Thailand Real Estate Market Size, Share, Trends and Forecast by Property, Business, Mode, and Region, 2026-2034

Thailand Real Estate Market Summary:

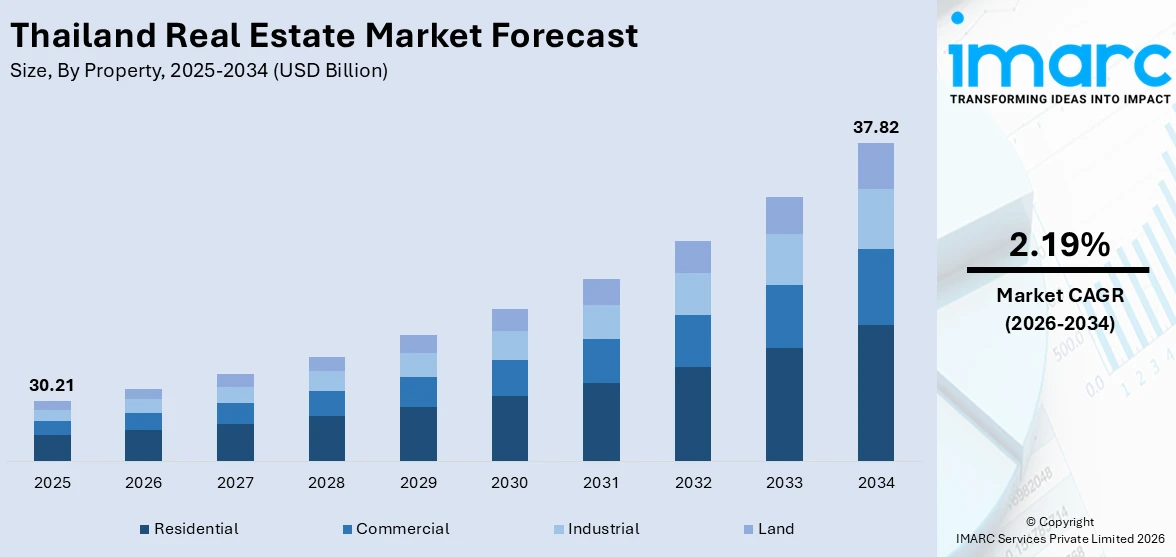

The Thailand real estate market size was valued at USD 30.21 Billion in 2025 and is projected to reach USD 37.82 Billion by 2034, growing at a compound annual growth rate of 2.19% from 2026-2034.

The real estate market in Thailand is witnessing consistent growth supported by urbanization, a resurgence in tourism, and increasing infrastructure development in key cities and economic zones. Encouraging policy changes that improve foreign ownership regulations and long-term residency benefits are directing global investment into the industry. Increasing interest in mixed-use projects and alternative property types also contributes to the Thailand real estate market share.

Key Takeaways and Insights:

- By Property: Residential leads the market with a share of 51.3% in 2025, driven by sustained housing demand across urban centers and the growing preference for modern, amenity-rich residential developments.

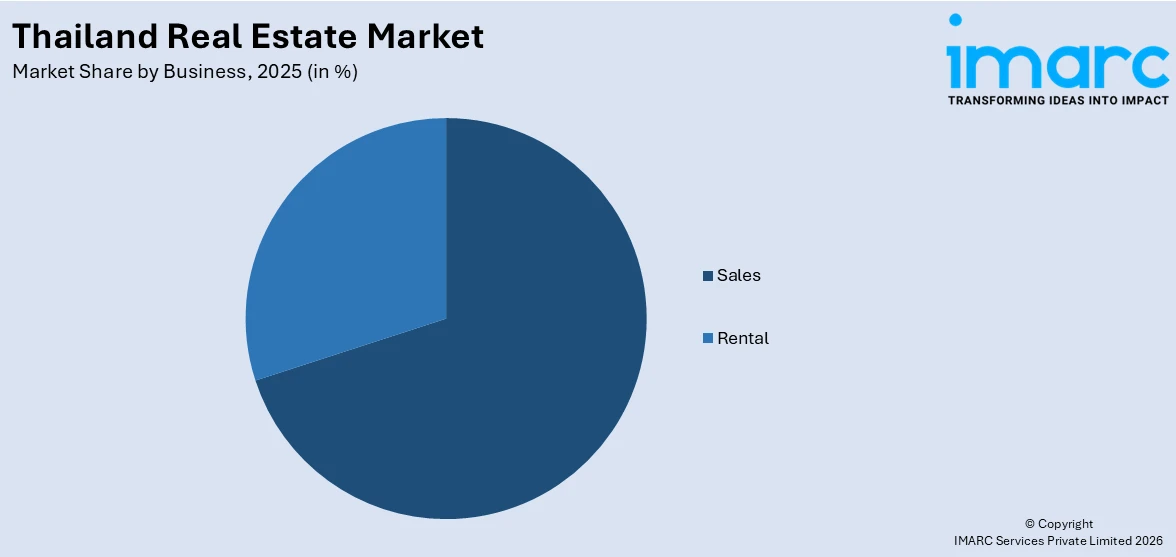

- By Business: Sales dominates the market with a share of 69.9% in 2025, supported by active buyer participation and government-backed transaction incentives driving condominium and low-rise property demand.

- By Mode: Offline represents the largest segment with a market share of 72.8% in 2025, as buyers consistently prefer in-person property inspections, agent-guided transactions, and face-to-face negotiations for high-value real estate purchases.

- By Region: Bangkok leads the market with a share of 52.3% in 2025, underpinned by its status as Thailand's commercial and financial capital, featuring dense transit networks and concentrated international investment activity.

- Key Players: The Thailand real estate market features a moderately competitive landscape, with established domestic developers and international investors spanning residential, commercial, and hospitality segments, adapting strategies to evolving demand patterns and policy changes.

To get more information on this market Request Sample

The real estate market in Thailand is propelled by swift urbanization, the growing demand for residential and mixed-use properties, and a rise in investments in infrastructure and tourism projects. The increasing urban populations and shifting lifestyles are driving the need for contemporary housing, condominiums, and cohesive communities, especially in large cities. Government efforts to encourage foreign investment and improve infrastructure connectivity are further bolstering the market growth. The rise of the tourism and hospitality industries is also catalyzing the demand for commercial and resort properties. In line with this trend, Airports of Thailand (AOT) initiated a project in 2025 to transform land surrounding six major airports into commercial and mixed-use real estate centers, encouraging private investment in logistics, hospitality, retail, and residential developments. These initiatives enhance land use, boost connectivity, and aid in the formation of integrated real estate ecosystems, thus fostering ongoing growth in Thailand's real estate sector.

Thailand Real Estate Market Trends:

Integration of Smart Technologies in Real Estate Development

The increasing integration of digital technologies and smart systems is emerging as a key trend in Thailand real estate market as developers focus on enhancing asset performance, sustainability, and tenant experience. Property owners are adopting data-driven solutions, automation, and digital infrastructure to improve building efficiency and operational management. These technologies also support energy optimization and personalized user experiences, aligning with evolving expectations of modern occupants. Reflecting this trend, in 2025, JLL launched Technology Advisory services in Thailand to support smart building adoption and digital transformation across real estate assets. The initiative highlights the growing importance of technology-enabled properties, as developers and investors prioritize innovation to remain competitive and meet the rising demand for intelligent, connected, and sustainable real estate environments.

Rising Demand for Lifestyle-Oriented Residential Developments

The growing preference for branded residences and lifestyle-focused living is shaping Thailand’s luxury real estate segment, particularly in key tourist destinations. High-net-worth individuals and international buyers are increasingly seeking premium properties that combine hospitality services, wellness features, and exclusive amenities. Developers are responding by partnering with global hospitality brands to create differentiated residential offerings. Reflecting this trend, in 2025, Proud Real Estate launched InterContinental-branded beachfront residences in Phuket, targeting global buyers interested in long-term, wellness-oriented living. This development signals Phuket’s evolution into a residential destination beyond tourism, with lifestyle-driven projects enhancing its appeal among international investors and reinforcing the growth of branded real estate across Thailand.

Increasing Sales and Marketing Initiatives

Aggressive marketing campaigns and promotional strategies are playing a vital role in impelling the Thailand real estate market. Developers are leveraging targeted promotions, property expos, and flexible purchasing schemes to attract buyers and accelerate sales cycles. These initiatives are particularly important in maintaining transaction volumes and improving market liquidity amid changing economic conditions. Reflecting this trend, in 2024, Sansiri launched a large-scale year-end promotion supported by expo participation, generating significant sales value and highlighting renewed buyer interest. Such campaigns demonstrate how developers are actively engaging with consumers and adapting sales strategies to drive market activity, contributing to improved demand conditions and sustained growth in Thailand’s residential real estate sector.

Market Outlook 2026-2034:

The real estate market in Thailand shows a consistent and encouraging growth path throughout the projected period, bolstered by enhancing demographic factors, continuous infrastructure spending, and forward-looking policy changes. The market generated a revenue of USD 30.21 Billion in 2025 and is projected to reach a revenue of USD 37.82 Billion by 2034, growing at a compound annual growth rate of 2.19% from 2026-2034. Bangkok will maintain its role as the primary source of market revenue, with tourism-related areas and industrial corridors broadening the growth foundation. Increased foreign involvement via revised ownership structures and transit-oriented developments is anticipated to support steady market momentum during the forecast period

Thailand Real Estate Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Property |

Residential |

51.3% |

|

Business |

Sales |

69.9% |

|

Mode |

Offline |

72.8% |

|

Region |

Bangkok |

52.3% |

Property Insights:

- Residential

- Commercial

- Industrial

- Land

Residential dominates with a market share of 51.3% of the total Thailand real estate market in 2025.

Residential holds the biggest market share fueled by significant urbanization trends, increasing population, and higher rates of household formation. The rising need for budget-friendly and mid-tier housing alternatives in major urban areas such as Bangkok, Chiang Mai, and Pattaya is propelling residential building and transactions. Young professionals and expatriates are on the lookout for apartments, condominiums, and townhouses, stimulating the growth of both high-rise and low-rise developments. Policies from the government that encourage home ownership, ease of obtaining mortgages, and housing incentives boost demand even more. Furthermore, enhancements in infrastructure, such as transportation systems and city facilities, increase the appeal of housing regions. These elements together guarantee that residential real estate continues to be the biggest and most vibrant sector in Thailand.

The growing desire for contemporary, safe, and convenience-focused homes is boosting the need for residential real estate throughout Thailand. Evolving lifestyles, such as smaller families and an increasing count of solo inhabitants, are prompting developers to prioritize compact, practical, and feature-rich housing options. The demand from international buyers and retirees is also fostering the expansion of upscale condominiums and serviced apartments. In line with this trend, in 2024, Eden Estate, collaborating with MQDC, introduced “Eden Ekkamai,” an exclusive, low-density residential development in central Bangkok offering a limited number of units and premium amenities. These advancements emphasize the increasing desire for unique, thoughtfully designed living spaces, underscoring the ongoing growth of Thailand’s residential property market.

Business Insights:

Access the comprehensive market breakdown Request Sample

- Sales

- Rental

Sales exhibit a clear dominance with a 69.9% share of the total Thailand real estate market in 2025.

Sales represent the largest segment because of the robust demand for residential and commercial properties, leading to high transaction volumes and substantial revenue generation. Real estate firms, agents, and builders actively participate in property promotion, client recruitment, and deal finalization, boosting overall business expansion. The existence of structured sales channels, such as online platforms, property expos, and specialized sales offices, improves visibility and access for prospective buyers and investors. Moreover, competitive pricing tactics, adaptable payment options, and promotional deals encourage property buying. The increasing interest from local purchasers, expatriates, and international investors fuels strong sales results, guaranteeing that real estate dealings continue to be the main business driver in Thailand.

The efficiency of sales operations in Thailand’s real estate sector is enhanced by the use of digital tools, customer relationship management systems, and focused marketing campaigns. Developers and brokers utilize online listings, virtual tours of properties, and social media interactions to draw in potential clients, reducing the sales cycle and boosting conversion rates. Collaborative alliances among developers, banks, and real estate firms enable financial solutions, improving affordability and buyer trust. Additionally, governmental policies that encourage foreign property ownership and provide investment incentives in real estate boost demand, directly influencing revenue generated from sales. As a result, effective and forward-thinking sales strategies remain at the forefront of business operations, establishing sales as the primary force in Thailand’s real estate sector.

Mode Insights:

- Online

- Offline

Offline leads with a market share of 72.8% of the total Thailand real estate market in 2025.

Offline dominates the market owing to the traditional preference of buyers and investors for direct, in-person property interactions. Many clients value physical site visits, face-to-face consultations, and personalized guidance when making high-value property decisions. Real estate developers and brokers organize property exhibitions, open houses, and on-site tours to showcase residential, commercial, and mixed-use developments, enhancing trust and transparency. Local buyers often prefer interacting with sales representatives and reviewing documents personally, while foreign investors rely on local agents for guidance. Additionally, offline channels allow negotiation flexibility, immediate clarification of legal and financial details, and stronger relationship building, sustaining their dominance as the primary mode of transaction in Thailand’s real estate market.

The continued reliance on offline methods is reinforced by the growing complexity and customization of real estate offerings in Thailand. Buyers and tenants prefer to experience property layouts, amenities, and neighborhood features directly, ensuring informed investment decisions. Developers utilize offline channels to provide comprehensive brochures, physical models, and immersive presentations that digital platforms cannot fully replicate. Networking events, real estate fairs, and community outreach programs further strengthen offline engagement, facilitating long-term client relationships. Moreover, legal and regulatory processes often necessitate in-person document verification and signing. As a result, offline interactions remain critical for trust, convenience, and effective deal closure, making them the leading mode in Thailand’s real estate market.

Regional Insights:

- Bangkok

- Eastern

- Northeastern

- Southern

- Northern

- Others

Bangkok dominates with a market share of 52.3% of the total Thailand real estate market in 2025.

Bangkok leads the market due to its status as the nation's economic, political, and cultural center. The city draws considerable domestic and international investment in residential, commercial, and mixed-use developments. The growth of condominiums, apartments, and townhouses is fueled by high population density, swift urbanization, and rising demand for contemporary housing. Bangkok's advanced infrastructure, featuring transportation systems, airports, and commercial areas, boosts connectivity and accessibility, establishing it as a favored site for real estate investment. Moreover, the existence of multinational companies, financial entities, and retail centers generates significant demand for office spaces and commercial real estate, further reinforcing Bangkok’s leading role in Thailand’s property market.

Bangkok's supremacy is further strengthened by the high demand from expatriates, retirees, and affluent professionals looking for upscale residential and mixed-use projects. Government backing for urban development, tourism, and international investment remains appealing to buyers and investors, motivating developers to launch comprehensive projects that merge residential, commercial, and lifestyle components. In line with this trend, One Bangkok, a significant mixed-use project by TCC Assets and Frasers Property, progressed toward its 2024, opening, combining offices, hotels, residences, and retail spaces while incorporating sustainability elements and green spaces. These advancements improve urban living conditions and strengthen Bangkok’s status as a top real estate market.

Market Dynamics:

Growth Drivers:

Why is the Thailand Real Estate Market Growing?

Increasing Use of Real Estate Investment Trusts for Capital Expansion

The adoption of real estate investment trusts (REITs) is emerging as a key factor influencing the Thailand real estate market as companies seek to unlock asset value and secure funding for expansion. REIT structures enable developers and hospitality groups to monetize existing assets while attracting institutional investors and improving capital efficiency. This approach supports portfolio diversification and long-term growth in the real estate sector. Reflecting this trend, in 2025, Onyx Hospitality Group announced plans to launch a leasehold REIT backed by four hospitality properties in Thailand. The initiative highlights how real estate firms are utilizing financial instruments to support expansion strategies and strengthen investment flows within the country’s growing hospitality and property markets.

Expansion of Affordable Housing Linked to Transit-Oriented Development

The development of affordable housing integrated with transportation infrastructure is becoming an important factor in Thailand’s real estate market. Developers and government institutions are focusing on improving housing accessibility for low- and middle-income populations while enhancing connectivity to urban centers. Transit-oriented developments are enabling residents to access employment hubs, services, and amenities more efficiently. Reflecting this trend, in 2026, BTS Group launched the “Baan Chao Thai” project in partnership with the Government Housing Bank to expand affordable housing near transit hubs. The initiative offers flexible financing options and low entry costs, highlighting the growing focus on inclusive housing solutions and supporting demand in Thailand’s affordable real estate segment.

Shift Toward Experiential and Wellness-Centric Real Estate Concepts

The growing emphasis on well-being and experiential living is influencing the design and development of real estate projects across Thailand. Developers are incorporating elements that promote mental wellness, social interaction, and lifestyle engagement within commercial and mixed-use spaces. These concepts enhance user experience and create differentiated environments that attract urban consumers. Reflecting this trend, in 2024, Frasers Property Thailand launched the “Grown-up Playground” at Samyan Mitrtown during Bangkok Design Week, featuring interactive spaces designed to support creativity and emotional engagement. This approach demonstrates how developers are redefining real estate as experiential environments, strengthening community engagement and supporting the evolution of lifestyle-oriented developments in Thailand.

Market Restraints:

What Challenges the Thailand Real Estate Market is Facing?

High Household Debt Constraining Buyer Mortgage Accessibility

Elevated household debt across Thailand's population significantly constrains prospective buyers' ability to secure mortgage financing. Financial institutions have tightened credit criteria in response to non-performing loan concerns, resulting in elevated mortgage rejection rates particularly in lower price categories. This credit barrier restricts first-time and middle-income buyer participation, suppressing transaction volumes and limiting residential market expansion across key segments.

Oversupply in Urban Condominium Markets

Concentrated condominium development in Bangkok has created localized oversupply conditions, particularly in the mid-market segment where unsold inventory has accumulated over successive development cycles. The mismatch between developer supply projections and actual buyer absorption capacity has resulted in prolonged sales periods, price discounting, and promotional incentives that compress developer margins. This oversupply dynamic discourages new project launches and creates uncertainty for investors anticipating capital appreciation returns.

Rising Construction Costs and Labor Shortages

Escalating construction costs, including land acquisition in prime locations, building materials, and labor wages, are squeezing developer margins and constraining the viability of new project launches. Structural labor shortages within Thailand's construction sector, driven by aging workforce demographics and competition from industrial employers, create delivery delays and quality complications. These pressures compel developers toward higher price segments, reducing the supply and affordability of mid-market housing for prospective buyers.

Competitive Landscape:

Thailand's real estate market features a moderately competitive landscape characterized by a diverse mix of established domestic property developers, international real estate conglomerates, and regional investors operating across residential, commercial, industrial, and hospitality asset classes. Domestic developers with strong brand recognition compete intensely in Bangkok and the Eastern seaboard, leveraging established land banks and customer trust. International investors are increasingly targeting premium segments, including luxury condominiums, data centers, logistics facilities, and hospitality properties, attracted by Thailand's competitive cost structure. Market differentiation strategies center on product quality, location premium, design innovation, and sustainability credentials, with green-certified developments gaining preference. The competitive environment is further shaped by strategic land acquisition, joint ventures between Thai and international development entities, and portfolio repositioning initiatives among established players adapting to shifting consumer preferences throughout the forecast period.

Recent Developments:

- November 2025: IHG and CG Capital launched Bangkok’s first freehold branded residences in Sukhumvit, marking a major step in luxury real estate. The THB 5.5 Billion InterContinental Residences project reflects rising demand for premium, hotel-style living among global investors.

- October 2025: PROUD Real Estate launched its second InterContinental branded residences in Phuket, investing over THB 2.5 Billion in a luxury beachfront project at Kamala Beach. The development targeted high-end buyers with limited units, premium amenities, and integrated hotel services, reinforcing Phuket’s appeal as a luxury property destination.

Thailand Real Estate Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Properties Covered | Residential, Commercial, Industrial, Land |

| Businesses Covered | Sales, Rental |

| Modes Covered | Online, Offline |

| Regions Covered | Bangkok, Eastern, Northeastern, Southern, Northern, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Thailand Real Estate Market Report

The Thailand real estate market size was valued at USD 30.21 Billion in 2025.

The Thailand real estate market is expected to grow at a compound annual growth rate of 2.19% from 2026-2034 to reach USD 37.82 Billion by 2034.

Residential holds the largest market share at 51.3% in 2025, driven by strong housing demand, urbanization, and the expansion of transit-oriented residential developments across Thailand's major metropolitan areas.

Key factors driving the Thailand real estate market include the rising adoption of smart technologies and digital infrastructure to enhance building efficiency and tenant experience. In 2025, JLL launched Technology Advisory services in Thailand to support smart building adoption and digital transformation across real estate assets.

Major challenges include elevated household debt constraining mortgage accessibility, oversupply conditions in Bangkok's condominium segment, rising construction costs and labor shortages, weak domestic purchasing power in mid-market segments, and regulatory complexity for foreign property ownership structures.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)