South Korea Digital Health Market Size, Share, Trends and Forecast by Type, Component, and Region, 2026-2034

South Korea Digital Health Market Size, Share, Trends & Forecast (2026-2034)

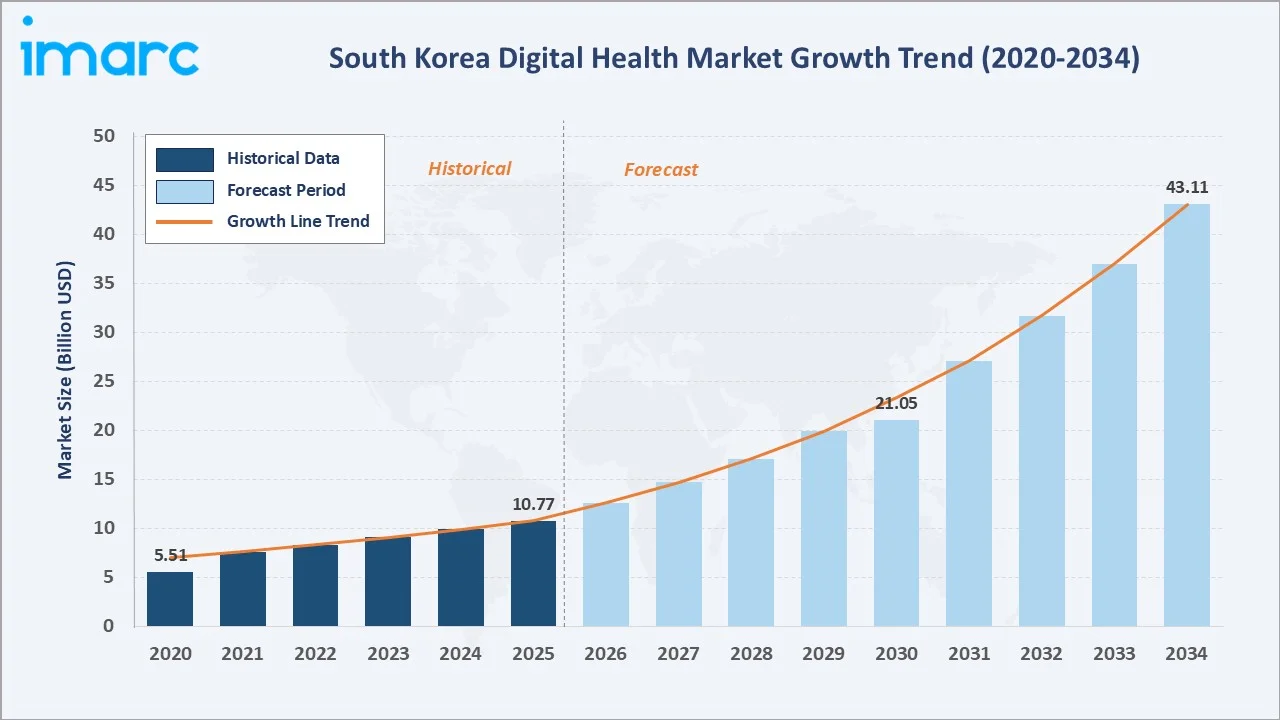

The South Korea digital health market size reached USD 10.77 Billion in 2025 and is projected to reach USD 43.11 Billion by 2034, exhibiting a CAGR of 14.34% during 2026-2034. Strong government digitization initiatives, rapid 5G deployment, AI integration in diagnostics, and growing demand for personalized remote healthcare are the primary forces driving growth.

