Stylus Pen Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, Application, End-User, and Region, 2026-2034

Global Stylus Pen Market Size, Share, Trends & Forecast 2026-2034

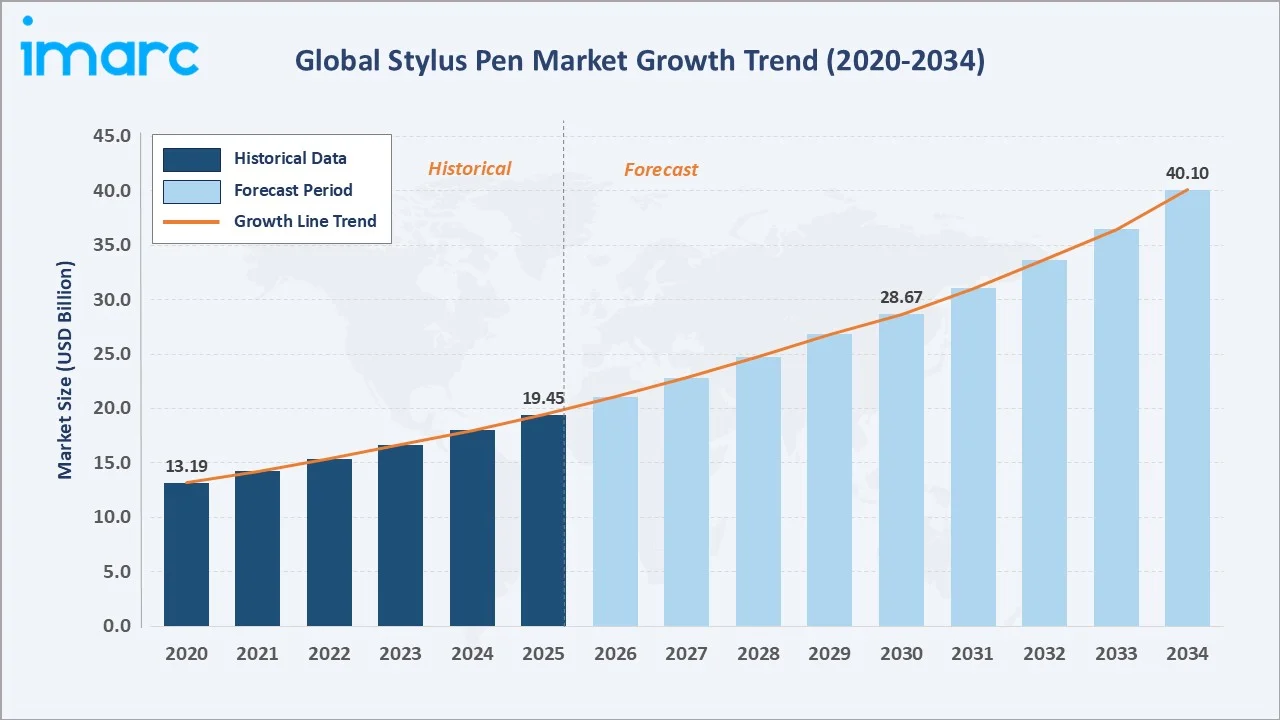

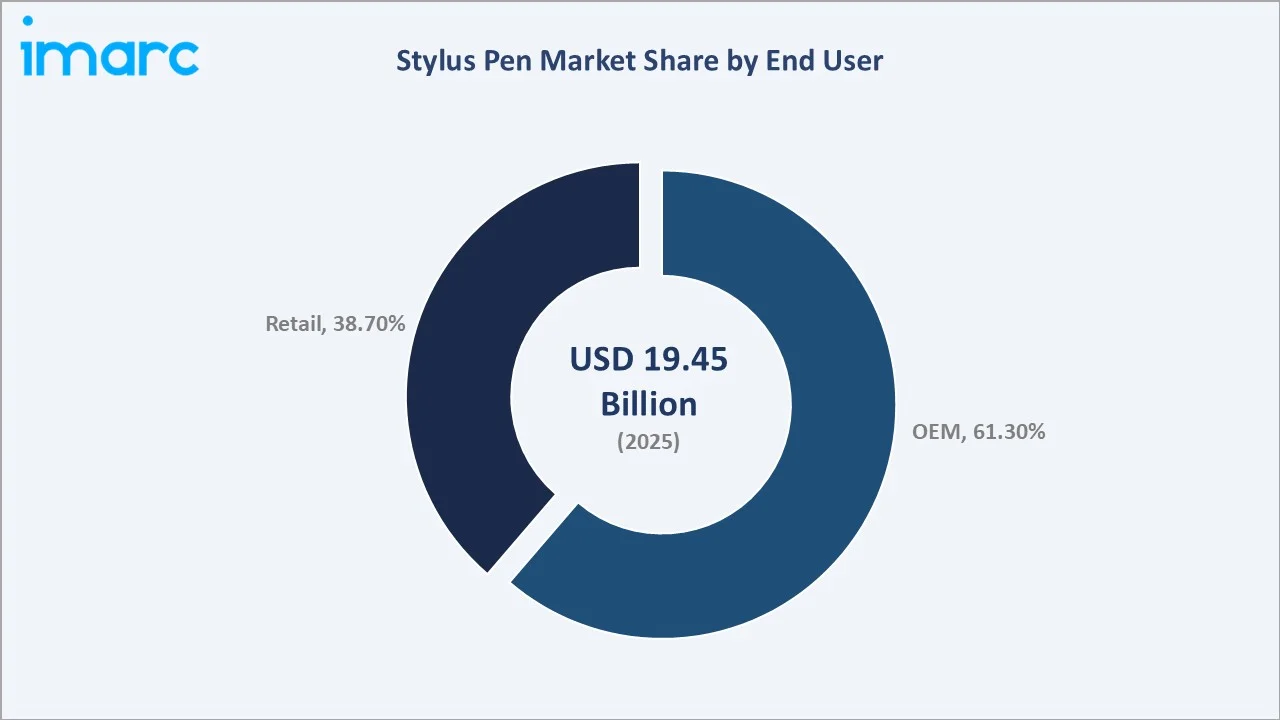

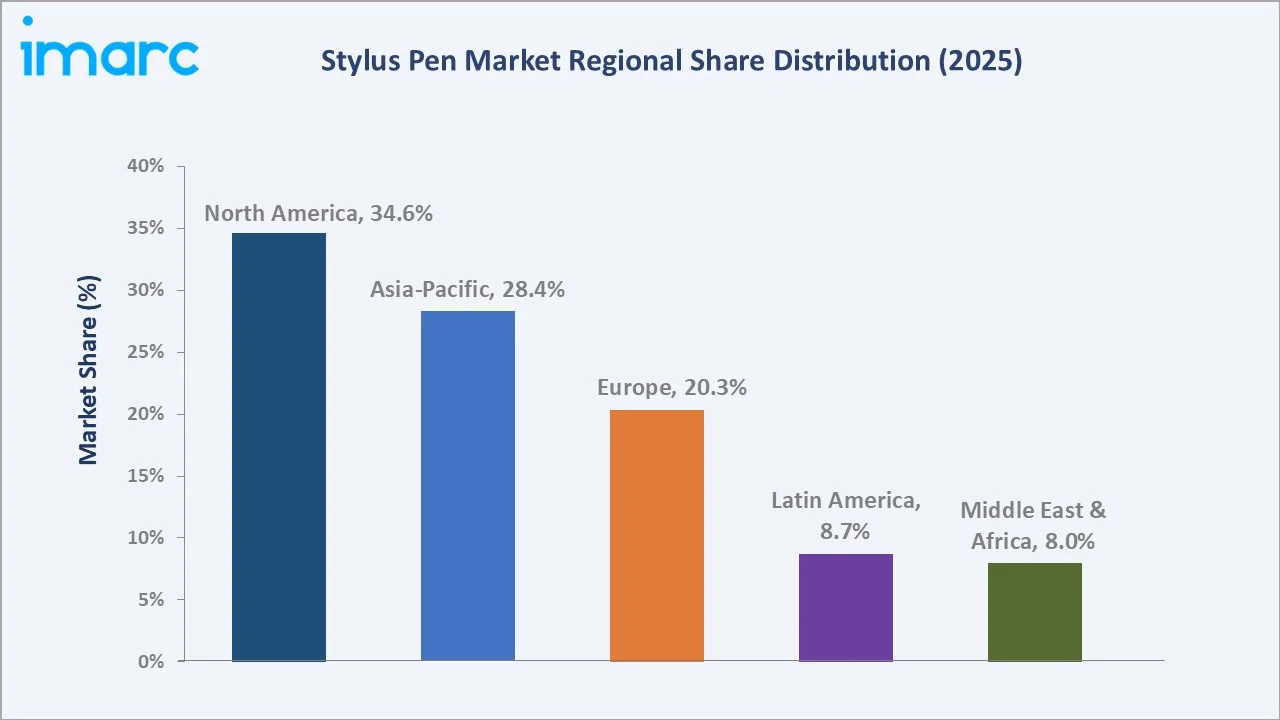

The global stylus pen market size reached USD 19.45 Billion in 2025 and is projected to reach USD 40.10 Billion by 2034, at a CAGR of 8.07% during 2026-2034. Proliferating touchscreen device adoption with global connected devices reached around 55.7 billion, according to the International Data Corporation (IDC), rising digital art and education sector demand, and active stylus technology innovation are the primary growth catalysts. Online channels lead distribution at 58.4%, while OEM dominates end-use at 61.3%. North America holds the largest regional share at 34.6% in 2025, anchored by Apple, Microsoft, and Wacom’s technology ecosystems.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 19.45 Billion |

|

Forecast Market Size (2034) |

USD 40.10 Billion |

|

CAGR (2026-2034) |

8.07% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.6%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~9.8% CAGR,2026-2034) |

|

Leading Distribution Channel |

Online (58.4%, 2025) |

|

Leading End-User |

OEM (61.3%, 2025) |

The stylus pen market growth from 2020 through 2034, the market expanded from USD 13.19 Billion in 2020 to USD 19.45 Billion in 2025. Anchored at USD 28.67 Billion in 2030, the forecast to USD 40.10 Billion, fueled by active stylus technology adoption and the surge in digital education platforms.

