Spain Data Center Market Size, Share, Trends and Forecast by Data Center Size, Tier Type, Absorption, and Region, 2026-2034

Spain Data Center Market Size, Share, Trends & Forecast (2026-2034)

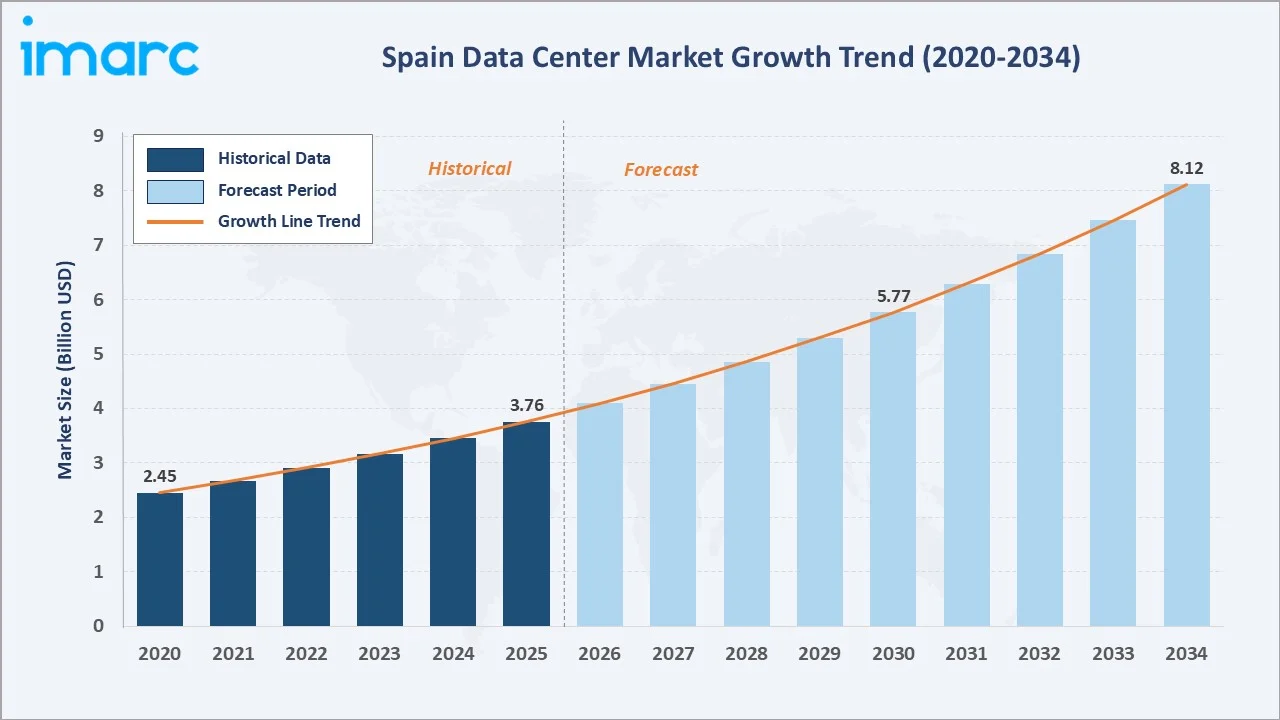

The Spain data center market reached USD 3.76 Billion in 2025 and is projected to reach USD 8.12 Billion by 2034, growing at a CAGR of 8.94% during 2026-2034. The market is driven by transformative hyperscaler investment commitments, accelerating enterprise cloud adoption, expanding submarine cable connectivity, and Spain's abundant renewable energy resources, which enable sustainable and cost-competitive operations.

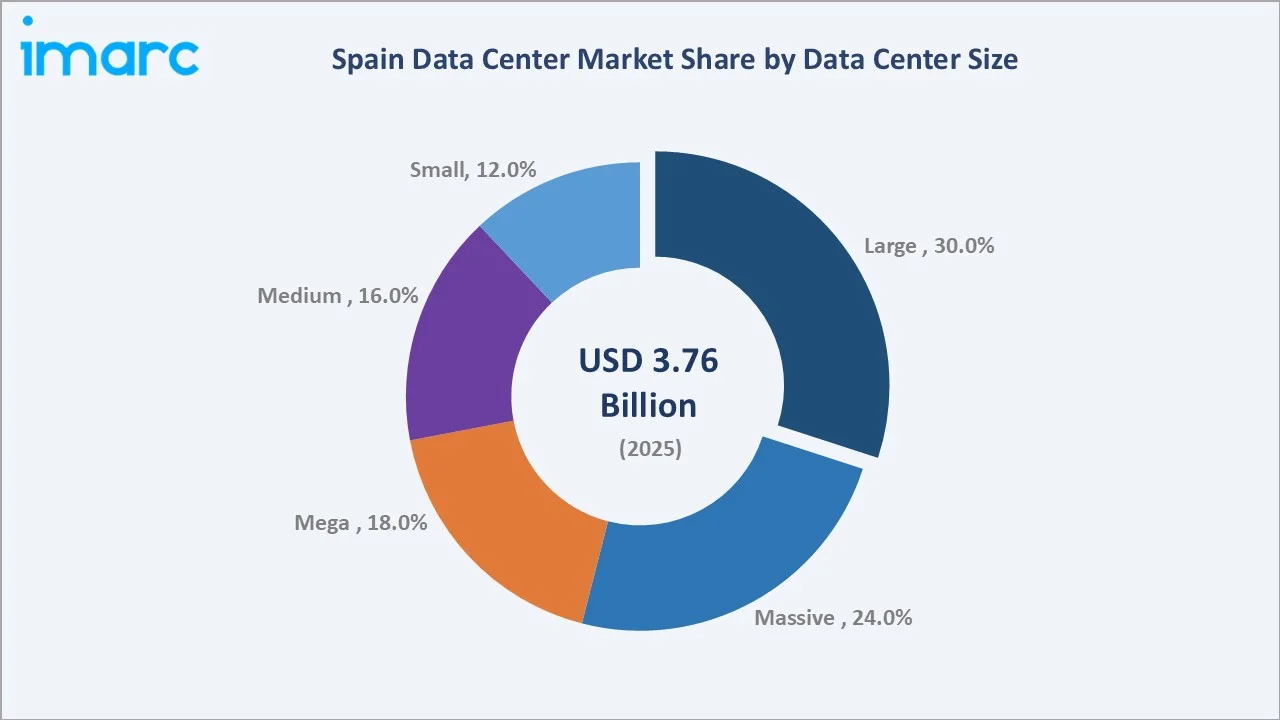

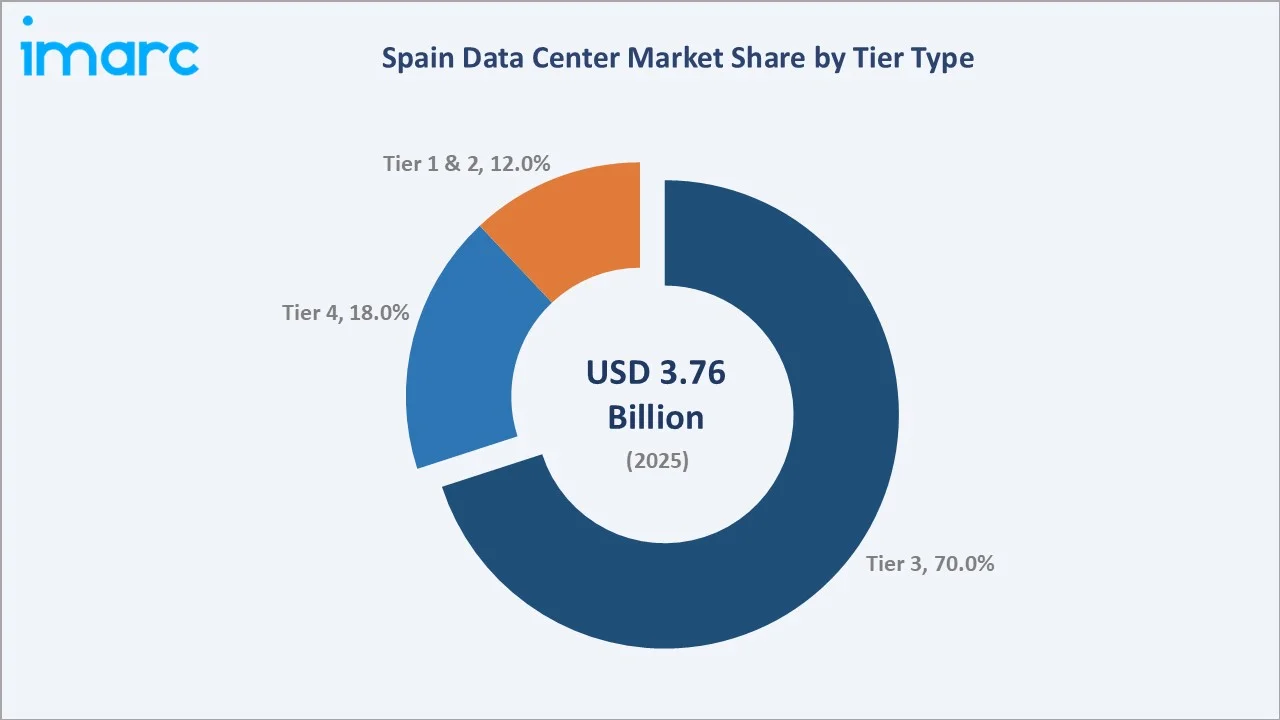

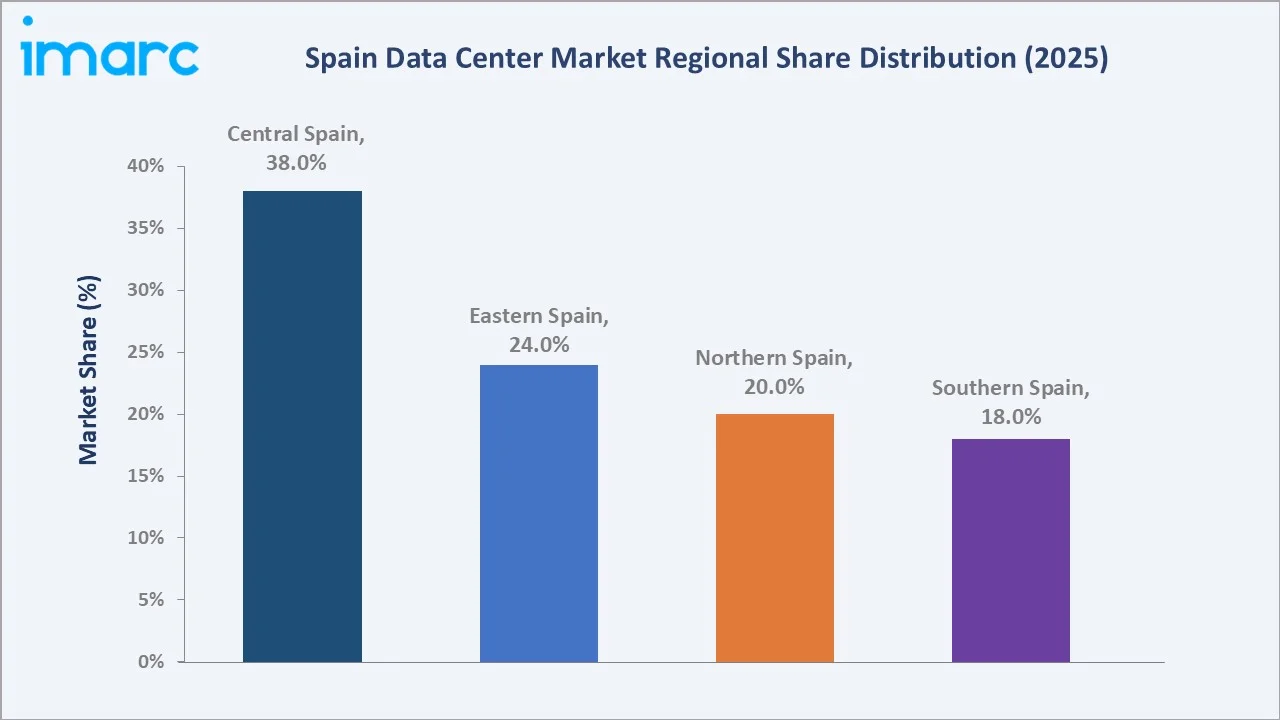

Large data centers lead at 30.0% by Data Center Size. Tier 3 dominates at 70.0% by Tier Type. Central Spain commands 38.0% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.76 Billion |

|

Forecast Market Size (2034) |

USD 8.12 Billion |

|

CAGR (2026-2034) |

8.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Data Center Size |

Large (30.0%, 2025) |

|

Dominant Tier Type |

Tier 3 (70.0%, 2025) |

|

Leading Region |

Central Spain (38.0%, 2025) |

The market expanded from USD 2.45 Billion in 2020 to USD 3.76 Billion in 2025, anchored at USD 5.77 Billion in 2030 and forecast to reach USD 8.12 Billion by 2034. Accelerating digital transformation, hyperscaler investment, and AI infrastructure buildout underpin the sustained 8.94% CAGR trajectory through the forecast period.

To get more information on this market, Request Sample

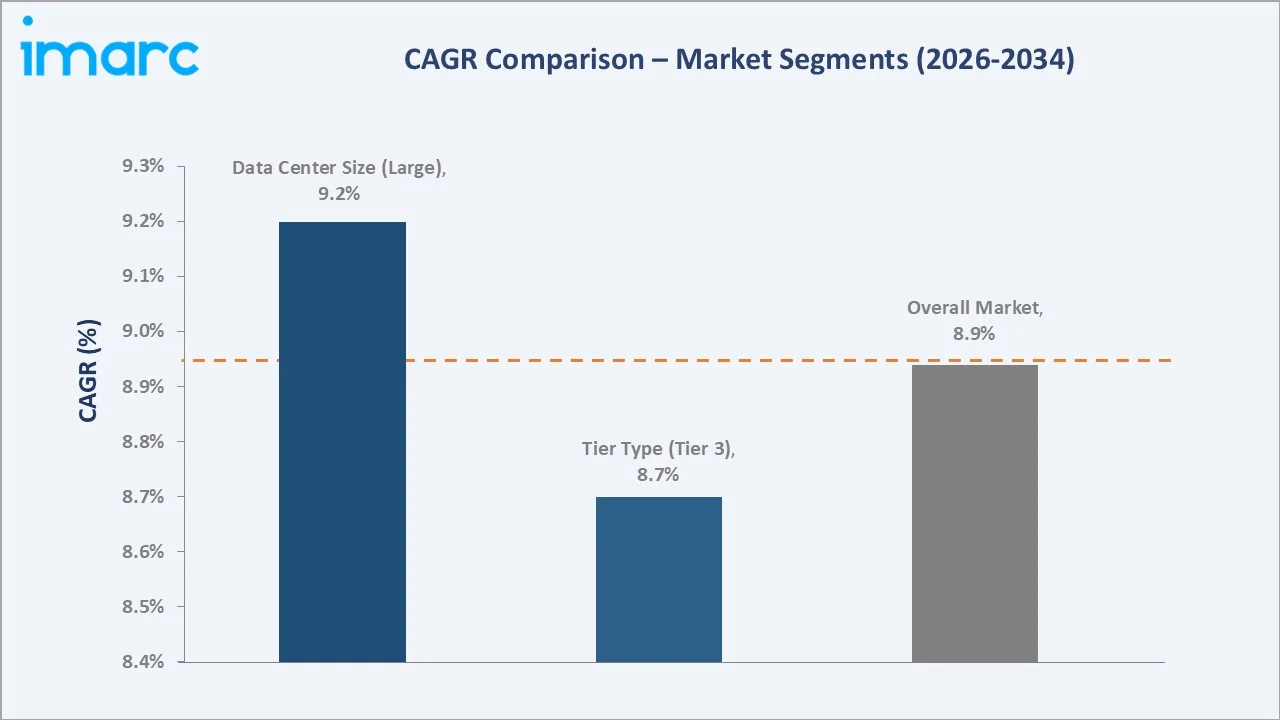

Large data centers grow at ~9.2% CAGR driven by enterprise mid-market requirements and balanced economics enabling efficient power utilization. Tier 3 facilities grow at ~8.7% CAGR as N+1 redundancy remains the preferred operational standard for Spanish enterprise customers. Central Spain grows fastest at ~9.5% CAGR through concentrated hyperscaler and government infrastructure investment.

Executive Summary

The Spain data center market reached USD 3.76 Billion in 2025, representing Southern Europe's most rapidly expanding digital infrastructure destination driven by structural demand convergence across hyperscaler expansion, enterprise cloud migration, AI infrastructure deployment, and submarine cable connectivity investment.

Large data centers dominate at 30.0% by capturing enterprise and mid-market digital transformation requirements through balanced economics and operational flexibility. Tier 3 leads at 70.0% through N+1 redundancy configurations that balance operational reliability with cost efficiency for mission-critical enterprise applications.

Central Spain at 38.0% leads through Madrid's network concentration, enterprise density, government institution proximity, and established hyperscaler campus presence.

Key Market Insights

|

Insight |

Data |

|

Dominant Data Center Size |

Large – 30.0% share (2025) |

|

Dominant Tier Type |

Tier 3 – 70.0% market share (2025) |

|

Leading Region |

Central Spain – 38.0% market share (2025) |

|

Market Opportunity |

AI-ready infrastructure; renewable PPA-powered hyperscale campuses; secondary city expansion; submarine cable-connected interconnection hubs |

Key Analytical Observations Supporting The Above Data:

- Large at 30.0%: The Large segment dominates by capturing enterprise requirements for scalable infrastructure between single-cabinet colocation and massive hyperscale configurations, addressing mid-market digital transformation needs across banking, telecommunications, and manufacturing sectors. Balanced economics enable efficient power utilization while maintaining flexibility for diverse tenant requirements.

- Tier 3 at 70.0%: The Tier 3 segment dominates due to enterprise preference for N+1 redundancy configurations that enable concurrent maintainability without requiring service interruption during routine equipment maintenance. These standard addresses operational requirements while maintaining cost efficiency compared to fully fault-tolerant Tier 4 architectures.

- Central Spain at 38.0%: Central Spain leads through Madrid's position as Spain's primary network connectivity hub, largest enterprise concentration, and proximity to national government institutions. Advanced fiber infrastructure, established data center clusters, and hyperscaler campus investments continue attracting international operators to the metropolitan region.

Spain Data Center Market Overview

The Spain data center market encompasses the design, construction, and operation of all data center facilities across colocation, hyperscale, and enterprise deployment models serving the Spanish digital economy. Spain has rapidly emerged as Southern Europe's premier digital infrastructure hub, driven by accelerating enterprise cloud adoption, AI workload expansion, and robust government digitalization initiatives.

The ecosystem integrates hyperscale cloud operators, colocation providers, enterprise facility managers, renewable energy suppliers, power equipment manufacturers, connectivity providers, and regulatory bodies, setting sustainability and operational standards. Macroeconomic factors include rising digital service consumption, government incentives for digitalization, growing AI and big data analytics requirements, and Spain's strategic geographic position as a European and transatlantic digital connectivity node.

Market Dynamics

To evaluate market opportunities, Request Sample

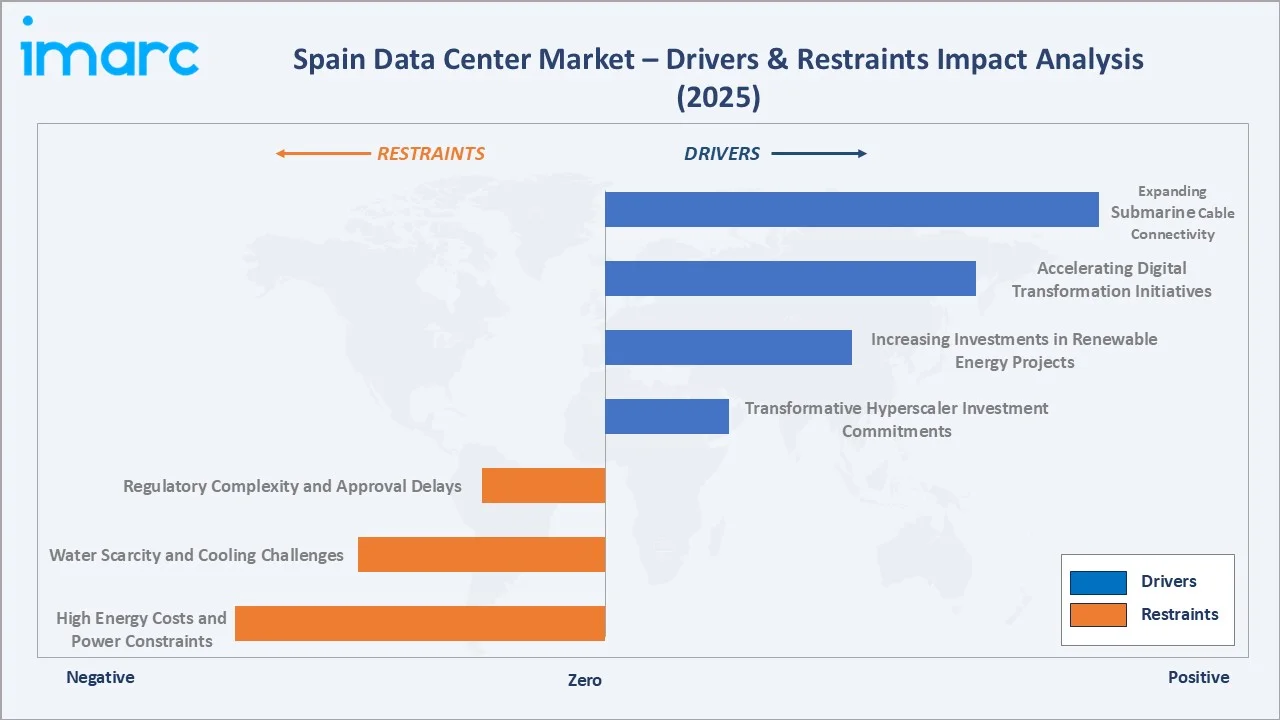

Market Drivers

- Transformative Hyperscaler Investment Commitments: Global technology giants have identified Spain as a strategic priority for European infrastructure expansion, committing unprecedented capital. In May 2024, AWS declared an investment for its Aragon region expansion, representing one of the largest single data center investments in European history. In October 2024, Blackstone committed investments to develop data center infrastructure in Aragon, reflecting hyperscaler confidence in Spain's digital infrastructure potential and renewable energy advantages.

- Increasing Investments in Renewable Energy Projects: Rising investments in renewable energy projects are strongly driving the Spain data center market by improving power availability, cost stability, and sustainability credentials. In May 2024, Digital Realty signed five power purchase agreements in France and Spain for solar and wind projects, advancing sustainability objectives and securing competitive long-term renewable energy supply. Renewable PPAs help operators control electricity costs while meeting strict carbon-reduction targets required by hyperscale cloud customers.

- Accelerating Digital Transformation Initiatives: Spanish enterprises across financial services, healthcare, retail, and manufacturing are accelerating cloud adoption and digital modernization programs that drive sustained data center demand. Government digitalization initiatives support this transformation through regulatory frameworks and investment incentives attracting international operators to expand capacity across Spain.

- Expanding Submarine Cable Connectivity: Spain's position as a landing hub for transatlantic and Africa-Europe submarine cable systems is driving network infrastructure investment that amplifies data center demand. Enhanced international bandwidth capacity positions Spanish facilities as preferred interconnection points for content delivery, cloud egress, and enterprise international traffic management across Europe, the Americas, and emerging African markets, attracting connectivity-dependent hyperscale and colocation investment.

Market Restraints

- High Energy Costs and Power Constraints: Rising electricity prices and uneven grid capacity increase operating expenses for data centers in Spain. High-density computing requires uninterrupted power, but in urban areas, infrastructure strain and limited expansion capacity delay new projects and extend development timelines. Investments in backup power systems and renewable energy integration further raise capital costs for operators, particularly in grid-constrained metropolitan markets.

- Water Scarcity and Cooling Challenges: Recurring droughts and limited water availability make traditional water-cooled systems difficult to sustain across Spain. Data center developers must adopt advanced liquid and air-based cooling systems, increasing upfront capital investment and operational complexity. Environmental pressure and public concern also create permitting challenges, especially in water-stressed regions of central and southern Spain, where data center development activity is concentrated.

- Regulatory Complexity and Approval Delays: Multiple layers of local and national regulations slow development timelines significantly. Environmental assessments, zoning rules, and sustainability mandates increase paperwork and compliance costs for developers. Policy variation across Spain's autonomous communities makes national expansion planning challenging, creating project uncertainty and discouraging rapid deployment decisions from international operators unfamiliar with regional regulatory frameworks.

Market Opportunities

- Growing Demand for AI-Optimized Data Center Infrastructure: Increasing adoption of artificial intelligence, machine learning, and high-performance computing (HPC) applications is driving investments in advanced data center facilities. Operators are focusing on developing high-density infrastructure equipped with enhanced power and cooling capabilities to support next generation computing workloads, creating new opportunities for capacity expansion and technological innovation.

- Expansion into Emerging Regional Markets: Data center development is increasingly extending beyond established metropolitan hubs as operators seek locations with greater power availability, lower land costs, and access to renewable energy resources. Secondary cities and regional markets are gaining prominence due to improved connectivity infrastructure, favorable investment conditions, and their ability to accommodate large-scale data center projects, supporting the overall growth and geographic diversification of the market.

Market Challenges

- Skilled Workforce Shortages Across Technical Disciplines: Data center operations, network engineering, and power systems management face growing talent shortages across Spain as market expansion outpaces workforce development. International competition for experienced personnel intensifies as global hyperscalers simultaneously establish Spanish operations, driving salary inflation and creating operational risk for smaller operators unable to match compensation packages offered by major cloud providers and established colocation platforms.

- Grid Infrastructure Constraints in Metropolitan Markets: Electrical grid saturation in Madrid and Barcelona is restricting new connections and extending project development timelines by several years for operators seeking capacity in Spain's primary markets. Limited transmission node availability requires developers to invest in alternative sites, renewable energy integration strategies, and energy storage solutions that increase project complexity and capital requirements beyond initial planning assumptions.

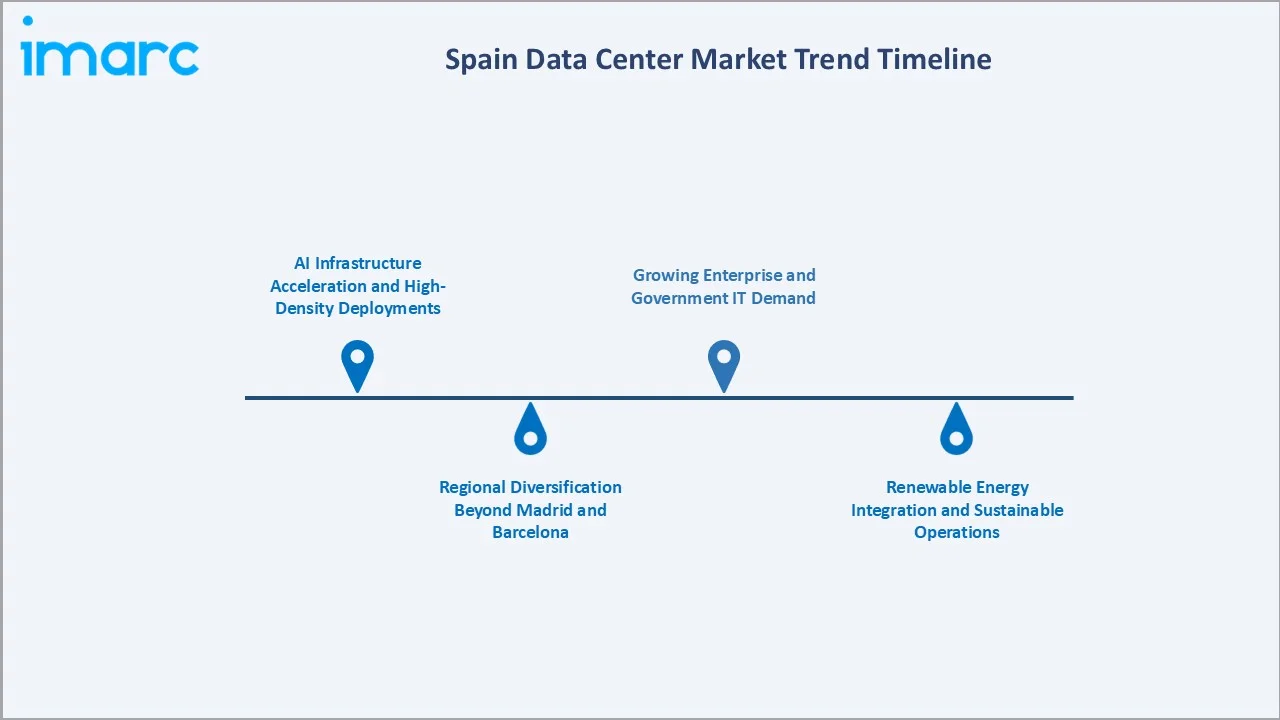

Emerging Market Trends

1. AI Infrastructure Acceleration and High-Density Deployments

Deployment of AI-ready facilities is reshaping Spain's data center landscape, with operators investing in specialized infrastructure to accommodate high-performance computing workloads. Advanced liquid immersion cooling systems manage increased rack densities supporting machine learning and generative AI applications, driving significant infrastructure differentiation among operators targeting hyperscale cloud customers with AI-intensive requirements.

2. Regional Diversification Beyond Madrid and Barcelona

Grid saturation in primary markets is driving infrastructure investment toward secondary regions offering better power availability and land accessibility. Geographic expansion enables operators to develop large-scale hyperscale campuses while avoiding grid connection delays that extend project timelines in congested metropolitan areas, creating new competitive markets across Spain.

3. Renewable Energy Integration and Sustainable Operations

Spain's abundant solar and wind resources are enabling data center operators to pursue power purchase agreements that secure long-term renewable energy access at competitive rates. Green energy credentials are increasingly required by hyperscale cloud customers with strict carbon-reduction targets, making renewable energy access a key site selection criterion. Expanding wind and solar capacity provides operators access to cleaner, more predictable energy sources critical for facilities running 24/7 operations.

4. Growing Enterprise and Government IT Demand

Enterprise digitalization and government IT modernization are major structural drivers of sustained market expansion. Businesses across finance, retail, manufacturing, and healthcare are increasingly dependent on cloud infrastructure, real-time analytics, and AI-enabled platforms. Government initiatives including e-governance, smart city programs, and public sector digital transformation are increasing demand for data storage, colocation, and disaster recovery solutions across Spanish public and private sector customers.

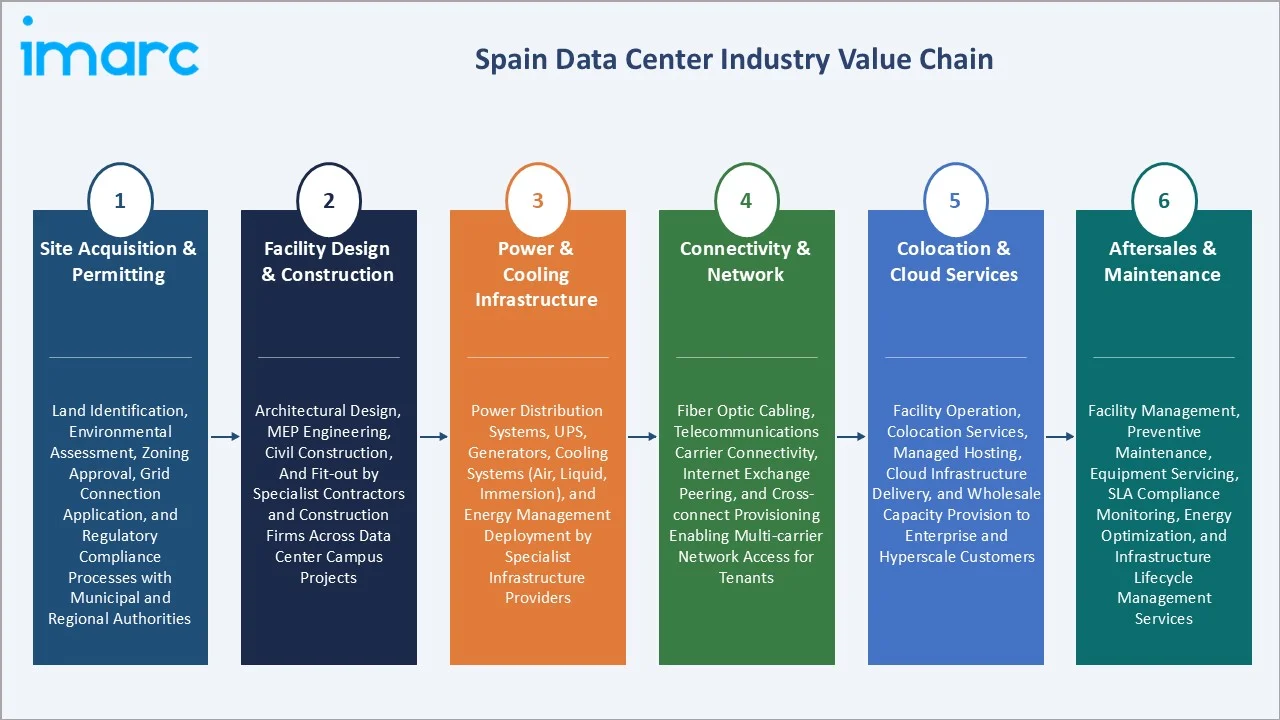

Industry Value Chain Analysis

The Spain data center value chain integrates site selection and permitting, facility design and construction, power and cooling infrastructure installation, IT equipment procurement, network connectivity provisioning, and ongoing operations and maintenance services. The value chain continues evolving toward integrated campus delivery formats bundling construction, power, and connectivity services for hyperscale operators seeking turnkey solutions.

|

Stage |

Key Activities & Participants |

|

Site Acquisition & Permitting |

Land identification, environmental assessment, zoning approval, grid connection application, and regulatory compliance processes with municipal and regional authorities |

|

Facility Design & Construction |

Architectural design, MEP engineering, civil construction, and fit-out by specialist contractors and construction firms across data center campus projects |

|

Power & Cooling Infrastructure |

Power distribution systems, UPS, generators, cooling systems (air, liquid, immersion), and energy management deployment by specialist infrastructure providers |

|

Connectivity & Network |

Fiber optic cabling, telecommunications carrier connectivity, internet exchange peering, and cross-connect provisioning enabling multi-carrier network access for tenants |

|

Colocation & Cloud Services |

Facility operation, colocation services, managed hosting, cloud infrastructure delivery, and wholesale capacity provision to enterprise and hyperscale customers |

|

Aftersales & Maintenance |

Facility management, preventive maintenance, equipment servicing, SLA compliance monitoring, energy optimization, and infrastructure lifecycle management services |

The power and cooling infrastructure stage is the Spain data center value chain's most capital-intensive and operationally critical tier, representing 35-45% of total facility construction cost. The connectivity and network stage is experiencing the most rapid evolution as submarine cable investments and internet exchange expansion strengthen Spain's position as a European digital hub.

Technology Landscape in the Spain Data Center Industry

Liquid Cooling and Immersion Technology

Liquid cooling and immersion technology is transforming Spain's data center infrastructure to support the thermal demands of AI and high-performance computing workloads. These systems enable significantly higher power densities per rack compared to traditional air cooling, supporting next-generation AI server configurations. Spanish operators are increasingly adopting direct liquid cooling and immersion solutions to differentiate facilities and attract hyperscale AI infrastructure contracts.

Software-Defined Infrastructure and Automation

Software-defined infrastructure and intelligent automation are enabling Spanish data center operators to optimize energy consumption, improve operational efficiency, and deliver dynamic capacity allocation to enterprise customers. AI-driven energy management platforms are reducing power usage effectiveness (PUE) ratios and enabling real-time optimization of cooling systems, power distribution, and IT load balancing across facility campuses.

Modular and Prefabricated Data Center Technology

Modular and prefabricated data center technology is accelerating deployment timelines in Spain by reducing on-site construction complexity and enabling faster capacity addition in response to hyperscale demand.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Data Center Size |

Large |

30.0% |

2025 |

|

Tier Type |

Tier 3 |

70.0% |

2025 |

|

Absorption |

Utilized |

70.0% |

2025 |

|

Region |

Central Spain |

38.0% |

2025 |

By Data Center Size

The Large segment leads at 30.0% in 2025, capturing enterprise requirements for scalable infrastructure between single-cabinet colocation and massive hyperscale configurations. Large facilities serve financial institutions, telecommunications providers, and multinational corporations requiring substantial computing resources, infrastructure redundancy, and carrier-neutral connectivity within cost parameters appropriate for mid-market digital transformation programs.

To access detailed market analysis, Request Sample

Massive at 24.0% reflects hyperscale-adjacent deployments from large cloud and technology companies requiring dedicated capacity at scale. Mega at 18.0% represents emerging hyperscale campus configurations from major cloud providers. Medium at 16.0% serves SME and government agency requirements. Small at 12.0% encompasses edge deployments and regional enterprise facilities serving local market requirements across Spain's secondary cities.

By Tier Type

Tier 3 leads at 70.0%, reflecting enterprise preference for N+1 redundancy configurations that enable concurrent maintainability without service interruption during routine equipment maintenance or upgrades. This infrastructure standard addresses the operational requirements of enterprise customers seeking reliable computing environments while maintaining cost efficiency compared to fully fault-tolerant Tier 4 configurations requiring 2N redundancy across all critical systems.

Tier 4 at 18.0% serves the highest-criticality enterprise applications requiring 2N redundancy, zero-downtime operations, and simultaneous maintainability across all power and cooling systems. Tier 1 and 2 at 12.0% encompasses smaller facilities, edge deployments, and lower-criticality enterprise applications where full redundancy requirements are not economically justified relative to application availability requirements.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

Central Spain |

38.0% |

Driven by Madrid's network connectivity, largest enterprise concentration, government institutions, advanced fiber infrastructure, and established hyperscaler campus presence |

|

Eastern Spain |

24.0% |

Driven by Barcelona and Valencia's digital business activity, port and submarine cable connectivity, technology startup growth, and smart city program development |

|

Northern Spain |

20.0% |

Benefits from cooler climate reducing cooling costs, cross-border data traffic with France, abundant renewable energy resources, and lower land costs enabling large-scale development |

|

Southern Spain |

18.0% |

Emerging region with rising investment, lower real estate costs, improving power infrastructure, and abundant solar energy availability supporting energy-efficient facility development |

Central Spain, at 38.0%, leads through Madrid's role as Spain's primary network hub, largest enterprise concentration, and national government presence. The region hosts the largest cloud, financial, and telecommunications customers in the country, with advanced network infrastructure and skilled workforce availability further strengthening its leadership position across all data center market segments.

Eastern Spain, at 24.0%, reflects Barcelona's established technology ecosystem and Valencia's growing connectivity infrastructure supported by port access and submarine cable systems. Northern Spain, at 20.0%, benefits from cooler climatic conditions, reducing cooling costs and cross-border connectivity with France. Southern Spain, at 18.0%, represents an emerging region capitalizing on abundant solar energy and improving grid infrastructure investments.

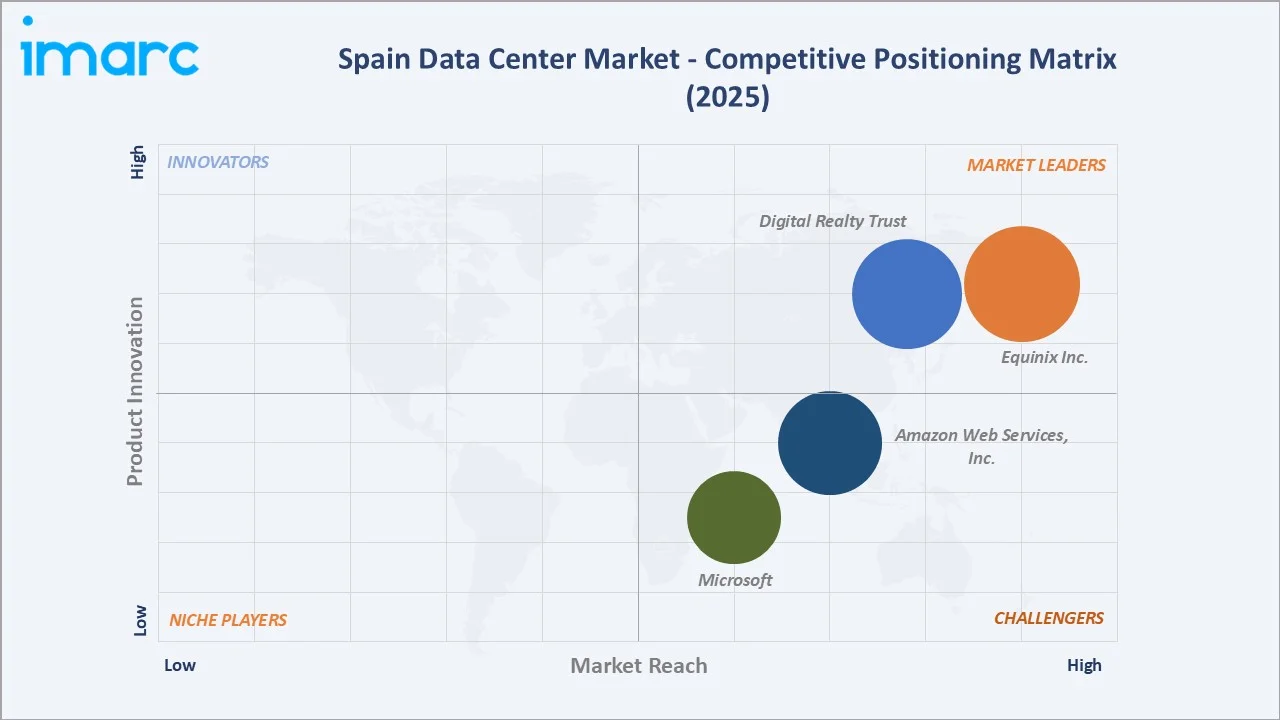

Competitive Landscape

The Spain data center market features a diverse competitive environment encompassing global hyperscalers, international colocation operators, and private equity-backed regional platform developers. Major colocation providers maintain substantial capacity portfolios concentrated in Madrid and Barcelona, offering carrier-neutral connectivity and enterprise-grade infrastructure to multinational and domestic customers. Competition increasingly centers on securing electrical grid capacity, renewable energy access, and strategic land positions enabling large-scale development.

|

Company Name |

Key Products/Services |

Market Position |

Core Strength |

|

Equinix Inc. |

Data Centers |

Market Leader |

A leading global carrier-neutral colocation provider offering interconnection-dense data center facilities and digital exchange platforms across primary markets |

|

Digital Realty Trust |

Data Centers |

Market Leader |

A major international data center REIT operating a large-scale colocation and hyperscale campus platform serving enterprise and cloud customers. |

|

Microsoft |

Microsoft Datacenters |

Strong Challenger |

A global hyperscale cloud operator providing public cloud infrastructure and enterprise services through multi-campus data center deployments. |

|

Amazon Web Services, Inc. |

AWS Data Center |

Strong Challenger |

A leading hyperscale cloud infrastructure provider with significant committed capital for regional cloud availability zone expansion |

Key players include Equinix Inc., Digital Realty Trust, Microsoft, Amazon Web Services, Inc., and others.

Key Company Profiles

Equinix, Inc.

Equinix, Inc. is a US-based global digital infrastructure company and the world's largest carrier-neutral colocation provider with a strong presence in the Spanish data center market through its International Business Exchange (IBX) facilities in Madrid and Barcelona, delivering interconnection-dense colocation services and digital exchange platforms.

- Key Products: Data Centers

- Strategic Focus: Expanding interconnection-dense colocation campuses and Platform Equinix ecosystem services across Spain, leveraging carrier-neutral positioning to serve hyperscale cloud on-ramp and enterprise hybrid IT demand while investing in renewable energy integration across European operations.

Digital Realty Trust

Digital Realty Trust is a US-based data center real estate investment trust (REIT) with a substantial Spanish presence through its direct hyperscale campus developments in Madrid and Barcelona, operating as one of the largest colocation providers in the Spanish market.

- Key Products: Data Centers

- Recent Developments: In May 2026, Digital Realty inaugurated its first data center in Barcelona, Spain, strengthening its presence across the Mediterranean region and expanding its digital infrastructure footprint on the Iberian Peninsula.

- Strategic Focus: Developing interconnected data center campuses aligned with a digital global framework, pursuing renewable power purchase agreements to meet customer sustainability requirements, and expanding hyperscale colocation capacity across primary and secondary Spanish markets.

Market Concentration Analysis

The Spain data center market is moderately concentrated at the colocation operator level, with the top 4-5 key players collectively maintaining a significant share of professional colocation capacity in the primary Madrid and Barcelona markets. Hyperscaler cloud providers account for a growing share of total capacity as committed investments in large-scale campus developments come online through the forecast period.

Market concentration is evolving as private equity investment drives platform consolidation among smaller colocation operators, while hyperscaler capacity additions expand the total addressable market faster than any single operator concentration can offset. The entry of new international operators, secondary city market development, and AI infrastructure specialist providers are progressively diversifying the competitive landscape beyond the established Madrid and Barcelona colocation platforms.

Investment & Growth Opportunities

Highest Growth Segments

Large data center facilities at ~9.2% CAGR, Tier 3 infrastructure at ~8.7% CAGR, Central Spain regional development at ~9.5% CAGR, AI-ready high-density facilities, renewable-powered hyperscale campus development, and secondary city colocation platforms represent the highest-growth investment vectors through 2034. AI infrastructure, submarine cable-connected interconnection hubs, and government cloud migration programs create premium investment opportunities across the forecast period.

Emerging Investment Opportunities

Secondary city data center development in Valencia, Zaragoza, Málaga, and Bilbao represents the highest-opportunity emerging investment category, combining lower land and energy costs with improving grid infrastructure and growing regional enterprise demand. These markets offer development economics superior to constrained primary markets while capturing structural demand from enterprises and public sector organizations outside Madrid and Barcelona.

Investment Themes

- Renewable energy-powered hyperscale campus development: Spain's abundant solar and wind resources enable competitive long-term PPAs that attract sustainability-focused hyperscalers and reduce operational cost uncertainty. Operators securing renewable energy access in advance of grid constraint resolution gain sustainable cost advantages over competitors dependent on conventional electricity market pricing.

- AI infrastructure investment for premium colocation demand: High-density AI computing facilities requiring advanced liquid cooling and power densities of 50-100 kW per rack represent premium investment opportunities. Cloud providers and enterprise AI adopters accelerating Spanish workload deployment create demand for differentiated infrastructure not available in standard colocation facilities.

- Submarine cable-connected interconnection hub development: Data center campuses co-located with submarine cable landing stations and major internet exchange points command premium colocation pricing through structural interconnection demand independent of broader economic cycles. Spain's cable landing position creates unique asset development opportunities unavailable to landlocked European markets.

Future Market Outlook (2026-2034)

The Spain data center market is projected to grow from USD 3.76 Billion in 2025 to USD 8.12 Billion by 2034, delivering an 8.94% CAGR over the forecast period. The market's anchor value of USD 5.77 Billion in 2030 represents Spain's digital infrastructure sector at a significant commercial inflection as committed hyperscaler campuses come fully online and secondary city markets mature into substantial standalone markets. Large data centers will consolidate their dominant position as enterprise demand scales with digital transformation maturity.

Three structural forces define Spain data center market growth through 2034 with exceptional confidence. Continued hyperscaler investment from AWS, Microsoft, Google, and Meta will deliver transformative capacity additions creating a multiplier effect on colocation and connectivity demand. Spain's renewable energy transition will reinforce its competitive position as Europe's most cost-effective sustainable data center destination. Enterprise and government cloud migration will sustain domestic demand growth independent of international investment cycles, ensuring market resilience through forecast horizon.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025), including data center facility directors, hyperscale cloud infrastructure leads, colocation sales executives, renewable energy project developers, and government digitalization program managers across Spain's primary and emerging data center markets in Madrid, Barcelona, Valencia, and Zaragoza.

Secondary Research

Secondary research encompassed company annual reports; IMARC Group Spain cloud market data; Spanish Ministry of Economic Affairs digital infrastructure publications; Red Eléctrica de España grid capacity data; submarine cable investment announcements and landing station databases; European Data Centre Association reports; and regional autonomous community investment promotion documentation. Over 50 secondary sources were reviewed and validated.

Forecasting Models

Market revenue forecasts were developed using demand-side bottom-up model: enterprise cloud migration volumes by sector multiplied by average colocation revenue per megawatt; hyperscaler committed investment schedules phased over construction and ramp-up timelines; government digital infrastructure program expenditure projections; and secondary city market development timing aligned with grid infrastructure upgrade schedules confirmed by Spanish electricity network operators.

Spain Data Center Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Data Center Sizes Covered | Large, Massive, Medium, Mega, Small |

| Tier Types Covered | Tier 1 and 2, Tier 3, Tier 4 |

| Absorptions Covered |

|

| Regions Covered | Northern Spain, Eastern Spain, Southern Spain, Central Spain |

| Companies Covered | Equinix Inc., Digital Realty Trust, Microsoft, Amazon Web Services, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Spain Data Center Market Report

The Spain data center market reached USD 3.76 Billion in 2025, driven by transformative hyperscaler investment commitments, accelerating enterprise cloud adoption, Spain's strategic position as a European digital gateway with transatlantic submarine cable connectivity, and Large data centers leading at 30.0%, Tier 3 at 70.0%, and Central Spain commanding 38.0% regional market share through Madrid's network concentration and enterprise density.

The Spain data center market grows at 8.94% CAGR during 2026-2034, reaching USD 8.12 Billion by 2034. This growth reflects sustained hyperscaler capital deployment, enterprise digital transformation programs, AI infrastructure expansion, secondary city market development, and renewable energy integration reinforcing Spain's competitive position as Southern Europe's most attractive sustainable data center destination.

Large data centers lead at 30.0%, capturing enterprise requirements for scalable infrastructure between single-cabinet colocation and massive hyperscale configurations. This segment benefits from balanced economics enabling efficient power utilization while maintaining flexibility for diverse tenant requirements across financial services, telecommunications, and multinational corporate customers undergoing digital transformation programs.

Tier 3 leads at 70.0% through enterprise preference for N+1 redundancy configurations balancing operational reliability with cost efficiency. Concurrent maintainability without service interruption supports mission-critical applications across banking, e-commerce, and telecommunications sectors where downtime carries significant financial implications, but absolute Tier 4 fault tolerance represents overengineering relative to operational requirements.

Central Spain leads at 38.0% through Madrid's position as Spain's primary network connectivity hub, largest enterprise concentration, and national government institution proximity. Advanced fiber infrastructure established data center clusters, and concentrated hyperscaler campus investments in the metropolitan region continue attracting both domestic and international operators across colocation and hyperscale facility formats.

Leading companies include Equinix Inc., Digital Realty Trust, Microsoft, Amazon Web Services, Inc., and others.

The Spain data center market is projected to reach approximately USD 5.77 Billion by 2030, with committed hyperscale campuses from AWS and Microsoft fully operational in Aragón, Large and Tier 3 segments maintaining market leadership, secondary city markets in Valencia and Zaragoza reaching significant commercial scale, and renewable energy-powered facilities establishing Spain as Southern Europe's most cost-competitive sustainable data center destination.

Three priority investment opportunities: renewable energy-powered hyperscale campus development leveraging Spain's solar and wind advantages for competitive PPA economics; AI-ready high-density infrastructure meeting liquid-cooling requirements for next-generation machine learning workloads; and secondary city colocation platform development in Valencia, Zaragoza, and Málaga capturing enterprise demand with superior development economics compared to grid-constrained primary markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)