South East Asia Automotive Piston Market Size, Share, Trends and Forecast by Material Type, Vehicle Type, Piston Coating Type, Piston Type, Distribution Channel, and Country, 2026-2034

South East Asia Automotive Piston Market Summary:

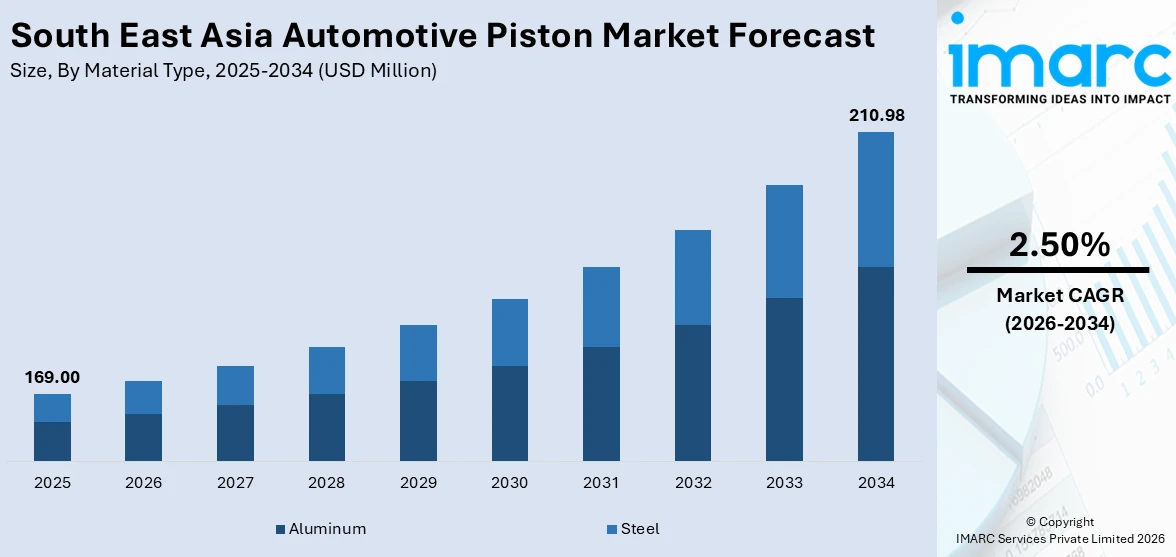

The South East Asia Automotive Piston market size was valued at USD 169.00 Million in 2025 and is projected to reach USD 210.98 Million by 2034, growing at a compound annual growth rate of 2.50% during 2026-2034.

The South East Asia automotive piston market is driven by rapid urbanization, rising vehicle ownership, and the growing demand for fuel-efficient internal combustion engines across the region. Expanding passenger car production, a robust OEM manufacturing ecosystem, and increasing adoption of advanced piston materials and coating technologies continue to shape competitive dynamics and create sustainable growth opportunities for market participants across the South East Asia market.

Key Takeaways and Insights:

- By Material Type: Aluminum represents the largest segment with a market share of 58% in 2025, owing to its lightweight properties, superior thermal conductivity, and compatibility with fuel-efficient passenger vehicle engines, making it the leading material type in Southeast Asian automotive manufacturing hubs.

- By Vehicle Type: Passenger cars dominate the market with a share of 55% in 2025, driven by increasing personal vehicle ownership, urbanization across key Southeast Asian economies, and sustained demand for compact and mid-sized vehicles.

- By Piston Coating Type: Dry film lubricant piston coating leads the market with a share of 40% in 2025, reflecting the growing OEM preference for friction-reducing coatings that enhance engine longevity and meet stringent fuel efficiency standards.

- By Piston Type: Trunk piston represents the largest segment with a market share of 51% in 2025, because of its widespread use in gasoline-powered passenger cars and light commercial vehicles, which remain the backbone of Southeast Asian automotive fleets.

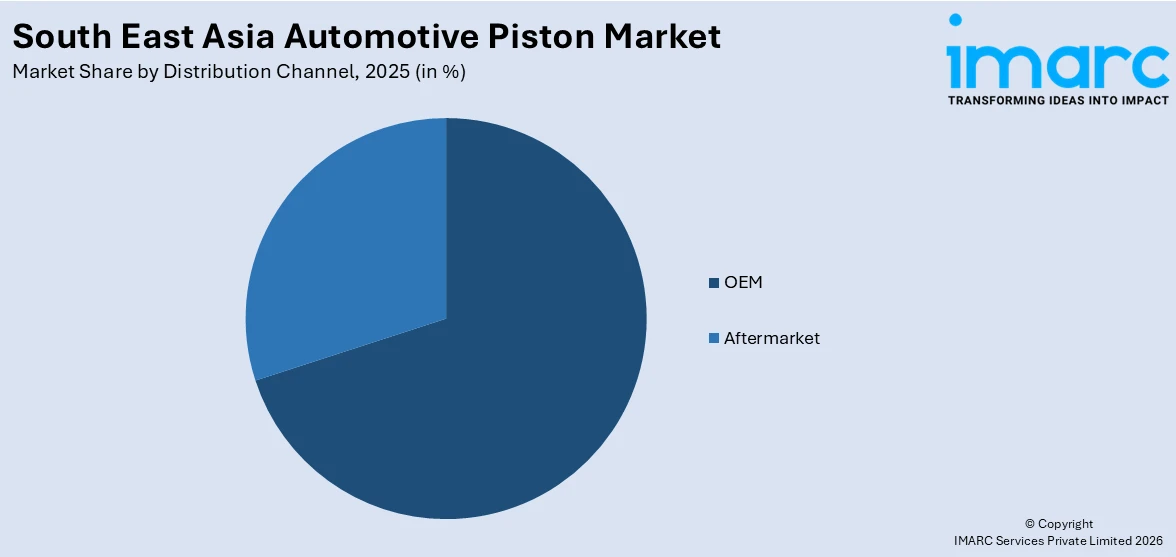

- By Distribution Channel: OEM dominates the market with a share of 69% in 2025, underpinned by well-established original equipment supply networks, high-volume vehicle assembly operations in Thailand and Indonesia, and stringent quality standards.

- Key Players: The South East Asia Automotive Piston market features moderate-to-highly competitive intensity, with international Tier-1 suppliers, regional manufacturers, and specialized coating technology providers competing across OEM and aftermarket distribution channels. Some of the key players in the market include Aisin Asia Pte Ltd. (Aisin Group), Art-Serina Piston Co. Ltd., and PT. Edico Utama.

To get more information on this market Request Sample

The South East Asia automotive piston market is underpinned by the region's enduring reliance on internal combustion engine vehicles and its established position as a global automotive manufacturing hub. Strong vehicle ownership levels and expanding transportation needs continue to drive demand for pistons across passenger and commercial vehicle segments. As of September 2024, the total number of vehicles in circulation in Thailand reached 44.8 million, including approximately 12.5 million passenger cars, reflecting sustained demand for engine-powered mobility. Growth in automotive production, rising replacement demand, and increasing use of light commercial vehicles are further supporting piston usage. In addition, well-established automotive supply chains, continuous industrial development, and increasing income levels are strengthening vehicle demand, thereby driving the need for engine components, such as pistons, across the South East Asia region.

South East Asia Automotive Piston Market Trends:

Rising Vehicle Ownership and Urbanization

The increasing vehicle ownership supported by population growth, urban expansion, and improving economic conditions is a key factor driving the demand for automotive piston in South East Asia. Increasing disposable incomes and expanding middle-class populations are encouraging higher adoption of passenger and commercial vehicles, strengthening overall vehicle usage across the region. Reflecting this improving economic capacity, the Philippine Statistics Authority (PSA) reported a 16.6% increase in gross savings, reaching PHP 7.70 trillion in 2024, indicating stronger individual spending potential. As urban connectivity improves and mobility requirements grow, the expanding vehicle parc continues to drive demand for pistons across both original equipment manufacturing and aftermarket segments in South East Asia.

Advancement in Engine Component Design for Performance and Efficiency

Continuous improvements in engine component design are emerging as a key trend driving the South East Asia automotive piston market, as manufacturers focus on enhancing vehicle performance, fuel efficiency, and durability. Automotive companies are increasingly optimizing piston structures and materials to withstand higher temperatures and pressures while improving combustion efficiency. These advancements support the development of more reliable and efficient internal combustion engines suited for both personal and commercial use. Reflecting this trend, in 2025, ISUZU Vietnam launched the MU-X 2025 featuring a 1.9L diesel engine with improved piston and valve design. Such innovations highlight the growing emphasis on precision-engineered components, driving demand for advanced piston technologies across the regional automotive market.

Increasing Aftermarket Demand for Engine Components

The expanding base of operational vehicles across South East Asia is driving the demand for automotive aftermarket components, including pistons, as aging vehicles require regular maintenance and part replacements. Engine components are subject to continuous wear due to high usage and varying road conditions, increasing the need for reliable replacement solutions to maintain performance and durability. Reflecting the strengthening of organized service infrastructure, in 2025, Shell Philippines launched the world’s first Helix Flagship Auto Workshop, introducing advanced diagnostics, branded lubricants, and trained technicians across multiple locations. Such developments enhance service accessibility and quality, supporting consistent aftermarket demand and reinforcing long-term growth in piston usage across the region.

Market Outlook 2025-2034:

The South East Asia automotive piston market is projected to grow steadily, driven by rising vehicle production, increasing demand for lightweight and coated pistons, and expanding adoption across passenger cars, motorcycles, and commercial vehicles. Market dynamics are shaped by technological advancements in materials and coatings that enhance engine efficiency and durability. The market generated a revenue of USD 169.00 Million in 2025 and is projected to reach a revenue of USD 210.98 Million by 2034, growing at a compound annual growth rate of 2.50% from 2026-2034.

South East Asia Automotive Piston Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Material Type |

Aluminum |

58% |

|

Vehicle Type |

Passenger Cars |

55% |

|

Piston Coating Type |

Dry Film Lubricant Piston Coating |

40% |

|

Piston Type |

Trunk Piston |

51% |

|

Distribution Channel |

OEM |

69% |

Material Type Insights:

- Aluminum

- Steel

Aluminum leads with a market share of 58% of the total South East Asia automotive piston market in 2025.

Aluminum holds the biggest market share due to its favorable combination of lightweight properties, high thermal conductivity, and corrosion resistance. Automotive manufacturers prefer aluminum because it reduces overall engine weight, improving fuel efficiency and lowering emissions, which aligns with stricter regional environmental regulations. The material’s excellent heat dissipation ensures optimal engine performance under high-temperature conditions, enhancing durability and reliability. Additionally, aluminum allows for precise casting and machining, facilitating the production of complex piston geometries required in modern internal combustion engines. These properties make aluminum the preferred choice over traditional materials, driving its dominance in the South East Asia automotive piston segment.

The preference for aluminum is further strengthened by ongoing technological advancements and increasing demand for high-performance vehicles in South East Asia. Growth in passenger cars, commercial vehicles, and motorcycles in countries such as Thailand, Indonesia, and Malaysia has spurred the need for lightweight, durable, and efficient engine components. Automotive manufacturers are investing in research to develop aluminum alloys with improved strength-to-weight ratios, reduced friction, and enhanced wear resistance. Rising adoption of turbocharged and high-compression engines also requires pistons capable of withstanding greater thermal and mechanical stresses, making aluminum the optimal choice. Consequently, these factors collectively reinforce aluminum’s leading position in the region’s automotive piston market.

Vehicle Type Insights:

- Passenger Cars

- Commercial Vehicles

- Others

The passenger cars dominate with a market share of 55% of the total South East Asia automotive piston market in 2025.

Passenger cars lead the market attributed to their dominant share in regional vehicle sales and the expanding middle-class population. Rising disposable incomes, urbanization, and growing demand for personal mobility are fueling passenger car ownership across countries such as Thailand, Indonesia, Malaysia, and Vietnam. Manufacturers are increasingly equipping vehicles with modern, fuel-efficient engines requiring high-quality pistons for enhanced performance, durability, and reduced emissions. The preference for lightweight, high-strength materials in passenger car engines further supports piston demand. Additionally, government policies promoting emission standards, fuel efficiency, and safety regulations incentivize the adoption of advanced piston technologies, reinforcing the passenger car segment as the leading driver in the regional market.

The dominance of passenger cars in the South East Asia automotive piston market is reinforced by rising demand for high-performance and reliable vehicles, along with continuous technological advancements. Growth across compact, mid-size, and luxury segments increases the need for pistons compatible with advanced engine designs, including turbocharged and hybrid systems. This trend is reflected in Vietnam, where total vehicle sales reached 340,142 units in 2024, with passenger cars accounting for 257,900 units, highlighting their strong share. Automotive manufacturers are investing in lightweight materials and precision engineering to meet performance requirements, while increasing urban mobility needs continue to sustain piston demand.

Piston Coating Type Insights:

- Thermal Barrier Piston Coating

- Dry Film Lubricant Piston Coating

- Oil Shedding Piston Coating

Dry film lubricant piston coating exhibits a clear dominance with a 40% share of the total South East Asia automotive piston market in 2025.

Dry film lubricant piston coating represents the largest segment driven by its superior friction-reducing properties and ability to enhance engine efficiency. This coating minimizes direct metal-to-metal contact between the piston and cylinder walls, reducing wear and extending component life. The thermal stability of dry film lubricants ensures consistent performance under high-temperature engine conditions, making them ideal for modern internal combustion engines. Additionally, this coating improves fuel efficiency by lowering mechanical losses and contribute to reduced emissions, aligning with regional environmental regulations. Automotive manufacturers across countries like Thailand, Indonesia, and Malaysia increasingly adopt this coating type to meet performance, durability, and sustainability requirements.

The preference for dry film lubricant coatings is further reinforced by the growing demand for high-performance and lightweight engines in passenger cars, commercial vehicles, and motorcycles. Advancements in coating technology, such as improved adhesion, wear resistance, and corrosion protection, enhance engine reliability and reduce maintenance costs. The adoption of turbocharged and high-compression engines, which operate under higher thermal and mechanical stress, further increases the need for durable piston coatings. Automotive OEMs and aftermarket suppliers are focusing on dry film lubricants due to their compatibility with aluminum and steel pistons, making them the preferred choice in the South East Asia market for both efficiency and long-term engine performance.

Piston Type Insights:

- Trunk Piston

- Crosshead Piston

- Slipper Piston

- Deflector Piston

The trunk piston leads with a market share of 51% of the total South East Asia automotive piston market in 2025.

Trunk piston dominated the market because of its widespread application in conventional internal combustion engines across passenger cars, motorcycles, and commercial vehicles. This piston is preferred for their simple design, durability, and cost-effectiveness, making it suitable for mass-produced vehicles in countries like Thailand, Indonesia, Malaysia, and Vietnam. Trunk piston can efficiently transfer combustion forces to the connecting rod while maintaining engine stability and performance under varying load conditions. Its compatibility with a range of engine sizes, materials, and coatings allows manufacturers to optimize production for fuel efficiency, reduced emissions, and reliability, driving strong adoption throughout the regional automotive sector.

The dominance of trunk piston is further reinforced by the growth in the automotive industry, particularly in affordable and mid-range vehicles that constitute the majority of sales in South East Asia. Manufacturers prioritize pistons that provide long-term engine durability with minimal maintenance, and trunk piston meet these requirements effectively. Additionally, the increasing focus on emission compliance and fuel efficiency in regional markets encourages the adoption of lightweight and thermally optimized trunk piston. As automotive production expands, OEMs and aftermarket suppliers continue to rely on trunk piston for their proven performance, ease of manufacturing, and adaptability, sustaining its leading position in the market.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- OEM

- Aftermarket

OEM dominates with a market share of 69% of the total South East Asia automotive piston market in 2025.

OEM is the leading segment due to its direct involvement in engine manufacturing and strong relationships with vehicle manufacturers. OEM supply pistons as integral components of engines in passenger cars, commercial vehicles, and motorcycles, ensuring compatibility, performance, and quality standards. By providing pistons directly to automotive assembly lines, OEM reduces dependency on third-party suppliers and streamline the supply chain. Its dominance is supported by large-scale production capacities, consistent delivery schedules, and adherence to regulatory requirements for emissions, durability, and efficiency. This direct channel ensures that pistons meet precise specifications, reinforcing OEMs’ position as the primary distribution route across the region.

The prominence of OEM is further strengthened by its ability to integrate advanced piston technologies, such as lightweight materials, coatings, and optimized designs, into vehicle engines. OEM collaborates closely with automotive manufacturers to develop pistons tailored for turbocharged, high-compression, and hybrid engines, supporting performance, fuel efficiency, and emission targets. Additionally, OEM offers warranty-backed components, enhancing trust and reliability for end users. As the South East Asian automotive industry grows with increasing vehicle production and modernization, reliance on OEM for high-quality, performance-oriented pistons continues to expand, making it the leading distribution channel in the market.

Regional Insights:

- Indonesia

- Thailand

- Singapore

- Philippines

- Vietnam

- Malaysia

- Others

Indonesia’s automotive piston market is driven by rising passenger car and motorcycle sales, rapid urbanization, and expanding commercial vehicle demand. Growth in manufacturing, infrastructure projects, and government incentives supporting local automotive production further boosts piston adoption, particularly lightweight aluminum and coated variants for improved engine performance and fuel efficiency.

Thailand is a vital automotive production hub, with strong demand for pistons in passenger cars, commercial vehicles, and motorcycles. Government policies, foreign investment, and the country’s well-established automotive supply chain support high-quality piston manufacturing and adoption of advanced materials and coatings.

Singapore’s market focuses on premium and high-performance automotive segments, emphasizing precision-engineered pistons for imported vehicles and performance engines. Advanced manufacturing, stringent emission regulations, and demand for reliable, durable components drive piston consumption.

The Philippines automotive piston market is growing because of the rising motorcycle and passenger vehicle sales, urbanization, and increasing adoption of fuel-efficient, lightweight pistons. Local assembly plants and rising disposable incomes support piston demand.

Vietnam experiences growth in piston demand fueled by expanding motorcycle production, rising passenger car ownership, and industrial vehicle manufacturing. Lightweight and coated pistons are increasingly used to enhance engine efficiency and meet regulatory standards.

Malaysia’s automotive piston market benefits from its established automotive manufacturing sector, government incentives, and increasing production of passenger and commercial vehicles. Adoption of aluminum and coated pistons supports fuel efficiency and engine performance.

Others, including Myanmar, Cambodia, and Laos, show gradual growth in piston demand, driven by increasing vehicle ownership, urbanization, and adoption of lightweight and efficient engine components to support emerging automotive markets.

Market Dynamics:

Growth Drivers:

Why is the South East Asia Automotive Piston Market Growing?

Favorable Government Policies Supporting Automotive Industry

Government initiatives promoting automotive manufacturing and industrial growth are positively influencing the automotive piston market in South East Asia. Policies offering tax incentives, investment support, and infrastructure development are encouraging the establishment and scaling of vehicle production facilities across the region. Governments are also prioritizing domestic manufacturing capabilities and attracting foreign direct investment into the automotive sector to strengthen industrial output. These initiatives improve supply chain efficiency and production capacity, creating a favorable environment for automotive manufacturers. As vehicle production increases under these supportive frameworks, demand for essential engine components, such as pistons, continues to grow across the region.

Development of Industrial and Commercial Vehicle Applications

The development of industrial and commercial vehicle applications across South East Asia is increasing the demand for automotive pistons due to rising activity in construction, logistics, and heavy-duty transport sectors. Vehicles operating in these environments require robust engine components capable of handling high loads and prolonged usage. The expansion of infrastructure projects, industrial output, and freight movement is leading to higher utilization of commercial vehicle fleets. This increased usage is driving both original equipment demand and aftermarket replacement needs for pistons. The requirement for consistent engine performance and durability in demanding operations continues to reinforce the importance of high-quality piston components.

Increasing Replacement Demand from Aging Vehicle Fleet

The large and aging vehicle fleet across South East Asia is driving the demand for replacement engine components, including pistons. As vehicles remain in use for longer periods, engine parts undergo continuous wear and require regular maintenance to ensure optimal performance and durability. Pistons, being subject to high pressure and temperature, are particularly prone to degradation over time, making them essential in repair cycles. The increasing average vehicle age is expanding the aftermarket segment, supported by the growing presence of service centers and maintenance networks. This sustained need for replacement parts is contributing to consistent piston demand across the region.

Market Restraints:

What Challenges the South East Asia Automotive Piston Market is Facing?

Growing Electric Vehicle Adoption Threatening Long-Term Demand

Accelerating EV adoption across South East Asia poses a structural challenge to long-term piston market growth, as fully electric powertrains eliminate the need for pistons. While current EV penetration remains limited relative to total vehicle sales, the gradual shift in OEM investment toward electrified platforms introduces growing uncertainty for future internal combustion engine piston demand.

Supply Chain Disruptions and Raw Material Price Volatility Impacting Piston Manufacturing Economics

Aluminum and specialty alloy price volatility, combined with global supply chain disruptions affecting precision components and coatings, creates cost uncertainty for piston manufacturers operating across Southeast Asia. Geopolitical trade tensions and US tariff uncertainties are particularly challenging for Thailand's export-oriented automotive supply chain, prompting manufacturers to reassess procurement strategies and supply chain resilience. These input cost pressures can compress manufacturing margins and complicate long-term pricing agreements with OEM customers operating on fixed-cost assembly budgets.

Competitive Pressure from Low-Cost Chinese Piston Producers Intensifying Across Regional Markets

The expanding presence of Chinese automotive manufacturers and component suppliers across Southeast Asia introduces competitive pricing pressure on established piston producers. Chinese OEM entrants leverage vertically integrated supply chains and scale manufacturing capabilities to offer competitively priced engine components, challenging incumbent suppliers to differentiate through quality, coating technology innovation, and engineering service capabilities. These competitive dynamic risks compressing margins for regional piston manufacturers with comparatively limited access to advanced material science R&D investment capabilities.

Competitive Landscape:

The South East Asia Automotive Piston market features a moderately competitive landscape characterized by the presence of established international Tier-1 suppliers, regional piston specialists, and vertically integrated automotive component manufacturers competing across OEM and aftermarket distribution channels. Key competitive factors include material innovation, precision manufacturing capabilities, coating technology expertise, and established OEM supply relationships built through decades of quality-certified performance. International suppliers leverage global R&D investments to introduce advanced piston designs incorporating integrated cooling galleries, optimized crown geometries, and next-generation dry film lubricant coatings that address evolving engine performance requirements. Regional manufacturers compete through competitive pricing, supply chain flexibility, and proximity to major automotive assembly hubs in Thailand and Indonesia. The expanding presence of Chinese automotive manufacturers in the region is reshaping competitive dynamics by introducing vertically integrated component sourcing, creating opportunities for supply chain diversification while intensifying pricing competition across segments.

Some of the key players in the market include

- Aisin Asia Pte Ltd. (Aisin Group)

- Art-Serina Piston Co. Ltd.

- PT. Edico Utama

Recent Developments:

- March 2026: Toyota Gazoo Racing Malaysia launched its team for the 2026 Thailand Super Series, entering two GR Supra GT4 Evo2 race cars in the GT4 category. The cars use a 3.0L inline-six turbo engine with high-performance pistons delivering strong torque (660 Nm), paired with a racing transmission and advanced driveline components.

- March 2026: Isuzu Malaysia opened registrations for the 2026 D-Max, introducing a new 2.2L MaxForce turbo diesel engine to replace the 1.9L unit. The engine features redesigned cylinders, low-friction pistons, improved injectors, and a variable geometry turbo, delivering 163 hp and 400 Nm with better fuel efficiency. Paired with a new 8-speed automatic transmission, the pickup offers improved performance and lower fuel usage, while maintaining multiple variants for both commercial and lifestyle use.

South East Asia Automotive Piston Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Material Types Covered | Aluminum, Steel |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicles, Others |

| Piston Coating Types Covered | Thermal Barrier Piston Coating, Dry Film Lubricant Piston Coating, Oil Shedding Piston Coating |

| Piston Types Covered | Trunk Piston, Crosshead Piston, Slipper Piston, Deflector Piston |

| Distribution Channels Covered | OEM, Aftermarket |

| Countries Covered | Indonesia, Thailand, Singapore, Philippines, Vietnam, Malaysia, Others |

| Companies Covered | Aisin Asia Pte Ltd. (Aisin Group), Art-Serina Piston Co. Ltd., PT. Edico Utama, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South East Asia Automotive Piston Market Research Report and Industry Forecast Report

The South East Asia automotive piston market size was valued at USD 169.00 Million in 2025.

The South East Asia automotive piston market is expected to grow at a compound annual growth rate of 2.50% from 2026-2034 to reach USD 210.98 Million by 2034.

Aluminum accounts for the largest revenue share of 58% in 2025, owing to its lightweight properties, superior thermal conductivity, and compatibility with gasoline-powered passenger vehicle engine platforms prevalent across the region.

Key factors driving the South East Asia automotive piston market include advancements in engine component design to improve fuel efficiency, durability, and performance. In 2025, ISUZU Vietnam launched the MU-X 2025 featuring a 1.9L diesel engine with improved piston and valve design, enhancing combustion efficiency and reliability

Major challenges include growing electric vehicle adoption reducing long-term ICE piston dernand, raw maternal price volatility and supply chain disruptions affecting manufacturing economics, and intensifying competitive pressure from low-cost Chinese component producers expanding their presence across Southeast Asian markets

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)