Specialty Food Ingredients Market Report by Product Type (Specialty Sensory Ingredients, Specialty Functional Ingredients), Source (Natural, Synthetic), Application (Beverages, Bakery and Confectionery, Dairy Products, Processed Foods, Meat Products, Savory and Sweet Snacks, and Others), Distribution Channel (Distributors, Manufacturers), and Region 2026-2034

Specialty Food Ingredients Market Size:

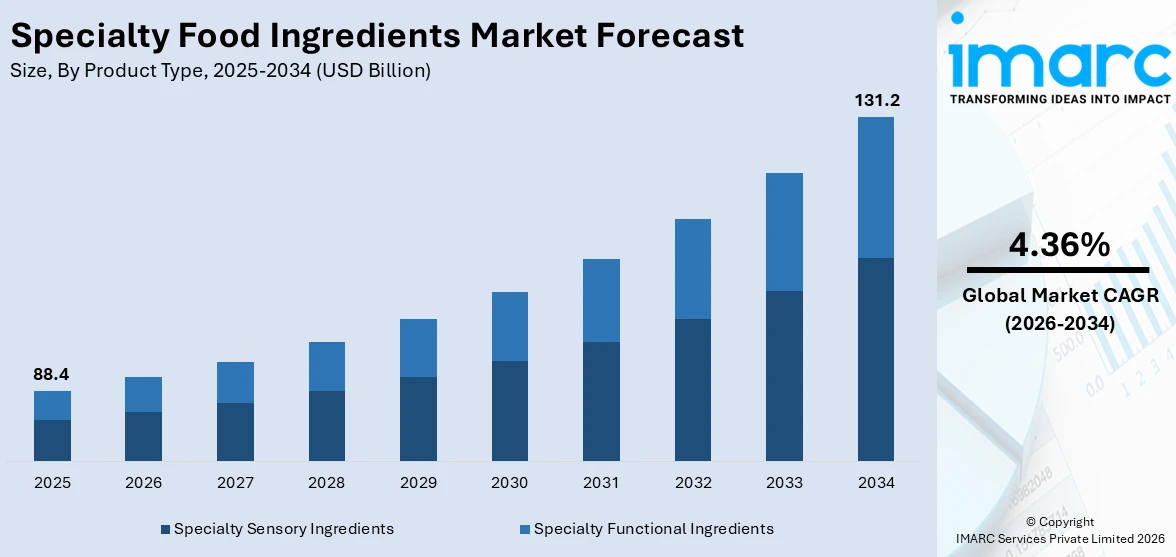

The global specialty food ingredients market size reached USD 88.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 131.2 Billion by 2034, exhibiting a growth rate (CAGR) of 4.36% during 2026-2034. North America leads the market, driven by a significant demand for novel, premium ingredients influenced by consumer desires for healthier and more sustainable food choices. The changing consumer preferences for unique and healthier food options, increasing health consciousness, a focus on technological advancements in ingredient processing, and rising demand for convenience and diverse culinary experiences are some of the other factors driving the market growth.

Market Size & Forecasts:

- Specialty food ingredients market was valued at USD 88.4 Billion in 2025.

- The market is projected to reach USD 131.2 Billion by 2034, at a CAGR of 4.36% from 2026-2034.

Dominant Segments:

- Product Type: Specialty sensory ingredients (flavors) hold the biggest market share because they improve the sensory experience of food items, addressing consumers’ increasing demand for distinctive, thrilling taste profiles. Their adaptability across different uses, along with a growing demand for customized and high-quality items, further supports their market leadership.

- Source: Natural dominates the specialty food ingredients market owing to its increasing attraction to health-oriented buyers looking for clean-label, eco-friendly products. As awareness about the advantages of natural sources grows, producers focus on these components to meet consumer preferences for cleanliness, limited processing, and environmental accountability, boosting the market demand.

