, feedback collection, and relationship building that supports brand development and product refinement.

Regional Insights:

- Gauteng

- KwaZulu-Natal

- Western Cape

- Mpumalanga

- Eastern Cape

- Others

Gauteng exhibits a clear dominance with a 34.2% share of the total South Africa gluten-free beer market in 2025.

Gauteng dominates the South Africa gluten-free beer market through concentrated urban population centers including Johannesburg and Pretoria, where higher disposable incomes support premium product purchases and greater awareness of dietary health trends drives gluten-free adoption. The province's dense hospitality infrastructure comprising restaurants, bars, and entertainment venues provides extensive on-trade distribution networks that facilitate product accessibility and brand visibility among target consumer demographics. Economic concentration within Gauteng generates sophisticated consumer segments familiar with international food trends and willing to experiment with specialized dietary products, creating favorable conditions for gluten-free beer market development.

Gauteng's retail landscape encompasses modern trade formats including supermarket chains and specialty liquor stores that allocate shelf space to emerging categories addressing health-conscious consumer demands. E-commerce infrastructure benefits from concentrated delivery logistics networks that enable efficient last-mile fulfillment, supporting digital commerce growth within gluten-free categories. The province houses craft brewery concentrations and beer culture institutions that drive product innovation, quality standards, and consumer education through brewery tours, tasting events, and craft beer festivals that showcase gluten-free alternatives alongside conventional offerings.

Market Dynamics:

Growth Drivers:

Why is the South Africa Gluten-Free Beer Market Growing?

Rising Prevalence and Diagnosis of Celiac Disease and Gluten Sensitivities

Growing medical awareness and improved diagnostic capabilities are expanding identified populations with gluten-related disorders, directly increasing demand for certified gluten-free beverage alternatives that enable social participation without dietary compromise. Enhanced screening protocols within healthcare systems, particularly for at-risk demographics including individuals with autoimmune conditions and family histories of gluten intolerance, are identifying previously undiagnosed cases requiring strict dietary management. Autoimmune diseases are on the rise in South Africa, with an estimated 2.5 million individuals impacted in the nation. This expanding diagnosed and self-identified consumer base creates sustained demand growth for compliant products that maintain quality equivalence with conventional alternatives, positioning gluten-free beer as essential category within inclusive beverage offerings.

Health-Conscious Lifestyle Adoption and Wellness Trends

Broader consumer shifts toward preventive health management, clean eating philosophies, and functional food consumption are driving gluten-free adoption beyond diagnosed medical populations, expanding addressable markets to include lifestyle-motivated consumers seeking perceived wellness benefits from dietary modifications. Contemporary wellness culture emphasizes elimination of inflammatory ingredients, artificial additives, and heavily processed components, with gluten increasingly perceived as unnecessary or potentially harmful even absent clinical diagnosis. Social media influencers, celebrity endorsements, and popular health literature promote gluten-free diets as mechanisms for weight management, improved digestion, enhanced mental clarity, and increased energy levels, creating mainstream acceptance that transcends medical necessity. This lifestyle positioning elevates gluten-free from niche medical requirement to aspirational dietary choice associated with health consciousness, body optimization, and informed consumer decision-making. This lifestyle-driven demand supplements medical necessity consumption, creating more robust market dynamics less vulnerable to diagnosis rate fluctuations while expanding distribution beyond specialty health channels into mainstream retail. IMARC Group predicts that the South Africa health and wellness market is projected to attain USD 42.01 Billion by 2033.

Indigenous Heritage Revitalization and Craft Beer Innovation

Government support for traditional sorghum cultivation combined with craft brewery interest in authentic African brewing techniques is creating unique market positioning opportunities that differentiate South African gluten-free beer from international competitors through cultural heritage narratives and indigenous ingredient utilization. The CEO of the Beer Association of South Africa (BASA) states that the beer industry operates not just as a consumer item but as an essential capital-heavy sector that connects agriculture, processing, logistics, retail, and hospitality. This connection sustains around 210,000 jobs across the country and highlights the importance of brewing to South Africa's economy. The convergence of traditional African brewing culture with modern craft beer sophistication creates distinctive competitive advantages unavailable to international brands, supporting export potential while strengthening domestic market differentiation through unique cultural positioning that combines wellness functionality with heritage celebration, educational storytelling, and community connection that transcends commodity beverage status.

Market Restraints:

What Challenges the South Africa Gluten-Free Beer Market is Facing?

Premium Pricing Barriers Limiting Market Penetration

Significantly higher production costs associated with gluten-free brewing create retail price premiums that restrict market accessibility beyond affluent consumer segments, limiting volume growth potential within price-sensitive demographics and constraining category expansion into mainstream consumption patterns. Specialized ingredients including certified gluten-free grains, enzyme treatments for gluten reduction, and dedicated production facilities to prevent cross-contamination elevate manufacturing expenses relative to conventional barley-based beers benefiting from established supply chains and economies of scale. Small production volumes characteristic of craft gluten-free producers further amplify unit costs through inability to leverage bulk purchasing discounts and fixed cost distribution across limited output.

Limited Distribution Networks and Product Availability

Gluten-free beer availability remains concentrated within urban centers and specialty retailers, creating accessibility barriers for consumers in rural areas, smaller towns, and conventional retail environments where category penetration remains minimal despite growing demand awareness. Distribution economics favor high-volume mainstream products, marginalizing smaller gluten-free producers unable to meet minimum order quantities or provide marketing support justifying retail shelf allocation. Many liquor stores and supermarkets maintain limited or nonexistent gluten-free beer selections, forcing consumers toward specialized health food outlets or direct brewery purchases that require intentional shopping missions rather than convenient impulse acquisitions during routine grocery trips. This distribution gap constrains category growth by limiting exposure opportunities and creating friction in purchase processes that discourage trial and reduce consumption frequency.

Quality Inconsistency and Shelf Life Limitations

Production challenges inherent to gluten-free brewing, particularly utilizing traditional sorghum fermentation methods, result in quality variability and shortened shelf life that undermine consumer confidence and repeat purchase likelihood essential for category establishment. Sorghum beer's tendency toward rapid souring absent pasteurization or preservative treatments limits distribution range and necessitates cold chain maintenance that elevates logistics costs and restricts retail placement to refrigerated sections commanding premium shelf fees.

Competitive Landscape:

The South Africa gluten-free beer market demonstrates evolving competitive dynamics characterized by established craft breweries competing with emerging specialized producers across premium positioning and heritage-based differentiation strategies. Market leadership reflects brewing expertise, sustainable production methodologies, and effective distribution partnerships that secure retail placement and on-premise venue relationships essential for category visibility and consumer education. Market participants pursue differentiation through ingredient sourcing narratives, brewing technique transparency, sustainability commitments, and experiential marketing via brewery tasting rooms and cultural events that build brand communities. Strategic partnerships between craft brewers and traditional sorghum beer producers represent emerging competitive dynamics that combine modern quality standards with indigenous authenticity, creating distinctive positioning unavailable to conventional craft breweries or traditional informal producers operating independently without access to formal distribution channels and quality infrastructure supporting commercial scalability.

South Africa Gluten-Free Beer Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Ingredient Types Covered |

Corn, Sorghum, Millet, Others |

|

Product Types Covered |

Ale, Lager, Other Beer Types |

|

Packaging Types Covered |

Bottles, Cans, Others |

|

Distribution Channels Covered |

On-Trade, Off-Trade |

|

Regions Covered |

Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South Africa Gluten-Free Beer Market Report

The South Africa gluten-free beer market size was valued at USD 1.54 Million in 2025.

The South Africa gluten-free beer market is expected to grow at a compound annual growth rate of 14.02% from 2026-2034 to reach USD 5.24 Million by 2034.

Sorghum-based gluten-free beer, holding the largest revenue share of 36.5% in 2025, leads the market owing to the grain’s deep cultural significance in traditional African brewing, natural gluten-free properties, and growing commercial adoption by craft breweries.

Key factors driving the South Africa gluten-free beer market include rising prevalence and diagnosis of celiac disease and gluten sensitivities expanding medically necessary consumption, health-conscious lifestyle adoption among wellness-oriented consumers seeking functional dietary modifications, indigenous heritage revitalization supported by government sorghum production initiatives, craft beer innovation integrating traditional brewing techniques, enhanced e-commerce distribution facilitating convenient product access, and growing consumer demand for inclusive beverage options that accommodate dietary restrictions without compromising taste satisfaction or social participation opportunities.

Major challenges include premium pricing barriers limiting accessibility beyond affluent consumer segments and restricting volume growth within price-sensitive demographics, limited distribution networks concentrating availability in urban centers while underserving rural and smaller town markets, and regulatory complexities surrounding gluten-free certification standards ensuring product compliance and consumer safety across diverse production methodologies and ingredient sourcing frameworks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)