South Africa Healthcare IT Market Size, Share, Trends and Forecast by Product and Services, Component, Delivery Mode, End User, and Province, 2026-2034

South Africa Healthcare IT Market Summary:

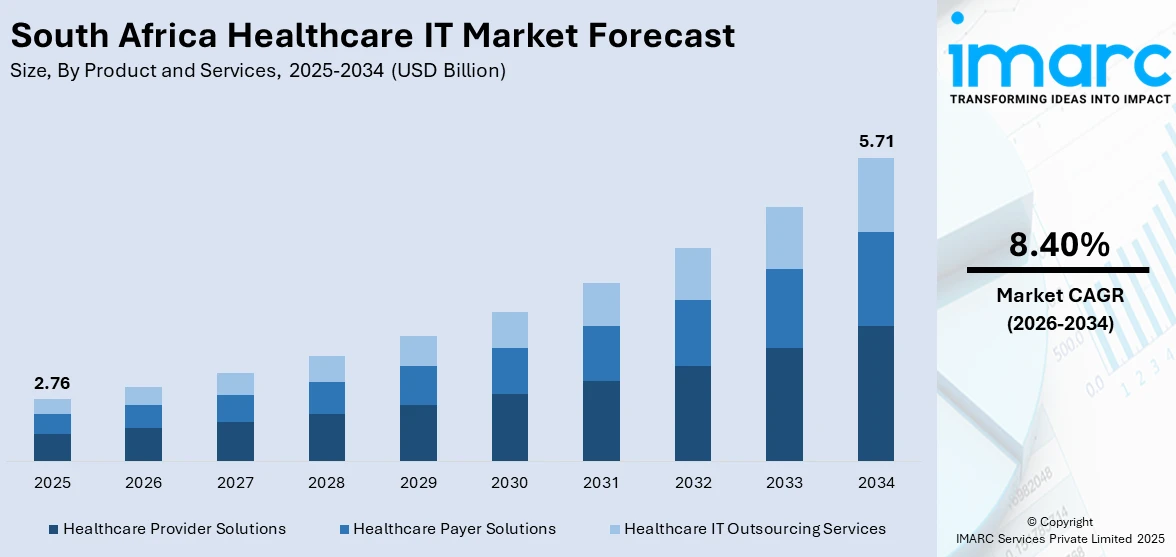

The South Africa healthcare IT market size was valued at USD 2.76 Billion in 2025 and is projected to reach USD 5.71 Billion by 2034, growing at a compound annual growth rate of 8.40% from 2026-2034.

Digital transformation initiatives driven by the National Health Insurance implementation are accelerating healthcare IT adoption across public and private sectors. The deployment of integrated electronic health record systems, cloud-based healthcare platforms, and telemedicine solutions addresses the nation's healthcare accessibility challenges while improving care coordination and operational efficiency. Government mandates for digital health infrastructure combined with rising smartphone penetration and increasing demand for remote healthcare services position technology as a critical enabler of healthcare system modernization, expanding the South Africa healthcare IT market share.

Key Takeaways and Insights:

- By Product and Services: Healthcare provider solutions dominate the market with a share of 54% in 2025, driven by comprehensive clinical and nonclinical IT solution requirements for hospitals and healthcare facilities.

- By Component: Software leads the market with a share of 46% in 2025, powering electronic health records, clinical decision support, and healthcare analytics applications.

- By Delivery Mode: Cloud-based represents the largest segment with a market share of 55% in 2025, enabling scalable and cost-effective healthcare IT deployments.

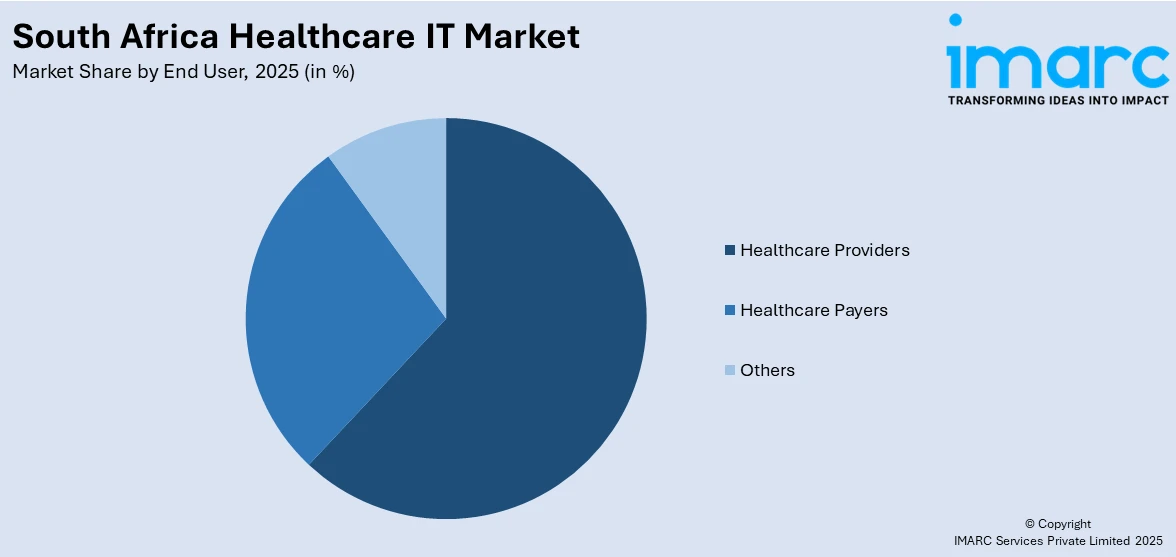

- By End User: Healthcare providers account for the largest share of 62% in 2025, as hospitals and clinics digitize patient records and clinical workflows.

- By Province: Gauteng dominates with 36% market share in 2025, benefiting from concentrated healthcare infrastructure and higher technology adoption rates.

- Key Players: The South Africa healthcare IT market exhibits moderate competitive intensity with multinational technology corporations competing alongside regional solution providers. International vendors partner with local implementation firms to deliver comprehensive healthcare information systems tailored to South Africa's regulatory requirements and healthcare delivery models.

To get more information on this market Request Sample

South Africa's healthcare IT landscape is undergoing rapid transformation as the country prepares for National Health Insurance rollout while addressing the quadruple burden of disease affecting its population. The National Digital Health Strategy 2019-2024 established critical foundations through the Health Patient Registration System project, creating a unified patient registry using South African identification numbers. This infrastructure enables interoperability across fragmented public and private healthcare systems while supporting population health management initiatives. The government's commitment to digital health governance combined with private sector innovation in cloud platforms, artificial intelligence applications, and mobile health solutions creates a dynamic ecosystem. However, persistent challenges including cybersecurity vulnerabilities, infrastructure gaps in rural areas, and workforce capacity constraints require sustained investment and public-private collaboration to achieve universal healthcare coverage goals. The 4th International Conference on Public Health in Africa (CPHIA 2025) occurred from 22 to 25 October 2025 in Durban, South Africa, focusing on the theme “Advancing Self-Reliance to Attain Universal Health Coverage and Health Security in Africa.”

South Africa Healthcare IT Market Trends:

Cloud-Based EHR Platforms Accelerating System Integration

Healthcare providers increasingly migrate to cloud-based electronic health record systems that offer superior scalability, reduced infrastructure costs, and seamless interoperability compared to legacy on-premise solutions. Cloud deployment enables real-time data access across multiple care settings, supporting coordinated patient management and reducing duplication of services. The transition aligns with National Health Insurance requirements for integrated patient information systems while addressing budget constraints through subscription-based pricing models. Web and cloud-based EHR systems captured a significant market share in South Africa's electronic health records segment in 2024, demonstrating strong provider preference for cloud architecture. Advanced platforms incorporate artificial intelligence for clinical decision support, automated documentation, and predictive analytics that enhance diagnostic accuracy and treatment planning efficiency. In 2025, In his State of the Nation Address, President Cyril Ramaphosa emphasized the government's intention to establish an electronic health record system. Ramaphosa stated that this would be included in the groundwork for the National Health Insurance (NHI). This involves creating the initial phase of a unified electronic health record system, the groundwork for forming ministerial advisory committees on health technologies and healthcare benefits, and the accreditation framework for healthcare service providers.

Telemedicine Expansion Bridging Geographic Healthcare Gaps

Remote consultation platforms proliferate across South Africa as healthcare organizations leverage telecommunications technology to extend specialist access to underserved rural populations and reduce patient travel burdens. Telemedicine services expanded rapidly following their emergency deployment during pandemic response, with sustained adoption driven by convenience, cost savings, and healthcare worker shortages. Mobile health applications including Find-A-Med, Kids First Aid, and Hello Doctor deliver primary care consultations, medication information, and health education to smartphone users nationwide. The HIV Clinicians Expert Telemedicine Platform is the largest telemedicine provider in South Africa, utilizing videolink technology to connect with individuals living with HIV throughout the nation, regardless of their location. Telehealth integration with electronic health records enables continuity of care documentation while facilitating remote patient monitoring for chronic disease management.

AI Enhancing Clinical Workflows and Diagnostics

Healthcare providers deploy AI-powered solutions for medical imaging analysis, disease prediction models, clinical decision support systems, and administrative workflow automation that improve care quality while reducing operational costs. Machine learning algorithms analyze vast datasets from electronic health records to identify at-risk patients, recommend treatment protocols, and flag potential medication interactions before adverse events occur. IMARC Group predicts that the South Africa's AI market is projected to reach USD 5,989.92 Million by 2033, as hospitals and clinics integrate intelligent systems for diagnostics and therapeutic planning. The Department of Science and Innovation announced the 110,000 Genomes Project in November 2024, planning to sequence genomes of South African participants to enable precision medicine applications tailored to the population's genetic diversity.

Market Outlook 2026-2034:

South Africa's healthcare IT sector demonstrates robust growth trajectory as digital transformation becomes imperative for achieving universal healthcare coverage through National Health Insurance implementation. Cloud computing adoption, artificial intelligence integration, and telemedicine platform deployment will reshape healthcare delivery models while addressing persistent challenges of geographic access inequality and resource constraints. The market generated a revenue of USD 2.76 Billion in 2025 and is projected to reach a revenue of USD 5.71 Billion by 2034, growing at a compound annual growth rate of 8.40% from 2026-2034. Government infrastructure investments prioritizing broadband connectivity to healthcare facilities combined with private sector innovation in mobile health applications create favorable conditions for sustained market expansion. Cybersecurity concerns owing to ransomware attack that disrupted services of the population drive demand for robust data protection solutions and disaster recovery capabilities.

South Africa Healthcare IT Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product and Services |

Healthcare Provider Solutions |

54% |

|

Component |

Software |

46% |

|

Delivery Mode |

Cloud-Based |

55% |

|

End User |

Healthcare Providers |

62% |

|

Province |

Gauteng |

36% |

Product and Services Insights:

- Healthcare Provider Solutions

- Clinical Solutions

- Nonclinical Healthcare IT Solutions

- Healthcare Payer Solutions

- Pharmacy Audit and Analysis Systems

- Claims Management Solutions

- Analytics and Fraud Management Solutions

- Member Eligibility Management Solutions

- Provider Network Management Solutions

- Billing and Accounts (Payment) Management Solutions

- Customer Relationship Management Solutions

- Population Health Management Solutions

- Others

- Healthcare IT Outsourcing Services

- Provider HCIT Outsourcing Services

- Payer IT Outsourcing Services

- Operational IT Outsourcing Services

Healthcare provider solutions dominate with a market share of 54% of the total South Africa healthcare IT market in 2025.

Healthcare Provider Solutions represent the foundational technology infrastructure enabling hospitals, clinics, and ambulatory care facilities to digitize patient records, streamline clinical workflows, and comply with regulatory reporting requirements. Clinical solutions including computerized physician order entry, electronic medication administration records, clinical decision support systems, and radiology information systems directly support patient care delivery through improved accuracy, reduced medical errors, and enhanced care coordination across departments. Nonclinical solutions encompassing revenue cycle management, human resources information systems, and supply chain management optimize administrative operations while reducing overhead costs.

The National Health Insurance implementation mandate accelerates provider solution adoption as healthcare organizations prepare for integrated information systems requirements supporting claims processing, quality reporting, and population health analytics. Cloud-based deployment models gain preference over traditional on-premise systems due to lower capital expenditure, automatic software updates, and scalability accommodating facility expansion without infrastructure replacement. Private hospitals and public facilities increasingly recognize comprehensive provider solutions as strategic investments essential for competitive service delivery, operational efficiency, and compliance with evolving digital health regulations.

Component Insights:

- Software

- Hardware

- Services

Software leads with a share of 46% of the total South Africa healthcare IT market in 2025.

Software components power the core functionality of healthcare information systems, encompassing electronic health record applications, practice management platforms, billing and coding software, clinical documentation tools, and data analytics engines that transform raw patient data into actionable insights. Application software enables healthcare providers to capture, store, retrieve, and exchange patient information while supporting clinical decision-making through evidence-based protocols and drug interaction alerts. The South African Medical Research Council developed specialized health information apps for primary healthcare workers, demonstrating locally developed software addressing specific operational needs of public sector facilities operating with limited resources.

Software-as-a-Service delivery models eliminate traditional barriers of high upfront licensing costs and complex installation procedures that previously prevented smaller healthcare facilities from accessing advanced clinical systems. Subscription-based pricing enables clinics to deploy sophisticated EHR platforms with monthly operating expenses rather than capital investments, democratizing access to enterprise-grade healthcare IT capabilities. AI software applications for medical imaging analysis, patient risk stratification, and administrative workflow automation represent high-growth segments as providers seek competitive advantages through technology-enabled efficiency gains.

Delivery Mode Insights:

- On-premises

- Cloud-based

Cloud-based exhibits a clear dominance with a 55% share of the total South Africa healthcare IT market in 2025.

Cloud-based healthcare IT deployment transforms system implementation economics by shifting costs from capital expenditure to operating expense while eliminating infrastructure management burdens that divert healthcare organizations from core clinical missions. Software-as-a-Service platforms hosted in secure data centers provide automatic backup, disaster recovery, and business continuity capabilities that many hospitals cannot economically replicate through on-premise installations. Cloud architectures enable seamless system scalability supporting healthcare facility expansion, seasonal volume fluctuations, and unexpected capacity demands without costly hardware procurement cycles.

Remote accessibility from any internet-connected device empowers clinicians to access patient records, enter documentation, and review test results from home, satellite clinics, or mobile care settings, enhancing workflow flexibility particularly valuable for telemedicine applications. Multi-tenant cloud platforms serving numerous healthcare clients distribute development costs across larger customer bases, enabling smaller vendors to deliver enterprise features at affordable price points competing effectively against traditional market leaders. Government infrastructure investments prioritizing broadband connectivity expansion particularly in underserved areas directly enable cloud healthcare IT adoption previously constrained by inadequate internet access.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Healthcare Providers

- Hospitals

- Ambulatory Care Centers

- Home Healthcare Agencies, Nursing Homes, and Assisted Living Facilities

- Diagnostic and Imaging Centers

- Pharmacies

- Healthcare Payers

- Private Payers

- Public Payers

- Others

Healthcare providers leads with a share of 62% of the total South Africa healthcare IT market in 2025.

Healthcare providers including hospitals, clinics, ambulatory surgery centers, diagnostic facilities, and pharmacies constitute the primary end users driving healthcare IT adoption through operational requirements for patient registration systems, clinical documentation platforms, medication management tools, and laboratory information systems. Hospitals represent the largest provider segment deploying comprehensive enterprise resource planning systems integrating clinical, financial, and administrative functions across inpatient wards, emergency departments, operating theaters, and ancillary service departments.

The National Health Insurance implementation creates unprecedented demand for provider information systems supporting claims submission, utilization management, quality metrics reporting, and population health analytics required under value-based care payment models. Private hospital groups maintain competitive advantage through technology investments enabling superior patient experiences including patient portals, mobile appointment scheduling, and electronic prescription delivery. Public sector facilities serving a major portion of South Africa's population confront enormous digitization challenges including aging infrastructure, budget constraints, and workforce capacity limitations that slow EHR adoption despite government mandates. Ambulatory care centers and diagnostic imaging facilities deploy specialized clinical systems optimized for high-volume outpatient workflows including radiology information systems interfacing directly with picture archiving and communication systems storing medical images.

Province Insights:

- Gauteng

- KwaZulu-Natal

- Western Cape

- Mpumalanga

- Eastern Cape

- Others

Gauteng exhibits a clear dominance with a 36% share of the total South Africa healthcare IT market in 2025.

Gauteng province commands healthcare IT market leadership through concentration of major public and private hospital networks, specialized medical facilities, and healthcare corporate headquarters within Johannesburg and Pretoria metropolitan areas. The province benefits from superior telecommunications infrastructure including extensive fiber optic networks and 4G/5G mobile coverage enabling reliable cloud platform connectivity essential for real-time electronic health record access and telemedicine applications. Healthcare spending increased reflecting government commitment to infrastructure modernization, with Gauteng receiving proportionally higher allocations supporting provincial hospital IT system upgrades and district health information system deployments.

Private medical aid scheme coverage concentrates in urban Gauteng areas where higher income levels and employment rates enable healthcare insurance adoption, driving demand for sophisticated provider systems supporting claims processing and member engagement platforms. Provincial government initiatives aligning with National Digital Health Strategy priorities accelerate public facility digitization through coordinated procurement, standardized system specifications, and shared services reducing individual hospital implementation costs. Medical technology vendors and healthcare IT consulting firms establish Gauteng operations providing local implementation support, system integration services, and ongoing maintenance reducing total cost of ownership compared to remote vendor relationships. Academic medical centers teaching hospitals pioneer advanced clinical system deployments, AI applications, and precision medicine initiatives that establish implementation frameworks subsequently adopted across broader healthcare networks.

Market Dynamics:

Growth Drivers:

Why is the South Africa Healthcare IT Market Growing?

National Health Insurance Implementation Mandating Integrated Systems

The National Health Insurance Bill signed into law in 2024 fundamentally restructures South Africa's healthcare financing and delivery model, requiring unprecedented information technology infrastructure enabling universal coverage administration, claims processing, provider credentialing, and quality monitoring across fragmented public and private sectors. The NHI legislation mandates development of a National Health Information Repository and Data system extracting patient information from electronic health records to support fund administration, actuarial analysis, and population health management. Healthcare providers must deploy certified information systems capable of electronic claims submission, eligibility verification, prior authorization processing, and standardized clinical documentation supporting outcomes-based reimbursement models replacing historical fee-for-service payment structures. The Health Patient Registration System project establishes unified patient identifiers using South African national ID numbers, creating foundational data infrastructure enabling seamless care coordination as patients access services across multiple facilities. Government digital health governance structures including the Ministerial Advisory Committee on eHealth provide strategic direction, standardized specifications, and implementation support accelerating healthcare organization IT adoption. NHI transformation represents the single most significant healthcare IT market driver generating sustained demand for provider solutions, payer platforms, outsourcing services, and infrastructure upgrades throughout the forecast period.

National Digital Health Strategy Establishing Comprehensive Framework

The National Digital Health Strategy 2019-2024 articulates government vision for person-centered digital health enabling better care coordination, improved population health outcomes, and enhanced patient engagement through technology-enabled healthcare delivery transformation. Strategic priorities including comprehensive electronic health record development, health systems business process digitization, and enhanced mobile health capabilities create clear roadmap guiding public sector investments and private sector innovation initiatives. The strategy establishes health information standards, interoperability frameworks, and cybersecurity requirements providing certainty enabling healthcare organizations and technology vendors to develop compliant solutions addressing government specifications. MomConnect maternal health program reaching millions of pregnant women through mobile messaging demonstrates successful mHealth implementation models scalable across additional clinical domains including chronic disease management, vaccination campaigns, and health education initiatives. Government recognition that digital health infrastructure represents essential enabler of healthcare system transformation drives sustained budget allocations, regulatory support, and public-private partnerships accelerating market development despite competing fiscal priorities. In 2025, during the G20 Social Summit in Johannesburg, South Africa unveiled a groundbreaking national initiative to address that query. The South African Health Products Regulatory Authority (SAHPRA) and PATH, supported by funding from Wellcome, have initiated the Comprehensive AI Regulation and Evaluation for Mental Health (CARE MH) program to create the first-ever regulatory framework for artificial intelligence in the realm of mental health.

Rising Smartphone Penetration Enabling Mobile Health Innovation

Smartphone adoption exceeding 60% of South Africa's population combined with expanding 4G and 5G network coverage creates massive addressable market for mobile health applications delivering healthcare services, health information, and patient engagement tools directly to consumers' mobile devices. As of early 2025, there are over 50 million internet users in South Africa. This has increased over 2.5 million users from 2024. Mobile health apps overcome traditional barriers of transportation costs, long clinic wait times, and geographic distance particularly benefiting rural populations lacking convenient access to healthcare facilities and specialist services. Messaging platforms enable cost-effective patient communications for appointment reminders, medication adherence support, test result notifications, and health education campaigns reaching patients who may not have sophisticated smartphones or data plans. Mobile health generates patient-reported health data including vital signs from connected wearable devices, symptom tracking, and medication adherence logs that populate electronic health records with longitudinal information supporting proactive chronic disease management and preventive care interventions. Startup ecosystem innovation accelerated by initiatives.

Market Restraints:

What Challenges the South Africa Healthcare IT Market is Facing?

Cybersecurity Vulnerabilities Threatening Critical Healthcare Operations

Healthcare organizations confront escalating cyber threats as attackers increasingly target sensitive patient data and critical clinical systems for ransomware attacks, data breaches, and operational disruption. Many healthcare facilities operate legacy IT infrastructure and medical devices lacking fundamental security features including encryption, access controls, and security monitoring, creating expanded attack surfaces that overwhelm limited cybersecurity resources. Financial pressures and operational urgencies incentivize healthcare organizations to pay ransoms quickly to restore critical systems, reinforcing attacker perceptions that healthcare targets yield higher probability of profitable outcomes compared to other industry sectors.

Infrastructure and Connectivity Gaps Constraining Rural Adoption

Inadequate broadband network infrastructure and unreliable electricity supply in rural and underserved areas fundamentally limit cloud-based healthcare IT deployment and real-time system access essential for comprehensive electronic health record functionality. High market-driven costs of telecommunications services combined with limited competition outside major metropolitan areas create economic barriers preventing smaller healthcare facilities from affording reliable internet connectivity supporting cloud applications. Healthcare workers in rural clinics frequently lack basic computer literacy and digital health training necessary for effective health information system utilization, while insufficient ongoing technical support leaves facilities unable to troubleshoot system issues or optimize platform configurations. Government infrastructure investments prioritizing broadband expansion to healthcare facilities progress slowly due to competing budget priorities and complex coordination across multiple departments responsible for telecommunications policy, healthcare services, and information technology governance.

Workforce Capacity and Budget Constraints Slowing Implementation

South Africa's critical shortage of healthcare professionals creates workforce capacity constraints limiting organizational bandwidth for health IT system selection, implementation project management, and staff training initiatives. Inadequate human resource capacity to procure and implement complex eHealth solutions was identified as main challenge in previous digital health strategy reviews, with public sector facilities particularly affected by limited technical staff expertise in health information system administration and data management. Budget limitations facing public healthcare system serving majority of population restrict capital available for IT infrastructure investments, software licensing, ongoing maintenance, and system upgrades despite government digital health priorities. Competing clinical priorities including staffing shortages, medical equipment needs, and facility maintenance consume available resources, relegating healthcare IT investments to lower priority despite recognized importance for operational efficiency and care quality improvement.

Competitive Landscape:

In the South African healthcare IT market, key players driving growth focus on digital transformation, data integration, and patient-centered care. Healthcare providers are increasingly adopting electronic health records, telemedicine, and digital patient management systems to streamline operations, improve clinical decision-making, and enhance service delivery. Insurers and wellness organizations are leveraging digital health platforms to optimize preventive care, monitor patient outcomes, and enable remote consultations. Technology vendors are introducing advanced solutions in clinical management, health data analytics, and cloud-based systems, supporting interoperability across public and private healthcare sectors. By collaborating with these market players and embracing innovative IT solutions, healthcare organizations can improve operational efficiency, enhance patient experiences, and strengthen data-driven decision-making. Strategic investment in digital infrastructure, cybersecurity, and workforce training further enables organizations to stay competitive, adapt to evolving healthcare demands, and position themselves for sustainable growth in a rapidly digitizing healthcare ecosystem.

South Africa Healthcare IT Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product and Services Covered |

|

| Components Covered | Software, Hardware, Services |

| Delivery Modes Covered | On-Premises, Cloud-Based |

| End Users Covered |

|

| Provinces Covered | Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South Africa Healthcare IT Market Report

The South Africa healthcare IT market size was valued at USD 2.76 Billion in 2025.

The South Africa healthcare IT market is expected to grow at a compound annual growth rate of 8.40% from 2026-2034 to reach USD 5.71 Billion by 2034.

Healthcare provider solutions dominated with 54% market share in 2025, driven by comprehensive clinical and nonclinical IT solution requirements supporting hospitals, clinics, and ambulatory care facilities as they digitize patient records, streamline workflows, and comply with National Health Insurance mandates for integrated information systems enabling claims processing, quality reporting, and population health management.

Key factors driving the South Africa Healthcare IT market include the National Health Insurance implementation signed into law in 2024 requiring integrated patient information systems, the National Digital Health Strategy establishing comprehensive frameworks and standards for digital health infrastructure, and rising smartphone penetration exceeding enabling mobile health applications delivering teleconsultation services and patient engagement tools directly to consumers.

Major challenges include escalating cybersecurity threats with healthcare organizations facing cyberattacks weekly and ransomware attack disrupting the National Health Laboratory Service, inadequate broadband infrastructure and connectivity gaps particularly in rural areas limiting cloud platform adoption, and workforce capacity constraints with critical healthcare professional shortages combined with insufficient technical expertise for complex health information system implementation and management.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)