South East Asia Private Equity Market Size, Share, Trends and Forecast by Fund Type and Country, 2026-2034

South East Asia Private Equity Market Summary:

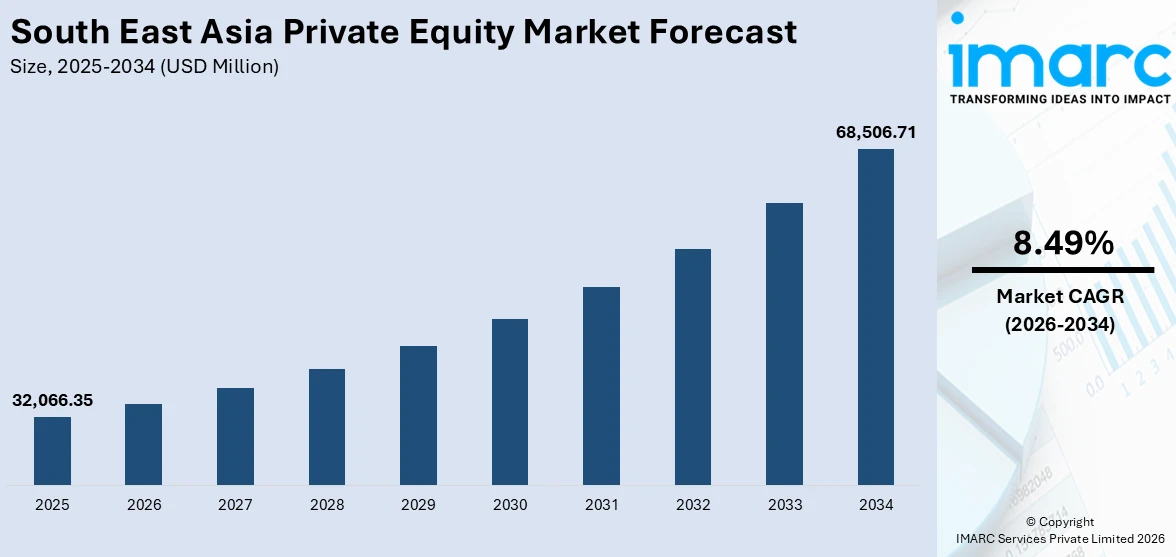

The South East Asia private equity market size was valued at USD 32,066.35 Million in 2025 and is projected to reach USD 68,506.71 Million by 2034, growing at a compound annual growth rate of 8.49% from 2026-2034.

South East Asia's private equity market is underpinned by a rapidly expanding digital economy, a youthful and increasingly affluent consumer base, and strong government-led initiatives to attract foreign capital. The region's diverse economies, ranging from Singapore's established financial hub to high-growth frontier markets, offer investors a broad spectrum of risk-return profiles across multiple fund types. Rising institutional interest in digital infrastructure, fintech, healthcare, and sustainable energy continues to channel capital into the region, strengthening overall South East Asia private equity market share.

Key Takeaways and Insights:

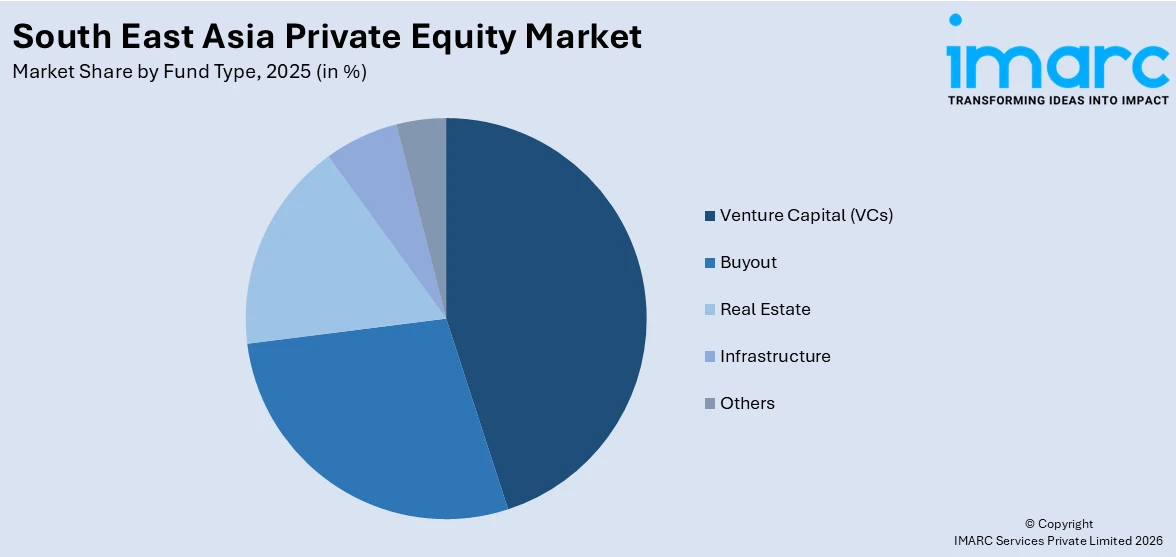

- By Fund Type: Venture capital (VCs) dominates the market with a share of 44.7% in 2025, owing to the region's thriving startup ecosystem, rapid digital adoption, and strong investor appetite for high-growth technology companies in fintech, e-commerce, and healthtech.

- By Country: Singapore leads the market with a share of 61.4% in 2025. This dominance is driven by the city-state's world-class financial infrastructure, transparent regulatory environment, and its position as the preferred base for global and regional private equity fund managers.

- Key Players: Key players drive the South East Asia private equity market by deploying capital across high-growth sectors, fostering portfolio company value creation, and leveraging regional networks to identify scalable opportunities. Their focus on digital transformation, operational improvement, and diversified exit strategies strengthens investor confidence and sustains deal flow across the region.

To get more information of this market Request Sample

The South East Asia private equity market is experiencing a pivotal transition toward value creation-led investing, as general partners increasingly prioritize sectors with structural demand tailwinds over opportunistic dealmaking. Digital infrastructure has emerged as a primary capital allocation theme, reflecting the region's accelerating technological transformation and the growing need for scalable, policy-supported platforms. Singapore continues to anchor the regional ecosystem, attracting a disproportionate share of private equity capital due to its stable regulatory environment, transparent legal framework, and well-established financial services infrastructure. Consumer, technology, media, telecommunications, and healthcare remain the primary sectors underpinning long-term portfolio strategy across the region. Meanwhile, the rising prominence of private credit and infrastructure funds is meaningfully reshaping capital allocation approaches, broadening the investable universe and offering limited partners a more diversified range of return profiles.

South East Asia Private Equity Market Trends:

Rise of Digital Infrastructure as a Primary Investment Theme

Digital infrastructure has emerged as the defining investment theme within the South East Asia private equity market, driven by soaring demand for data centers, telecommunications towers, and cloud computing platforms. The rapid expansion of artificial intelligence applications and digital financial services is fueling unprecedented demand for scalable, energy-efficient infrastructure. Governments across the region are actively supporting this transition through digital economy frameworks and investment facilitation programs. The alignment of private equity capital with government-backed digitalization strategies is creating durable, long-term investment opportunities across multiple markets.

Growing Prominence of Private Credit and Alternative Asset Classes

Private credit has gained significant traction as an alternative asset class within the South East Asia private equity market, reflecting both borrowers' need for flexible financing and investors' search for yield in a competitive deal environment. As traditional equity markets face valuation pressures and exit challenges, limited partners are increasingly allocating to credit strategies that offer more predictable return profiles. The establishment of dedicated private credit vehicles by major institutional investors in late 2024, including Temasek's formation of a SGD 10 Billion private credit entity in December 2024, underscores the structural nature of this trend.

Sector Diversification Beyond Traditional Technology Investments

South East Asia's private equity landscape is undergoing meaningful sector diversification, with investors expanding beyond pure-play technology to incorporate healthcare, energy transition, and consumer services. Healthcare dealmaking has grown substantially, driven by rising demand for quality medical services across aging populations and underserved communities. Renewable energy and natural resources are attracting increased capital as governments accelerate decarbonization commitments. This diversification reflects a broader maturation of the regional market, with general partners adopting more balanced portfolio strategies that reduce concentration risk and capture secular growth across multiple economic sectors.

Market Outlook 2026-2034:

The South East Asia private equity market is poised for sustained long-term growth, supported by robust macroeconomic fundamentals, deepening capital markets, and expanding investable universe across multiple sectors and geographies. The region's collective GDP growth trajectory, underpinned by strong domestic consumption, manufacturing diversification, and digital transformation, creates a highly conducive environment for private capital deployment. Improving exit pathways through secondary transactions, strategic trade sales, and a gradually recovering IPO market are expected to enhance capital recycling over the forecast period. Rising interest from Middle Eastern sovereign wealth funds and global institutional investors is further broadening the regional investor base, providing additional capital depth. Looking ahead, digital infrastructure and renewable energy are expected to remain the primary beneficiaries of private equity capital, while Indonesia, Vietnam, Malaysia, and the Philippines present compelling growth markets for deployment. The market generated a revenue of USD 32,066.35 Million in 2025 and is projected to reach a revenue of USD 68,506.71 Million by 2034, growing at a compound annual growth rate of 8.49% from 2026-2034.

South East Asia Private Equity Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Fund Type |

Venture Capital (VCs) |

44.7% |

|

Country |

Singapore |

61.4% |

Fund Type Insights:

Access the comprehensive market breakdown Request Sample

- Buyout

- Venture Capital (VCs)

- Real Estate

- Infrastructure

- Others

Venture Capital (VCs) dominates with a market share of 44.7% of the total South East Asia private equity market in 2025.

Venture capital investment across South East Asia is fueled by the region's dynamic startup ecosystem and one of the world's fastest-growing digital economies. The rapid proliferation of fintech platforms, e-commerce enablers, and health technology companies has created a rich pipeline of early and growth-stage investment opportunities. Major urban centers including Singapore, Jakarta, and Ho Chi Minh City have emerged as innovation hubs attracting both local and international venture capital managers. Government programs supporting startup incubation, entrepreneurship, and digital skills development further reinforce venture capital's structural role within the regional private equity landscape.

The fintech sector consistently attracts the largest share of venture capital activity, driven by a large unbanked and underbanked population presenting compelling opportunities for digital financial services providers. The scalability of technology-enabled business models across the region's diverse markets continues to validate the venture capital investment thesis. Deep tech, artificial intelligence infrastructure, and life sciences are increasingly attracting dedicated venture capital interest, reflecting the ecosystem's maturation beyond consumer internet toward more sophisticated, capital-intensive, and high-barrier technology sectors with meaningful long-term value creation potential.

Country Insights:

- Indonesia

- Thailand

- Singapore

- Philippines

- Vietnam

- Malaysia

- Others

Singapore represents the leading segment with a 61.4% share of the total South East Asia Private Equity market in 2025.

The dominance of Singapore in the South East Asia private equity market is a reflection of its unique combination of strengths that are unmatched in the region. Its transparent legal system, robust rule of law, widely recognized regulatory systems, and talent pool have enabled the country to become the preferred domicile for the vast majority of the region’s fund managers and their investment vehicles. The Monetary Authority of Singapore’s forward-looking support for the asset management industry, including its variable capital company regimes, has enabled the country to attract an ever-growing number of global private equity firms to establish or expand their operations in the country.

In addition to its position as a fund domicile, Singapore also attracts direct investments into its own market, including sectors such as digital infrastructure, healthcare, education, and real estate, which also adds to its share of the regional deal flow. Several Singapore-related institutional investors also have a significant presence in the regional deal flow, acting as limited partners as well as co-investors. Singapore’s connection to the global capital markets, as well as its position as a gateway for investors interested in the broader Southeast Asian economies, adds to its position at the heart of the regional private equity landscape. In the future, its continued investments in smart city infrastructure, financial services innovation, and data infrastructure will ensure its position at the top of the market through the forecast period, despite the increasing interest in Indonesia, Vietnam, and Malaysia from the international general partner community.

Market Dynamics:

Growth Drivers:

Why is the South East Asia Private Equity Market Growing?

Rapid Digital Economy Expansion and Technology-Driven Deal Flow

Southeast Asia's digital economy represents one of the most significant structural growth drivers underpinning the region's private equity market. The convergence of high smartphone penetration, a young and digitally native population, and increasing internet connectivity has created fertile ground for technology-enabled businesses across e-commerce, fintech, logistics, and software-as-a-service verticals. General partners are attracted by the scale of opportunity presented by a market of over 680 million consumers undergoing simultaneous economic development and digital transformation. Investment interest has expanded beyond consumer internet into enterprise software, AI infrastructure, and deep technology, broadening the investable universe for private equity fund managers. Additionally, the maturation of the first generation of Southeast Asian unicorns has created a self-reinforcing ecosystem where successful exits validate the regional investment thesis, drawing additional global capital into the market.

Favorable Demographics and Rising Middle-Class Consumption

Southeast Asia's demographic profile represents a powerful long-term driver for private equity investment, offering a growing pool of productive workers, consumers, and entrepreneurs across the region's key markets. Countries such as Indonesia, the Philippines, and Vietnam are home to large, youthful populations with rising incomes and rapidly evolving consumption patterns, creating sustained demand for healthcare, financial services, consumer goods, and education. The region's burgeoning middle class, which is expected to represent hundreds of millions of consumers over the coming decade, is drawing private equity capital into consumer-oriented sectors that benefit from both volume growth and premiumization trends. Indonesia attracted USD 55.3 Billion in foreign direct investment in 2024, reflecting international confidence in the country's consumption-driven economic model. Private equity managers are capitalizing on this demographic dividend by building portfolios of scalable businesses that serve middle-market consumers, particularly in markets where formal financial services and quality healthcare remain underpenetrated. This broad consumer opportunity creates a complementary investment dynamic alongside technology-focused strategies, supporting overall deal activity and portfolio diversification across the regional private equity market.

Strong Institutional Capital Inflows and Sovereign Wealth Fund Participation

The South East Asia private equity market has benefited materially from a sustained increase in institutional capital participation, including significant allocations from Middle Eastern sovereign wealth funds, Japanese institutional investors, and global pension funds seeking exposure to the region's growth premium. This broadening of the limited partner base has provided meaningful support to fundraising activity and enabled the formation of larger, more diversified funds capable of executing complex transactions. The participation of institutional capital also brings governance improvements, operational expertise, and global networks that enhance the quality of portfolio company management and the credibility of the regional private equity ecosystem. Singapore's role as a regional financial hub further facilitates capital aggregation, with the Monetary Authority of Singapore's supportive regulatory architecture enabling fund managers to efficiently structure and deploy cross-border investment strategies across the diverse markets of Southeast Asia.

Market Restraints:

What Challenges the South East Asia Private Equity Market is Facing?

Challenging Exit Environment and Prolonged Portfolio Holding Periods

One of the most persistent challenges confronting the South East Asia private equity market is the difficulty in achieving timely and value-accretive exits. The region's capital markets infrastructure remains relatively underdeveloped compared to more mature markets, with IPO activity constrained by thin secondary market liquidity and limited institutional investor depth. Trade sales, while increasingly prevalent, are often subject to extended negotiation timelines and valuation gaps between buyers and sellers. Aging portfolios have accumulated across the regional private equity industry, with general partners holding assets for longer than originally anticipated while awaiting improved exit conditions. This dynamic constrains capital recycling, limits distributions to limited partners, and creates pressure on fund performance metrics.

Geopolitical Uncertainty and Macroeconomic Volatility

The South East Asia private equity market operates in a geopolitical environment characterized by significant uncertainty, including trade policy shifts, regional territorial disputes, and evolving dynamics between major global powers. The introduction of US tariffs in early 2025 created immediate disruption to deal-making activity, with total private equity investment value in Southeast Asia declining sharply in the first half of 2025 as investors adopted a more cautious stance. Valuation gaps widened as buyers and sellers struggled to reach agreement on fair value in an environment of elevated macroeconomic uncertainty. Currency volatility across regional markets adds a further layer of complexity to cross-border investment and return calculations. General partners must now devote substantial analytical resources to assessing tariff exposure and supply chain vulnerabilities within their portfolio companies, adding friction to deal execution and portfolio management processes.

Regulatory Fragmentation and Operational Complexity Across Markets

Southeast Asia's institutional diversity presents a significant operational challenge for private equity fund managers seeking to deploy capital consistently across the region's ten member states. Each jurisdiction operates under distinct legal frameworks, tax regimes, foreign investment restrictions, and corporate governance standards, requiring specialized local expertise and legal counsel to navigate effectively. Fund structures that work efficiently in Singapore may face substantial complications when applied to investment activity in Indonesia, Vietnam, or Myanmar due to sector-specific ownership limitations, capital repatriation restrictions, and varying interpretations of regulatory requirements. This fragmentation raises the cost of doing business and limits the ability of fund managers to execute pan-regional strategies at scale. Smaller and mid-market private equity firms, in particular, face disproportionate compliance burdens that can constrain their competitive positioning relative to larger, better-resourced global managers with dedicated legal and compliance infrastructure.

Competitive Landscape:

The South East Asia private equity market is characterized by a competitive environment with global fund managers, regional specialists, and sector specialists. Global fund managers with a dedicated strategy in the Asia Pacific region have strengthened their presence in the region, using their international network and large fund sizes to compete in the region. Regional specialists are benefiting from their local knowledge, established network, and the ability to operate in a complex and challenging environment. One notable trend is the integration of private equity and private credit strategies, with the major managers in the private equity industry launching a wide range of products to provide a comprehensive solution to the market. Specialist funds in the healthcare, technology, and infrastructure sectors are also on the rise, a testament to the sophistication of the general partners and limited partners in the region. Competition is high in the region, and fund managers are differentiating themselves in the market through their value creation and exit track record.

South East Asia Private Equity Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fund Types Covered | Buyout, Venture Capital (VCs), Real Estate, Infrastructure, Others |

| Countries Covered | Indonesia, Thailand, Singapore, Philippines, Vietnam, Malaysia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South East Asia Private Equity Market Report

The South East Asia private equity market size was valued at USD 32,066.35 Million in 2025.

The South East Asia private equity market is expected to grow at a compound annual growth rate of 8.49% from 2026-2034 to reach USD 68,506.71 Million by 2034.

Venture capital (VCs) dominated the market with a share of 44.7%, driven by the region's thriving startup ecosystem, rapid digital economy expansion, and strong investor appetite for high-growth technology companies across fintech, e-commerce, and healthtech sectors.

Key factors driving the South East Asia private equity market include the region's rapid digital economy expansion, favorable demographics and rising middle-class consumption, strong institutional capital inflows from sovereign wealth funds, and increasing dealmaking activity in digital infrastructure and renewable energy sectors.

Major challenges include a difficult exit environment with limited IPO market depth, geopolitical uncertainty and trade policy volatility impacting deal-making confidence, regulatory fragmentation across the region's diverse jurisdictions, fundraising challenges linked to lower distributions to limited partners, and elevated competition for quality assets driving valuation pressures.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)