Syngas Market Size, Share, Trends and Forecast by Gasifier Type, Feedstock, Technology, End-Use, and Region, 2026-2034

Global Syngas Market Size, Share, Trends & Forecast (2026-2034)

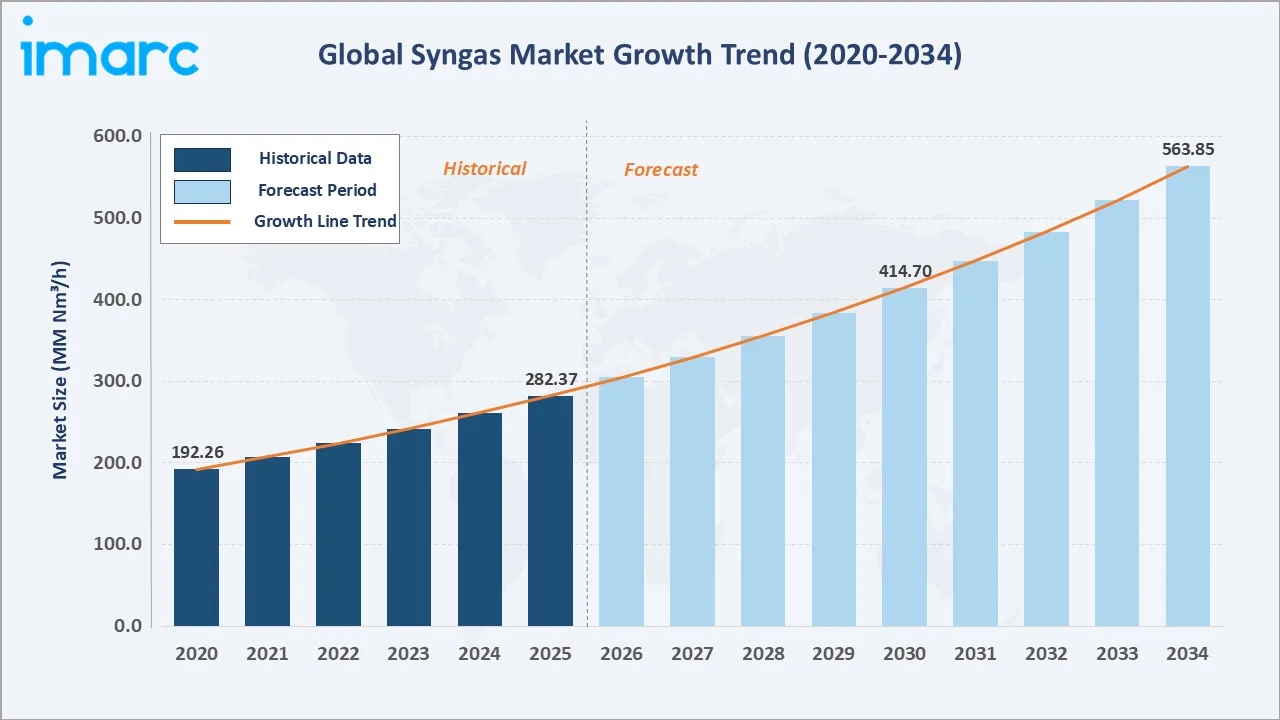

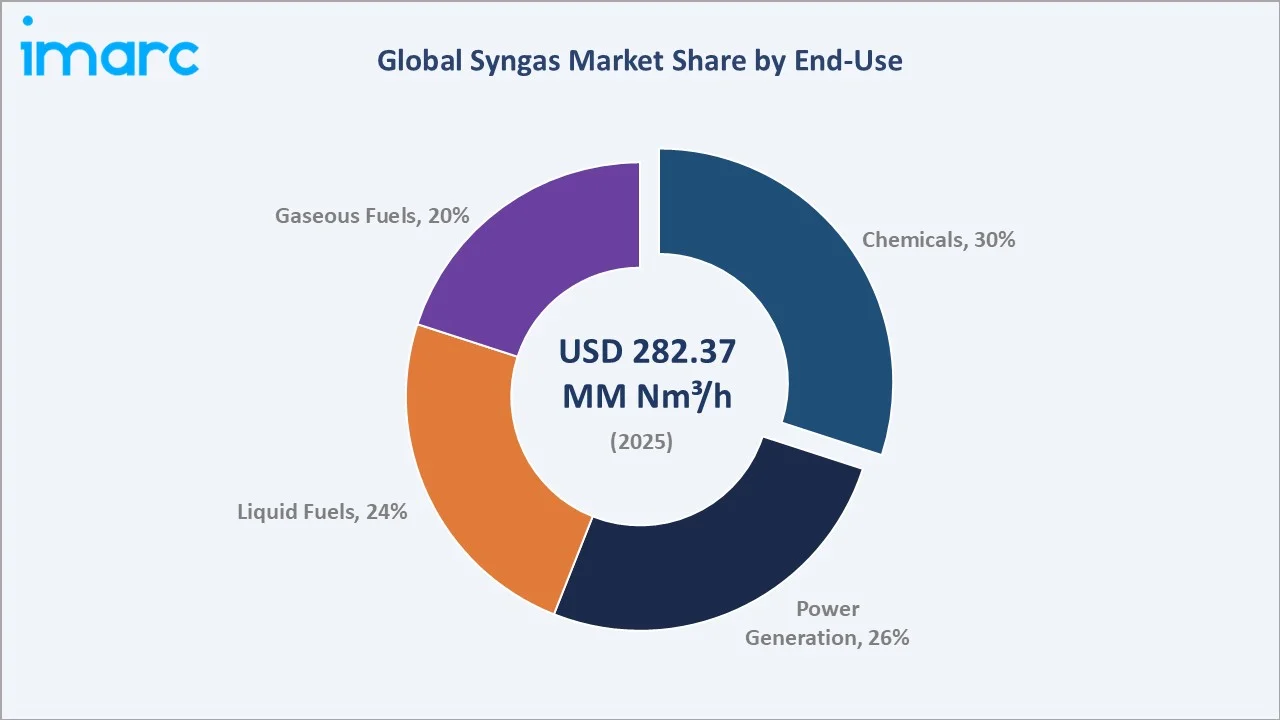

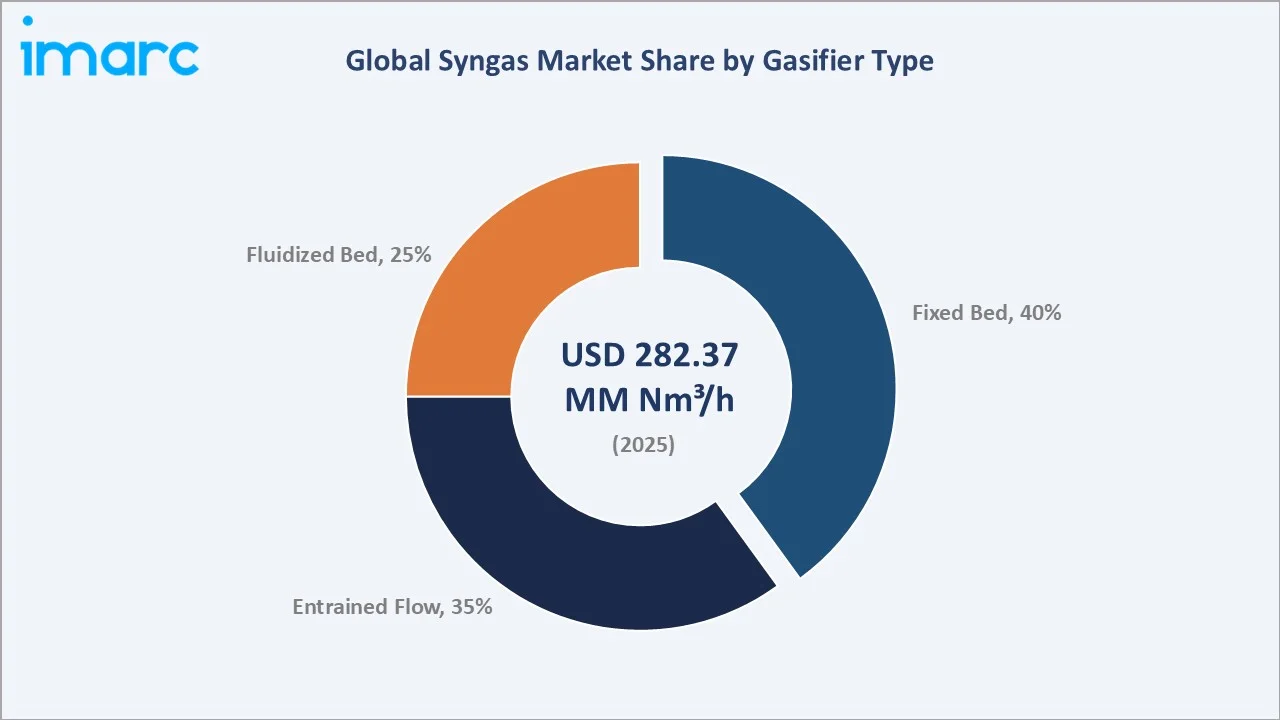

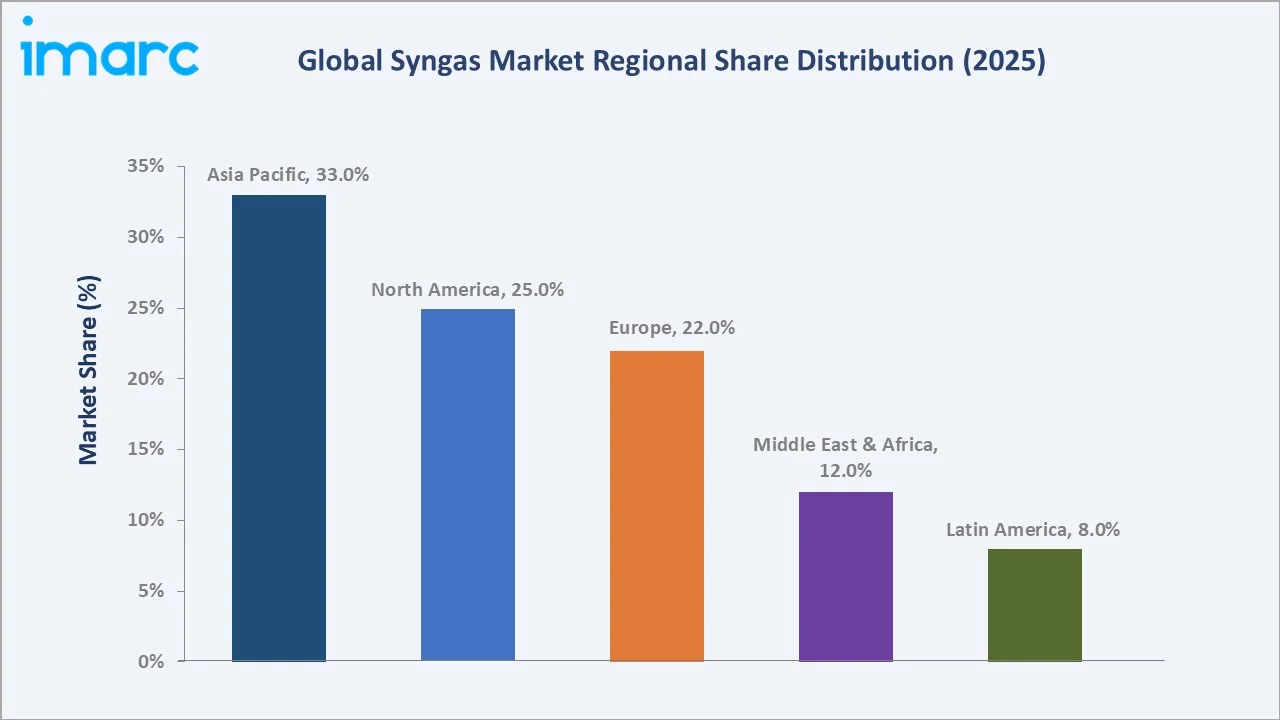

The global syngas market size reached 282.37 MM Nm³/h in 2025and is projected to reach 563.85 MM Nm³/h by 2034, exhibiting a CAGR of 7.99% during 2026-2034. Accelerating energy transition, rising demand for clean hydrogen, and expanding chemical manufacturing are collectively driving syngas market growth. Chemicals dominate with a 30% end-use share in 2025, while Fixed Bed gasifiers lead gasifier-type segmentation at 40%. Asia Pacific commands a 33% regional share, reinforced by large-scale industrial output across China and India.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

282.37 MM Nm³/h |

|

Forecast Market Size (2034) |

563.85 MM Nm³/h |

|

CAGR (2026-2034) |

7.99% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (33% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading End-Use Segment |

Chemicals (30%, 2025) |

|

Leading Gasifier Type |

Fixed Bed (40%, 2025) |

The chart below illustrates syngas market growth from 2020 through 2034, combining historical performance with forecast projections driven by clean energy and hydrogen demand.

To get more information on this market, Request Sample

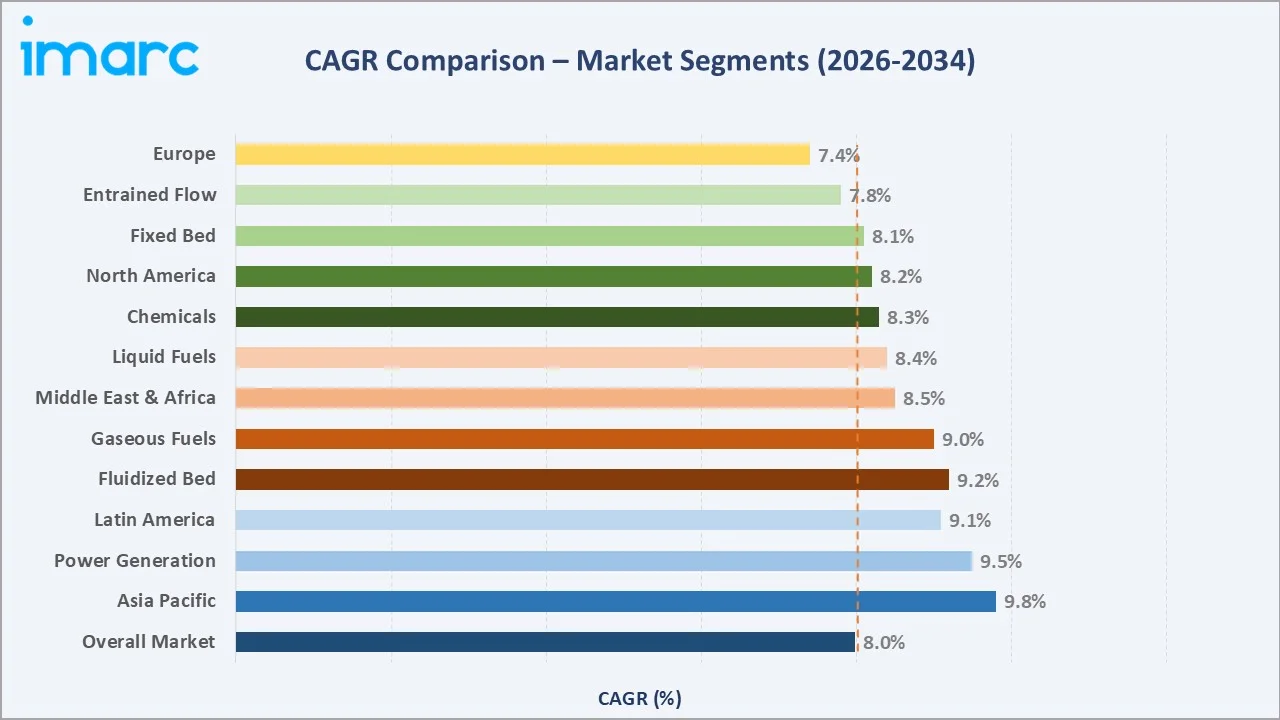

CAGR analysis indicates that Power Generation and Fluidized Bed gasifiers will be the fastest-growing segments in the global syngas market through 2034, driven by decarbonization investments and green syngas expansion.

Executive Summary

The global syngas market is transforming due to energy transition, green hydrogen demand, and industrial decarbonization. The market is projected to grow from 282.37 MM Nm³/h in 2025 to 563.85 MM Nm³/h by 2034, at a 7.99% CAGR, driven by rising gasification investments and expanding applications across chemicals, power, and fuels.

Chemicals hold the largest share at 30% in 2025, driven by ammonia, methanol, and hydrogen production. Fixed Bed gasifiers lead with 40%, due to simplicity and lower capital costs, while Power Generation ranks second at 26%, supported by IGCC plant deployments.

Asia Pacific leads with 33% share in 2025, driven by China’s coal-to-chemicals sector and India’s rising energy demand. North America holds 25%, supported by U.S. hydrogen initiatives and IRA investments, while Europe accounts for 22% and is the one of the fastest-growing region due to the EU Green Deal and REPowerEU.

Key Market Insights

|

Insight |

Data |

|

Largest End-Use Segment |

Chemicals – 30% share (2025) |

|

Second End-Use Segment |

Power Generation – 26% share (2025) |

|

Leading Gasifier Type |

Fixed Bed – 40% share (2025) |

|

Fastest Growing Gasifier |

Fluidized Bed – CAGR ~9.2% (2026-2034) |

|

Leading Region |

Asia Pacific – 33% revenue share (2025) |

|

Second Region |

North America – 25% revenue share (2025) |

|

Top Companies |

Air Products, Air Liquide, BASF SE, Linde plc, Shell, Siemens Energy |

|

Market Opportunity |

Green hydrogen via biomass gasification and CCUS integration |

Key Analytical Observations Supporting The Above Data:

- Chemicals’ 30% share in 2025 highlights syngas’ critical role as a feedstock for ammonia, methanol, hydrogen, and dimethyl ether, with rising demand across fertilizers, energy storage, and pharmaceuticals.

- Power Generation’s 26% share in 2025 is supported by IGCC technology deployment across Japan, South Korea, and the United States, where syngas offers a lower-emission alternative to direct coal combustion.

- Fixed Bed gasifiers’ 40% market leadership is attributable to their cost-effectiveness and operational suitability for coal and biomass feedstocks across emerging markets, particularly in South and Southeast Asia.

- Asia Pacific’s 33% global dominance is reinforced by Coal-based synthetic ammonia and methanol accounted for 78% and 84% of total ammonia and methanol output, through syngas pathways as of 2024.

- North America’s 25% share is underpinned by the U.S. clean hydrogen market, with over USD 8 Billion allocated under the Bipartisan Infrastructure Law for hydrogen hubs, many of which integrate syngas production.

- Linde plc and Air Products together generated approximately USD 45 billion in FY2024 revenues from industrial gases, hydrogen, and syngas-related operations globally.

Global Syngas Market Overview

Syngas (synthesis gas) is a mixture primarily of hydrogen and carbon monoxide, often containing carbon dioxide and trace gases, produced via gasification or reforming of carbon-based feedstocks such as coal, natural gas, petroleum, pet-coke, biomass, and industrial waste. The syngas value chain includes feedstock suppliers, gasification technology providers, syngas producers, downstream processors, and end-use industrial consumers.

Syngas is a key intermediate for producing ammonia, methanol, hydrogen, and synthetic fuels, with applications across chemicals, power, refining, and transportation. Market growth is driven by net-zero targets, energy diversification, rising fertilizer demand, and expanding clean hydrogen investments.

Market Dynamics

To evaluate market opportunities, Request Sample

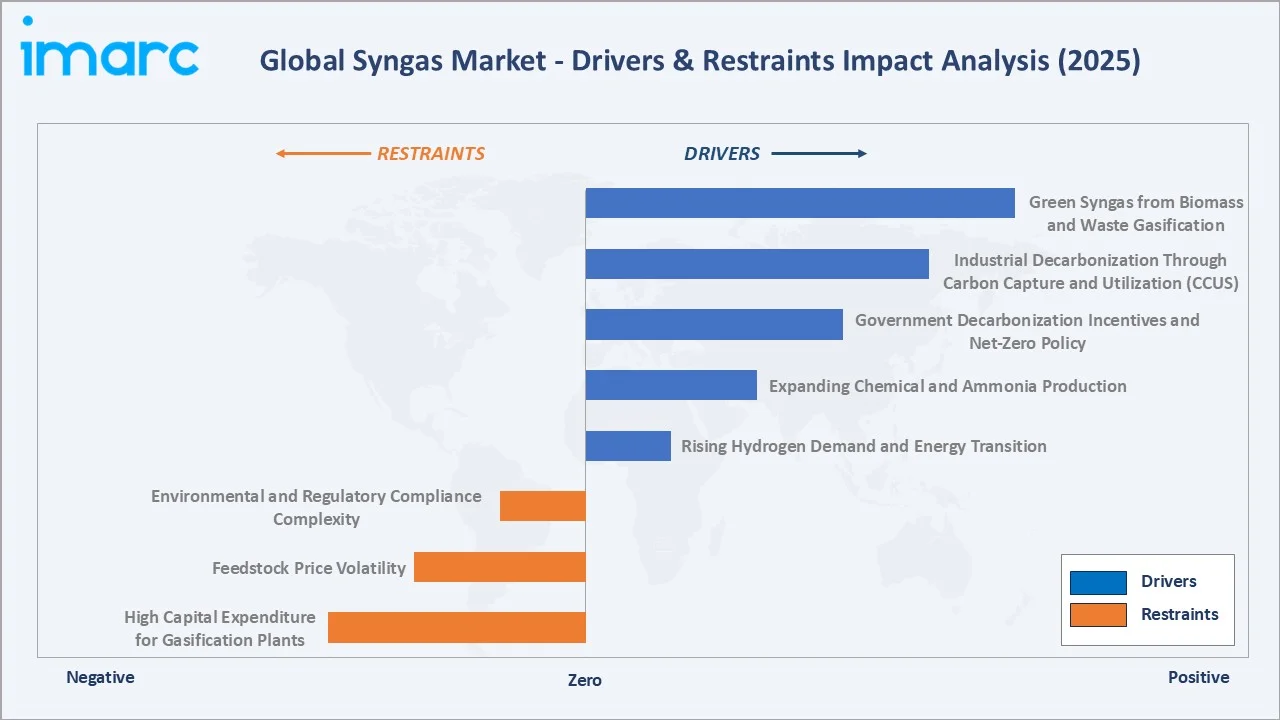

Market Drivers

- Rising Hydrogen Demand and Energy Transition: Rising hydrogen demand is driving syngas growth, as over 90% of global hydrogen is produced via steam methane reforming and coal gasification. Increasing demand from steel, refining, and fuel cell applications is further supporting market expansion.

- Expanding Chemical and Ammonia Production: Ammonia, the largest downstream application of syngas, reached approximately 180 million tonnes globally in 2024. Rising food demand and agricultural expansion are sustaining fertilizer demand, supporting syngas market growth across Asia Pacific, North America, and the Middle East.

- Government Decarbonization Incentives and Net-Zero Policy: Policy support including the U.S. IRA hydrogen tax credit (up to USD 3/kg), the EU’s 10 million tonnes renewable hydrogen target by 2030, and China’s 14th Five-Year hydrogen strategy is accelerating global investment in hydrogen, syngas, and gasification infrastructure.

- Industrial Decarbonization Through Carbon Capture and Utilization (CCUS): Integrating CCUS with syngas production enables low-carbon blue hydrogen, as CO₂ can be efficiently captured from concentrated syngas streams, driving increased industrial investment in pre-combustion carbon capture.

Market Restraints

- High Capital Expenditure for Gasification Plants: Large-scale gasification plants typically require investments ranging from several hundred million to multi-billion dollars, creating high entry barriers and longer project timelines, particularly in emerging markets.

- Feedstock Price Volatility: Syngas production economics are closely tied to coal and natural gas prices. During the 2021–2022 European energy crisis, TTF gas prices surged above €300/MWh , significantly increasing feedstock costs and compressing margins for SMR-based syngas and hydrogen producers across Europe.

- Environmental and Regulatory Compliance Complexity: Stricter emission limits for SO₂, NOx, and particulates require gasification plants to invest in gas cleaning and flue-gas treatment systems. Additionally, EU ETS carbon prices averaging around €65 per tonne CO₂ in 2025 have increased operating costs for conventional syngas producers.

Market Opportunities

- Green Syngas from Biomass and Waste Gasification: Rising investment in biomass and municipal solid waste gasification is creating new syngas opportunities, as these feedstocks enable low-carbon or carbon-negative syngas production. The global biomass gasification market is projected to grow steadily through 2030, supporting syngas market diversification.

- Blue and Green Hydrogen Infrastructure Development: Saudi Arabia’s NEOM green hydrogen project, backed by Air Products, targets approximately 600 tonnes of green hydrogen per day, making it one of the world’s largest hydrogen supply chains. Similar large-scale projects in Australia, Chile, and Europe are supporting long-term syngas and hydrogen market expansion.

- Power-to-X and Synthetic Fuels: Growing interest in sustainable aviation fuel and e-methanol is creating new syngas demand channels. The EU ReFuelEU Aviation regulation mandates SAF blending to reach 6% by 2030, while syngas-based Fischer-Tropsch and methanol-to-jet pathways are emerging as key low-carbon aviation fuel production routes.

Market Challenges

- Technology Maturity Gap for Green Syngas: Electrolysis-based green hydrogen and biomass gasification remain costlier than conventional coal and natural gas syngas routes, requiring sustained R&D and scale-up to achieve cost parity, creating a multi-year commercialization challenge.

- Water Availability for Gasification Operations: Large-scale gasification plants are water-intensive, and water scarcity in key coal-producing regions such as India, Inner Mongolia (China), and South Africa is limiting capacity expansion.

- Supply Chain Risk for Gasifier Equipment: Specialized gasifier components rely on a limited supplier base, and geopolitical disruptions, port congestion, and rising steel prices are extending lead times and increasing project costs.

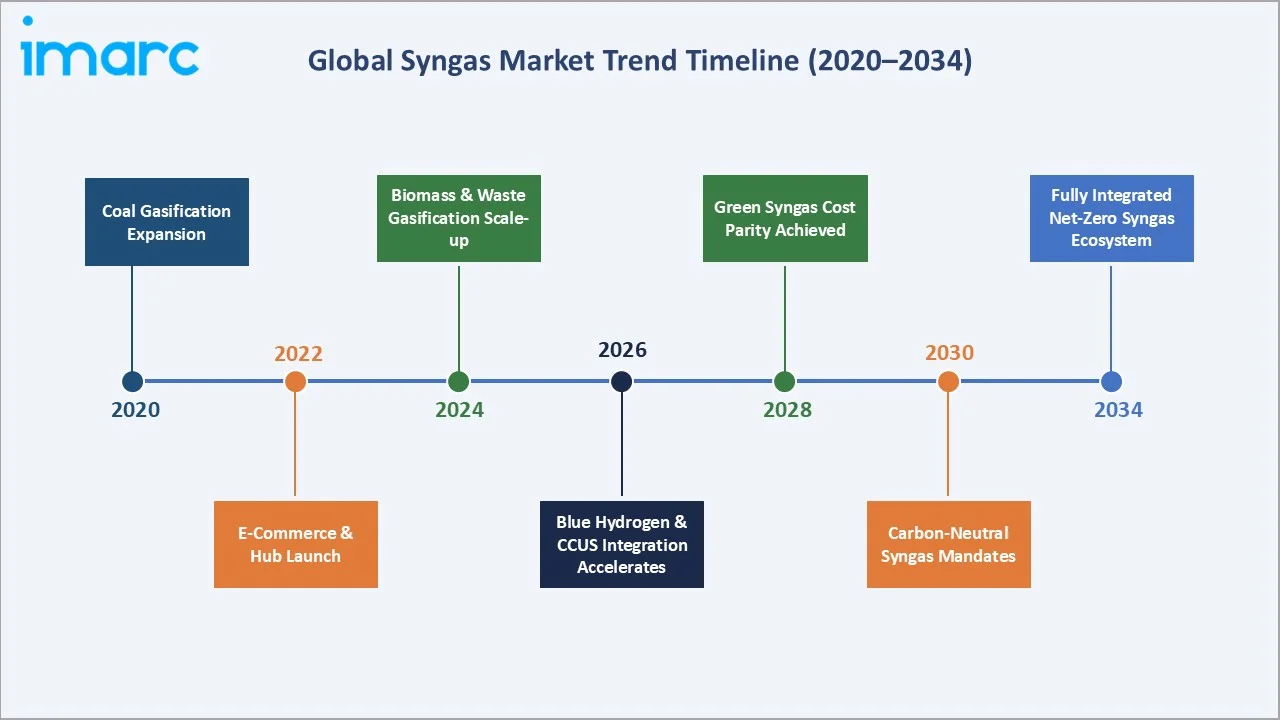

Emerging Market Trends

1. Scale-up of Coal-to-Chemicals in Asia

China’s coal-to-chemicals sector expanded between 2020 and 2023, with new gasification projects concentrated in Xinjiang, Inner Mongolia, and Shaanxi to strengthen domestic feedstock security. China produced over 80 million tonnes of methanol in 2023, with more than 70% coal-based, while around 85% of ammonia production relies on coal-derived syngas.

2. Hydrogen-from-Syngas Infrastructure Scale-up

Steam methane reforming with carbon capture remains a leading low-carbon hydrogen pathway, with numerous large-scale CCUS-enabled projects under development globally. This positions syngas-based infrastructure as a key foundation for the low-carbon hydrogen economy through 2030.

3. Biomass and Waste-to-Syngas Commercialization

Advanced gasification of agricultural residues, forestry waste, and municipal solid waste is gaining traction across Europe, North America, and Japan. Companies such as Enerkem and Sierra Energy are scaling waste-to-syngas facilities that convert non-recyclable waste into methanol, hydrogen, and low-carbon fuels, offering significantly lower lifecycle emissions compared to fossil-based production.

4. CCUS Integration in Blue Hydrogen Production

Pre-combustion carbon capture integrated with syngas-based hydrogen production is advancing, with projects such as Air Products’ Edmonton Net-Zero Hydrogen Complex and Shell’s Quest CCS facility demonstrating commercial blue hydrogen deployment. Syngas-based systems can achieve over 90% carbon capture efficiency, supporting low-carbon hydrogen scale-up..

5. Power-to-X and Synthetic Fuel Applications

Syngas is increasingly used in Power-to-X processes, where renewable hydrogen combined with captured CO₂ produces e-methanol, e-ammonia, and synthetic aviation fuels. EU SAF mandates and shipping decarbonization targets are expected to significantly increase synthetic fuel demand through 2030, supporting syngas market growth .

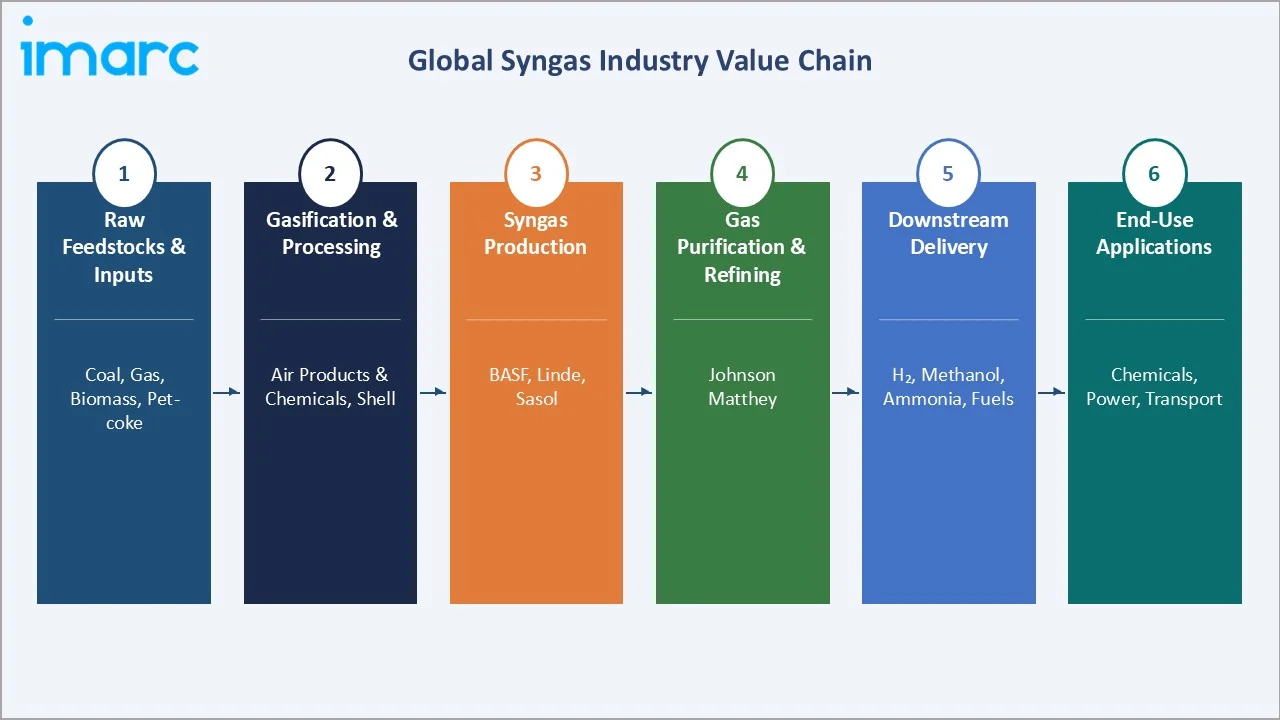

Industry Value Chain Analysis

|

Stage |

Key Players / Description |

|

Feedstock Sourcing |

Mining companies (Glencore, CONSOL Energy), gas producers (ExxonMobil, Shell), biomass aggregators |

|

Gasification Technology |

Air Products & Chemicals, Air Liquide, Siemens Energy, Shell |

|

Syngas Production & Refining |

BASF SE, Linde plc, Chiyoda Corporation, AHT Syngas Technology, Sasol |

|

Gas Purification & Conditioning |

Johnson Matthey, Clariant AG |

|

Downstream Processing (H₂, MeOH, NH₃) |

Yara International, Mitsubishi Heavy Industries, ThyssenKrupp |

|

End-Use Applications |

Chemical plants, power utilities, fuel refiners, industrial manufacturers |

The syngas value chain spans five interconnected stages, from upstream feedstock sourcing through to end-use application delivery. Each stage involves specialized technology, infrastructure, and industry players that together determine the cost-competitiveness and carbon intensity of syngas produced.

Technology Landscape in the Syngas Industry

The syngas technology landscape is defined by four primary production routes, each with distinct feedstock compatibility, efficiency profiles, and carbon intensity characteristics. Technology selection has material implications for capital cost, operating flexibility, and decarbonization potential.

Steam methane reforming remains the dominant syngas production route due to high efficiency and cost competitiveness. Partial oxidation is widely used for refinery hydrogen production, while auto-thermal reforming combines SMR and POX for large-scale blue and green hydrogen. Emerging SOEC-based technologies, including Topsoe’s e-fuel pathways, are targeting commercial deployment later this decade.

Combined reforming integrates pre-reforming with primary reforming to improve feedstock flexibility and energy efficiency. Advanced gasification technologies such as entrained-flow and fluidized bed systems handle coal, pet-coke, and biomass with conversion efficiencies above 75%.Digital monitoring, AI-driven optimization, and advanced safety systems are further improving plant performance and reliability.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Gasifier Type | Fixed Bed | 40% | 2025 |

| Feedstock | Coal | 32% | 2025 |

| Technology | Steam Reforming | 25% | 2025 |

| End-Use | Chemicals | 30% | 2025 |

| Region | Asia Pacific | 33% | 2025 |

By End-Use

The Chemicals segment commands the largest end-use share at 30% in 2025, driven by syngas’ essential role in producing ammonia (for fertilizers), methanol, hydrogen, and dimethyl ether. Global fertilizer demand remains structurally elevated, with food security concerns sustaining ammonia output growth across Asia Pacific and the Middle East.

To access detailed market analysis, Request Sample

Power Generation holds 26% share in 2025, driven by IGCC deployments in Japan, the U.S., and South Korea. Liquid Fuels account for 24%, led by Fischer-Tropsch and GTL capacity in South Africa and Qatar, while Gaseous Fuels hold 20%, growing as hydrogen blending in gas grids gains approval across the EU and UK.

The Chemicals segment is forecast to maintain dominance through 2034, with green ammonia and green methanol production from biomass-derived syngas representing the fastest-growing sub-segment at an estimated CAGR exceeding 11% during 2026-2034.

By Gasifier Type

Fixed Bed gasifiers hold the largest 40% share in 2025, driven by simple design, lower costs, and strong performance with coal and biomass. Entrained Flow gasifiers account for 35%, favored for large-scale coal-to-chemicals plants in China and petrochemical complexes in the Middle East due to high throughput and feedstock flexibility.

Fluidized Bed gasifiers hold 25% share in 2025and are the fastest-growing segment, driven by their ability to process diverse feedstocks such as biomass and low-rank coal. This flexibility supports growing waste-to-syngas and distributed energy projects in Europe and North America.

The shift toward Fluidized Bed technology reflects the industry's move toward feedstock flexibility and lower-carbon syngas production, aligned with net-zero decarbonization goals across key market.

Regional Market Insights

|

Region |

Share (2025) |

Growth Drivers |

Regulatory Impact |

Major Companies |

|

Asia Pacific |

33% |

Rapid industrialization, large chemical capacity, energy security policy, China & India dominance |

IEA Net-Zero mandates, China NEV policy, India PLI scheme |

Air Products, Linde (Asia), CNPC, Sinopec |

|

North America |

25% |

Mature chemical & refining sector, H₂ hub investments, growing clean energy adoption |

U.S. DOE Hydrogen Strategy, IRA clean hydrogen incentives |

Air Products, Linde plc, Air Liquide (US ops) |

|

Europe |

22% |

Decarbonization mandates, green hydrogen scale-up, industrial emission reduction targets |

EU Green Deal, REPowerEU, ETS carbon pricing |

Air Liquide (EU), Siemens Energy, Linde Plc |

|

Middle East & Africa |

12% |

Oil & gas integration, diversification programs (Vision 2030), petrochemical expansion |

Saudi Vision 2030, NEOM green hydrogen project |

Saudi Aramco, SABIC, Air Products (NEOM) |

|

Latin America |

8% |

Expanding refining sector, Brazil biofuels synergy, growing industrial base |

Brazil RenovaBio, national energy transition policies |

Petrobras, Air Liquide (LATAM), Chiyoda |

Asia Pacific leads the global syngas market with a 33% share in 2025, driven by China’s coal chemicals, India’s fertilizer demand, and Southeast Asia’s expanding chemical sector. Policies such as China’s coal chemical strategy and India’s National Hydrogen Mission are supporting continued gasification capacity expansion through 2034.

North America holds 25% share, supported by hydrogen hub investments and IRA incentives. Europe accounts for 22%, driven by green syngas and decarbonization policies. The Middle East & Africa hold 12% with oil and gas integration, while Latin America holds 8%, supported by Brazil’s bioenergy-syngas expansion.

Competitive Landscape

|

Company |

Brand Name |

Market Position |

Focus Area |

|

Air Products and Chemicals, Inc. |

Air Products |

Leader |

Gasification technology, H₂ infrastructure, net-zero energy |

|

Linde plc |

Linde |

Leader |

Industrial gases, syngas supply, CCUS integration |

|

L'Air Liquide S.A |

Air Liquide |

Leader |

Hydrogen solutions, syngas, industrial gas supply |

|

BASF SE |

BASF |

Challenger |

Chemicals, syngas catalysis, methanol & ammonia |

|

Shell Global Solutions International B.V. |

Shell |

Challenger |

Shell gasification, GTL (gas-to-liquids) technology |

|

Siemens Energy AG |

Siemens Energy |

Challenger |

Gasification equipment, electrolysis, clean energy |

|

Chiyoda Corporation |

Chiyoda |

Emerging |

SPERA hydrogen, natural gas reforming technology |

|

A.H.T. Syngas Technology N.V. |

AHT Syngas |

Emerging |

Fixed bed gasification, biomass waste-to-syngas |

The global syngas market is led by a concentrated group of industrial gas majors and specialized technology providers. Air Products and Chemicals, Inc. reported revenues of approximately USD 12.1 billion in FY2024 , supported by large-scale hydrogen supply contracts and gasification project development. Meanwhile, Linde plc generated approximately USD 33.0 billion in FY2024, maintaining leadership in industrial gases, hydrogen production, and global syngas infrastructure.

Key Company Profiles

Air Products and Chemicals, Inc.

Air Products and Chemicals, Inc., headquartered in Allentown, Pennsylvania, U.S., is one of the world's leading industrial gas and hydrogen suppliers with strong capabilities in syngas production, gasification, and clean hydrogen infrastructure. Air Products reported FY2024 revenue of approximately USD 12.7 billion , supported by growth in hydrogen, gasification, and clean energy projects across the Middle East, North America, and Asia.

Product & Service Portfolio: Syngas/gasification solutions, hydrogen supply, industrial gases (oxygen, nitrogen, hydrogen), air separation technologies, and on-site gas generation infrastructure.

Recent Developments: Air Products, alongside ACWA Power and NEOM, is developing the USD 8.4 billion NEOM Green Hydrogen Project in Saudi Arabia. The facility is expected to produce up to 600 tonnes per day of green hydrogen, converted into around 1.2 million tonnes of green ammonia annually for global export. As of 2025, the project has reached around 80% construction completion, with commercial operations targeted between 2026–2027.

Strategic Focus: Air Products focuses on large-scale green and blue hydrogen, gasification, and clean ammonia projects to support low-carbon energy markets. The company is also expanding its syngas and hydrogen operations across the Middle East and Asia through strategic investments.

L'Air Liquide S.A.

Air Liquide, headquartered in Paris, France, is one of the world's largest industrial gas companies, reporting EUR 27.06 billion in revenue in FY2024 . The company operates in 70+ countries and provides hydrogen, syngas, and industrial gas infrastructure supporting refining, chemicals, and clean energy markets.

Product & Service Portfolio: Industrial gases, syngas and hydrogen production (SMR, ATR, electrolysis), carbon capture solutions, cryogenic air separation units, hydrogen liquefaction, and gas pipeline and distribution infrastructure.

Recent Developments: In May 2022, Air Liquide commissioned a large-scale liquid hydrogen facility in North Las Vegas, Nevada, with a 30 tonnes/day production capacity to support mobility and industrial demand in California and western U.S. markets. The plant is powered by renewable energy and strengthens Air Liquide’s hydrogen and syngas-derived fuel infrastructure.

Strategic Focus: Air Liquide focuses on clean hydrogen production, syngas infrastructure, hydrogen mobility, and low-carbon industrial solutions, with expansion across Europe, North America, and Asia-Pacific.

Linde plc

Linde plc is the world’s largest industrial gases and engineering company, headquartered in Woking, United Kingdom (legal domicile: Dublin, Ireland). The company reported approximately USD 33.0 billion in revenue in FY2024 and operates across more than 100 countries with extensive hydrogen, syngas, and industrial gas infrastructure. Linde has delivered over 4,000 air separation and hydrogen/syngas plants globally , supporting industries such as refining, chemicals, and energy.

Product & Service Portfolio: Industrial gases (oxygen, nitrogen, hydrogen), syngas and hydrogen production plants (SMR, ATR, electrolysis), air separation units (ASUs), HyCO/syngas plants, carbon capture solutions, hydrogen liquefaction and storage, and pipeline gas distribution infrastructure.

Recent Developments: In 2024, Linde announced a USD 2 billion investment to supply clean hydrogen and syngas-derived hydrogen to Dow’s Path2Zero project in Alberta, Canada, supporting low-carbon chemical production. The facility will use autothermal reforming and carbon capture technologies to produce low-carbon hydrogen. In 2025, Linde signed a long-term agreement to build a world-scale air separation unit for a low-carbon ammonia facility in Louisiana, supporting hydrogen and syngas-based production. Linde will invest over USD 400 million in the project.

Strategic Focus: Linde focuses on large-scale hydrogen and syngas infrastructure, low-carbon hydrogen production, and carbon capture solutions to support industrial decarbonization. The company is expanding clean energy and hydrogen projects across North America, Europe, and Asia to accelerate the energy transition.

Market Concentration Analysis

The global syngas market is moderately concentrated, with leading players including Air Products, Linde, Air Liquide, Shell, and Siemens Energy accounting for around 35–40% of technology licensing and large-scale plant revenues in 2025. This concentration is driven by high capital requirements, proprietary technologies, and long-term project partnerships that Favor established companies.

