South East Asia Luxury Fashion Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, End User, and Country, 2026-2034

South East Asia Luxury Fashion Market Summary:

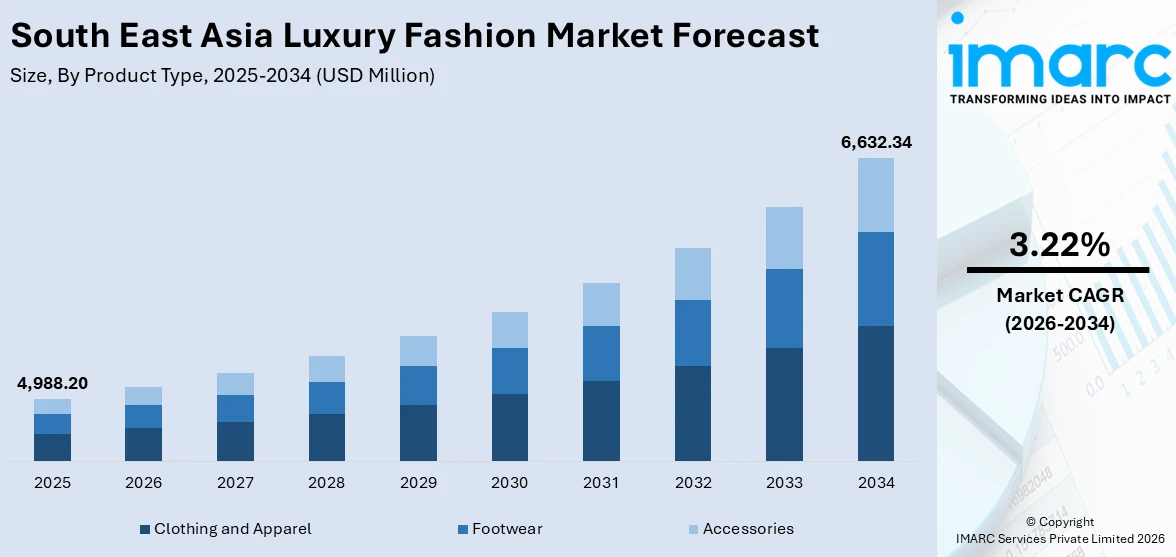

The South East Asia luxury fashion market size was valued at USD 4,988.20 Million in 2025 and is projected to reach USD 6,632.34 Million by 2034, growing at a compound annual growth rate of 3.22% from 2026-2034.

The market is driven by rising disposable incomes, rapid urbanization, and an expanding affluent middle-class population across the region. Growing digital penetration, evolving consumer preferences toward premium and exclusive fashion products, and increasing brand consciousness among younger demographics are further propelling demand. Additionally, the flourishing tourism industry and the proliferation of luxury retail channels are creating a favorable environment for sustained expansion of the South East Asia luxury fashion market share.

Key Takeaways and Insights:

- By Product Type: Clothing and apparel dominate the market with a share of 48% in 2025, driven by strong consumer preference for premium designer garments and increasing demand for exclusive collections.

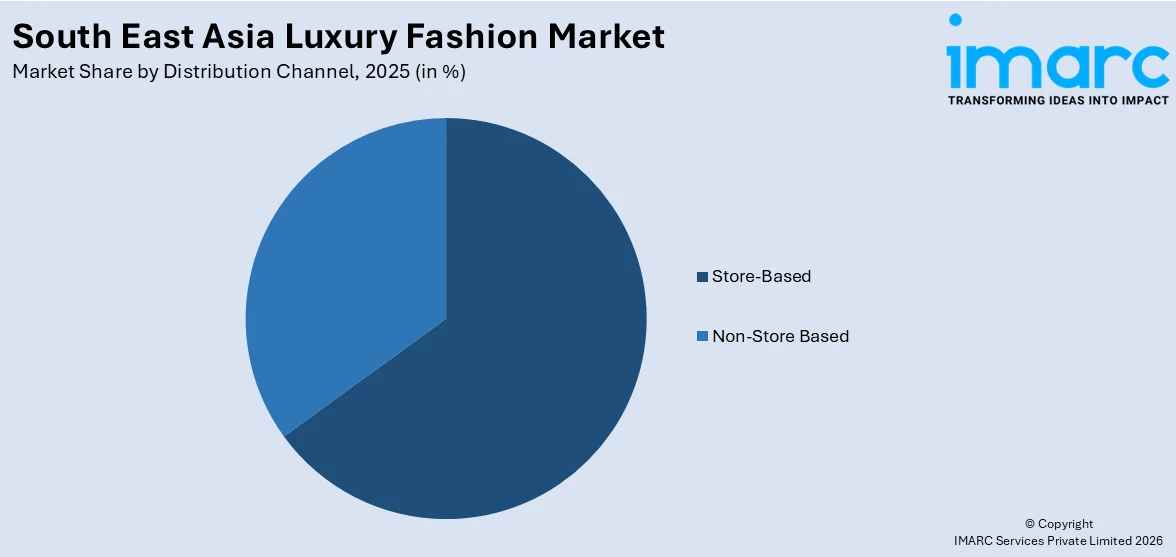

- By Distribution Channel: Store-based leads the market with a share of 65% in 2025, owing to the experiential nature of luxury shopping and personalized in-store services offered by flagship boutiques.

- By End User: Women represent the largest segment with a market share of 55% in 2025, driven by strong inclination toward fashion-forward luxury products and higher spending propensity on premium accessories.

- Key Players: The South East Asia luxury fashion market exhibits a moderately fragmented competitive landscape, with established global luxury conglomerates competing alongside premium regional players across diverse product segments and distribution channels, leveraging brand heritage, digital innovation, and localized marketing strategies to capture market share.

To get more information on this market Request Sample

The South East Asia luxury fashion market is experiencing robust growth, underpinned by a confluence of economic, cultural, and technological factors reshaping the regional consumer landscape. Rapid urbanization and the steady expansion of the affluent middle class across key economies are elevating aspirations for premium and exclusive fashion products. In October 2024, Siam Piwat Group, in collaboration with global fashion media WWD, hosted the “SOUTHEAST ASIA – Luxury’s New Future” event to position Bangkok as a global fashion and luxury hub, signalling intensified industry focus on the region’s potential. The increasing penetration of digital platforms and social media is amplifying brand visibility, enabling consumers to engage with luxury fashion houses and driving purchasing decisions. Furthermore, the region's thriving tourism ecosystem, particularly in hub cities, is stimulating luxury retail traffic and cross-border shopping. Evolving lifestyle preferences, a growing emphasis on personal expression through fashion, and heightened brand consciousness among younger demographics are collectively creating a dynamic and favorable demand environment for luxury fashion across South East Asia.

South East Asia Luxury Fashion Market Trends:

Rise of Digital-First Luxury Engagement and Social Commerce

The South East Asia luxury fashion market is witnessing a significant shift toward digital-first consumer engagement, with brands increasingly leveraging social commerce platforms, livestream shopping, and immersive digital experiences to connect with younger, tech-savvy audiences. In November 2025, Lazada celebrated a 170,000‑strong brand ecosystem at its LazMall Brand Gala in Singapore, underscoring how premium and branded sellers are driving quality‑led online commerce across Southeast Asia and reinforcing digital platforms as key channels for luxury and high‑end fashion engagement. Consumers across the region are embracing mobile-driven purchasing journeys, blending online discovery with seamless checkout experiences.

Growing Consumer Preference for Sustainable and Ethical Luxury

Sustainability is emerging as a defining trend within the South East Asia luxury fashion landscape, as increasingly conscious consumers demand transparency in sourcing, production, and environmental impact. According to reports, in 2025, Jing Daily reported that 60% of Singaporean consumers now prefer sustainable brands, particularly younger buyers valuing ethics and transparency alongside aesthetics, highlighting the growing regional appetite for responsible luxury. Luxury brands are responding by integrating eco-friendly materials, adopting circular fashion models, and highlighting ethical craftsmanship in their collections. The rise of certified pre-owned luxury platforms is gaining traction among value-conscious younger buyers seeking premium fashion with reduced environmental footprints. This shift toward conscious consumption is reshaping brand positioning strategies and influencing product development across the regional luxury ecosystem.

Expansion of Experiential Retail and Hyper-Localized Brand Strategies

Luxury fashion brands are increasingly adopting experiential retail concepts and hyper-localized strategies to deepen consumer engagement across South East Asia. As per sources, other immersive flagship store openings in Bangkok’s luxury district included Louis Vuitton’s “The Place Bangkok” and Dior’s “Gold House,” which combined café experiences with art and craftsmanship to enrich the in-store experience. Moreover, flagship stores are being reimagined as immersive cultural destinations featuring interactive displays, curated art installations, and personalized concierge services that elevate the in-store experience beyond traditional retail. Simultaneously, brands are tailoring design narratives and marketing campaigns to reflect the rich cultural diversity of the region, incorporating locally inspired motifs and collaborating with regional artisans to create exclusive collections resonating with distinct aesthetic sensibilities across diverse markets.

Market Outlook 2026-2034:

The South East Asia luxury fashion market is poised for steady revenue growth over the forecast period, supported by rising affluence, expanding digital infrastructure, and deepening brand penetration across key regional economies. Revenue is expected to be driven by sustained consumer demand for premium and exclusive fashion offerings, the proliferation of omnichannel retail strategies, and the growing influence of social commerce. The emergence of tier-two cities as luxury retail destinations and increasing participation of younger, digitally connected consumers are anticipated to create additional revenue streams, positioning the market for consistent expansion. The market generated a revenue of USD 4,988.20 Million in 2025 and is projected to reach a revenue of USD 6,632.34 Million by 2034, growing at a compound annual growth rate of 3.22% from 2026-2034.

South East Asia Luxury Fashion Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Clothing and Apparel |

48% |

|

Distribution Channel |

Store-Based |

65% |

|

End User |

Women |

55% |

Product Type Insights:

- Clothing and Apparel

- Jackets and Coats

- Skirts

- Shirts and T-Shirts

- Dresses

- Trousers and Shorts

- Denim

- Underwear and Lingerie

- Others

- Footwear

- Accessories

- Gems and Jewellery

- Belts

- Bags

- Watches

Clothing and apparel dominate with a market share of 48% of the total South East Asia luxury fashion market in 2025.

Clothing and apparel hold the leading position in the South East Asia luxury fashion market, commanding the largest share of overall revenue. This dominance is attributed to the enduring consumer preference for premium designer garments that serve as primary expressions of personal style and social status. According to reports, fashion clothing was the most frequently purchased luxury category among Southeast Asian luxury consumers, ahead of beauty, jewellery and accessories. The region's growing affluent population increasingly seeks high-quality fabrics, impeccable tailoring, and exclusive collections from established fashion houses, driving sustained demand across formal, casual, and occasion-wear categories within the luxury clothing segment.

The influence of global fashion weeks, regional celebrity endorsements, and digital style influencers is amplifying aspirational demand for luxury apparel across South East Asian markets. Consumers are increasingly drawn to limited-edition releases and seasonal collections that offer exclusivity and distinctiveness. The expansion of luxury brand retail footprints in metropolitan centers and the growing accessibility through curated online platforms are collectively reinforcing the segment's dominant position within the broader luxury fashion market across the region.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Store-Based

- Non-Store Based

Store-based leads with a share of 65% of the total South East Asia luxury fashion market in 2025.

The store-based commands the leading position in the South East Asia luxury fashion market, driven by the inherently experiential nature of luxury shopping. Consumers in the region place significant value on personalized in-store services, including dedicated styling consultations, product authentication assurance, and tactile experience of engaging with premium materials before making purchase decisions. In December 2025, Swiss maison Piaget opened its new “Radiance” flagship boutique at ION Orchard in Singapore, a concept store blending heritage, immersive design, and local cultural elements to deepen customer engagement.

The continued investment by luxury fashion houses in expanding their physical retail networks across emerging luxury hubs underscores the channel's strategic importance. Pop-up stores, brand experience centers, and concierge-led shopping events are further enriching the in-store proposition. While digital channels are growing rapidly, the store-based segment retains its leading position due to the emotional and sensory dimensions of the luxury purchase journey, where ambiance, exclusivity, and face-to-face brand interaction remain critical differentiators for discerning consumers.

End User Insights:

- Men

- Women

- Unisex

Women exhibit a clear dominance with a 55% share of the total South East Asia luxury fashion market in 2025.

Women represent the leading end-user category in the South East Asia luxury fashion market, reflecting the strong and growing purchasing power of female consumers across the region. Women demonstrate a pronounced inclination toward premium fashion products spanning clothing, footwear, and accessories, driven by aspirations for self-expression, social distinction, and alignment with evolving global fashion trends. The expanding participation of women in the professional workforce and entrepreneurial ventures has significantly enhanced their discretionary spending capacity on luxury goods.

Luxury fashion brands are increasingly tailoring their product portfolios and marketing narratives to resonate with the preferences and cultural sensibilities of female consumers in South East Asia. From curated capsule collections to exclusive collaborations, the industry is actively catering to diverse style preferences and occasions. The influence of social media platforms, fashion influencers, and digital content creators in shaping purchasing decisions further amplifies the segment's leading position, as women remain the primary drivers of aspirational luxury fashion consumption across the region.

Country Insights:

- Indonesia

- Thailand

- Singapore

- Philippines

- Vietnam

- Malaysia

- Others

Indonesia is a major market for luxury fashion in South East Asia, driven by a growing affluent consumer base and urbanization trends in key cities. The growing popularity of social media and digital platforms is also enhancing brand awareness for the younger generation, while the development of luxury retail spaces in key cities is creating a conducive environment for the growth of luxury fashion retail.

Thailand is a major hub for luxury fashion in South East Asia, with a growing base driven by its successful tourism industry and existing retail landscape in key cities. The country attracts high-net-worth individuals from around the world, and they prefer luxury retail spaces, while the affluent population within the country is showing a growing affinity for luxury fashion brands.

Singapore is an established luxury fashion hub in South East Asia, with the advantage of being an established financial center with high levels of consumer expenditure. Singapore offers an advanced luxury retail environment with world-class shopping districts and luxury flagship store propositions. The cosmopolitan consumer base and high levels of tourism ensure an extremely buoyant demand environment for luxury fashion products.

The Philippines is an emerging luxury fashion market in South East Asia, driven by improving disposable income levels and an expanding base of young, fashion-oriented consumers. The trend of digital connectivity and social media usage is enhancing the aspirational buying behavior of consumers, and the creation of luxury retail environments in metropolitan cities is improving accessibility to luxury fashion products for the discerning Filipino consumer.

Vietnam has been observing rising demand for luxury fashion products, attributed to the high growth rate of the economy and the emergence of the affluent middle-class segment with rising purchasing power. The young and technology-savvy population of Vietnam has shown high potential for luxury fashion products, with the country's growing retail infrastructure and brand awareness among aspirational groups indicating high growth potential for the luxury fashion market.

Malaysia plays a significant role in the South East Asia luxury fashion market, with the country benefiting from its diverse and multicultural consumer landscape with rising purchasing power. Malaysia has a well-developed retail infrastructure, with the country offering premium shopping experiences and offering duty-free benefits for luxury shoppers. In addition, the rising digital landscape and fashion awareness among the young population are boosting the demand for luxury fashion products.

Others in South East Asian markets collectively contribute to the regional luxury fashion landscape, driven by gradual economic development and increasing exposure to global fashion trends. Rising urbanization, growing internet penetration, and expanding middle-class populations across these emerging economies are creating new opportunities for luxury fashion brands seeking to establish presence and capture demand in previously underserved consumer segments.

Market Dynamics:

Growth Drivers:

Why is the South East Asia Luxury Fashion Market Growing?

Rising Affluence and Expansion of the Middle and Upper-Class Consumer Base

The South East Asia luxury fashion market is benefiting substantially from the region's sustained economic development, driving an expansion of the middle and upper-class consumer base across major economies. Rapid industrialization, growing employment opportunities in high-value sectors, and increasing household incomes are elevating consumer purchasing power and shifting spending patterns toward premium and aspirational products. According to reports, in 2025, Singapore was reported to be home to over 240,000 millionaires, with luxury brand sales in the city‑state expected to rise, underlining how growing affluence continues to fuel premium spending in key Southeast Asian hubs. As disposable incomes rise, a growing segment of the population is transitioning from mass-market fashion to luxury offerings, seeking superior craftsmanship, exclusivity, and brand prestige throughout the region.

Flourishing Tourism Industry and Growth of Luxury Travel Retail

The thriving tourism sector across South East Asia serves as a powerful catalyst for the luxury fashion market, with key destinations attracting high-net-worth individuals and international travelers who actively seek premium shopping experience during their visits. As per sources, in November 2025, Condé Nast Traveler ranked Bangkok among the world’s best shopping cities, highlighting its growing global appeal and drawing increased retail‑tourism traffic to luxury malls and designer boutiques. Major cities across the region have established themselves as luxury retail hubs, offering world-class shopping infrastructure featuring flagship stores, designer boutiques, and duty-free luxury outlets. The convergence of leisure travel and luxury shopping is driving significant retail traffic with brands capitalizing through exclusive travel-retail collections.

Increasing Urbanization and Infrastructure Development Supporting Premium Retail Expansion

Accelerating urbanization across South East Asian economies is creating concentrated consumer markets with enhanced infrastructure that supports luxury fashion retail expansion. The development of premium shopping malls, mixed-use lifestyle destinations, and integrated luxury retail districts in rapidly growing urban centers is providing brands with high-quality physical retail environments to showcase their collections. As per sources, ICONSIAM’s ICONLUXE added Balenciaga, Fendi, Loewe, and Loro Piana, expanding its luxury precinct to over 25,000 sqm, hosting 30+ flagship brands and reinforcing Bangkok’s high-end retail dominance. This urban transformation is fostering aspirational consumer lifestyles, increasing exposure to international fashion trends, and enabling luxury brands to establish strategically positioned retail touchpoints that cater to the region's expanding urban affluent population.

Market Restraints:

What Challenges the South East Asia Luxury Fashion Market is Facing?

Proliferation of Counterfeit Products Undermining Brand Trust

The widespread availability of counterfeit luxury fashion products across South East Asia remains a significant restraining factor, eroding brand equity and consumer trust. The region's extensive informal retail networks and growth of unregulated online marketplaces have facilitated distribution of imitation goods, making it increasingly challenging for consumers to distinguish between authentic and counterfeit products.

Price Sensitivity and Economic Disparities Across Regional Markets

Despite rising affluence in certain segments, significant income disparities persist across South East Asian economies, limiting the addressable consumer base for luxury fashion products. A substantial portion of the population remains price-sensitive, prioritizing essential expenditures over discretionary luxury purchases. Economic fluctuations and currency volatility across different countries further constrain uniform market expansion.

Regulatory and Import Duty Barriers Impacting Luxury Retail Pricing

Complex regulatory frameworks and elevated import duties imposed on luxury goods across several South East Asian markets contribute to increased retail prices, reducing affordability and limiting consumer access. Varying customs policies, taxation structures, and trade regulations across the region create operational complexities for luxury fashion brands seeking to establish or expand their retail presence effectively.

Competitive Landscape:

The South East Asia luxury fashion market features a moderately fragmented competitive landscape characterized by the presence of established global luxury conglomerates alongside emerging premium regional players. Market participants are employing diverse strategies encompassing brand heritage reinforcement, digital innovation, and localized marketing approaches to strengthen their competitive positioning. Key competitive differentiators include product exclusivity, omnichannel retail integration, and personalized customer engagement. The market is witnessing intensifying competition through the expansion of flagship retail networks, strategic celebrity and influencer partnerships, and investment in experiential retail concepts. The growing emphasis on sustainability credentials and digital commerce capabilities is further shaping competitive dynamics, as brands seek to capture the evolving preferences of the region's increasingly discerning and digitally connected luxury fashion consumers.

Recent Developments:

- In November 2025, Italian luxury leather brand BONAVENTURA opened its first Southeast Asian flagship store at Central Park, Bangkok. The largest store globally, it features exclusive Vanity Bags, bespoke personalization services, and immersive Italian craftsmanship, marking Thailand as a strategic hub for BONAVENTURA’s regional expansion.

- In March 2024, Louis Vuitton opened Louis Vuitton The Place Bangkok at Gaysorn Amarin, marking its sixth store in Thailand and strengthening its Southeast Asian presence. The flagship spans four floors, combining dining, café, retail, and exhibition spaces, offering immersive luxury experiences while Thailand becomes the country with the most Louis Vuitton stores in the region.

South East Asia Luxury Fashion Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered |

|

| Distribution Channels Covered | Store-Based, Non-Store Based |

| End Users Covered | Men, Women, Unisex |

| Countries Covered | Indonesia, Thailand, Singapore, Philippines, Vietnam, Malaysia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South East Asia Luxury Fashion Market Report

The South East Asia luxury fashion market size was valued at USD 4,988.20 Million in 2025.

The South East Asia luxury fashion market is expected to grow at a compound annual growth rate of 3.22% from 2026-2034 to reach USD 6,632.34 Million by 2034.

Clothing and apparel product type held the largest South East Asia luxury fashion market share, driven by strong consumer preference for premium designer garments, the influence of global fashion trends, and increasing demand for exclusive collections.

Key factors driving the South East Asia luxury fashion market include rising disposable incomes and expanding affluent middle class, digital transformation and proliferation of online luxury retail channels, and the flourishing tourism industry boosting luxury travel retail.

Major challenges include the proliferation of counterfeit products undermining brand trust, significant price sensitivity and economic disparities across regional markets, complex regulatory and import duty barriers impacting luxury retail pricing, varying infrastructure development across countries, and limited brand awareness in tier-two and tier-three cities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)