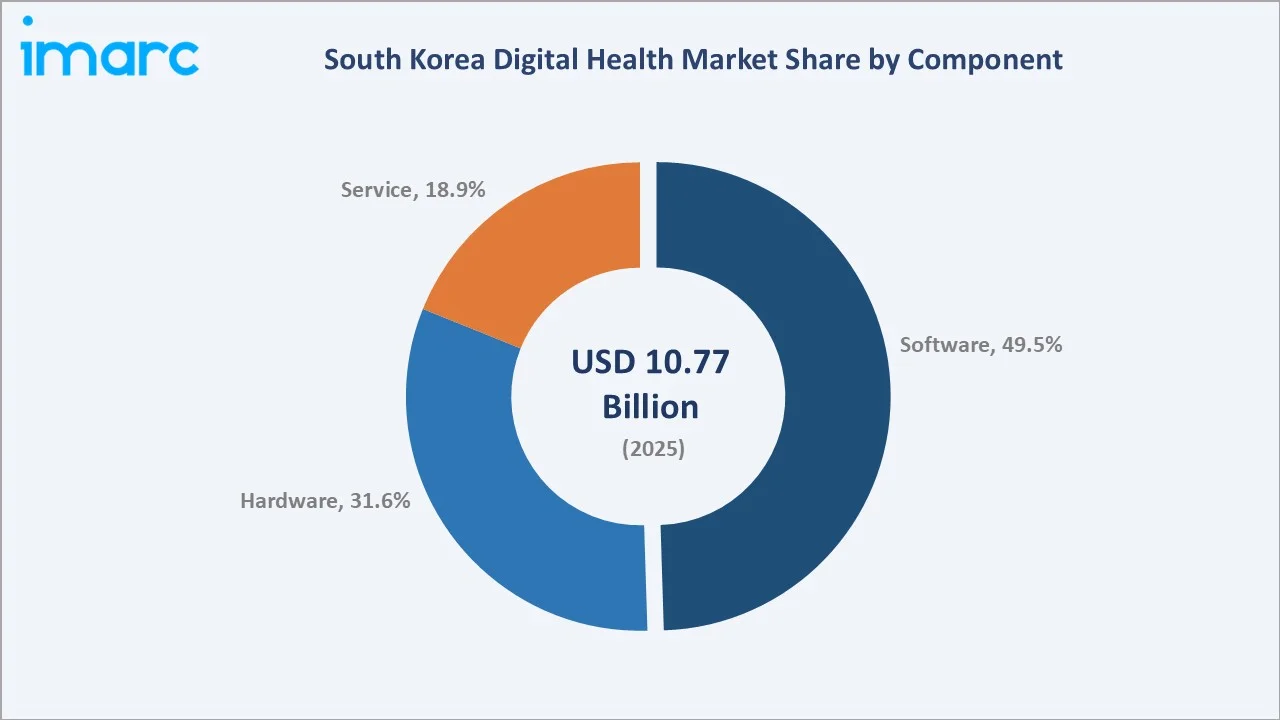

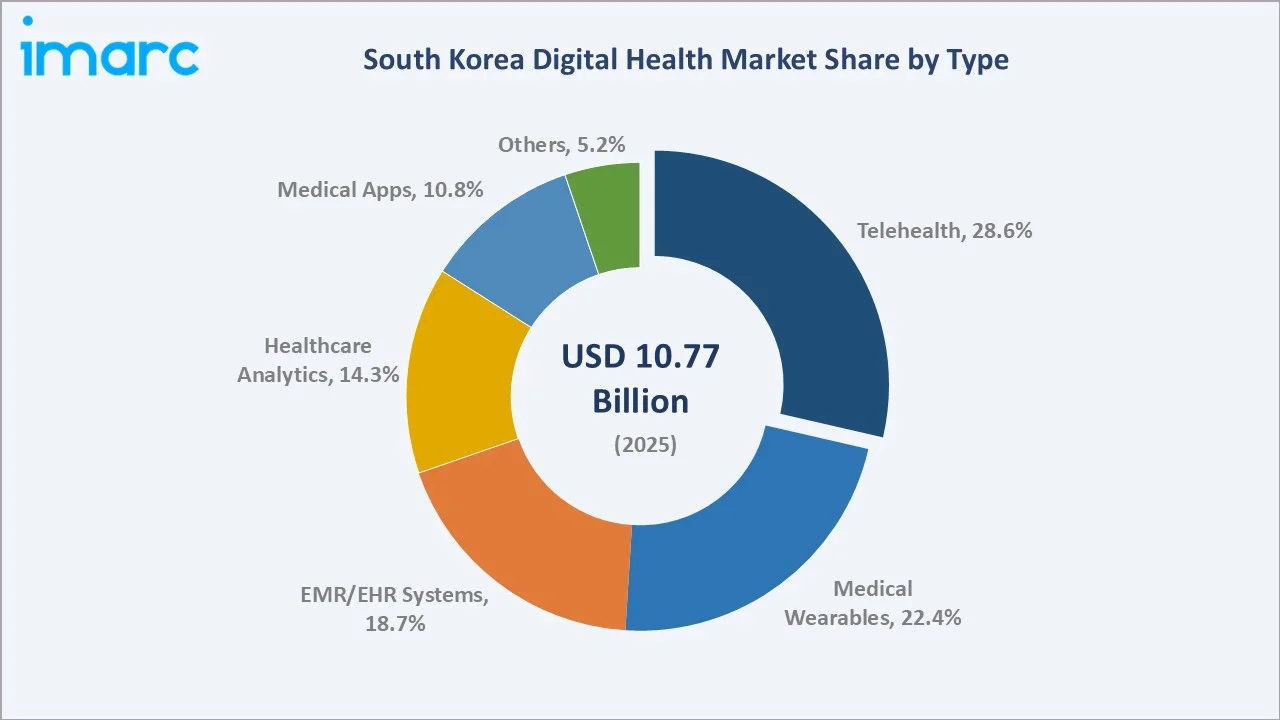

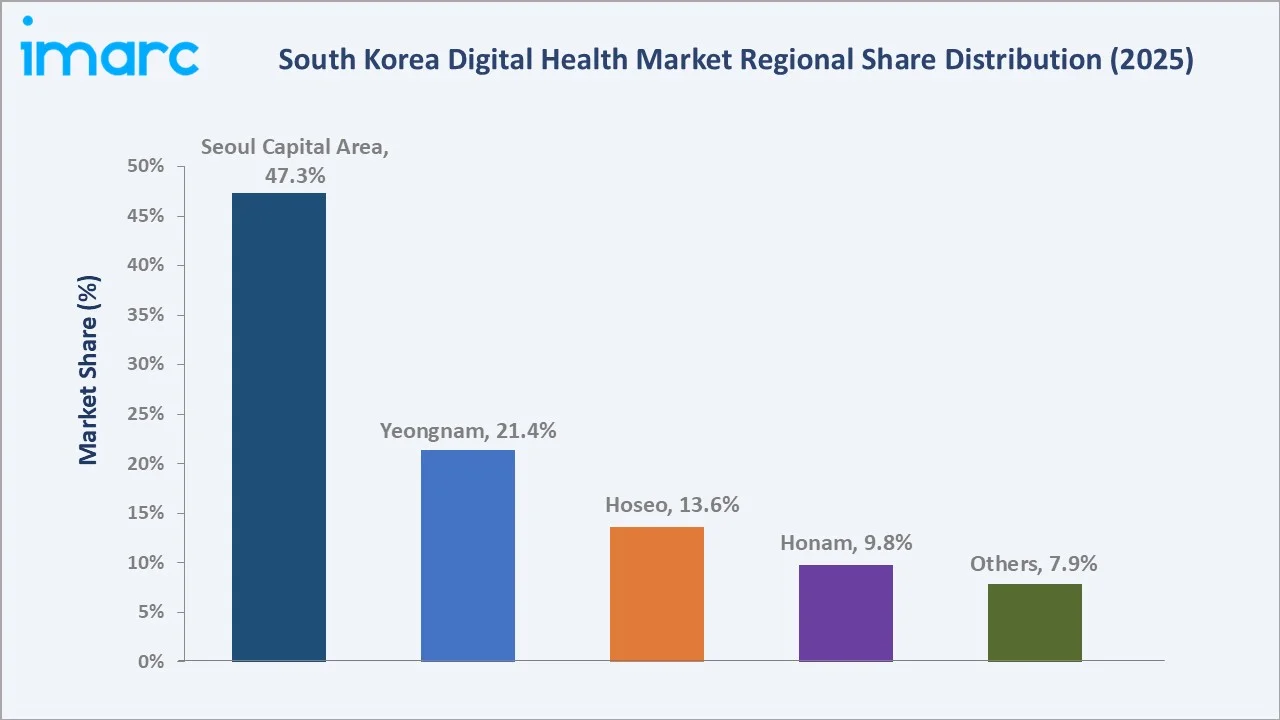

Software dominates the component mix at 49.5% in 2025, while Telehealth leads the type segment at 28.6%. Seoul Capital Area commands a dominant 47.3% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.77 Billion |

|

Forecast Market Size (2034) |

USD 43.11 Billion |

|

CAGR (2026-2034) |

14.34% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Seoul Capital Area (47.3% share, 2025) |

|

Second Region |

Yeongnam (21.4% share, 2025) |

|

Leading Component |

Software (49.5%, 2025) |

|

Leading Type |

Telehealth (28.6%, 2025) |

The South Korea digital health market trajectory from 2020 through 2034, with historical expansion to USD 10.77 Billion in 2025, reflects consistent technology-driven demand. The forecast to USD 43.11 Billion captures accelerating AI healthcare adoption, 5G-enabled remote monitoring, and government-backed digital transformation investment.

To get more information on this market, Request Sample

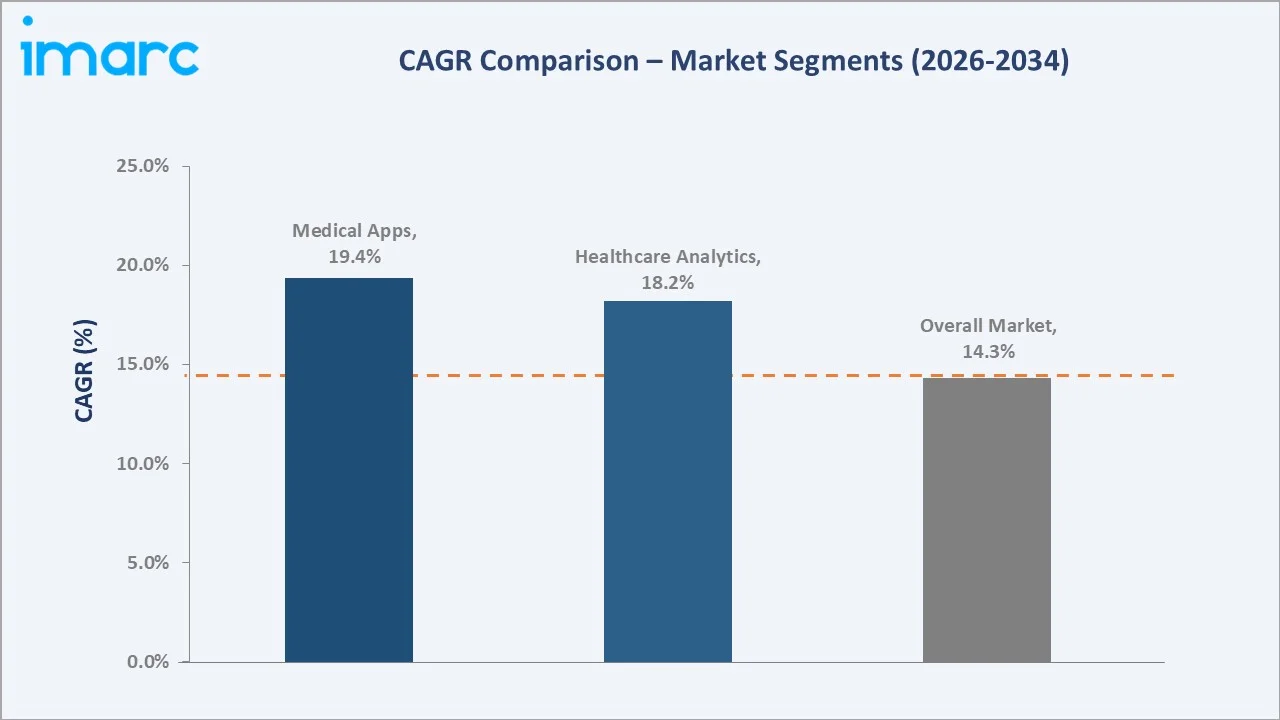

The CAGR trajectories across key component, type, and regional sub-segments, with Medical Apps at ~19.4% CAGR and Healthcare Analytics at ~18.2% CAGR, are the fastest-growing categories within the South Korea digital health industry analysis through 2034.

Executive Summary

The South Korea digital health market is on a sustained high-growth trajectory from USD 10.77 Billion in 2025 to USD 43.11 Billion by 2034. Digital health, encompassing telehealth platforms, wearable medical devices, EMR/EHR systems, healthcare analytics, and mobile health applications, benefits from South Korea's world-class ICT infrastructure, AI capabilities, and proactive regulatory environment.

Software leads the component segment at 49.5% in 2025, driven by cloud-based health platforms, AI diagnostic software, and hospital management systems. Hardware at 31.6% reflects growing wearable adoption and medical device integration. Telehealth dominates type segments at 28.6%, followed by Medical Wearables at 22.4% and EMR/EHR Systems at 18.7%.

Seoul Capital Area dominates at 47.3% in 2025, concentrating South Korea's top-tier medical institutions, government health agencies, and digital health startups. Yeongnam follows at 21.4%, driven by major industrial and healthcare centers in Busan, Daegu, and Ulsan.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Software - 49.5% share (2025) |

|

Leading Type |

Telehealth - 28.6% share (2025) |

|

Leading Region |

Seoul Capital Area - 47.3% share (2025) |

|

Second Region |

Yeongnam - 21.4% share (2025) |

|

Top Companies |

Kakao Healthcare Corp., Lunit Inc., SAMSUNG SDS, VUNO Inc., Deep Bio Inc., Huinno Co., Ltd, 3billion, Inc. |

Key Analytical Observations Expanding on the Above Data:

- Software's 49.5% share in 2025 reflects South Korea's advanced cloud adoption and AI-first approach to healthcare digitization. Hospital EMR systems, AI diagnostic platforms like Lunit and VUNO, and government e-health portals collectively drive the software segment's dominance.

- Telehealth at 28.6% in 2025 leads because of South Korea's rapid regulatory evolution during and post-COVID-19, enabling remote consultations, digital prescriptions, and AI-assisted triage at scale across the country.

- Seoul Capital Area's 47.3% dominance reflects the concentration of top-tier hospitals, leading health tech companies, and the Ministry of Health and Welfare headquarters driving national digital health policy and spending.

- Yeongnam's 21.4% share captures the digital transformation of industrial healthcare facilities in South Korea's southeastern manufacturing belt, with growing employer-sponsored digital health and occupational health digitization.

South Korea Digital Health Market Overview

Digital health in South Korea encompasses the convergence of healthcare delivery, information technology, and data analytics to improve patient outcomes, healthcare access, and system efficiency. The ecosystem spans telemedicine platforms enabling remote consultations, EMR/EHR systems for digital record management, AI-powered diagnostic tools, wearable monitoring devices, mobile health applications, and healthcare analytics platforms.

South Korea's digital health ecosystem uniquely benefits from a regulatory environment that has rapidly evolved to accommodate technological innovation, a single-payer National Health Insurance system facilitating standardized data access, and global technology leadership in semiconductors, 5G, and AI that enables domestic health technology development at world-class standards.

Market Dynamics

To evaluate market opportunities, Request Sample

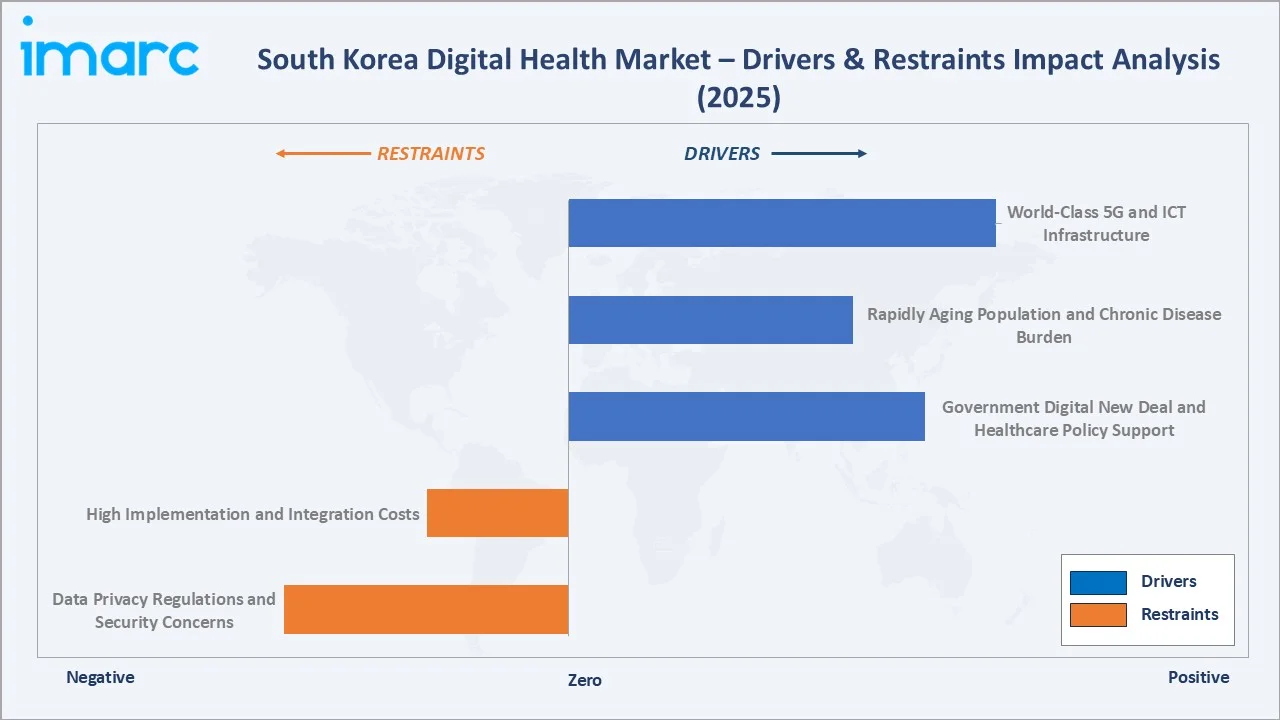

Market Drivers

- Government Digital New Deal and Healthcare Policy Support: South Korea's Digital New Deal has allocated over KRW 58.2 trillion toward digital transformation, with healthcare digitization as a core pillar. The Ministry of Health and Welfare actively promotes AI-based diagnostics, cloud-based health data infrastructure, and telehealth platform deployment across public and private hospitals.

- Rapidly Aging Population and Chronic Disease Burden: South Korea is one of the world's fastest-aging societies, with citizens aged 65+ expected to surpass 20% of the population by 2026. This demographic reality drives sustained demand for remote patient monitoring, digital chronic disease management, and telehealth services that extend care access beyond hospital infrastructure.

- World-Class 5G and ICT Infrastructure: South Korea's near-universal 5G coverage and the world's highest internet speeds provide the connectivity backbone enabling real-time health data transmission, ultra-low-latency remote diagnostics, and seamless integration between wearable devices and clinical decision support systems.

Market Restraints

- Data Privacy Regulations and Security Concerns: The Personal Information Protection Act (PIPA) and healthcare-specific data regulations impose strict requirements on patient health data collection, storage, and processing, increasing compliance costs for digital health platform operators and slowing cross-institutional data sharing.

- High Implementation and Integration Costs: Transitioning legacy hospital IT systems to modern digital health platforms requires substantial capital investment. Smaller clinics and regional hospitals face significant financial barriers to adoption, creating a two-speed market where large urban institutions advance rapidly while smaller providers lag.

Market Opportunities

- AI-Powered Precision Medicine and Genomics: South Korea's strong genomics research infrastructure and AI capabilities position the country as a potential global leader in precision medicine platforms. Companies like 3billion, specializing in rare disease genomics, represent the vanguard of a precision medicine ecosystem that will scale significantly through 2034.

- Digital Mental Health Platforms: South Korea's growing mental health awareness, combined with cultural barriers to in-person consultations, creates substantial market opportunity for digital mental health applications, AI-powered therapy tools, and telepsychiatry platforms targeting the country's working-age population.

Market Challenges

- Permanent Telehealth Legislation Uncertainty: Despite significant expansion of remote healthcare during COVID-19, South Korea has not enacted permanent telehealth legislation as of 2025, creating regulatory uncertainty for platform developers and healthcare providers investing in telemedicine infrastructure.

- Interoperability and Data Standardization Gaps: Despite government efforts to standardize health data formats, fragmented EMR systems across hospitals and clinics impede seamless patient data sharing, limiting the value proposition of AI analytics platforms that require comprehensive longitudinal health data.

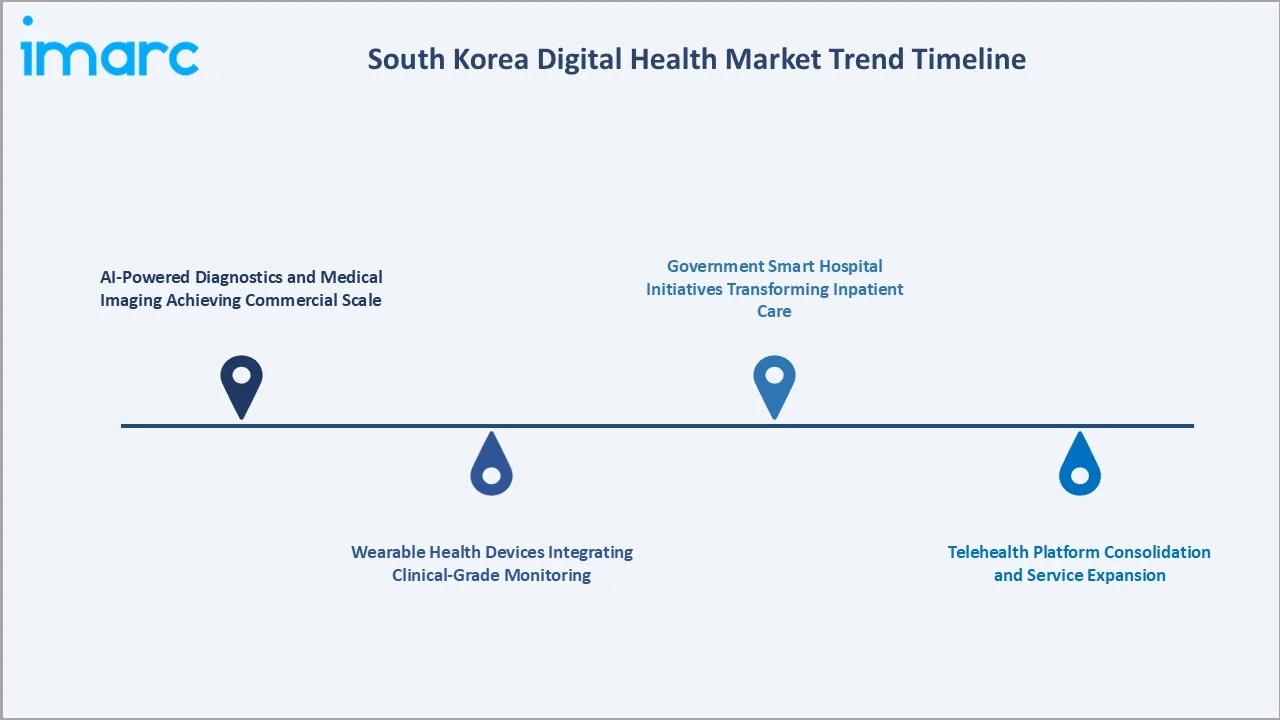

Emerging Market Trends

1. AI-Powered Diagnostics and Medical Imaging Achieving Commercial Scale

South Korean medical AI companies Lunit and VUNO have transitioned from clinical validation to commercial revenue at scale in 2025, with Lunit's AI imaging solutions deployed across hospitals in over 50 countries. MFDS approval pathways for AI-based medical devices have matured, enabling faster commercialization. These developments are establishing South Korea as a global AI diagnostics export hub.

2. Wearable Health Devices Integrating Clinical-Grade Monitoring

Samsung, Huinno, and other Korean manufacturers are launching wearables with clinical-grade ECG, blood pressure, and glucose monitoring capabilities. The integration of consumer wearable data into hospital EMR systems creates continuous monitoring capabilities beyond clinical settings, enabling early intervention for cardiovascular and metabolic conditions among Korea's aging population.

3. Telehealth Platform Consolidation and Service Expansion

Major Korean tech platforms Kakao and Naver are investing heavily in comprehensive digital health platforms, integrating appointment scheduling, remote consultation, prescription delivery, and health record management. This consolidation trend is accelerating user adoption and creating network effects that favor large integrated platforms over specialized single-service providers.

4. Government Smart Hospital Initiatives Transforming Inpatient Care

The Ministry of Health and Welfare's Smart Hospital program is funding digital transformation at leading Korean medical institutions, deploying AI clinical decision support, robotic process automation for administrative tasks, and real-time patient monitoring systems. Smart hospital certifications are becoming competitive differentiators for top-tier hospitals attracting medical tourism patients.

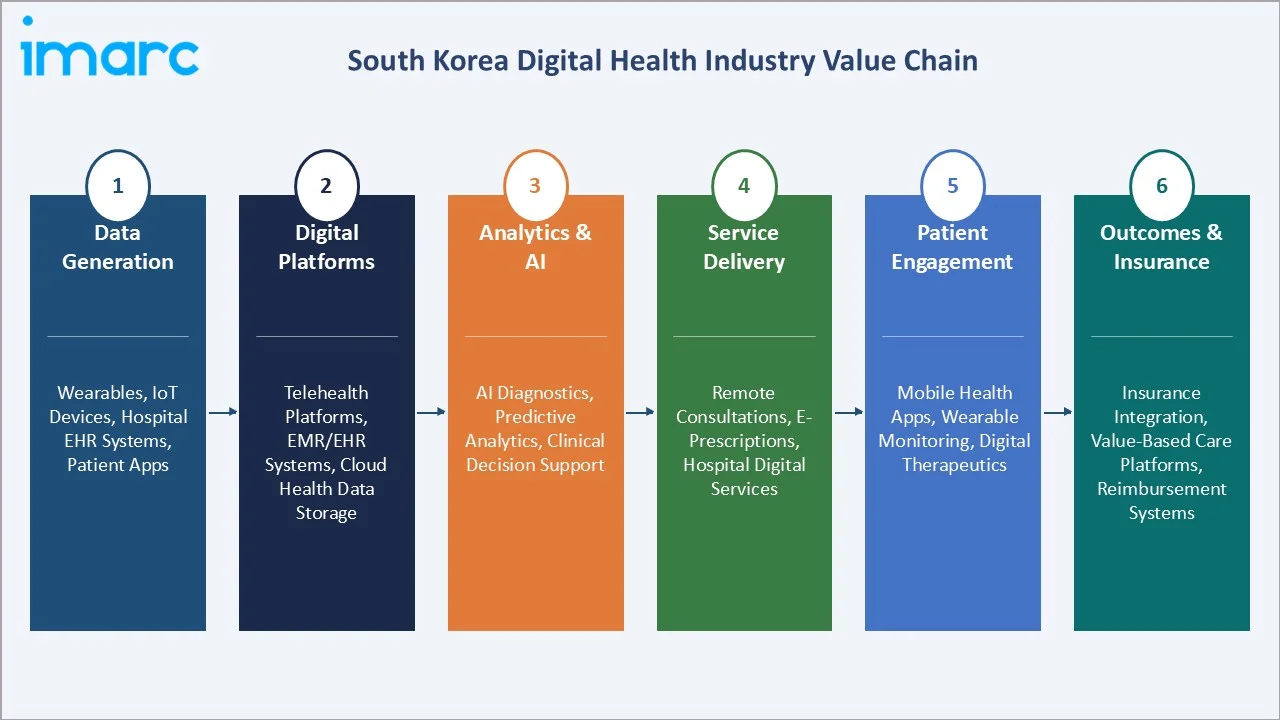

Industry Value Chain Analysis

The South Korea digital health value chain spans six stages from data generation through outcomes measurement. AI analytics and platform development capture the highest value-add margins, while device hardware faces increasing commoditization pressure from Chinese manufacturers competing on price.

|

Stage |

Key Players / Examples |

|

Data Generation |

Wearables, IoT Devices, Hospital EHR Systems, Patient Apps |

|

Digital Platforms |

Telehealth Platforms, EMR/EHR Systems, Cloud Health Data Storage |

|

Analytics & AI |

AI Diagnostics, Predictive Analytics, Clinical Decision Support |

|

Service Delivery |

Remote Consultations, E-Prescriptions, Hospital Digital Services |

|

Patient Engagement |

Mobile Health Apps, Wearable Monitoring, Digital Therapeutics |

|

Outcomes & Insurance |

Insurance Integration, Value-Based Care Platforms, Reimbursement Systems |

Technology Landscape in the South Korea Digital Health Industry

Artificial Intelligence and Machine Learning in Clinical Decision Support

AI deployment in South Korean healthcare has advanced rapidly from research prototypes to clinically approved and commercially deployed systems. VUNO's DeepCARS AI system for predicting in-hospital cardiac arrest has been installed across 50,000 hospital beds by 2025, representing a mature commercial AI deployment at national scale. Lunit's imaging AI for chest X-ray and pathology analysis is embedded in hospital PACS workflows at major medical centers.

5G-Enabled Remote Patient Monitoring and Telemedicine

South Korea's 5G network, with near-universal urban coverage by 2025, enables real-time transmission of high-resolution medical imaging, continuous vital sign monitoring from wearable devices, and video consultation quality enabling remote auscultation and examination. SK Telecom and KT's 5G health platform investments are creating infrastructure for hospital-grade remote monitoring services.

Electronic Health Record Interoperability and Health Data Exchange

The government's My Health Way platform provides citizens with centralized access to their health records from any participating institution, supporting the development of longitudinal health data assets required for AI training and personalized medicine applications. FHIR-based API standards are being adopted across major hospital EMR systems to enable data exchange.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Telehealth |

28.6% |

2025 |

|

Component |

Software |

49.5% |

2025 |

|

Region |

Seoul Capital Area |

47.3% |

2025 |

By Component

Software commands a 49.5% majority share in 2025, driven by the rapid adoption of cloud-based health platforms, AI diagnostic software, hospital EMR systems, and telemedicine application suites. South Korea's robust software development ecosystem and government's cloud-first health IT policy are accelerating enterprise software procurement across healthcare institutions.

To access detailed market analysis, Request Sample

Hardware at 31.6% in 2025 reflects the growing adoption of clinical-grade wearable devices, medical IoT sensor deployment, and the digitization of diagnostic equipment. Samsung Medison's AI-integrated ultrasound and digital radiography systems represent the high-value hardware segment, while consumer wearables from Samsung and LG drive volume growth. Service at 18.9% captures implementation, integration, training, and managed digital health service contracts across hospitals and clinics.

By Type

Telehealth dominates the type segment at 28.6% in 2025, reflecting South Korea's rapid expansion of remote consultation platforms during and after the COVID-19 pandemic. Kakao Healthcare, Naver Health, and numerous startups offer integrated telehealth services covering remote consultations, digital prescriptions, and remote monitoring. Post-pandemic legislative support for telehealth has sustained adoption.

Medical Wearables at 22.4% in 2025 grow fastest among established type segments, driven by Samsung's Galaxy Watch health features achieving clinical validation, Huinno's clinical ECG wearables, and growing prescription digital therapeutics. EMR/EHR Systems at 18.7% reflect the ongoing digitization of smaller clinics and regional hospitals beyond the large academic medical centers that completed EMR adoption earlier. Healthcare Analytics at 14.3% and Medical Apps at 10.8% round out the type of segment, with both categories exhibiting the fastest projected growth rates through 2034.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Seoul Capital Area |

47.3% |

Concentration of top hospitals, tech hubs, government digitization drives |

|

Yeongnam (Southeastern Region) |

21.4% |

Major industrial and medical centers in Busan, Daegu, Ulsan |

|

Hoseo (Central Region) |

13.6% |

Growing smart hospital initiatives; proximity to major pharma clusters |

|

Honam (Southwestern Region) |

9.8% |

Rural telemedicine adoption; government-backed digital health pilots |

|

Others |

7.9% |

Gangwon, Jeju and other regions benefiting from telehealth expansion |

Seoul Capital Area's 47.3% market dominance in 2025 is driven by the extraordinary concentration of South Korea's healthcare leadership: the Big 5 hospitals (Samsung Medical Center, Asan Medical Center, Severance Hospital, Seoul National University Hospital, and Seoul St. Mary's Hospital), the MOHW and MFDS headquarters, and the highest density of health technology startups and investment activity in the country.

Yeongnam, with 21.4% in 2025, captures the digital transformation of South Korea's southeastern industrial heartland. The Busan-Ulsan-Daegu metropolitan cluster's large employer base drives occupational health digitization and employee wellness platforms, while government investments in Busan's smart city and healthcare innovation district initiatives create incremental digital health procurement.

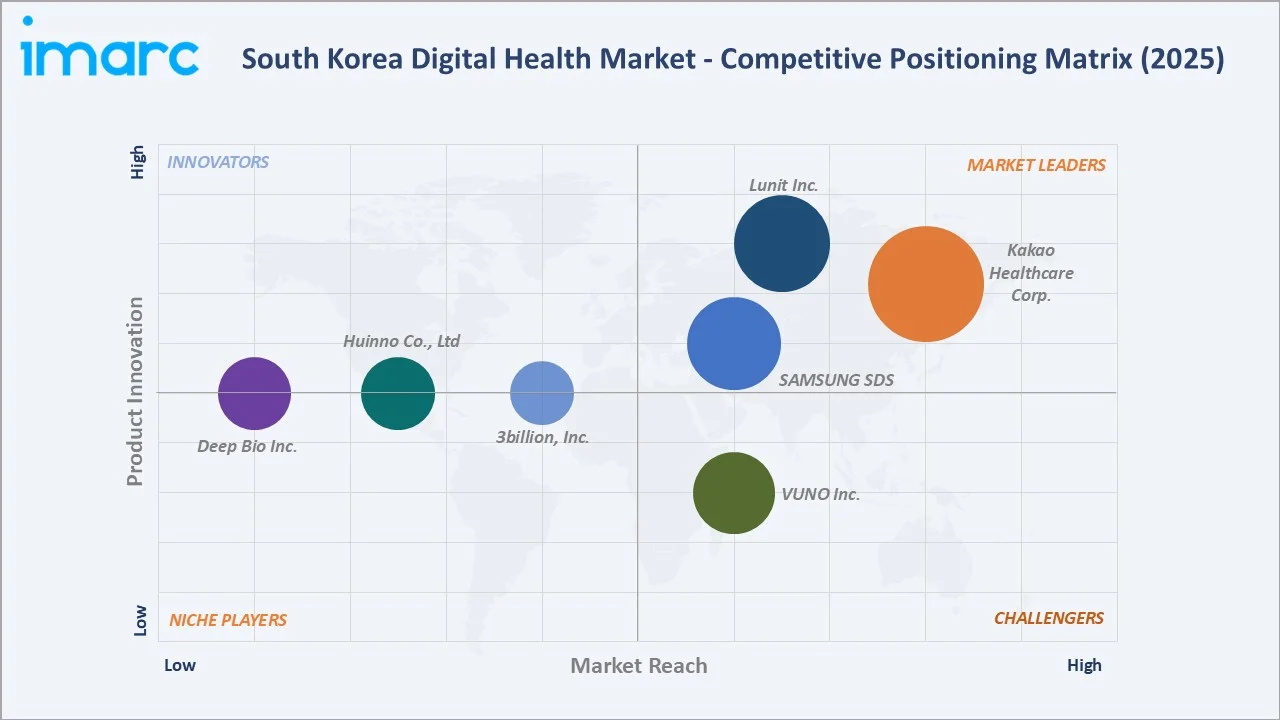

Competitive Landscape

The South Korea digital health market is moderately concentrated, with domestic Korean companies dominating across telehealth, AI diagnostics, and wearable devices, while global companies including participate primarily through platform and infrastructure partnerships rather than direct service delivery.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Kakao Healthcare Corp. |

PASTA, Healthcare Data Research Suite (HRS) |

Leader |

Consumer digital health; AI-powered health management |

|

Lunit Inc. |

Lunit SCOPE IO, Lunit SCOPE IHC Suite, Lunit SCOPE GP, Lunit INSIGHT MMG, Lunit INSIGHT DBT, Lunit INSIGHT CXR |

Leader |

Microsoft collaboration; Foundation Model Service (FMS) commercial platform; AI oncology |

|

SAMSUNG SDS |

Nexmed EHR |

Leader |

Hospital digital transformation; enterprise EHR deployment; digital health IT solutions |

|

VUNO Inc. |

VUNO Med |

Challenger |

Critical care AI monitoring |

|

Deep Bio Inc. |

DeepDx, DeepCDx |

Emerging |

AI pathology; cancer diagnostics; global expansion focus |

|

Huinno Co., Ltd |

MEMO Cue, MEMO Care |

Emerging |

Wearable cardiac monitoring; clinical-grade remote ECG |

|

3billion, Inc. |

GEBRA |

Emerging |

Rare disease genomics; AI-driven genetic analysis |

Key players include Kakao Healthcare Corp., Lunit Inc., SAMSUNG SDS, VUNO Inc., Deep Bio Inc., Huinno Co., Ltd, 3billion, Inc., and others.

Key Company Profiles

Kakao Healthcare Corp.

Kakao Healthcare is South Korea's leading consumer digital health platform, operating as a subsidiary of Kakao Corporation. Leveraging Kakao's dominant messaging and payment ecosystem, Kakao Healthcare delivers integrated telehealth consultations, prescription management, and AI-powered health management.

- Product Portfolio: PASTA, Healthcare Data Research Suite (HRS)

- Recent Developments: In April 2024, Kakao Healthcare signed a memorandum of understanding (MOU) with Konyang University Hospital, South Korea, to jointly develop patient-centered digital health services and accelerate medical innovation through advanced technology integration. Under the agreement, the two organizations will collaborate on establishing a digital healthcare system, developing a medical big data collaboration framework, and creating advanced solutions aimed at improving hospital operational efficiency.

- Strategic Focus: Kakao Healthcare's strategy leverages its unmatched consumer platform reach to build the largest digital health user base in Korea, converting Kakao's existing users into health platform subscribers through seamless integration with existing Kakao services, while monetizing through subscription health services and insurance distribution.

Lunit Inc.

Lunit is South Korea's leading AI oncology company, deploying FDA-cleared and CE-marked AI solutions for cancer detection and treatment response prediction across hospitals. The company is the benchmark for commercial AI medical imaging globally.

- Product Portfolio: Lunit SCOPE IO, Lunit SCOPE IHC Suite, Lunit SCOPE GP, AI Radiology Software, Lunit INSIGHT MMG, Lunit INSIGHT DBT, Lunit INSIGHT CXR, and others.

- Recent Developments: In May 2026, Lunit signed a memorandum of understanding (MOU) with Severance Hospital to jointly expand the development and clinical application of medical artificial intelligence and digital health technologies based on medical science foundation models. Under the partnership, the two organizations will collaborate on research, development, and real-world deployment of AI solutions designed to support clinical decision-making and hospital operations. The agreement also includes cooperation in data sharing, identification of clinical application scenarios, and commercialization of AI-powered healthcare technologies.

- Strategic Focus: Lunit's strategy focuses on building the most clinically validated and globally deployed AI oncology portfolio, targeting hospital system clients with comprehensive cancer detection and treatment decision support suites, while pursuing regulatory clearances across major markets to expand addressable revenue.

Market Concentration Analysis

The South Korea digital health market exhibits moderate concentration at the national level, with domestic Korean companies holding dominant positions in all major segments. Unlike global digital health markets dominated by US and European platforms, South Korea's digital health ecosystem is primarily served by domestic companies benefiting from cultural proximity, regulatory expertise, and government procurement preferences.

Consolidation is accelerating as major Korean technology conglomerates including Kakao, Naver, Samsung, and SK Group deploy capital into digital health platforms. This corporate consolidation is creating well-funded competitors capable of sustainable investment in AI, data infrastructure, and regulatory compliance at scales inaccessible to pure-play health startups.

Investment & Growth Opportunities

Fastest-Growing Segments

Medical Apps at ~19.4% CAGR through 2034 represent the highest-growth type segment, driven by prescription digital therapeutics approval pathways, chronic disease management application adoption, and mental health app penetration among South Korea's digitally native younger population.

Emerging Segments

Healthcare Analytics at ~18.2% CAGR through 2034 represents the highest growth established segment with significant enterprise revenue potential. Hospital and insurer demand for population health management, predictive readmission analytics, and claims analysis platforms is accelerating as health data infrastructure matures, and real-world evidence generation becomes a regulatory requirement for AI medical devices.

Venture & Investment Trends

South Korean venture capital investment in digital health reached record levels in 2024-2025, with medical AI companies attracting significant domestic and international institutional investment. The commercial revenue inflection demonstrated by Lunit and VUNO in 2025 has reduced perceived risk for institutional investors, with several Korean medical AI companies progressing toward KOSDAQ listings or global exchange dual listings. Government-backed Korea Health Industry Development Institute (KHIDI) programs continue to co-fund digital health R&D, providing non-dilutive capital for early-stage companies.

Future Market Outlook (2026-2034)

The South Korea digital health market is forecast to expand from USD 10.77 Billion in 2025 to USD 43.11 Billion by 2034 at a CAGR of 14.34%, adding USD 32.34 Billion in incremental annual market value over the forecast period. This sustained high-growth trajectory reflects South Korea's structural advantages in technology infrastructure, AI capabilities, and a healthcare system operating under a single-payer framework that facilitates data standardization.

Three technological forces will most significantly shape the South Korea digital health landscape through 2034. AI-driven precision medicine integrating genomic, wearable, and clinical data will create personalized treatment recommendation systems that transform chronic disease management. 5G-enabled hospital-grade remote monitoring will extend clinical-quality care to home settings, fundamentally restructuring outpatient care delivery. Digital therapeutics achieving insurance reimbursement status will create a new prescription drug-equivalent category generating recurring revenue streams for software developers.

Research Methodology

Primary Research

Primary research encompassed structured interviews with South Korea digital health industry stakeholders, including senior executives at leading health technology companies, hospital CIOs and clinical informaticists, government health ministry officials, venture capital investors specializing in Korean health tech, and healthcare provider executives. Primary data validated market sizing, segment share estimates, technology adoption timelines, and competitive positioning data.

Secondary Research

Key secondary sources include Korea Health Industry Development Institute (KHIDI) annual reports, Ministry of Health and Welfare digital health policy documents, National Health Insurance Service (NHIS) digitization data, Ministry of Science and ICT 5G healthcare deployment statistics, Korea Pharmaceutical and Bio-Industry Association reports, Korea Disease Control and Prevention Agency digital health publications, and trade publications including Biz Watch Korea, Medical Observer, and Healthcare IT News Asia Pacific.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating South Korea's GDP growth trajectory, healthcare expenditure trends as a percentage of GDP, digital health penetration rate benchmarks from comparable markets, regulatory approval rates for AI medical devices, and government digital health budget commitments through 2034.

South Korea Digital Health Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Telehealth, Medical Wearables, EMR/EHR Systems, Medical Apps, Healthcare Analytics, Others |

| Components Covered | Software, Hardware, Service |

| Regions Covered | Seoul Capital Area, Yeongnam (Southeastern Region), Honam (Southwestern Region), Hoseo (Central Region), Others |

| Companies Covered | Kakao Healthcare Corp., Lunit Inc., SAMSUNG SDS, VUNO Inc., Deep Bio Inc., Huinno Co., Ltd, 3billion, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the South Korea digital health market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the South Korea digital health market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the South Korea digital health industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the South Korea Digital Health Market Report

The South Korea digital health market size reached USD 10.77 Billion in 2025 and is projected to reach USD 43.11 Billion by 2034, exhibiting a CAGR of 14.34% during 2026-2034.

Software leads the component segment with a 49.5% share in 2025, driven by cloud-based health platforms, AI diagnostic software, and EMR/EHR system deployments across South Korean hospitals and clinics.

Medical Apps exhibit the highest projected CAGR of ~19.4% through 2034, followed by Healthcare Analytics at ~18.2% CAGR, driven by prescription digital therapeutics and population health management platform adoption.

Seoul Capital Area dominates with a 47.3% share in 2025, reflecting the concentration of top-tier hospitals, health technology companies, government agencies, and innovation investment in the greater Seoul metropolitan area.

Key players include Kakao Healthcare Corp., Lunit Inc., SAMSUNG SDS, VUNO Inc., Deep Bio Inc., Huinno Co., Ltd, 3billion, Inc., and others.

The key growth drivers include the South Korean government’s Digital New Deal allocating over KRW 58.2 trillion toward digital transformation, a rapidly aging population driving demand for remote monitoring and telehealth services, near-universal 5G network coverage enabling real-time health data transmission, and accelerating AI integration in clinical diagnostics through approved platforms from Lunit and VUNO.

The major challenges include the absence of permanent telehealth legislation creating regulatory uncertainty for platform operators, strict data privacy requirements under the Personal Information Protection Act (PIPA) increasing compliance costs, interoperability gaps between fragmented hospital EMR systems limiting AI analytics value, and high implementation costs creating adoption barriers for smaller clinics and regional healthcare providers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)