Market fragmentation is higher at regional and application levels, especially in biomass gasification, distributed production, and emerging markets. As a result, the market is concentrated in technology but fragmented in plant operations and feedstock sourcing, with independent producers and regional manufacturers holding a significant volume share.

Consolidation is increasing in clean hydrogen and biomass gasification, with major industrial gas companies acquiring startups and forming partnerships to build integrated clean syngas value chains. Examples include Air Liquide’s partnership with Enerkem and Air Products’ investment in the ACWA Power NEOM project, positioning them for green hydrogen expansion through 2030–2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Fluidized Bed gasification is the fastest-growing segment, driven by its suitability for biomass and waste feedstocks used in low-carbon syngas production across Europe and North America. Meanwhile, power generation is witnessing strong growth, supported by IGCC plant development and hydrogen co-firing in combined cycle power systems.

Emerging Market Expansion

India is a major emerging opportunity for syngas investment, supported by the National Hydrogen Mission targeting 5 million tonnes of green hydrogen by 2030 . Additionally, India consumes approximately 17-19 million tonnes of ammonia annually, with more than 50% of its hydrogen requirement used in fertilizer production , largely derived from syngas, creating strong demand for both conventional and green syngas production.

Saudi Arabia’s Vision 2030 and the NEOM green hydrogen project represent major investments in syngas and hydrogen infrastructure. With 4 GW electrolyzer capacity, NEOM is expected to produce green hydrogen and ammonia at scale for global export markets.

Venture & Strategic Investment Trends

Investment in gasification, green syngas, and hydrogen infrastructure is accelerating globally, led by blue and green hydrogen projects. Meanwhile, carbon capture providers such as Baker Hughes, Fluor, and Mitsubishi Heavy Industries are attracting strategic investments for CCUS integration with syngas and hydrogen facilities.

Future Market Outlook (2026-2034)

The global syngas market forecast projects sustained volume expansion from 282.37 MM Nm³/h in 2025 to 563.85 MM Nm³/h by 2034 at a CAGR of 7.99% – representing a near-doubling of production capacity over the nine-year forecast period. Growth will be driven by hydrogen demand expansion, emerging market industrialization, biomass gasification commercialization, and progressive integration of CCUS across conventional syngas facilities.

Three key forces will reshape the syngas market through 2034: the shift toward green syngas as renewable costs decline, digitalization of gasification operations to improve efficiency and reliability, and growing synthetic fuel mandates in aviation and shipping, driving long-term demand for Fischer-Tropsch fuels and methanol from syngas.

By 2034, syngas is expected to evolve from a primarily fossil-fuel-derived industrial intermediate into a diversified platform for clean energy production, supported by policy frameworks, technology cost reductions, and growing corporate net-zero commitments across major chemical, power, and industrial end-use sectors.

Research Methodology

Primary Research

Primary research included structured interviews and surveys (2024–2025) with key syngas stakeholders, including project developers, industrial gas companies, chemical producers, energy policy experts, and hydrogen sector investment analysts.

Secondary Research

Secondary sources included company reports (Air Products, Air Liquide, Linde, BASF, Shell), industry associations, government energy data, regulatory publications, and trade media such as Hydrocarbon Processing, Gasification Technologies Council, and Chemical Engineering Progress.

Forecasting Models

Market estimates were developed using combined top-down and bottom-up approaches, incorporating plant-level capacity, feedstock demand, and end-use consumption alongside macroeconomic factors such as GDP, industrial output, energy prices, and hydrogen demand. Scenario analysis across base, optimistic, and conservative assumptions was used to define growth projections.

Syngas Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | MM Nm3/h |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Gasifier Types Covered | Fixed Bed, Fluidized Bed, Entrained Flow |

| Feedstocks Covered | Coal, Natural Gas, Petroleum, Pet-Coke, Biomass and Waste |

| Technologies Covered | Steam Reforming, Partial Oxidation, Combined or Two-Step Reforming, Auto Thermal Reforming, Others |

| End Uses Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Air Products and Chemicals, Inc., Linde plc, L'Air Liquide S.A, BASF SE, Shell Global Solutions International B.V., Siemens Energy AG, Chiyoda Corporation, A.H.T. Syngas Technology N.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the syngas market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global syngas market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the syngas industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Syngas Market Report

The global syngas market reached 282.37 MM Nm³/h in 2025, driven by rising hydrogen demand, expanding chemical manufacturing, and growing gasification investments across Asia Pacific, North America, and Europe.

The market is projected to reach 563.85 MM Nm³/h by 2034, growing at a CAGR of 7.99% during 2026-2034, driven by hydrogen scale-up, biomass gasification commercialization, and industrial decarbonization programs globally.

Chemicals lead the syngas market with a 30% share in 2025, driven by syngas’ essential role as a feedstock for ammonia, methanol, hydrogen, and specialty chemical production across global industrial facilities.

Fixed Bed gasifiers command a 40% share in 2025 due to their cost-effectiveness and proven performance with coal and biomass feedstocks, particularly across developing markets in South and Southeast Asia.

Asia Pacific leads with a 33% share in 2025, anchored by China’s coal-to-chemicals industry, India’s fertilizer and hydrogen programs, and government policies promoting gasification and energy security across the region.

Key drivers include rising hydrogen demand, expanding ammonia and methanol production, government net-zero incentives, CCUS integration with blue hydrogen, and biomass waste gasification commercialization across major industrial economies.

Asia Pacific is also the fastest-growing region, driven by India’s National Hydrogen Mission, China’s coal chemical expansion, and ASEAN industrial growth creating sustained new gasification capacity demand through 2034.

Leading companies include Air Products and Chemicals, Inc., Linde plc, L'Air Liquide S.A., BASF SE, Shell Global Solutions International B.V., Siemens Energy AG, Chiyoda Corporation, and A.H.T. Syngas Technology N.V.

Power Generation holds a 26% end-use share in 2025, driven by IGCC power plant deployments in Japan, the U.S., and South Korea, where syngas enables cleaner electricity generation than direct coal combustion.

Fluidized Bed gasifiers hold a 25% share in 2025 and represent the fastest-growing gasifier type at ~9.2% CAGR through 2034, driven by waste and biomass feedstock compatibility and smaller distributed energy applications.

AI-driven gasification optimization, advanced CCUS integration, electrolysis-based green syngas, and biomass gasification are improving carbon intensity, plant efficiency, and enabling low-carbon syngas production at competitive economics.

Syngas-based technologies such as SMR and coal gasification currently dominate global hydrogen production and are expected to serve as a bridge between fossil-based and emerging green hydrogen supply chains through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)