Takaful Market Size, Share, Trends and Forecast by Product Type and Region, 2026-2034

Global Takaful Market Size, Share, Trends & Forecast (2026-2034)

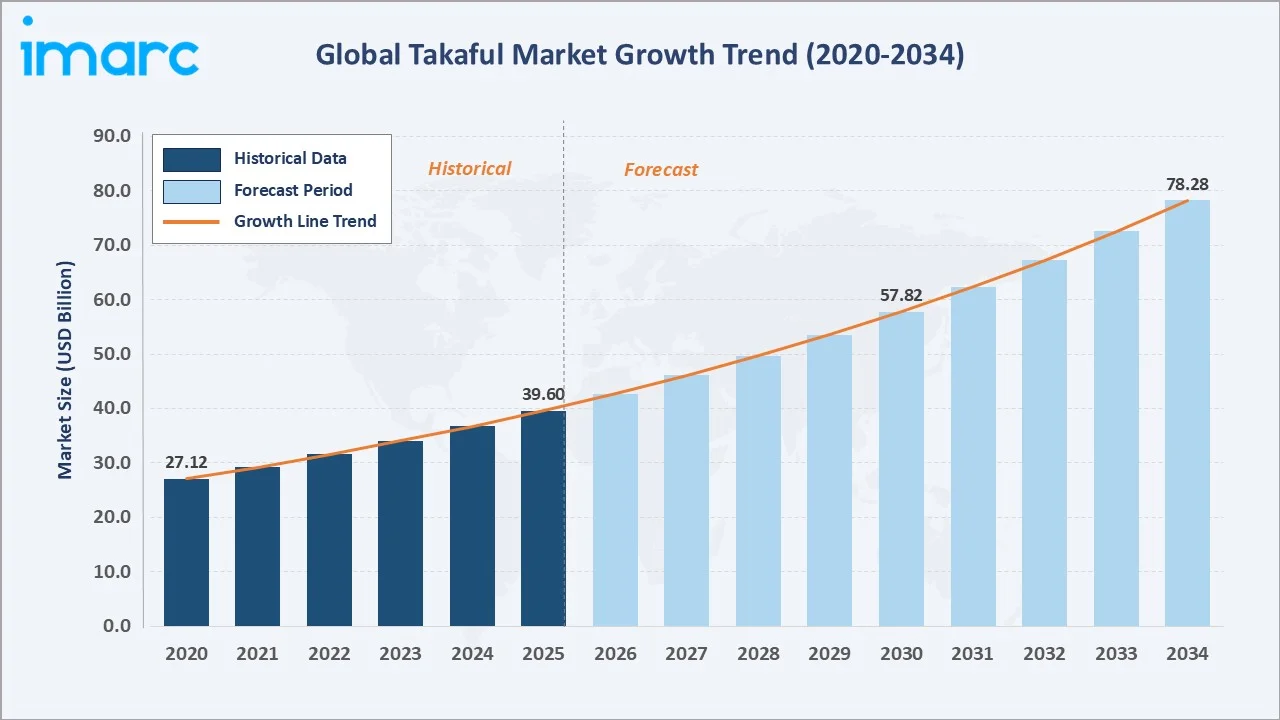

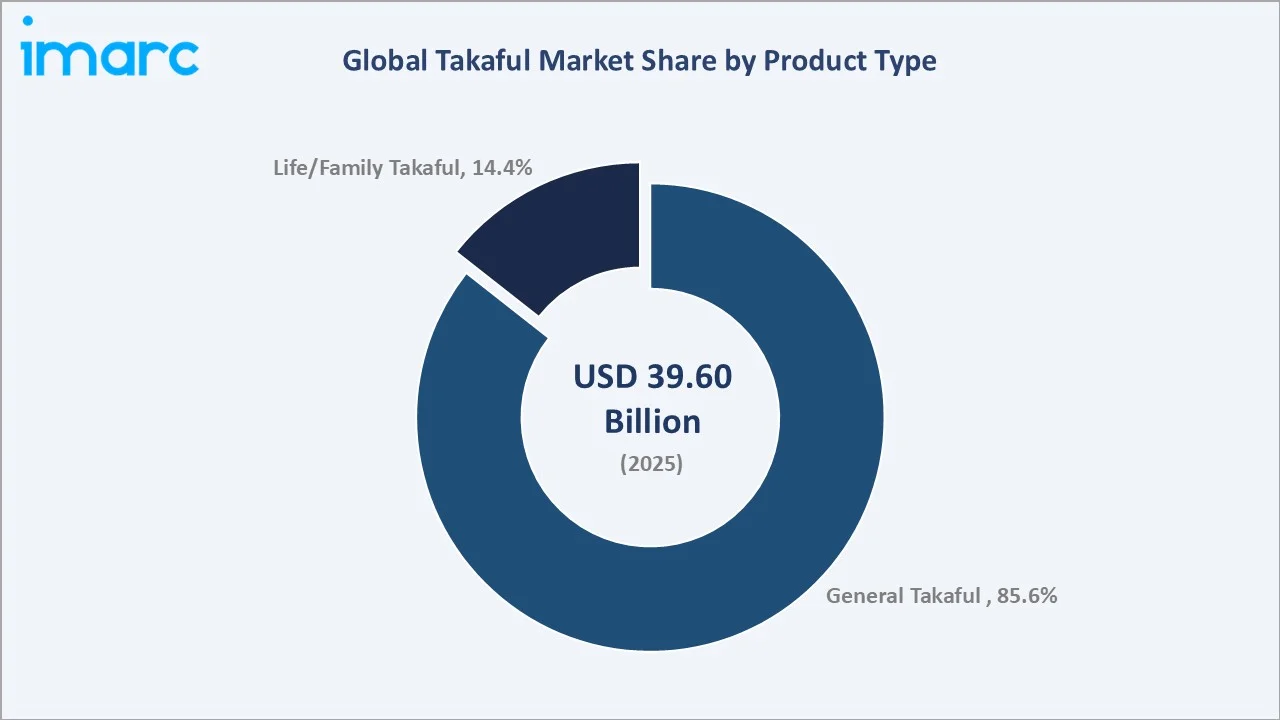

The global takaful market size was valued at USD 39.60 Billion in 2025 and is projected to reach USD 78.28 Billion by 2034, exhibiting a CAGR of 7.87% during the forecast period 2026-2034. Rapid expansion of the Muslim global population, growing Shariah-compliant financial awareness, and strong regulatory support from GCC governments are driving takaful market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 39.60 Billion |

|

Forecast Market Size (2034) |

USD 78.28 Billion |

|

CAGR (2026-2034) |

7.87% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

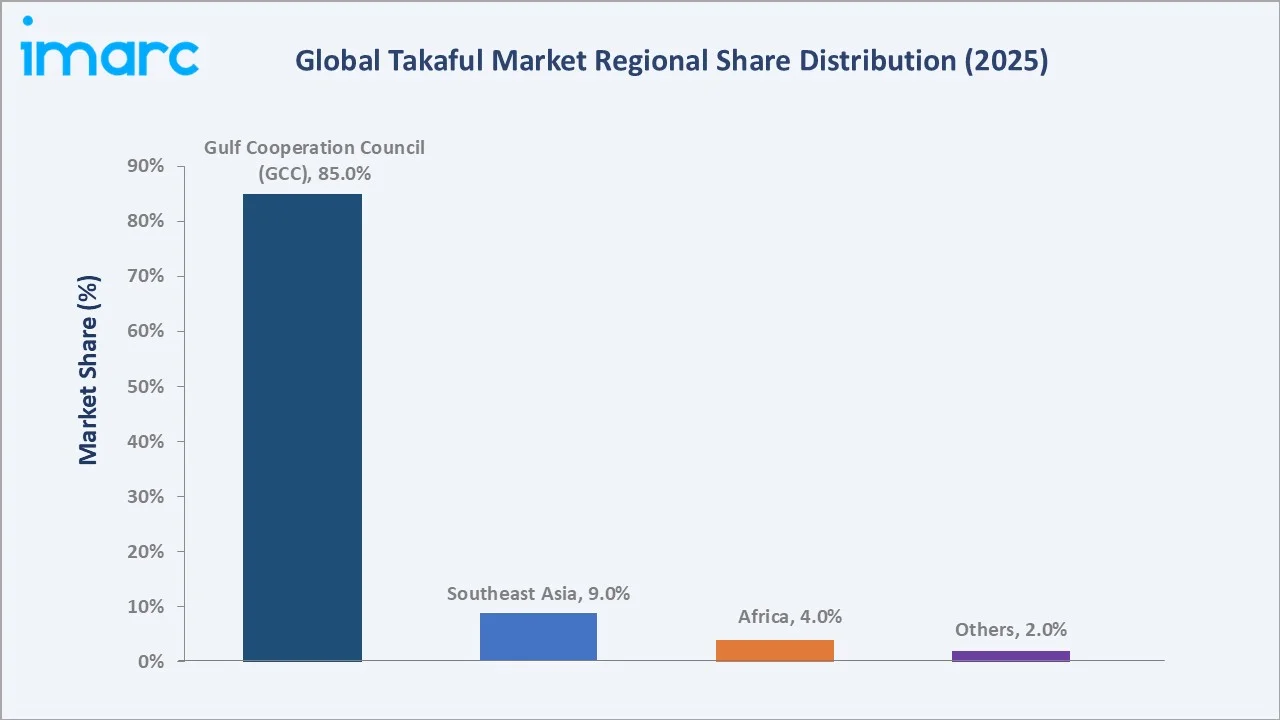

Gulf Cooperation Council (GCC) – 85% share (2025) |

|

Fastest Growing Region |

Southeast Asia (~9.3% CAGR) |

|

Leading Product Type |

General Takaful – 85.6% share (2025) |

The global takaful market growth trajectory from 2020 through 2034 highlights the contrast between historical expansion and a sustained forecast curve, powered by an expanding Muslim population, rising disposable incomes, and growing regulatory acceptance of Islamic finance across GCC, Southeast Asian, and African markets.

To get more information on this market, Request Sample

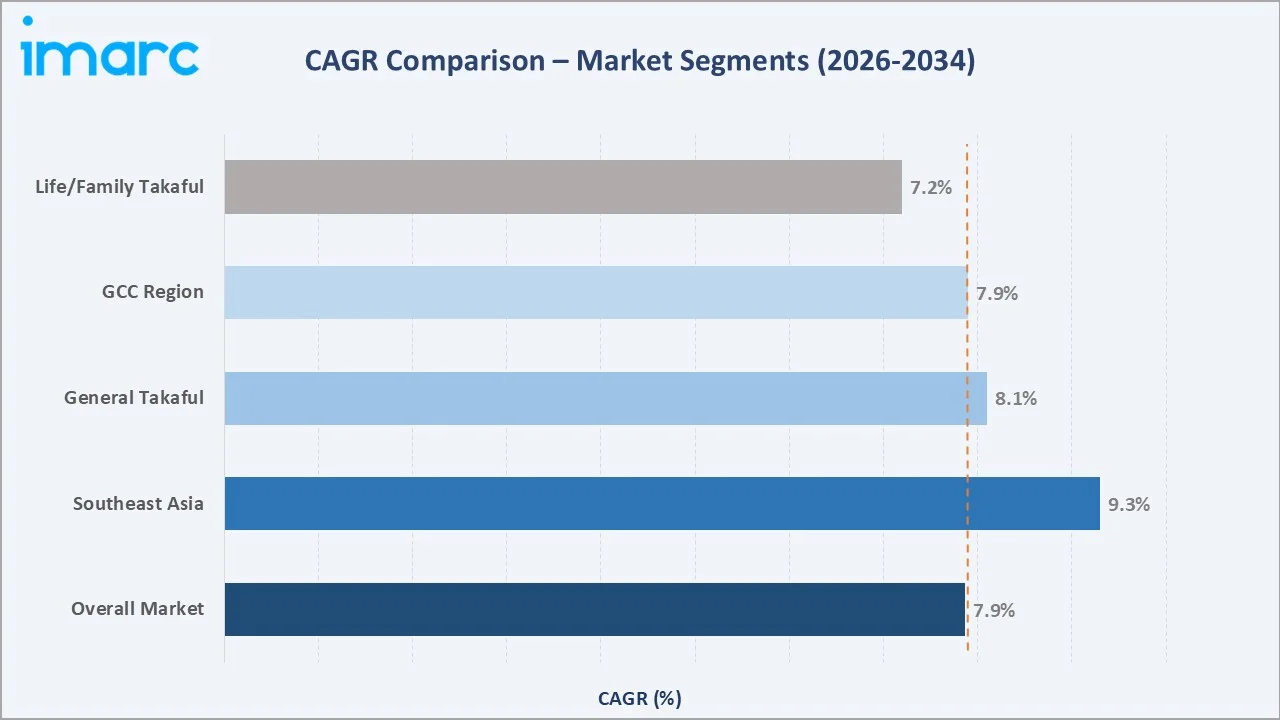

Segment-level CAGR comparisons highlight Southeast Asia region and the General Takaful segment as the fastest-growing sub-categories within the global takaful market forecast through 2034, outpacing both the market average and Life/Family Takaful growth.

Executive Summary

The global takaful market is undergoing a significant structural transformation. It is driven by the rapid spread of Islamic finance, Shariah-compliant insurance awareness, and government-backed regulatory frameworks across GCC nations. Valued at USD 39.60 Billion in 2025, the market is forecast to reach USD 78.28 Billion by 2034 at a CAGR of 7.87%.

General Takaful commands an 85.6% share in 2025, driven by widespread adoption across property, motor, and liability insurance lines. Life/Family Takaful accounts for 14.4% but holds high growth potential, particularly in younger, economically active Muslim-majority populations in Southeast Asia and Africa. The GCC remains the dominant regional bloc at 85%, anchored by Saudi Arabia, UAE, and Qatar—markets where Islamic finance is embedded in national financial architectures.

The takaful market outlook is strongly positive through 2034. Southeast Asia, representing 9% of global revenue in 2025, is projected to be the fastest-growing region, advancing at approximately 9.3% CAGR. Africa, though small at 4%, presents a high-upside, underpenetrated market opportunity. The entry of digital platforms and insurtech is reshaping distribution and expanding access to previously underserved Muslim-majority populations globally.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

General Takaful – 85.6% share (2025) |

|

Second Product Type |

Life/Family Takaful – 14.4% share (2025) |

|

Dominant Region |

GCC – 85% revenue share (2025) |

|

Fastest Growing Region |

Southeast Asia – ~9.3% CAGR (2026-2034) |

|

Top Companies |

Syarikat Takaful Malaysia Keluarga Berhad, Malayan Banking Berhad, Salama Islamic Arab Insurance Company, Abu Dhabi National Takaful Co. P.S.C., Qatar Islamic Insurance, and Great Eastern Takaful Berhad |

|

Market Opportunity |

Africa and South Asia – large, underserved Muslim populations with low takaful penetration rates |

Key Analytical Observations Supporting The Above Data:

- General Takaful's 85.6% dominance in 2025 reflects the near-universal adoption of Shariah-compliant motor, property, and commercial insurance lines across GCC markets, where conventional insurance faces regulatory and societal restrictions.

- Life/Family Takaful's 14.4% share understates long-term growth potential. In Malaysia, Family Takaful penetration remains relatively low compared to the eligible population, indicating substantial growth potential as Islamic financial literacy and awareness continue to improve.

- The GCC's 85% dominance in 2025 reflects Saudi Arabia's status as the world's largest takaful market, with insurers in the country accounting for 88% of total regional premiums in 2021, and continuing to drive growth through strong regulatory support, expanding product portfolios, and increasing adoption across key segments.

- Southeast Asia's 9% share and ~9.3% CAGR are underpinned by Malaysia's mature Islamic finance ecosystem, Indonesia's compulsory health insurance framework, and growing takaful adoption in Bangladesh and Pakistan.

- Africa, representing 4% of global revenue, holds high structural upside. Sub-Saharan Africa has a large Muslim population with very low takaful penetration, creating a significant greenfield opportunity for microinsurance and family takaful products.

Global Takaful Market Overview

Takaful is a cooperative, Shariah-compliant insurance model in which participants pool contributions to mutually guarantee one another against financial loss. Unlike conventional insurance, takaful prohibits interest (riba), excessive uncertainty (gharar), and gambling (maysir). The global market encompasses two primary product lines: General Takaful, covering property, motor, and liability risks; and Life/Family Takaful, addressing long-term savings, health, and life protection needs.

The takaful industry operates at the intersection of Islamic finance regulation, macroeconomic growth in Muslim-majority economies, and evolving consumer demand for ethical financial products. Growth is structurally supported by expanding young Muslim populations, rising middle-class incomes across GCC and Southeast Asia, and government-led frameworks mandating Islamic finance. The global Muslim population exceeded 2.0 billion in 2025, representing over 25% of the world's population - a structural demand base that continues to underpin takaful market expansion at a sustained CAGR of 7.87% through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

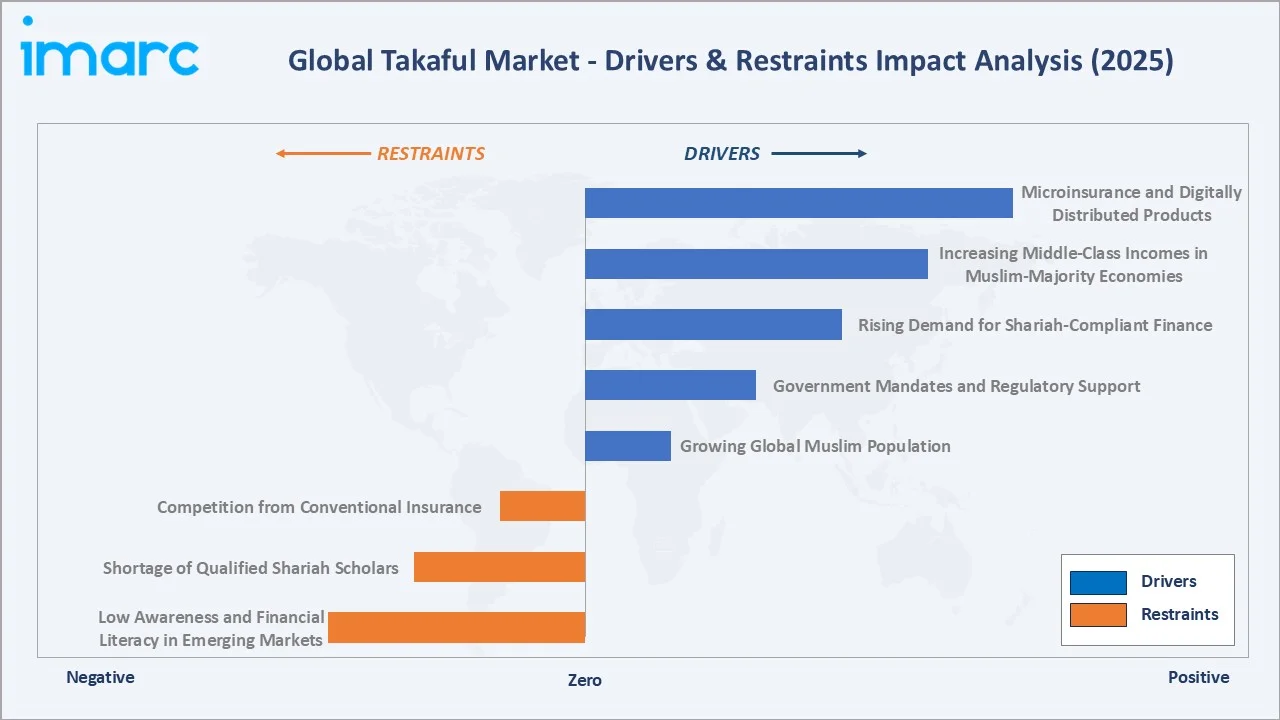

Market Drivers

- Growing Global Muslim Population: With over 2.0 billion Muslims globally in 2025, and a projected increase to 2.2 billion by 2030, the structural demand base for Shariah-compliant financial products continues to expand. GCC markets, home to high-income Muslim populations, remain the primary volume driver.

- Government Mandates and Regulatory Support: GCC central banks and Islamic financial regulators have made significant investments in formalizing takaful as a mainstream financial product. Saudi Arabia's Vision 2030 financial inclusion roadmap explicitly targets the expansion of Islamic insurance penetration among SMEs and households.

- Rising Demand for Shariah-Compliant Finance: Islamic banking accounts for over 70% of total Islamic finance assets, and assets projected to grow from USD 4 trillion in 2024 to USD 5.2 trillion by 2028 As consumers increasingly seek ethical, halal financial products, demand for takaful is expanding alongside broader Islamic banking and sukuk markets.

- Increasing Middle-Class Incomes in Muslim-Majority Economies: Rising per-capita incomes in Saudi Arabia, UAE, Malaysia, and Indonesia are converting previously underinsured populations into active takaful participants, driving premium volume growth across both General and Family lines.

Market Restraints

- Low Awareness and Financial Literacy in Emerging Markets: In Africa and South Asia, takaful penetration remains very low, primarily due to limited financial awareness, underdeveloped distribution infrastructure, and the continued reliance on informal risk-sharing mechanisms.

- Shortage of Qualified Shariah Scholars: Each takaful product must be certified by a Shariah supervisory board. The global shortage of qualified scholars creates bottlenecks in product development and compliance, particularly for newer entrants seeking to innovate product structures.

- Competition from Conventional Insurance: In markets where both conventional and Shariah-compliant options coexist - such as Southeast Asia and Turkey - takaful operators face significant pricing and brand competition from established global insurance groups.

Market Opportunities

- Microinsurance and Digitally Distributed Products: Digital takaful platforms are enabling cost-effective distribution in underserved markets. Indonesia, Bangladesh, and Nigeria offer significant scale opportunities for mobile-delivered microinsurance products targeting low-income Muslim households.

- Family Takaful Expansion in Southeast Asia: With relatively higher Family Takaful penetration in Malaysia, neighbouring markets such as Indonesia home to one of the world’s largest Muslim populations remain significantly underpenetrated, representing a substantial structural growth opportunity for takaful providers.

- Corporate Takaful and Bancatakaful Distribution: The growing network of Islamic banks across GCC and Southeast Asia provides a high-trust, cost-efficient distribution channel for takaful products, with bancatakaful emerging as a key contributor to family takaful premium growth, particularly in markets like Malaysia.

Market Challenges

- Retakaful Capacity Constraints: The global retakaful market remains considerably smaller than conventional reinsurance, limiting the risk transfer capacity available to primary takaful operators for large commercial risks.

- Standardization Across Jurisdictions: Divergent Shariah interpretations across GCC and Southeast Asian regulators create product fragmentation. AAOIFI and IFSB standards are widely referenced, but adoption is inconsistent, complicating cross-border product development.

Emerging Market Trends

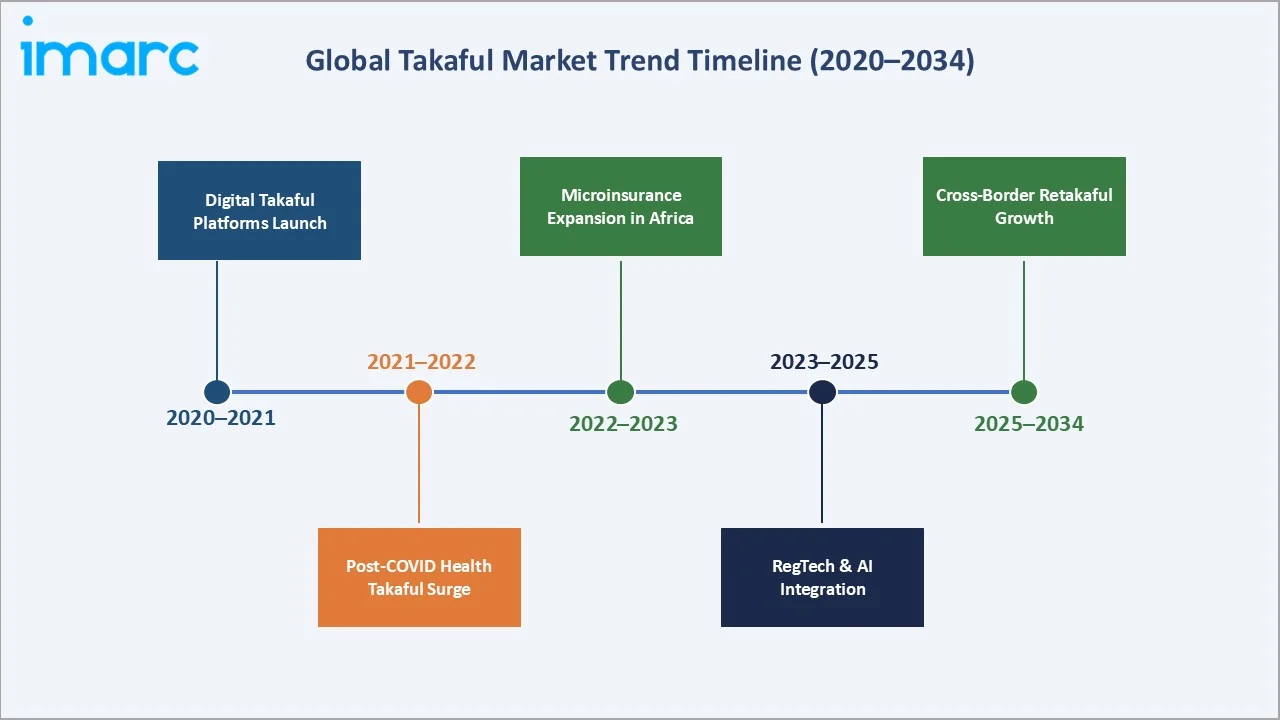

1. Accelerating Digital Takaful Platform Adoption

Insurtech and digital-first takaful operators are disrupting traditional distribution models. Mobile-delivered takaful products, powered by AI-driven underwriting, are expanding access in previously unreachable rural Muslim-majority markets across Southeast Asia and Africa.

2. Post-COVID Health and Critical Illness Takaful Surge

The COVID-19 pandemic accelerated health takaful enrolment across GCC and Southeast Asia, increasing demand for protection-oriented products. Health and medical takaful offerings have since become key growth drivers in the family takaful segment, supported by rising healthcare costs and heightened consumer awareness of health-related risks.

3. Microinsurance Expansion in Africa

With a large Muslim population and very low takaful penetration in Sub-Saharan Africa, micro-takaful products are increasingly being developed by regional operators in countries such as Nigeria, Kenya, and Senegal. Financial inclusion initiatives led by institutions like the African Development Bank are supporting these efforts through regulatory frameworks and funding mechanisms, enabling broader market expansion.

4. RegTech and AI Integration in Compliance

Shariah compliance verification and regulatory reporting are increasingly being automated through RegTech platforms. AI-assisted Shariah audit tools are reducing scholar bottlenecks, while machine learning models are improving fraud detection and claims management efficiency for takaful operators across the GCC.

5. Cross-Border Retakaful Capacity Building

Leading global reinsurers including Munich Re and Swiss Re have established dedicated Islamic windows (retakaful units). The global retakaful capacity is expanding steadily, enabling primary takaful operators to underwrite larger commercial risks and infrastructure-linked products in high-growth GCC economies.

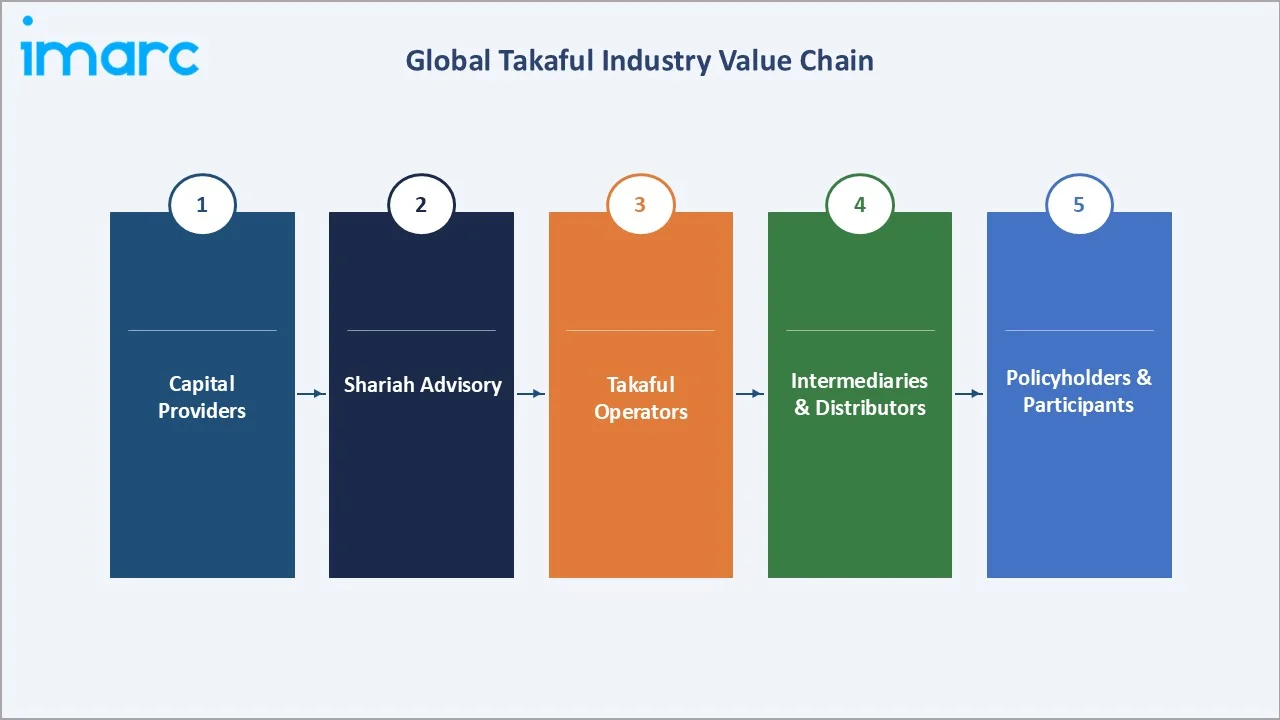

Industry Value Chain Analysis

The global takaful industry value chain spans five integrated stages - from capital provisioning through participant engagement. Each stage presents distinct regulatory, operational, and commercial dynamics.

|

Stage |

Key Participants & Role |

|

Capital Providers |

Shareholders, Islamic development banks, sovereign wealth funds (e.g. Saudi PIF, Abu Dhabi Investment Authority) |

|

Shariah Advisory & Governance |

AAOIFI, IFSB, national Shariah boards, independent scholars certifying product structures |

|

Takaful Operators |

General and Family takaful companies managing participants' funds under wakala or mudaraba models |

|

Intermediaries & Distribution |

Agents, brokers, bancatakaful channels (Islamic banks), digital platforms, direct-to-consumer apps |

|

Policyholders / Participants |

Individual consumers, SMEs, corporates, government entities contributing to the mutual pool |

Takaful operators hold the highest strategic position in the value chain, managing Shariah-compliant surplus redistribution and the investment of participants’ funds in halal asset classes. Bancatakaful channels represent a major share of distribution in mature markets, making Islamic banks a critical gateway and strategic partner for expanding family takaful reach.

Technology Landscape in the Takaful Industry

Digital Distribution and Insurtech Platforms

Mobile-first and web-based takaful platforms are transforming customer acquisition and policy management across GCC and Southeast Asia. Saudi Arabia's regulatory sandbox, managed by SAMA, has approved over 15 insurtech pilots between 2022 and 2024, with several focused on takaful automation.

AI and Machine Learning in Underwriting

AI-driven underwriting tools are improving risk selection accuracy and reducing mispricing in takaful operations. Malaysian operators such as Etiqa and Great Eastern Takaful have integrated machine learning models for health takaful risk assessment, streamlining underwriting processes and significantly reducing turnaround times.

Shariah RegTech and Compliance Automation

RegTech platforms are automating Shariah compliance monitoring, audit trails, and regulatory reporting. Automated Shariah audit tools are reducing the dependence on manual scholar review for routine product compliance. AAOIFI's digital certification frameworks are being adopted by UAE and Bahrain-based operators.

Blockchain for Transparency and Claims Processing

Blockchain-based smart contracts are being piloted for takaful claims processing and surplus sharing calculations. The immutable ledger capability of blockchain aligns naturally with takaful's transparency and mutual accountability principles. UAE and Bahrain have seen the most active blockchain takaful pilot activity as of 2024.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | General Takaful | 85.6% | 2025 |

| Region | Gulf Cooperation Council (GCC) | 85.0% | 2025 |

By Product Type

To access detailed market analysis, Request Sample

General Takaful leads the global takaful market with an 85.6% share in 2025. Demand is driven by mandatory motor takaful regulations in Saudi Arabia, UAE, and Malaysia, as well as robust commercial property insurance adoption among GCC corporates.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Gulf Cooperation Council (GCC) |

85% |

Saudi Vision 2030 financial inclusion, compulsory motor takaful, UAE/Qatar corporate insurance growth |

|

Southeast Asia |

9% |

Malaysia Family Takaful maturation, Indonesia underpenetration, digital platforms, Bank Negara Malaysia regulatory support |

|

Africa |

4% |

Microinsurance growth, Nigeria/Kenya Islamic finance regulation, AfDB financial inclusion programs, large, underserved Muslim population |

|

Others |

2% |

South Asia (Pakistan, Bangladesh), Turkey, UK Islamic finance windows, growing diaspora Muslim populations in Europe |

The Gulf Cooperation Council (GCC) commands an 85% global revenue share in 2025. Saudi Arabia is the world's single largest takaful market. Compulsory motor takaful, health insurance mandates for expatriates, and expanding SME coverage under Vision 2030 financial sector targets are the primary drivers. The UAE and Qatar are exhibiting strong corporate and commercial takaful growth, supported by mega-project pipelines and high-income populations.

Southeast Asia represents 9% of global revenue in 2025 and is the fastest-growing region at approximately 9.3% CAGR through 2034. Malaysia, anchored by Bank Negara Malaysia's Islamic Financial Services Act and a mature bancatakaful distribution network.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Syarikat Takaful Malaysia Keluarga Berhad |

Takaful Malaysia |

Leader |

SEA market leadership, digital bancatakaful |

|

Malayan Banking Berhad |

Etiqa Takaful |

Leader |

Digital-first platform, Maybank bancatakaful reach |

|

Salama Islamic Arab Insurance Company |

Salama Takaful |

Leader |

GCC + Africa multi-market operator |

|

Abu Dhabi National Takaful Co. P.S.C. |

ADNTakaful |

Leader |

UAE corporate & health takaful coverage |

|

Qatar Islamic Insurance |

Qatar Islamic Insurance (QIIC) |

Challenger |

Qatar market anchor, commercial lines strength |

|

Great Eastern Takaful Berhad |

Great Eastern Takaful |

Challenger |

Malaysia Family Takaful innovation |

The global takaful market's competitive landscape is moderately concentrated at the top, with a long tail of regional operators. Leading players compete on Shariah compliance credentials, digital distribution innovation, bancatakaful partnerships, and product breadth. Strategic expansions and cross-border licensing agreements are key competitive tools in 2024–2025.

Key Company Profiles

Syarikat Takaful Malaysia Keluarga Berhad

Syarikat Takaful Malaysia Berhad is one of Malaysia’s leading Islamic insurances (takaful) providers and is widely recognized as the country’s first takaful operator. Established in 1984 and headquartered in Kuala Lumpur .

- Product & Platform Portfolio: The portfolio spans motor, fire, personal accident, medical, education, and mortgage takaful products, distributed through bancatakaful (BIMB), agents, and a digital-first mobile app.

- Recent Developments: In 2025, Syarikat Takaful Malaysia Keluarga Berhad is strengthening its long-term growth outlook through strategic expansion and market share gains. The company reported a 9% year-on-year increase in takaful revenue to about RM1.85 billion in the first half of 2025, reflecting resilient performance.

- Strategic Focus: Bancatakaful channel deepening, digital product distribution, and expansion of Family Takaful among Malaysia's young Muslim-majority population.

Malayan Banking Berhad

Malayan Banking Berhad (Maybank) is the largest financial services group in Malaysia and one of the leading banks in Southeast Asia. Established in 1960 and headquartered in Kuala Lumpur, it is listed on Bursa Malaysia and operates as a universal bank offering a wide range of financial products and services.

- Product & Platform Portfolio: The portfolio spans motor takaful, fire and property takaful, personal accident, medical and health, education, investment-linked, and mortgage/home financing takaful.

- Recent Developments: In 2026, Malayan Banking Berhad has launched its ROAR30 (2026–2030) strategy, with a strong emphasis on expanding its Islamic finance ecosystem, including takaful. The bank aims to scale its global Islamic finance business as a core growth pillar, targeting leadership across ASEAN and positioning itself among the top global Islamic banking and takaful players by 2030.

- Strategic Focus: Digital ecosystem integration, cross-selling within the Maybank financial services group, and regional ASEAN expansion.

Salama Islamic Arab Insurance Company

Salama Islamic Arab Insurance Company is the world's oldest and one of the largest takaful operators by premium volume, headquartered in Dubai, UAE. It operates across multiple regions including the Middle East, Africa, and parts of Asia.

- Product & Platform Portfolio: Salama's portfolio includes General Takaful (motor, property, marine, engineering) and Family Takaful, with a particular strength in corporate and commercial insurance lines across GCC.

- Recent Developments: In 2025, Salama Islamic Arab Insurance Company expanded its Life Takaful offerings via Policybazaar.ae and launched a new Home Finance Takaful solution in partnership with ADIB, while also enhancing its health takaful portfolio with products such as EBP, Flexi, and the new MediShield plan featuring global coverage and telehealth services.

- Strategic Focus: Multi-market GCC/Africa footprint, corporate insurance volume growth, and digital claims processing improvement.

Market Concentration Analysis

The global takaful market exhibits moderate concentration at the top tier. The leading five operators - Syarikat Takaful Malaysia Keluarga Berhad, Malayan Banking Berhad, Salama Islamic Arab Insurance Company, Abu Dhabi National Takaful Co. P.S.C., Qatar Islamic Insurance - collectively account for an estimated 25–32% of global takaful revenue in 2025. The remaining share is distributed across a large number of regional operators, Islamic insurance windows of conventional insurers, and emerging microinsurance providers.

The market is experiencing a bifurcated competitive dynamic. At the premium operator tier, consolidation is occurring around digital platform capabilities, bancatakaful partnerships, and regulatory compliance infrastructure. In contrast, the African and South Asian markets are characterized by high fragmentation, with dozens of small regional operators competing primarily on price and community trust networks. This dual dynamic is expected to persist through 2034, with gradual consolidation in mature GCC and Southeast Asian markets offset by new entrant growth in underpenetrated emerging markets.

Investment & Growth Opportunities

Fastest-Growing Segments

Family/Life Takaful is the highest-growth structural opportunity, with Southeast Asia’s underpenetration offering significant addressable market upside. Health Takaful is the fastest-growing sub-segment within General Takaful, driven by expanding health coverage mandates and increasing demand across key Islamic finance markets such as Saudi Arabia, the UAE, and Malaysia.

Emerging Market Expansion

Indonesia represents the highest-potential single emerging market, with 242+ million Muslims. Nigeria, Bangladesh, and Pakistan collectively represent a large, underinsured Muslim population. Digital distribution infrastructure is increasingly improving market accessibility and making these markets more viable for product launches by regional and global takaful operators.

Venture and Strategic Investment Trends

Islamic fintech investments globally have grown significantly in recent years, with increasing capital flowing into takaful-focused insurtech platforms. Key investment focus areas include AI-powered underwriting for health takaful, microinsurance platforms enabling mobile-first distribution in Africa and South Asia, and blockchain-enabled re-takaful settlement systems. Bancatakaful partnership agreements between Islamic banks and takaful operators continue to attract strategic investments across the GCC and Southeast Asia.

Future Market Outlook (2026-2034)

The global takaful market forecast projects steady value expansion from USD 39.60 Billion in 2025 to USD 78.28 Billion by 2034 at a CAGR of 7.87%. The GCC will retain regional leadership while the Southeast Asian and African markets drive incremental growth through new participant acquisition and product innovation.

Three structural shifts will reshape the takaful market through 2034. Digital-first distribution will displace traditional agent networks as the primary channel in Southeast Asia and emerging African markets by 2028–2030, reducing distribution costs and enabling mass-market product launches. Mandatory health takaful frameworks in high-population Muslim markets will convert large uninsured populations into premium contributors. Meanwhile, the formalization of international takaful standards by AAOIFI and IFSB is expected to unlock cross-border product development, enabling operators to scale efficiently across multiple jurisdictions.

Research Methodology

Primary Research

Primary research was conducted in 2024–2025 through structured interviews with takaful industry stakeholders, including product directors at leading operators, bancatakaful managers at Islamic banks, Shariah board members, and institutional investors in Islamic finance. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include IFSB Global Islamic Finance Development Reports, AAOIFI Shariah Standards, Saudi SAMA Insurance Market Reports, Bank Negara Malaysia Takaful Statistics, World Bank Islamic Finance reports, Islamic Development Bank publications, Refinitiv Eikon Islamic finance data, and regional takaful association databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating Muslim population growth rates, per-capita income growth, regulatory mandate impacts, and historical takaful market evolution patterns. Scenario analysis - base, optimistic, and conservative cases - was performed to account for macroeconomic and regulatory uncertainty.

Takaful Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Life/Family Takaful, General Takaful |

| Regions Covered | Gulf Cooperation Council (GCC), Southeast Asia, Africa, Others |

| Companies Covered | Syarikat Takaful Malaysia Keluarga Berhad, Malayan Banking Berhad, Salama Islamic Arab Insurance Company, Abu Dhabi National Takaful Co. P.S.C., Qatar Islamic Insurance, Great Eastern Takaful Berhad, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, takaful market outlook, and dynamics of the market from 2020-2034.

- The takaful market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the takaful industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Takaful Market Report

The global takaful market was valued at USD 39.60 Billion in 2025, driven by a growing Muslim population, rising Shariah-compliant financial awareness, and strong regulatory support across GCC markets.

The market is projected to reach USD 78.28 Billion by 2034, exhibiting a CAGR of 7.87%, supported by Southeast Asian expansion, digital distribution, and Health Takaful mandates.

General Takaful leads with an 85.6% share in 2025, driven by compulsory motor and health insurance mandates across Saudi Arabia, UAE, and Malaysia.

The Gulf Cooperation Council (GCC) dominates with an 85% share in 2025. Saudi Arabia alone contributes approximately 30% of global takaful gross written contributions.

Southeast Asia is the fastest-growing region, advancing at approximately 9% CAGR through 2034, driven by Indonesia's underpenetrated market and Malaysia's maturing Family Takaful ecosystem.

Key drivers include global Muslim population growth, Shariah-compliant finance demand, government regulatory mandates, rising middle-class incomes, digital distribution platforms, and health insurance expansion.

Major players include Syarikat Takaful Malaysia Keluarga Berhad, Malayan Banking Berhad, Salama Islamic Arab Insurance Company, Abu Dhabi National Takaful Co. P.S.C., Qatar Islamic Insurance, and Great Eastern Takaful Berhad, and other.

The global takaful market is projected to reach approximately USD 57.82 Billion in 2030, reflecting sustained 7.87% CAGR growth.

Family Takaful is a Shariah-compliant life and savings protection product. It accounts for 14.4% of the global market in 2025 but holds significant growth potential in underpenetrated Southeast Asian and African markets.

Key opportunities include Health Takaful expansion, digital microinsurance platforms in Africa and South Asia, Indonesia's underpenetrated Family Takaful market, bancatakaful partnerships, and AI-driven underwriting technology.

Digital takaful platforms, AI-powered underwriting, RegTech compliance tools, and blockchain-based claims processing are transforming distribution, operational efficiency, and product innovation across the global takaful market.

General Takaful covers short-term risks including motor, property, fire, and marine. Life/Family Takaful addresses long-term needs including life protection, savings, education funding, and critical illness coverage under Shariah principles

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)