Taiwan Data Center Market Size, Share, Trends and Forecast by Component, Type, Enterprise Size, End User, and Region, 2026-2034

Taiwan Data Center Market Size, Share, Trends & Forecast (2026-2034)

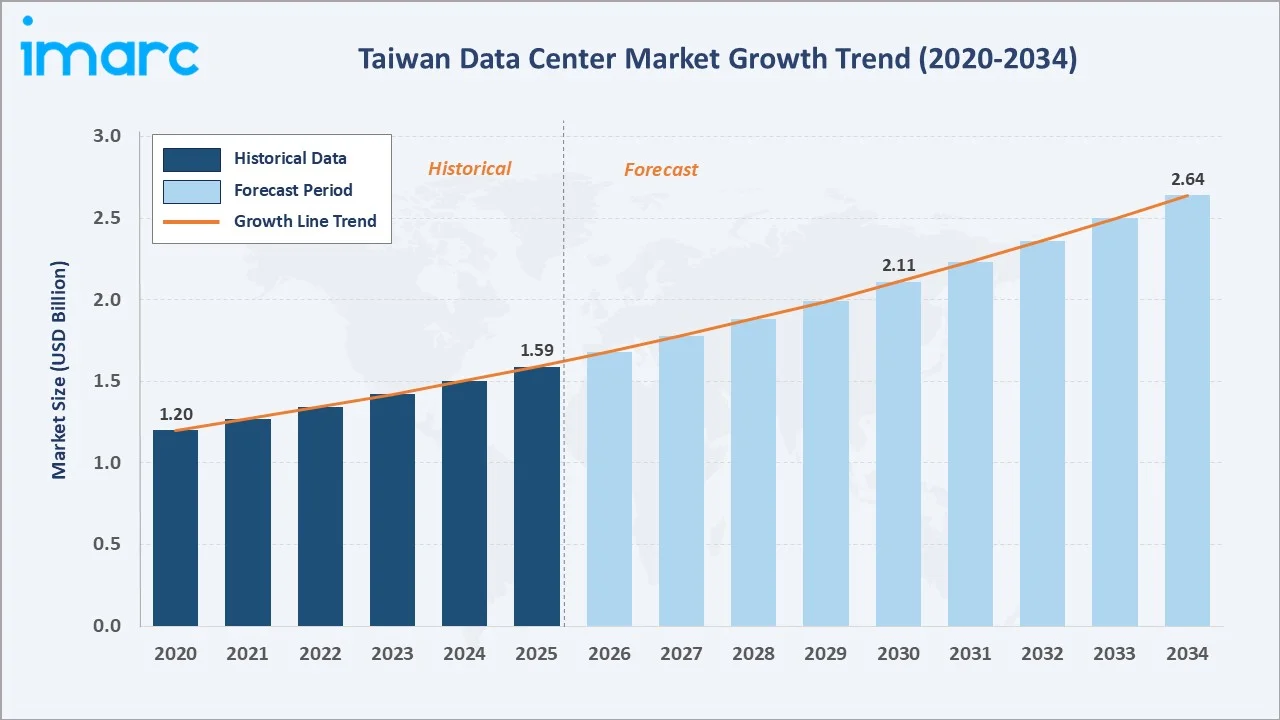

The Taiwan data center market size reached USD 1.59 Billion in 2025 and is projected to reach USD 2.64 Billion by 2034, exhibiting a CAGR of 5.76% during 2026-2034. Rising cloud adoption, government-led digital transformation, semiconductor ecosystem synergies, and global hyperscaler investments are the primary forces driving market growth.

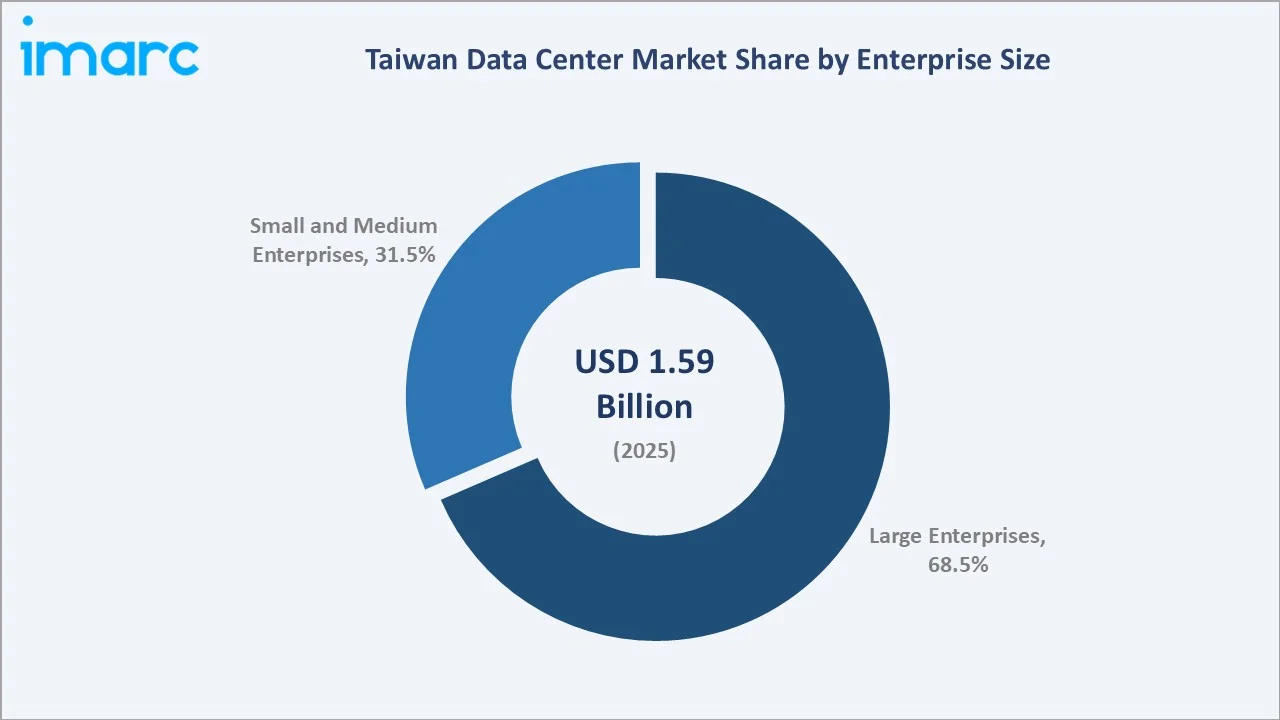

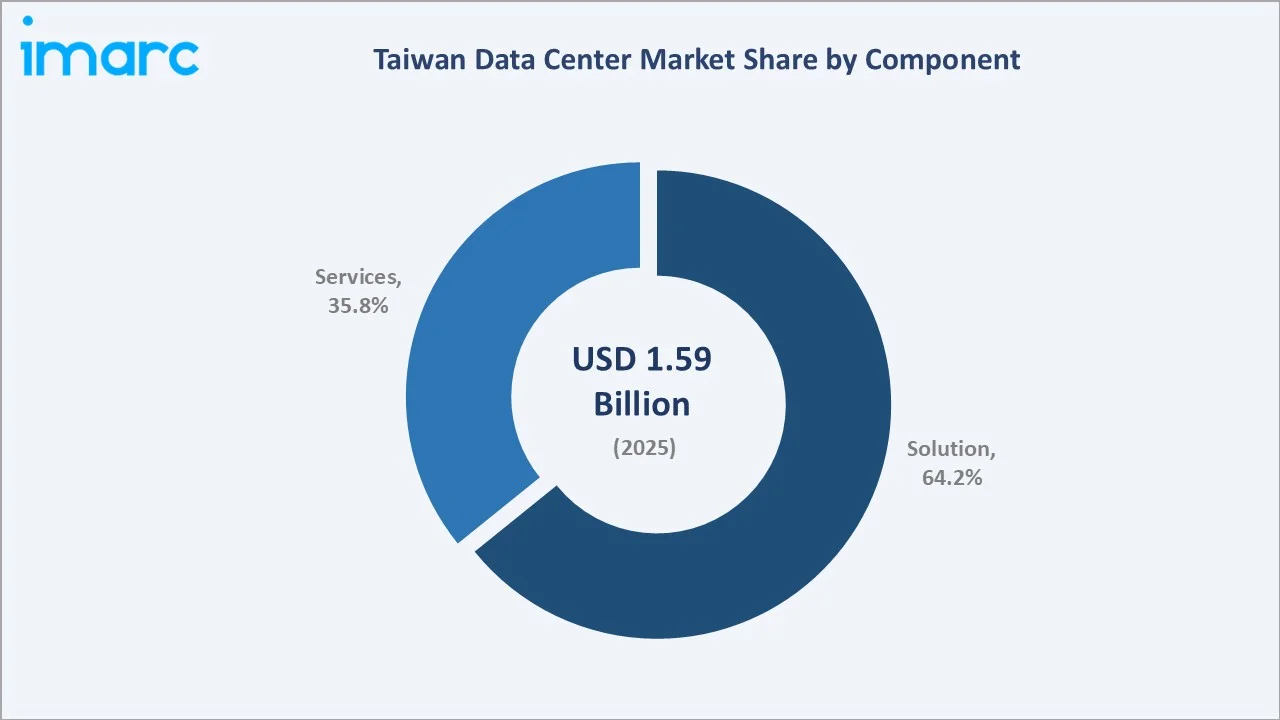

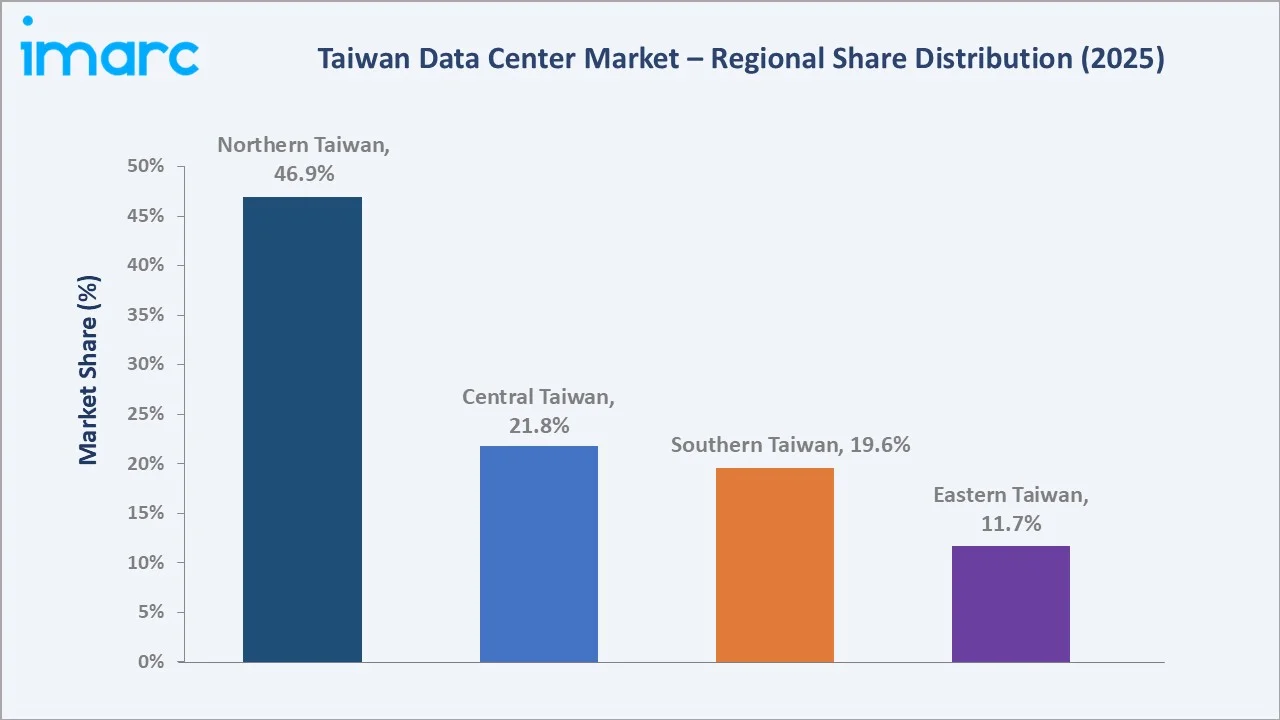

Large enterprises dominate enterprise size at 68.5% in 2025. Solution leads the component segment at 64.2%. Northern Taiwan commands a dominant 46.9% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.59 Billion |

|

Forecast Market Size (2034) |

USD 2.64 Billion |

|

CAGR (2026-2034) |

5.76% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Northern Taiwan (46.9% share, 2025) |

|

Second Largest Region |

Central Taiwan (21.8% share, 2025) |

|

Leading Enterprise Size |

Large Enterprises (68.5%, 2025) |

|

Leading Component |

Solution (64.2%, 2025) |

The Taiwan data center market growth trajectory from 2020 through 2034, with historical expansion to USD 1.59 Billion in 2025, reflects consistent cloud-driven demand. The forecast to USD 2.64 Billion captures accelerating AI computing, digital transformation, and hyperscaler-led investment.

To get more information on this market, Request Sample

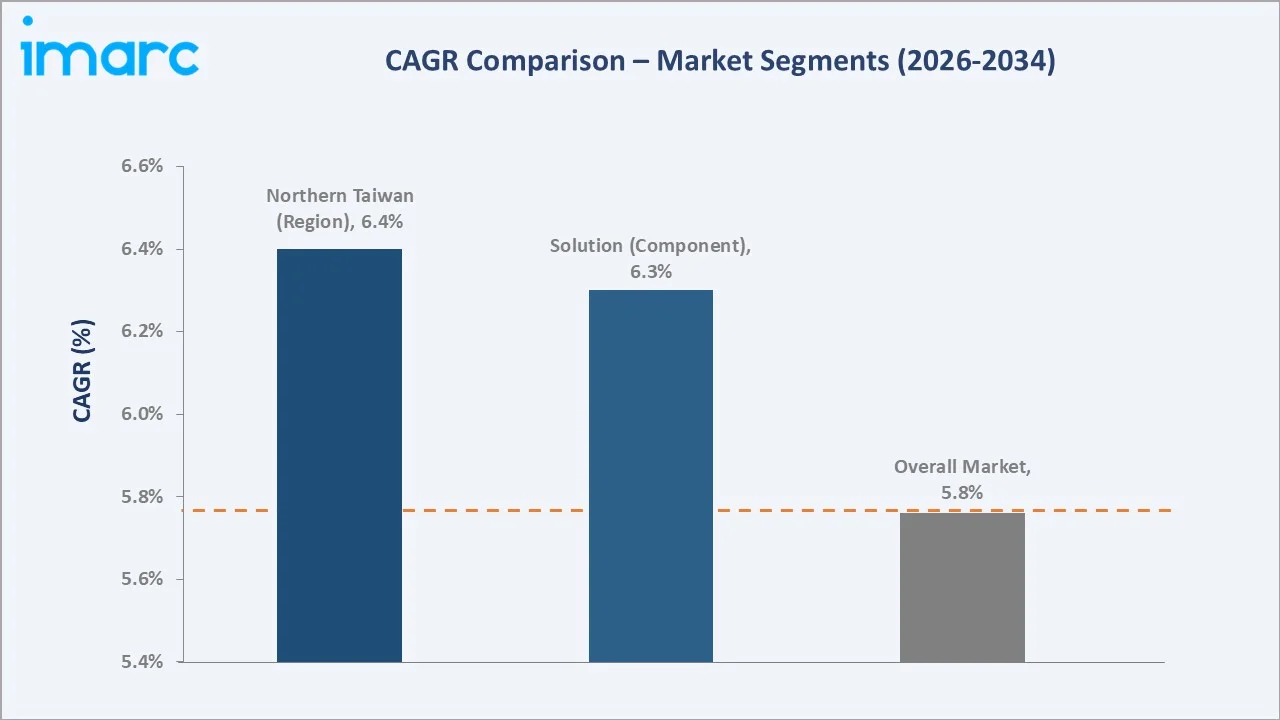

CAGR trajectories across enterprise size and component sub-segments, with Solution at ~6.3% CAGR and Northern Taiwan at ~6.4% CAGR, represent the fastest-growing categories within the Taiwan data center industry through 2034.

Executive Summary

The Taiwan data center market is on a sustained growth trajectory from USD 1.59 Billion in 2025 to USD 2.64 Billion by 2034. Data centers are critical infrastructure enabling cloud computing, AI workloads, financial transaction processing, government digitalization, and telecommunications services for Taiwan’s technology-driven economy.

Large enterprises dominate enterprise size at 68.5% in 2025, reflecting their higher infrastructure requirements and IT budgets. Small and Medium Enterprises at 31.5% are growing through adoption of colocation and cloud-based data center services.

The Solution segment leads components at 64.2%, driven by software-defined infrastructure and cloud management platforms.

Northern Taiwan commands 46.9% of the 2025 market, reflecting Taipei’s concentration of technology companies and financial institutions. Central Taiwan (21.8%) and Southern Taiwan (19.6%) are gaining traction due to government-backed digital cluster development and lower land costs attracting greenfield data center investment.

Key Market Insights

|

Insight |

Data |

|

Largest Enterprise Size |

Large Enterprises – 68.5% share (2025) |

|

Leading Component |

Solution – 64.2% share (2025) |

|

Leading Region |

Northern Taiwan – 46.9% share (2025) |

|

Second Largest Region |

Central Taiwan – 21.8% share (2025) |

|

Top Companies |

Amazon Web Services, Inc., Microsoft, Chunghwa Telecom Co., Ltd. |

Key Analytical Observations Expanding on the Above Data:

- Large enterprises at 68.5% in 2025 dominate due to high-volume data processing needs, regulatory compliance requirements, and dedicated infrastructure budgets across BFSI, IT, and government sectors.

- Solution’s 64.2% share in 2025 reflects enterprise adoption of integrated software platforms, hyperconverged infrastructure, security solutions, and AI-enabled data center management systems.

- Northern Taiwan’s 46.9% dominance reflects Taipei’s role as Taiwan’s primary technology and financial hub, with dense interconnection density and proximity to submarine cable landing stations.

- Central Taiwan benefits from the semiconductor manufacturing ecosystem in the Hsinchu Science Park, creating adjacent data center demand from chip design and R&D-intensive tenants.

Taiwan Data Center Market Overview

Taiwan’s data center market encompasses colocation, hyperscale, edge, and enterprise-owned facilities providing IT infrastructure services across compute, storage, networking, and managed services. The island’s strategic position as a semiconductor manufacturing hub creates unique synergies with data center demand from chip design, AI training, and advanced manufacturing applications.

The ecosystem integrates global hyperscalers, colocation operators, domestic telecom carriers, IT system integrators, and end-user industries spanning BFSI, IT and telecom, government, energy and utilities, and manufacturing. Taiwan’s robust 100 Gbps fiber backbone and submarine cable connectivity reinforces its attractiveness as an Asia-Pacific data center destination.

Market Dynamics

To evaluate market opportunities, Request Sample

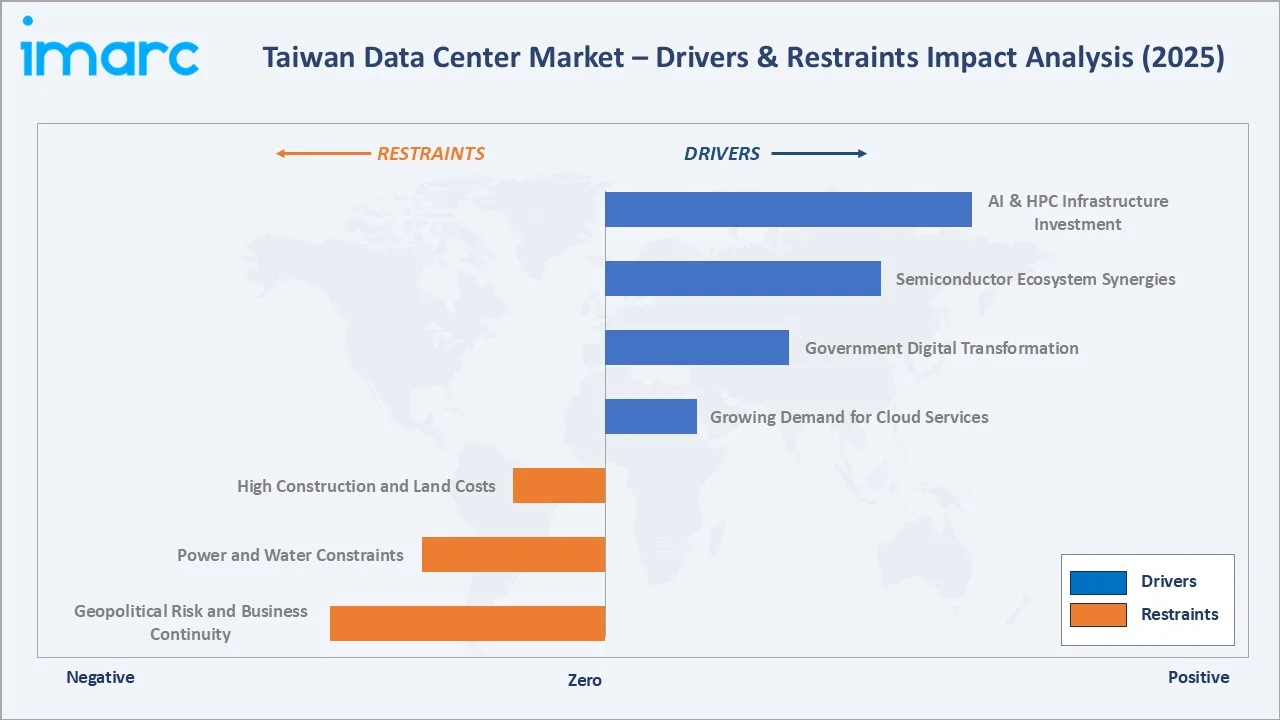

Market Drivers

- Growing Demand for Cloud Services: AWS announced plans to invest billions over 15 years in Taiwan infrastructure by 2025, meeting surging cloud demand from BFSI, healthcare, and e-commerce sectors requiring scalable, secure cloud solutions.

- Government Digital Transformation: Taiwan’s AI Center of Excellence (AICoE), leveraging the Taiwania 2 supercomputer, accelerates AI workloads and national digital initiatives, creating direct data center capacity demand from public sector.

- Semiconductor Ecosystem Synergies: Advanced node fab investments generate intensive data processing requirements for chip design simulation, quality control, and supply chain systems requiring low-latency, high-availability data center infrastructure.

Market Restraints

- High Construction and Land Costs: Data center construction in Taipei commands significant premiums versus regional markets, constraining greenfield development capacity in the primary demand zone and extending payback periods for new builds.

- Power and Water Constraints: Taiwan’s electricity grid, under strain from industrial demand growth, creates challenges for PUE optimization and large-scale data center power procurement at competitive rates.

Market Opportunities

- Edge Computing Expansion: Taiwan’s 5G rollout and IoT adoption in smart manufacturing are creating distributed edge data center demand adjacent to factory and logistics cluster locations requiring ultra-low latency processing.

- Green Data Center Development: Corporate sustainability mandates and government carbon-neutral targets are creating demand for liquid-cooled, renewable-powered data center infrastructure eligible for preferential financing and tax incentives.

Market Challenges

- Geopolitical Risk and Business Continuity: Cross-strait geopolitical tensions create business continuity concerns for international enterprises establishing primary data centers in Taiwan, influencing multi-site disaster recovery architecture decisions.

- Skilled Workforce Shortage: Competition for data center operations specialists, network engineers, and cybersecurity professionals intensifies as hyperscaler expansion activity accelerates across Northern Taiwan’s data center cluster.

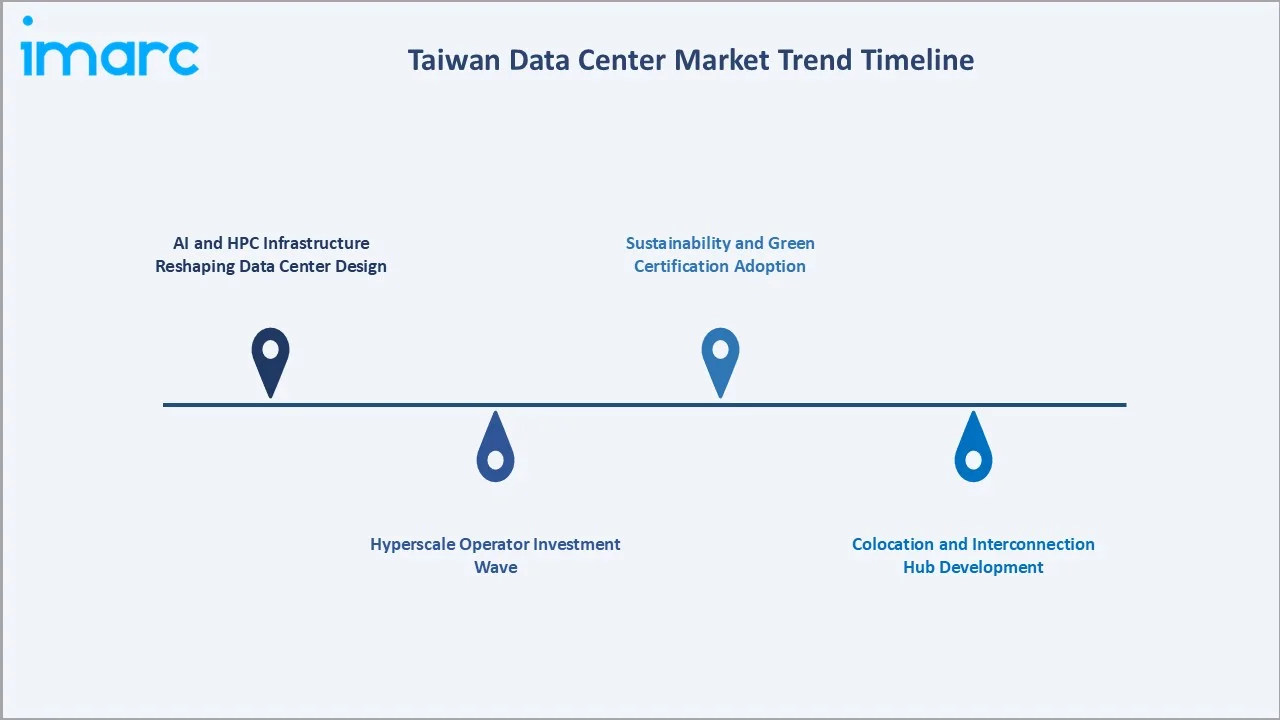

Emerging Market Trends

1. AI and HPC Infrastructure Reshaping Data Center Design

Taiwan’s position as the global epicenter of AI chip production is directly driving specialized AI-optimized data center construction. GPU-dense racks requiring liquid cooling and dedicated high-voltage power infrastructure represent a distinct architectural shift from legacy enterprise data center designs.

2. Hyperscale Operator Investment Wave

Global hyperscalers are committing multi-billion-dollar investments to Taiwan data center infrastructure through 2030, attracted by submarine cable access, semiconductor ecosystem proximity, and skilled technical talent availability across Northern Taiwan’s technology cluster.

3. Colocation and Interconnection Hub Development

Northern Taiwan is emerging as a regional interconnection hub with carrier-neutral colocation facilities offering direct cross-connects to major submarine cable systems, attracting financial services, CDN providers, and international enterprise tenants seeking low-latency connectivity.

4. Sustainability and Green Certification Adoption

Leading operators are pursuing LEED Platinum, ISO 50001 energy management, and Taiwan Green Building certification, driven by multinational tenant sustainability requirements and alignment with Taiwan’s 2050 net-zero carbon policy commitment.

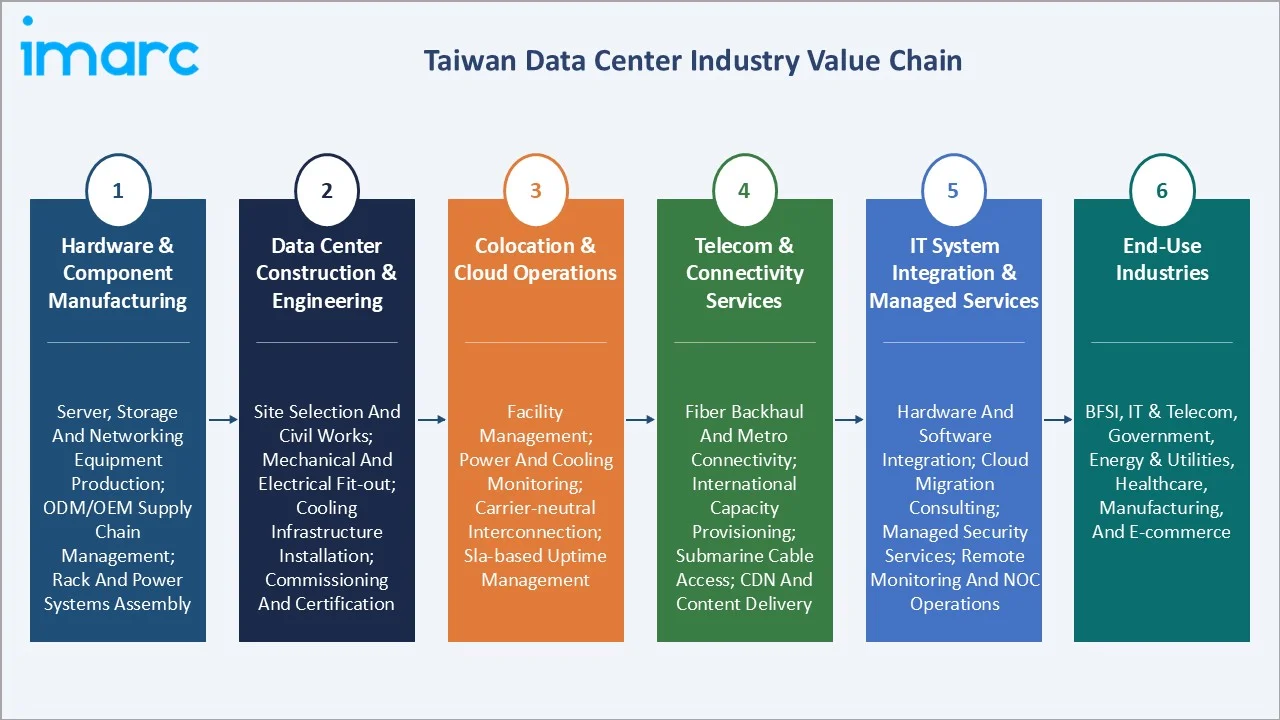

Industry Value Chain Analysis

The Taiwan data center value chain spans six stages from hardware manufacturing through end-user consumption. Operations and IT service delivery capture the highest recurring revenue margins, while construction and setup represent peak capital intensity periods requiring specialist project financing and engineering capabilities.

|

Stage |

Key Activities / Examples |

|

Hardware & Component Manufacturing |

Server, storage and networking equipment production; ODM/OEM supply chain management; rack and power systems assembly |

|

Data Center Construction & Engineering |

Site selection and civil works; mechanical and electrical fit-out; cooling infrastructure installation; commissioning and certification |

|

Colocation & Cloud Operations |

Facility management; power and cooling monitoring; carrier-neutral interconnection; SLA-based uptime management |

|

Telecom & Connectivity Services |

Fiber backhaul and metro connectivity; international capacity provisioning; submarine cable access; CDN and content delivery |

|

IT System Integration & Managed Services |

Hardware and software integration; cloud migration consulting; managed security services; remote monitoring and NOC operations |

|

End-Use Industries |

BFSI, IT & Telecom, Government, Energy & Utilities, Healthcare, Manufacturing, and e-Commerce |

Technology Landscape in the Taiwan Data Center Industry

Liquid Cooling and Thermal Management Innovation

Direct liquid cooling and immersion cooling adoption is accelerating in Taiwan’s AI-oriented data centers, where GPU rack densities of 30-100 kW per rack exceed conventional air-cooling capacity. Taiwan’s ODM manufacturers are integrating liquid cooling as standard in hyperscale rack designs for next-generation AI training infrastructure.

Software-Defined Infrastructure and AI-Driven Operations

Software-defined networking, hyperconverged infrastructure, and AI-driven infrastructure management platforms are enabling dynamic workload orchestration across Taiwan’s data center ecosystem, reducing operational headcount while improving resource utilization rates and predictive maintenance outcomes.

Renewable Energy Integration and Power Management

Corporate power purchase agreements for offshore wind and solar energy are being integrated into data center power procurement strategies, supporting ESG reporting requirements for multinational tenants and alignment with Taiwan’s 2050 net-zero carbon policy commitment.

Security and Sovereign Cloud Technology

Taiwan’s government is establishing sovereign cloud infrastructure with dedicated hardware security modules, confidential computing enclaves, and data residency guarantees to meet government agency and regulated industry data localization and cybersecurity requirements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solution |

64.2% |

2025 |

|

Type |

🔒 |

🔒 |

2025 |

|

Enterprise Size |

Large Enterprises |

68.5% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Northern Taiwan |

46.9% |

2025 |

By Enterprise Size

Large enterprises command a 68.5% majority share in 2025 owing to their substantial IT infrastructure requirements, regulatory compliance mandates, and dedicated data center procurement budgets. Financial institutions, technology companies, and government agencies collectively represent the core large enterprise demand base in Taiwan.

To access detailed market analysis, Request Sample

Small and Medium Enterprises at 31.5% in 2025 are the faster-growing segment as colocation pricing and cloud-native deployment models lower the barrier to premium data center services. Taiwan’s vibrant SME technology ecosystem in software, fintech, and IoT hardware is driving this growth trajectory.

By Component

The Solution segment dominates the component breakdown at 64.2% in 2025, encompassing IT infrastructure hardware, software platforms, security solutions, and cloud management tools. Solution’s dominance reflects the capital intensity of hardware refresh cycles and the growing adoption of software-defined infrastructure platforms.

Services at 35.8% in 2025 encompass managed services, professional services, colocation services, and consulting, growing as enterprises increasingly outsource non-core infrastructure operations. Managed security services and cloud migration consulting are the fastest-growing service sub-categories within the segment.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Northern Taiwan |

46.9% |

Technology and financial hub; hyperscaler campus expansion; submarine cable access; high interconnection density |

|

Central Taiwan |

21.8% |

Semiconductor cluster ecosystem; advanced manufacturing digital infrastructure; R&D and engineering data workloads |

|

Southern Taiwan |

19.6% |

Industrial zone expansion; government-backed digital investment; disaster recovery and backup facility development |

|

Eastern Taiwan |

11.7% |

Lower land and power costs; government digital infrastructure incentives; emerging edge computing deployment |

Northern Taiwan’s 46.9% market dominance in 2025 is driven by Taipei’s concentration of multinational technology companies, financial institutions, and government agencies. The region benefits from dense carrier-neutral colocation facilities and direct access to major submarine cable systems connecting Taiwan to global internet infrastructure.

Central Taiwan, with 21.8% in 2025, benefits from the advanced semiconductor manufacturing ecosystem generating adjacent data center demand for chip design simulation, EDA software infrastructure, and supply chain management systems requiring low-latency connectivity to fabrication facilities.

Southern Taiwan at 19.6% is experiencing accelerating data center development supported by lower land costs, government digital infrastructure incentives, and growing industrial sector digitalization requirements from manufacturing clusters in the region.

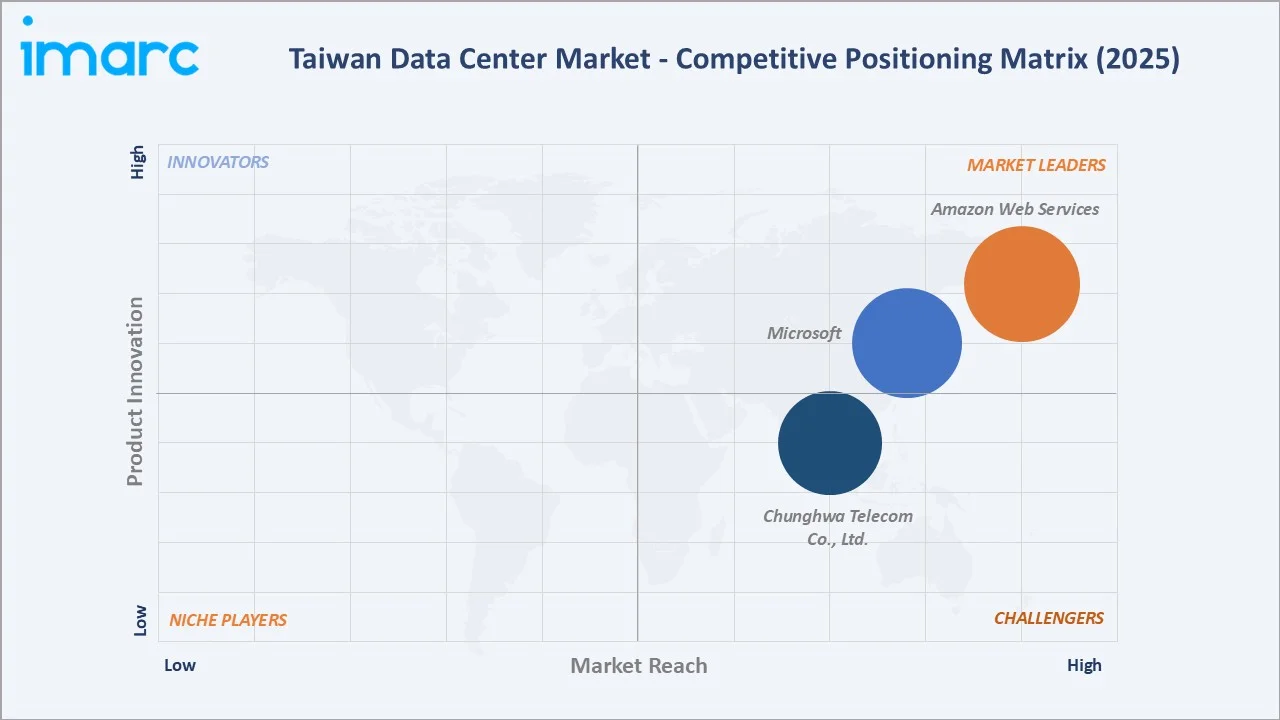

Competitive Landscape

The Taiwan data center market is moderately consolidated, with global hyperscalers and international colocation operators competing alongside domestic telecom carriers for enterprise customers. Northern Taiwan’s interconnection-dense market is dominated by international operators, while regional markets are served by domestic telecom-affiliated data center providers.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Amazon Web Services, Inc. |

AWS Data Centers |

Leader |

Public cloud; AI/ML; enterprise and government cloud |

|

Microsoft |

Microsoft Datacenters |

Leader |

Enterprise cloud; sovereign cloud; AI-optimized infrastructure |

|

Chunghwa Telecom Co., Ltd. |

Data Center Services |

Challenger |

National incumbent; government cloud; hybrid infrastructure |

Key players include Amazon Web Services, Inc., Microsoft, Chunghwa Telecom Co., Ltd., and others.

Key Company Profiles

Amazon Web Services, Inc.

Amazon Web Services, Inc. is the world's leading cloud infrastructure provider and the most significant international entrant into Taiwan's data center market, serving enterprises, government agencies, semiconductor manufacturers, and financial institutions across Taiwan.

- Product Portfolio: AWS Data Centers

- Recent Developments: In June 2025, Amazon launched the AWS Asia Pacific (Taipei) Region, committing more than USD 5 Billion toward the construction, operation, and maintenance of its data center infrastructure in Taiwan over the long term. The new Region delivers low-latency compute, secure data residency, and robust compliance capabilities for regulated industries, with a third AWS Direct Connect location added within the Chief Telecom HD data center near Taipei to provide customers with higher speed and bandwidth connectivity.

- Strategic Focus: Amazon Web Services leverages its global cloud platform, AI and machine learning services, and deep enterprise partnerships—including with Chunghwa Telecom, TSMC, Cathay Financial Holdings, and Trend Micro—to capture high-value cloud migration and AI workload demand from Taiwan's semiconductor, financial services, and manufacturing sectors, while investing in local workforce upskilling through AWS Academy and AWS Skill Builder to accelerate enterprise cloud adoption.

Chunghwa Telecom Co., Ltd.

Chunghwa Telecom is Taiwan’s national incumbent telecommunications carrier and the largest IDC operator by domestic revenue, operating data center facilities across all major Taiwan regions with strength in government cloud and regulated industry sectors.

- Product Portfolio: Data Center Services

- Recent Developments: In December 2025, Chunghwa Telecom partnered with HPE to launch a next-generation international disaster recovery center aimed at helping enterprises strengthen cyber resilience and protect critical business data against ransomware attacks. The new facility will leverage HPE’s Cyber Resilience Vault technology, enabling businesses to achieve near real-time backup recovery with second-level Recovery Point Objectives (RPO) and minute-level Recovery Time Objectives (RTO).

- Strategic Focus: Chunghwa Telecom leverages its national network infrastructure, government relationships, and existing enterprise customer base to defend market leadership in domestic colocation while expanding into cloud and AI-enabled managed services.

Market Concentration Analysis

The Taiwan data center market is moderately concentrated at the national level. Northern Taiwan’s market is dominated by international operators competing for hyperscaler and large enterprise tenants, while domestic telecom carriers hold stronger positions in mid-market and government segments requiring local compliance and sovereignty guarantees.

Consolidation is accelerating through hyperscaler campus acquisitions and international PE-backed roll-up strategies. Institutional capital flows into Taiwan’s data center market reflect its positioning as a critical Asia-Pacific infrastructure asset with long-term contracted cash flows from investment-grade hyperscaler and enterprise tenants.

Investment & Growth Opportunities

Fastest-Growing Segments

The Solution segment at ~6.3% CAGR through 2034 is the highest-growth component category, driven by AI infrastructure hardware refresh cycles, software-defined storage and networking adoption, and cybersecurity platform investment across enterprise and government sectors.

Emerging Markets

Southern and Eastern Taiwan, growing above the national average CAGR, represent the fastest-growing regions through 2034. Lower land and power costs, government incentives for data center investment outside Taipei, and growing manufacturing sector digitalization are driving new capacity development.

Venture & Investment Trends

Global infrastructure funds are active in Taiwan data center acquisitions, attracted by stable long-term leased cash flows from hyperscaler tenants. Green financing instruments including sustainability-linked bonds are gaining adoption for new data center construction projects targeting green building certification and renewable energy commitments.

Future Market Outlook (2026-2034)

The Taiwan data center market is forecast to expand from USD 1.59 Billion in 2025 to USD 2.64 Billion by 2034 at a CAGR of 5.76%, adding USD 1.05 Billion in incremental annual market value over the forecast period. This sustained growth reflects Taiwan’s strategic position as Asia-Pacific’s premier semiconductor and technology hub.

Three structural forces will most significantly shape the Taiwan data center landscape through 2034. AI infrastructure demand will drive specialized GPU cluster data center construction. Government sovereign cloud mandates will generate domestic public sector data center investment. Submarine cable expansion will reinforce Taiwan’s role as a regional internet exchange hub, attracting further international colocation and interconnection investment.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews in 2024-2025 with Taiwan data center industry stakeholders, including senior operations managers at colocation operators, enterprise IT procurement directors, government technology officials, and cloud services architects at hyperscaler Taiwan teams.

Secondary Research

Key secondary sources include Taiwan MOEA Industrial Development Bureau data center reports, Taiwan Network Information Center internet infrastructure surveys, IDC Asia-Pacific cloud and data center forecasts, Gartner cloud infrastructure spending data, and industry publications including Data Center Frontier and Datacenter Dynamics.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, cloud spending proxies, digital transformation indices, and historical market evolution patterns. Scenario analysis was performed to account for geopolitical and macroeconomic uncertainty.

Taiwan Data Center Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Residential, Commercial, Industrial, Infrastructure (Transportation), Energy and Utilities Construction |

| Types Covered | Colocation, Hyperscale, Edge, Others |

| Enterprises Size Covered | Large Enterprises, Small and Medium Enterprises |

| End Users Covered | BFSI, IT and Telecom, Government, Energy and Utilities, Others |

| Regions Covered | Northern Taiwan, Central Taiwan, Southern Taiwan, Eastern Taiwan |

| Companies Covered | Amazon Web Services, Inc., Microsoft, Chunghwa Telecom Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Taiwan data center market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Taiwan data center market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Taiwan data center industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Taiwan Data Center Market Report

The Taiwan data center market reached USD 1.59 Billion in 2025, reflecting consistent demand from cloud services growth, digital transformation investment, and hyperscaler infrastructure expansion across the island.

The market is projected to reach USD 2.64 Billion by 2034, growing at a CAGR of 5.76% during 2026-2034, driven by AI computing infrastructure demand, government digitalization initiatives, and sustained hyperscaler investment in Taiwan.

Large enterprises lead with a 68.5% market share in 2025, valued for their high IT infrastructure requirements, regulatory compliance mandates, and dedicated procurement budgets across BFSI, IT, telecom, and government sectors.

Solution dominates at 64.2% in 2025, representing IT infrastructure hardware, software-defined platforms, security solutions, and cloud management systems. The segment benefits from continuous enterprise hardware refresh cycles and platform modernization investment.

Northern Taiwan commands a dominant 46.9% market share in 2025, driven by Taipei’s concentration of technology companies, financial institutions, and hyperscaler facilities with direct access to international submarine cable systems.

Northern Taiwan leads at ~6.4% CAGR through 2034, supported by continued hyperscaler campus expansion, interconnection hub development, and growing financial services and enterprise colocation demand in the Taipei metropolitan area.

Leading companies include Amazon Web Services, Inc., Microsoft, Chunghwa Telecom Co., Ltd., and others.

Key end-use sectors include BFSI, IT and Telecom, Government and Public Sector, Energy and Utilities, Healthcare, and Manufacturing, with BFSI and IT & Telecom collectively representing the highest demand concentration.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)