South Africa Orphan Drugs Market Size, Share, Trends and Forecast by Drug Type, Disease Type, Phase, Top Selling Drugs, Distribution Channel, and Region, 2026-2034

South Africa Orphan Drugs Market Overview:

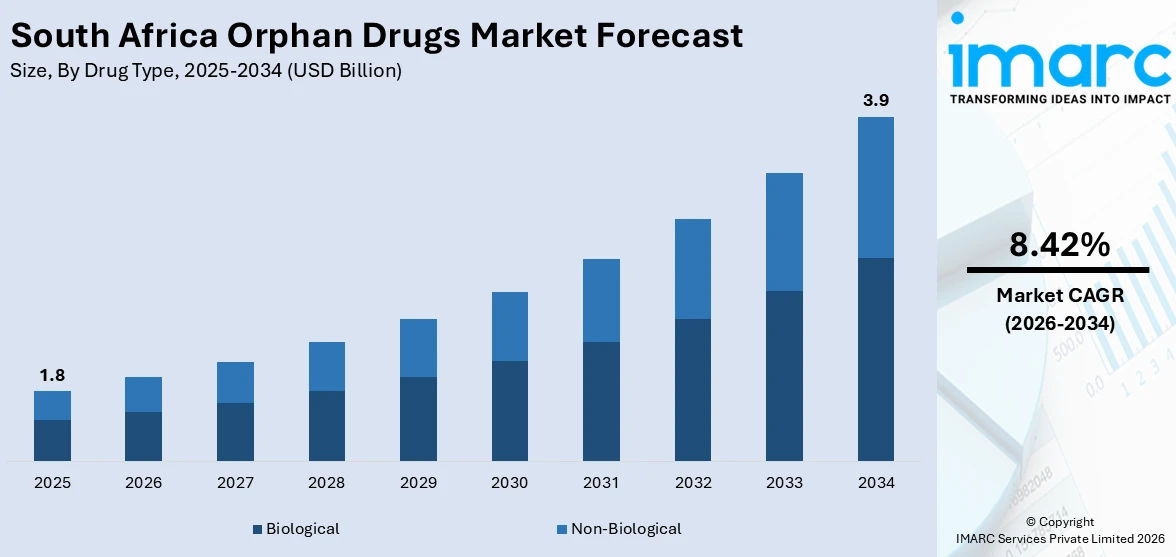

The South Africa orphan drugs market size reached USD 1.8 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 3.9 Billion by 2034, exhibiting a growth rate (CAGR) of 8.42% during 2026-2034. The market is driven by rising prevalence of rare diseases, increasing awareness and improved diagnosis, and growing government and NGO support for patient access to specialized therapies. Expanding healthcare infrastructure, coupled with collaborations between global pharmaceutical companies and local stakeholders, further supports South Africa orphan drugs share. Favorable regulatory pathways and incentives for orphan drug development, along with heightened investment in research and clinical trials, also contribute to meeting unmet medical needs and driving demand in the region.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2034 | USD 3.9 Billion |

| Market Growth Rate 2026-2034 | 8.42% |

South Africa Orphan Drugs Market Trends:

Rising Prevalence and Diagnosis of Rare Diseases

The growing prevalence of rare genetic and metabolic disorders in South Africa is a major driver in the South Africa orphan drugs trends. Historically, many rare diseases remained undiagnosed due to limited awareness, insufficient diagnostic infrastructure, and a shortage of specialist care. As, advances in genetic testing capable of detecting about 80% of rare diseases—alongside improved diagnostic tools and greater healthcare provider awareness, have significantly increased accurate identification of these conditions. Early and precise diagnosis has driven demand for specialized treatments, including orphan drugs. Patient advocacy groups and NGOs further support this trend by educating communities, reducing stigma, and promoting timely medical attention. As more patients are identified and registered, the market for orphan drugs in South Africa expands, creating substantial opportunities for pharmaceutical companies and healthcare providers to address unmet medical needs while improving patient outcomes.

To get more information on this market Request Sample

Government and NGO Support for Access to Therapies

Approximately 4.2 million South Africans about 1 in 15 people live with one of nearly 7,000 rare diseases, highlighting the urgent need for effective treatments. This significant disease burden has prompted growing support from government health agencies and non-governmental organizations (NGOs), which are driving adoption of orphan drugs. Authorities are working to establish frameworks that improve access to high-cost, specialized therapies, though policies remain less developed than in Europe or the U.S. At the same time, NGOs, patient advocacy groups, and international partnerships are filling critical gaps by funding treatments, lobbying for supportive legislation, and offering financial and emotional assistance. These collaborative efforts ensure more patients benefit from life-saving orphan drugs despite systemic challenges. By bridging funding gaps and creating stronger healthcare pathways, this ecosystem directly enhances patient access and fuels South Africa orphan drugs market growth.

Growing Pharmaceutical Collaborations and Research Investments

Collaborations between global pharmaceutical companies, local distributors, and research institutions are accelerating the growth of the orphan drugs market in South Africa. International drug developers are increasingly partnering with South African stakeholders to expand their reach and address unmet medical needs. These collaborations often involve licensing agreements, clinical trials, and local manufacturing partnerships that reduce costs and improve accessibility. At the same time, rising investment in research and development is fostering the exploration of rare disease treatments tailored to the African context. Universities and medical research institutions are contributing through studies on local disease prevalence and treatment outcomes. Additionally, regulatory bodies in South Africa are working to streamline approval processes for critical therapies, which enhances the attractiveness of the market for global players. Such collaborations and investments ensure that orphan drugs become more available, affordable, and widely distributed across the healthcare system.

South Africa Orphan Drugs Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the region level for 2026-2034. Our report has categorized the market based on drug type, disease type, phase, top selling drugs, and distribution channel.

Drug Type Insights:

- Biological

- Non-Biological

The report has provided a detailed breakup and analysis of the market based on the drug type. This includes biological, and non-biological.

Disease Type Insights:

- Oncology

- Hematology

- Neurology

- Cardiovascular

- Others

A detailed breakup and analysis of the market based on the disease type have also been provided in the report. This includes oncology, hematology, neurology, cardiovascular, and others.

Phase Insights:

- Phase I

- Phase II

- Phase III

- Phase IV

The report has provided a detailed breakup and analysis of the market based on the phase. This includes phase I, phase II, phase III, and phase IV.

Top Selling Drugs Insights:

- Revlimid

- Rituxan

- Copaxone

- Opdivo

- Keytruda

- Imbruvica

- Avonex

- Sensipar

- Soliris

- Others

A detailed breakup and analysis of the market based on the top selling drugs have also been provided in the report. This includes revlimid, rituxan, copaxone, opdivo, keytruda, imbruvica, avonex, sensipar, soliris, and others.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

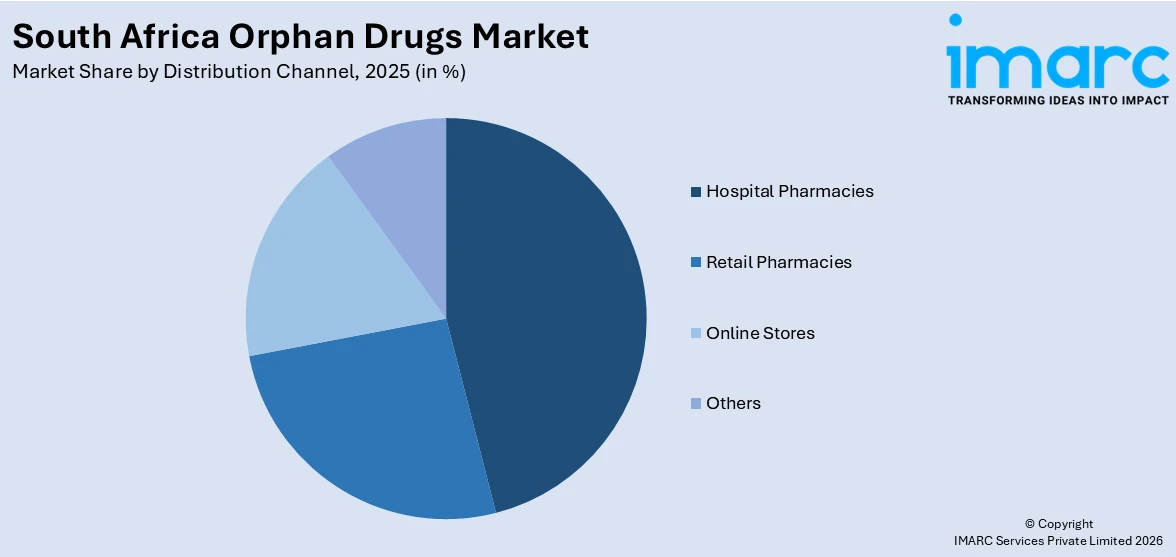

- Hospital Pharmacies

- Retail Pharmacies

- Online Stores

- Others

The report has provided a detailed breakup and analysis of the market based on the distribution channel. This includes hospital pharmacies, retail pharmacies, online stores, and others.

Regional Insights:

- Gauteng

- KwaZulu-Natal

- Western Cape

- Mpumalanga

- Eastern Cape

- Others

The report has also provided a comprehensive analysis of all the major regional markets, which include Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, and others.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

South Africa Orphan Drugs Market News:

- In February 2025, Arbor Biotechnologies announced FDA orphan drug and rare pediatric disease designations for ABO-101, a gene-editing therapy targeting primary hyperoxaluria type 1 (PH1). Following IND clearance in December 2024, a Phase 1/2 trial (redePHine) is set to begin in H1 2025 to assess safety, tolerability, and efficacy in adults and children. Arbor will also present supporting preclinical data and study design at the 20th International Pediatric Nephrology Association Congress in Cape Town.

South Africa Orphan Drugs Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drug Types Covered | Biological, Non-Biological |

| Disease Types Covered | Oncology, Hematology, Neurology, Cardiovascular, Others |

| Phases Covered | Phase I, Phase II, Phase III, Phase IV |

| Top Selling Drugs Covered | Revlimid, Rituxan, Copaxone, Opdivo, Keytruda, Imbruvica, Avonex, Sensipar, Soliris, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Stores, Others |

| Regions Covered | Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the South Africa orphan drugs market performed so far and how will it perform in the coming years?

- What is the breakup of the South Africa orphan drugs market on the basis of drug type?

- What is the breakup of the South Africa orphan drugs market on the basis of disease type?

- What is the breakup of the South Africa orphan drugs market on the basis of phase?

- What is the breakup of the South Africa orphan drugs market on the basis of top selling drugs?

- What is the breakup of the South Africa orphan drugs market on the basis of distribution channel?

- What is the breakup of the South Africa orphan drugs market on the basis of region?

- What are the various stages in the value chain of the South Africa orphan drugs market?

- What are the key driving factors and challenges in the South Africa orphan drugs market?

- What is the structure of the South Africa orphan drugs market and who are the key players?

- What is the degree of competition in the South Africa orphan drugs market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the South Africa orphan drugs market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the South Africa orphan drugs market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the South Africa orphan drugs industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)