South Africa Retail Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Province, 2026-2034

South Africa Retail Market Summary:

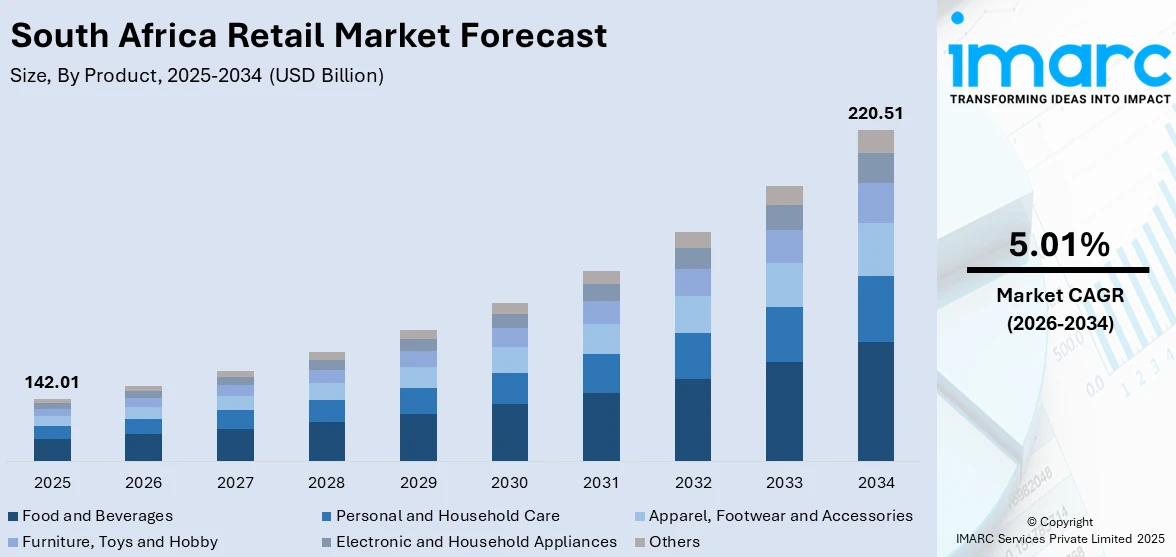

The South Africa retail market size was valued at USD 142.01 Billion in 2025 and is projected to reach USD 220.51 Billion by 2034, growing at a compound annual growth rate of 5.01% from 2026-2034.

Major retailers' strategic investments, changing consumer preferences, and growing digital infrastructure are all contributing to the revolutionary expansion of the South African retail business. The advent of omnichannel retailing tactics and quick-commerce platforms has completely changed how customers shop. The nation's shopping habits are changing due to rising urbanization, expanding middle-class ambitions, and rising smartphone adoption. The resurgence of consumer spending is being aided by government economic relief initiatives, lowering inflation, and falling interest rates. These factors, along with the aggressive growth of well-known retail chains and the arrival of international e-commerce behemoths, are establishing South Africa as a vibrant retail center and boosting the country's overall retail market share.

Key Takeaways and Insights:

- By Product: Food and beverages dominate the market with a share of 32% in 2025, demonstrating how South African consumers prioritize making necessary supermarket purchases in the face of financial strain. Quick-commerce grocery delivery services, growing retail networks, and rising demand for reasonably priced nutrition are all improving segment performance.

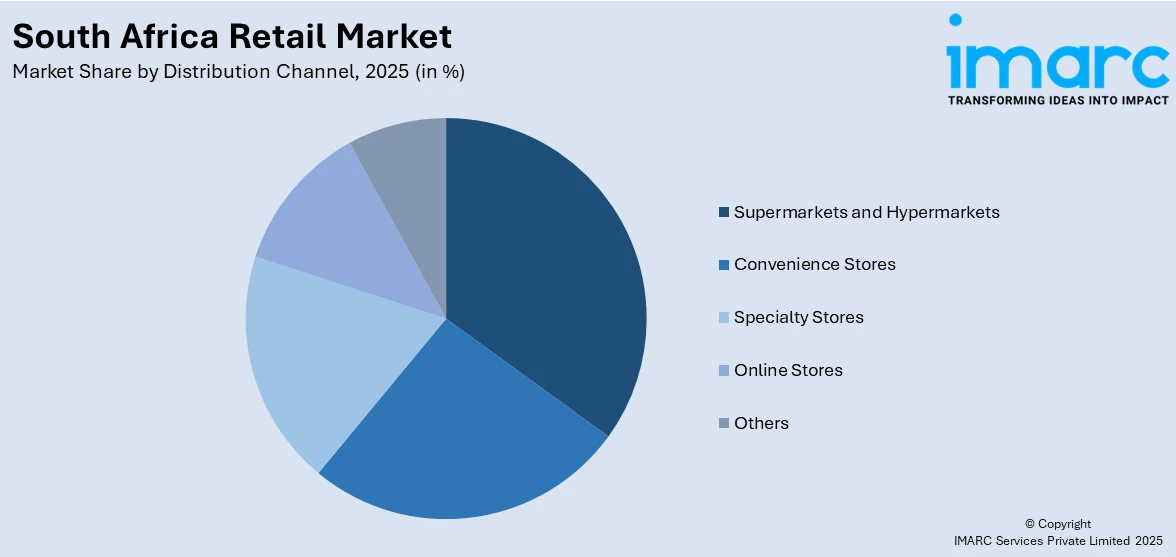

- By Distribution Channel: Supermarkets and hypermarkets lead the market with a share of 45% in 2025. This dominance is driven by consumer preference for one-stop shopping destinations offering competitive pricing, extensive product variety, and integrated services including financial solutions and loyalty programs.

- By Province: Gauteng is the largest region with 36% share in 2025, driven by the concentration of South Africa's economic activity in Johannesburg and Pretoria metropolitan areas, higher disposable incomes, and extensive retail infrastructure development.

- Key Players: Key players drive the South Africa retail market by expanding store networks, enhancing digital capabilities, and developing innovative loyalty programs. Their investments in omnichannel integration, quick-commerce platforms, and value-oriented private label offerings boost customer engagement and market penetration.

To get more information on this market Request Sample

The South Africa retail market is advancing as economic conditions stabilize and consumer confidence gradually recovers. The sector has demonstrated remarkable resilience, with retailers adapting to changing consumer behaviors through digital transformation and omnichannel strategies. Grocery shopping habits have been drastically changed by the speedy adoption of quick-commerce platforms; businesses like Checkers Sixty60 saw a 47% increase in sales in the first half of 2025, bringing in around R19 billion. Traditional brick-and-mortar retailers are successfully integrating online capabilities while expanding their physical footprints to capture diverse consumer segments. The market is witnessing intensified competition as global players enter the South African landscape, driving innovation and enhancing consumer value propositions. Private label products have emerged as a significant growth driver, with consumers increasingly seeking quality alternatives at competitive price points. Government economic relief measures, including the two-pot retirement system that facilitated substantial withdrawals, have provided temporary support to consumer spending, contributing to stronger retail performance during the festive shopping season.

South Africa Retail Market Trends:

Rapid E-Commerce and Digital Commerce Expansion

As e-commerce adoption surpasses pre-pandemic levels, South Africa's retail landscape is going through a major digital shift. Online retailers are gaining market share by providing quick delivery, affordable prices, and convenience. Accessibility for previously underserved consumer segments is being improved through the integration of buy-now-pay-later choices and mobile payment solutions. With platforms like Checkers Sixty60 emerging as the top supermarket delivery services in South Africa, quick-commerce grocery services have become dominant forces. Since their launch, these services have grown significantly and created a large number of new job opportunities, indicating the growth of the South African retail market.

Rise of Private Label Products and Value Retailing

Private label and store brand products are becoming more popular among budget-conscious consumers because they provide quality that is on par with major brands at lower price points. In an effort to increase profit margins and foster client loyalty, retailers are diversifying their private label offerings. As people look to optimize their purchasing power in the face of economic difficulties, the bargain retail sector is expanding rapidly. Private label brands performed exceptionally well, showing broad consumer appeal across a variety of product categories, experiencing strong sales value growth, and significantly outperforming total market growth.

Omnichannel Integration and Experiential Retail Innovation

Retailers are creating unified shopping experiences that satisfy changing customer expectations by skillfully fusing digital and physical channels. Major retail chains are starting to provide click-and-collect services, integrated loyalty programs, and tailored marketing as standard features. Investing in technology integration and retail renovations is improving consumer engagement and increasing sales. The commercial significance of integrated retail strategies and customer-centric approaches is demonstrated by industry study, which shows that merchants engaging in experience shopping and full omnichannel innovation are earning significant sales increases.

Market Outlook 2026-2034:

The South Africa retail market outlook remains cautiously optimistic as macroeconomic conditions gradually improve and consumer sentiment strengthens. Moderating inflation, declining interest rates, and the absence of load-shedding are creating a more favorable operating environment for retailers. The market generated a revenue of USD 142.01 Billion in 2025 and is projected to reach a revenue of USD 220.51 Billion by 2034, growing at a compound annual growth rate of 5.01% from 2026-2034. Digital commerce will continue driving structural changes in the retail landscape, with online sales projected to account for an increasing share of total retail turnover. Competition will intensify as global retail giants establish stronger footholds while domestic players strengthen their value propositions. Investment in supply chain infrastructure, technology platforms, and sustainable practices will differentiate market leaders from competitors in an increasingly demanding consumer environment.

South Africa Retail Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Product | Food and Beverages | 32% |

| Distribution Channel | Supermarkets and Hypermarkets | 45% |

| Province | Gauteng | 36% |

Product Insights:

- Food and Beverages

- Personal and Household Care

- Apparel, Footwear and Accessories

- Furniture, Toys and Hobby

- Electronic and Household Appliances

- Others

Food and beverages dominate with a market share of 32% of the total South Africa retail market in 2025.

The food and beverages segment maintains its leadership position in the South Africa retail market,. This dominance reflects the essential nature of grocery purchases and the prioritization of food spending by South African households across all income levels. The segment benefits from extensive supermarket and hypermarket networks that provide convenient access to diverse product ranges at competitive prices. Modern trade channels continue expanding their fresh food offerings, bakery departments, and ready-to-eat meal solutions to capture evolving consumer preferences. South African consumers spent nearly R637 Billion on fast-moving consumer goods through traditional and modern trade channels during 2024, with food and liquor representing the largest category at R359 Billion.

The segment's growth is further supported by the rapid expansion of quick-commerce grocery delivery services that have transformed how urban consumers purchase food products. Retailers are investing heavily in cold chain infrastructure, fresh produce sourcing networks, and in-store food preparation facilities to differentiate their offerings. Private label food products are gaining substantial market share as price-conscious consumers seek quality alternatives to branded items. The integration of loyalty programs with grocery purchases is driving customer retention and increasing purchase frequency.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Stores

- Others

Supermarkets and hypermarkets lead with a share of 45% of the total South Africa retail market in 2025.

Supermarkets and hypermarkets command the largest share of South Africa's retail distribution landscape, driven by their ability to offer comprehensive product assortments under single roofs. These formats provide consumers with competitive pricing through bulk purchasing power, extensive fresh food departments, and integrated services including financial products, pharmacy services, and loyalty programs. The channel benefits from established consumer shopping habits and the convenience of one-stop shopping destinations. South Africa currently has approximately 2,000 shopping centers with expansion plans in the pipeline, reflecting continued investment confidence in modern retail infrastructure. Major chains continue expanding their footprints while simultaneously investing in store refurbishments and format innovations.

The supermarket and hypermarket segment is witnessing significant competitive dynamics as market leaders aggressively expand while others undertake restructuring initiatives. Leading retail groups have demonstrated exceptional growth momentum, opening numerous new stores across their South African segments. The rise of hybrid wholesale-retail formats is capturing value-conscious shoppers who previously relied solely on traditional supermarkets. Investment in omnichannel capabilities is enabling supermarkets to compete effectively with pure-play e-commerce platforms while leveraging their extensive physical store networks for fulfillment. The discount supermarket segment is experiencing particularly strong growth, with major retailers planning substantial expansion of their value-oriented store formats in the coming years.

Provincial Insights:

- Gauteng

- KwaZulu-Natal

- Western Cape

- Mpumalanga

- Eastern Cape

- Others

Gauteng exhibits a clear dominance with 36% share of the total South Africa retail market in 2025.

Gauteng province leads the South Africa retail market, reflecting its position as the country's economic heartland and most densely populated region. The province encompasses major metropolitan areas including Johannesburg and Pretoria, which together account for the highest concentration of consumer spending power in South Africa. Gauteng benefits from sophisticated retail infrastructure, extensive shopping mall networks, and high levels of urbanization that support diverse retail formats. The province attracts significant retail investment due to its large consumer base and relatively higher household incomes. Commercial property investment data confirms Gauteng's dominance, with the province accounting for the largest share of total deal volume while recording strong year-on-year trading density growth across its shopping centers.

The competitive landscape in Gauteng is particularly intense, with major retailers vying for prime locations in affluent suburbs and growing township markets. Premium retail destinations such as Sandton City continue attracting luxury brands and high-end consumers, while value-oriented retailers expand their presence in emerging markets. Shoprite recently marked a significant milestone with the opening of its 150th supermarket in Gauteng at the Carlton Centre in Johannesburg, creating 41 new jobs and demonstrating continued commitment to the province's central business district. The province is witnessing dynamic shifts in retail formats, with smaller community-focused centres outperforming larger regional malls in certain metrics, reflecting changing consumer preferences for convenience-oriented shopping. E-commerce adoption rates in Gauteng remain among the highest nationally, driving retailers to strengthen their digital capabilities and last-mile delivery networks.

Market Dynamics:

Growth Drivers:

Why is the South Africa Retail Market Growing?

Government Economic Relief Measures and Policy Support

Government initiatives and economic relief programs are providing meaningful support to consumer spending capacity in South Africa. The introduction of targeted policy interventions is helping households navigate economic pressures while maintaining retail expenditure levels. Regulatory reforms in customs and taxation are creating a more level playing field for domestic retailers competing with international e-commerce platforms. The government's focus on economic stabilization and infrastructure development is building long-term foundations for sustainable retail growth. The implementation of the two-pot retirement system allowed consumers to access a portion of their retirement funds, providing substantial liquidity injection into household budgets ahead of the festive shopping season. This unprecedented access to retirement savings supported stronger-than-expected retail performance during the critical fourth quarter of the year.

Easing Inflationary Pressures and Declining Interest Rates

The moderation of inflation rates is progressively restoring consumer purchasing power that had been significantly eroded during previous high-inflation periods. Declining interest rates are reducing household debt servicing costs and freeing up disposable income for retail purchases. The stabilization of food prices is particularly important given the dominant share of food spending in South African household budgets. Improved economic conditions are gradually rebuilding consumer confidence and willingness to make discretionary purchases. Recent data indicates a significant decline in food inflation, marking the lowest food inflation level in many years. This marked improvement means that consumers can allocate more of their budgets to everyday items beyond basic necessities. The South African Reserve Bank has complemented this relief by implementing consecutive benchmark lending rate cuts, offering meaningful relief from previously elevated borrowing costs.

Aggressive Store Expansion and Retail Infrastructure Investment

Major retailers are demonstrating strong confidence in the South African market through substantial investment in new store openings and existing store upgrades. The expansion of modern retail formats into previously underserved areas is bringing convenient shopping options to broader consumer segments. Investment in supply chain infrastructure, distribution centers, and technology platforms is enhancing operational efficiency and customer service capabilities. Competition among retailers is driving innovation in store formats, product offerings, and customer engagement strategies. South Africa's FMCG corporate retailers have significantly expanded their continental presence, consistently opening new stores over recent years and achieving substantial growth in store footprint. Planned capital expenditures for the coming financial year will focus on store expansions, maintenance, IT infrastructure, and strategic growth initiatives, reflecting the industry's sustained commitment to market development and service enhancement.

Market Restraints:

What Challenges the South Africa Retail Market is Facing?

Persistent Economic Pressures and High Unemployment

South Africa's elevated unemployment rate continues to constrain aggregate consumer spending capacity. Households face ongoing financial stress from accumulated debt burdens, rising living costs, and limited income growth opportunities. The economic divide between higher and lower income segments is widening, creating uneven retail demand patterns across product categories. Lower-income households have demonstrated the most significant reduction in retail purchases, with notable volume declines as families prioritize essential spending over discretionary items.

Infrastructure Challenges and Operational Cost Pressures

Although load-shedding has subsided, retailers continue bearing costs from previous investments in backup power generation and energy security measures. Transportation infrastructure limitations and logistics inefficiencies add complexity and cost to retail supply chains. Water supply concerns in certain regions pose additional operational risks for retailers dependent on reliable utility services. Rising security costs to protect stores, distribution centers, and employees from criminal activity are eroding profit margins and constraining investment capacity for some retail operators.

Intensified Competition from Global E-Commerce Platforms

The entry of international e-commerce giants including Amazon, Shein, and Temu has intensified competitive pressures on domestic retailers. These platforms offer extensive product selections and aggressive pricing that local retailers struggle to match. Cross-border e-commerce has disrupted traditional retail models, particularly in fashion and general merchandise categories. While regulatory changes including increased customs duties and VAT enforcement are narrowing price advantages for international platforms, competition remains formidable as global players continue adapting strategies to the South African market.

Competitive Landscape:

The South Africa retail market is characterized by intense competition among established domestic players and emerging international entrants. Market leaders are differentiating through aggressive store expansion, omnichannel capabilities, and customer loyalty programs. The sector is witnessing consolidation as stronger players acquire underperforming competitors and occupy vacated retail locations. Competition extends beyond pricing to encompass product quality, shopping convenience, digital capabilities, and customer experience. Retailers are investing in technology platforms, supply chain optimization, and private label development to strengthen competitive positions. Strategic partnerships between retailers and financial services providers are creating new value propositions. The entry of global retail giants is accelerating innovation and raising service standards across the industry, ultimately benefiting South African consumers through enhanced choice, improved quality, and competitive pricing.

Recent Developments:

- In September 2025, Walmart announced plans to open its first Walmart-branded stores in South Africa by year-end, introducing a comprehensive product range including fresh groceries, household essentials, apparel, and technology products. The retail giant aims to partner with South African suppliers and entrepreneurs to offer locally sourced merchandise alongside global brands, bringing its signature everyday low prices and global retail standards to the market.

South Africa Retail Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Food and Beverages, Personal and Household Care, Apparel, Footwear and Accessories, Furniture, Toys and Hobby, Electronic and Household Appliances, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, Others |

| Provinces Covered | Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South Africa Retail Market Report

The South Africa retail market size was valued at USD 142.01 Billion in 2025.

The South Africa retail market is expected to grow at a compound annual growth rate of 5.01% from 2026-2034 to reach USD 220.51 Billion by 2034.

Food and beverages dominated the market with a share of 32%, reflecting essential consumer priorities and the extensive network of supermarkets serving daily grocery needs across all income segments in South Africa.

Key factors driving the South Africa retail market include easing inflation, declining interest rates, rapid e-commerce expansion, aggressive store network growth by major retailers, and government economic relief measures supporting consumer spending recovery.

Major challenges include persistent high unemployment rates exceeding 32%, infrastructure constraints, rising operational costs, intensified competition from global e-commerce platforms, and economic pressures limiting consumer spending capacity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade