South Korea Bakery Products Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

South Korea Bakery Products Market Summary:

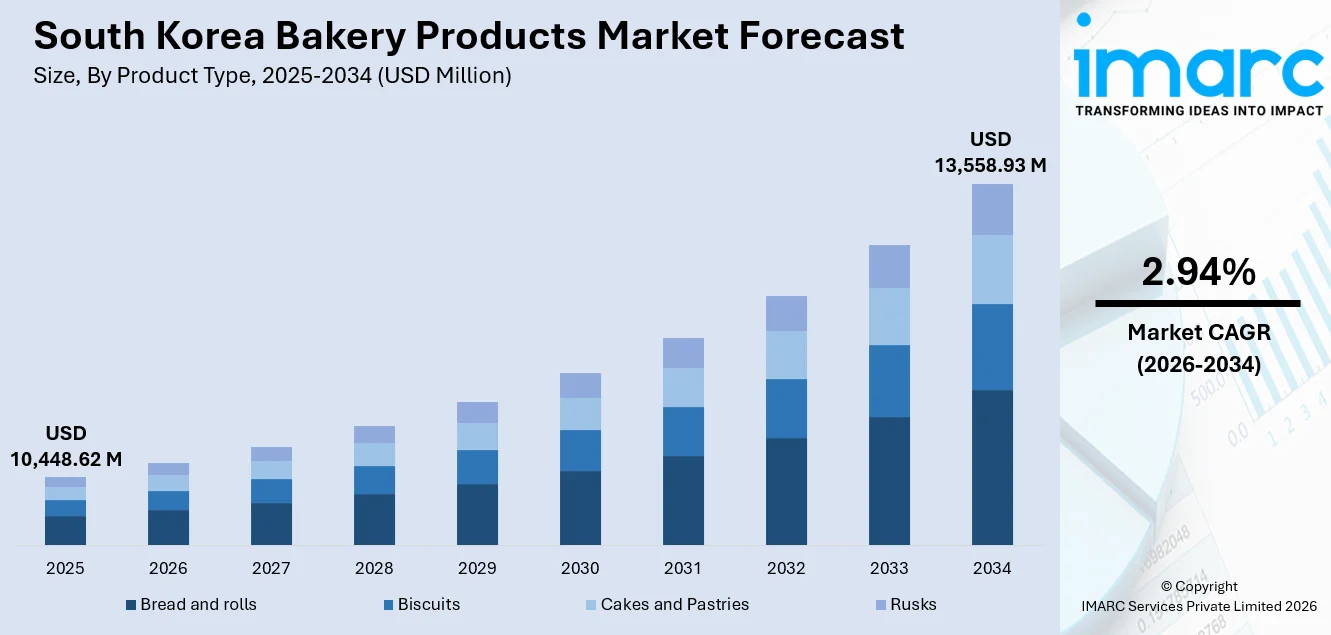

The South Korea bakery products market size was valued at USD 10,448.62 Million in 2025 and is projected to reach USD 13,558.93 Million by 2034, growing at a compound annual growth rate of 2.94% from 2026-2034.

The South Korea bakery products market is witnessing steady growth, supported by changing dietary habits, rising demand for convenient and premium baked goods, and the strong presence of organized retail, with bread and rolls leading consumption, supermarkets and hypermarkets dominating distribution, and urban regions such as the Seoul Capital Area driving market performance amid evolving consumer preferences and product innovation.

Key Takeaways and Insights:

- By Product Type: Bread and rolls dominate the market with a share of 39.8% in 2025, due to their role as daily staples, wide product variety, convenience for urban consumers, and strong availability across artisanal bakeries, in-store bakeries, and organized retail outlets.

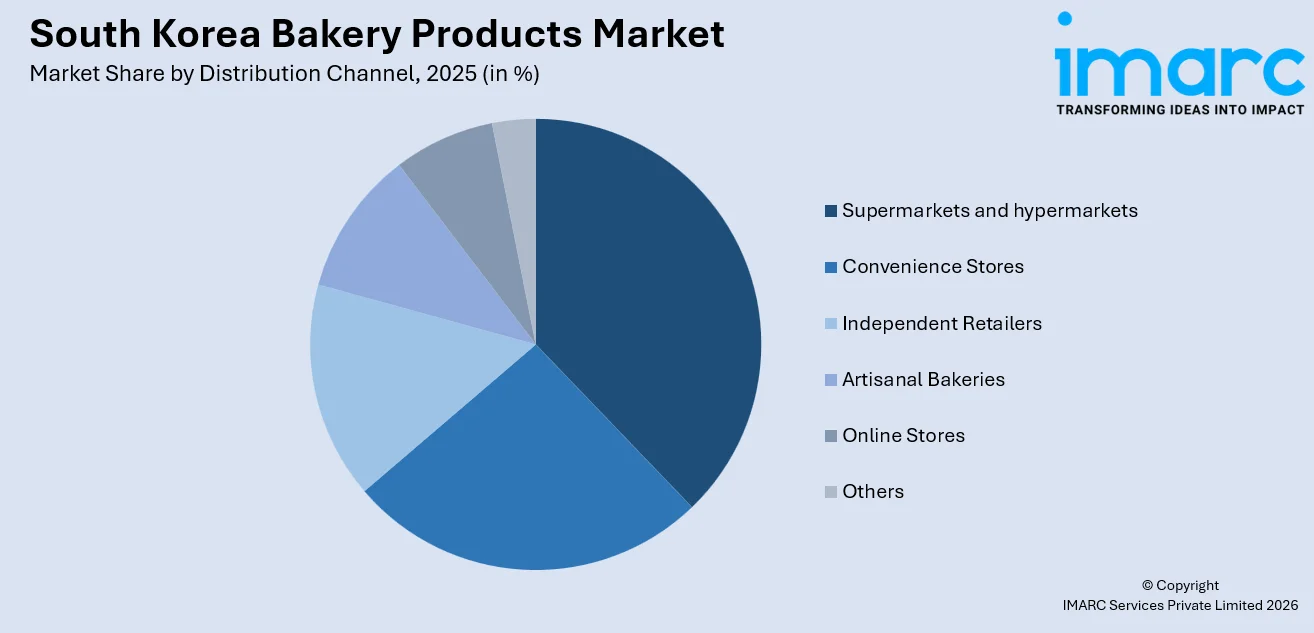

- By Distribution Channel: Supermarkets and hypermarkets lead the market with a share of 36.5% in 2025, because they offer one-stop shopping, strong in-store bakery presence, competitive pricing, frequent promotions, and broad product assortments appealing to household consumers.

- By Region: Seoul Capital Area comprises the largest region with 41.9% share in 2025, owing to high population density, higher disposable incomes, busy lifestyles, advanced retail infrastructure, and strong demand for both fresh and packaged bakery products.

- Key Players: The competitive landscape features a mix of large domestic manufacturers and artisanal bakery chains focusing on product innovation, premiumization, private-label expansion, and retail partnerships. Companies compete on freshness, quality, pricing, and brand loyalty while strengthening distribution networks and introducing differentiated offerings.

To get more information on this market Request Sample

The South Korea bakery products market is characterized by stable demand supported by changing consumption patterns, increased urbanization, and the growing integration of bakery items into daily meal routines. Consumers are showing a rising preference for high-quality, freshly prepared products as well as packaged baked goods with extended shelf life. Innovation in flavors, textures, and formulations, including reduced-sugar and functional variants, is shaping product development strategies. For instance, in January 2026, CU launched hot breads including burritos and low-sugar sausage breads, with coffee bundle discounts, targeting Korea’s ‘cur-bread’ trend as consumers pair bread with coffee for convenient, affordable morning meals at convenience stores. Furthermore, organized retail formats and in-store bakeries continue to influence purchasing behavior through improved accessibility and consistent quality standards. Regional demand remains concentrated in metropolitan areas where modern retail infrastructure and lifestyle-driven consumption are most pronounced. Moreover, competitive activity is intensifying as manufacturers and bakery chains invest in branding, operational efficiency, and supply chain optimization to maintain market relevance.

South Korea Bakery Products Market Trends:

Health-Focused Reformulations and Functional Breads

South Korea’s bakery products market is experiencing a notable shift toward health-oriented reformulations, with manufacturers introducing low-sugar, whole-grain, and fiber-enriched breads to meet growing consumer demand for nutritional value without sacrificing taste. These products appeal to health-conscious consumers seeking better alternatives to traditional bakery items, driven by rising public awareness of dietary impacts. Retailers and bakeries are expanding this segment, incorporating ingredients such as oats, seeds, and legumes, aligning product portfolios with broader wellness trends and lifestyle preferences.

Premiumization and Artisanal Offerings

Premium and artisanal bakery products are gaining traction as consumers increasingly value quality, craftsmanship, and unique flavor profiles. As such, in February 2025, Paris Baguette launched its premium health bread brand PARAN LABEL across Korea, using advanced fermentation and Nordic-inspired whole grains to align with slow-aging and healthy pleasure trends while improving taste, nutrition, and consumer perception of health-focused bakery products. Small-batch sourdough, specialty pastries, and gourmet loaves have emerged in both urban bakeries and retail chains, supported by heightened interest in food experiences. This trend reflects disposable income growth among key demographics and a willingness to pay for differentiated products. Bakery operators are leveraging premium ingredients and curated presentation to enhance perceived value and reinforce brand positioning in a competitive market landscape.

Convenience and Ready-to-Eat Bakery Innovation

Convenience-driven bakery products are expanding as consumers seek quick, portable options that fit modern lifestyles. Retailers are introducing ready-to-eat items such as filled buns, handheld sandwiches, and snackable pastries at convenience stores and supermarkets, targeting busy professionals and students. For example, in December 2025, Starbucks Korea’s Yoo Yong-wook Barbecue Two-Cut Beef Sandwich sold out on launch day at Reserve stores, becoming a top-selling item. Strong demand prompted store expansion, chef-led events, and limited-time promotions under the Tasty Journey collaboration program. These innovations often integrate cross-category appeal, pairing bakery products with beverages or meal solutions. Enhanced packaging, freshness retention technologies, and limited-time seasonal offerings further support market growth by increasing appeal and frequency of purchase among convenience-oriented shoppers.

Market Outlook 2026-2034:

The South Korea bakery products market is expected to advance steadily as consumer demand for convenience, premium offerings, and functional baked goods continues to evolve. Growth will also be supported by innovation in product formulation, expansion of online and delivery channels, and increasing investment in retail bakery experiences. For instance, in December 2025, South Korea’s SPC Group said Paris Baguette reached 700 global stores with a new Westfield London opening, highlighting rapid overseas growth, strong UK franchise performance, and ambitions to strengthen brand competitiveness across Europe’s bakery market. Similarly, urban lifestyle trends and rising disposable incomes are likely to bolster product consumption. Additionally, strategic collaborations between bakeries and specialty brands, along with digital engagement strategies, will contribute to market resilience and diversification in the coming years. The market generated a revenue of USD 10,448.62 Million in 2025 and is projected to reach a revenue of USD 13,558.93 Million by 2034, growing at a compound annual growth rate of 2.94% from 2026-2034.

South Korea Bakery Products Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Bread and Rolls |

39.8% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

36.5% |

|

Region |

Seoul Capital Area |

41.9% |

Product Type Insights:

- Biscuits

- Cookies

- Cream Biscuits

- Glucose Biscuits

- Marie Biscuits

- Non-Salt Cracker Biscuits

- Salt Cracker Biscuits

- Milk Biscuits

- Others

- Bread and Rolls

- Artisanal Bakeries

- In-Store Bakeries

- Packaged

- Cakes and Pastries

- Artisanal Bakeries

- In-Store Bakeries

- Packaged

- Rusks

- Artisanal Bakeries

- In-Store Bakeries

- Packaged

Bread and rolls dominate with a market share of 39.8% of the total South Korea bakery products market in 2025.

Bread and rolls represent the largest product category in the market, driven by their strong integration into daily dietary habits. These products are widely consumed as breakfast items, meal substitutes, and convenient snacks across households and urban consumers. Their versatility, compatibility with both Western-style and localized flavors, and consistent availability across retail formats support sustained demand. Manufacturers continue to diversify offerings to address varying preferences related to texture, portion size, and usage occasions.

The dominance of bread and rolls is further reinforced by continuous product innovation and premium positioning. Producers are increasingly focusing on improving freshness, shelf life, and sensory attributes to enhance consumer appeal. Seasonal launches, specialty formulations, and value-added variants strengthen category visibility and encourage repeat purchases. In addition, bread and rolls benefit from efficient production scalability and strong placement within organized retail and in-store bakery formats, supporting stable category leadership.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Convenience Stores

- Supermarkets and Hypermarkets

- Independent Retailers

- Artisanal Bakeries

- Online Stores

- Others

Supermarkets and hypermarkets lead the market with a share of 36.5% of the total South Korea bakery products market in 2025.

Supermarkets and hypermarkets constitute the leading distribution channel for bakery products in South Korea, supported by their extensive reach and high consumer footfall. These outlets provide a comprehensive assortment of fresh and packaged bakery items, enabling consumers to compare options conveniently during routine grocery shopping. The presence of in-store bakeries further enhances product freshness perception, driving impulse purchases and reinforcing the channel’s importance in everyday consumption patterns. Data from navigation platform Tmap Mobility shows that bakeries accounted for four of the top 10 most-searched restaurants during South Korea’s 2024 summer travel season.

Channel leadership is also supported by strong supply chain efficiency and pricing competitiveness. Supermarkets and hypermarkets leverage scale advantages to maintain consistent availability and promotional activity, strengthening consumer loyalty. Private-label bakery products contribute to value positioning, while standardized quality controls ensure reliability across locations. As retailers continue investing in upgraded bakery sections and improved merchandising, this channel is expected to remain central to market distribution dynamics.

Regional Insights:

- Seoul Capital Area

- Yeongnam (Southeastern Region)

- Honam (Southwestern Region)

- Hoseo (Central Region)

- Others

Seoul Capital Area represents the leading region with a 41.9% share of the total South Korea bakery products market in 2025.

The Seoul Capital Area represents the leading regional market for bakery products, supported by dense population concentration and advanced retail infrastructure. IGES states that Seoul Special Metropolitan City is South Korea’s capital and largest city, with an estimated population of about 9.6 million residents as of 2025. Likewise, high urbanization levels, fast-paced lifestyles, and strong demand for convenient food options underpin consistent consumption. The region benefits from widespread access to modern supermarkets, premium in-store bakeries, and specialty bakery chains, ensuring broad product exposure and frequent purchasing opportunities for consumers.

Regional dominance is further strengthened by higher average household spending capacity and strong receptiveness to new product launches. Consumers in the Seoul Capital Area are more inclined toward premium and differentiated bakery offerings, encouraging innovation and early adoption. The concentration of leading foodservice operators, retail headquarters, and logistics networks also supports efficient distribution and rapid market penetration, reinforcing the region’s sustained leadership in the national bakery products market.

Market Dynamics:

Growth Drivers:

Why is the South Korea Bakery Products Market Growing?

Convenience Store Bakery Expansion and Menu Innovation

Convenience stores in South Korea are increasingly diversifying bakery offerings to meet evolving consumer needs for ready-to-eat foods. Chains such as CU and GS25 have introduced a range of hot breads, burritos, and premium sandwiches positioned as meal alternatives, while also bundling items with beverages to boost sales. Major convenience store chains say private-brand bread now makes up over 20 percent of bakery sales, with CU’s PB share more than doubling from 9.4 percent in 2023 to 21 percent between January and September 2025. Likewise, enhanced product rotations and seasonal promotions improve foot traffic and strengthen the role of convenience formats in bakery distribution, reflecting changing lifestyle patterns and demand for accessible, quality bakery solutions.

Digital and Direct-to-Consumer Engagement

Digital engagement and direct-to-consumer channels are shaping the bakery products market as online platforms and delivery services gain prominence. Bakeries and retail brands are leveraging mobile apps, social media, and e-commerce partnerships to expand reach, offer pre-order options, and provide customized product promotions. Real-time consumer feedback and targeted marketing campaigns help businesses refine assortments and strengthen brand loyalty. As delivery infrastructure improves, the online segment is becoming a strategic growth channel for both fresh and packaged bakery products.

Collaborations with Health and Specialty Food Movements

Collaborations between traditional bakery brands and health-focused or specialty food initiatives are emerging as a distinguishing trend. Established franchises are partnering with nutrition experts or leveraging research to introduce breads with improved nutritional profiles, whole grains, and functional ingredients. These efforts address growing public interest in balanced diets and wellness without compromising sensory appeal. The result is an expanded presence of artisanal and thoughtfully formulated products that align with broader shifts toward health-conscious consumption within the bakery market. For instance, in February 2025, Shinsegae Food is introducing Paris-based BO&MIE to Korea with its first store in Gangnam, bringing artisanal French baking using stone-milled flour and natural sourdough as part of its strategy to strengthen its premium bakery business.

Market Restraints:

What Challenges the South Korea Bakery Products Market is Facing?

Rising Costs of Ingredients and Production

The South Korea bakery products market faces considerable pressure from rising input and production costs. Fluctuations in global wheat prices, increased expenses for dairy and specialty ingredients, and higher energy costs are compressing margins for both large-scale manufacturers and smaller artisanal producers. These cost pressures make it difficult to maintain competitive pricing without compromising quality. Smaller bakeries, in particular, may struggle to absorb rising operational costs, which can hinder expansion and limit product innovation.

Shifts in Dietary Preferences and Health Awareness

Changing consumer preferences toward low-carbohydrate, low-sugar, and gluten-free diets pose a challenge for traditional bakery products. As health consciousness grows, segments of the population are reducing consumption of conventional breads, cakes, and pastries in favor of alternatives perceived as healthier, such as fresh produce or functional foods. This shift requires manufacturers to invest in reformulation and new product development, which may increase R&D costs and extend time-to-market for health-oriented bakery offerings.

Intense Competition and Market Saturation

The South Korea bakery sector is highly competitive, with numerous domestic brands, artisanal bakeries, and international franchises vying for consumer attention. Market saturation, especially in urban centers, makes differentiation difficult and increases marketing and promotional expenses. Smaller operators often find it challenging to compete with large retail chains that benefit from economies of scale and extensive distribution networks. This competitive intensity can limit pricing power, reduce profitability, and constrain growth for mid-sized and emerging bakery brands.

Competitive Landscape:

The competitive landscape of the South Korea bakery products market is shaped by intense rivalry among large domestic manufacturers, established franchise bakery chains, and a dense base of independent artisanal operators. Branded players compete through standardized quality, nationwide store networks, and rapid product rollouts, while artisanal bakeries differentiate through craftsmanship, premium ingredients, and localized offerings. Meanwhile, organized retailers strengthen competition by expanding private-label bakery ranges and improving in-store bakery execution. Pricing pressure remains persistent due to frequent promotions and high store density, particularly in metropolitan areas. Moreover, digital ordering, delivery partnerships, and brand collaborations are increasingly used to defend market share and build consumer loyalty.

Recent Developments:

- In September 2025, The YouTuber Syuka opened his pop-up ETF Bakery in Seoul to sell salted butter rolls at 990 won which created a pricing dispute about bread. Local bakers reacted to customer praise of low prices by stating that their actual costs, which included labor expenses and imported wheat costs, made it impossible to compete with such low prices.

- In February 2025, Tim Hortons Korea, marking its third year, launches a “second phase” focused on localization, fresh in-store baking, menu diversification, and flagship store experiences. It plans to expand from 25 to 50 company-owned stores in 2026, ultimately targeting 150 within five years to strengthen market presence.

South Korea Bakery Products Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

|

|

Distribution Channels Covered |

Convenience Stores, Supermarkets and Hypermarkets, Independent Retailers, Artisanal Bakeries, Online Stores, Others |

|

Regions Covered |

Seoul Capital Area, Yeongnam (Southeastern Region), Honam (Southwestern Region), Hoseo (Central Region), Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the South Korea Bakery Products Market Report

The South Korea bakery products market size was valued at USD 10,448.62 Million in 2025.

The South Korea bakery products market is expected to grow at a compound annual growth rate of 2.94% from 2026-2034 to reach USD 13,558.93 Million by 2034.

Bread and rolls dominated the market with a share of 39.8%, reflecting their widespread consumption, versatility, and staple status in the country’s food culture.

Key factors driving the South Korea bakery products market include rising consumer demand for convenience foods, increasing urbanization, growing popularity of premium and artisanal baked goods, innovative product offerings, expanding café culture, and a surge in health-conscious and ready-to-eat bakery options.

Major challenges include high labor and ingredient costs, reliance on imported wheat, price sensitivity among consumers, competition from convenience stores and cafés, supply chain complexities, and pressure to balance affordability with premium quality in baked goods.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)