Styrene Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition

Styrene Price Trend, Index and Forecast

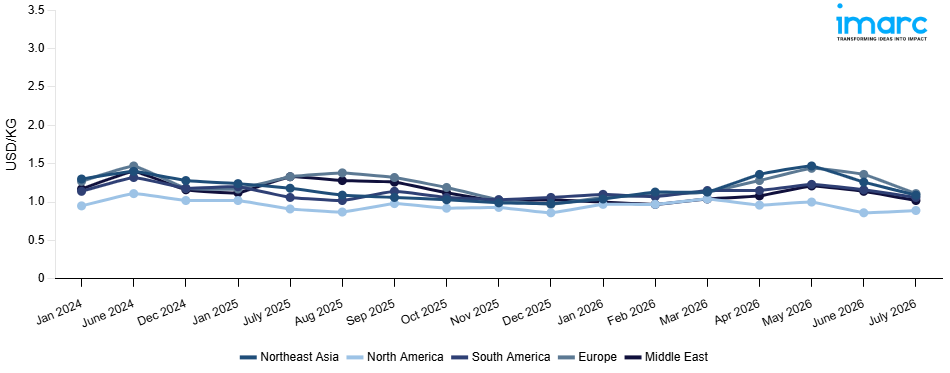

Track real-time and historical styrene prices across global regions. Updated monthly with market insights, drivers, and forecasts.

Styrene Prices July 2026

| Region | Price (USD/KG) | Latest Movement |

|---|---|---|

| Northeast Asia | 1.09 | -13.5% ↓ Down |

| Europe | 1.11 | -18.4% ↓ Down |

| South America | 1.06 | -8.6% ↓ Down |

| Middle East | 1.02 | -10.5% ↓ Down |

| North America | 0.89 | 3.5% ↑ Up |

Styrene Price Index (USD/KG):

The chart below highlights monthly styrene prices across different regions.

Get Access to Monthly/Quarterly/Yearly Prices, Request Sample

Market Overview Q1 Ending March 2026

Northeast Asia: The styrene prices in Northeast Asia reached 1.13 USD/KG in March 2026. The upward pricing movement registered between December and March 2026 was 15.3%. The substantial price appreciation was primarily driven by tightened supply conditions resulting from scheduled maintenance turnarounds at key steam cracker and styrene monomer production facilities, which significantly constrained regional availability. Robust demand from the polystyrene, ABS resin, and expandable polystyrene manufacturing sectors intensified procurement competition amid limited spot market volumes. Escalating upstream benzene and ethylene feedstock costs further elevated production expenses for regional manufacturers. Additionally, heightened consumption from the packaging, automotive components, and construction insulation segments sustained strong offtake fundamentals, while strategic inventory building by downstream polymer producers anticipating continued supply tightness amplified purchasing activity, reinforcing pronounced bullish pricing momentum throughout the quarter.

Europe: The styrene prices in Europe reached 1.13 USD/KG in March 2026. The upward pricing movement registered between December and March 2026 was 16.5%. The significant price appreciation was underpinned by severely constrained supply due to unscheduled plant outages and scheduled maintenance shutdowns at key dehydrogenation and co production facilities, which critically limited regional styrene availability. Sustained demand from the polystyrene, synthetic rubber, and ABS manufacturing sectors maintained robust procurement activity throughout the quarter. Rising upstream benzene and ethylene feedstock costs further reinforced upward pricing pressures across the supply chain. Additionally, elevated energy costs associated with ethylbenzene dehydrogenation processes intensified production cost pressures, while limited import alternatives due to firm international benchmark valuations and elevated freight expenses restricted buyers' sourcing flexibility, maintaining persistently bullish market conditions throughout the quarter.

South America: The styrene prices in South America reached 1.15 USD/KG in March 2026. The upward pricing movement registered between December and March 2026 was 8.5%. The notable price appreciation has been attributed to sustained demand from the polystyrene, expandable polystyrene, and synthetic rubber manufacturing industries, as these sectors maintained healthy levels of procurement activity, coupled with stable consumption from the packaging and construction sectors. Increases in the costs of upstream benzene and ethylene based feedstock used in the production process have raised regional suppliers' production costs, thereby supporting prevailing prices. Constrained supply conditions, driven by limited domestic production capacity, have also supported prevailing prices.

Middle East: The styrene prices in the Middle East reached 1.04 USD/KG in March 2026. The upward pricing movement registered between December and March 2026 was 1.0%. The marginal price increase reflected a largely stable market environment, with steady demand from the polystyrene and synthetic rubber manufacturing sectors sustaining baseline procurement activity throughout the quarter. Firm upstream benzene and ethylene feedstock costs provided incremental pricing support for regional producers. Controlled production output from established dehydrogenation facilities maintained balanced supply demand dynamics, preventing excess market availability. Additionally, moderate consumption from the packaging and construction insulation segments sustained consistent offtake fundamentals, while equilibrium between supply levels and downstream requirements limited significant pricing fluctuation, contributing to near flat yet marginally bullish market conditions across the quarterly period.

Market Overview Q4 Ending December 2025

Northeast Asia: The styrene prices in Northeast Asia reached 0.98 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 7.7%. Prices for styrene remained lower in the quarter as demand downstream from the construction and packaging sectors waned. Local markets also witnessed increased stocks as buyers cut their lifts. Prices fell toward the end due to increased pressure from cheaper feedstocks and higher production levels.

Europe: The styrene prices in Europe reached 0.97 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 26.7%. Prices in European markets were much lower as the automotive and consumer goods industries were not making enough purchases. Low offtake and high stocks made producers to cut their offers. Meanwhile, cheaper energy, trimmed manufacturing costs, accelerating the drop over the quarter.

South America: The styrene prices in South America reached 1.06 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 6.9%. Sluggish consumption from key end-use industries such as plastics, packaging, and construction limited procurement activity, leading converters and processors to operate below capacity and defer large-volume purchases. Regional inventories remained elevated, partly due to steady import availability that outpaced local demand, placing additional pressure on sellers to lower offers to maintain turnover.

Middle East: The styrene prices in the Middle East reached 1.03 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 18.3%. Prices declined, with regional demand weak and supply more than sufficient. Imports from Asian markets jumped, further piling on competitive pressure. Low downstream demand led to the further reduction of prices as traders slashed quotations in order to destock.

North America: The styrene prices in North America reached 0.86 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 12%. Sustained plant operating rates maintained a steady flow of styrene output, resulting in elevated inventory levels that eased immediate supply pressures and reduced bargaining leverage for sellers. Domestic demand from key downstream sectors such as plastics, packaging, and automotive components remained subdued, leading buyers to defer sizeable purchases and maintain cautious procurement strategies.

Market Overview Q3 Ending September 2025

Northeast Asia: Styrene prices in Northeast Asia registered significant downward pressure. The primary driver was subdued demand from downstream polystyrene and ABS resin markets in China, Japan, and South Korea. Automotive and consumer electronics sectors, which account for large styrene consumption, experienced slower recovery due to weakened export orders and reduced consumer spending in major markets. On the supply side, high plant operating rates in China contributed to excess domestic availability, prompting producers to redirect volumes to regional exports. However, freight rates on Asia–Europe trade lanes fluctuated due to Red Sea security concerns, marginally increasing landed costs for exporters. Meanwhile, crude oil and benzene feedstock prices softened, reducing production costs and further weighing on styrene values. Currency depreciation of the Japanese yen and Korean won against the US dollar also impacted import competitiveness, shaping procurement strategies across the region.

Europe: The downward movement was mainly driven by weaker downstream demand from the construction and packaging industries, where polystyrene and ABS applications slowed due to muted consumer spending and housing activity. Supply conditions remained stable as major European producers, including Germany and the Netherlands, operated without significant plant disruptions. However, high energy and feedstock costs, particularly benzene and ethylene, continued to exert upward pressure on production expenses. The depreciation of the euro against the US dollar further complicated import transactions, raising the effective landed cost of imported styrene. Additionally, stricter compliance costs around EU environmental and safety regulations added to logistics and storage expenses.

South America: Styrene prices in South America increased. The rise was largely attributed to supply-side constraints and strong domestic demand, especially from Brazil’s automotive and packaging sectors. Plant maintenance activities in key regional producers temporarily reduced output, while dependence on imports from the US Gulf Coast and Asia amplified exposure to freight volatility. Currency fluctuations, particularly the depreciation of the Brazilian real against the US dollar, added to the cost of imports, making styrene procurement costlier for domestic processors. On the logistics front, higher port handling charges in Santos and Buenos Aires contributed to elevated supply chain costs. Moreover, limited local infrastructure for bulk handling of petrochemicals led to higher inland transportation expenses. Demand for downstream derivatives such as expandable polystyrene (EPS) in insulation and packaging remained resilient, which supported stronger offtake.

Middle East: The market was influenced by robust production rates in Saudi Arabia and the UAE, where integrated facilities ensured stable output despite fluctuating benzene feedstock values. Export availability increased as suppliers sought to capture demand in Asia, but heightened competition from lower-cost Chinese cargoes limited price realizations. Domestic consumption from plastics and packaging segments remained steady, though demand from construction was constrained due to delays in mega-infrastructure projects. Shipping costs through the Suez Canal corridor spiked intermittently due to security risks, impacting export margins. Additionally, high energy input costs and compliance expenditures for environmental standards in Gulf economies added to operational expenses. However, abundant regional supply coupled with limited incremental demand kept styrene prices on a softening path in Q3 2025.

North America: The rise was primarily attributed to tighter regional supply and improving downstream demand. Feedstock benzene values also strengthened due to higher crude oil benchmarks, raising production costs for styrene. On the demand side, downstream segments such as polystyrene for food packaging and ABS for automotive components displayed stronger offtake, particularly as US consumer spending rebounded modestly during late summer. Export activity gained momentum as buyers in Latin America and Europe turned to US cargoes amid fluctuating Asian supplies, helping support price resilience. Logistics conditions added further cost layers, trucking shortages across Texas and Louisiana raised domestic freight rates, while Gulf Coast port handling fees edged higher following new compliance requirements for hazardous cargo.

Styrene Price Trend, Market Analysis, and News

IMARC's latest publication, “Styrene Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition,” presents a detailed examination of the styrene market, providing insights into both global and regional trends that are shaping prices. This report delves into the spot price of styrene at major ports and analyzes the composition of prices, including FOB and CIF terms. It also presents detailed styrene prices trend analysis by region, covering North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. The factors affecting styrene pricing, such as the dynamics of supply and demand, geopolitical influences, and sector-specific developments, are thoroughly explored. This comprehensive report helps stakeholders stay informed with the latest market news, regulatory updates, and technological progress, facilitating informed strategic decision-making and forecasting.

Styrene Industry Analysis

The global styrene industry size reached USD 62.92 Billion in 2025. By 2034, IMARC Group expects the market to reach USD 94.36 Billion, at a projected CAGR of 4.60% during 2026-2034. The market is driven by expanding demand for polystyrene in packaging, insulation materials in construction, and ABS resins in automotive applications. Rising consumption in consumer electronics and the shift toward lightweight materials in vehicles are additional drivers fueling the industry expansion.

Latest developments in the styrene industry:

- April 2025: Clariant and Technip Energies teamed up to unveil a breakthrough catalyst for styrene production that operated at an industry-first ultra-low steam-to-oil (S/O) ratio. The new catalyst, branded StyroMax UL-100, represented a major advance in styrene monomer technology.

- April 2024: Ineos completed the acquisition of Naphtachimie, Gexaro and Appryl, which were a 50: 50 Joint Venture between Ineos and TotalEnergies in Southern France at Lavera.

- November 2022: Chevron Philips Chemical Company LLC and Qatar Energy announced that they are proceeding with the construction of an $ 8.5 billion integrated polymers facility in orange TX likely to create more than 500 full time jobs and approximately 4500 construction jobs in generate an estimated $50 billion for the community in residual economic impacts.

Product Description

Styrene is an aromatic hydrocarbon monomer classified as a derivative of benzene, appearing as a colorless, oily liquid with a distinctive sweet odor. It is a vital petrochemical feedstock, ranking among the most consumed monomers worldwide. Its defining attribute lies in its versatility, as it readily polymerizes to produce a broad range of plastics and resins. Industrially, styrene is primarily used in manufacturing polystyrene, acrylonitrile butadiene styrene (ABS), styrene-butadiene rubber (SBR), and unsaturated polyester resins. These materials enhance product performance by delivering durability, insulation, and lightweight properties, making styrene indispensable across packaging, automotive, construction, and consumer goods industries.

Report Coverage

| Key Attributes | Details |

|---|---|

| Product Name | Styrene |

| Report Features | Exploration of Historical Trends and Market Outlook, Industry Demand, Industry Supply, Gap Analysis, Challenges, Styrene Price Analysis, and Segment-Wise Assessment. |

| Currency/Units | US$ (Data can also be provided in local currency) or Metric Tons |

| Region/Countries Covered | The current coverage includes analysis at the global and regional levels only. Based on your requirements, we can also customize the report and provide specific information for the following countries: Asia Pacific: China, India, Indonesia, Pakistan, Bangladesh, Japan, Philippines, Vietnam, Thailand, South Korea, Malaysia, Nepal, Taiwan, Sri Lanka, Hongkong, Singapore, Australia, and New Zealand Europe: Germany, France, United Kingdom, Italy, Spain, Russia, Turkey, Netherlands, Poland, Sweden, Belgium, Austria, Ireland, Switzerland, Norway, Denmark, Romania, Finland, Czech Republic, Portugal and Greece* North America: United States and Canada Latin America: Brazil, Mexico, Argentina, Columbia, Chile, Ecuador, and Peru Middle East & Africa: Saudi Arabia, UAE, Israel, Iran, South Africa, Nigeria, Oman, Kuwait, Qatar, Iraq, Egypt, Algeria, and Morocco The list of countries presented is not exhaustive. Information on additional countries can be provided if required by the client. |

| Information Covered for Key Suppliers |

|

| Customization Scope | The report can be customized as per the requirements of the customer |

| Report Price and Purchase Option |

Plan A: Monthly Updates - Annual Subscription

Plan B: Quarterly Updates - Annual Subscription

Plan C: Biannually Updates - Annual Subscription

|

| Post-Sale Analyst Support | 360-degree analyst support after report delivery |

| Delivery Format | PDF and Excel through email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report presents a detailed analysis of styrene pricing, covering global and regional trends, spot prices at key ports, and a breakdown of FOB and CIF prices.

- The study examines factors affecting styrene price trend, including input costs, supply-demand shifts, and geopolitical impacts, offering insights for informed decision-making.

- The competitive landscape review equips stakeholders with crucial insights into the latest market news, regulatory changes, and technological advancements, ensuring a well-rounded, strategic overview for forecasting and planning.

- IMARC offers various subscription options, including monthly, quarterly, and biannual updates, allowing clients to stay informed with the latest market trends, ongoing developments, and comprehensive market insights. The styrene price charts ensure our clients remain at the forefront of the industry.

Frequently Asked Questions About the Styrene Price Index Report

The styrene prices in July 2026 were 1.09 USD/Kg in Northeast Asia, 1.11 USD/Kg in Europe, 1.06 USD/Kg in South America, 1.02 USD/Kg in the Middle East, and 0.89 USD/Kg in North America.

The styrene pricing data is updated on a monthly basis.

We provide the pricing data primarily in the form of an Excel sheet and a PDF.

Yes, our report includes a forecast for styrene prices.

The regions covered include North America, Europe, Asia Pacific, Middle East, and Latin America. Countries can be customized based on the request (additional charges may be applicable).

Yes, we provide both FOB and CIF prices in our report.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Inquire Before Buying

Inquire Before Buying

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Why Choose Us

IMARC offers trustworthy, data-centric insights into commodity pricing and evolving market trends, enabling businesses to make well-informed decisions in areas such as procurement, strategic planning, and investments. With in-depth knowledge spanning more than 1000 commodities and a vast global presence in over 150 countries, we provide tailored, actionable intelligence designed to meet the specific needs of diverse industries and markets.

1000

+Commodities

150

+Countries Covered

3000

+Clients

20

+Industry

Robust Methodologies & Extensive Resources

IMARC delivers precise commodity pricing insights using proven methodologies and a wealth of data to support strategic decision-making.

Subscription-Based Databases

Our extensive databases provide detailed commodity pricing, import-export trade statistics, and shipment-level tracking for comprehensive market analysis.

Primary Research-Driven Insights

Through direct supplier surveys and expert interviews, we gather real-time market data to enhance pricing accuracy and trend forecasting.

Extensive Secondary Research

We analyze industry reports, trade publications, and market studies to offer tailored intelligence and actionable commodity market insights.

Trusted by 3000+ industry leaders worldwide to drive data-backed decisions. From global manufacturers to government agencies, our clients rely on us for accurate pricing, deep market intelligence, and forward-looking insights.