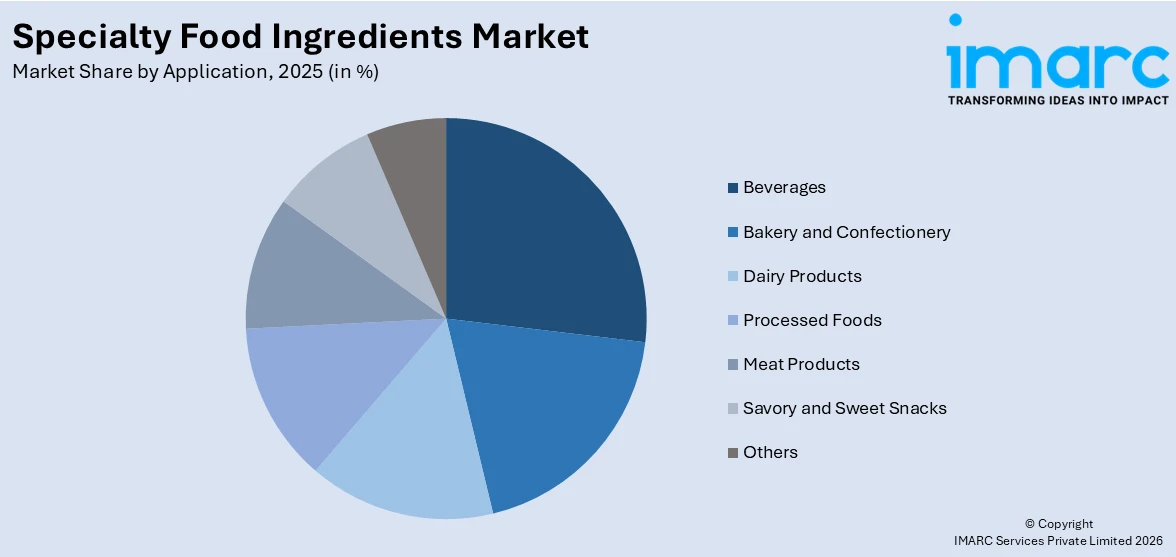

- Application: Beverages account for the largest market share attributed to rising consumer interest in health-focused and functional beverages. The rising demand for unique flavors, natural components, and personalized nutrition in drinks fosters the use of specialty ingredients, establishing them as a vital area for product distinction and market expansion.

- Distribution Channel: Distributors represent the largest segment due to their vast networks, allowing for effective supply chain management and broad product distribution. Their connections with manufacturers and retailers guarantee prompt delivery, competitive pricing, and access to a diverse selection of specialty ingredients, aiding in market growth.

- Region: North America leads the market, driven by a significant demand for novel, premium ingredients influenced by consumer desires for healthier and more sustainable food choices. The area utilizes cutting-edge food technology, strong manufacturing capabilities, and a solid consumer market centered on health and wellness trends.

Key Players:

- The leading companies in specialty food ingredients market include Archer Daniels Midland Company, Associated British Foods Plc, Cargill Incorporated, Chr. Hansen Holding A/S, DuPont de Nemours Inc., Givaudan, Ingredion Incorporated, Kerry Group plc, Koninklijke DSM N.V., Sensient Technologies Corporation, and Tate & Lyle plc.

Key Drivers of Market Growth:

- Sustainability and Ethical Sourcing: Sustainability is a critical factor influencing consumer decisions regarding food items. Initiatives such as transparent supply chains and environmentally friendly packaging are becoming crucial distinguishing factors, bolstered by regulations encouraging sustainable production methods.

- Plant-Based and Alternative Proteins: Plant-based diets are driving the need for non-animal protein alternatives that replicate traditional proteins in flavor, consistency, and nutritional value. This transition is leading to significant investment in research activities in plant proteins, algae-based products, and cultured components.

- Technological Advancements in Ingredient Innovation: Innovative techniques like precision fermentation, enzyme engineering, and microencapsulation are transforming ingredient performance. These developments improve stability, nutrition, and taste while allowing sustainable sourcing. Automation and digital technologies enhance production efficiency, enabling businesses to produce innovative, clean-label items that satisfy the evolving needs of today's consumers.

- Increasing Health and Wellness Focus: Rising awareness about the connection between nutrition and health is catalyzing the demand for functional ingredients that enhance wellness without sacrificing flavor. Businesses are concentrating on clean-label products, natural sweeteners, and plant-based proteins while broadening their offerings to target immunity, heart health, and digestive wellness.

- Regulatory and Food Safety Standards: Stringent international food regulations encourage companies to focus on product safety and transparency. Adhering to labeling standards and authorized additives fosters consumer confidence and access to the market. These rules also encourage innovation as companies develop safer, natural components that align with changing safety standards and clean-label demands.

- Growing Geriatric Population: An aging population is driving the need for components that enhance bone strength, joint flexibility, and heart health. Bioactive peptides, collagen, and enriched minerals are gaining popularity. Businesses are developing accessible formats to satisfy the increasing demand for functional foods that enhance longevity and improve quality of life.

Future Outlook:

- Strong Growth Outlook: The specialty food ingredients market is poised for strong growth owing to rising consumer demand for healthier, more sustainable food options, coupled with innovations in food technology and product development. Increasing awareness about functional ingredients and diverse dietary needs further offers a favorable market outlook.

- Market Evolution: The specialty food ingredients market is evolving as individual preferences shift towards healthier, natural, and functional foods. Ongoing advancements in technology and production methods, along with a growing emphasis on sustainability, are driving innovation and expanding the range of specialty ingredients available in the market.

Consumers are increasingly looking for unique and diverse flavors in their food. This desire for novel experiences is driving the need for unique ingredients, as individuals seek out exotic or unusual flavors to enhance their meals and improve the dining experience. Furthermore, improvements in food processing, preservation, and extraction methods are facilitating the development of novel, specialized ingredients. This advancement enables producers to create distinctive and practical ingredients that address particular consumer demands, contributing to the specialty food ingredients market growth. Apart from this, the clean label trend, in which consumers seek clarity regarding food components, is resulting in the adoption of unique ingredients that are natural, minimally processed, and devoid of artificial additives. This shift toward cleaner food products is leading to higher demand for high-quality, recognizable ingredients.

To get more information on this market Request Sample

Specialty Food Ingredients Market Trends:

Sustainability and Ethical Sourcing

The growing awareness about environmental issues is influencing consumer choices, resulting in high demand for ingredients made through sustainable methods. Businesses are concentrating on lowering carbon emissions, utilizing renewable resources, and decreasing waste during the manufacturing process. The ethical procurement of raw materials, featuring fair trade certifications and traceable supply chains, is becoming a key selling proposition for food brands. This change is also promoting investment in repurposing food by-products and creating sustainable packaging to match consumer values. Ingredient producers are creating innovative plant-based and alternative options that use fewer resources, guaranteeing environmental accountability and cost-effectiveness. Governments and regulatory agencies are promoting sustainable practices by establishing guidelines and incentives for businesses to implement more eco-friendly technologies. The focus on sustainability is not merely a marketing edge but a competitive necessity, as brands that do not meet environmental standards risk losing consumer confidence. In line with this trend, in 2025, Singapore-based RELSUS™ launched a state-of-the-art plant protein facility in Ujjain, India, using its Ultra-Precise Filtration™ technology to produce clean, functional, and sustainable ingredients.

Rise of Plant-Based and Alternative Proteins

The increasing transition towards plant-based diets and flexitarian lifestyles is driving the demand for specialty ingredients derived from non-animal sources. Consumers are frequently seeking options that mimic the texture, flavor, and nutritional advantages of conventional proteins, encouraging advancements in plant-based proteins, algae-sourced products, and cultured ingredients. This increase in interest is motivating companies to enhance the quality, functionality, and overall sensory experience of these items. In 2025, Zyra Protein launched a plant-derived protein powder using just four components—pea protein, date powder, strawberry powder, and salt. The non-GMO, vegan, and gluten-free formulation not only promotes healthy living but also finances charitable efforts for underprivileged communities. As plant-based diets gain popularity, ingredient suppliers providing adaptable, eco-friendly, and ethically sound solutions are establishing a more robust presence in the changing specialty food ingredients sector.

Technological Advancements in Ingredient Innovation

Innovative technologies in food science and biotechnology are transforming the specialty ingredients industry growth. Precision fermentation, enzyme modification, and microencapsulation methods are facilitating the development of high-quality ingredients with enhanced stability, bioavailability, and taste characteristics. These developments assist manufacturers in providing products that satisfy intricate consumer needs, including sustainable sourcing and improved nutritional value. Technology is facilitating the extraction of new compounds from natural sources, leading to plant-derived alternatives and enhanced functional ingredients. Automation and digital technologies are enhancing the manufacturing process, lowering expenses, and guaranteeing uniform quality. Ingredient firms are investing significantly in research operations to produce innovative solutions that provide clean-label attractiveness while preserving product effectiveness. These developments are enhancing not just the sensory and nutritional traits of foods but are also creating new possibilities for customized nutrition and specific dietary products designed for individual health requirements.

Specialty Food Ingredients Market Growth Drivers:

Growing Health and Wellness Focus

Consumer demand for healthier eating is transforming the specialty food ingredients market, driven by increasing recognition about the importance of nutrition for long-term health. Producers are creating natural sweeteners, plant-derived proteins, and functional fibers to improve nutritional value while preserving flavor and quality. The clean-label trend, where shoppers favor items with few additives and familiar ingredients, is encouraging businesses to focus on developing innovative formulations aimed at lifestyle-related health issues. For example, in 2025, the fitness brand HRX launched a plant-based shake made with oat milk that offers 25g of protein in each 200ml serving, and is free from dairy, lactose, and processed sugars, fitting these trends seamlessly. These products showcase the industry's emphasis on functional aspects, such as enhanced vitamins and probiotics, along with approaches for immunity, digestive health, and heart wellness. Ingredient suppliers are expanding their offerings to address these needs and maintain competitiveness in a progressively health-aware global market.

Regulatory and Food Safety Standards

Producers are allocating resources for enhanced testing and quality assurance processes to comply with food safety standards. Adhering to these standards not only avoids product recalls but also enhances consumer trust in ingredient quality. Laws regarding clean-label assertions, permissible additives, and nutritional enhancement are encouraging companies to redesign products with safer and more natural ingredients. Ingredient suppliers are collaborating with regulatory bodies to guarantee that their products comply with global standards, crucial for accessing new markets. This regulatory pressure is encouraging innovation, as firms aim to develop ingredients that uphold performance while complying with changing safety and labeling standards. In this highly competitive market, being proactive about compliance and transparency is a key factor for long-term growth and consumer acceptance.

Aging Population and Functional Health Needs

The increasing worldwide geriatric population is driving the need for foods that promote healthy aging, concentrating on components that improve bone density, joint mobility, and heart health. Specialty ingredients, including bioactive peptides, collagen, and enhanced minerals, are gaining popularity for their effectiveness in tackling health issues related to aging. Producers are focusing on creating easily digestible formats, such as soft foods, powders, and liquid supplements, to address the needs of older customers. The World Health Organization (WHO) states that by 2030, one in every six individuals globally will be aged 60 or above, and this figure is projected to increase to 2.1 billion by 2050. This demographic change is generating a steady and expanding market for functional foods and supplements designed to enhance quality of life, offering substantial long-term prospects for ingredient providers concentrating on nutrition solutions for the aging population.

Specialty Food Ingredients Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product type, source, application, and distribution channel.

Breakup by Product Type:

- Specialty Sensory Ingredients

- Enzymes

- Emulsifiers

- Flavors

- Colorants

- Others

- Specialty Functional Ingredients

- Vitamins

- Minerals

- Antioxidants

- Preservatives

- Others

Specialty sensory ingredients (flavors) accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product type. This includes specialty sensory ingredients (enzymes, emulsifiers, flavors, colorants, and others) and specialty functional ingredients (vitamins, minerals, antioxidants, preservatives, and others). According to the report, specialty sensory ingredients (flavors) represented the largest segment.

