Sports Fishing Equipment Market Size, Share, Trends and Forecast by Product Type, Application, End User, Distribution Channel, and Region, 2026-2034

Sports Fishing Equipment Market Size, Share, Trends & Forecast (2026-2034)

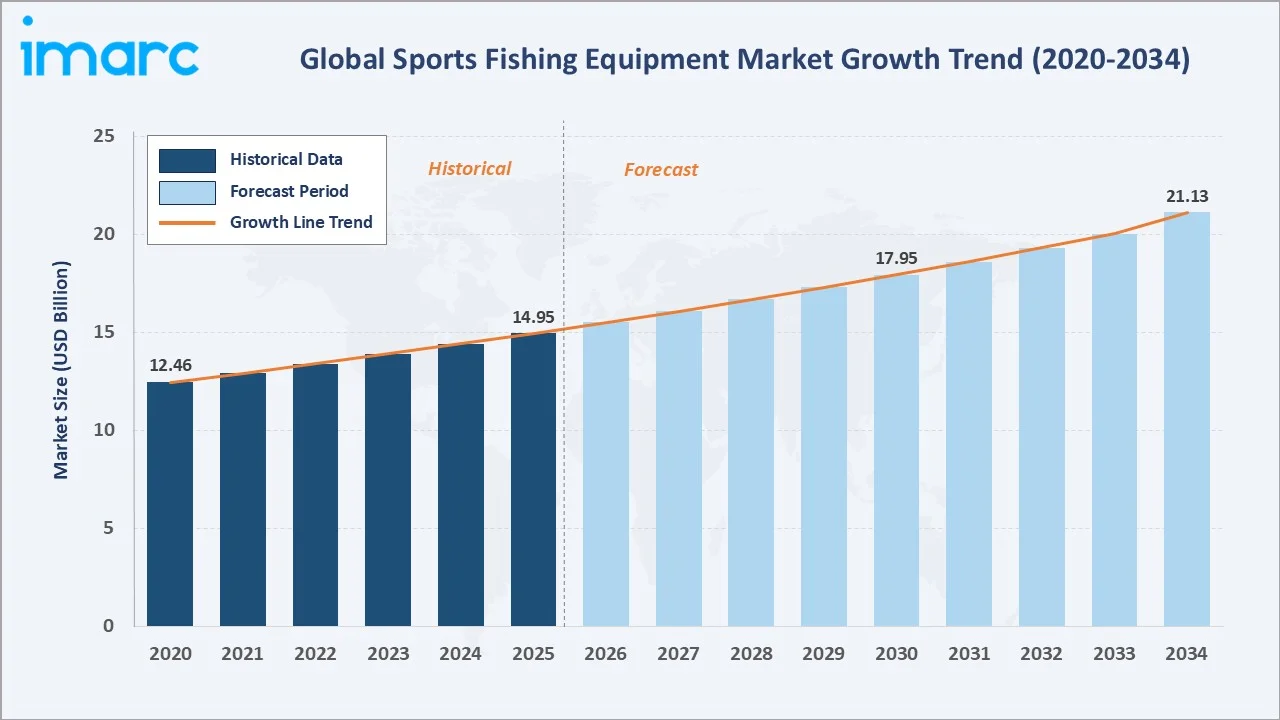

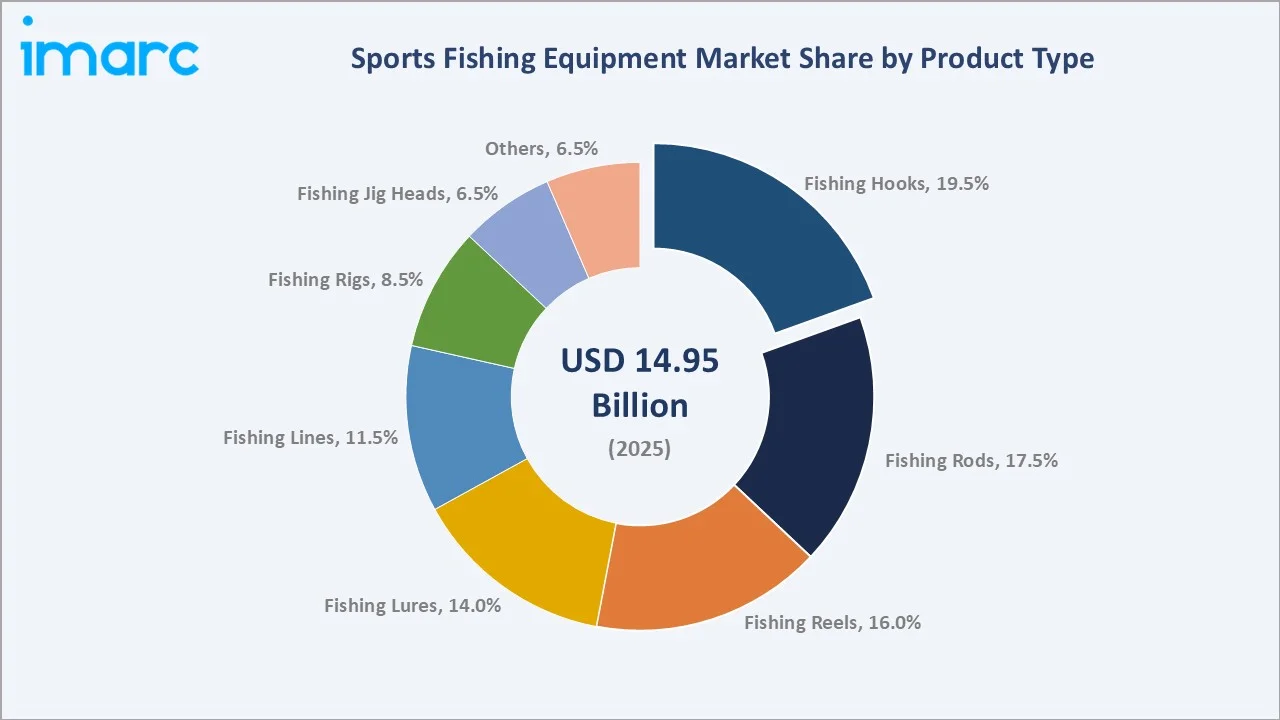

The global sports fishing equipment market reached USD 14.95 Billion in 2025 and is projected to reach USD 21.13 Billion by 2034, growing at a CAGR of 3.72% during 2026-2034. The market is driven by the growing popularity of recreational and competitive fishing activities, supported by rising participation in outdoor leisure pursuits. In 2024, recreational fishing in the U.S. reached a record high, with 57.9 million Americans aged 6 and above participating, representing 19% of the population. This strong participation base is driving demand for sports fishing equipment, as more anglers purchase rods, reels, tackle, lines, lures, and accessories. Fishing hooks lead at 19.5%. Freshwater fishing dominates the application at 57.0%. North America commands 34.0% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.95 Billion |

|

Forecast Market Size (2034) |

USD 21.13 Billion |

|

CAGR (2026-2034) |

3.72% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Fishing Hooks (19.5%, 2025) |

|

Dominant Application |

Freshwater Fishing (57.0%, 2025) |

|

Leading Region |

North America (34.0%, 2025) |

The global sports fishing equipment market expanded from USD 12.46 Billion in 2020 to USD 14.95 Billion in 2025, anchored at USD 17.95 Billion in 2030, and forecast to reach USD 21.13 Billion by 2034. The sports fishing equipment market encompasses all tackle, gear, and accessories used in recreational sport fishing, from terminal tackle (hooks, lures, jigs, rigs) through primary equipment (rods, reels, lines) to specialty items (sonar, GPS, fishing apparel, tackle storage). COVID-19 created a structural shift in the market, the pandemic's lockdown-driven outdoor recreation surge generating new fishing license sales and creating a structurally elevated participation base above the pre-2020 trend that has been sustained through 2025 as post-pandemic consumers retain outdoor recreation habits formed during COVID isolation.

To get more information on this market, Request Sample

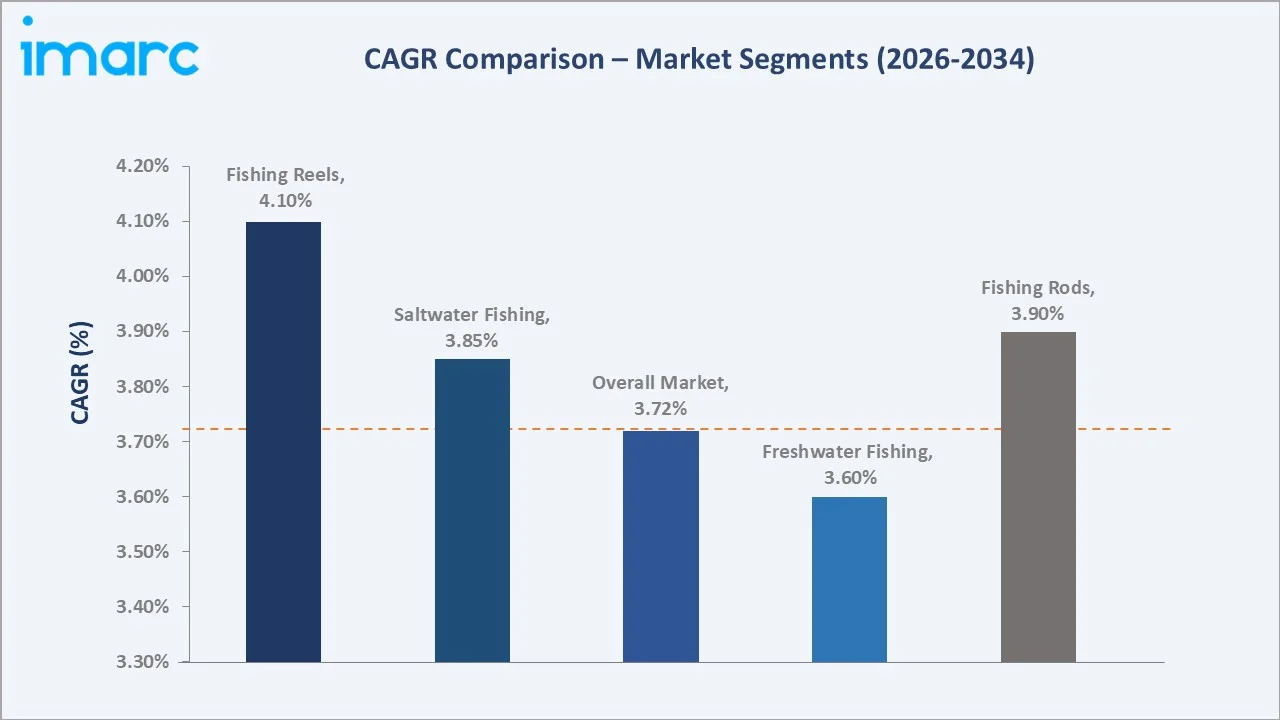

Fishing reels grow fastest at ~4.1% CAGR through premium spinning, baitcasting, and fly reel technology upgrade cycles. Saltwater fishing application grows at ~3.85% CAGR through offshore sportfishing expansion, coastal angling participation growth, and international fishing tourism development.

Executive Summary

The global sports fishing equipment market at USD 14.95 Billion in 2025 represents one of the most commercially resilient recreational equipment categories, a product market whose commercial foundation is the global angling community's estimated recreational fishers creating the most widely participated outdoor sporting activity by participant count above any team or individual competitive sport. Sports fishing equipment's commercial uniqueness is its consumable replacement dynamic, with fishing hooks, lures, lines, and rigs being regularly lost, worn, or retired during fishing activity, creating a recurring consumable revenue stream above the durable equipment (rods, reels) upgrade cycle that sustains market revenue above one-time purchase categories. The market is projected to reach USD 21.13 Billion by 2034.

Fishing hooks at 19.5% lead through consumable volume dynamics. Freshwater fishing at 57.0% leads application through bass, trout, carp, and panfish's global recreational dominance. North America leads regionally at 34.0%.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Fishing Hooks - 19.5% share (2025) |

|

Dominant Application |

Freshwater Fishing - 57.0% market share (2025) |

|

Leading Region |

North America - 34.0% share (2025) |

|

Market Opportunity |

Premium technology fishing gear upgrade cycle; e-commerce D2C fishing brand platforms; freshwater bass tournament gear; saltwater offshore sportfishing expansion; sustainable, eco-friendly fishing gear |

Key Analytical Observations Supporting The Above Data:

- Fishing Hooks at 19.5%: Fishing hooks dominate as they are essential, frequently replaced consumables used across almost all fishing methods. Their wide availability, low cost, and demand across recreational and competitive fishing support steady sales volume.

- Freshwater Fishing at 57.0%: Freshwater fishing dominates due to the wide availability of lakes, rivers, ponds, and reservoirs, making it more accessible and affordable for recreational anglers. Its high participation rate drives steady demand for rods, reels, hooks, lures, lines, and other basic fishing gear.

- North America at 34.0%: North America dominates regionally due to high recreational fishing participation, strong outdoor leisure culture, and widespread access to freshwater and coastal fishing locations. The presence of leading equipment brands and higher consumer spending on premium fishing gear further support regional growth.

Sports Fishing Equipment Market Overview

The global sports fishing equipment market encompasses all tackle, gear, and accessories used in recreational and competitive sport fishing, from the most basic terminal tackle through the most sophisticated electronics. The market's commercial breadth reflects recreational fishing's diversity of disciplines: bass fishing with artificial lures, fly fishing with handcrafted flies, offshore trolling with large game lures, ice fishing with specialty jigging tackle, and carp fishing with specialist bait rigs, creating parallel equipment ecosystems that share technology components but are served by discipline-specific brand communities.

The market ecosystem integrates globally distributed raw material and component supply, brand manufacturing, brand development, multi-channel retail, and the angling community's competitive fishing culture that creates the aspirational brand engagement above purely functional equipment purchase. Macroeconomic factors include rising disposable incomes, growing spending on outdoor recreation and tourism, and increasing participation in leisure fishing activities.

Market Dynamics

To evaluate market opportunities, Request Sample

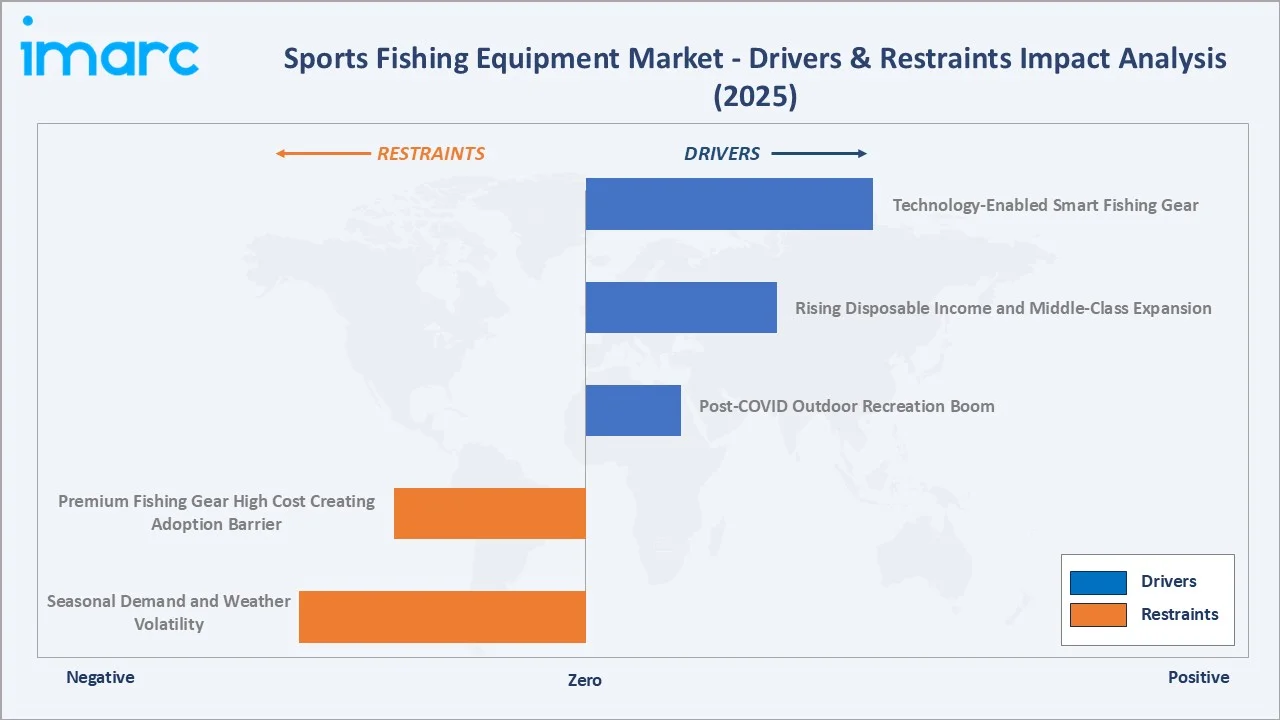

Market Drivers

- Post-COVID Outdoor Recreation Boom: The post-COVID outdoor recreation boom is driving the market as consumers increasingly prefer open-air, low-crowd leisure activities for relaxation and wellness. Fishing gained popularity as a family-friendly and socially distanced activity, boosting demand for rods, reels, hooks, lures, tackle boxes, and apparel. The trend also encouraged new and younger participants to enter the sport. As outdoor hobbies remain popular, repeat purchases and gear upgrades continue to support market growth.

- Rising Disposable Income and Middle-Class Expansion: Rising disposable income and middle-class expansion are increasing consumer spending on leisure and outdoor recreation. As households allocate more budget to hobbies, demand for rods, reels, hooks, lures, tackle boxes, and fishing apparel is rising. In 2025, the global middle class exceeded 4 billion people for the first time, becoming the majority. World Data Lab projects this trend to continue, with nearly 1 billion more people joining the middle class over the next decade, reaching 5.7 billion consumer-class individuals out of a global population of 8.7 billion. Middle-class consumers are also upgrading from basic gear to branded, durable, and technologically advanced equipment. This supports higher sales across both entry-level and premium fishing product categories.

- Technology-Enabled Smart Fishing Gear: Technology-enabled smart fishing gear improves anglers’ accuracy, convenience, and overall fishing experience. Products such as fish finders, GPS-enabled devices, smart rods, bite sensors, and connected reels help users locate fish, monitor activity, and increase catch efficiency. These innovations encourage hobbyists and professional anglers to upgrade from traditional equipment. Growing interest in premium, app-connected, and performance-based gear is further supporting market growth.

Market Restraints

- Seasonal Demand and Weather Volatility: Seasonal demand and weather volatility hamper the market as fishing activity often declines during extreme heat, heavy rainfall, storms, or off-season months. Unpredictable weather can reduce fishing trips, delay tournaments, and lower consumer purchases of rods, reels, hooks, lures, and accessories. This creates uneven sales cycles for manufacturers and retailers. As a result, companies may face inventory buildup, discounted pricing, and fluctuating revenue across seasons.

- Premium Fishing Gear High Cost Creating Adoption Barrier: The high cost of premium fishing gear is limiting adoption among beginners and price-sensitive anglers. Advanced rods, reels, fish finders, smart gear, and branded accessories often require higher upfront spending. This can delay purchases or push consumers toward low-cost alternatives. As a result, premium product penetration remains limited, especially in emerging and budget-conscious markets.

Market Opportunities

- Sustainable and Eco-Friendly Fishing Gear Innovation: Sustainable and eco-friendly fishing gear innovation presents an opportunity as consumers increasingly prefer products with lower environmental impact. Biodegradable fishing lines, lead-free sinkers, recyclable lures, and responsibly sourced materials can attract eco-conscious anglers. Around 550,000 tonnes of fishing gear waste have built up across the European Economic Area, with nearly 12,000 tonnes added each year. To address this issue, the Fishing Without Plastic (PE.S.PLA) project focused on developing biodegradable materials for artisanal fishing gear to reduce ghost gear, microplastic pollution, and overall environmental damage. As sustainability becomes a key buying factor, companies can differentiate themselves and expand premium product offerings.

- Fishing Tourism and Adventure Travel Integration: The integration of fishing tourism and adventure travel increases participation in destination-based fishing experiences. Growing demand for guided fishing trips, sportfishing charters, and outdoor adventure packages encourages anglers to purchase specialized gear and accessories. Popular fishing destinations also drive demand for premium, travel-friendly, and high-performance equipment. As fishing becomes part of broader tourism experiences, equipment sales benefit from both new and experienced participants.

Market Challenges

- Overfishing Concerns and Declining Fish Populations in Specific Water Bodies: Overfishing concerns and declining fish populations in certain lakes, rivers, and coastal waters are reducing fishing opportunities and catch rates. Lower fish availability can discourage recreational anglers from participating as frequently, leading to reduced demand for rods, reels, hooks, lures, and other gear. Governments may also impose stricter fishing quotas, seasonal closures, and conservation measures to protect aquatic ecosystems. These restrictions can limit fishing activity and slow equipment sales growth in affected regions.

- Competition from Alternative Outdoor Recreational Activities: Competition from alternative outdoor recreational activities diverts consumer time and spending toward pursuits such as hiking, camping, cycling, kayaking, and adventure sports. Younger consumers may prefer activities that offer greater social interaction or fitness benefits. This can reduce participation in recreational fishing and limit demand for fishing gear and accessories. As a result, manufacturers and retailers must invest more in marketing, innovation, and engagement initiatives to attract and retain anglers.

Emerging Market Trends

1. Garmin LiveScope and Real-Time Sonar Transforming Bass Fishing Technique

Garmin launched LiveScope XR sonar in July 2022, which provides real-time visuals of fish and underwater structures, offering views around the boat up to 500 feet in freshwater and 350 feet in saltwater. Designed for deeper-water use, the system is well-suited for coastal and open-water fishing applications. This technology is transforming bass fishing techniques by improving casting accuracy, bait presentation, and catch efficiency. As anglers seek more data-driven and performance-oriented fishing experiences, demand for advanced fish finders, sonar systems, and compatible accessories is rising. This trend is also encouraging premium gear upgrades among serious recreational and tournament anglers.

2. Professional Tournament Fishing Creating Aspirational Equipment Specification Cascade

Professional tournament fishing is creating an aspirational equipment trend as recreational anglers closely follow the gear used by top competitors. High-performance rods, reels, lures, electronics, and tackle setups showcased in tournaments influence consumer buying decisions. This creates a specification cascade, where premium features gradually move into mainstream products. As a result, brands benefit from stronger demand for advanced, tournament-grade fishing equipment.

3. Ice Fishing Renaissance Creating North America's Winter Equipment Growth Market

The ice fishing renaissance is emerging, particularly in North America, where winter angling is gaining renewed interest. This is increasing demand for specialized gear such as ice rods, augers, shelters, insulated apparel, sonar devices, and safety accessories. In August 2025, Evolution launched Ice Fishing. Set in an arctic-themed environment, the game refreshes the money wheel format with three bonus rounds, suspenseful play, and multiplier wins of up to 5,000x. The trend extends the fishing season beyond warmer months, helping retailers generate off-season revenue. Rising participation in winter tournaments and social ice fishing events is further supporting equipment upgrades and category expansion.

4. Fly Fishing's Sustainable Outdoor Brand Positioning Creating Premium Consumer Lifestyle Alignment

Fly fishing is emerging due to its strong association with sustainability, conservation, and outdoor wellness. Environmentally conscious consumers increasingly view fly fishing as an eco-friendly recreational activity that aligns with responsible outdoor practices. This positioning is driving demand for high-quality rods, reels, apparel, and accessories made from sustainable materials. As a result, brands are leveraging premium craftsmanship and conservation-focused messaging to attract affluent and lifestyle-oriented anglers.

Industry Value Chain Analysis

The global sports fishing equipment value chain integrates carbon fiber and synthetic material supply, precision mechanical component manufacturing, brand manufacturing, brand development and marketing, and multi-channel retail.

|

Stage |

Key Participants |

|

Raw Material Supply |

Carbon fiber suppliers, fiberglass manufacturers, aluminum producers, plastic resin suppliers, nylon and braided line material providers |

|

Component Manufacturing |

Hook manufacturers, reel component producers, rod blank manufacturers, lure and bait producers, electronics and sonar component suppliers |

|

Branding & Product Development |

Fishing equipment brands, product design teams, R&D centers, technology developers, professional angler consultants |

|

Marketing & Promotion |

Sports fishing associations, tournament organizers, digital marketing agencies, sponsorship partners, social media influencers |

|

Retail & Sales Channels |

Specialty fishing stores, sporting goods retailers, e-commerce platforms, outdoor recreation chains, and direct-to-consumer channels |

|

End Users & After-Sales Services |

Recreational anglers, professional fishermen, fishing tourism operators, repair and maintenance service providers, and warranty support centers |

The branding & product development stage is the value chain's most commercially intensive competitive investment point. The angler experience and community stage create the value chain's most commercially durable competitive advantage.

Technology Landscape in the Sports Fishing Equipment Industry

Carbon Fiber Rod Blank Technology

Carbon fiber rod blank technology enables the production of lighter, stronger, and more sensitive fishing rods. Advanced carbon fiber materials improve casting distance, accuracy, and fish detection while reducing angler fatigue during extended use. Manufacturers are also developing high-modulus carbon blanks that offer superior strength-to-weight ratios and durability. This innovation is driving premium product demand and encouraging anglers to upgrade to high-performance fishing gear.

Precision Reel Bearing and Gear Technology

Precision reel bearing and gear technology enhances reel smoothness, durability, and retrieval efficiency. Advanced ball bearings and precision-engineered gear systems reduce friction, improve casting performance, and provide greater control during fish fights. Manufacturers are increasingly using corrosion-resistant materials and tighter gear tolerances to improve reliability in both freshwater and saltwater environments. These innovations are driving demand for high-performance reels among recreational and professional anglers.

App-Connected Fishing Devices

App-connected fishing devices link gear such as fish finders, smart rods, bite alarms, and GPS tools with mobile applications. These devices help anglers track fish activity, water depth, weather conditions, location data, and catch records in real time. In June 2025, onWater Fish, a leading app for anglers and water-based exploration, launched its Summer 2025 update with advanced tools to help users analyze fishing patterns, make smarter on-water decisions, and support conservation. The update includes a smart Journal, an AI-powered Trout Measuring Tool, and MyWaters, which offers personalized insights and alerts when conditions match previous fishing success. The technology improves convenience, decision-making, and overall fishing performance. As anglers seek data-driven experiences, demand for connected and smart fishing equipment is increasing.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Fishing Hooks |

19.5% |

2025 |

|

Application |

Freshwater Fishing |

57.0% |

2025 |

|

End User |

Individual Consumer |

🔒 |

2025 |

|

Distribution Channel |

Specialty and Sports Stores |

🔒 |

2025 |

|

Region |

North America |

34.0% |

2025 |

By Product Type

Fishing hooks lead at 19.5% (2025). The fishing hook segment encompasses J-hooks, circle hooks, offset worm hooks, treble hooks, and specialty hooks across various size ranges, creating the most commercially diverse product sub-category in sports fishing equipment above more narrowly specified rod and reel categories.

To access detailed market analysis, Request Sample

Fishing rods at 17.5% represent the most aspirational upgrade category. Fishing reels at 16.0% grow fastest at ~4.1% CAGR. Fishing lures at 14.0% represent the most creatively diverse category. Fishing lines at 11.5% include monofilament, braided, and fluorocarbon. Fishing rigs at 8.5%, fishing jig heads at 6.5%, and others at 6.5% of market value.

By Application

Freshwater fishing leads at 57.0% (2025). The freshwater segment encompasses bass fishing, carp fishing, trout and salmon fishing, and panfish and walleye fishing, creating the most commercially diverse freshwater equipment demand across multiple species and technique categories.

Saltwater fishing at 43.0% grows at ~3.85% CAGR through offshore sportfishing expansion and coastal inshore angling participation growth. Saltwater fishing encompasses inshore coastal, nearshore reef and wreck, offshore pelagic, and big game, creating saltwater's most commercially premium per-session tackle investment above freshwater recreational fishing across all geographic markets.

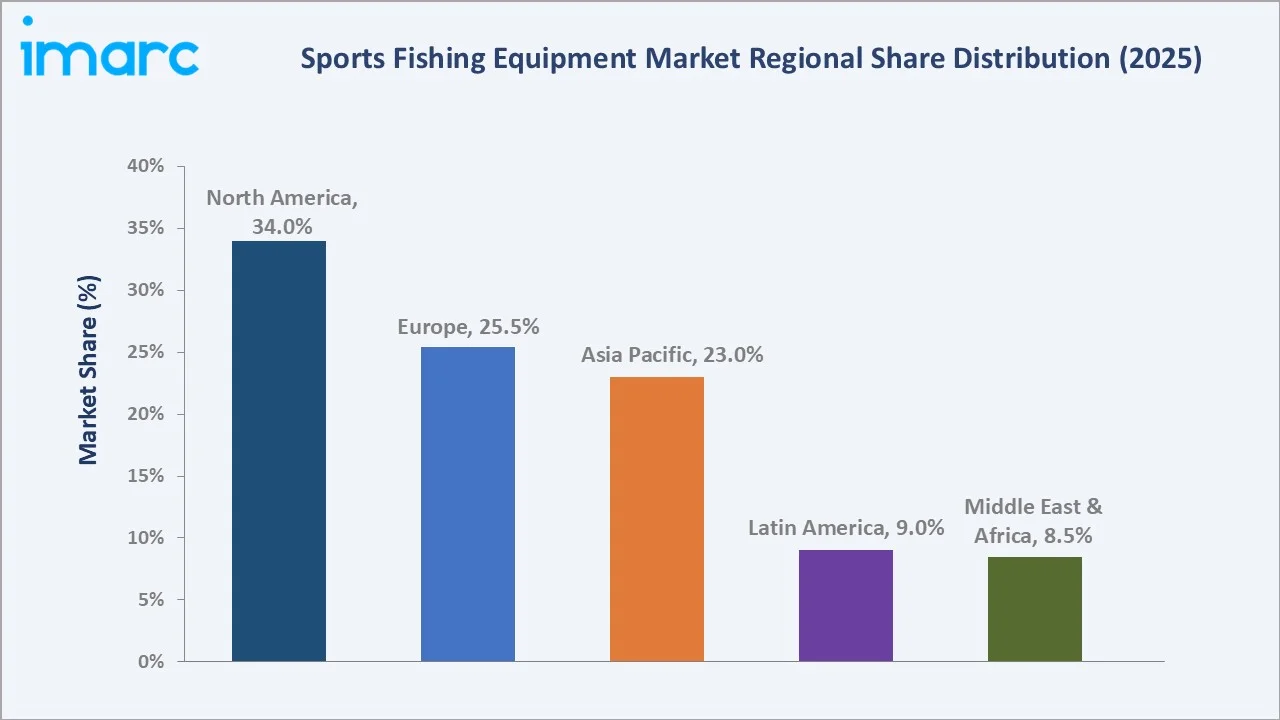

Regional Market Insights

|

Region |

Share (2025) |

Key Sports Fishing Equipment Market Drivers & Characteristics |

|

North America |

34.0% |

Supported by high participation in recreational fishing, strong outdoor recreation spending, and widespread access to freshwater and coastal fishing locations. |

|

Europe |

25.5% |

Driven by a well-established angling culture, a growing focus on sustainable fishing practices, and increasing demand for specialized fishing equipment. |

|

Asia Pacific |

23.0% |

Driven by rising disposable incomes, expanding middle-class populations, and increasing interest in recreational outdoor activities. |

|

Latin America |

9.0% |

Supported by abundant freshwater and coastal fishing resources, increasing recreational fishing participation, and growing tourism-related fishing activities. |

|

Middle East & Africa |

8.5% |

Emerging due to growing interest in sportfishing, expanding coastal tourism, and increasing investment in outdoor recreational activities. |

North America's 34.0% market leadership reflects the USA's licensed anglers creating the most commercially active single-nation fishing equipment retail market, anchored by superstores. Europe's 25.5% reflects the continent's diverse fishing cultures. Asia Pacific's 23.0% reflects Japan's premium reel technology manufacturing and domestic market, alongside China's rapidly growing recreational fishing participation.

Latin America's 9.0% is growing through Brazil's fishing tourism and freshwater biodiversity, creating an above-standard destination fishing attraction for international premium tackle investment. The Middle East and Africa's 8.5% are growing through South Africa's established freshwater and saltwater fishing culture.

Competitive Landscape

The global sports fishing equipment competitive landscape is commercially stratified across three dimensions: Japanese precision reel technology leaders, USA multi-brand portfolio holders, and specialty brand leaders.

|

Company |

Key Products |

Market Position |

Core Strength |

|

|

STELLA SW D, STELLA SW C, STELLA FK, TWINPOWER SW C, EXSENCE B, CALCUTTA CONQUEST MD, ANTARES B |

Market Leader |

Shimano Inc. is recognized for developing high-performance reels, rods, and accessories through advanced engineering. |

|

|

CountDown Elite, Soft Peto Prerigged, X-Rap Saltwater, X-Rap Magnum, Tungsten Mustach Jig, Wax Tail Jig, Tungsten Fly Jig |

Market Leader |

Rapala VMC Corporation is a manufacturer and distributor of a comprehensive range of sports fishing equipment. The company is widely recognized for its high-quality lures, fishing hooks, and accessories. |

|

|

Emeraldas Amorous Joint, Emeraldas Dirt LC, Emeraldas Dirt LC Negard, Emeraldas Boat CTR, LeoBlitz S300J, Emeraldas MX |

Market Leader |

Globeride, Inc. is a leading manufacturer of high-end fishing tackle, primarily known for its globally recognized Daiwa brand. |

|

|

Legend X2, Legend Xtreme, Legend Elite, Legend Elite Panfish, Legend Elite Musky, Rogue V Boat, Rogue V Slow Pitch, Rogue V Jig |

Established Player |

St. Croix Rods plays a premier role in sports fishing by manufacturing high-performance, durable, and technologically advanced rods designed to give anglers a competitive edge. |

|

|

Helios D Fly Rod, Recon Freshwater Fly Rod, Hydros Reel, Ratio Reel, Clearwater Reel |

Niche Player |

The Orvis Company, Inc. is widely recognized as a leader in the fly-fishing industry and the oldest continuously operating fly-fishing tackle manufacturer in the world. |

The competitive landscape's most commercially consequential dynamic is the D2C disruption. Small batch premium lure brands are capturing premium angler spending above the established brand distributors' traditional channel control.

Key Company Profiles

SHIMANO INC.

SHIMANO INC. is one of the leading manufacturers of fishing tackle, cycling components, and rowing equipment. In the sports fishing equipment market, the company is renowned for its premium fishing reels, rods, lures, lines, and fishing accessories.

- Key Products: STELLA SW D, STELLA SW C, STELLA FK, TWINPOWER SW C, EXSENCE B, CALCUTTA CONQUEST MD, ANTARES B.

- Recent Developments: In January 2026, Shimano North America Fishing expanded its Compre rod lineup with three key additions: the redesigned Compre Muskie, redesigned Compre Walleye, and the new Compre Lite series. These rods feature premium components, updated styling, and Shimano’s DIAFLASH technology to improve performance across various freshwater fishing applications.

- Strategic Focus: Focuses on continuous product innovation, emphasizing advanced reel technologies, lightweight rod materials, and precision-engineered components to enhance angling performance.

Rapala VMC Corporation

Rapala VMC Corporation is a leading manufacturer and marketer of fishing tackle and sports fishing equipment. The company offers a broad portfolio that includes fishing lures, hooks, lines, rods, reels, terminal tackle, tools, accessories, and outdoor products.

- Key Products: CountDown Elite, Soft Peto Prerigged, X-Rap Saltwater, X-Rap Magnum, Tungsten Mustach Jig, Wax Tail Jig, Tungsten Fly Jig.

- Strategic Focus: Strengthening its position through continuous innovation in fishing lures, hooks, terminal tackle, and other performance-driven fishing products.

Market Concentration Analysis

The global sports fishing equipment market is moderately concentrated at the premium tier. The USA market's unique feature is retail concentration, a single retail parent operating a high number of stores, estimated to represent 15-25% of USA fishing tackle retail sales, creating the most commercially concentrated single-chain fishing tackle retail relationship that gives significant vendor negotiation leverage above independent tackle dealers.

Market concentration is evolving through e-commerce's D2C channel disruption, with small premium brands capturing premium angler spending above traditional distributor control, Amazon marketplace creating price transparency that compresses traditional retail margin, and brand DTC websites creating direct consumer relationships that undercut traditional distributor relationships.

Investment & Growth Opportunities

Highest Growth Segments

Fishing reels (~4.1% CAGR through premium technology upgrade), saltwater fishing application (~3.85% CAGR through offshore sportfishing expansion), fishing electronics and sonar (~15-20% CAGR from small base), sustainable fishing gear (~8-10% CAGR), ice fishing equipment (~6-8% CAGR), and Asia Pacific premium tackle adoption (~5-7% CAGR) represent the highest-growth fishing equipment investment vectors through 2034.

Emerging Investment Opportunities

The fishing electronics and technology integration market represents the most commercially dynamic adjacent market to traditional fishing tackle, creating cross-selling and technology ecosystem opportunities for fishing equipment brands and retailers above traditional tackle-only product category boundaries.

Investment Themes

- Premium carbon fiber fishing rod manufacturing investment: The USA professional bass fishing tournament circuit's annual tackle upgrade cycle creates the most commercially reliable annual revenue driver for premium fishing rod brands. Investment in high-modulus carbon fiber rod blank manufacturing technology and tournament angler endorsement program creates the most commercially structured premium fishing rod market entry above general market brand competition without tournament specification differentiation.

- Sustainable and eco-friendly fishing gear product development, creating regulatory compliance and conservation-aligned premium market: Lead weight replacement, biodegradable soft plastic lures, and fluorocarbon-free fishing line collectively create the most commercially aligned sustainable outdoor recreation product investment above industries without fishing's strong conservation culture creating above-standard consumer sustainability premium acceptance from anglers who identify as environmental stewards above average consumer sustainability motivation.

Future Market Outlook (2026-2034)

The global sports fishing equipment market is projected to grow from USD 14.95 Billion in 2025 to USD 21.13 Billion by 2034, delivering a 3.72% CAGR over the forecast period. The market's anchor value of USD 17.95 Billion in 2030 represents sports fishing equipment at its most commercially mature structural phase. The post-COVID participation surge's upgrade cycle is reaching completion as new anglers have progressed through first gear, second gear, and established angler equipment tiers, with market growth increasingly driven by Asia Pacific's emerging premium market, saltwater fishing's above-freshwater-CAGR growth, and technology integration, creating above-standard equipment investment per angler above purely tackle spending.

Three structural forces define the growth of the sports fishing equipment market through 2034: global fishing participation's demographic transition, technology integration creating above-equipment-only market expansion, and sustainability regulation and environmental fishing community alignment creating premium eco-friendly tackle adoption.

Research Methodology

Primary Research

Primary research comprised structured interviews with global sports fishing equipment industry stakeholders, including product development directors, brand managers, tournament directors, retail buyers, and angler survey data from recreational and competitive anglers across North America, Europe, and the Asia Pacific.

Secondary Research

Secondary research encompassed company annual reports, the world records database for fish, and competitive tournament statistics. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using the angler participation model: global licensed and registered recreational angler population by region multiplied by average annual fishing equipment spending per angler by region, creating base market revenue. Premium upgrade cycle multiplier applied to base model. Regional growth rate calibrated against fishing license data trend and retail sales data.

Sports Fishing Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Fishing Rods, Fishing Reels, Fishing Hooks, Fishing Lures, Fishing Lines, Fishing Rigs, Fishing Jig Heads, Others |

| Applications Covered | Freshwater Fishing, Saltwater Fishing |

| End Users Covered | Individual Consumer, Clubs, Sports Organizers |

| Distribution Channels Covered | Specialty and Sports Stores, Departmental and Discount Stores, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | SHIMANO INC., Rapala VMC Corporation, GLOBERIDE Inc., St. Croix Rods, The Orvis Company Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the sports fishing equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global sports fishing equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the sports fishing equipment industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Sports Fishing Equipment Market Report

The global sports fishing equipment market reached USD 14.95 Billion in 2025, driven by rising participation in recreational fishing, growing outdoor leisure spending, and increasing demand for advanced rods, reels, hooks, lures, and accessories. Product innovation, fishing tourism, and the popularity of competitive angling are further supporting market growth.

The global sports fishing equipment market grows at 3.72% CAGR during 2026-2034, reaching USD 21.13 Billion by 2034. The overall growth is sustained by post-COVID elevated fishing participation retention, Asia Pacific premium market emergence, technology integration creating above-tackle equipment spending, and sustainable fishing gear premiumization through eco-friendly product adoption.

Fishing hooks lead at 19.5% through the most commercially volume-intensive consumable dynamic in fishing tackle, the world's recreational fishing community consuming a high number of hooks through regular loss, damage, and replacement, creating recurring purchase demand independent of equipment upgrade motivation.

Freshwater fishing leads at 57.0% through the global accessibility advantage of freshwater fisheries above coastal saltwater access limitation, bass fishing's dominant freshwater tackle economy, and trout and salmon fly fishing's specialist premium gear specification.

North America leads at 34.0% through the USA's leading licensed angler base, creating the most commercially dominant fishing tackle retail format, and USA bass fishing tournament culture, creating an annual premium equipment specification cascade from professional tournament anglers to USA bass anglers.

Leading companies include SHIMANO INC., Rapala VMC Corporation, GLOBERIDE, Inc., St. Croix Rods, and The Orvis Company, Inc., among others.

The global sports fishing equipment market is projected to reach approximately USD 17.95 Billion by 2030, with China's premium fishing tackle adoption as middle-class anglers upgrade from domestic brands to imported premium specifications, USA bass fishing sonar and electronics becoming mainstream recreational, and eco-friendly fishing gear growth.

Three priority investment opportunities: premium carbon fiber fishing rod manufacturing for USA tournament bass fishing specification, Asia Pacific premium fishing reel market development targeting China and Australia middle class angler upgrade, and sustainable eco-friendly fishing gear premium product launch targeting North American and European conservation-motivated angler demographic.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)