South Africa Molybdenum Market Size, Share, Trends and Forecast by Product Type, Sales Channel, End Use, and Province, 2026-2034

South Africa Molybdenum Market Summary:

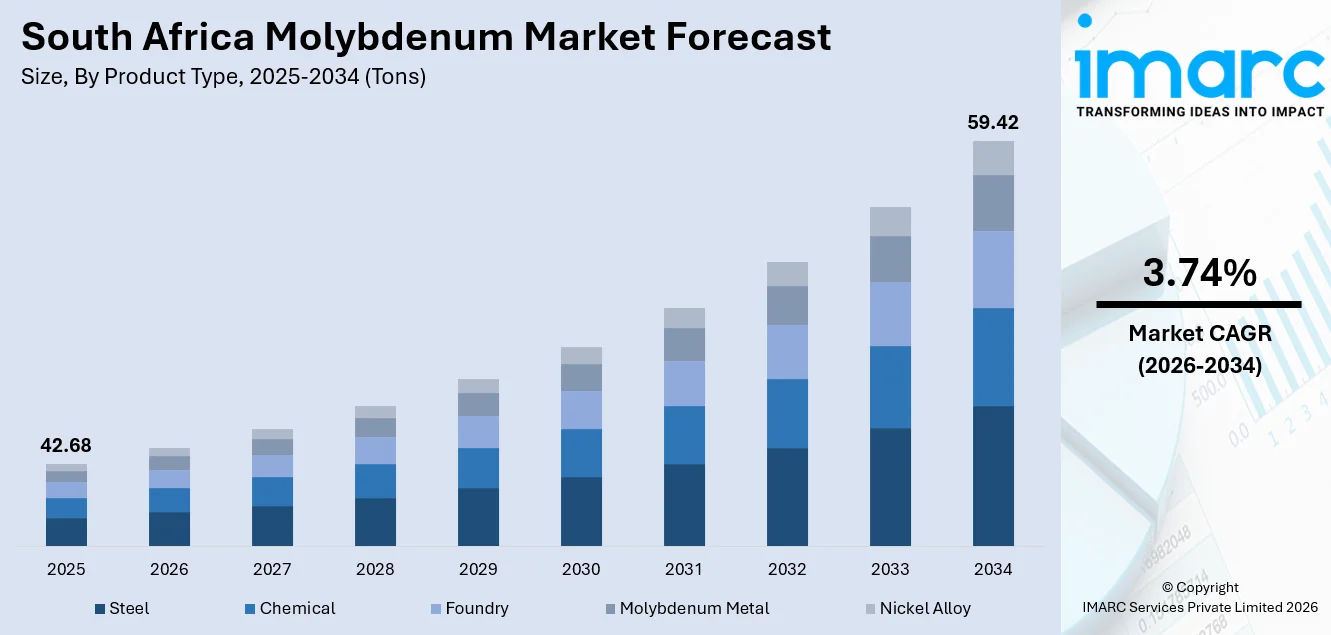

The South Africa molybdenum market size reached 42.68 Tons in 2025 and is projected to reach 59.42 Tons by 2034, growing at a compound annual growth rate of 3.74% from 2026-2034.

The market is fueled by the growing steel production industry, increasing oil and gas exploration, and developing infrastructure networks in the country. The rising use of molybdenum alloys in the automotive and heavy machinery industries also fuels the market. Moreover, the developing energy sector and advancements in aerospace and defense technology are creating sustained consumption opportunities, thereby adding to the overall development of the South Africa molybdenum market share.

Key Takeaways and Insights:

- By Product Type: Steel dominates the market with a share of 44% in 2025, driven by the widespread use of molybdenum as an alloying agent in stainless and structural steel production across South Africa.

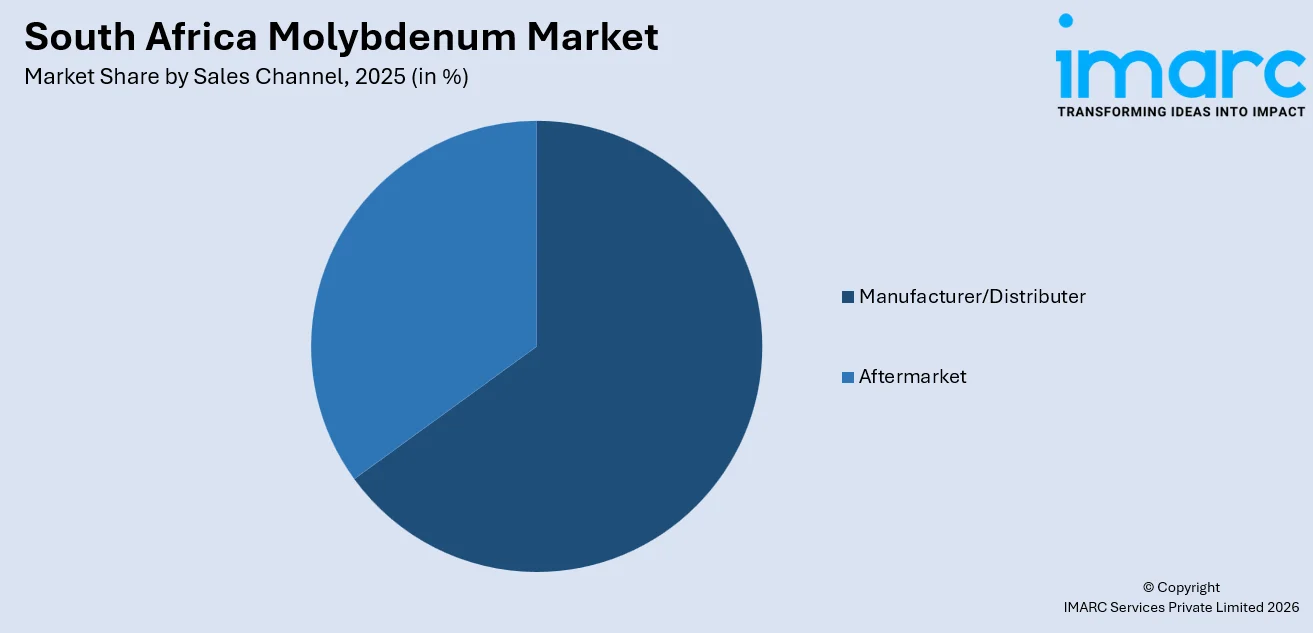

- By Sales Channel: Manufacturer/distributor leads the market with a share of 65% in 2025, owing to established procurement networks connecting molybdenum producers directly with steel mills and industrial manufacturers.

- By End Use: Oil and gas represent the largest segment with a market share of 24% in 2025, driven by the extensive use of molybdenum in corrosion-resistant pipeline steels and refinery catalysts.

- By Province: Gauteng leads the market with a share of 30% in 2025, owing to the concentration of steel manufacturing facilities, industrial hubs, and automotive production plants in the Johannesburg metropolitan area.

- Key Players: The South Africa molybdenum market exhibits a moderately consolidated competitive landscape, with established global mining and metals corporations competing alongside regional distributors and specialty alloy manufacturers across diverse product and application segments.

To get more information on this market Request Sample

The South Africa molybdenum market is experiencing steady growth, propelled by several interconnected demand drivers across the country's industrial landscape. The steel manufacturing sector remains the primary consumer of molybdenum, utilizing it as a critical alloying element to enhance the corrosion resistance, strength, and hardenability of various steel grades used in construction, automotive, and heavy machinery applications. According to reports, in May 2025, the South African government approved its Critical Minerals and Metals Strategy and the Mineral Resources Development Bill to strengthen regulatory certainty and attract investment into exploration and value-chain development for key minerals, supporting broader industrial metals demand including alloy inputs. Moreover, the oil and gas industry contributes significantly to molybdenum consumption through its demand for high-performance pipeline steels and catalytic applications in petroleum refining processes. Additionally, the chemical and petrochemical sectors are increasingly adopting molybdenum-based catalysts and corrosion-resistant alloys for processing operations.

South Africa Molybdenum Market Trends:

Growing Integration of Molybdenum in Renewable Energy Infrastructure

South Africa's accelerating transition toward renewable energy sources is creating new demand avenues for molybdenum-based materials. The construction of wind turbine components, solar panel mounting structures, and energy transmission infrastructure requires high-strength corrosion-resistant steel alloys where molybdenum serves as a vital alloying element. In 2025, JUWI announced plans to develop three large scale solar PV projects totaling 340 MW in South Africa, aimed at supplying clean power to energy intensive industries and strengthening renewable infrastructure. The country's commitment to diversifying its energy mix beyond coal dependency is driving investments in renewable energy projects that rely on specialized steel grades containing molybdenum for enhanced durability and performance in harsh environmental conditions.

Rising Demand for High-Performance Alloys in Automotive Manufacturing

The automotive sector in South Africa is increasingly adopting molybdenum-containing alloys for manufacturing lightweight yet durable vehicle components. As local and international automakers expand production capabilities, the demand for advanced steel grades incorporating molybdenum for improved strength-to-weight ratios and heat resistance continues to grow. In October 2025, South Africa’s automotive sector secured R 15.8 billion in confirmed capital expenditure from major OEMs, focused on modernising plants and upgrading production systems to support advanced vehicle and component manufacturing. This trend is particularly evident in the production of engine components, exhaust systems, and structural parts that require superior mechanical properties to meet evolving performance and emission standards in both domestic and export markets.

Expanding Applications in Chemical Processing and Catalytic Industries

The chemical and petrochemical sectors in South Africa are witnessing increased utilization of molybdenum-based catalysts and corrosion-resistant materials. Molybdenum oxide compounds are gaining prominence in hydrodesulfurization and hydrodenitrogenation processes essential for refining operations. In March 2025, Astron Energy, a unit of Glencore, announced a multi-billion-rand investment to upgrade its South African refinery with advanced hydrotreating processing units to meet Euro 5 cleaner fuel standards, enhancing catalyst and process technology deployment. The growing sophistication of the country's chemical manufacturing industry is driving demand for molybdenum-containing stainless steels and specialty alloys capable of withstanding aggressive chemical environments, high temperatures, and extreme pressure conditions encountered in modern processing facilities.

Market Outlook 2026-2034:

The South Africa molybdenum market is poised for sustained revenue growth during the forecast period, supported by expanding industrial activities and diversifying end-use applications. Revenue generation is expected to strengthen as the steel manufacturing sector modernizes production capabilities and infrastructure development projects progress across the country. The oil and gas industry's continued reliance on molybdenum-based catalysts and corrosion-resistant alloys will remain a significant revenue contributor. Additionally, emerging applications in renewable energy and advanced manufacturing are anticipated to create new revenue streams, driving overall market expansion. The market size was estimated at 42.68 Tons in 2025 and is expected to reach 59.42 Tons by 2034, reflecting a compound annual growth rate of 3.74% over the forecast period 2026-2034.

South Africa Molybdenum Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Steel |

44% |

|

Sales Channel |

Manufacturer/Distributor |

65% |

|

End Use |

Oil and Gas |

24% |

|

Province |

Gauteng |

30% |

Product Type Insights:

- Steel

- Chemical

- Foundry

- Molybdenum Metal

- Nickel Alloy

Steel dominates with a market share of 44% of the total South Africa molybdenum market in 2025.

Steel leads the market, reflecting the fundamental role of molybdenum as an essential alloying agent in steel production. Molybdenum enhances the hardenability, toughness, tensile strength, and corrosion resistance of various steel grades, making it indispensable for producing stainless steel, structural steel, tool steel, and high-speed steel. As per sources, the South African government and the Industrial Development Corporation provided R380 million in support to ArcelorMittal South Africa’s operations to safeguard domestic steel production capacity and preserve industrial output.

The dominance of the steel segment is reinforced by South Africa's established steel manufacturing infrastructure concentrated in key industrial provinces. Growing demand from downstream industries including construction, mining equipment manufacturing, and automotive production continues to drive consumption of molybdenum-alloyed steel products. The increasing preference for corrosion-resistant steel grades in coastal and industrial environments further sustains strong demand. Additionally, the modernization of existing steel mills and adoption of advanced metallurgical processes that require precise molybdenum additions support the continued leadership of this segment.

Sales Channel Insights:

Access the comprehensive market breakdown Request Sample

- Manufacturer/Distributer

- Aftermarket

Manufacturer/distributor leads with a share of 65% of the total South Africa molybdenum market in 2025.

The manufacturer/distributor dominates the South Africa molybdenum market, reflecting established supply chain networks that connect global molybdenum producers with domestic industrial consumers. In 2025, Metal Line Africa expanded its warehousing and logistics facilities in Durban and KwaZulu-Natal to support increased handling and distribution of bulk metals, reinforcing supply chain reliability for industrial and export markets. This channel encompasses direct procurement relationships between molybdenum suppliers and major steel manufacturers, industrial alloy producers, and large-scale engineering firms requiring consistent bulk supply of molybdenum products.

The segment is expected to maintain its leading position due to the existing steel production infrastructure in South Africa, mainly in the major industrial provinces. The rising demand from the downstream sectors of the construction, mining equipment, and automotive industries continues to fuel the consumption of molybdenum-alloyed steel products. The rising demand for corrosion-resistant steel products in the coastal and industrial regions also continues to fuel the demand. Moreover, the upgrading of existing steel production facilities and the adoption of advanced metallurgical technology, which requires accurate molybdenum addition, continues to fuel the leading position of this segment.

End Use Insights:

- Oil and Gas

- Automotive

- Heavy Machinery

- Energy

- Aerospace and Defense

- Others

Oil and gas exhibit a clear dominance with a 24% share of the total South Africa molybdenum market in 2025.

The oil and gas lead the South Africa molybdenum market by end use, driven by extensive application of molybdenum in petroleum refining catalysts and corrosion-resistant pipeline infrastructure. According to reports, Sapref restarted its 180,000-barrel-per-day Durban refinery after operational disruptions, reinforcing continued demand for hydrotreating catalysts and molybdenum-alloyed refinery equipment used in desulfurization and processing units. Molybdenum-based catalysts are essential for hydrodesulfurization processes that remove sulfur compounds from crude oil, while molybdenum-alloyed steels provide the durability and chemical resistance required for pipelines, storage vessels, and processing equipment.

South Africa's petroleum refining operations and gas processing facilities rely heavily on molybdenum-containing materials to maintain operational efficiency and safety standards. The country's strategic position as a refining hub for the southern African region and its ongoing investments in gas infrastructure development continue to sustain strong demand for molybdenum. The growing emphasis on fuel quality standards and environmental compliance in refining operations further drives adoption of advanced molybdenum-based catalytic systems and specialty alloys across this leading end-use segment.

Provincial Insights:

- Gauteng

- KwaZulu-Natal

- Western Cape

- Mpumalanga

- Eastern Cape

- Others

Gauteng dominates with a market share of 30% of the total South Africa molybdenum market in 2025.

Gauteng province dominates the South Africa molybdenum market, reflecting its position as the country's primary industrial and manufacturing heartland. The province hosts the largest concentration of steel manufacturing facilities, automotive production plants, and heavy engineering operations in South Africa. The Johannesburg metropolitan area and surrounding industrial corridors serve as major consumption centers for molybdenum-alloyed products. The well-established industrial ecosystem in Gauteng creates a concentrated demand base that drives significant molybdenum consumption across multiple downstream applications and manufacturing activities.

The economic significance of Gauteng extends beyond steel manufacturing to encompass diverse industrial activities including chemical processing, machinery manufacturing, and construction that all contribute to molybdenum demand. The province's well-developed transport infrastructure, proximity to raw material sources, and concentration of skilled labor make it the natural hub for molybdenum consumption and distribution. Additionally, the presence of major industrial procurement centers and distribution networks within Gauteng facilitates efficient supply chain operations that reinforce the province's leading position in the broader market.

Market Dynamics:

Growth Drivers:

Why is the South Africa Molybdenum Market Growing?

Expanding Steel Manufacturing and Infrastructure Development

South Africa's steel manufacturing sector serves as the primary growth engine for the molybdenum market, with ongoing modernization efforts and capacity expansion driving increased consumption of molybdenum as an essential alloying element. In 2025, Transnet announced R127 bn in planned rail and port upgrades to modernise logistics infrastructure supporting steel, mining, and heavy industry supply chains in South Africa. Moreover, the government's National Development Plan emphasizes large-scale infrastructure construction including transportation networks, power generation facilities, and urban development projects that demand high-performance steel grades containing molybdenum.

Growing Oil and Gas Sector and Petrochemical Processing Activities

The expansion of South Africa's oil refining capabilities and petrochemical processing operations is driving increased demand for molybdenum-based catalysts and corrosion-resistant alloys. According to reports, PetroSA announced plans to resume production at its Mossel Bay GTL refinery following Cabinet-backed investment approvals aimed at refurbishing and upgrading critical refining infrastructure. Moreover, refinery operators require molybdenum oxide catalysts for critical hydrodesulfurization and hydrotreating processes that ensure compliance with fuel quality standards. Additionally, the petroleum industry's need for high-performance pipeline materials, storage tank components, and processing equipment fabricated from molybdenum-alloyed steels continues to grow as existing facilities undergo modernization and new processing capacity is developed to meet regional energy demands.

Advancing Automotive and Aerospace Manufacturing Capabilities

South Africa's automotive manufacturing sector, which serves both domestic and international markets, is increasingly adopting molybdenum-containing steel alloys and specialty materials for vehicle component production. In November 2025, Beijing Automotive Group (BAIC) South Africa announced it will begin local assembly of the B30 SUV at its Gqeberha plant, enhancing production capability and local component use. The demand for lightweight yet high-strength materials in engine components, transmission parts, exhaust systems, and structural elements drives consumption of molybdenum-alloyed products.

Market Restraints:

What Challenges the South Africa Molybdenum Market is Facing?

High Import Dependency and Price Volatility

South Africa's reliance on imported molybdenum exposes the market to international price fluctuations and supply chain disruptions. The country lacks significant domestic molybdenum mining operations, making it dependent on global supply dynamics influenced by production decisions in major producing countries. Currency exchange rate variations further compound pricing uncertainties, affecting procurement costs for local manufacturers and limiting predictable budgeting for industrial consumers.

Availability of Substitute Materials and Alternative Alloys

The availability of alternative alloying elements such as chromium, vanadium, and manganese that can partially replicate certain properties of molybdenum poses a competitive challenge. Some manufacturers explore cost-effective substitutes particularly during periods of elevated molybdenum prices, potentially limiting consumption growth. Research into alternative alloy compositions and advanced material technologies continues to expand the range of options available to end users.

Economic Uncertainties and Industrial Output Fluctuations

Macroeconomic challenges including fluctuating industrial output, energy supply constraints, and periodic economic slowdowns impact molybdenum demand in South Africa. The steel manufacturing sector, as the primary consumer, is particularly sensitive to broader economic conditions affecting construction activity and manufacturing output. Infrastructure project delays and reduced industrial investment during economic downturns can temporarily suppress molybdenum consumption across multiple end-use segments.

Competitive Landscape:

The South Africa molybdenum market features a moderately consolidated competitive structure characterized by the presence of established global mining and metals corporations alongside regional distributors and specialty material suppliers. Market participants compete across multiple dimensions including product quality, pricing strategies, supply chain reliability, and technical support capabilities. The competitive dynamics are shaped by the dominance of international suppliers who control the upstream molybdenum production and processing, while domestic distributors and alloy manufacturers focus on downstream value addition and customer service.

South Africa Molybdenum Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Steel, Chemical, Foundry, Molybdenum Metal, Nickel Alloy |

| Sales Channels Covered | Manufacturer/Distributer, Aftermarket |

| End Uses Covered | Oil and Gas, Automotive, Heavy Machinery, Energy, Aerospace and Defense, Others |

| Province Covered | Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South Africa Molybdenum Market Report

The South Africa molybdenum market reached a volume of 42.68 Tons in 2025.

The South Africa molybdenum market is expected to grow at a compound annual growth rate of 3.74% from 2026-2034 to reach 59.42 Tons by 2034.

Steel held the largest South Africa molybdenum market share, driven by the extensive use of molybdenum as an alloying agent in stainless steel, structural steel, and tool steel production across construction, automotive, and industrial manufacturing sectors throughout the country.

Key factors driving the South Africa molybdenum market include expanding steel manufacturing activities, growing oil and gas refining operations, rising infrastructure development, increasing automotive production, and the advancing adoption of molybdenum-based alloys in energy and aerospace applications.

Major challenges include high import dependency on international suppliers, molybdenum price volatility driven by global supply dynamics, availability of substitute alloying elements, economic uncertainties affecting industrial output, energy supply constraints, and currency fluctuations impacting procurement costs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)