The escalating demand for specialty sensory ingredients, including flavors is primarily driven by the ever-growing consumer inclination toward unique and enhanced sensory experiences in food products. These ingredients play a pivotal role in elevating the taste, texture, and visual appeal of food items, meeting the rising consumer expectations for novel and indulgent gastronomic encounters. As consumers seek heightened sensory pleasures in their culinary choices, the demand for specialty sensory ingredients continues to surge, fostering innovation and differentiation in the global food industry.

On the other hand, the surging demand for specialty functional ingredients, encompassing vitamins, minerals, antioxidants, and preservatives, is primarily fueled by the increasing health consciousness among consumers. As individuals prioritize wellness and nutrition, there is a growing inclination toward food products fortified with functional ingredients that offer specific health benefits. This trend is propelling the specialty food ingredients market, with consumers actively seeking products that satiate taste preferences as well as contribute to their overall well-being.

Breakup by Source:

- Natural

- Synthetic

Natural holds the largest share in the industry

A detailed breakup and analysis of the market based on the source have also been provided in the report. This includes natural and synthetic. According to the report, natural accounted for the largest market share.

The growing consumer preference for clean-label and minimally processed products represents one of the main factors catalyzing the demand for specialty food ingredients sourced from natural origins. With a heightened focus on health and sustainability, consumers are seeking food items with ingredients derived from natural sources, avoiding artificial additives. This shift in preference has led to an increased demand for natural specialty food ingredients, including flavors, colors, and sweeteners, as consumers prioritize products that align with their desire for wholesome and authentic culinary experiences.

Apart from this, the rising need for consistency, cost-effectiveness, and technological advancements is spurring the adoption of specialty food ingredients sourced synthetically as they offer a reliable and reproducible source of flavors, colors, and other additives, ensuring uniformity in taste and appearance. Moreover, advancements in food science and technology have enabled the creation of synthetic ingredients that mimic natural counterparts while providing certain functional benefits. The synthetic specialty food ingredients market caters to the food industry's requirements for stable and economically viable solutions, especially in mass production scenarios, thereby bolstering the market growth.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Beverages

- Bakery and Confectionery

- Dairy Products

- Processed Foods

- Meat Products

- Savory and Sweet Snacks

- Others

Beverages represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the application. This includes beverages, bakery and confectionery, dairy products, processed foods, meat products, savory and sweet snacks, and others. According to the report, beverages represented the largest segment.

The rising consumer preference for unique and innovative drink experiences is fueling the adoption of specialty food ingredients in the beverage sector. Specialty ingredients such as natural flavors, exotic extracts, and functional additives are incorporated into beverages to enhance taste profiles, provide health benefits, and differentiate products in a crowded market. As consumers seek diverse and premium beverage options, there is an increasing demand for specialty ingredients in the beverage industry, which is contributing to the market growth.

In addition to this, the demand for specialty food ingredients in bakeries and confectionery is driven by the need for unique flavors, textures, and extended shelf life, meeting consumer expectations for indulgent and high-quality treats.

Concurrently, the expanding use of specialty ingredients in the dairy sector is fueled by the pursuit of enhanced nutritional profiles, improved taste, and texture, as consumers increasingly seek premium and functional dairy options.

Along with this, the processed foods segment sees a surge in demand for specialty ingredients to ensure stability, flavor enhancement, and nutritional fortification, meeting the consumer demand for convenient and high-quality processed food items.

Furthermore, the widespread product utilization in meat products due to its role in improving taste, texture, and shelf life, catering to the evolving preferences of consumers for unique and flavorful meat-based offerings is aiding in market expansion.

In line with this, the extensive demand for specialty ingredients in snacks propelled by the need for bold flavors, unique textures, and functional benefits, aligning with the growing consumer preference for on-the-go snack options is influencing the market growth.

Across various other food applications, the demand for specialty food ingredients is characterized by a need for differentiation, whether through natural or synthetic sources, catering to specific consumer preferences and industry requirements.

Breakup by Distribution Channel:

- Distributors

- Manufacturers

Distributors exhibit a clear dominance in the market

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes distributors and manufacturers. According to the report, distributors accounted for the largest market share.

The desire for efficient supply chain management and broader market reach is propelling the demand for specialty food ingredients through the distributor channel which plays a crucial role in connecting manufacturers of specialty ingredients with a diverse range of food producers. As the global food industry seeks diverse and high-quality components, distributors streamline the process of sourcing and delivering specialty ingredients, ensuring a seamless flow of products to meet the dynamic demands of manufacturers and consumers, which is acting as another significant growth-inducing factor.

In contrast, the need for direct access to high-quality and customized components is fueling the demand for specialty food ingredients through the manufacturer channel. Manufacturers play a pivotal role in shaping the demand for specialty ingredients by incorporating them into diverse food products. This direct engagement allows manufacturers to innovate and differentiate their offerings, meeting the evolving preferences of consumers. As the food industry continues to prioritize unique formulations and sensory experiences, manufacturers contribute significantly to the growth and dynamism of the specialty food ingredients market.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest specialty food ingredients market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America’s heightened focus on health and wellness, evolving consumer preferences for unique flavors and textures, and a robust food industry that prioritizes innovation are providing an impetus to the market growth. As consumers increasingly seek diverse and high-quality food options, manufacturers in the region are incorporating specialty ingredients to meet these demands. Additionally, a growing awareness of the link between diet and health is driving the adoption of specialty ingredients that contribute to improved nutritional profiles, further fueling market growth in the region.

Besides this, Europe’s rich culinary heritage, a focus on natural and clean-label products, and consumer preferences for unique flavors are also positively impacting the growth of the specialty food ingredients market.

Moreover, in the Asia Pacific, a rising population, increasing urbanization, and a growing middle class contribute to the demand for diverse and premium food options, fostering the growth of specialty food ingredients.

Concurrent with this, the cultural diversity across the Middle East and Africa region combined with an increasing preference for natural and clean-label products and surging the demand for unique and authentic flavors are influencing the market growth.

Additionally, Latin America is experiencing a growing demand for specialty food ingredients due to a rich culinary tradition and a rising middle-class population. Consumers in the region seek diverse and premium food experiences, driving market growth.

Leading Key Players in the Specialty Food Ingredients Industry:

The global specialty food ingredients market exhibits a dynamic and competitive landscape characterized by the presence of key players striving for market dominance. Major companies are actively engaged in R&D to innovate and introduce novel specialty ingredients that cater to changing consumer preferences. These companies often focus on strategic collaborations, partnerships, and acquisitions to expand their product portfolios and global reach. The market is also influenced by the presence of regional and local players, contributing to the diversity of offerings. Additionally, the competitive dynamics are shaped by the constant pursuit of clean-label solutions, sustainable sourcing, and technological advancements. As the industry evolves, the competitive landscape continues to witness new entrants and partnerships, reflecting the ongoing efforts to meet the demands of a discerning consumer base.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Archer Daniels Midland Company

- Associated British Foods Plc

- Cargill Incorporated

- Chr. Hansen Holding A/S

- DuPont de Nemours Inc.

- Givaudan

- Ingredion Incorporated

- Kerry Group plc

- Koninklijke DSM N.V.

- Sensient Technologies Corporation

- Tate & Lyle plc

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News:

- In July 2025, Prodalim launched its Coloring Foodstuffs and Natural Colors product lines, expanding its portfolio of clean-label, plant-based, upcycled ingredients. These natural color solutions, derived from fruits, vegetables, and other natural sources, offer vibrant hues for various food and beverage applications while ensuring stability and regulatory compliance. The launch strengthens Prodalim’s position as an innovation partner in sustainable food and beverage ingredients.

- In July 2025, Austria-based Revo Foods launched Minced Fungi Protein, a high-protein, low-fat product made from fermented mycoprotein with just four ingredients. Each 160g pack offers 25g of protein and all nine essential amino acids, boasting a Nutri-Score “A” rating. The product targets fitness-conscious consumers and is now available via Revo’s online store and select European retailers.

- In July 2025, Novita Foods Inc. launched MmMm Rice Pudding in four all-natural, gluten-free flavors, starting in the Metro New York area. The new flavors—Lemon Berry, Mango, Vanilla Chocolate Chip, and Vanilla—aim to capture the nostalgic taste of classic American diner desserts. CEO Pervez highlighted the brand's focus on quality, local ingredients, and digestive-friendly indulgence.

- In June 2025, Italian specialty food company Toschi Vignola announced plans to expand operations in India, citing the country's growing economy and rising demand for Western foods. CEO Stefano Toschi highlighted India’s evolving food preferences and increasing appetite for premium products like syrups and coffee solutions.

- In April 2025, ICL Food Specialties announced its participation in IFFA 2025 in Frankfurt, showcasing ingredient solutions to enhance texture, stability, taste, and mouthfeel in meat, poultry, and seafood products. A key highlight is the launch of Rovitaris SprouTx, a textured soy protein designed to eliminate the typical "beany" taste in plant-based meats. ICL aims to support next-gen alternative proteins with improved taste and performance.

- In August 2024, Above Food announced its acquisition of The Redwood Group’s Specialty Crop Food Ingredients Division for $34 million, marking its first US-based sourcing and manufacturing expansion. This move strengthened its ‘Seed-to-Fork’ strategy and North American footprint.

- In December 2023, Kerry Group plc, entered into a definitive agreement to acquire part of the global lactase enzyme business of Chr. Hansen Holding A/S and Novozymes A/S. The acquisition, which includes NOLA® Products, will further enhance Kerry’s biotechnology solutions capability.

- In December 2023, Archer Daniels Midland Company (ADM) acquired Revela Foods, a firm specializing in dairy flavor ingredients and solutions. This acquisition is set to enhance ADM's capabilities in the global dairy and savory flavors portfolio.

- In June 2023, Associated British Foods announced the complete acquisition of dairy firm National Milk Records.

Specialty Food Ingredients Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Sources Covered | Natural, Synthetic |

| Applications Covered | Beverages, Bakery and Confectionery, Dairy Products, Processed Foods, Meat Products, Savory and Sweet Snacks, Others |

| Distribution Channels Covered | Distributors, Manufacturers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Archer Daniels Midland Company, Associated British Foods Plc, Cargill Incorporated, Chr. Hansen Holding A/S, DuPont de Nemours Inc., Givaudan, Ingredion Incorporated, Kerry Group plc, Koninklijke DSM N.V., Sensient Technologies Corporation, Tate & Lyle plc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the specialty food ingredients market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global specialty food ingredients market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the specialty food ingredients industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Specialty Food Ingredients Market Report

The global specialty food ingredients market was valued at USD 88.4 Billion in 2025.

We expect the global specialty food ingredients market to exhibit a CAGR of 4.36% during 2026-2034.

The rising demand for specialty food ingredients, such as colors, emulsifiers, enzymes, proteins, preservatives, flavor enhancers, etc., as they aid in reducing the food waste and improving taste, texture, and appearance of dishes, is primarily driving the global specialty food ingredients market.

The sudden outbreak of the COVID-19 pandemic has led to the changing consumer inclination from conventional brick-and-mortar distribution channels towards online retail platforms for the purchase of specialty food ingredients.

Based on the product type, the global specialty food ingredients market has been divided into specialty sensory ingredients and specialty functional ingredients, where specialty sensory ingredients, including flavors, currently exhibit a clear dominance in the market.

Based on the source, the global specialty food ingredients market can be categorized into natural and synthetic. Currently, natural accounts for the majority of the global market share.

Based on the application, the global specialty food ingredients market has been segregated into beverages, bakery and confectionery, dairy products, processed foods, meat products, savory and sweet snacks, and others. Among these, beverages currently exhibit a clear dominance in the market.

Based on the distribution channel, the global specialty food ingredients market can be bifurcated into distributors and manufacturers. Currently, distributors hold the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global specialty food ingredients market include Archer Daniels Midland Company, Associated British Foods Plc, Cargill Incorporated, Chr. Hansen Holding A/S, DuPont de Nemours Inc., Givaudan, Ingredion Incorporated, Kerry Group plc, Koninklijke DSM N.V., Sensient Technologies Corporation, and Tate & Lyle plc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade