Surgical Dressing Market Size, Share, Trends and Forecast by Product, Application, End User, and Region, 2026-2034

Surgical Dressing Market Size and Share:

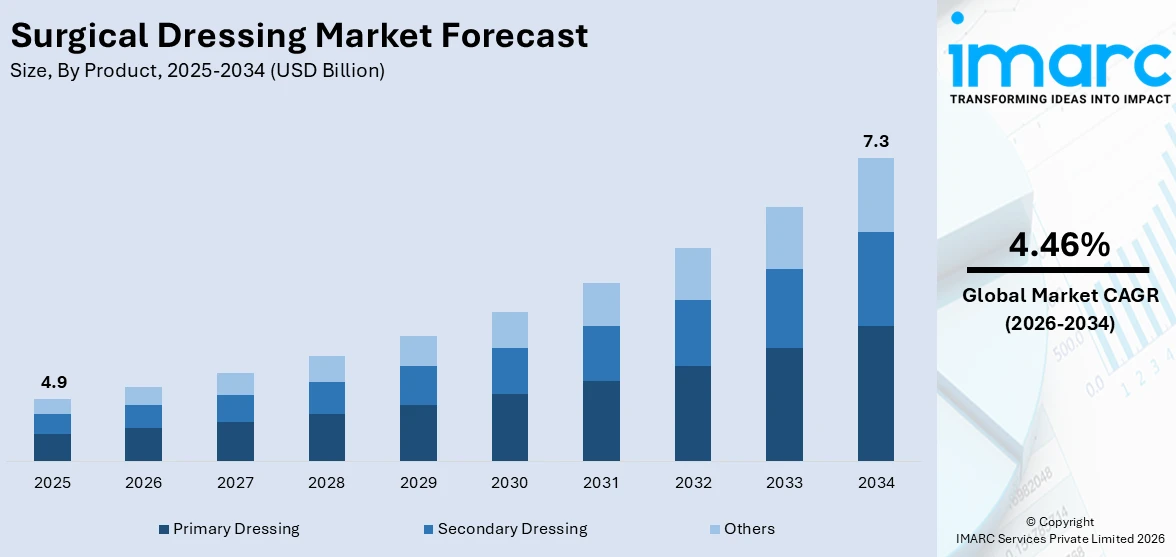

The global surgical dressing market size was valued at USD 4.9 Billion in 2025. The market is projected to reach USD 7.3 Billion by 2034, exhibiting a CAGR of 4.46% from 2026-2034. North America currently dominates the market, holding a market share of over 38% in 2025. The market is driven by the rising volume of surgical procedures, growing incidence of chronic wounds, and increasing geriatric population. Increased use of minimally invasive surgeries, technological advancements in dressing materials, and increased emphasis on infection control and better recovery of patients are fueling market demand. Healthcare professionals are increasingly adopting advanced wound care solutions in clinical practice to improve treatment outcomes and comfort for the patients, which together contribute to the growth of the surgical dressing market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 4.9 Billion |

|

Market Forecast in 2034

|

USD 7.3 Billion |

| Market Growth Rate 2026-2034 | 4.46% |

With healthcare systems emphasizing improving patient outcomes and minimizing postoperative complications, the need for high-performance surgical dressings has grown. These dressings offer optimal protection of wounds, absorb exudate, and allow for quicker healing, which is ever more sought after in hospital and outpatient treatment as well. Growth of specialty hospitals and treatment facilities globally has enabled the adoption of advanced dressing solutions into standard surgical procedures. According to reports, in April 2024, Remedium Healthcare launched NuVeria Labs' Sacral Silicone Dressing on Amazon, offering advanced wound care with superior comfort, prolonged wear, and accessible home and clinical application. Furthermore, increased awareness on the part of health professionals about infection prevention, patient safety, and evidence-based best practice approaches to wound care has also seen high uptake. The focus on developing sterile conditions and minimizing post-surgical complications further supports the preference for technology-driven products. Intensified global focus towards better recovery protocols, along with increased emphasis on patient-focused care, has created a promising scenario for the incorporation of surgical dressings, leading to consistent market growth globally.

To get more information on this market Request Sample

In United States, the market for surgical dressings is dominated by the growing number of surgical procedures and the continuous upsurge in healthcare infrastructure with 85% share in 2024. Expansion in ambulatory surgery centers, specialty clinics, and hospitals has enhanced accessibility for surgical care, which directly increased the demand for quality wound management solutions. Surgical dressings are becoming more used to provide post-operative protection, minimize the likelihood of infection, and promote patient comfort. As per sources, in September 2024, US-based Solventum launched the V.A.C. Peel and Place Dressing, an all-in-one solution for negative pressure wound therapy, reducing application time by 61% and extending wear up to seven days. Moreover, health facility investments and efforts to promote standardized surgery have further contributed to the adoption of advanced dressing technology into regular treatment. As healthcare practitioners are more aware of wound care best practices, the trend is toward products that enhance the healing process and maximize recovery. The union of increased volume of surgeries, well-stacked health infrastructure, and focus on efficacious post-operative care helps create a consistent surgical dressing market growth pattern., with long-term opportunities for innovation and growth in wound care.

Surgical Dressing Market Trends:

Increased Number of Chronic Conditions and Wound Cases

Rising occurrences of chronic wounds, ulcers, and burns are a strong impetus for the wound care industry. Increasing chronic diseases, inactive lifestyle, and unhealthy eating have helped fuel an increasing patient population that demands advanced treatment. In the United States alone, 42% of Americans have two or more chronic diseases, and 12% have five or more, necessitating a severe need for advanced solutions. Moreover, the increase in organ transplant surgeries, most notably knee and hip replacements, has also increased demand for post-surgical dressings and follow-ups. Road traffic accidents further enhance the need for good-quality surgical treatments, giving way to greater adoption of surgical dressings. The increasing geriatric population, which has reduced capabilities for wound healing, increases market demand. With estimated global population aged 65 and above predicted to hit 2.2 billion during the late 2070s, overtaking children under the age of 18, these aspects together outline the main surgical dressing market trends and highlight the long-term growth potential for wound care products and services globally.

Widening Healthcare Infrastructure and Outpatient Services

Ambulatory surgery centers and specialty clinics' expansion is fueling demand in the wound care market. These facilities provide low-cost outpatient treatments, expanding access to advanced wound management solutions. The increased use of minimally invasive procedures, most notably cardiovascular and orthopedic procedures, has also fueled the demand for surgical dressings and associated products. Government programs focusing on sanitized, affordable healthcare are increasing patient accessibility and growth prospects for wound care products worldwide. For instance, the Indian government invested Rs. 99,858 crore (USD 11.50 billion) during the Union Budget 2025–26 on the growth and improvement of healthcare infrastructure, emphasizing global attention towards well-equipped hospitals. Concurrently, easy product availability via online and offline organized retail platforms enables larger market coverage and convenience. The synergistic impact of growing infrastructure, policy favorability, and growing surgical interventions provides a strong foundation to perpetuate future growth and offers long-term prospects for the global wound care market.

Technological Innovation and Wound Care Innovation

Technological innovation remains a driving force behind the wound care market, improving the effectiveness of treatments and patient outcomes. Improvements in surgical technologies, pain management modalities, and post-operative care products are facilitating medical practitioners to provide quicker, more efficient recovery routes. The rising demand for minimally invasive treatments, along with more cardiovascular and orthopedic procedures, highlights the role of innovation in fuelling market growth. Increased healthcare spending worldwide enables hospitals and clinics to embrace advanced wound care technologies, from advanced dressings to infection prevention products. Moreover, studies into speeding up healing, minimizing complications, and enhancing overall patient experience support a competitive and dynamic market environment. These developments, together with positive government healthcare policies and growing awareness of post-operative care, keep the wound care market responsive to changing patient needs while promoting efficiency, safety, and better outcomes in healthcare systems globally.

Surgical Dressing Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global surgical dressing market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, application, and end user.

Analysis by Product:

- Primary Dressing

- Film Dressing

- Hydrogel Dressing

- Hydrocolloid Dressing

- Foam Dressing

- Alginate Dressing

- Others

- Secondary Dressing

- Absorbents

- Bandages

- Adhesive Tapes

- Protectives

- Others

- Others

The primary dressing segment contributed 50.2% in 2025 and remains the largest player in the surgical dressing market outlook because of its vital function in wound care being one of the prominent drivers. These dressings are used directly over surgical wounds to absorb exudate, act as a protective barrier against infection, and facilitate healing. Their versatility and suitability to most surgical procedures make them a favorite among healthcare providers. Development in the field of material science has enhanced the functionality of primary dressings, integrating features like increased absorption, antimicrobial activity, and patient comfort. These features render them especially effective for post-operative care in both inpatient and outpatient environments. Increasing cognizance among surgeons and clinicians regarding the necessity for optimized wound healing further supports the use of primary dressings. In addition, the growing volume of surgeries and focus on reducing post-operative complications are factors that support the continued growth of this segment globally.

Analysis by Application:

- Ulcers

- Burns

- Organ Transplants

- Cardiovascular Disease

- Diabetes Based Surgeries

- Others

Burns segment held 30.3% share in 2025, as burn injuries require specialized care to prevent infection, accelerate healing, and reduce scarring, fueling strong demand for advanced surgical dressings. These dressings are designed to maintain optimal moisture, absorb exudate, and protect damaged tissue, supporting faster recovery and minimizing complications. The rising incidence of burn cases worldwide, caused by accidents, fire-related injuries, and industrial hazards, has led healthcare providers to increasingly adopt hydrocolloid, hydrogel, and antimicrobial dressings for effective wound management. Medical professionals prefer these advanced dressings to improve healing outcomes, reduce pain, and prevent infection, particularly in severe or chronic burn cases. The segment benefits from growing awareness of proper burn treatment protocols, technological innovations in dressing materials, and improvements in biocompatibility and durability. Together, these factors are driving consistent demand for burn-specific surgical dressings and contributing to the overall expansion of the global surgical dressing market.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Hospital

- Specialty Clinics

- Home Healthcare

- Ambulatory Surgery Centers

- Others

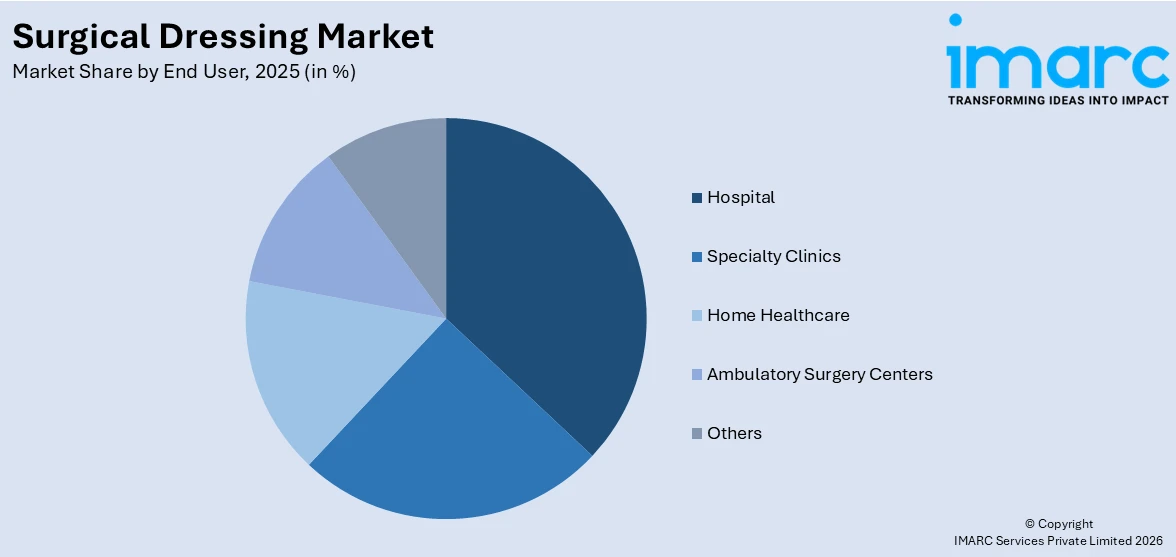

The hospital segment contributed 37.4% in 2025 and continues to be the biggest end-user of surgical dressings worldwide. These are major sites for surgeries that cover from routine treatments to complicated procedures involving advanced wound care options. The uptake of surgical dressings in hospitals follows the demand for clean, effective, and efficient wound management techniques that promote patient safety and hasten recovery. Hospitals are investing more in high-performance dressings with qualities including antimicrobial barrier, increased absorbency, and patient comfort. The boosting number of surgeries, growth in healthcare infrastructure, and emphasis on minimizing post-operative complications are the factors driving the persistent demand for surgical dressings at hospitals. Moreover, the hospitals tend to be institutions of excellence where medical staff are trained to use advanced dressings effectively, revalidating their pivotal role in the implementation of these products. Hence, the hospital segment represents a leading contributor to general market growth.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

The North America market held 38% share in 2025 and remains the leading surgical dressing market owing to developed healthcare facilities and high volumes of surgical procedures. The region's established hospitals, ambulatory surgery centers, and specialty clinics are progressively embracing advanced wound care solutions to maximize patient recovery and reduce post-operative complications. Increasing healthcare technology investments and infection prevention focus have also propelled the need for high-quality surgical dressings. Furthermore, an aging population and rising incidence of chronic conditions that necessitate multiple surgeries have also fueled market expansion. Healthcare professionals' awareness of best practices in wound care and evidence-based practices also underpin the strong adoption of surgical dressings across North America. The intersection of technological advancement, organized healthcare delivery systems, and intense patient demand establishes the region as a major driver of the global market.

Key Regional Takeaways:

United States Surgical Dressing Market Analysis

United States has witnessed increased surgical dressing adoption due to a surge in chronic wounds, ulcers, and burns. For instance, 6 out of 10 Americans have one chronic disease and four out of 10 have two or more chronic diseases that account for ninety percent of the USD 4.5 Trillion annual health care costs in the nation. Rising cases of diabetic foot ulcers, pressure sores, and venous leg ulcers have accelerated the demand for advanced wound care solutions. Burn injuries and traumatic wounds from accidents also contribute to the increased need for specialized surgical dressings. With higher prevalence of lifestyle diseases and surgical procedures, healthcare providers are focusing on efficient wound management. The emphasis on reducing hospital stay durations and preventing infection rates further propels the demand for innovative dressing types. Enhanced awareness among patients and physicians, alongside technological advancements in wound healing materials, continues to support market growth.

Asia Pacific Surgical Dressing Market Analysis

Asia-Pacific is experiencing a rapid increase in knee and hip replacement surgeries, which is significantly boosting the demand for surgical dressings. A rise in aging population, coupled with more sedentary lifestyles, has led to a growing incidence of orthopedic disorders, necessitating joint replacement procedures. Hospitals and surgical centers in urban and semi-urban areas are performing a higher volume of knee and hip surgeries, requiring sterile and efficient wound care post-operation. Surgical dressing products that support faster healing and reduce infection risks are being widely adopted. Innovations in dressing materials and improvements in hospital infrastructure are further accelerating the trend.

Europe Surgical Dressing Market Analysis

Europe is observing a notable rise in surgical dressing adoption, primarily attributed to its growing geriatric population. According to the WHO, the population aged 60 and older is rapidly growing in the WHO European Region. In 2021, there were 215 Million; by 2030, it is projected to be 247 Million, and by 2050, over 300 Million. Aging individuals are more susceptible to chronic wounds, surgical interventions, and slower wound healing, increasing the reliance on effective wound care solutions. Post-operative care for elderly patients requires advanced dressing products that ensure comfort, minimize complications, and promote healing. Healthcare systems across the region are adapting to the needs of older demographics, resulting in greater usage of customized surgical dressing options. Rising hospital admissions for age-related conditions and a higher frequency of surgeries among older adults are contributing factors. The geriatric population also demands home-based wound care solutions, further supporting the market.

Latin America Surgical Dressing Market Analysis

Latin America is witnessing increased investment in the healthcare sector, which is directly influencing the growth of the surgical dressing market. For instance, budget allocation for Brazil’s Unified Health System is expected to boost by 6.2% in 2025. As public and private stakeholders expand hospital infrastructure and upgrade medical facilities, the need for quality wound care products is growing. The focus on enhancing surgical outcomes and reducing infection rates is prompting healthcare institutions to adopt advanced surgical dressings.

Middle East and Africa Surgical Dressing Market Analysis

Middle East and Africa are seeing increased surgical dressing adoption due to expanding healthcare facilities and privatization across both regions. For instance, the Saudi healthcare sector is experiencing unprecedented privatization as part of Vision 2030, with over 290 hospitals and 2,300 health institutions transitioning into private operations. With more hospitals, clinics, and surgical centres being established, there is a greater need for standardized wound care protocols. Investments in healthcare infrastructure, including modern surgical units, are raising the demand for efficient post-operative care solutions.

Competitive Landscape:

The competitive dynamics of the surgical dressing market are influenced by ongoing innovation, product differentiation, and growth in distribution channels. Industry players are setting their sights on creating more sophisticated dressing products with better absorbency, antimicrobial capabilities, and patient comfort to keep up with increasing demand in hospitals, specialty clinics, and ambulatory surgery centers. Strategic moves like partnerships, alliances, and forays into emerging markets are helping firms enhance their market positions and expand their customer bases. Higher spending on research and development is propelling the launch of next-generation dressings designed to meet specific surgical and chronic wound needs. The increasing use of minimally invasive procedures and increased awareness of successful wound management also spur competition. Focused on technological growth and patient-centric solutions, the surgical dressing industry is about to grow consistently, indicating a favorable surgical dressing market forecast.

The report provides a comprehensive analysis of the competitive landscape in the surgical dressing market with detailed profiles of all major companies, including:

- 3M Company

- Advancis Medical

- B. Braun Melsungen AG

- Cardinal Health Inc.

- Coloplast A/S

- Convatec Group plc

- DeRoyal Industries Inc.

- Molnlycke Health Care AB

- Paul Hartmann AG

- Smith & Nephew Plc

Latest News and Developments:

- July 2025: UWE Bristol researchers developed a breakthrough surgical dressing that progressed from lab innovation to global application after Convatec Group plc acquired its commercialization rights in a USD 224 Million deal, aiming to transform care for slow-healing wounds and diabetic ulcers.

- July 2025: Scientists from BITS Pilani Hyderabad developed a smart wound dressing that killed infection-causing bacteria and signaled infection presence without antibiotics. The dressing also enabled instant infection detection through a color-based photo analysis app, addressing challenges in early infection identification in chronic or deep wounds.

- July 2025: CelluHeal™ launched its full line of advanced wound dressings, including Cellufil® and Cellusheet® collagen products, for online purchase across the USA, Canada, and internationally, offering professional dressing solutions for surgical wounds, ulcers, burns, and tattoo aftercare.

- May 2025: Summit Products Group officially launched and announced a strategic alliance with NovaBone to enhance surgical dressing and regenerative wound care, becoming the exclusive distributor of NovaForm® Wound Matrix, a bioengineered dressing recently cleared by the FDA for managing surgical and chronic wounds.

- May 2025: Forward Science released PerioStōm®, an FDA-cleared oral wound dressing designed to support healing after dental procedures like scaling and root planing, using chitosan microspheres for antimicrobial and anti-inflammatory benefits. The dressing was applied with precision and aimed to reduce biofilm, patient discomfort, and enhance periodontal outcomes.

Surgical Dressing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Applications Covered | Ulcers, Burns, Organ Transplants, Cardiovascular Disease, Diabetes Based Surgeries, Others |

| End Users Covered | Hospital, Specialty Clinics, Home Healthcare, Ambulatory Surgery Centers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 3M Company, Advancis Medical, B. Braun Melsungen AG, Cardinal Health Inc., Coloplast A/S, Convatec Group plc, DeRoyal Industries Inc., Molnlycke Health Care AB, Paul Hartmann AG, Smith & Nephew Plc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the surgical dressing market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global surgical dressing market.

- The study maps the leading as well as the fastest growing regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the surgical dressing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Surgical Dressing Market Size Report

The surgical dressing market was valued at USD 4.9 Billion in 2025.

The surgical dressing market is projected to exhibit a CAGR of 4.46% during 2026-2034, reaching a value of USD 7.3 Billion by 2034.

The market is dominated by the growing number of surgeries, growing chronic wound and post-operative complication cases, and the expanding geriatric population. Improvement in healthcare infrastructure, rising infection prevention awareness, growing adoption of minimally invasive surgery, and innovation in wound care products contribute further to the steady demand and growth in the market.

North America currently dominates the surgical dressing market, accounting for a share of 38%. The position of leadership in the region is backed by strong healthcare infrastructure, large volumes of surgical procedures, and mass adoption of new-generation wound care technologies. Healthcare technology investments established hospital and ambulatory centers, and focus on patient safety and recovery processes support North America's leadership in the market.

Some of the major players in the surgical dressing market include 3M Company, Advancis Medical, B. Braun Melsungen AG, Cardinal Health Inc., Coloplast A/S, Convatec Group plc, DeRoyal Industries Inc., Molnlycke Health Care AB, Paul Hartmann AG, Smith & Nephew Plc, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)