To get more information on this market, Request Sample

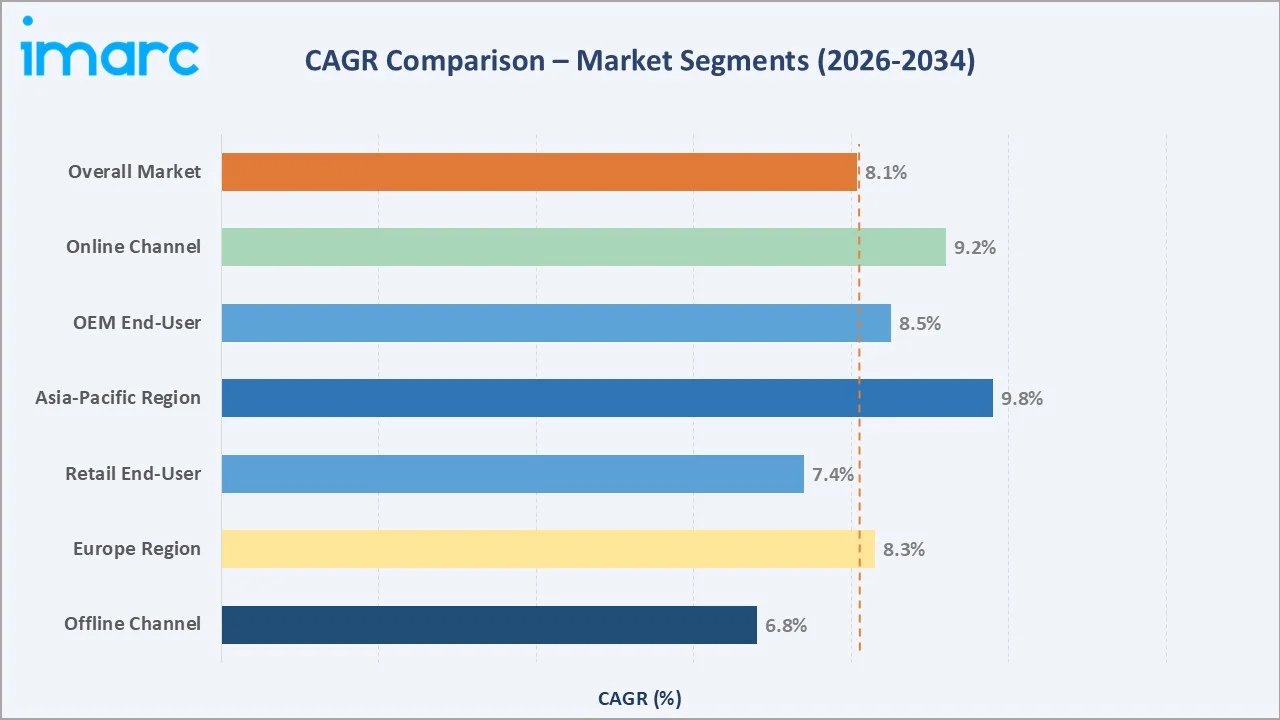

The CAGR across key segments, Asia-Pacific leads at ~9.8% CAGR, reflecting rapid touchscreen device adoption in China, India, and Southeast Asia. The online channel at ~9.2% outpaces the overall market rate of 8.07%, driven by DTC brand expansion and e-commerce platform penetration through 2034.

Executive Summary

The global stylus pen market is expanding at a robust 8.07% CAGR from USD 19.45 Billion in 2025 to USD 40.10 Billion by 2034. A stylus pen is a precision input device, available in resistive, capacitive, and active technology variants, used to interact with touchscreen devices, including tablets, smartphones, interactive whiteboards, and pen-display monitors. Active styluses, which embed electronic components enabling pressure sensitivit, tilt recognition, and palm rejection, command the largest and fastest-growing product segment due to their superior performance in professional art, design, and enterprise note-taking workflows.

Online channels command 58.4% of distribution in 2025, reflecting the e-commerce-first purchasing behavior of both individual consumers and small business buyers, alongside the direct-to-consumer strategies of brands. OEM end-use at 61.3% captures device-bundled stylus procurement where technology OEMs integrate styluses as standard accessories, creating captive demand pipelines that grow in proportion to tablet and convertible laptop shipments.

North America leads regionally at 34.6%, anchored by strong enterprise digital transformation spending and a mature creative professional community. Asia-Pacific at 28.4% is the fastest-growing region, driven by China’s 1.1 billion smartphone users and India’s rapidly expanding education technology market.

Key Market Insights

|

Insight |

Data / Finding |

|

Leading Distribution |

Online – 58.4% (2025); DTC + e-commerce channel dominance |

|

Leading End-User |

OEM – 61.3% (2025); device-bundled stylus with iPad, S Pen, Surface Pen |

|

Leading Region |

North America – 34.6% (2025); Apple, Microsoft, Wacom HQ advantage |

|

Fastest Region |

Asia-Pacific – ~9.8% CAGR; China + India digital adoption surge |

Key Analytical Observations Supporting the Above Data:

- Online channels at 58.4% in 2025, reflect the structural shift in consumer electronics purchasing. Apple’s direct online store, Wacom’s DTC web platform, and XPPen’s Amazon-first strategy collectively demonstrate that premium and mid-range stylus brands.

- OEM end-use at 61.3% in 2025 is structurally driven by device bundling economics. The OEM-captive procurement relationships create a growth pipeline that directly mirrors global tablet shipment growth.

- North America’s 34.6% share (2025) is built on both consumer and enterprise adoption strength. Enterprise digital transformation spending, with Microsoft Surface deployments across Fortune 500 companies, creates structural B2B stylus demand independent of consumer market cycles.

- Asia-Pacific’s 28.4% share benefits from multiple concurrent drivers. China’s tablet computer shipments rose 13.1% from the previous year to 33.8 million units in 2025, India’s EdTech market growth, and South Korea’s Samsung S Pen ecosystem all contribute structural Asia-Pacific growth above the global market average.

Global Stylus Pen Market Overview

A stylus pen is a precision input device designed for use with capacitive, resistive, or active-digitizer touchscreen surfaces across tablets, smartphones, interactive whiteboards, pen displays, and convertible laptops. Three primary technology types define the market: resistive styluses (simple passive tips, no battery required), capacitive styluses (conductive tips compatible with capacitive screens), and active styluses (electronically powered, pressure-sensitive, with palm rejection and tilt detection).

The ecosystem spans raw material suppliers, component manufacturers, OEM assembly facilities, quality and certification testing, distribution networks, and end-use markets across education, professional design, enterprise, gaming, and healthcare. Global tablet shipments increased 5% year over year to 151.9 million units (IDC), and the rising US education technology market collectively forms the macroeconomic demand backdrop driving structural stylus pen market growth.

