South Korea Antibody-Drug Conjugate (ADC) Market Size, Share, Trends and Forecast by Component, Target, Application, End User, and Region, 2026-2034

South Korea Antibody-Drug Conjugate (ADC) Market Summary:

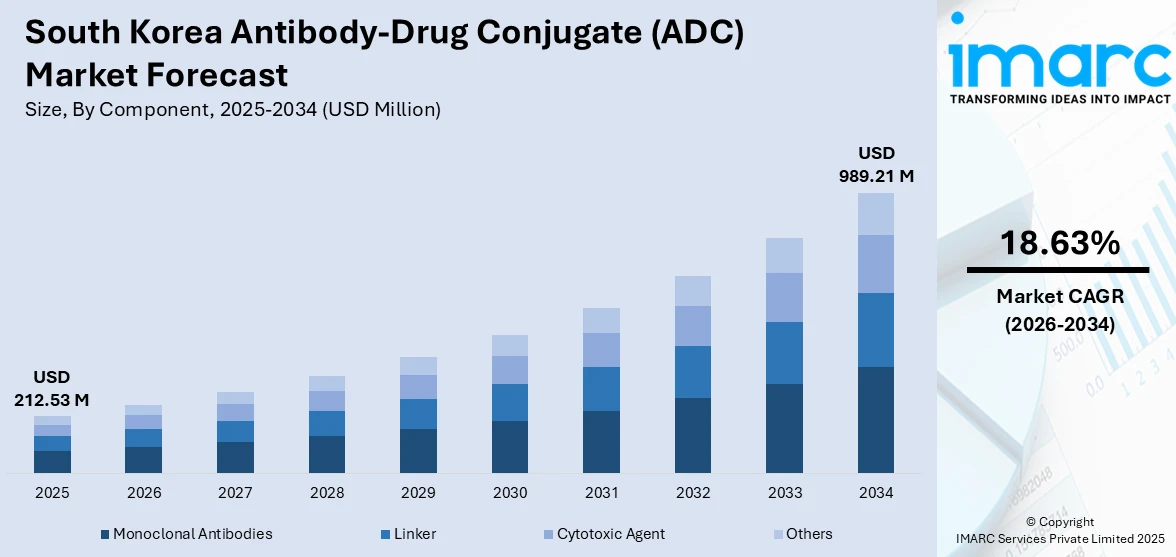

The South Korea antibody-drug conjugate (ADC) market size was valued at USD 212.53 Million in 2025 and is projected to reach USD 989.21 Million by 2034, growing at a compound annual growth rate of 18.63% from 2026-2034.

The South Korea antibody-drug conjugate market is advancing rapidly as targeted oncology therapies gain prominence within the country’s healthcare framework. Growing demand for precision medicine, expanding clinical trial activity, and strengthened biopharmaceutical infrastructure are accelerating market momentum. Rising cancer incidence, increased government support for innovative drug development, and deepening global partnerships are reinforcing the market’s trajectory, positioning South Korea as an influential participant in the evolving ADC landscape.

Key Takeaways and Insights:

- By Component: Monoclonal antibodies dominate the market with a share of 48.3% in 2025, driven by their critical role as the targeting backbone in ADC therapies, enabling selective delivery of cytotoxic payloads to cancer cells while minimizing systemic toxicity across therapeutic applications.

- By Target: Antibody-small-molecule drug conjugates lead the market with a share of 39.7% in 2025, owing to their superior pharmacokinetic properties, enhanced tumor penetration capabilities, and well-established clinical validation across multiple oncology indications in the South Korean healthcare system.

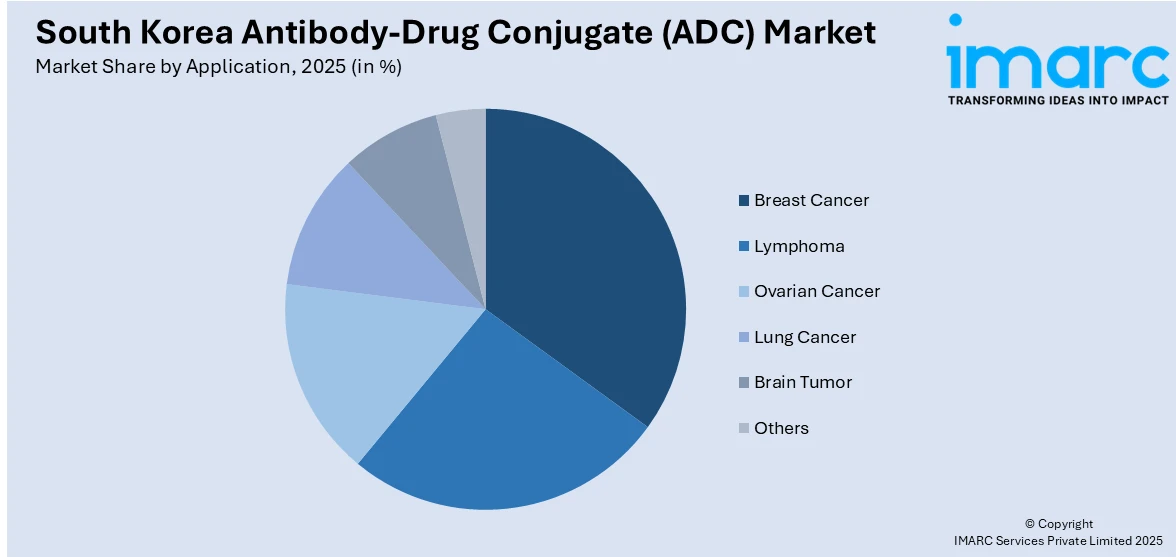

- By Application: Breast cancer holds the largest segment with a share of 31.4% in 2025, reflecting the high incidence of breast cancer among South Korean women, expanded ADC approvals for HER2-positive and HER2-low subtypes, and growing clinical adoption of next-generation conjugate therapies.

- By End User: Hospitals represent the leading segment with a share of 42.6% in 2025, supported by comprehensive oncology infrastructure, integrated multidisciplinary treatment teams, and established infusion capabilities that enable the safe administration of complex ADC regimens to cancer patients.

- By Region: Seoul Capital Area exhibits a clear dominance in the market with 58.9% share in 2025, driven by the concentration of major tertiary hospitals, leading cancer research centers, advanced clinical trial infrastructure, and a dense population base that supports high patient volumes and treatment accessibility.

- Key Players: Key players drive the South Korea ADC market by advancing proprietary conjugation platforms, expanding clinical pipelines, strengthening contract manufacturing capabilities, and forging strategic global licensing partnerships to accelerate innovative cancer treatment development and commercialization across diverse oncology indications.

To get more information on this market Request Sample

The South Korea antibody-drug conjugate market is gaining substantial traction as the country strengthens its position as a global oncology innovation hub. The rising prevalence of cancer remains a central catalyst, with approximately 292,000 new cancer cases projected in the country in 2024 according to the Korea National Cancer Incidence Database, underscoring the urgent demand for targeted therapeutic solutions. Government-led initiatives, including the establishment of the National Bio Committee in May 2025 to bolster global competitiveness in novel drug and advanced biopharmaceutical technologies, are accelerating ADC research and development. The country’s advanced clinical trial infrastructure, with Seoul consistently ranking among the top global cities for pharmaceutical company-led clinical trials, provides a fertile ground for ADC validation. Expanding reimbursement frameworks under the national health insurance system, coupled with growing investments in biomanufacturing capabilities, are supporting broader ADC accessibility. Deepening partnerships between domestic biotech firms and multinational pharmaceutical companies are further catalyzing pipeline expansion, reinforcing the South Korea antibody-drug conjugate (ADC) market share.

South Korea Antibody-Drug Conjugate (ADC) Market Trends:

Expansion of Domestic ADC Platform Technologies

South Korean biotech firms are rapidly building proprietary ADC development platforms that integrate antibody engineering, linker chemistry, and payload optimization. Companies are leveraging patient-derived cell models and big data-driven target discovery to design precision conjugates for cancers with high unmet medical needs. In October 2025, AimedBio, a Samsung Medical Center spin-off, secured a licensing deal worth up to USD 991 Million with Boehringer Ingelheim for a novel tumor-targeted ADC candidate, underscoring the growing global recognition of South Korean ADC innovation capabilities and supporting the South Korea antibody-drug conjugate (ADC) market growth.

Growing Integration of ADC Manufacturing Infrastructure

South Korea is emerging as a significant ADC manufacturing base, with leading contract development and manufacturing organizations investing in dedicated conjugation facilities. The convergence of large-scale antibody production expertise with specialized ADC capabilities is positioning the country as a competitive global CDMO destination. In January 2025, Samsung Biologics extended its collaboration with LigaChem Biosciences for ADC services at its new dedicated ADC facility equipped with a 500-liter reactor, spanning late discovery to development and conjugation, strengthening the domestic ADC manufacturing ecosystem.

Accelerating Regulatory Reforms for Faster ADC Approvals

The Korean Ministry of Food and Drug Safety is streamlining drug approval processes to facilitate quicker market entry for innovative cancer therapies, including ADCs. Regulatory modernization efforts are reducing review timelines and enhancing transparency for biopharmaceutical applicants. Effective from January 2025, the MFDS implemented a comprehensive overhaul of its new drug approval system, introducing dedicated review teams of 10 to 15 specialists per application and targeting completion of the approval process from 420 to 295 days, significantly accelerating patient access to novel ADC treatments.

Market Outlook 2026-2034:

The South Korea antibody-drug conjugate market is poised for sustained expansion through the forecast period, driven by accelerating clinical adoption of targeted oncology therapies and deepening biopharmaceutical innovation. Expanding indications for existing ADCs across breast cancer, lung cancer, and hematologic malignancies are expected to broaden the addressable patient population. Government strategies aimed at positioning South Korea among the top five global biopharmaceutical powers, coupled with investments in advanced manufacturing infrastructure, are reinforcing long-term market confidence. Strengthening cross-border licensing partnerships and increasing R&D investment in next-generation conjugation technologies will continue to propel innovation and market development. The market generated a revenue of USD 212.53 Million in 2025 and is projected to reach a revenue of USD 989.21 Million by 2034, growing at a compound annual growth rate of 18.63% from 2026-2034.

South Korea Antibody-Drug Conjugate (ADC) Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Monoclonal Antibodies |

48.3% |

|

Target |

Antibody-Small-Molecule Drug Conjugates |

39.7% |

|

Application |

Breast Cancer |

31.4% |

|

End User |

Hospitals |

42.6% |

|

Region |

Seoul Capital Area |

58.9% |

Component Insights:

- Monoclonal Antibodies

- Linker

- Cytotoxic Agent

- Others

Monoclonal antibodies dominate with a market share of 48.3% of the total South Korea antibody-drug conjugate (ADC) market in 2025.

Monoclonal antibodies serve as the foundational targeting component in ADC architecture, enabling precise recognition and binding to tumor-associated antigens on cancer cell surfaces. Their selectivity ensures that cytotoxic payloads are delivered directly to malignant cells while sparing healthy tissue, which is critical for therapeutic efficacy and safety. In South Korea, advancements in IgG-based monoclonal antibody engineering and bispecific antibody development are expanding the range of targetable cancer indications.

The increasing number of ADC approvals utilizing monoclonal antibody platforms is reinforcing segment dominance. HER2-directed monoclonal antibodies, in particular, have demonstrated significant clinical success in treating breast and gastric cancers, driving widespread adoption across South Korean oncology centers. The growing pipeline of next-generation monoclonal antibodies engineered for improved binding affinity, stability, and reduced immunogenicity is further strengthening the segment. Ongoing advancements in antibody humanization techniques and site-specific conjugation methods are enhancing therapeutic precision, enabling more effective payload delivery while minimizing off-target effects and supporting broader clinical integration.

Target Insights:

- Antibody-Protein Toxin Conjugates

- Antibody-Chelated Radionuclide Conjugates

- Antibody-Small-Molecule Drug Conjugates

- Antibody-Enzyme Conjugates

Antibody-small-molecule drug conjugates lead with a share of 39.7% of the total South Korea antibody-drug conjugate (ADC) market in 2025.

Antibody-small-molecule drug conjugates represent the most commercially validated ADC target class, combining monoclonal antibodies with potent small-molecule cytotoxic payloads to achieve targeted cancer cell destruction. Their well-characterized pharmacokinetic profiles, controllable drug-to-antibody ratios, and established manufacturing processes make them the preferred configuration for clinical development. In South Korea, the strong pipeline of topoisomerase I inhibitor-based ADCs is expanding the therapeutic reach of this target class. LigaChem Biosciences, a prominent South Korean ADC developer, secured partnerships with global companies including Amgen and Ono Pharmaceutical through its ConjuAll platform for small-molecule conjugate development.

The clinical success of small-molecule payload ADCs in addressing both solid tumors and hematologic malignancies is sustaining the segment's leading position. These conjugates offer favorable therapeutic windows that balance potent anticancer activity with manageable toxicity profiles, which is critical for patient compliance and treatment outcomes. The increasing regulatory acceptance of cleavable linker technologies optimized for small-molecule payloads is facilitating faster clinical translation. Continued refinement of drug-to-antibody ratio optimization and payload release mechanisms is further enhancing treatment specificity, enabling broader oncology applications across diverse cancer indications.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Lymphoma

- Ovarian Cancer

- Lung Cancer

- Breast Cancer

- Brain Tumor

- Others

Breast cancer holds the largest segment with a 31.4% share of the total South Korea antibody-drug conjugate (ADC) market in 2025.

Breast cancer represents the primary therapeutic application for ADCs in South Korea, reflecting both the high disease burden and the substantial clinical advances in HER2-targeted conjugate therapies. The expanding classification of treatable breast cancer subtypes, including HER2-positive, HER2-low, and triple-negative categories, has significantly broadened the eligible patient population for ADC interventions. The growing adoption of second-line and subsequent-line ADC treatments in clinical practice is reinforcing the segment’s dominance.

The regulatory expansion of ADC indications for breast cancer subtypes is a critical growth catalyst. Approvals enabling treatment of HER2-low breast cancer patients, who previously had limited targeted therapy options, have opened new treatment pathways and driven clinical uptake. The integration of ADCs into standard oncology protocols at major South Korean hospitals and cancer centers is further accelerating adoption. The five-year relative survival rate for cancer patients in South Korea reached 72.1 percent as reported by the Mistry of Health and Welfare and the Korea Central Cancer Registry, reflecting the country’s advanced treatment capabilities and reinforcing clinician confidence in prescribing innovative ADC therapies for breast cancer management.

End User Insights:

- Hospitals

- Specialized Cancer Centers

- Academic Research Institutes

- Biotechnology Companies

- Others

Hospitals exhibit a clear dominance with a 42.6% share of the total South Korea antibody-drug conjugate (ADC) market in 2025.

Hospitals constitute the principal end-user segment for ADC therapies in South Korea, driven by their comprehensive oncology departments, multidisciplinary treatment teams, and established infusion infrastructure necessary for administering complex biologic therapies. Major tertiary hospitals in the country integrate cancer centers within their organizational structure rather than operating them as separate entities, which facilitates seamless collaboration across specialties and accelerates clinical research. South Korea’s advanced hospital network supports high patient throughput for ADC treatments. Seoul ranked first globally as a clinical trial city for pharmaceutical company-led studies, reflecting the exceptional research and treatment capabilities of the country’s hospital system.

The national health insurance system’s coverage of approved oncology treatments further strengthens hospital-based ADC utilization by reducing financial barriers for patients seeking advanced therapies. Hospitals also serve as the primary sites for ADC clinical trials, enabling early patient access to investigational conjugate therapies. The Korea Drug Development Fund expanded its support from 78 new drug development projects in 2024 to 128 in 2025, with oncology accounting for 52 percent of total projects, reflecting the increasing clinical activity within hospital settings that is driving ADC adoption and establishing hospitals as the central delivery channel for targeted cancer treatments.

Regional Insights:

- Seoul Capital Area

- Yeongnam (Southeastern Region)

- Honam (Southwestern Region)

- Hoseo (Central Region)

- Others

Seoul Capital Area represents the leading region with a 58.9% share of the total South Korea antibody-drug conjugate (ADC) market in 2025.

The Seoul Capital Area commands the dominant regional share in the South Korea ADC market, underpinned by the concentration of the nation’s foremost tertiary hospitals, specialized cancer centers, and leading academic research institutions. The region houses major healthcare facilities including Seoul National University Hospital, Asan Medical Center, and Samsung Medical Center, which serve as primary hubs for ADC clinical adoption and research. The capital area’s dense population base ensures substantial patient volumes for oncology treatments.

The Seoul Capital Area benefits from an advanced clinical trial ecosystem that attracts global pharmaceutical companies seeking to validate ADC candidates in well-controlled research environments. The region’s integration of hospital-based cancer centers with academic research capabilities enables rapid translation of scientific discoveries into clinical practice, supporting faster ADC adoption. The presence of major biopharmaceutical headquarters, regulatory agencies, and investment firms within the capital region further enhances the market ecosystem.

Market Dynamics:

Growth Drivers:

Why is the South Korea Antibody-Drug Conjugate (ADC) Market Growing?

Rising Cancer Prevalence and Expanding Therapeutic Demand

The escalating burden of cancer across South Korea is a fundamental driver of ADC market expansion, creating sustained demand for advanced targeted therapies that offer improved efficacy and reduced systemic toxicity compared to conventional chemotherapy. The country’s aging population demographic structure, coupled with lifestyle-related risk factors, continues to push cancer incidence upward across multiple tumor types. Breast cancer, lung cancer, and colorectal cancer remain among the most frequently diagnosed malignancies, each representing significant opportunities for ADC therapeutic intervention. The expanding recognition of molecularly defined cancer subtypes, such as HER2-low breast cancer, is broadening the addressable patient population for conjugate therapies. South Korea projected approximately 292,221 new cancer cases in 2024 according to the Korea National Cancer Incidence Database, representing a continued upward trend that reinforces demand for innovative oncology treatments. The increasing five-year survival rates across cancer types further encourage adoption of advanced treatments that extend patient outcomes, driving sustained market growth.

Government-Led Biopharmaceutical Innovation Initiatives

The South Korean government has positioned biopharmaceutical development as a national strategic priority, implementing comprehensive policy frameworks and investment programs that directly benefit ADC research, development, and commercialization. Regulatory reforms aimed at streamlining drug approval processes, financial incentives for clinical trials, and infrastructure investments in biomanufacturing facilities are collectively strengthening the ADC ecosystem. The government's ambitious targets for pharmaceutical sector growth are creating a favorable environment for both domestic innovators and international partners. The National Bio Committee was established as an advisory body to enhance the country's global competitiveness in novel drug and advanced biopharmaceutical technology development, building on ongoing reforms targeting significant reduction of drug development timelines and associated costs. The government's Third Five-Year Comprehensive Plan for the Bio-Pharmaceutical Industry aims to place South Korea among the leading global pharmaceutical powers, catalyzing ADC innovation through enhanced public-private partnerships and expanded funding for translational oncology research.

Deepening Global Licensing Partnerships and Cross-Border Collaboration

South Korean biotech firms are expanding their presence in the antibody-drug conjugate space through licensing agreements with global pharmaceutical companies. These partnerships signal rising confidence in the country’s capabilities in linker technologies, payload development, and conjugation platforms. By collaborating with established multinational players, local companies gain financial backing, regulatory guidance, and access to global marketing channels. This support enables smoother clinical progression and broader international reach for ADC candidates. Growing cross-border collaboration is also enhancing research capabilities at home and elevating South Korea’s standing in the competitive global biopharmaceutical market.

Market Restraints:

What Challenges the South Korea Antibody-Drug Conjugate (ADC) Market is Facing?

High Manufacturing Complexity and Production Costs

The intricate manufacturing process of antibody-drug conjugates, which requires precise conjugation of monoclonal antibodies with cytotoxic payloads through specialized linker chemistry, imposes significant production costs and quality control challenges. Each production step demands strict compliance with current good manufacturing practice standards, specialized facilities, and advanced analytical capabilities. These complexities elevate the cost of ADC therapies, potentially limiting affordability and restricting broader patient access within the South Korean healthcare system.

Reimbursement and Pricing Pressures Under National Health Insurance

While the national health insurance system ensures broad healthcare coverage, the stringent reimbursement evaluation process for high-cost oncology therapies can delay patient access to newly approved ADC treatments. The Health Insurance Review and Assessment Service applies rigorous cost-effectiveness assessments that may restrict coverage scope or impose utilization limitations. These pricing pressures create uncertainty for pharmaceutical companies regarding commercial viability and may slow the rate of clinical adoption for innovative ADC therapies in the market.

Limited Domestic Clinical Trial Capacity for Complex Biologics

Despite South Korea’s strong overall clinical trial infrastructure, the specialized requirements for ADC trials, including biomarker-driven patient stratification, pharmacokinetic monitoring, and management of unique toxicity profiles, can strain existing resources. The relatively small domestic patient population for certain rare cancer subtypes may necessitate reliance on multinational trial designs, introducing additional regulatory and logistical complexities that can extend development timelines and increase costs for ADC sponsors.

Competitive Landscape:

The South Korea antibody-drug conjugate market features an increasingly dynamic competitive landscape characterized by the convergence of domestic biotech innovators and established multinational pharmaceutical companies. Competition is intensifying across the ADC value chain, from target discovery and antibody engineering through conjugation manufacturing and clinical commercialization. Domestic firms are differentiating through proprietary platform technologies, including novel linker-payload systems and patient-derived cell-based discovery approaches, while global players are leveraging established regulatory expertise and commercial distribution networks. Strategic alliances between Korean biotechs and international partners are reshaping competitive dynamics, enabling resource sharing and accelerating pipeline development. Contract development and manufacturing organizations are competing to capture growing outsourcing demand by expanding dedicated ADC production capabilities and offering integrated end-to-end services.

South Korea Antibody-Drug Conjugate (ADC) Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Million |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Components Covered |

Monoclonal Antibodies, Linker, Cytotoxic Agent, Others |

|

Targets Covered |

Antibody-Protein Toxin Conjugates, Antibody-Chelated Radionuclide Conjugates, Antibody-Small-Molecule Drug Conjugates, Antibody-Enzyme Conjugates |

|

Applications Covered |

Lymphoma, Ovarian Cancer, Lung Cancer, Breast Cancer, Brain Tumor, Others |

|

End Users Covered |

Hospitals, Specialized Cancer Centers, Academic Research Institutes, Biotechnology Companies, Others |

|

Regions Covered |

Seoul Capital Area, Yeongnam (Southeastern Region), Honam (Southwestern Region), Hoseo (Central Region), Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The South Korea antibody-drug conjugate (ADC) market size was valued at USD 212.53 Million in 2025.

The South Korea antibody-drug conjugate (ADC) market is expected to grow at a compound annual growth rate of 18.63% from 2026-2034 to reach USD 989.21 Million by 2034.

Monoclonal antibodies dominated the market with a share of 48.3%, driven by their essential role as the targeting backbone in ADC therapies enabling precise delivery of cytotoxic payloads to tumor cells across multiple cancer indications.

Key factors driving the South Korea antibody-drug conjugate (ADC) market include rising cancer prevalence, government biopharmaceutical innovation initiatives, expanding ADC indications, growing global licensing partnerships, advanced clinical trial infrastructure, and increasing investment in ADC manufacturing capabilities.

Major challenges include high manufacturing complexity and production costs, reimbursement and pricing pressures under the national health insurance system, limited domestic clinical trial capacity for specialized biologics, and supply chain dependencies for raw materials and specialized conjugation inputs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)