Tissue Diagnostics Market Size, Share, Trends and Forecast by Product Type, Technology, Disease, End User, and Region, 2026-2034

Tissue Diagnostics Market Size and Share:

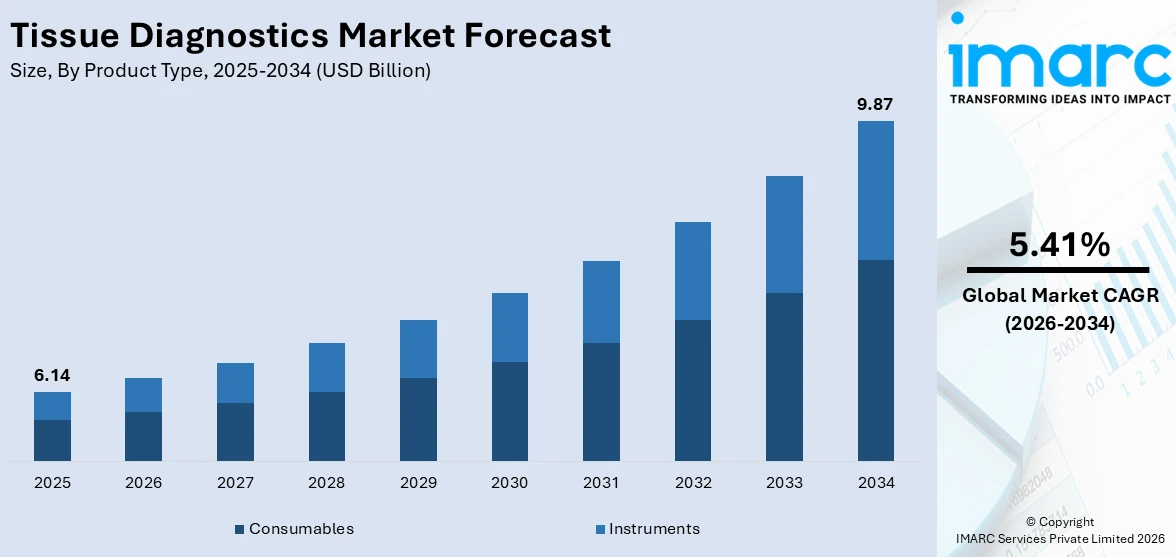

The global tissue diagnostics market size was valued at USD 6.14 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 9.87 Billion by 2034, exhibiting a CAGR of 5.41% from 2026-2034. North America currently dominates the market, holding a market share of 44.76%. The industry represents a critical healthcare component, enabling accurate disease detection and treatment planning through advanced histological and immunohistochemical analysis. This sector encompasses technologies and consumables facilitating precise cellular and molecular examination of tissue samples. Growing emphasis on personalized medicine, expanding cancer prevalence, and technological advancements in digital pathology reshape diagnostic capabilities worldwide. The industry evolves with innovations in automation, artificial intelligence, and workflow optimization, driving enhanced diagnostic accuracy and efficiency, contributing to expanding tissue diagnostics market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 6.14 Billion |

|

Market Forecast in 2034

|

USD 9.87 Billion |

| Market Growth Rate 2026-2034 | 5.41% |

The rising global cancer burden serves as a fundamental catalyst propelling the tissue diagnostics industry forward. As populations age and lifestyle factors contribute to increasing oncology cases worldwide, healthcare systems require sophisticated diagnostic capabilities to identify malignancies accurately and early. For instance, Roche recently secured FDA clearance for its VENTANA DP 600 high‑volume slide scanner, which significantly boosts its digital pathology capacity to scan hundreds of tissue slides and accelerate diagnosis. Tissue-based testing remains the definitive method for confirming cancer diagnoses, determining tumor characteristics, and guiding targeted therapy selection. The expanding understanding of tumor heterogeneity and molecular profiles necessitates comprehensive tissue analysis, driving demand for advanced diagnostic solutions. Healthcare providers increasingly recognize that precise tissue diagnostics enable better treatment stratification, reducing unnecessary interventions while ensuring appropriate therapeutic approaches. The growing adoption of precision oncology frameworks globally emphasizes the indispensable role of tissue analysis in modern cancer care. Furthermore, emerging biomarker discoveries and companion diagnostics development require robust tissue testing infrastructure, reinforcing the sector's essential position in contemporary healthcare delivery systems and fostering sustained expansion across diverse geographic markets and healthcare environments.

To get more information on this market Request Sample

Within the United States, which commands 84% of the North American landscape, substantial healthcare infrastructure investments and favorable reimbursement policies create a conducive environment for tissue diagnostics adoption. American healthcare institutions prioritize diagnostic accuracy and efficiency, driving adoption of cutting-edge technologies and comprehensive testing protocols. The robust regulatory framework ensures high quality standards while encouraging innovation in diagnostic methodologies. Academic medical centers and research institutions across the nation actively collaborate with diagnostic laboratories, fostering continuous improvement in tissue analysis techniques and workflow optimization. The emphasis on value-based care models incentivizes accurate initial diagnoses, positioning tissue diagnostics as cost-effective tools that prevent misdiagnosis and inappropriate treatments. Additionally, the concentration of pharmaceutical and biotechnology companies developing targeted therapies creates symbiotic relationships with diagnostic providers, as drug development increasingly depends on companion diagnostics requiring sophisticated tissue testing capabilities, thereby reinforcing market momentum and technological advancement within American healthcare systems.

Tissue Diagnostics Market Trends:

Digital Transformation and Artificial Intelligence Integration

The digital revolution is fundamentally transforming how pathologists analyze and interpret tissue samples, with artificial intelligence algorithms demonstrating remarkable capabilities in pattern recognition and diagnostic assistance. Digital pathology platforms enable remote consultations, facilitate collaborative reviews, and support continuous learning through extensive image databases. For example, PathAI recently received FDA 510(k) clearance for its AISight® Dx platform for primary clinical diagnosis, underscoring its readiness for real‑world pathology workflows. Machine learning models trained on vast datasets can identify subtle morphological features that might escape human observation, enhancing diagnostic consistency and accuracy. The integration of computational pathology with laboratory information systems streamlines workflows, reduces turnaround times, and minimizes administrative burdens on pathologists. These technological advances also enable quantitative analysis of biomarkers, providing objective measurements that support clinical decision-making. As validation studies demonstrate AI's clinical utility and regulatory pathways become clearer, adoption accelerates across academic centers and community hospitals. The convergence of imaging technologies, computational power, and algorithm sophistication represents a paradigm shift that promises to enhance diagnostic capabilities significantly while addressing pathologist workforce shortages globally.

Personalized Medicine and Biomarker-Driven Diagnostics

The shift toward personalized treatment approaches necessitates comprehensive molecular characterization of tissue samples, fundamentally influencing tissue diagnostics market trends and diagnostic requirements. Oncologists increasingly rely on biomarker profiles to select optimal therapies, predict treatment responses, and monitor disease progression. Immunohistochemistry and molecular testing panels have become standard components of tissue analysis protocols, revealing actionable genetic alterations and protein expressions that guide therapeutic decisions. The expanding repertoire of targeted therapies and immunotherapies demands corresponding diagnostic capabilities to identify suitable patient populations. Tissue-based testing provides the biological context necessary for interpreting genomic findings and understanding tumor microenvironments. Pathology laboratories continuously expand their testing menus to accommodate emerging biomarkers and evolving clinical guidelines. This trend drives investment in advanced instrumentation, specialized reagents, and technical expertise. As pharmaceutical companies develop novel targeted agents, companion diagnostic requirements multiply, creating sustained demand for sophisticated tissue analysis capabilities that bridge diagnostic insights with therapeutic interventions across multiple disease categories.

Workflow Automation and Laboratory Efficiency Enhancement

Laboratories face mounting pressure to process increasing tissue volumes while maintaining quality standards and controlling operational costs, driving adoption of automated solutions throughout the diagnostic workflow. Automated staining platforms ensure consistent reagent application and standardized protocols, reducing variability and improving reproducibility. For example, Roche’s VENTANA HE 600 system offers fully automated H&E staining on individual slides, helping labs maintain stain consistency and freeing staff from repetitive manual tasks. Robotic systems handle specimen processing, slide preparation, and coverslipping with precision and efficiency beyond manual capabilities. Track-and-trace technologies provide real-time visibility into specimen locations and processing status, minimizing misidentification risks and optimizing resource allocation. Integrated laboratory information systems coordinate activities across departments, eliminate redundant data entry, and generate comprehensive audit trails. These automation initiatives address workforce challenges by enabling technologists to focus on complex tasks requiring human expertise rather than repetitive manual procedures. As laboratories expand testing capabilities and accommodate higher throughput demands, automation becomes essential for maintaining rapid turnaround times without compromising diagnostic quality. The continuous evolution of automation technologies promises further efficiency gains and quality improvements across tissue diagnostic workflows.

Tissue Diagnostics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global tissue diagnostics market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, technology, disease, and end user.

Analysis by Product Type:

- Instruments

- Consumables

Consumables dominate the tissue diagnostics landscape with a commanding 59.2% share, reflecting the recurring revenue nature of reagents, antibodies, stains, and disposable supplies essential for routine laboratory operations. Every tissue sample requires multiple consumable items throughout the diagnostic process, from fixation and embedding through staining and coverslipping. The continuous demand for these materials creates stable revenue streams for suppliers while ensuring laboratories maintain adequate inventory levels to support uninterrupted operations. Antibody panels for immunohistochemistry represent particularly valuable consumable categories, as expanding biomarker testing requirements drive utilization across oncology and other specialties. Special stains, chromogenic detection systems, and mounting media constitute additional essential supplies that laboratories purchase regularly. Quality and consistency of consumable products directly impact diagnostic accuracy, encouraging laboratories to establish relationships with reliable suppliers. As testing volumes increase globally and molecular characterization becomes more comprehensive, consumable consumption rises proportionally. The segment benefits from technological advances that introduce improved reagent formulations and novel antibody specificities, sustaining tissue diagnostics market growth through continuous innovation.

Analysis by Technology:

- Immunohistochemistry

- In Situ Hybridization

- Digital Pathology and Workflow Management

- Special Staining

Digital pathology and workflow management technologies capture 30% of the market, representing the transformative impact of digitization on traditional microscopy-based diagnostics. Whole slide imaging scanners convert glass slides into high-resolution digital images accessible through sophisticated viewing software, enabling remote interpretation, collaborative consultations, and advanced image analysis. Workflow management systems integrate with laboratory information systems, tracking specimens from accessioning through reporting while optimizing resource allocation and reducing manual errors. These technologies address critical challenges including pathologist workforce shortages, geographic access disparities, and quality consistency requirements across distributed healthcare networks. Cloud-based platforms facilitate seamless image sharing between institutions, supporting tumor boards, second opinions, and expert consultations without physical slide transportation. The segment attracts significant investment as healthcare systems recognize digital pathology's potential to enhance diagnostic capabilities, improve operational efficiency, and enable artificial intelligence deployment. Regulatory approvals for primary diagnosis using digital images validate the technology's clinical reliability, accelerating adoption beyond academic centers into community hospitals and commercial laboratories seeking competitive advantages through technological modernization.

Analysis by Disease:

- Breast Cancer

- Gastric Cancer

- Lymphoma

- Prostate Cancer

- Non-Small Cell Lung Cancer

- Others

Breast cancer applications account for 50.66% of disease-specific tissue diagnostics utilization, reflecting both the malignancy's prevalence and the comprehensive testing protocols established through decades of clinical research. Breast tissue analysis requires multiple specialized techniques including histological grading, hormone receptor assessment, HER2 testing, and increasingly, proliferation marker evaluation. The well-established screening and diagnostic pathways for breast cancer ensure high biopsy volumes flowing through pathology laboratories globally. Treatment decisions depend critically on accurate tissue characterization, with receptor status directly determining therapeutic approaches including endocrine therapy and targeted antibody treatments. The heterogeneity of breast cancer necessitates thorough tissue evaluation to identify optimal treatment strategies for individual patients. Clinical guidelines mandate specific immunohistochemical testing panels, creating consistent demand for tissue diagnostic services. Additionally, breast cancer serves as a model disease for developing and validating novel diagnostic technologies, with innovations often piloted in breast pathology before expanding to other malignancies. The combination of high disease burden, established testing standards, and ongoing therapeutic advances sustains breast cancer's predominant position within tissue diagnostics applications.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Research Laboratories

- Pharmaceutical Companies

- Contract Research Organizations

- Others

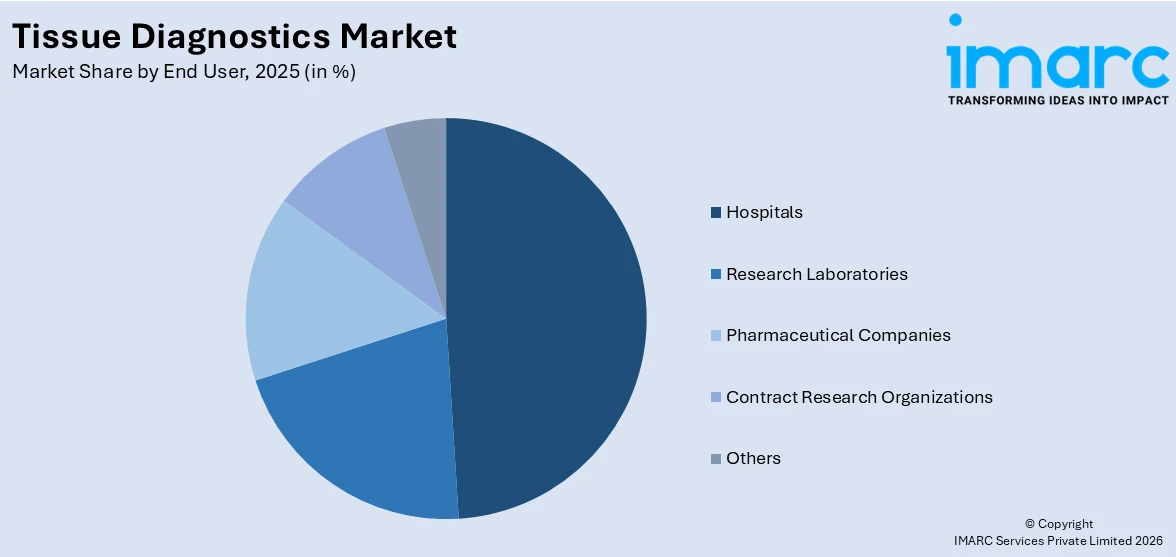

Hospitals constitute 49% of end-users, representing the primary venue where tissue diagnostics services are delivered through integrated pathology departments serving both inpatient and outpatient populations. Hospital-based laboratories benefit from proximity to clinical teams, enabling rapid communication regarding urgent cases, complex diagnostic questions, and multidisciplinary tumor boards. These facilities handle diverse specimen types spanning surgical resections, biopsies, and cytology samples across multiple specialties including oncology, gastroenterology, pulmonology, and dermatology. The breadth of services required in hospital settings drives investment in comprehensive diagnostic capabilities, advanced instrumentation, and specialized expertise. Academic medical centers within this segment also contribute to research initiatives, clinical trial support, and training programs that advance the field. Hospital laboratories often serve as reference centers for community providers requiring specialized testing or expert consultations. The integration of tissue diagnostics within hospital operations facilitates coordination of care, supports quality improvement initiatives, and enables efficient resource utilization. As hospitals adopt value-based care models and population health approaches, tissue diagnostics become essential tools for ensuring accurate diagnoses that guide appropriate therapeutic interventions.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

North America commands 44.76% of the regional distribution, reflecting the continent's advanced healthcare infrastructure, substantial research investments, and favorable reimbursement environment supporting sophisticated diagnostic services. The region benefits from concentrated pharmaceutical and biotechnology activity driving companion diagnostics development, clinical trial requirements, and continuous innovation in tissue analysis methodologies. Regulatory frameworks established by agencies provide clear pathways for new technology approvals while maintaining rigorous quality standards. Healthcare providers across the region prioritize diagnostic accuracy and adopt emerging technologies rapidly when clinical benefits are demonstrated. The presence of leading academic medical centers, reference laboratories, and specialized pathology practices creates a competitive environment fostering excellence and innovation. Additionally, awareness of precision medicine benefits among physicians and patients supports utilization of comprehensive tissue testing panels. The established laboratory infrastructure, trained workforce, and culture of technological adoption position North America as the predominant market. Ongoing investments in digital pathology, molecular diagnostics, and workflow automation sustain the region's leadership while addressing evolving healthcare needs.

Key Regional Takeaways:

United States Tissue Diagnostics Market Analysis

The United States represents the world's most developed tissue diagnostics market, characterized by extensive laboratory infrastructure, advanced technological adoption, and comprehensive reimbursement coverage facilitating access to sophisticated diagnostic services. American healthcare institutions invest heavily in pathology capabilities, recognizing tissue diagnostics as fundamental to quality patient care and clinical decision-making. The concentration of pharmaceutical companies developing targeted therapies creates robust demand for companion diagnostics requiring specialized tissue testing. Academic medical centers lead innovation through research collaborations, clinical trial support, and training programs that advance diagnostic methodologies. Commercial reference laboratories provide scalable testing solutions complementing hospital-based services. Regulatory pathways established by the FDA ensure rigorous validation of new technologies while supporting innovation. The emphasis on precision medicine across oncology and other specialties drives comprehensive molecular characterization of tissue samples. Digital pathology adoption accelerates as healthcare systems recognize benefits for remote consultations, workflow efficiency, and artificial intelligence integration. The mature market continues evolving through consolidation, technological advancement, and expanding test menus addressing emerging clinical needs across therapeutic areas.

Asia Pacific Tissue Diagnostics Market Analysis

The Asia Pacific region demonstrates rapid expansion in tissue diagnostics capabilities, driven by rising cancer incidence, expanding healthcare infrastructure, and increasing government investments in diagnostic services across diverse economies. Countries including Japan, China, Australia, South Korea, and India pursue distinct pathways toward diagnostic modernization, with Japan and Australia exhibiting advanced capabilities comparable to Western markets while emerging economies rapidly develop foundational infrastructure. Growing middle-class populations demand improved healthcare access, encouraging public and private sector investments in laboratory facilities and equipment. Medical tourism in certain countries creates opportunities for centers of excellence offering sophisticated diagnostic services. Regional variations in disease prevalence patterns influence testing priorities, with particular emphasis on gastric, liver, and lung cancers prevalent across Asia. Technology adoption accelerates as awareness of precision medicine benefits increases among healthcare providers and regulatory bodies establish approval frameworks. Digital pathology implementation addresses workforce shortages and geographic access challenges across vast territories. International collaborations facilitate knowledge transfer, training programs, and quality standardization initiatives. The dynamic landscape presents substantial opportunities as healthcare systems modernize and populations gain access to contemporary diagnostic capabilities.

Europe Tissue Diagnostics Market Analysis

Europe's tissue diagnostics market reflects diverse healthcare systems unified by strong regulatory frameworks, emphasis on evidence-based medicine, and commitment to quality standards exemplified by European Union directives and professional society guidelines. Countries including Germany, France, the United Kingdom, Italy, and Spain maintain sophisticated diagnostic infrastructure supporting comprehensive cancer care pathways. The region prioritizes healthcare accessibility through universal coverage models ensuring diagnostic services reach broad populations regardless of socioeconomic status. European pathology networks facilitate quality assurance programs, proficiency testing, and collaborative research advancing diagnostic methodologies. The in vitro diagnostic regulation provides rigorous oversight ensuring safety and performance standards while supporting innovation. Academic institutions across Europe contribute substantially to pathology research, biomarker discovery, and technology validation through well-designed clinical studies. Digital pathology adoption progresses steadily with several countries implementing national digital pathology programs addressing workforce challenges and geographic access needs. The emphasis on cost-effectiveness encourages efficient resource utilization and evidence-based test utilization. Regional variations in reimbursement policies and healthcare organization influence technology adoption rates, while overall commitment to diagnostic quality sustains market development and technological advancement.

Latin America Tissue Diagnostics Market Analysis

Latin America's tissue diagnostics landscape undergoes significant transformation as countries invest in healthcare infrastructure modernization and expand access to diagnostic services across urban and rural populations. Brazil, Mexico, Argentina, and Chile lead regional development with established pathology services in major metropolitan areas, while other nations progressively build diagnostic capabilities. Economic development and rising healthcare expenditures enable investments in modern laboratory equipment, quality reagents, and workforce training programs. Public health initiatives emphasizing cancer screening and early detection drive demand for tissue diagnostic services, particularly in breast, cervical, and prostate cancer applications. Private healthcare sectors in several countries offer advanced diagnostic capabilities attracting both domestic patients and medical tourists. Regulatory frameworks evolve to address quality standards and technology approvals, though implementation varies across jurisdictions. Partnerships with international organizations facilitate knowledge transfer, training programs, and quality improvement initiatives. Geographic and economic disparities create challenges in ensuring equitable access to sophisticated diagnostic services across diverse populations. Digital pathology presents opportunities for extending specialist expertise to underserved areas through teleconsultation capabilities. Market development continues as healthcare systems prioritize diagnostic infrastructure in pursuit of improved patient outcomes.

Middle East and Africa Tissue Diagnostics Market Analysis

The Middle East and Africa region exhibits substantial heterogeneity in tissue diagnostics capabilities, with Gulf Cooperation Council countries demonstrating advanced infrastructure and sophisticated services while many African nations face significant developmental challenges. Countries including the United Arab Emirates, Saudi Arabia, and South Africa invest heavily in healthcare infrastructure, establishing modern pathology laboratories equipped with contemporary technologies. Medical tourism in certain Gulf states drives creation of centers of excellence offering comprehensive diagnostic services meeting international standards. However, many African countries struggle with limited resources, workforce shortages, and inadequate laboratory infrastructure constraining diagnostic capabilities. International aid organizations and public health initiatives support capacity building through training programs, equipment donations, and quality improvement projects. Rising cancer burden across the region creates urgent demand for expanded diagnostic services, yet resource limitations impede rapid development. Digital pathology and telepathology offer potential solutions for addressing geographic disparities and specialist shortages by connecting remote facilities with expert consultants. Regional variations in disease patterns, including infectious disease burdens, influence diagnostic priorities and resource allocation. Market development progresses unevenly with concentrated advancement in specific countries while substantial populations lack access to basic diagnostic services, presenting both humanitarian needs and opportunities.

Competitive Landscape:

The competitive environment is characterized by diverse participants spanning multinational corporations, specialized diagnostics firms, and regional suppliers competing across technology platforms, consumable portfolios, and service models. Established entities leverage extensive product portfolios, global distribution networks, and substantial research capabilities to maintain market positions through continuous innovation and strategic acquisitions. Emerging participants focus on niche technologies including digital pathology platforms, artificial intelligence applications, and specialized reagent systems differentiated by performance characteristics or workflow integration capabilities. Competition intensifies around digital transformation with multiple vendors offering whole slide imaging solutions, image management systems, and computational pathology tools. Consumable suppliers compete primarily on product quality, antibody specificity, and technical support services that influence laboratory adoption decisions. Strategic partnerships between diagnostic companies and pharmaceutical firms advance companion diagnostics development, creating specialized testing requirements. The tissue diagnostics market forecast anticipates continued consolidation as larger entities acquire innovative technologies while maintaining competitive dynamics that drive ongoing advancement across the diagnostic landscape.

The report provides a comprehensive analysis of the competitive landscape in the tissue diagnostics market with detailed profiles of all major companies, including:

- Agilent Technologies, Inc.

- Becton, Dickinson and Company (BD)

- Bio SB

- BioGenex Laboratories

- F. Hoffmann-La Roche Ltd. (Roche Holding AG)

- Leica Biosystems Nussloch GmbH (Danaher Corporation)

- Merck KGaA

- Qiagen N.V.

- Sakura Finetek Japan Co., Ltd. (Sakura Seiki Co. Ltd.)

- Thermo Fisher Scientific Inc.

Latest News and Developments:

- In Nov 2025: Hologic’s Genius™ Digital Diagnostics System earned expanded CE‑marking in Europe, now enabling whole-slide imaging of tissue biopsies alongside cytology, unifying cell and tissue workflows on a single platform for labs.

- In Sep 2025: Roche highlights digital pathology + AI + companion diagnostics for tissue specimens. In Sep, Labcorp partnered with Roche to expand digital pathology access, underscoring scaling of tissue-diagnostics infrastructure.

Tissue Diagnostics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Instruments, Consumables |

| Technologies Covered | Immunohistochemistry, In Situ Hybridization, Digital Pathology and Workflow Management, Special Staining |

| Diseases Covered | Breast Cancer, Gastric Cancer, Lymphoma, Prostate Cancer, Non-Small Cell Lung Cancer, Others |

| End Users Covered | Hospitals, Research Laboratories, Pharmaceutical Companies, Contract Research Organizations, Others |

| Regions Covered | North America, Europe, Asia Pacific, Middle East and Africa, Latin America |

| Companies Covered | Agilent Technologies, Inc., Becton, Dickinson and Company (BD), Bio SB, BioGenex Laboratories, F. Hoffmann-La Roche Ltd. (Roche Holding AG), Leica Biosystems Nussloch GmbH (Danaher Corporation), Merck KGaA, Qiagen N.V., Sakura Finetek Japan Co., Ltd. (Sakura Seiki Co. Ltd.), Thermo Fisher Scientific Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the tissue diagnostics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global tissue diagnostics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the tissue diagnostics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Tissue Diagnostics Market Report

The tissue diagnostics market was valued at USD 6.14 Billion in 2025.

The tissue diagnostics market is projected to exhibit a CAGR of 5.41% during 2026-2034, reaching a value of USD 9.87 Billion by 2034.

Rising cancer incidence globally, expanding personalized medicine adoption, and technological innovations in digital pathology drive market expansion. Increasing emphasis on accurate disease characterization for targeted therapy selection, growing biomarker testing requirements, and healthcare infrastructure investments support sustained demand. Additionally, aging populations, improved screening programs, workforce automation needs, and regulatory support for novel diagnostics contribute to tissue diagnostics market outlook advancement.

North America currently dominates the tissue diagnostics market, accounting for a share of 44.76%. The region benefits from advanced healthcare infrastructure, substantial research investments, favorable reimbursement policies, and rapid technology adoption. Concentrated pharmaceutical activity, established regulatory frameworks, comprehensive laboratory networks, trained workforce availability, and strong emphasis on precision medicine position North America as the leading market for tissue diagnostic services.

Some of the major players in the tissue diagnostics market include Agilent Technologies, Inc., Becton, Dickinson and Company (BD), Bio SB, BioGenex Laboratories, F. Hoffmann-La Roche Ltd. (Roche Holding AG), Leica Biosystems Nussloch GmbH (Danaher Corporation), Merck KGaA, Qiagen N.V., Sakura Finetek Japan Co., Ltd. (Sakura Seiki Co. Ltd.), Thermo Fisher Scientific Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)