Market Dynamics

To evaluate market opportunities, Request Sample

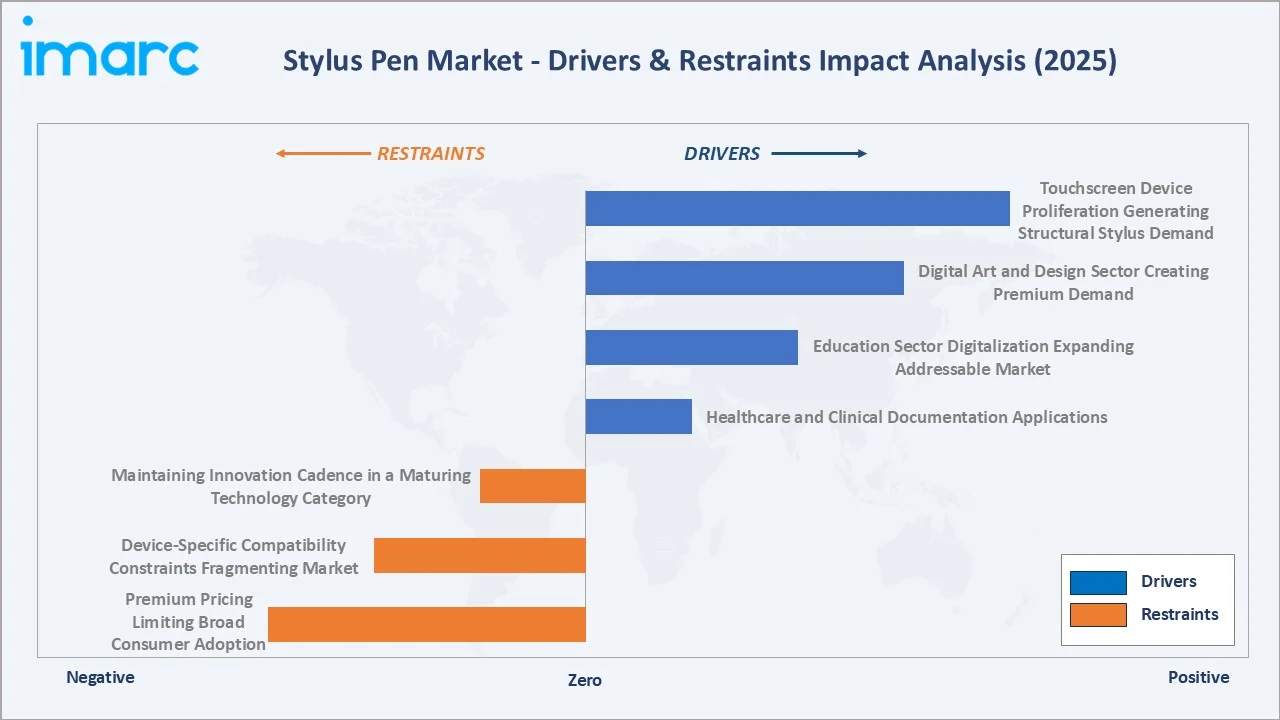

Market Drivers

- Touchscreen Device Proliferation Generating Structural Stylus Demand: The global connected devices reached around 55.7 billion, according to the International Data Corporation (IDC), with touchscreen-capable tablets and smartphones representing the primary stylus-compatible device category.

- Digital Art and Design Sector Creating Premium Demand: The global digital art market, with an estimated 12 million professional digital artists globally, represent the core premium stylus demand pool.

- Education Sector Digitalization Expanding Addressable Market: Digital Stationary Consortium’s 2023 survey found that 38% of digital pen users use their device daily for note-taking, list-making, and editing, creating significant stylus demand from a market largely untapped at premium price points.

Market Restraints

- Premium Pricing Limiting Broad Consumer Adoption: The price points restrict premium active stylus adoption to approximately 18–22% of iPad users and 12–15% of Surface device users, leaving 78–82% of device owners without stylus accessories.

- Device-Specific Compatibility Constraints Fragmenting Market: Apple Pencil is exclusively compatible with Apple iPads; Samsung S Pen works exclusively with Samsung Galaxy devices. This device lock-in strategy, while commercially rational for OEMs, creates consumer confusion and limits the aftermarket stylus market size.

Market Opportunities

- Healthcare and Clinical Documentation Applications: Digital stylus-based clinical note-taking is growing as an alternative to keyboard-based electronic health records (EHR) entry.

- Emerging Market Education Demand in Asia-Pacific and Latin America: India’s EdTech sector growth, Brazil’s 40 million students in 175,000 primary and secondary schools, and Indonesia’s annual education technology spending collectively represent early-stage markets where mid-range stylus pen adoption is expected to rise.

Market Challenges

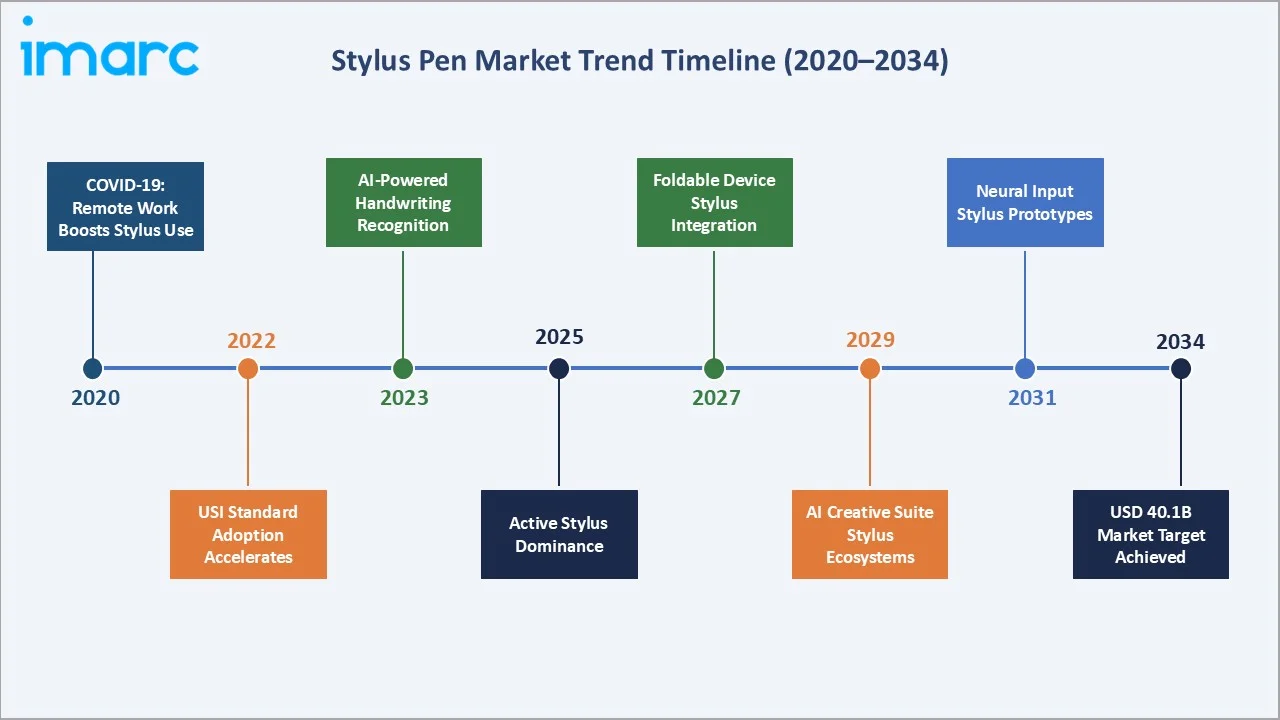

- Universal Stylus Initiative (USI) Standardization Adoption Rate: USI 2.0 promises cross-device stylus compatibility across manufacturers, but adoption requires OEM hardware investment that creates inertia against standardization.

- Maintaining Innovation Cadence in a Maturing Technology Category: Pressure sensitivity has reached 8,192 levels, tilt recognition is standard in premium devices, and palm rejection has been largely solved through hardware and software algorithms.

Emerging Market Trends

1. Active Stylus Technology Becoming the Market Standard

Active styluses, powered by battery or USB charging and embedding electronic pressure and tilt sensors, now represent the fastest-growing segment as price parity with premium passive styluses narrows.

2. AI-Powered Handwriting Recognition Elevating Stylus Utility

Artificial intelligence-powered handwriting-to-text conversion, integrated into Apple Notes (iOS 17+), Samsung Notes, and Microsoft OneNote, is dramatically expanding the productive use case for stylus pens beyond art and design into mainstream note-taking and text input workflows.

3. Foldable and Flexible Device Integration Creating New Stylus Segments

Samsung launched the fifth generation of Galaxy foldables: Galaxy Z Flip5 and Galaxy Z Fold5 in July 2023, and the emerging category of foldable tablets and rollable displays is creating new form factor-specific stylus requirements.

4. Sustainable Design and Circular Economy Initiatives

Environmental sustainability is emerging as a purchase decision factor in both consumer and enterprise stylus procurement. These sustainability initiatives are increasingly required in public sector and education procurement specifications across EU member states, where the Ecodesign for Sustainable Products Regulation (ESPR) will apply to electronic accessories from 2027.

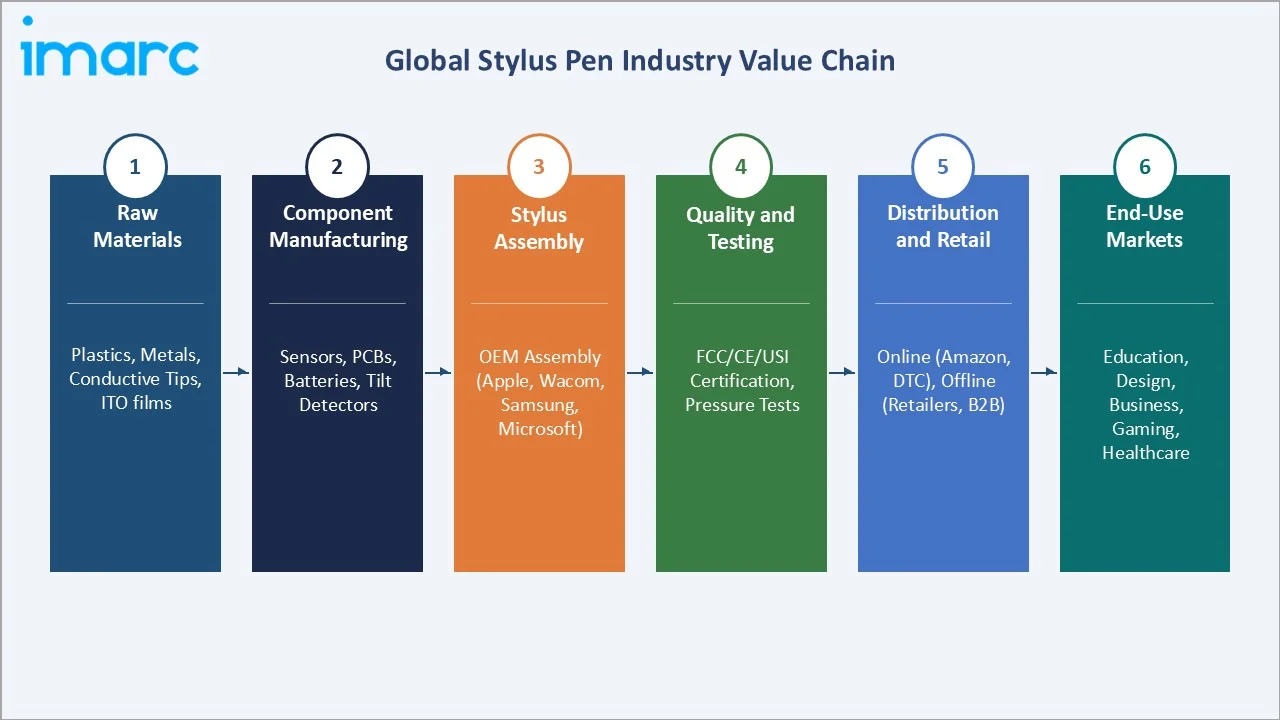

Industry Value Chain Analysis

The stylus pen value chain captures greatest value at the OEM assembly and branded product stages, where Apple, Wacom, and Samsung command gross margins of 40–60% on premium active stylus products versus 10–15% at the component supplier stage.

|

Stage |

Key Players & Examples |

|

Raw Materials |

Conductive plastics, ITO touch films, metals (stainless steel housing), lithium cells |

|

Component Manufacturing |

MEMS pressure sensors, Wacom EMR sensors, Bluetooth SoCs, nibs and tips |

|

Stylus Assembly |

Apple Inc. (Pencil series), Wacom Co. Ltd., Samsung (S Pen), Microsoft (Surface Pen), Logitech (Crayon) |

|

Quality & Certification |

FCC Part 15 (US), CE Marking (EU), RoHS Directive compliance, USI 2.0 certification, Bluetooth SIG qualification, Apple MFi certification |

|

Distribution |

Online: Amazon, Apple Store, Samsung.com, Wacom eStore; Offline: Best Buy, Staples, Micro Center, art supply stores; B2B: CDW, Insight, SHI International |

|

End-Use Markets |

Education, Professional Design, Enterprise, Retail Consumer, Gaming |

Apple’s vertical integration, designing the Apple Pencil’s electromagnetic sensor array in-house and manufacturing via Foxconn-managed supply chains in China, enables gross margins on Apple Pencil, versus Wacom’s more commoditized supply chain margins on comparable premium active stylus products. This margin differential reflects the value of ecosystem lock-in that Apple achieves through iPad-exclusive compatibility.

Technology Landscape in the Stylus Pen Industry

Active Stylus and Electromagnetic Resonance (EMR) Technology

Electromagnetic resonance (EMR) technology, pioneered by Wacom and widely licensed, enables passive stylus operation through electromagnetic field interaction with the digitizer layer embedded beneath the display.

Bluetooth and Wireless Connectivity Integration

Bluetooth Low Energy (BLE) connectivity, now standard in premium active styluses, enables features including wireless button shortcut programming, battery status indication, Find My device integration (Apple Pencil), and over-the-air firmware updates. These wireless capabilities are generating 12–18% ASP premiums over non-Bluetooth active styluses.

Universal Stylus Initiative (USI) Standardization

USI 2.0 (Universal Stylus Initiative) defines an open standard enabling active stylus interoperability across participating manufacturers’ touchscreen devices. Penoval USI2.0 Stylus is rechargeable and offers 4,096 levels of pressure sensitivity. This standardization wave represents the most significant structural shift in stylus market dynamics since the introduction of active technology.

AI-Powered Input and Handwriting Recognition

On-device machine learning for handwriting recognition converts stylus handwriting to digital text in real time with 95–98% accuracy across major languages. These AI capabilities transform the stylus from a creative tool into a universal text input device, expanding the addressable user base.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Active Stylus |

🔒 |

2025 |

|

Distribution Channel |

Online |

58.4% |

2025 |

|

Application |

Tablets |

🔒 |

2025 |

|

End-User |

OEM |

61.3% |

2025 |

|

Region |

North America |

34.6% |

2025 |

By Distribution Channel

Online channels command 58.4% of stylus pen distribution in 2025, reflecting both DTC brand strategy and e-commerce marketplace dominance in consumer electronics. The online channel’s 9.2% projected CAGR through 2034 outpaces offline at ~6.8%, driven by expanding e-commerce penetration in Asia-Pacific markets and DTC brands building direct customer relationships that generate higher lifetime value.

To access detailed market analysis, Request Sample

Offline channels at 41.6% in 2025 serve enterprise B2B procurement, retail impulse purchase, and in-store demonstration channels, critical for premium stylus conversion. Best Buy’s dedicated Apple, Samsung, and Microsoft accessories sections drive high-ASP stylus sales through physical demonstration of pressure sensitivity and tip precision that online channels cannot replicate.

By End-User

OEM end-use at 61.3% in 2025 captures the device-bundled stylus procurement channel, where technology manufacturers integrate styluses as standard or optional accessories. Global tablet shipments growing at 5% year over year (IDC) directly translate to OEM stylus procurement growth.

Retail end-use at 38.7% in 2025, encompasses aftermarket compatible stylus purchases and standalone premium art stylus sales. The global digital art and creative tools market growth directly supports retail stylus demand from professional and semi-professional creators. Education procurement, where schools purchase compatible styluses for existing device fleets rather than new bundled devices, represents the fastest-growing retail channel growth in North America and Western Europe, driven by USI-compatible stylus purchasing for Chromebook education fleets.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Data |

|

North America |

34.6% |

US K-12 EdTech; Apple Pencil + Surface Pen ecosystem; Enterprise digital transformation; student 1:1 device programs |

|

Asia-Pacific |

28.4% |

China’s high tablet/large-screen users; India EdTech growth; Japan manga/digital art culture |

|

Europe |

20.3% |

EU ESPR sustainability mandates; Germany/France/UK creative sectors; EASA digital documentation; Right to Repair regulation driving durability |

|

Latin America |

8.7% |

Brazil student addressable market; Mexico enterprise digitalization; EdTech investment growth; XPPen + Huion affordable stylus demand |

|

Middle East & Africa |

8.0% |

Saudi Vision 2030 education digitalization; UAE enterprise technology adoption; Africa EdTech growth; Increasing smartphone stylus accessories demand |

North America’s 34.6% regional dominance reflects both premium consumer and enterprise adoption strength. Apple’s iPad’s 55–60% US education tablet market share creates a captive Apple Pencil demand pool growth as new iPad cohorts enter education programs.

Asia-Pacific, with 28.4% in 2025, benefits from the region’s status as the world’s largest touchscreen device manufacturing and consumption market. China’s tablet computer shipments rose 13.1% from the previous year to 33.8 million units in 2025, representing the single largest potential stylus addressable market globally. India’s EdTech market growth is driving government-subsidized tablet deployments, where affordable stylus accessories are capturing first-adoption purchases.

Competitive Landscape

The global stylus pen market is moderately concentrated. The top 5 players collectively account for an estimated 65–75% of total global stylus market revenue in 2025.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Apple Inc. |

Apple Pencil Pro, Apple Pencil USB-C |

Leader |

Pixel-perfect precision, Tilt sensitivity, Wireless pairing and charging, Free engraving |

|

Wacom Co. Ltd. |

Bamboo Ink and Bamboo Ink Plus |

Leader |

4,096 pressure levels; digital art brand leadership |

|

Samsung Electronics |

Galaxy S Pen |

Leader |

Integrated foldable device stylus; Galaxy ecosystem |

|

Microsoft Corporation |

Surface Slim Pen |

Leader |

N-Trig 4,096 pressure levels; BLE; enterprise adoption growth; Office integration |

|

Logitech International |

Logitech Crayon (USB-C), Logitech Crayon (Lightning) |

Leader |

Crayon price democratization; USB-C charging; broad compatibility |

|

HP Development Company |

HP Rechargeable MPP 2.0 Tilt Pen, HP MPP1.51 Pen, HP 705 Rechargeable Multi Pen, HP 700 Rechargeable Multi Pen, HP Slim Rechargeable Pen, HP wireless Rechargeable USI Pen |

Challenger |

USI 2.0 compatible; Windows ecosystem; Enterprise procurement; Education channel strength |

|

ASUSTeK Computer |

ASUS Styluses |

Challenger |

Zenbook flip stylus; USI-compatible; Asia-Pacific market reach |

|

Dell Inc. |

Dell Active Pen, Dell Latitude 7350 Detachable Active Pen, and Dell Pro Premium Active Pen |

Challenger |

Latitude / XPS enterprise stylus; Microsoft Ink certified; B2B channel focus |

|

Staedtler Mars GmbH |

Mars Lumograph digital 180 22-3, Mars Lumograph digital Jumbo 180J 22-3, Noris digital classic 180 22, Noris digital Jumbo 180J 22, Noris digital mini 180M |

Emerging |

Eco-certified pencil design; FSC materials; Education channel; EU sustainability positioning |

|

XPPen Technology |

X4 Smart Chip Stylus, X3 Pro Slim Stylus, X3 Pro Roller Stylus, X3 Pro Smart Chip Stylus, PA6 Battery-Free Stylus, PA5 Battery-Free Stylus, P05D Battery-Free Stylus, PH2 Battery-Free Stylus |

Emerging |

Affordability leader USD; Asia-Pacific emerging markets; Compatible with 8,192 levels on legacy PA series. |

The market bifurcates between premium ecosystem-locked OEM styluses (Apple Pencil, Samsung S Pen, Microsoft Surface Pen) commanding high price points and aftermarket/compatible styluses from Adonit, XPPen, and Staedtler at low.

Key Company Profiles

Apple Inc.

Apple Inc., with its iPad segment, is contributing to the market. Apple’s Apple Pencil, launched in 2015, is the world’s highest-revenue stylus product by value, capturing global premium active stylus revenue.

- Product Portfolio: Apple Pencil Pro, Apple Pencil USB-C

- Recent Developments: In October 2023, Apple introduced a new, more affordable Apple Pencil with pixel-perfect accuracy, low latency, and tilt sensitivity.

- Strategic Focus: Apple’s stylus strategy centers on tightly integrating Apple Pencil differentiation with each new iPad hardware generation, using Pencil’s premium features to create upgrade incentives that drive both new Pencil and new iPad purchases simultaneously.

Wacom Co. Ltd.

Wacom Co. Ltd. is the creator of electromagnetic resonance (EMR) stylus technology that underlies the majority of the global professional graphic tablet market.

- Product Portfolio: Bamboo Ink and Bamboo Ink Plus

- Recent Developments: In October 2025, Wacom Co, Ltd., said that its unique digital pen technology has been adopted by Samsung Electronics’ Galaxy Tab S11 Ultra and Galaxy Tab S11.

- Strategic Focus: Wacom’s strategy focuses on premium professional market leadership through continuous EMR technology advancement and deep software ecosystem partnerships with Adobe Creative Cloud, Clip Studio Paint, and Autodesk.

Samsung Electronics

Samsung Electronics is headquartered in Suwon, South Korea. Samsung’s S Pen stylus, introduced with the Galaxy Note series in 2011 and expanded to Galaxy Tab S, Galaxy Z Fold, and select Galaxy S smartphone series, is the world’s most widely distributed integrated device stylus by unit volume.

- Product Portfolio: Galaxy S Pen, Galaxy S Pen Fold Edition, Galaxy S Pen Pro, and the Galaxy S Pen Creator Edition.

- Recent Developments: In July 2023, Samsung Electronics launched its fifth generation of Galaxy foldables like Galaxy Z Fold5.

- Strategic Focus: Samsung’s S Pen strategy leverages the stylus as a Galaxy ecosystem differentiator, particularly in the premium foldable smartphone segment where S Pen integration is a primary purchase driver. The Galaxy AI integration, combining AI note summarization, Circle to Search, and Live Translate for handwritten text, represents Samsung’s strategy to position S Pen as an AI-augmented input device rather than merely a precision drawing tool, targeting productivity-focused enterprise and professional users.

Microsoft Corporation

Microsoft Corporation is headquartered in Redmond, Washington. Microsoft’s Surface Pen launched in 2012 and now in its Slim Pen 2 iteration (2021), is the world’s leading enterprise-focused active stylus, serving corporate, education, and government customers across Microsoft’s Surface Pro, Surface Laptop Studio, and Surface Go device lineup.

- Product Portfolio: Microsoft Surface Pen, Microsoft Surface Slim Pen 2, and Microsoft Ink Workspace.

- Recent Developments: Microsoft expanded Surface Pen compatibility to Microsoft Copilot AI features, enabling stylus-drawn sketches to be automatically described and enhanced by AI within Microsoft Designer and Microsoft Paint Cocreator.

- Strategic Focus: Microsoft’s stylus strategy integrates Surface Pen as a core productivity device within Microsoft 365 and Azure AI ecosystems, targeting enterprise knowledge workers who benefit from handwriting-to-text conversion, digital signature workflows, and AI-augmented inking.

Market Concentration Analysis

The stylus pen market is highly concentrated at the premium tier. Apple alone is estimated to capture 30–35% of global stylus revenue through its Apple Pencil franchise, reflecting the premium pricing and high iPad installed base penetration among US and Western European consumers. The top 3 players Apple, Wacom, and Samsung collectively hold an estimated 52–65% of global stylus revenue, with the remainder highly fragmented across 100+ compatible stylus manufacturers serving price-sensitive global markets.

Consolidation trends are emerging at the mid-market tier. Chinese manufacturers are gaining share in Asia-Pacific and Latin America education markets through aggressive price, potentially displacing Wacom’s entry-level consumer products over the 2026–2030 period.

Investment & Growth Opportunities

Fastest-Growing Segments

Asia-Pacific, at ~9.8% CAGR is the highest-growth regional investment opportunity. China’s high tablet/large-screen device users at current stylus penetration versus North America’s penetration gap, potential additional stylus users as device capabilities and consumer awareness grow. Investment in mid-price active stylus products for China, India, and Southeast Asia education markets is projected to generate more in incremental stylus revenue by 2030. The online channel at ~9.2% CAGR is the highest-return distribution investment, with DTC e-commerce stylus brands achieving customer acquisition.

Emerging Markets

India’s EdTech market growth and Brazil’s primary/secondary school students represent the two highest-potential emerging market stylus demand pools. Both markets are currently dominated by affordable compatible stylus brands, with premium active stylus penetration.

Venture and Investment Trends

USI-compatible stylus accessory startups are attracting early-stage investment as the cross-device compatibility standard creates a new market opportunity independent of OEM ecosystems. AI-powered stylus input, integrating on-device language models for real-time handwriting enhancement, predictive ink completion, and multi-language simultaneous translation represents the next investment frontier, with Apple, Microsoft, and Google all filing handwriting AI patents at accelerating rates in 2023–2024.

Future Market Outlook 2026-2034

The global stylus pen market is positioned for sustained, broad-based growth through 2034, anchored by irreversible digital transformation across education, enterprise, and creative professional sectors. From USD 19.45 Billion in 2025, the market is forecast to reach USD 28.67 Billion by 2030 and USD 40.10 Billion by 2034, representing a USD 20.65 Billion absolute expansion over the nine-year forecast period at a 8.07% CAGR.

Technological disruptions, including AI-augmented handwriting recognition, haptic feedback styluses that simulate paper texture by 2029–2030, and neural-interface stylus prototypes enabling thought-to-ink conversion by the early 2030s, are expected to materially expand the stylus user base beyond its current creative and professional core.

The next decade will witness a fundamental expansion of the stylus’s role in human-computer interaction. As AI writing assistants, generative art tools, and digital collaboration platforms increasingly reward stylus input over keyboard and mouse, offering deeper creative control, more natural interaction, and AI-augmented output quality, stylus pens will transition from specialist accessories to mainstream productivity tools.

Research Methodology

Primary Research

Primary research encompassed over 55 structured interviews in 2024–2025 with stylus pen market participants including product managers and CMOs, purchasing directors, enterprise IT procurement managers, and education technology consultants specializing in 1-to-1 device programs.

Secondary Research

Key secondary sources include IDC Worldwide Tablet Tracker, Ericsson Mobility Report (2024), Apple FY2024 Annual Report, Apple FY2024 10-K filing, Samsung Electronics FY2023 Annual Report, Logitech FY2024 Annual Report, Digital Stationary Consortium (DSC) Digital Pen User Survey (2023), HolonIQ Global Education Technology Market Outlook (2024), and trade journals including Avocet Computing, The Verge, and XDA Developers.

Forecasting Models

IMARC’s Bottom-Up and Top-Down estimation models were applied in parallel and cross-validated. Bottom-Up aggregates stylus demand by device compatibility category across regional markets. Top-Down applies global tablet shipment forecasts (IDC), education technology spending projections, and digital creative market size benchmarks as upper-bound validation parameters.

Stylus Pen Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Resistive Stylus, Capacitive Stylus, Active Stylus |

| Distribution Channels Covered | Online, Offline |

| Applications Covered | Smart Phones, Tablets, Interactive Whiteboards |

| End-Users Covered | OEM, Retail |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Apple Inc., Wacom Co. Ltd., Samsung Electronics, Microsoft Corporation, Logitech International, HP Development Company, ASUSTeK Computer, Dell Inc., Staedtler Mars GmbH, XPPen Technology., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the stylus pen market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global stylus pen market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the stylus pen industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Stylus Pen Market Report

The global stylus pen market reached USD 19.45 Billion in 2025, growing from USD 13.19 Billion in 2020. Growth is driven by tablet proliferation, digital art demand, and active stylus technology adoption across OEM ecosystems.

The market is projected to reach USD 40.10 Billion by 2034 at a CAGR of 8.07%, with an intermediate anchor of USD 28.67 Billion in 2030, driven by Asia-Pacific expansion and AI-powered stylus integration.

Online channels lead at 58.4% in 2025, driven by DTC brand strategies from Apple Store, Wacom eStore, and Amazon marketplace. E-commerce stylus categories grew 12-15% annually versus 4-6% for physical retail in 2020-2025.

OEM dominates at 61.3% in 2020-2025, capturing device-bundled stylus procurement. Apple’s active iPad base, Samsung’s S Pen device shipments, and Microsoft Surface enterprise programs drive OEM channel growth.

North America leads at 34.6% in 2025, anchored by the US EdTech market, student 1-to-1 device programs, Apple Pencil ecosystem dominance, and Microsoft Surface enterprise deployments.

Asia-Pacific at 28.4% (2025) is growing fastest at ~9.8% CAGR, driven by China’s device users, India’s EdTech sector growth, Japan’s digital art culture, and affordable stylus adoption.

Key players include Apple Inc., Wacom Co. Ltd., Samsung Electronics, Microsoft Corporation, Logitech International, HP Development Company, ASUSTeK Computer, Dell Inc., Staedtler Mars GmbH, and XPPen Technology.

Key drivers include tablet shipments, professional digital artists globally, and rising EdTech market.

AI-powered handwriting recognition (Apple Scribble, Microsoft Ink) achieves 95-98% text accuracy, transforming styluses from creative tools to universal input devices. Samsung Galaxy AI S Pen Circle to Search and AI note summarization represent the next AI-stylus integration frontier.

USI 2.0 (2021) is an open cross-device stylus compatibility standard covering 4,096 pressure levels and tilt recognition. With USI-compatible Chromebooks in US K-12 education, USI is projected to cover 300M+ devices by 2028.

Key challenges include device-specific compatibility constraints, premium pricing limiting mass adoption, market saturation in mature professional segments, and USI standardization adoption lag among premium device OEMs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade