South East Asia B2B Payments Market Size, Share, Trends and Forecast by Payment Type, Payment Mode, Enterprise Size, Industry Vertical, and Country, 2026-2034

South East Asia B2B Payments Market Summary:

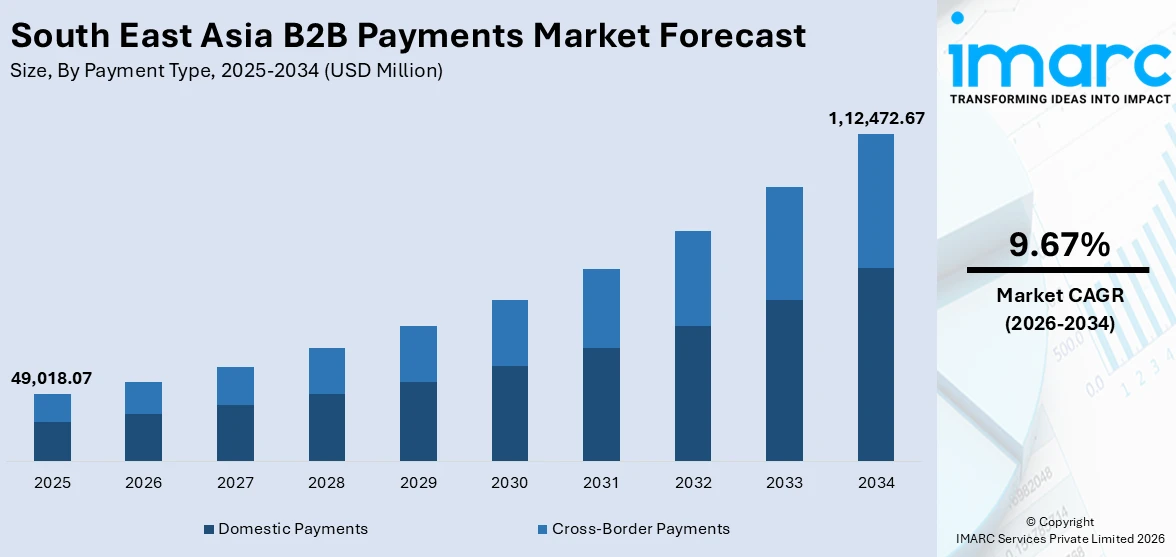

The South East Asia B2B payments market size was valued at USD 49,018.07 Million in 2025 and is projected to reach USD 1,12,472.67 Million by 2034, growing at a compound annual growth rate of 9.67% during 2026-2034.

Digital infrastructure expansion, government-backed cashless initiatives, and the rapid integration of fintech platforms are accelerating payment modernization across the region. The rising intra-ASEAN trade, the growing small and medium-sized enterprises (SMEs) participation in digital commerce, and increasing demand for real-time cross-border settlement capabilities are collectively reshaping the South East Asia B2B payments market. Automation, open banking frameworks, and API-driven integration are further enabling enterprises to streamline processes and reduce transaction costs.

Key Takeaways and Insights:

- By Payment Type: Domestic payments represent the largest segment with a market share of 58% in 2025, driven by the growing intra-regional commerce, expanding real-time payment infrastructure, and increasing adoption of national instant payment rails across Southeast Asian economies.

- By Payment Mode: Digital dominates the market with a share of 70% in 2025, reflecting rapid fintech adoption, government cashless economy mandates, and the proliferation of mobile-first B2B payment platforms across the region.

- By Enterprise Size: Large enterprises lead the market with a share of 55% in 2025, owing to higher transaction volumes, robust treasury management systems, and earlier adoption of integrated ERP-linked payment solutions for multi-currency operations.

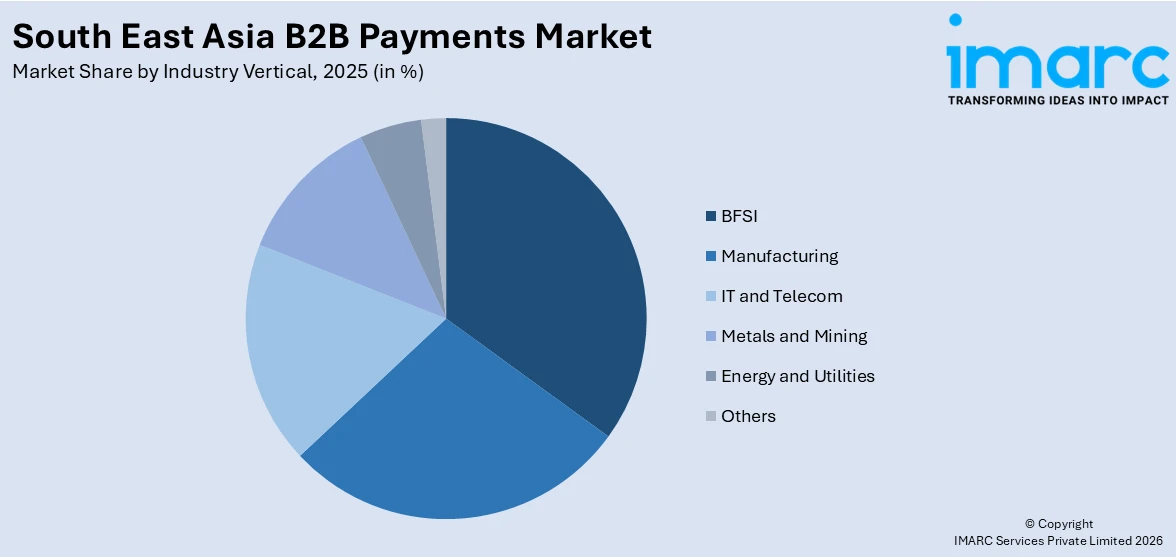

- By Industry Vertical: BFSI represents the largest segment with a market share of 26% in 2025, given its inherent dependency on efficient payment processing, compliance-driven digital migration, and high-volume interbank settlement activity.

- Key Players: The South East Asia B2B payments market features strong competition among global payment networks, regional fintech firms, and digital-native banks, each developing innovative solutions to capture the growing enterprise transaction volumes across diverse verticals.

To get more information on this market Request Sample

The South East Asia B2B payments market is advancing at a significant pace as businesses across the region accelerate their shift away from manual and paper-based processes toward digitally integrated financial ecosystems. Enterprises are adopting digital invoicing, automated payment workflows, and centralized treasury systems to improve financial visibility, reduce processing delays, and support cross-border trade operations. The expansion of regional supply chains and growing participation of small and medium enterprises in international commerce are further increasing demand for secure and efficient B2B payment infrastructure. Reflecting this trend, in 2024, SUNRATE launched its global payment and treasury management platform in Vietnam to strengthen cross-border B2B payment services and international collections, enabling businesses to streamline global transactions and improve financial operations. As organizations prioritize faster settlement, better financial transparency, and integrated payment systems, the adoption of digital B2B payment platforms across Southeast Asia continues to expand rapidly, supporting modernized financial management and regional trade growth.

South East Asia B2B Payments Market Trends:

Digitalization of Supply Chain Financial Transactions

A key trend supporting the South East Asia B2B payments market is the increasing digitalization of financial transactions across supply chains. Businesses are adopting integrated payment solutions that replace manual invoicing and settlement processes with automated digital systems. These platforms help enterprises improve cash-flow visibility, accelerate payment cycles, and strengthen financial coordination between suppliers and buyers. Digital payment infrastructures also provide real-time transaction insights and improve financial transparency within supply networks. The shift toward digital supply chain finance is encouraging businesses to implement scalable B2B payment platforms. As evidence, in 2025, Visa partnered with C.P. Vietnam and Vietnam International Bank to introduce digital payment solutions aimed at modernizing supply chain transactions and supporting SMEs through improved financial tools.

Automation of Industry-Specific B2B Payment Processes

Businesses in transaction-intensive industries are increasingly adopting automated payment systems to reduce operational complexity and improve financial efficiency. Digital B2B payment platforms enable automated settlement processes, minimize reconciliation errors, and enhance payment security between business partners. Automation is particularly important in sectors where frequent transactions occur between intermediaries, service providers, and suppliers. These solutions simplify financial operations by reducing reliance on manual processing and enabling faster payment cycles. For instance, in 2024, Mastercard partnered with NTT DATA and OneHotel in Thailand to launch a digital B2B payment platform that automates virtual card payment processing between online travel agents and hotels, improving reconciliation efficiency and reducing transaction delays.

Rising Demand for Efficient Cross-Border Payment Infrastructure

The expansion of cross-border trade across Southeast Asia is driving the need for faster and more reliable international B2B payment systems. Businesses require payment solutions capable of supporting multi-currency transactions, faster settlement cycles, and seamless fund transfers across global markets. Digital payment infrastructure enables companies to reduce processing delays, improve transaction transparency, and manage cross-border financial operations more efficiently. These capabilities are becoming essential for enterprises engaged in international trade and regional supply chain networks. Supporting this trend, in 2025, Visa partnered with USSC Money Services Inc. to launch Visa Direct in the Philippines, enabling businesses to send cross-border payments directly to eligible cards, bank accounts, and digital wallets across more than 195 countries and 150 currencies.

Market Outlook 2026-2034:

The South East Asia B2B payments market is poised for sustained expansion over the forecast period, supported by rapid digitalization of financial services, growing cross-border trade, and increasing adoption of electronic payment platforms by small and medium firms. Businesses across the region are shifting from traditional cash and manual processes to digital invoicing, automated payment systems, and real-time settlement solutions. The market generated a revenue of USD 49,018.07 Million in 2025 and is projected to reach a revenue of USD 1,12,472.67 Million by 2034, growing at a compound annual growth rate of 9.67% from 2026-2034.

South East Asia B2B Payments Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Payment Type |

Domestic Payments |

58% |

|

Payment Mode |

Digital |

70% |

|

Enterprise Size |

Large Enterprises |

55% |

|

Industry Vertical |

BFSI |

26% |

Payment Type Insights:

- Domestic Payments

- Cross-Border Payments

Domestic payments exhibit a clear dominance with a 58% share of the total South East Asia B2B payments market in 2025.

Domestic payments represent the largest segment driven by the high volume of transactions conducted within national supply chains. Businesses across sectors such as manufacturing, retail, logistics, and wholesale frequently process payments with local suppliers, distributors, and service providers. These transactions typically involve routine operational payments, including procurement settlements, vendor invoices, payroll services, and utility expenses. The strong presence of small and medium enterprises across the region further contributes to the dominance of domestic payment flows, as these businesses primarily operate within national markets. Increasing adoption of digital invoicing platforms, real-time payment systems, and automated accounting solutions is making domestic transactions faster, more transparent, and easier to manage for businesses of all sizes.

Government-led digital payment initiatives and expanding fintech ecosystems are also supporting the growth of domestic payments across South East Asia. Several countries in the region have introduced national instant payment infrastructures and interoperable digital banking networks that enable businesses to process payments quickly and securely within domestic markets. Banks and fintech providers are offering integrated payment platforms that combine invoicing, reconciliation, and payment tracking features, helping companies improve financial management and reduce operational delays. In addition, regulatory frameworks encouraging electronic payments and reducing dependence on cash transactions are accelerating the transition toward digital domestic payments. These developments continue to strengthen domestic payment volumes and reinforce their leading share in the market.

Payment Mode Insights:

- Traditional

- Digital

Digital dominates with a market share of 70% of the total South East Asia B2B payments market in 2025.

Digital holds the biggest market share because of the rapid digital transformation of financial systems across the region. Businesses are increasingly adopting digital payment platforms to improve transaction speed, reduce operational costs, and enhance transparency in financial processes. Electronic invoicing, online banking platforms, and integrated payment gateways allow companies to manage vendor payments, supplier settlements, and recurring transactions more efficiently than traditional methods. The expansion of internet penetration and smartphone usage has also made digital payment solutions more accessible to businesses of all sizes. As companies seek to streamline financial operations and improve record accuracy, digital payment systems are becoming the preferred mode for B2B transactions across key regional economies.

The growing presence of fintech providers and digital banking services is further strengthening the adoption of digital B2B payment modes across South East Asia. Financial technology firms are offering advanced solutions that support automated payments, real-time transaction tracking, and integrated financial management tools for enterprises. These platforms help businesses reduce manual paperwork, minimize payment delays, and improve cash flow visibility across supply chains. Additionally, several regional banks are partnering with fintech companies to introduce secure digital payment infrastructure tailored for corporate transactions. Supportive government initiatives promoting cashless economies and electronic payment systems are also encouraging businesses to shift toward digital payment modes, reinforcing their dominant position within the market.

Enterprise Size Insights:

- Large Enterprises

- Small and Medium-sized Enterprises

Large enterprises lead with a market share of 55% of the total South East Asia B2B payments market in 2025.

Large enterprises dominate the market owing to their high transaction volumes and complex supplier networks. These organizations regularly process large-value payments with domestic and international vendors, distributors, and service providers, creating strong demand for efficient B2B payment systems. Large companies often manage extensive procurement operations and multi-layered supply chains that require secure, reliable, and scalable payment infrastructure. As a result, they invest significantly in advanced payment platforms that support automated invoicing, payment scheduling, and financial reconciliation. Their greater financial resources also allow them to implement integrated enterprise resource planning systems that connect payment processes with accounting, procurement, and financial management functions.

In addition, large enterprises are typically early adopters of digital financial technologies that improve payment efficiency and operational control. Many organizations deploy centralized treasury management systems to monitor and process payments across multiple subsidiaries and geographic markets. These systems enable businesses to manage liquidity, reduce transaction errors, and maintain accurate financial records across large-scale operations. Partnerships with banks, fintech providers, and digital payment platforms further support the adoption of advanced B2B payment solutions among large enterprises. The ability to integrate payment systems with broader financial management tools helps these organizations streamline business processes, strengthen supplier relationships, and maintain consistent payment performance, reinforcing their leading position in the market.

Industry Vertical Insights:

Access the comprehensive market breakdown Request Sample

- BFSI

- Manufacturing

- IT and Telecom

- Metals and Mining

- Energy and Utilities

- Others

BFSI exhibits a clear dominance with a 26% share of the total South East Asia B2B payments market in 2025.

BFSI leads the market in due to the sector’s high dependence on secure, high-frequency financial transactions between institutions, service providers, and corporate clients. Banks, insurance companies, and financial institutions regularly process large volumes of payments related to interbank settlements, vendor services, regulatory fees, and technology partnerships. The sector’s strong emphasis on operational accuracy and compliance encourages the use of advanced B2B payment systems that support automated processing, real-time tracking, and secure transaction verification. Additionally, financial institutions are continuously upgrading payment infrastructure to support digital banking services, cross-border financial operations, and integrated treasury management systems that ensure efficient fund transfers within complex financial ecosystems.

The expansion of digital banking platforms and fintech collaborations is further strengthening the BFSI sector’s dominance in B2B payment activities across South East Asia. Financial institutions are actively integrating digital payment networks, automated clearing systems, and blockchain-enabled transaction platforms to improve processing speed and transparency. These technologies help banks and financial service providers manage large-scale institutional payments while maintaining strong security standards. Moreover, the growing demand for financial services across corporate sectors increases the number of transactions handled by banks and payment service providers. Continuous investment in payment infrastructure, regulatory compliance systems, and financial technology innovation allows the BFSI sector to maintain a central role in facilitating B2B payment flows across the regional economy.

Country Insights:

- Indonesia

- Thailand

- Singapore

- Philippines

- Vietnam

- Malaysia

- Others

Indonesia holds a significant position in the market, attributed its large business ecosystem and expanding digital payment infrastructure. Growing adoption of electronic invoicing, fintech payment platforms, and government initiatives promoting cashless transactions are encouraging enterprises to shift toward efficient digital B2B payment systems.

Thailand’s B2B payments market is growing owing to increasing digital financial adoption and strong government support for electronic payment infrastructure. Businesses are increasingly utilizing digital banking platforms, automated payment systems, and real-time transaction services to improve operational efficiency and manage supplier and vendor payments effectively.

Singapore represents a highly advanced B2B payments market influenced by strong financial infrastructure and widespread digital banking adoption. The country’s position as a regional financial hub encourages businesses to use secure digital payment systems, automated invoicing platforms, and cross-border transaction solutions for efficient corporate payment management.

The Philippines B2B payments market is growing with the expansion of digital banking services and increasing adoption of electronic payment platforms by enterprises. Government-led financial inclusion initiatives and improving fintech ecosystems are encouraging businesses to adopt digital B2B payment systems for faster and more transparent financial transactions.

The market in Vietnam is witnessing growth driven by rapid economic development and increasing enterprise digitalization. Businesses are adopting electronic payment platforms, digital banking services, and automated invoicing tools to streamline financial operations and support expanding domestic trade and supply chain transactions.

Malaysia’s B2B payments market is supported by well-developed banking infrastructure and strong fintech innovation. Enterprises are increasingly adopting digital payment platforms and automated financial management systems to improve transaction efficiency, enhance payment transparency, and support business operations across growing domestic and regional trade networks.

Others South East Asian countries are gradually strengthening their B2B payments ecosystems as businesses adopt digital financial tools and payment technologies. Increasing internet penetration, expanding fintech services, and government initiatives promoting electronic payments are encouraging enterprises to transition toward more efficient and transparent B2B payment processes.

Market Dynamics:

Growth Drivers:

Why is the South East Asia B2B Payments Market Growing?

Growing Adoption of Fintech Payment Platforms by SMEs

Small and medium enterprises across Southeast Asia are increasingly turning to fintech-based payment platforms to modernize financial operations and manage business transactions more efficiently. Digital payment applications allow businesses to consolidate payment management, track financial activity, and improve vendor payment processes through centralized interfaces. These solutions help SMEs overcome limitations associated with traditional banking systems while providing greater financial visibility and control over cash flow. Fintech platforms are also expanding access to secure digital payment infrastructure for smaller enterprises participating in regional supply chains. Reflecting this development, in 2024, PayMate launched a business payments application in Malaysia designed to help SMEs streamline vendor payments, manage cash flow, and conduct secure transactions through a unified digital platform.

Growing Focus on Financial Transparency and Compliance

Organizations are placing greater emphasis on maintaining transparent financial operations and complying with regulatory requirements related to financial reporting, taxation, and transaction monitoring. B2B payment platforms provide detailed transaction records, audit trails, and reporting capabilities that help businesses maintain compliance with financial regulations. These systems support improved financial governance by enabling organizations to monitor payment flows, verify transaction authenticity, and maintain accurate financial documentation. As regulatory frameworks across Southeast Asian economies evolve and businesses operate across multiple jurisdictions, enterprises are adopting structured B2B payment systems that support transparent and compliant financial management practices.

Increasing Need for Secure and Fraud-Resistant Payment Systems

With the growing volume of digital financial transactions, businesses are prioritizing payment systems that provide strong security and fraud prevention mechanisms. B2B payment platforms incorporate security features, such as encryption protocols, identity verification, transaction monitoring, and access control mechanisms, to safeguard financial transactions. These systems help organizations reduce risks associated with payment fraud, unauthorized transactions, and financial data breaches. As enterprises process larger transaction volumes across digital payment channels, the demand for secure payment infrastructures capable of protecting financial information and ensuring transaction integrity continues to increase across the Southeast Asian B2B payments market.

Market Restraints:

What Challenges the South East Asia B2B Payments Market is Facing?

Fragmented Regulatory Landscape Across Jurisdictions

Southeast Asia's diverse mix of regulatory frameworks creates significant complexity for businesses conducting cross-border B2B payments. Varying compliance requirements related to anti-money laundering, foreign exchange controls, and know-your-customer procedures increase administrative overhead for enterprises operating across multiple countries. Inconsistent standards in banking infrastructure and payment messaging formats further complicate efforts to achieve seamless regional payment interoperability and scale digital B2B payment operations.

Cybersecurity Risks and Payment Fraud Challenges

Rising digital payment volumes are increasing exposure to cybersecurity risks, creating hesitation among businesses when adopting fully digital B2B payment systems. Many small and medium firms lack advanced cybersecurity infrastructure and effective fraud detection capabilities, which weakens confidence in automated payment workflows and slows the transition from traditional payment methods to digital platforms.

Integration Costs and Legacy System Dependencies

Many businesses across Southeast Asia continue to operate legacy enterprise systems incompatible with modern digital payment platforms, creating significant integration costs and operational friction. Smaller enterprises and those in less developed markets often lack the technical expertise and financial resources required to migrate from traditional payment methods. High initial investment requirements for system upgrades and integration testing slow the pace of digital B2B payment adoption and widen the gap between technologically advanced and traditional players.

Competitive Landscape:

The South East Asia B2B payments market features a competitive environment shaped by the convergence of global payment networks, regional fintech innovators, digital banks, and traditional financial institutions. Market participants are investing in real-time payment connectivity, multi-currency settlement capabilities, and AI-powered compliance tools to differentiate their offerings. Strategic partnerships between payment service providers and enterprise software platforms are broadening access to automated payment solutions. Regulatory sandboxes and licensing frameworks across Singapore, Indonesia, and Malaysia are enabling new entrants to develop and scale innovative payment infrastructure, intensifying competition while simultaneously expanding the overall market.

Recent Developments:

- August 2025: PayMate announced its expansion into Indonesia through a USD 400 million acquisition deal with fintech provider DigiAsia. The move enabled PayMate to strengthen its B2B digital payments ecosystem and expand cross-border payment capabilities across Southeast Asia. The partnership also aimed to support SME financial services, embedded finance solutions, and digital settlement infrastructure across emerging Asian markets.

- June 2025: PingPong announced the expansion of its B2B cross-border payments platform into Malaysia after receiving a Money Services Business licence from Bank Negara Malaysia. The move strengthens PingPong’s presence in Southeast Asia and enables enterprises, financial institutions, and SaaS firms to conduct compliant international payments through its platform. The expansion also supports growing regional demand for secure and scalable cross-border payment infrastructure.

South East Asia B2B Payments Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Payment Types Covered | Domestic Payments, Cross-Border Payments |

| Payment Modes Covered | Traditional, Digital |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| Industry Verticals Covered | BFSI, Manufacturing, IT and Telecom, Metals and Mining, Energy and Utilities, Others |

| Countries Covered | Indonesia, Thailand, Singapore, Philippines, Vietnam, Malaysia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South East Asia B2B Payments Market Report

The South East Asia B2B payments market size was valued at USD 49,018.07 Million in 2025.

The South East Asia B2B payments market is expected to grow at a compound annual growth rate of 9.67% during 2026-2034 to reach USD 1,12,472.67 Million by 2034.

Domestic payments hold the largest revenue share of 58% in 2025, driven by the deepening of real-time payment infrastructure across the region and the high frequency of intra-country supplier and vendor payment transactions across Southeast Asian economies.

Key factors driving the South East Asia B2B payments market include the growing digitalization of supply chain financial transactions, as businesses replace manual invoicing with automated payment platforms that improve cash-flow visibility and efficiency. In 2025, Visa partnered with C.P. Vietnam and Vietnam International Bank to introduce digital B2B supply chain payment solutions.

Major challenges include fragmented regulatory frameworks across jurisdictions increasing compliance complexity, rising cybersecurity threats and payment fraud risks, and high integration costs associated with transitioning from legacy enterprise systems to modern digital payment platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade