Space Launch Services Market Size, Share, Trends and Forecast by Payload, Launch Platform, Service Type, Orbit, Launch Vehicle, End User, and Region, 2026-2034

Space Launch Services Market Size and Share:

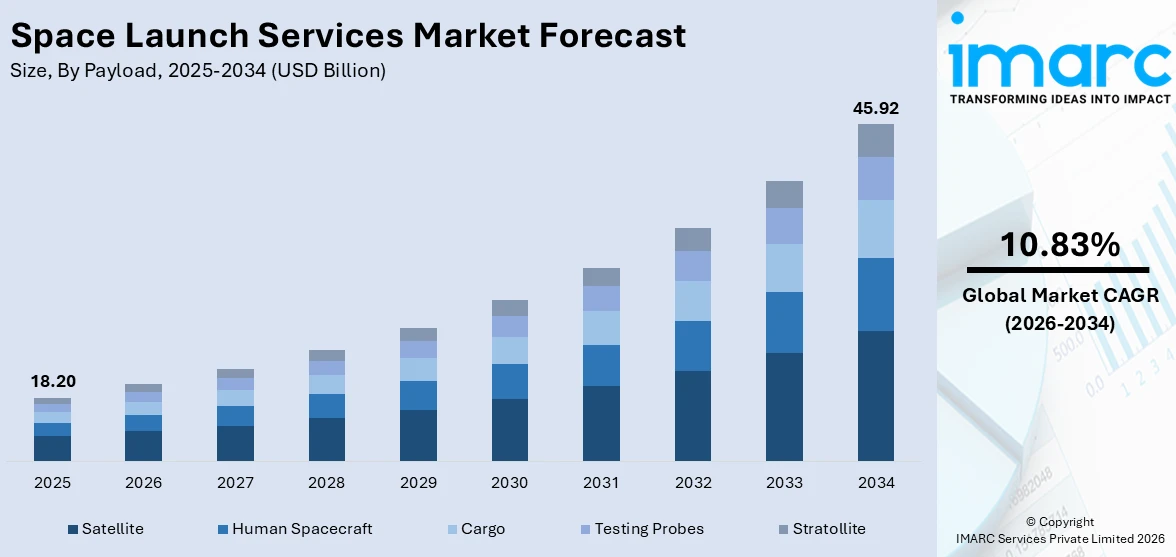

The global space launch services market size was valued at USD 18.20 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 45.92 Billion by 2034, exhibiting a CAGR of 10.83% from 2026-2034. North America currently dominates the market, holding a market share of 30% in 2025. The region benefits from the most advanced spaceport infrastructure, sustained government expenditure on national security and civil space missions, and the presence of leading commercial launch providers driving rapid innovation in reusable rocket technology, thereby contributing to the space launch services market share.

The global space launch services market is advancing rapidly, driven by the increasing deployment of satellite constellations for broadband connectivity, Earth observation, and navigation services that require reliable and cost-effective launch solutions. Additionally, the emergence of new private-sector launch providers is intensifying competition, fostering technological innovation, and diversifying the range of available mission profiles. The expansion of space tourism and deep-space exploration programs is also creating new launch demand streams that support long-term industry growth. Moreover, the advancement of reusable launch vehicle technology is significantly reducing per-mission costs, enabling higher launch frequency and broadening access to space for commercial and government customers alike. The growing emphasis on national security space capabilities across multiple countries is further offering a favorable space launch services market outlook.

The United States is becoming a vital player in the space launch services market due to its well-established infrastructure, technological advancements, and strong commercial and government sector involvement. Additionally, the US benefits from its robust network of private space companies that drive innovation, particularly in reusable rocket technology. These advancements are helping to reduce the overall cost of launching satellites and increase the frequency of launches. A notable example of this trend is SES’s 2025 announcement of an extended multi-launch services agreement with Relativity Space. This partnership, which includes the use of the Terran R rocket’s reusable capabilities, will see launches begin in late 2026 from Cape Canaveral, further solidifying US's position in the global market.

To get more information on this market Request Sample

Space Launch Services Market Trends:

Growth of Space-Based Earth Observation

The increasing reliance on space-based technologies for Earth observation and environmental monitoring is a significant factor propelling the market growth. Space-based platforms offer real-time data for a wide array of applications, including climate monitoring, disaster management, agricultural planning, and urban development. As governments, corporations, and environmental agencies seek to improve their ability to monitor Earth from space, there is a rise in the demand for launch services to deploy these satellites. In addition, the rapid expansion of commercial Earth observation efforts is leading to the establishment of various small satellite constellations, all requiring dependable and cost-effective launch solutions. For example, in 2025, Luxembourg's Earth Observation System (LUXEOSys) satellite was successfully launched aboard a SpaceX Falcon 9 rocket from Vandenberg Space Force Base. This satellite, positioned in a sun-synchronous orbit at 450 km, will provide up to 100 high-resolution images per day, supporting applications such as climate monitoring, security, and disaster response. This demand for frequent, reliable launches continues to fuel the growth of the space launch services market.

Rising Demand for Continuous Climate and Environmental Monitoring

With the growing concerns over climate change and environmental sustainability, there is a higher need for accurate, long-term data collection from space. Satellites dedicated to monitoring Earth’s changing climate, such as those tracking sea level rise, play a crucial role in enhancing disaster response, refining weather forecasting, and improving infrastructure resilience. The upcoming launch of NASA and the European Space Agency's Sentinel-6B satellite in 2025 exemplifies this trend. Set to launch aboard SpaceX’s Falcon 9 rocket, Sentinel-6B will continue vital sea level monitoring, building upon the data provided by its predecessor, Sentinel-6 Michael Freilich. The satellite planned to deliver crucial information for climate research, storm forecasting, and infrastructure protection, ensuring data collection for at least the next three decades. This increasing demand for climate-focused space missions continues to drive the need for reliable and cost-effective launch services.

Advancements in Satellite Technology

Advancements in satellite technology, including smaller, more efficient, and less costly satellite designs, are significantly increasing the demand for frequent launches to place these satellites into orbit. Innovations, such as miniaturized payloads and more durable satellite components allow for a broader range of space missions at lower costs, thus driving the need for more launch services. The rise of small satellite constellations, in particular, is a crucial factor in this growth, as these networks require specialized transport to orbit. For example, in 2026, SpaceX successfully launched the GPS III-SV09 satellite for the U.S. Space Force from Cape Canaveral. This satellite, the ninth in the GPS III series, is designed to offer enhanced resistance to jamming, providing improved navigation and security capabilities. Notably, SpaceX completed this launch with an unprecedented turnaround time of just 41 days, reflecting the growing demand for rapid, efficient, and cost-effective launch services, which further strengthens the market growth.

Space Launch Services Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global space launch services market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on payload, launch platform, service type, orbit, launch vehicle, and end user.

Analysis by Payload:

- Satellite

- Small Satellite (Less Than 1000 Kg)

- Large Satellite (Above 1000 Kg)

- Human Spacecraft

- Cargo

- Testing Probes

- Stratollite

Satellite holds 52% of the market share. The dominance of the segment is primarily driven by the increasing investments in communication, Earth observation, and navigation constellations across both government and commercial sectors. The rising need for broadband connectivity in underserved regions, coupled with the growing defense requirements for persistent surveillance and secure communications, is catalyzing the demand for satellite launch missions. Moreover, the expanding role of satellite constellations in supporting global communications and environmental monitoring is influencing the market. A key example of this trend is the 2025 launch of the BlueBird Block-2 satellite by ISRO’s LVM3-M6 mission, which marked India's heaviest commercial satellite launch to date. Weighing 6,100 kg, the satellite was successfully deployed into Low Earth Orbit. This mission strengthens India's position in global space commercialization, facilitated by ISRO's commercial arm, NewSpace India Ltd (NSIL), and highlights the increasing global reliance on satellite payloads for a variety of critical applications.

Analysis by Launch Platform:

- Land

- Air

- Sea

Land leads the market with a share of 70%, maintaining its dominant position in the space launch services industry. This is due to the well-established infrastructure of coastal and inland spaceports that support a wide range of orbital missions. These facilities are equipped with comprehensive ground support systems, such as integration halls, mission control centers, and propellant handling equipment, ensuring reliable, repeatable launch operations at scale. The presence of such robust infrastructure allows for the consistent execution of high-volume launches, essential for supporting the growing demand for satellite deployments. Moreover, the continued expansion and modernization of existing launch complexes are crucial for accommodating the higher cadence of operations required by the increasing number of satellite constellations. As global satellite networks expand to meet the demands of communication, Earth observation, and other applications, land-based platforms will remain central to the success of these missions, further solidifying their leadership in the market.

Analysis by Service Type:

- Pre-Launch

- Post-Launch

Pre-launch dominates the market with a share of 57%, encompassing a broad range of essential activities required before mission execution. This segment includes payload integration, mission planning, regulatory compliance, environmental testing, and launch vehicle preparation, all of which are critical for the success of satellite missions. The growing complexity of modern satellite missions, coupled with an increasing number of multi-manifest and rideshare launches, is driving the demand for specialized pre-launch capabilities. As satellite missions become more intricate, there is a rise in the need for detailed coordination between launch providers, satellite operators, and regulatory authorities. This complex ecosystem necessitates highly specialized pre-launch service to ensure timely and safe mission execution. Furthermore, the increasing number of commercial and government space activities is expanding the scope and value of pre-launch service offerings, highlighting the crucial role these services play in the success of the rapidly growing space industry. The space launch services market forecast indicates continued growth, driven by the increasing demand for advanced pre-launch capabilities.

Analysis by Orbit:

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geosynchronous Orbit

- Polar Orbit

Low Earth Orbit (LEO) remains the leading segment, holding a share of 50%. This dominance is driven by the rapid expansion of broadband satellite constellations, which are revolutionizing global communications by providing high-speed internet access to underserved regions. The growth of LEO-based constellations is fueled by both government and commercial investments, aiming to improve connectivity, surveillance, and data relay capabilities. A significant example of this trend is the European Space Agency's (ESA) confirmation of the target launch date for its Celeste LEO-PNT in-orbit demonstration mission, scheduled for March 24, 2026. This mission will feature two satellites launched by Rocket Lab and will test next-generation satellite navigation technologies, including new frequency bands to enhance performance. The Celeste mission aims to complement the Galileo system by improving resilience and expanding satellite navigation capabilities in LEO. This underscores the growing strategic importance of LEO in advancing satellite navigation and communications systems globally.

Analysis by Launch Vehicle:

- Small Launch Vehicle

- Heavy Launch Vehicle

Heavy launch vehicle dominates the market with a 59% share, playing a crucial role in deploying high-value government payloads, large communication satellites, and multi-satellite constellation batches that require substantial lift capacity. This vehicle is designed to provide the necessary thrust for missions targeting geostationary transfer orbits, deep-space trajectories, and heavy reconnaissance platforms, where precision and power are paramount. The increasing demand for national security space missions, including satellite systems for surveillance, reconnaissance, and secure communications, is one of the key factors driving the growth of heavy-lift launch vehicle. Additionally, the expansion of commercial mega-constellations, which involve launching large numbers of satellites into LEO for global communications, is further boosting investment in these capabilities. As both government and commercial sectors increasingly rely on large-scale, complex satellite deployments, heavy launch vehicle continues to play an essential role in meeting the growing demands for space access.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

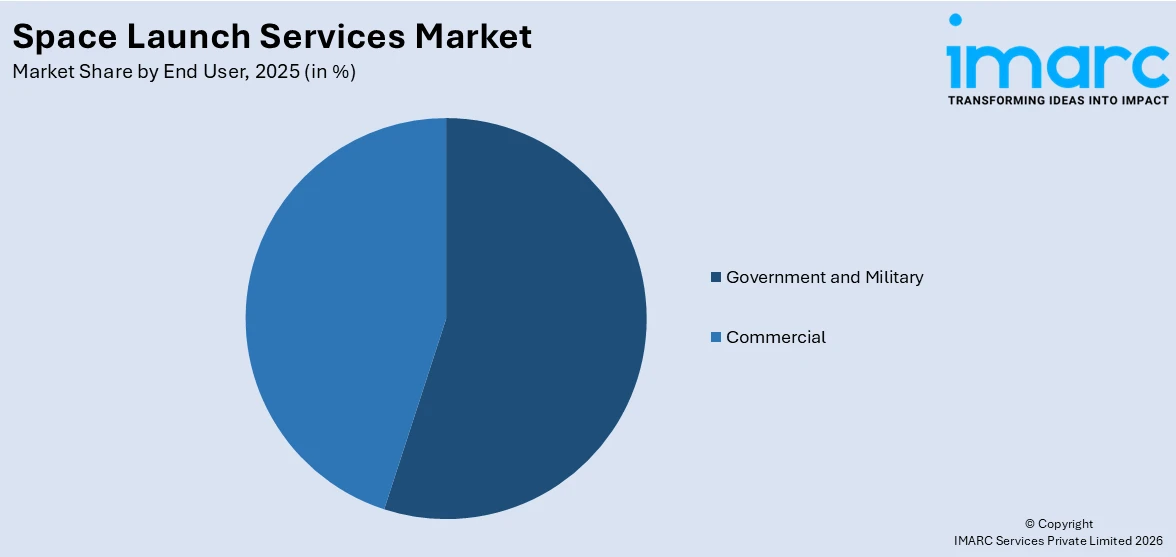

- Government and Military

- Commercial

Government and military hold a market share of 55%, driven by the critical role of space-based assets in national defense, intelligence gathering, and secure communications. Defense agencies across the globe are increasingly expanding their satellite constellations to enhance capabilities in surveillance, missile warning, and navigation, which in turn sustains a high demand for reliable and efficient launch services. The need for secure and timely satellite deployments is a key factor behind this ongoing demand. A prime example of this trend is India’s NewSpace India Limited (NSIL), which was set to launch the GSAT-N3 communication satellite in Q1 2026 to meet the S-Band communication needs of the Government of India. Additionally, NSIL planned to launch its first fully industry-made PSLV in Q2 2025, a significant milestone in India’s commercial space ambitions. These initiatives highlight the growing importance of space launch services for both defense and commercial applications, reinforcing the market's robust growth trajectory.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 30% of the share, enjoys the leading position in the market. The region's dominance is underpinned by its advanced technological infrastructure, significant investments in space exploration, and a thriving commercial space sector. The region continues to be at the forefront of innovation, with both government agencies and private companies contributing to its dominance in space activities. A significant example of this is Maritime Launch Services (MLS), based in Nova Scotia, which successfully launched its second suborbital test rocket in 2025. This achievement marked a key milestone in the development of Canada's first commercial spaceport, Spaceport Nova Scotia. The success of this test launch is a critical step toward establishing Canada’s sovereign space capabilities and expanding commercial space operations within the region. The ongoing advancements in space infrastructure is contributing to the space launch services market growth, further solidifying North America's leadership in the industry.

Key Regional Takeaways:

United States Space Launch Services Market Analysis

The United States space launch services market is driven by substantial government investments in both national defense and civil space missions, alongside a thriving commercial sector led by innovative private launch providers. The country's extensive network of operational launch facilities, located along the Atlantic and Pacific coasts, further strengthens its position in the global market. A key example of this growth is SpaceX’s plan to begin construction of a 380-foot-tall Starship Gigabay at Kennedy Space Center in April 2025. This facility, modeled after SpaceX's Megabay in Texas, will be critical for the finalization of the Super Heavy boosters for Starship launches. The Gigabay is expected to support Starship's launches from Pad 39A, with construction anticipated to last until August 2026. This timeline aligns with upcoming high-profile missions, including NASA’s Artemis III lunar landing, underscoring the ongoing expansion and technological advancements shaping the US space launch services market.

Europe Space Launch Services Market Analysis

The Europe space launch services market is undergoing a significant transformation, driven by substantial investments aimed at restoring and expanding the region’s autonomous access to space. This transformation is crucial as Europe seeks to bolster its capabilities in satellite deployment and space exploration. A prime example of this progress is the successful 2025 launch of two Galileo satellites aboard an Ariane 6 rocket, marking the 14th launch for Europe's satellite navigation system. This mission expanded the Galileo constellation to 29 active satellites, significantly enhancing its global resilience and capacity to provide high-accuracy navigation services. The successful launch highlights Europe's leadership in offering independent and reliable navigation services worldwide, reducing reliance on other global systems. With such advancements, Europe continues to strengthen its position in the space launch services market, underscoring its commitment to maintaining a robust and autonomous space infrastructure for both commercial and governmental purposes.

Asia-Pacific Space Launch Services Market Analysis

The space launch services market growth in the Asia Pacific is fueled by increasing government investment in indigenous launch capabilities and satellite programs across the region. This growth is particularly evident in China, which completed 50 commercial space launches in 2025, accounting for 54% of its total space missions. A key achievement during this period was the successful placement of 311 commercial satellites into orbit, showcasing China’s expanding space capabilities. Notably, the country has made significant strides in reusable rocket technology, highlighted by the maiden flight of the Zhuque-3 rocket. The commercial space sector in China continues to grow, with notable advancements such as the successful test launch of Galactic Energy’s PALLAS-2 rocket. These developments underscore the region’s rapid progress and its increasing role in the global space launch services market.

Latin America Space Launch Services Market Analysis

The Latin America space launch services market is witnessing growth as several nations expand their space programs and invest in satellite infrastructure to support telecommunications, environmental monitoring, and agricultural management. For instance, in 2026, Brazil’s National Institute for Space Research (INPE) selection of the Vega C rocket to launch the Amazonia-1B Earth observation satellite in 2027. The contract, awarded to SpaceLaunch, represents a significant milestone for Avio as it continues to expand its global presence. This collaboration highlights Latin America’s growing role in space exploration and underscores the region’s commitment to advancing satellite capabilities for environmental and agricultural applications. These developments are a clear reflection of the ongoing space launch services market trends in the region, characterized by increasing investments and expanding space capabilities.

Middle East and Africa Space Launch Services Market Analysis

The Middle East and Africa space launch services market is experiencing growth as nations in the region establish and expand dedicated space programs to support national development and strategic security needs. A key development in this trend is RH Aero Systems' inauguration of a new 2,800 m² service center at Dubai South's Mohammed bin Rashid Aerospace Hub in 2026. This facility will serve as the regional hub for ground support equipment and engine tooling services across the Middle East, Africa, and India. This expansion aligns with RH Aero's growth strategy, providing faster turnaround times and closer service proximity to clients, further supporting the region's growing space industry.

Competitive Landscape:

The global space launch services market features a dynamic competitive landscape characterized by the presence of both established government-backed launch organizations and the rapidly growing commercial providers. Leading players are investing heavily in reusable rocket technology, vertical integration of spacecraft manufacturing, and expansion of spaceport infrastructure to increase launch cadence and reduce mission costs. Strategic partnerships between government agencies and commercial operators are reshaping procurement models, with fixed-price contracts and multi-year launch agreements becoming the industry standard. Companies are also pursuing diversification into adjacent services, including satellite manufacturing, in-orbit servicing, and mission management, to capture greater value across the space mission lifecycle. The competitive environment is further intensified by new market entrants developing innovative small-lift and medium-lift vehicles targeting underserved segments of the market.

The report provides a comprehensive analysis of the competitive landscape in the space launch services market with detailed profiles of all major companies, including:

- Antrix Corporation Limited

- Arianespace SA

- Astra

- China Great Wall Industry Corporation

- Glavkosmos

- ILS International Launch Services

- Mitsubishi Heavy Industries Ltd.

- Orbital Express Launch Limited

- SpaceX

- United Launch Alliance, LLC.

Latest News and Developments:

- In December 2025, Rocket Lab secured USD 816 Million contract with the U.S. Space Development Agency (SDA) to design and manufacture 18 satellites for missile warning and tracking. This contract is part of the SDA’s Tracking Layer Tranche 3 program. With this win, Rocket Lab's defense-related contracts exceed USD 1.3 Billion.

- In December 2025, United Launch Alliance (ULA) successfully launched the Leo 4 mission, deploying 27 more satellites for Amazon's Leo constellation. This brings ULA's total contribution to 108 satellites, as they continue to play a key role in Amazon’s goal of connecting the world through broadband services. The launch reinforces ULA's pivotal partnership with Amazon, with more missions lined up for future satellite deployments.

Space Launch Services Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Payloads Covered |

|

| Launch Platforms Covered | Land, Air, Sea |

| Service Types Covered | Pre-Launch, Post-Launch |

| Orbits Covered | Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geosynchronous Orbit, Polar Orbit |

| Launch Vehicles Covered | Small Launch Vehicle, Heavy Launch Vehicle |

| End Users Covered | Government and Military, Commercial |

| Region Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Antrix Corporation Limited, Arianespace SA, Astra, China Great Wall Industry Corporation, Glavkosmos, ILS International Launch Services, Mitsubishi Heavy Industries Ltd., Orbital Express Launch Limited, SpaceX, United Launch Alliance, LLC., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the space launch services market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global space launch services market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the space launch services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Space Launch Services Market Report

The space launch services market was valued at USD 18.20 Billion in 2025.

The space launch services market is projected to exhibit a CAGR of 10.83% during 2026-2034, reaching a value of USD 45.92 Billion by 2034.

The space launch services market is driven by the increasing demand for Earth observation satellites, advancements in satellite technology, and the need for continuous climate monitoring. These trends are creating a need for frequent, cost-effective, and efficient launches to support diverse space missions and long-term environmental data collection.

North America currently dominates the space launch services market, accounting for a share of 30%. The region benefits from the world's most advanced spaceport infrastructure, substantial government investment in defense and civil space programs, leading commercial launch providers, and a mature regulatory environment that supports rapid licensing.

Some of the major players in the space launch services market include Antrix Corporation Limited, Arianespace SA, Astra, China Great Wall Industry Corporation, Glavkosmos, ILS International Launch Services, Mitsubishi Heavy Industries Ltd., Orbital Express Launch Limited, SpaceX, United Launch Alliance, LLC., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade