South Africa Tin Market Size, Share, Trends and Forecast by Product Type, Application, End Use Industry, and Province, 2026-2034

South Africa Tin Market Summary:

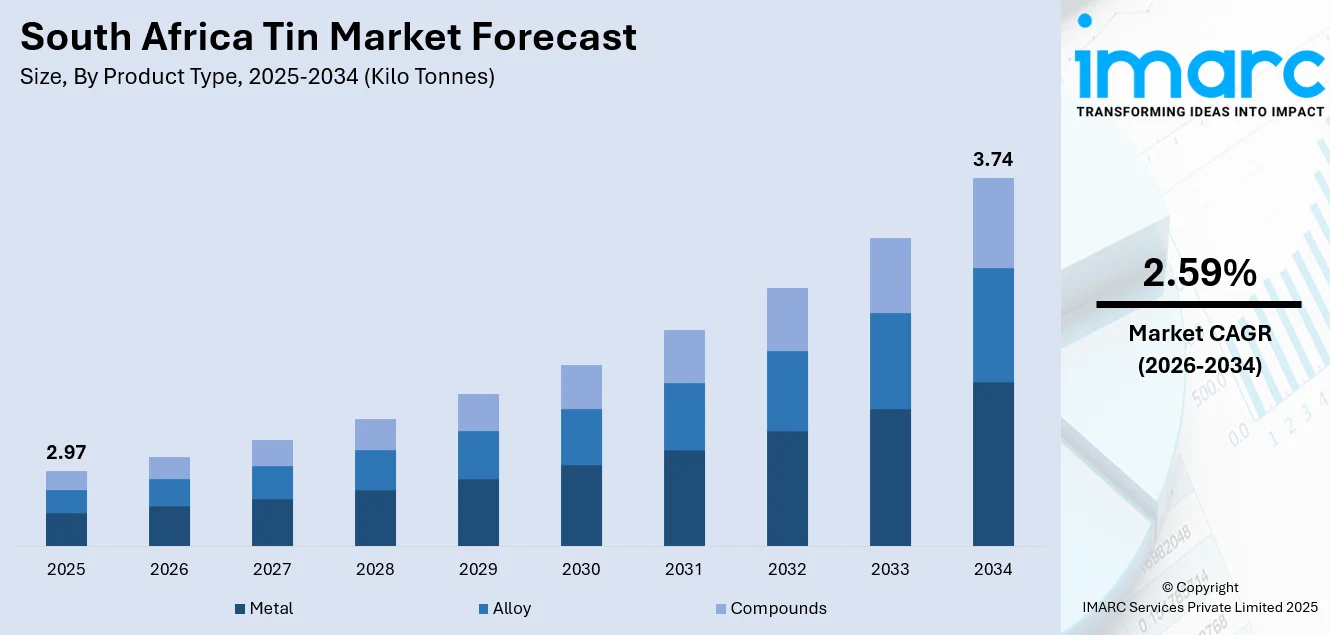

The South Africa tin market size reached 2.97 Kilo Tonnes in 2025 and is projected to reach 3.74 Kilo Tonnes by 2034, growing at a compound annual growth rate of 2.59% from 2026-2034.

The South Africa tin market is primarily driven by the expanding electronics manufacturing sector, which demands tin-based soldering materials for circuit boards and semiconductor assembly. Additionally, the growth of the automotive industry, supported by the South African Automotive Master Plan 2035, and the rising demand for corrosion-resistant packaging solutions in the food and beverage sector are creating sustained demand for tin products.

Key Takeaways and Insights:

- By Product Type: Metal dominates the market with a share of 60% in 2025, driven by its extensive use in soldering applications, alloy production, and electroplating processes across industrial sectors.

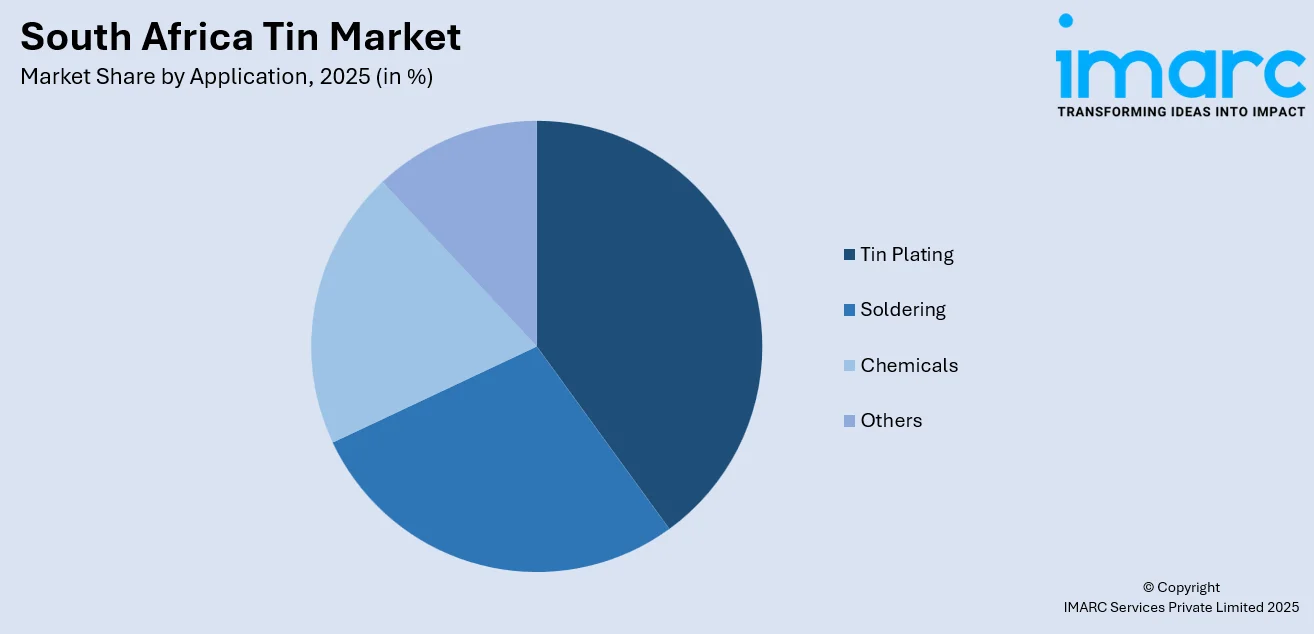

- By Application: Tin plating leads the market with a share of 28% in 2025, supported by growing demand for corrosion-resistant coatings in food packaging and industrial components.

- By End Use Industry: Electronics represents the largest segment with a market share of 35% in 2025, reflecting the sector's critical reliance on tin-based solder materials for electronic component assembly.

- By Province: Gauteng dominates with a market share of 30% in 2025, because it serves as South Africa’s leading manufacturing center, hosting nearly half of the country’s industrial capacity and supporting a wide range of production activities across multiple sectors.

- Key Players: The competitive landscape features a mix of international smelters, regional distributors, and specialized tin product manufacturers. These players serve diverse end-use industries through established distribution networks, competing on supply reliability, product quality, and technical support capabilities.

To get more information on this market Request Sample

The South Africa tin market encompasses the production, importation, processing, and distribution of tin metal, alloys, and compounds across diverse industrial applications. The market serves critical sectors including electronics manufacturing, automotive production, food and beverage packaging, glass production, and construction. In May 2025, the South African government approved its Critical Minerals and Metals Strategy and the draft Mineral Resources Development Bill, aiming to strengthen policy and regulatory certainty and maximise the country’s role in global minerals value chains, which could influence future downstream processing of metals including tin and related industrial inputs. South Africa relies predominantly on tin imports to meet domestic demand, with the country representing the largest importer and consumer of tin on the African continent, accounting for the majority of regional consumption.

South Africa Tin Market Trends:

Growing Adoption of Lead-Free Soldering in Electronics Manufacturing

The transition toward lead-free solder alloys is reshaping tin consumption patterns across South Africa's electronics sector. Regulatory alignment with international standards, including the EU's Restriction of Hazardous Substances (RoHS) Directive, is accelerating the adoption of tin-silver-copper (SAC) alloys in local manufacturing facilities. For example, South African manufacturers are increasingly producing and sourcing RoHS‑compliant SAC and lead‑free solder materials to meet environmental and export requirements, reflecting a broader industrial shift toward eco‑friendly electronics production. The expanding consumer electronics market and growing smartphone penetration are driving sustained demand for high-purity tin soldering materials essential for circuit board assembly and electronic component manufacturing.

Rising Integration of Tin in Electric Vehicle and Renewable Energy Applications

The automotive sector's evolution toward electrification is creating new demand channels for tin-based materials. Advanced driver-assistance systems (ADAS), infotainment units, and battery management systems have significantly increased tin usage per vehicle. In January 2026, the South African government introduced a 150% tax incentive for manufacturers investing in new production facilities and equipment for electric and hydrogen‑powered vehicles, a policy designed to accelerate local new energy vehicle (NEV) production and attract investment into EV and battery ecosystems. Government incentives supporting new energy vehicle manufacturing investments signal accelerating demand for tin in battery components, power electronics, charging infrastructure, and solar photovoltaic applications, positioning the country for sustained growth in green technology sectors.

Emphasis on Sustainable and Recycled Tin Supply Chains

Environmental sustainability is emerging as a critical market driver, with manufacturers increasingly prioritizing responsibly sourced and recycled tin materials. For example, producer responsibility organisations like MetPac‑SA have recently been scaling up metal recycling and circularity efforts across South Africa, promoting collection infrastructure and traceability systems to ensure higher volumes of recycled metal feedstock re‑enter the industrial supply chain. This shift is encouraging local processors to develop tin recycling capabilities, obtain sustainability certifications, and implement traceability systems to meet evolving customer requirements and demonstrate environmental responsibility throughout the value chain.

Market Outlook 2026-2034:

The South Africa tin market is poised for steady expansion over the forecast period, supported by industrialization initiatives, infrastructure development, and growing consumer electronics penetration. The automotive sector's transition toward electric vehicles and the packaging industry's demand for food-safe coatings will sustain tin consumption growth. Additionally, government investment programs targeting manufacturing sector expansion and special economic zone development are expected to attract tin-consuming industries to the country. The market size was estimated at 2.97 Kilo Tonnes in 2025 and is expected to reach 3.74 Kilo Tonnes by 2034, reflecting a compound annual growth rate of 2.59% over the forecast period 2026-2034.

South Africa Tin Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Metal |

60% |

|

Application |

Tin Plating |

28% |

|

End Use Industry |

Electronics |

35% |

|

Province |

Gauteng |

30% |

Product Type Insights:

- Metal

- Alloy

- Compounds

The metal dominates with a market share of 60% of the total South Africa tin market in 2025.

Tin metal represents the foundational product form consumed across South Africa's industrial landscape, serving as the primary input for soldering, plating, and alloy production applications. The metal segment's dominance reflects the country's robust electronics manufacturing base, which requires high-purity tin for circuit board assembly and component soldering. Major semiconductor manufacturers and electronics assemblers operating in special economic zones drive consistent demand for refined tin metal supplies.

The metal segment benefits from South Africa's import-dependent supply structure, with refined tin sourced primarily from Southeast Asian smelters to meet domestic quality specifications. Industrial consumers prioritize metal purity levels and supply reliability, creating opportunities for established international suppliers with certified production facilities. The segment's growth trajectory aligns with expanding electronics production and increasing adoption of tin-intensive technologies in automotive and renewable energy applications.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Soldering

- Tin Plating

- Chemicals

- Others

The tin plating leads with a share of 28% of the total South Africa tin market in 2025.

Tin plating applications serve critical functions across South Africa's packaging, automotive, and industrial manufacturing sectors by providing corrosion-resistant protective coatings. The segment's prominence reflects growing demand from the food and beverage industry, where tinplate packaging ensures product safety and extended shelf life. In 2025, the Metal Packaging Association of South Africa (MetPac‑SA) reported progress in meeting Extended Producer Responsibility (EPR) targets under new environmental regulations, strengthening recycling and recovery of tinplate and other metal packaging as part of national circular economy goals. Major domestic packaging manufacturers operate as key producers of tinplate cans, serving the canned food, beverage, and aerosol markets throughout the country.

The application segment benefits from increasing urbanization and changing consumer preferences toward convenient packaged foods, with a significant proportion of South Africans residing in urban areas and this share projected to expand further. Industrial tin plating services also support automotive component manufacturing, electrical equipment production, and construction materials, diversifying demand sources across economic cycles and ensuring stable consumption patterns regardless of fluctuations in individual end-use sectors.

End Use Industry Insights:

- Automotive

- Electronics

- Packaging (Food and Beverages)

- Glass

- Others

The electronics dominates with a market share of 35% of the total South Africa tin market in 2025.

The electronics industry represents the primary consumption channel for tin in South Africa, driven by manufacturing operations, consumer device assembly, and telecommunications infrastructure expansion. The semiconductor market continues to expand steadily, creating sustained demand for tin-based soldering materials essential for circuit board production. The electrotechnical sector maintains significant local value and employs a substantial workforce, reinforcing its position as a cornerstone of the national economy.

Electronics manufacturers operating in designated industrial zones benefit from government incentives promoting local content and technological capability development. The sector's growth is supported by expanding telecommunications infrastructure, including next-generation network deployment, and increasing penetration of consumer electronics across urban and rural markets. Government commitments to infrastructure development, including investments in electronics assembly facilities, are expected to further support tin consumption growth and strengthen domestic manufacturing capabilities in the coming years.

Provincial Insights:

- Gauteng

- KwaZulu-Natal

- Western Cape

- Mpumalanga

- Eastern Cape

- Others

Gauteng exhibits a clear dominance with a 30% share of the total South Africa tin market in 2025.

Gauteng's market leadership reflects its position as South Africa's primary manufacturing and industrial hub, accounting for the largest share of the nation's manufacturing capacity and GDP contribution. The province houses the highest concentration of electronics manufacturers, automotive component suppliers, and industrial consumers that drive tin demand. The majority of foreign direct investment projects in Gauteng flow to the manufacturing sector and its subsectors, reinforcing the region's industrial concentration.

The region benefits from established infrastructure, skilled workforce availability, and proximity to major transportation networks including the country's busiest international airport. The Automotive Supplier Park in Rosslyn hosts component manufacturers serving major original equipment manufacturers, creating consistent demand for tin-based soldering and plating materials. The Gauteng Growth and Development Agency's focus on attracting substantial investment over the coming years signals continued regional expansion and sustained tin consumption growth.

Market Dynamics:

Growth Drivers:

Why is the South Africa Tin Market Growing?

Expanding Electronics Manufacturing and Semiconductor Industry

The electronics sector's expansion represents a fundamental growth driver for South Africa's tin market, with the country positioned as a regional technology hub serving continental markets. The consumer electronics market continues to expand steadily, creating sustained demand for tin-based soldering materials essential for circuit board assembly and electronic component manufacturing. In March 2025, Microsoft announced a further R5.4 billion investment to expand its cloud and AI infrastructure in South Africa, building on previous data centre developments in Johannesburg and Cape Town and underscoring the country’s rising role in advanced tech deployments that rely on tin‑intensive electronic systems for servers and networking equipment. Major technology companies are investing in South African AI and cloud infrastructure, driving demand for tin-intensive data center equipment and electronic systems. The semiconductor industry's growth trajectory further reinforces tin consumption as manufacturers require high-purity soldering materials for advanced chip packaging and assembly operations.

Automotive Industry Development and Electrification Transition

South Africa's automotive sector contributes significantly to manufacturing output and GDP, creating substantial demand for tin through component manufacturing, soldering applications, and protective coatings. The South African automotive market reached USD 14.47 billion in 2024, highlighting the sector’s scale and strategic importance, with projections indicating continued expansion in the coming decade. The South African Automotive Master Plan targets significant production growth, representing substantial expansion from current output levels. Government incentives for new energy vehicle manufacturing investments accelerate the transition toward electric vehicles, which require increased tin usage in battery management systems, power electronics, and charging infrastructure. Growing interest from international automakers in establishing local assembly operations signals expanding automotive sector investment and sustained tin demand growth.

Growth in Food Packaging and Beverage Industry

The packaging industry's expansion, driven by urbanization and changing consumer preferences, supports sustained demand for tin plating applications. The South Africa packaging market continues to grow steadily, with the food and beverage sector representing the largest end-user of tinplate packaging. Demand is driven by the shift toward convenient, ready-to-eat products and extended shelf-life requirements. For example, South Africa’s Coleus Packaging invested approximately R40 million (about USD 2.11 million) in 2024 to install a new, high‑speed metal crown manufacturing line at its Alrode facility, boosting capacity for metal closures used in beverages and bottled products across the country and wider African markets. Major food manufacturers are expanding production facilities across the country, exemplifying the manufacturing growth driving tin packaging demand. The country's growing middle class and accelerating urbanization trends further support packaged food consumption growth and tinplate demand expansion.

Market Restraints:

What Challenges the South Africa Tin Market is Facing?

Import Dependency and Supply Chain Vulnerabilities

South Africa's heavy reliance on tin imports exposes the market to supply chain disruptions, currency fluctuations, and geopolitical risks affecting global tin trade flows. The country maintains limited domestic tin mining or smelting capacity, requiring procurement from Southeast Asian producers vulnerable to export restrictions and production disruptions. This dependency creates cost volatility and supply uncertainty for domestic manufacturers, limiting their ability to plan long-term operations effectively.

Price Volatility and Raw Material Cost Pressures

Global tin prices have experienced significant fluctuations, with prices reaching record levels before subsequent corrections. These price swings create challenges for downstream manufacturers in budgeting and maintaining competitive pricing strategies. The rand's volatility against major currencies amplifies import cost uncertainty, squeezing margins for tin processors and end-users. Manufacturers struggle to pass increased costs to customers, impacting profitability and investment capacity across the value chain.

Competition from Alternative Materials and Technologies

The tin market faces ongoing competition from substitute materials in key applications, including aluminum and plastic packaging alternatives, conductive adhesives in electronics, and alternative coating technologies. Environmental concerns regarding mining and sustainability considerations are driving some manufacturers to explore tin-free solutions, particularly in packaging applications where paper and biodegradable alternatives continue gaining market acceptance and consumer preference, potentially limiting long-term tin demand growth.

Competitive Landscape:

The South Africa tin market features a fragmented competitive structure comprising international metal suppliers, regional distributors, and specialized processing companies. Major global tin producers from Southeast Asia serve the South African market through established distribution channels and long-term supply agreements. Domestic industrial conglomerates incorporate tin materials into their manufacturing operations across packaging, steel production, and metal fabrication segments, while specialized metal trading companies facilitate import and distribution activities throughout the country. Competition centers on supply reliability, product quality certification, technical support capabilities, and competitive pricing strategies. Market participants differentiate themselves through value-added services including just-in-time delivery, customized alloy formulations, and technical consultation for end-use applications. The competitive landscape is further shaped by sustainability credentials, with buyers increasingly prioritizing suppliers demonstrating responsible sourcing practices.

Recent Developments:

- In November 2025, South Africa’s critical minerals strategy, which includes minerals like tin, has drawn industry scrutiny for offering weak investment incentives, with no tax holidays, royalty relief, or targeted financial measures to attract exploration and development, contributing to regulatory uncertainty and potentially dampening mining investment dynamics in 2025.

South Africa Tin Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Kilo Tonnes |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Metal, Alloy, Compounds |

| Applications Covered | Soldering, Tin Plating, Chemicals, Others |

| End Use Industries Covered | Automotive, Electronics, Packaging (Food and Beverages), Glass, Others |

| Province Covered | Gauteng, KwaZulu-Natal, Western Cape, Mpumalanga, Eastern Cape, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South Africa Tin Market Report

The South Africa tin market reached a volume of 2.97 Kilo Tonnes in 2025.

The South Africa tin market is expected to grow at a compound annual growth rate of 2.59% from 2026-2034 to reach 3.74 Kilo Tonnes by 2034.

The metal segment held the largest market share at 60%, driven by its extensive application in soldering, electroplating, and alloy production across electronics, automotive, and packaging industries.

Key factors driving the South Africa tin market include expanding electronics manufacturing and semiconductor industry growth, automotive sector development and electrification initiatives, and rising demand for corrosion-resistant packaging in the food and beverage sector.

Major challenges include import dependency exposing the market to supply chain vulnerabilities, tin price volatility affecting manufacturer margins, and competition from alternative materials in packaging and electronics applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)