South East Asia Edtech Market Size, Share, Trends and Forecast by Sector, Type, Deployment Mode, End User, and Country, 2026-2034

South East Asia Edtech Market Summary:

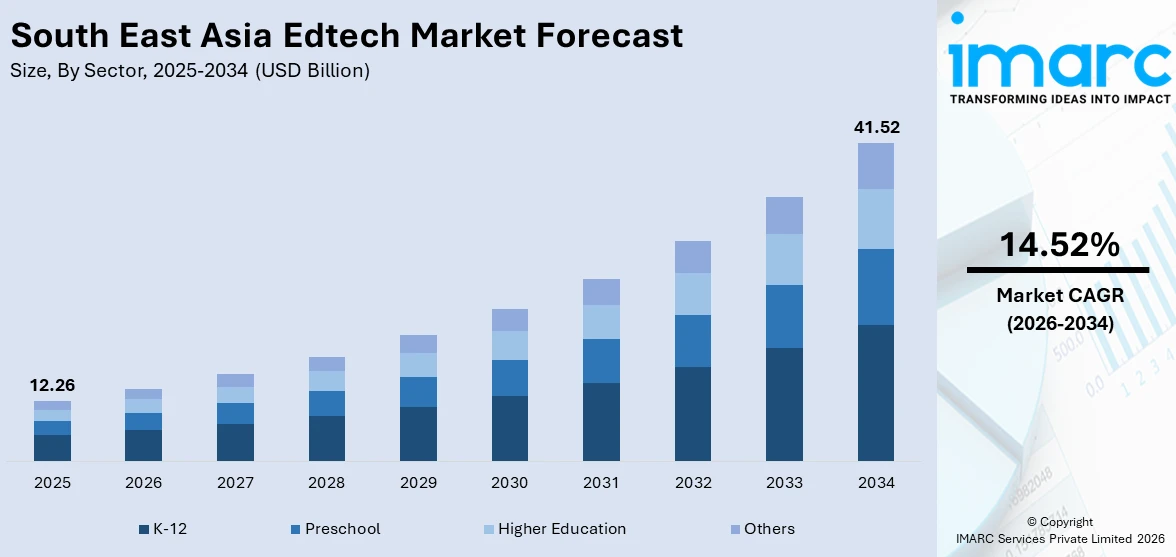

The South East Asia edtech market size was valued at USD 12.26 Billion in 2025 and is projected to reach USD 41.52 Billion by 2034, growing at a compound annual growth rate of 14.52% from 2026-2034.

The market is experiencing robust growth, underpinned by the region’s youthful demographics, accelerating digital infrastructure development, and strong governmental commitment to modernizing education systems. The proliferation of mobile internet connectivity across urban and rural areas has broadened access to digital learning platforms, while a culturally ingrained emphasis on academic achievement continues to fuel household investment in supplementary educational technologies. The convergence of artificial intelligence (AI), cloud computing, and adaptive learning methodologies is further reshaping instructional delivery across K-12, higher education, and corporate training, thereby expanding the South East Asia edtech market share.

Key Takeaways and Insights:

- By Sector: K-12 dominates the market with a share of 57% in 2025, driven by the region’s massive school-age population spanning primary and secondary education levels, alongside intensifying classroom digitalization initiatives supported by national education ministries.

- By Type: Hardware leads the market with a share of 42% in 2025, attributed to ongoing institutional procurement of interactive whiteboards, tablets, laptops, and digital classroom infrastructure essential for deploying technology-enabled learning environments across schools and universities.

- By Deployment Mode: On-premises represent the largest segment with a market share of 70% in 2025, reflecting established institutional preferences for locally hosted systems that ensure data sovereignty, comply with national regulatory frameworks, and provide reliable performance in areas with inconsistent internet connectivity.

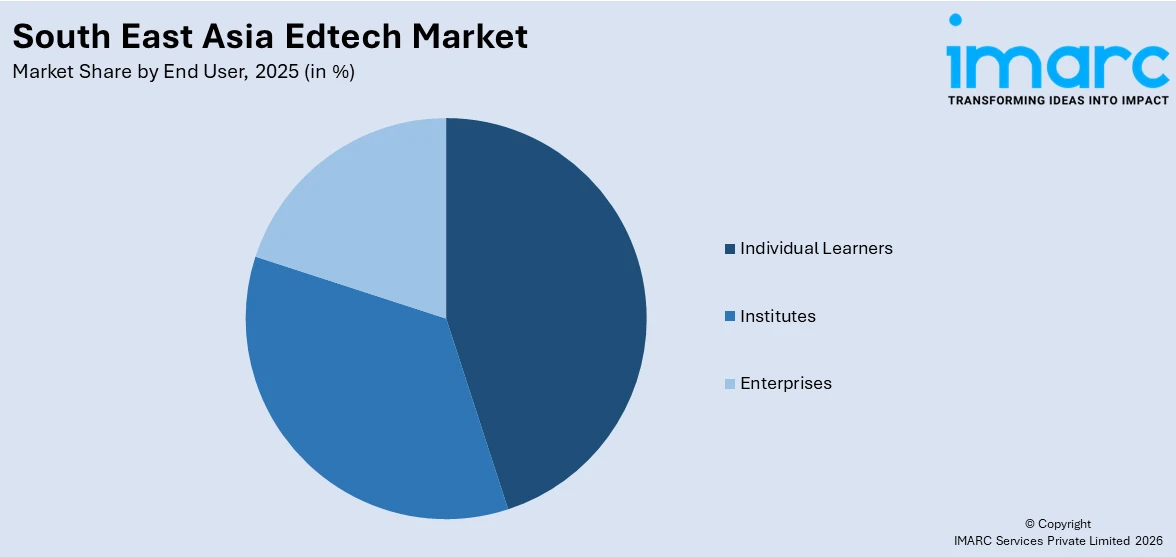

- By End User: Individual learners account for the largest segment with a market share of 41% in 2025, fueled by rising consumer demand for self-directed learning platforms, tutoring applications, and online skill development resources accessible via smartphones and personal devices.

- By Country: Indonesia dominates with a share of 30% in 2025, owing to its position as the most populous nation in the region with over 270 million people, a rapidly expanding digital economy, and proactive government efforts to integrate technology into public education systems.

- Key Players: The South East Asia edtech market exhibits a highly fragmented and competitive landscape, characterized by a dynamic mix of regional startups, established domestic platforms, and international technology providers competing across diverse product categories including learning management systems, tutoring platforms, content delivery solutions, and enterprise training tools.

To get more information on this market Request Sample

The market environment is characterized by the cumulative impact of demographic, technological, and policy factors that create the necessary momentum for the procurement of digital education solutions. The region has a population of 703,013,809 individuals and the population below the age of 25 is quite large. The digitalization initiatives undertaken by the governments of the respective countries in the region, such as the EdTech Masterplan 2030 in Singapore and Ruang GTK, a digital teacher development program in Indonesia, have contributed to the momentum in the procurement of digital education solutions. The shift to the hybrid learning concept, which encompasses the amalgamation of both digital and analog learning approaches, has gained momentum as the structural changes in the education ecosystem have been sustained in the recent past. The commencement of the era of incorporating artificial intelligence (AI) and machine learning (ML) in digital education solutions has facilitated the creation of customized learning experiences that can be couched at the personal level, as the content is aligned with the abilities of the learners. The dynamic startup environment characterized by the massive presence of ed-tech companies in the region continues to attract investor interest in the market.

South East Asia Edtech Market Trends:

Rise of AI-Powered Personalized and Adaptive Learning

AI is increasingly being integrated into edtech platforms across Southeast Asia to deliver hyper-personalized learning experiences. AI-driven tools are enabling real-time assessment of student performance, automated content recommendations, and adaptive difficulty adjustments that cater to individual learning paces. Singapore’s Ministry of Education has deployed AI tools through its Student Learning Space platform, including an Adaptive Learning System that creates personalized learning paths for students in mathematics and geography. This trend is particularly significant in a region marked by diverse learning needs and varying levels of educational infrastructure, as AI-powered solutions can bridge quality gaps at scale. In 2026, the Department of Education (DepEd) and Microsoft Philippines are maintaining their partnership to enhance national literacy results by reinforcing foundational skills for learners and assisting educators with Microsoft’s user-friendly AI-driven tools. Microsoft Learning Accelerators integrate AI-driven coaching and progress monitoring to assist students in enhancing fundamental abilities in reading, mathematics, and well-being, while developing future-ready skills like digital information literacy and proficient communication.

Expansion of Hybrid and Blended Learning Models

The adoption of hybrid learning methodologies, combining digital and in-person instruction, has become a defining feature of the Southeast Asian education landscape. Educational institutions and edtech providers are developing integrated ecosystems that allow seamless transitions between online coursework and physical classroom engagement. For instance, Indonesia-based Ruangguru now operates over 280 learning centers alongside its digital platform, delivering a comprehensive blended learning experience to millions of students across the country. This approach addresses the region’s geographical dispersion and infrastructure variability while maintaining the interpersonal dynamics critical to effective pedagogy.

Growing Focus on Workforce Upskilling and Digital Literacy

Southeast Asia’s rapidly evolving digital economy is driving significant demand for workforce-oriented edtech solutions focused on professional upskilling and digital literacy development. Countries across the region are facing acute shortages of digitally skilled professionals, with Indonesia alone requiring an estimated nine million digital professionals by 2030 to sustain its digital economy growth trajectory. This workforce imperative is fueling the expansion of corporate training platforms, professional certification programs, and skills-based learning modules tailored to industry-specific competency requirements, creating a substantial growth vector for the edtech market beyond traditional academic segments.

Market Outlook 2026-2034:

The South East Asia edtech market is poised for sustained expansion over the forecast period, driven by continued government investment in digital education infrastructure, rising middle-class spending on supplementary learning tools, and the deepening integration of emerging technologies such as artificial intelligence, virtual reality, and cloud-based delivery systems into educational platforms. The market generated a revenue of USD 12.26 Billion in 2025 and is projected to reach a revenue of USD 41.52 Billion by 2034, growing at a compound annual growth rate of 14.52% from 2026-2034. The region’s favorable demographic profile, characterized by a large and growing youth population alongside increasing internet and smartphone penetration rates, provides a strong structural foundation for long-term market growth. Additionally, cross-border partnerships between regional and international edtech firms are expected to enhance content quality and expand market reach across linguistically and culturally diverse populations.

South East Asia Edtech Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Sector |

K-12 |

57% |

|

Type |

Hardware |

42% |

|

Deployment Mode |

On-premises |

70% |

|

End User |

Individual Learners |

41% |

|

Country |

Indonesia |

30% |

Sector Insights:

- Preschool

- K-12

- Higher Education

- Others

K-12 dominates with a market share of 57% of the total South East Asia edtech market in 2025.

The K-12 segment’s commanding position is fundamentally driven by the region’s vast school-age population and the accelerating pace of classroom digitalization across primary and secondary education systems. National governments throughout Southeast Asia have prioritized the integration of digital tools into K-12 curricula, recognizing that technology-enabled instruction can address systemic challenges including teacher shortages, geographic access barriers, and inconsistent quality of educational delivery in rural and underserved communities.

Furthermore, the K-12 segment benefits from strong parental willingness to invest in supplementary digital education, particularly in markets where academic success is culturally regarded as a pathway to social and economic advancement. The proliferation of interactive learning applications, gamified content platforms, and AI-powered tutoring systems has transformed supplementary education, making it more accessible and engaging for young learners. Platforms offering personalized support in core subjects and standardized test preparation continue to experience robust adoption across both urban centers and emerging digital markets within the region.

Type Insights:

- Hardware

- Software

- Content

Hardware leads with a share of 42% of the total South East Asia edtech market in 2025.

The hardware segment’s leading position reflects the foundational role that physical devices and digital infrastructure play in enabling technology-based education across Southeast Asia. Institutional procurement of interactive display panels, student tablets, laptop computers, and classroom networking equipment constitutes a significant share of edtech expenditure, particularly as governments implement large-scale programs to equip public schools with digital learning capabilities and bridge the technology access gap between urban and rural educational institutions.

Additionally, the hardware segment is sustained by the region’s expanding internet infrastructure development, which necessitates continuous investment in connectivity-enabling devices and supporting equipment. The growing adoption of bring-your-own-device policies in secondary and higher education institutions, combined with the increasing affordability of consumer electronics, is further amplifying hardware demand. As digital learning ecosystems mature across the region, the interdependence between hardware deployment and software adoption ensures that infrastructure investment remains a critical enabler of the broader edtech market’s expansion.

Deployment Mode Insights:

- Cloud-based

- On-premises

On-premises exhibit a clear dominance with a 70% share of the total South East Asia edtech market in 2025.

The on-premises deployment mode’s substantial market share reflects the prevailing institutional preference for locally hosted educational technology systems across Southeast Asia. Educational institutions, government agencies, and corporate training organizations in the region continue to favor on-premises solutions due to considerations around data security, regulatory compliance with national data protection frameworks, and the need for reliable system performance in areas where internet connectivity remains inconsistent or bandwidth-constrained.

However, the deployment landscape is gradually evolving as cloud infrastructure expands and internet reliability improves across the region. While on-premises systems currently dominate due to established institutional procurement practices and legacy infrastructure investments, the cloud-based segment is experiencing accelerating growth driven by its inherent scalability, lower upfront capital requirements, and capacity to support real-time collaborative learning environments. The ongoing development of regional data center infrastructure by major cloud service providers is expected to progressively address sovereignty and latency concerns, potentially shifting the deployment balance over the forecast period.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Individual Learners

- Institutes

- Enterprises

Individual learners lead with a share of 41% of the total South East Asia edtech market in 2025.

The individual learners segment’s market share underscores the powerful consumer-driven dynamics shaping the Southeast Asian edtech landscape. The region’s large youth demographic, coupled with rising middle-class disposable incomes and deepening smartphone penetration, has created favorable conditions for direct-to-consumer edtech platforms offering self-paced learning, tutoring services, language acquisition programs, and professional skill development courses. The cultural emphasis on educational attainment and competitive academic environments drives strong individual investment in supplementary learning resources.

Moreover, the individual learners segment is being further energized by the growing demand for lifelong learning and professional upskilling among working adults seeking to remain competitive in rapidly evolving job markets. The accessibility and affordability of mobile-first learning platforms have democratized access to quality educational content, enabling learners across diverse socioeconomic backgrounds to pursue self-directed academic and professional development. The segment’s consumer-led growth model is reinforced by the region’s high mobile usage rates and the increasing sophistication of app-based learning experiences.

Country Insights:

- Indonesia

- Thailand

- Singapore

- Philippines

- Vietnam

- Malaysia

- Others

Indonesia exhibits a clear dominance with a 30% share of the total South East Asia edtech market in 2025.

Indonesia’s leading market share is principally driven by its status as the most populous country in Southeast Asia, with 287,065,540 inhabitants and a demographic profile skewed toward younger age cohorts. The nation’s rapidly expanding digital economy, supported by increasing mobile internet penetration and a thriving technology startup ecosystem, has created a fertile environment for edtech adoption. The Indonesian government’s proactive digital education initiatives, including the Ruang GTK platform for educator professional development and the planned integration of coding and artificial intelligence topics into school curricula for the upcoming academic year, are further accelerating market growth.

Additionally, Indonesia’s vast geographical spread across thousands of islands presents unique challenges in delivering equitable educational access, positioning edtech as a critical solution for bridging urban-rural quality gaps. The country’s edtech startup ecosystem is among the most vibrant in the region, with platforms addressing diverse educational needs from K-12 tutoring and test preparation to vocational training and workforce development. The convergence of strong demographic fundamentals, government policy support, and entrepreneurial innovation establishes Indonesia as the primary growth engine for the broader Southeast Asian edtech market.

Market Dynamics:

Growth Drivers:

Why is the South East Asia Edtech Market Growing?

Favorable Demographic Profile and Rising Digital Connectivity

Southeast Asia’s demographic composition constitutes a fundamental structural driver for the edtech market, with the region home to a predominantly young population that represents one of the largest addressable markets for educational technology globally. The combination of a massive school-age cohort and a rapidly expanding working-age population creates sustained demand across both academic and professional learning segments. Concurrently, the region is experiencing significant improvements in digital infrastructure, with mobile internet penetration rates climbing steadily and smartphone adoption becoming increasingly widespread across all socioeconomic strata. This expanding digital connectivity is removing traditional access barriers to quality educational content, enabling learners in previously underserved rural and remote communities to engage with digital learning platforms. The Philippines is rapidly advancing towards a digital future. Aligned with President Ferdinand Marcos Jr.’s instruction to prioritize digital connectivity, the National Digital Connectivity Plan (NDCP), the nation’s inaugural master plan for digital infrastructure, received approval from the Infrastructure Development Committee (INFRACOM), as formally verified in accordance with Executive Order No. 72, s. 2024, at the 7th Economy and Development (ED) Council Meeting, led by the President, on January 26, 2026, at the Bahay Pangulo Pavilion, PSC Compound, Otis, Manila.

Proactive Government Policies and Public Investment in Digital Education

National governments across Southeast Asia are implementing comprehensive digital education strategies that are meaningfully accelerating the institutional adoption of educational technology solutions. These policy frameworks encompass curriculum modernization initiatives, teacher digital literacy programs, public school technology infrastructure upgrades, and the establishment of national digital learning platforms. Singapore’s EdTech Masterplan 2030 exemplifies this trend, articulating a vision for nurturing digitally empowered and future-ready learners through technology-enhanced pedagogical approaches. Similarly, Indonesia’s Merdeka Belajar educational reform agenda and Vietnam’s targets to digitize the entire national education system by the end of this decade are creating significant institutional demand for edtech products and services. These government-led initiatives are particularly impactful as they operate at scale, influencing procurement decisions across thousands of public educational institutions and establishing technology adoption benchmarks that the private education sector subsequently follows. In 2025, The Malaysian government is promoting digital inclusion in education via a new program that will provide 387 Sekolah Jenis Kebangsaan Tamil (SJKT) with 400 smartboards and associated digital learning tools. The initiative, backed by a RM5 million funding, seeks to guarantee that Tamil national-type schools are included in the nation’s rapid digital transformation efforts.

Integration of Artificial Intelligence and Emerging Technologies

The deepening integration of artificial intelligence (AI), machine learning (ML), and other emerging technologies into educational platforms represents a transformative growth driver for the Southeast Asian edtech market. AI-enabled capabilities including adaptive content delivery, automated assessment and feedback systems, intelligent tutoring interfaces, and predictive learning analytics are fundamentally enhancing the value proposition of edtech solutions by enabling levels of personalization and instructional effectiveness that traditional educational approaches cannot achieve. These technological advancements are particularly significant in the Southeast Asian context, where diverse linguistic landscapes, varying curriculum standards across countries, and wide disparities in teacher-to-student ratios create acute demand for scalable solutions that can adapt to individual learner needs. The region’s growing pool of technology talent and the increasing availability of cloud computing infrastructure are further lowering the barriers to AI integration, enabling edtech providers of all sizes to incorporate sophisticated algorithmic capabilities into their product offerings. IMARC Group predicts that the South East Asia artificial intelligence market is projected to reach USD 17,229.4 Million by 2033.

Market Restraints:

What Challenges the South East Asia Edtech Market is Facing?

Persistent Digital Divide and Infrastructure Gaps

Despite significant progress in expanding digital connectivity, Southeast Asia continues to grapple with substantial disparities in internet access and digital infrastructure quality between urban and rural areas. Many remote and economically disadvantaged communities across the region lack the reliable broadband connectivity and device availability necessary to fully participate in technology-enabled education, limiting the addressable market for edtech solutions and constraining the scalability of digital learning initiatives in underserved populations.

Fragmented Regulatory and Curriculum Frameworks

The Southeast Asian edtech market operates across multiple national jurisdictions with distinct regulatory environments, curriculum standards, language requirements, and data protection frameworks. This fragmentation creates significant operational complexity for edtech providers seeking to scale across countries, requiring substantial investment in content localization, regulatory compliance, and market-specific product adaptation that elevates barriers to entry and limits the pace at which successful solutions can be replicated across the broader regional market.

Limited Digital Literacy Among Educators and Institutional Resistance

The effective integration of educational technology into instructional practice is constrained by varying levels of digital literacy and technological readiness among educators across the region. Many teachers, particularly in public school systems and rural educational institutions, lack adequate training and ongoing professional development support to effectively leverage digital tools in their teaching methodologies, resulting in underutilization of deployed technology resources and limiting the pedagogical impact of edtech investments.

Competitive Landscape:

The South East Asia edtech market is characterized by a highly fragmented and intensely competitive landscape comprising a diverse array of participants ranging from early-stage startups to mature regional platforms and global technology corporations. The market features innumerable edtech companies operating across the region, with Singapore serving as the primary hub for startup headquarters and cross-border expansion, while Indonesia and Vietnam function as key innovation and adoption markets. Competitive dynamics are shaped by product differentiation strategies centered on AI-powered personalization capabilities, content localization depth, hybrid learning delivery models, and mobile-first user experience design. The market has witnessed increasing consolidation activity as better-funded platforms seek to acquire complementary capabilities and expand their geographic footprint, while selective venture capital investment continues to favor companies demonstrating proven business models and sustainable unit economics over early-stage experimentation.

South East Asia Edtech Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Sectors Covered | Preschool, K-12, Higher Education, Others |

| Types Covered | Hardware, Software, Content |

| Deployment Modes Covered | Cloud-based, On-premises |

| End Users Covered | Individual Learners, Institutes, Enterprises |

| Countries Covered | Indonesia, Thailand, Singapore, Philippines, Vietnam, Malaysia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South East Asia Edtech Market Report

The South East Asia edtech market size was valued at USD 12.26 Billion in 2025.

The South East Asia edtech market is expected to grow at a compound annual growth rate of 14.52% from 2026-2034 to reach USD 41.52 Billion by 2034.

The K-12 sector held the largest market share of 57% in 2025, driven by the region’s extensive school-age population, intensifying classroom digitalization efforts, and strong parental investment in supplementary digital education resources.

Key factors driving the South East Asia edtech market include favorable demographic dynamics with a large youth population, expanding digital connectivity and smartphone penetration, proactive government digital education policies, and the deepening integration of artificial intelligence and adaptive learning technologies into educational platforms.

Major challenges include the persistent digital divide between urban and rural areas with uneven internet infrastructure, fragmented regulatory and curriculum frameworks across multiple national jurisdictions, limited digital literacy among educators in public school systems, high content localization costs for multilingual markets, and institutional resistance to transitioning from traditional pedagogical approaches to technology-enabled instruction.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)