Tonometer Market Size, Share, Trends and Forecast by Type, Technology, Portability, End User, and Region, 2026-2034

Global Tonometer Market Size, Share, Trends & Forecast (2026-2034)

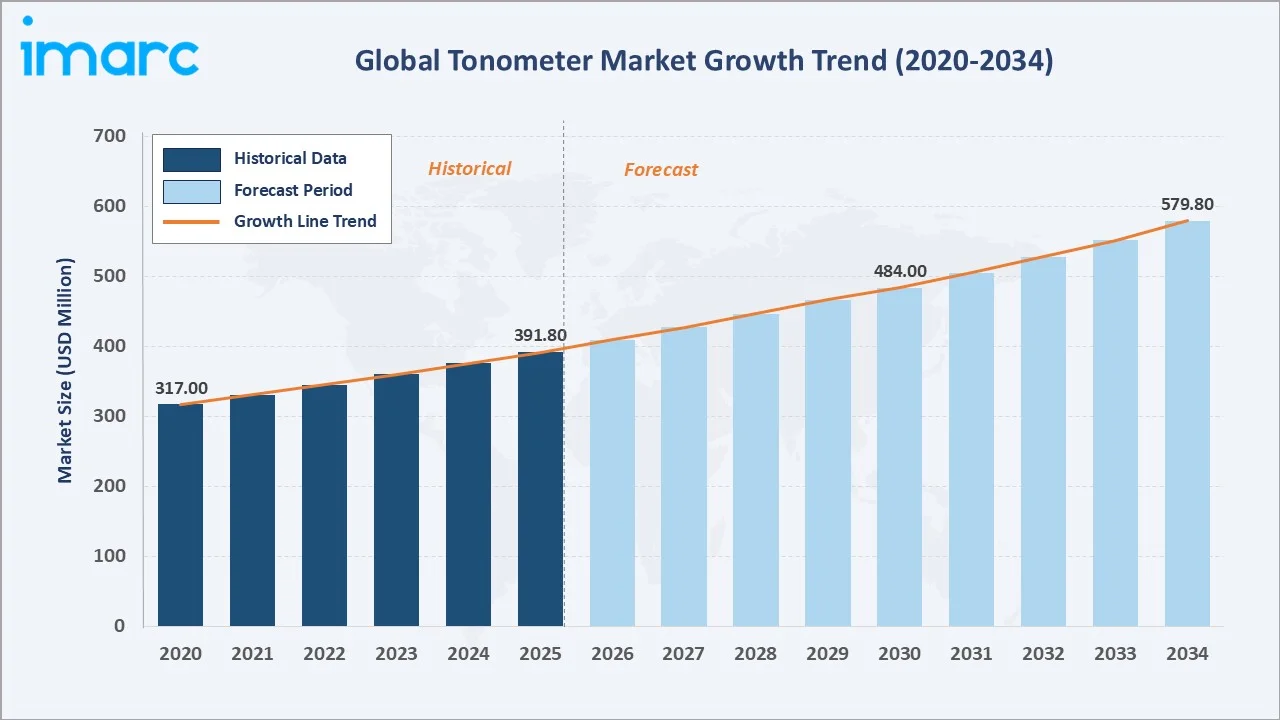

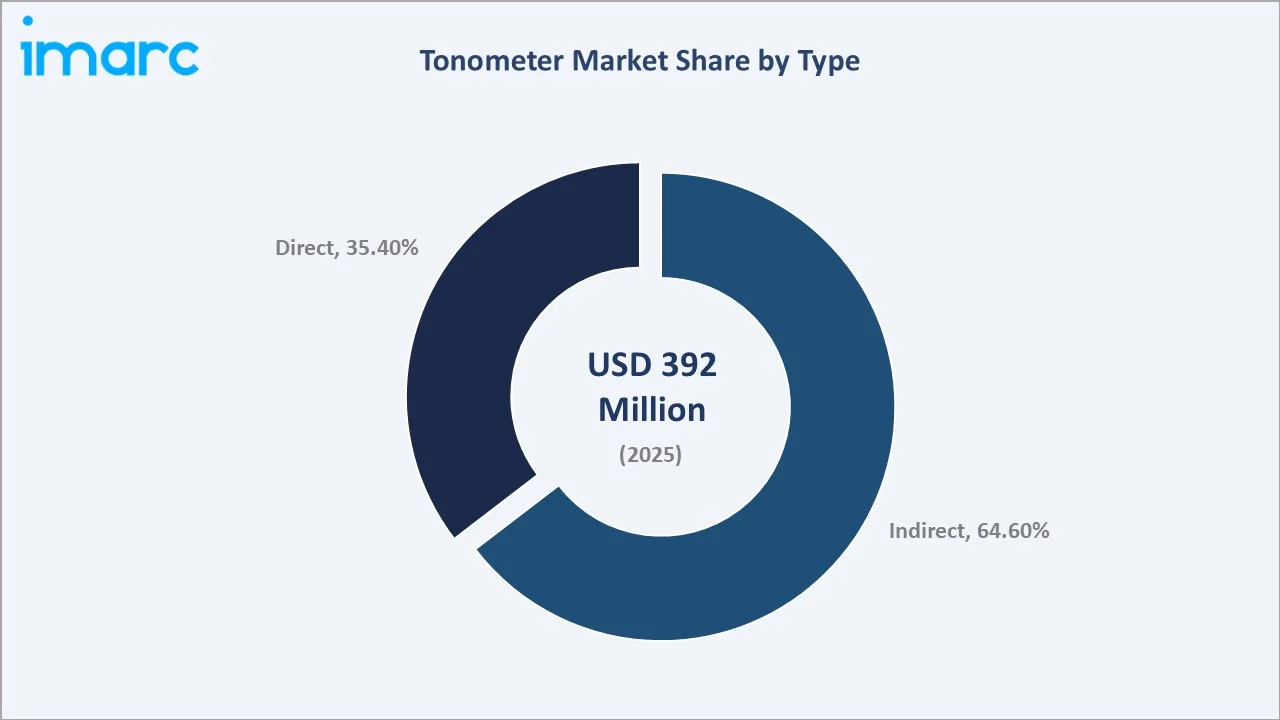

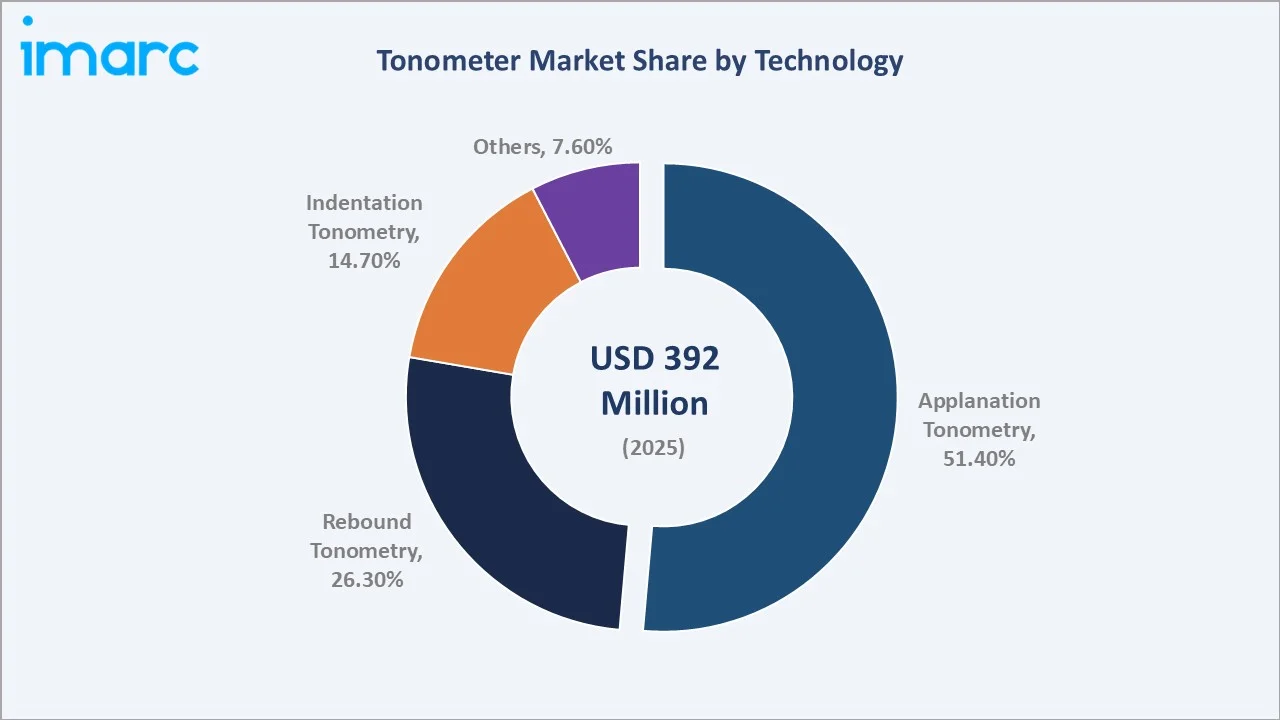

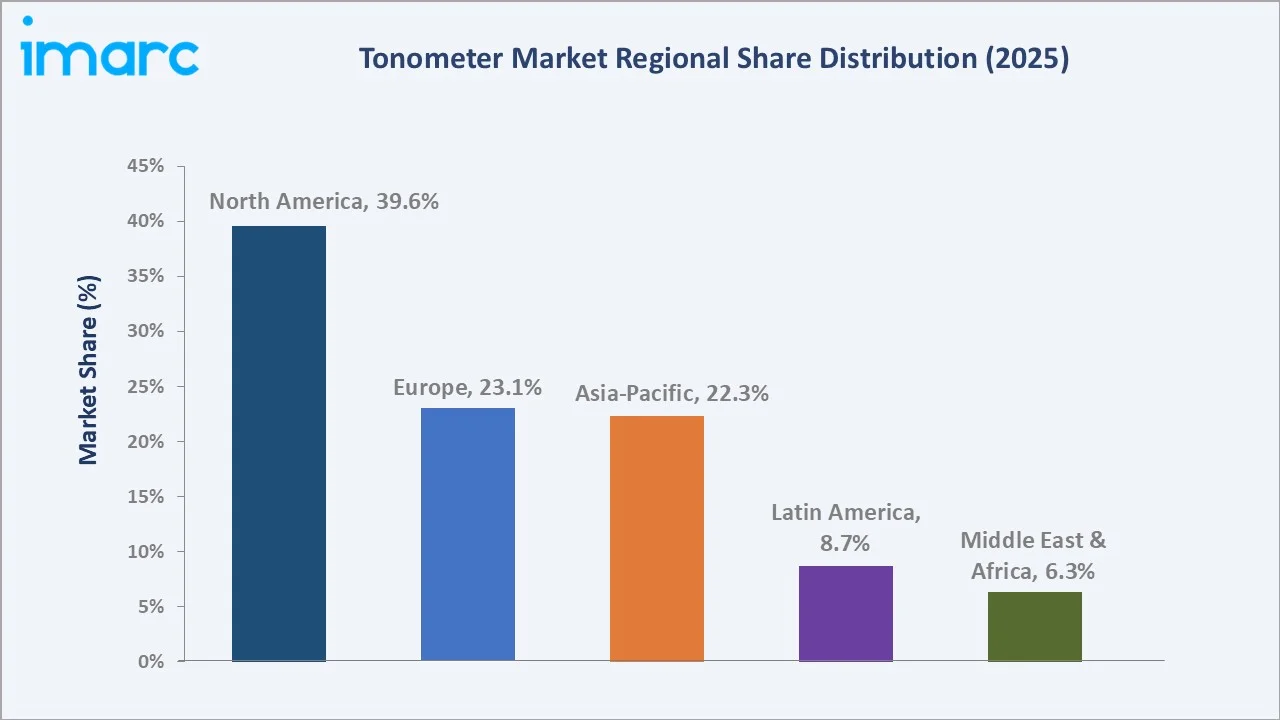

The global tonometer market size reached USD 391.8 Million in 2025. It is projected to reach USD 579.8 Million by 2034, at a CAGR of 4.3% during 2026-2034. Rising global glaucoma prevalence, affecting over 80 million people worldwide and is expected to exceed 110 million by 2040, aging demographics, and AI-integrated portable devices are the core demand drivers. Indirect tonometers lead at 64.6% share, while applanation technology dominates at 51.4%. North America holds the largest regional share at 39.6%, underpinned by strong reimbursement frameworks and widespread ophthalmic screening programs.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 391.8 Million |

|

Forecast Market Size (2034) |

USD 579.8 Million |

|

CAGR (2026-2034) |

4.3% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (39.6%, 2025) |

|

Fastest-Growing Region |

Asia-Pacific (~5.6% CAGR, 2026-2034) |

|

Leading Type |

Indirect Tonometry (64.6%, 2025) |

|

Leading Technology |

Applanation Tonometry (51.4%, 2025) |

The tonometer market growth from 2020 through 2034, expanded to USD 391.8 Million in 2025, and the forecast trajectory toward USD 579.8 Million reflects sustained clinical adoption and portable device expansion.

To get more information on this market, Request Sample

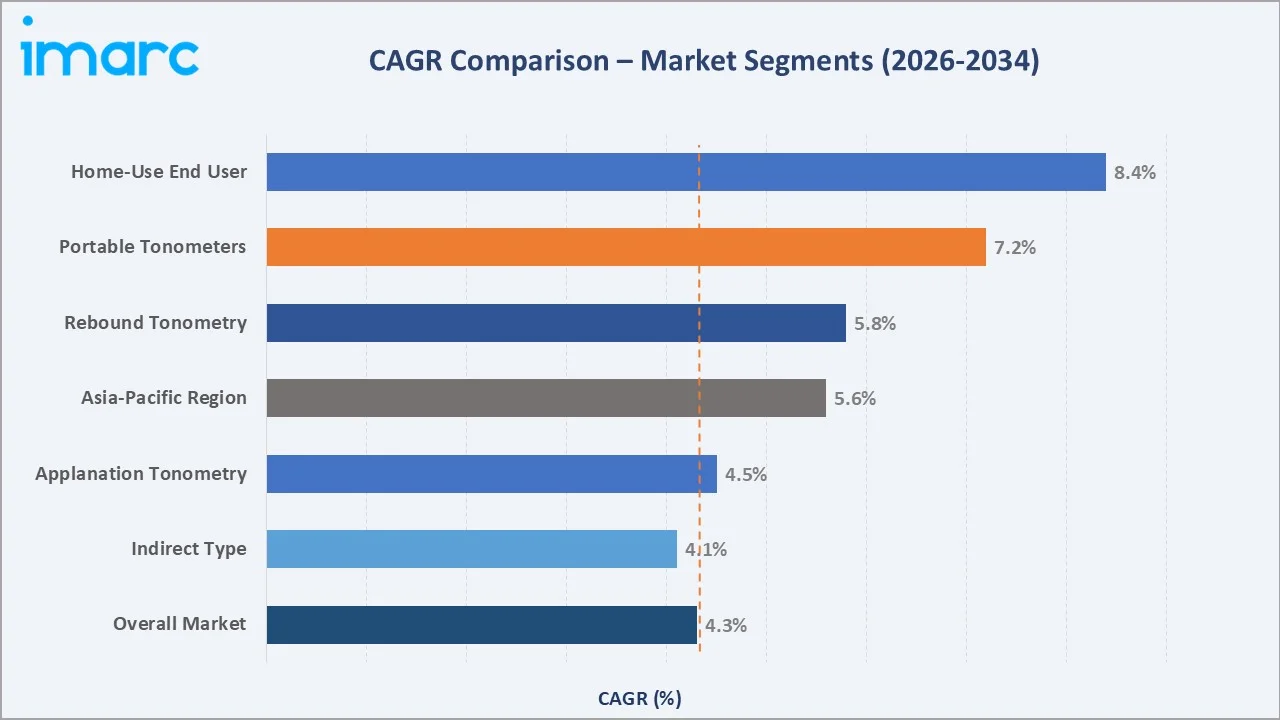

The CAGR across key segments with home-use end-user leads at ~8.4% and portable devices at ~7.2%, reflecting the shift toward decentralized, patient-convenient intraocular pressure (IOP) monitoring through 2034.

Executive Summary

The global tonometer market is expanding steadily, driven by a convergence of clinical necessity and device innovation. Glaucoma remains the leading cause of irreversible blindness globally with over 80 million individuals are estimated to be living with glaucoma. Regular IOP measurement is the primary diagnostic tool, making tonometers indispensable in ophthalmic practice.

Indirect tonometers command 64.6% of the 2025 type segment, as non-contact air-puff designs eliminate anesthesia requirements and reduce cross-contamination risk. Applanation tonometry, the clinical gold standard, holds 51.4% technology share. Rebound tonometry is the fastest-growing at ~5.8% CAGR, driven by iCare's handheld platforms gaining wide adoption in pediatric and home-care settings.

North America leads at 39.6% in 2025, supported by FDA-approved device pipelines, strong private insurance reimbursement, and high ophthalmologist density. Asia-Pacific at 22.3% is the fastest-growing region, fueled by expanding ophthalmic infrastructure in China, India, and Japan.

Key Market Insights

|

Insight |

Data / Finding |

|

Largest Type |

Indirect - 64.6% share (2025) |

|

Leading Technology |

Applanation Tonometry - 51.4% (2025) |

|

Leading Region |

North America - 39.6% (2025) |

|

Fastest-Growing Region |

Asia-Pacific - ~5.6% CAGR (2026-2034) |

Key Analytical Observations Aligned with the Above Data:

- Indirect tonometers, with 64.6% in 2025, dominate because non-contact designs remove anesthesia requirements, lowering procedural risk in high-throughput clinic settings. Non-contact tonometer from NIDEK (NT-1/1e, April 2023) reduces operator dependency and improve throughput.

- Applanation tonometry at 51.4% retains its dominance as the ISO-recognized clinical standard. Goldmann Applanation Tonometry (GAT) provides the reference against which all other methods are validated.

- North America's 39.6% leadership reflects the US Centers for Medicare & Medicaid Services (CMS) coverage of glaucoma screening for high-risk beneficiaries. Approximately 18,000 ophthalmologists practice in the US, creating a dense deployment base for slit-lamp-mounted and handheld tonometers.

Global Tonometer Market Overview

A tonometer is a medical device that measures intraocular pressure (IOP), the fluid pressure inside the eye. Elevated IOP is the primary modifiable risk factor for glaucoma, the world's leading cause of irreversible blindness. Devices span clinical slit-lamp-mounted gold-standard Goldmann tonometers, handheld portable rebound devices, and non-contact air-puff instruments.

Applications extend from hospital ophthalmology wards and ophthalmic clinics to mobile screening camps, telemedicine platforms, and emerging home-monitoring use cases. The majority of participants (88%) were able to use the tonometer independently. Most felt confident in using the home tonometer (94%), with proficiency generally reached by the third day of use.

Market Dynamics

To evaluate market opportunities, Request Sample

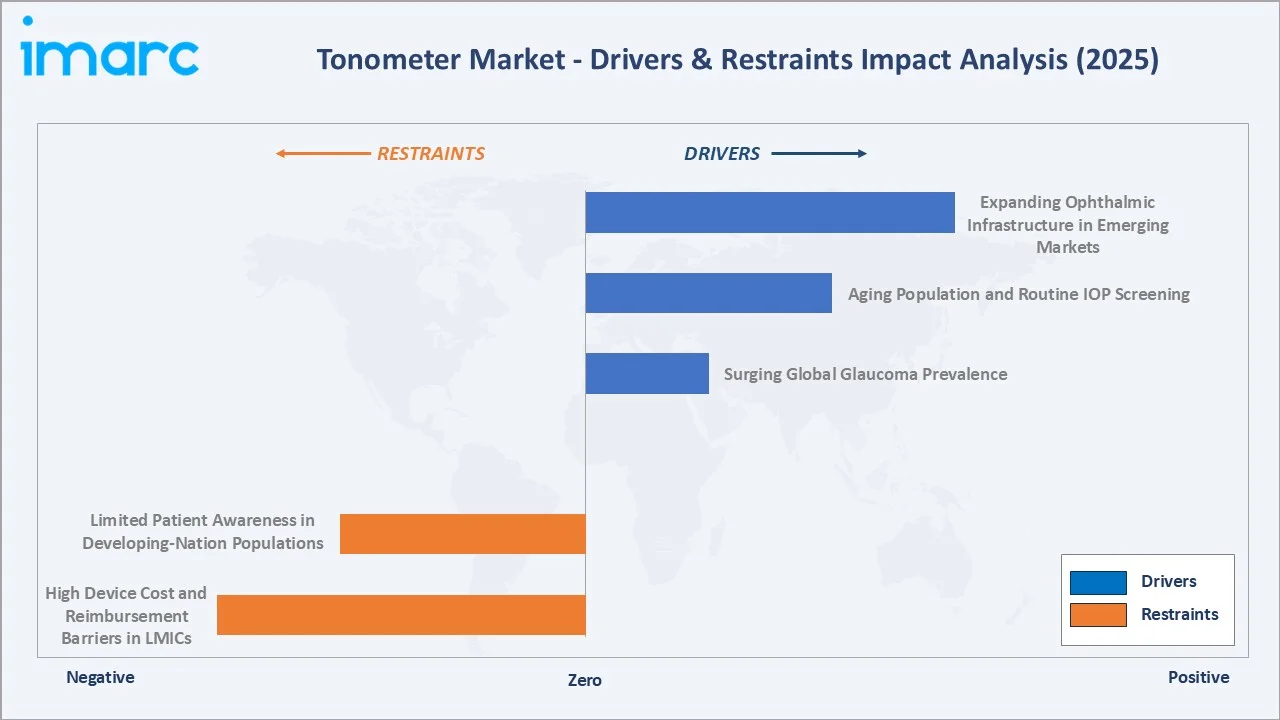

Market Drivers

- Surging Global Glaucoma Prevalence: The global glaucoma cases to rise from 80 million to 110 million by 2040, with more cases undiagnosed in developing economies.

- Aging Population and Routine IOP Screening: The global population aged 60+ is expected to reach 2.1 billion by 2050. Age is the strongest independent risk factor for elevated IOP and primary open-angle glaucoma.

- Expanding Ophthalmic Infrastructure in Emerging Markets: The National Blindness Control Program& Visual Impairment in India, China's Healthy China 2030 vision care targets, and WHO's VISION 2020 successors are collectively driving government procurement of tonometers for district-level eye care facilities.

Market Restraints

- High Device Cost and Reimbursement Barriers in LMICs: In Sub-Saharan Africa, South Asia, and parts of Southeast Asia, inadequate reimbursement structures limit procurement to donor-funded programmes, constraining market penetration in the world's highest-glaucoma-burden geographies.

- Limited Patient Awareness in Developing-Nation Populations: In much of Africa, only about 1 in 20 individuals with glaucoma are aware of their condition, and more than 50% are already blind in one eye when they seek help. Low disease awareness reduces the demand pull for IOP screening services that would otherwise drive tonometer procurement at primary care level.

Market Opportunities

- Portable and Wearable IOP Monitoring for Home Care: The home tonometry market represents the fastest-expanding opportunity. iCare HOME2, cleared by the FDA in 2022, enables patients with glaucoma to measure their own IOP at home without assistance.

- AI Predictive Analytics for Glaucoma Risk Stratification: Machine learning models trained on longitudinal IOP datasets, combined with OCT disc imaging, can predict glaucomatous visual field progression 3-5 years ahead of onset.

- Government Vision Screening Programmes in Asia-Pacific: India's Ayushman Bharat health programme covers glaucoma screening in April 2022. These policy-backed institutional procurement programmes create predictable, volume-significant tonometer demand through 2028.

Market Challenges

- Calibration Maintenance and Quality Assurance Costs: In resource-constrained settings, calibration equipment unavailability leads to progressive measurement drift that clinicians may not detect, creating both patient safety and regulatory compliance challenges for device maintenance programme operators.

- Competition from Integrated Multi-Function Diagnostic Platforms: Ophthalmic diagnostic platforms integrating OCT, corneal topography, pachymetry, and tonometry in a single device are gaining adoption in tertiary centers.

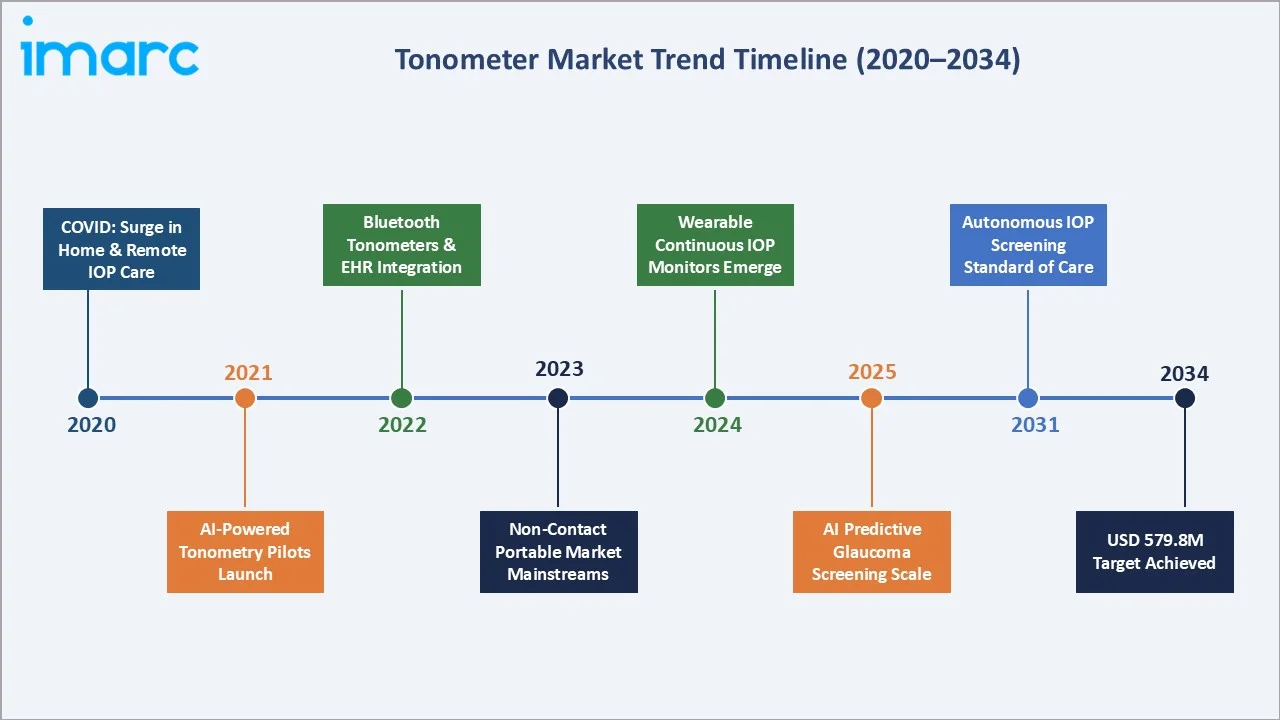

Emerging Market Trends

1. AI-Powered Diagnostic Integration Redefining Tonometry

In May 2024, Topcon Healthcare and Microsoft announced a collaboration to develop AI-driven 'Healthcare from the Eye' solutions on Azure cloud. AI algorithms analyze IOP data alongside retinal imaging to detect systemic conditions including hypertension, diabetes, and neurological disorders.

2. Rebound Tonometers Entering Home and Primary Care

Reichert's Tono-Vera’s US launch in May 2024 features the patented ActiView positioning system proving Refined Rebound Tonometer Experience with Bluetooth connectivity for real-time IOP data transmission. Eliminating anesthesia and disposable probes makes home rebound tonometry both clinically practical and commercially viable.

3. Non-Contact Tonometers Automating Routine Screening

NIDEK's NT-1/1e launched in April 2023 eliminates pachymetry to reduce workflow complexity, offering automated IOP measurement with voice guidance and patient safety features. Non-contact platforms are reducing the operator skill threshold for routine screening, enabling deployment to optometry and primary care settings outside specialist ophthalmology.

4. EHR and Telemedicine Platform Integration

Bluetooth and Wi-Fi-enabled tonometers are increasingly integrated with EHR systems. IOP data captured during routine consultations auto-populates glaucoma monitoring templates, supporting longitudinal trend analysis and clinical decision alerts when IOP exceeds individualized target thresholds.

5. Wearable Continuous IOP Monitoring Research Advancing

Continuous IOP monitoring using contact lens-embedded sensors measures 24-hour IOP fluctuation patterns that single clinic-based measurements cannot capture. Commercial wearable continuous IOP monitors are projected to reach early-adopter specialist markets by 2027-2029, expanding the addressable tonometry market into a new continuous-monitoring category.

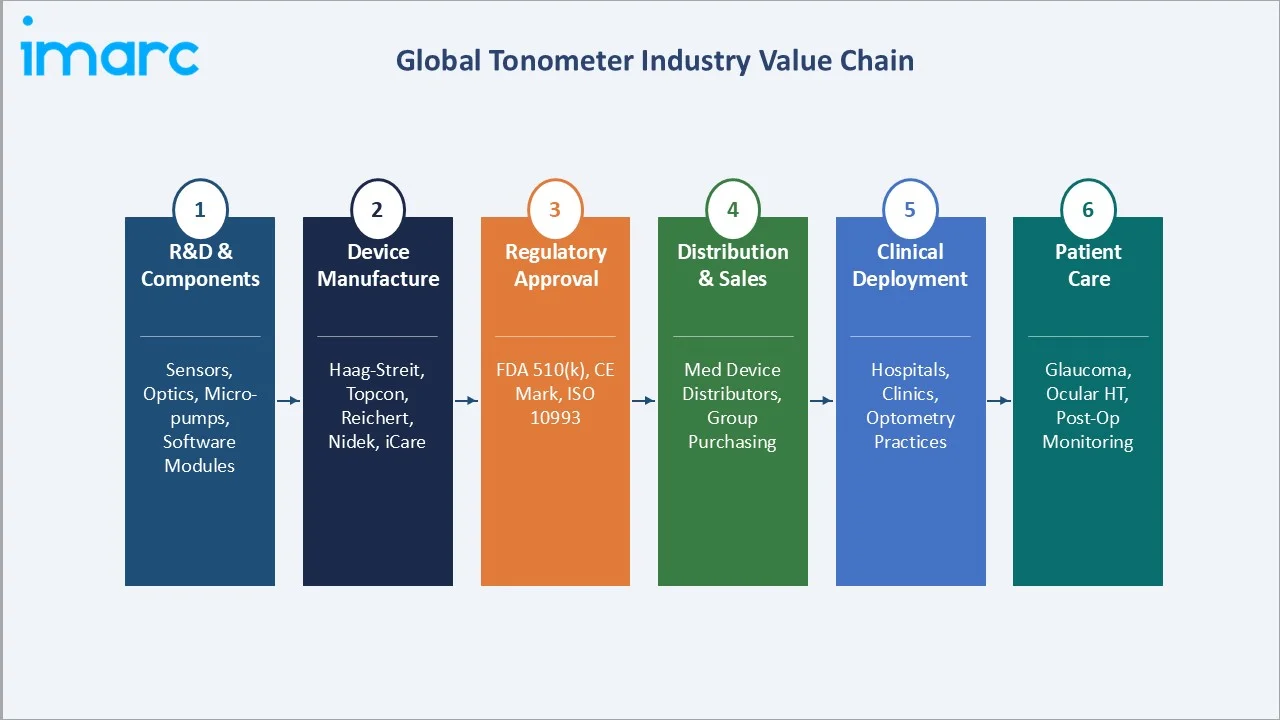

Industry Value Chain Analysis

The tonometer value chain spans six stages. Device manufacturers and regulatory compliance represent the highest fixed cost stages, while distribution and clinical service create the highest recurring revenue opportunities.

|

Stage |

Key Players / Examples |

|

R&D & Components |

Precision optics (Edmund Optics), MEMS sensors (Murata), micro-pneumatic pumps (Parker Hannifin), AI software modules |

|

Device Manufacturing |

Haag-Streit, Topcon, NIDEK, Reichert, iCare, Keeler, Marco, Tomey |

|

Regulatory Approval |

FDA 510(k) (US), CE Marking + ISO 10939 (EU), CDSCO Class C (India), PMDA (Japan), TGA (Australia) |

|

Distribution & Sales |

Henry Schein Medical, Patterson Companies, Medline Industries, specialist ophthalmic distributors, direct OEM sales |

|

Clinical Deployment |

Tertiary hospitals, ophthalmic specialty clinics, community eye care centers, telemedicine platforms, optometry practices |

|

Patient Care |

Glaucoma patients, ocular hypertension patients, post-surgical IOP monitoring, diabetic eye disease screening, home self-monitoring |

Distribution captures an estimated 18-22% gross margin through exclusive dealer arrangements in hospital group purchasing. iCare’s direct-to-patient home tonometry model, bypassing traditional distribution through physician-prescribed self-monitoring kits, represents a margin-enhancing DTC channel evolution that established OEMs are beginning to replicate.

Technology Landscape in the Tonometer Industry

Applanation Technology: The Clinical Gold Standard

Goldmann Applanation Tonometry, measuring the force required to flatten a standard 3.06 mm corneal area, remains the reference standard against which all other modalities are calibrated. Digital applanation systems now embed electronic force transducers that eliminate subjective mire endpoint interpretation, achieving repeatability in clinical validation studies.

Rebound Tonometry: Enabling Patient Self-Monitoring

Rebound tonometry, firing a magnetized probe at the corneal surface and measuring deceleration, requires no anesthesia or fluorescein. iCare's HOME2 platform, cleared by the FDA, allows patients to self-measure IOP at home with results of the Goldmann reference.

AI and Connectivity: Next-Generation Tonometry

Machine learning algorithms applied to longitudinal IOP datasets are enabling predictive glaucoma progression modelling. Topcon's partnership with Microsoft Azure demonstrates the commercial trajectory. Cloud-native tonometry platforms generating persistent longitudinal IOP profiles represent the market's highest-value software layer through 2034.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Indirect |

🔒 |

2025 |

|

Technology |

Applanation Tonometry |

51.4% |

2025 |

|

Portability |

Handheld |

72.2% |

2025 |

| End User | Ophthalmic Centers | 62.0% | 2025 |

|

Region |

North America |

39.6% |

2025 |

By Type

Indirect tonometers, non-contact air-puff and rebound designs that measure IOP without touching the cornea, command 64.6% in 2025. They eliminate anesthesia, reduce infection risk, and are faster to administer, enabling higher patient throughput in ophthalmic screening settings. NIDEK NT-1/1e and Topcon CT-1P represent the premium non-contact segment offering automated measurement with safety features for challenging patient groups.

To access detailed market analysis, Request Sample

Direct tonometers, including Goldmann applanation, Tonopen, and iCare handheld rebound devices, hold 35.4% in 2025. Despite a lower overall share, this segment commands the highest average selling prices. Direct tonometers are irreplaceable in tertiary clinical settings where reference-standard IOP measurements are legally and clinically mandated for glaucoma diagnosis and medico-legal documentation.

By Technology

Applanation tonometry at 51.4% retains its dominant position. Goldmann applanation remains the required comparison method in all clinical device validation studies, effectively mandating its continued presence in any ophthalmic center where new tonometer technologies are evaluated.

Rebound tonometry at 26.3% (2025) is the fastest-growing technology. The no-touch, no-anesthesia user experience drives adoption in pediatric ophthalmology, veterinary practice, and patient home-monitoring, three segments where contact techniques are impractical. Indentation tonometry (14.7%), represented by Schiotz instruments, serves resource-limited settings where low device cost outweighs measurement precision limitations. The others category (7.6%) includes ocular response analyzer (ORA), dynamic contour tonometry (DCT), and emerging wearable IOP sensor technologies in clinical validation.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers |

|

North America |

39.6% |

CMS glaucoma screening coverage; FDA 510(k) pipeline; 18,000 US ophthalmologists; high reimbursement |

|

Europe |

23.1% |

EGS guidelines mandating GAT; Haag-Streit Swiss HQ; CE/ISO-compliant device ecosystem; NHS screening |

|

Asia-Pacific |

22.3% |

China 14th Five-Year Eye Health Plan; India NPCB; aging Japan population; growing optometry sector |

|

Latin America |

8.7% |

Brazil SUS public eye care expansion; Mexico glaucoma awareness programs; regional distributor growth |

|

Middle East & Africa |

6.3% |

UAE and Saudi Vision 2030 health goals; WHO VISION programme; donor-funded rural eye camps |

North America commands 39.6% in 2025 through a combination of structural healthcare demand and strong commercial ecosystems. The US CMS covers annual glaucoma screening for high-risk Medicare beneficiaries, those with diabetes mellitus, a family history of glaucoma, African American heritage over age 50, or Hispanic heritage over age 65, directly driving clinic-level tonometer procurement.

Asia-Pacific at 22.3% (2025) is growing at the fastest rate, driven by three concurrent forces. Japan's aging population, 29.4% of citizens are aged 65+, generates the highest per-capita glaucoma diagnostic demand in the Asia-Pacific region. Europe (23.1%) benefits from the European Glaucoma Society's standardized care guidelines mandating Goldmann applanation as the preferred IOP measurement modality for all clinical glaucoma diagnoses, sustaining consistent slit-lamp-mounted applanation tonometer procurement across the EU's ophthalmology practices.

Competitive Landscape

The global tonometer market is moderately consolidated. The market bifurcates between premium clinical platforms and accessible portable innovators.

|

Company Name |

Key Brand/Products |

Market Position |

Core Strength |

|

Haag-Streit Group |

Applanation Tonometer 900 & 870, Tonosafe, Perkins MK3 |

Leader |

Tonometry, eye pressure measurement, diagnostic tools |

|

Topcon Corporation |

CT-80 and OMNIA |

Leader |

Ophthalmic equipment, portable tonometers, refractors |

|

Reichert Technologies (Ametek) |

Tono-Vera Tonometer, Tono-Pen AVIA Tonometer, CT210 Contact Tonometer |

Leader |

Digital tonometry, diagnostic instruments for eye care |

|

NIDEK CO. LTD. |

NT-1 / NT-1e Non-Contact Tonometer and Auto Ref/Kerato/Tono/Pachymeter TONOREF III |

Leader |

Ophthalmic equipment, auto tonometry, refractive systems |

|

iCare Finland Oy |

iCare HOME2 and iCare ST500 |

Challenger |

Portable tonometry, eye pressure measurement solutions |

|

Keeler |

PachPen Handheld Pachymeter, TonoCare, Pulsair Desktop Tonometer, AccuPen Handheld Tonometer, Pulsair intelliPuff Tonometer, KAT (R-Type) applanation tonometer, KAT (T-Type) applanation tonometer, KAT (Z-Type) applanation tonometer, D-KAT (R-Type) Digital Keeler Applanation Tonometer, D-KAT (T-Type) Digital Keeler Applanation Tonometer |

Challenger |

Portable tonometers, handheld eye pressure measurement tools |

|

Tomey Corporation |

FT-1000 Non-Contact Tonometer |

Emerging |

Tonometers for ophthalmology, diagnostic and imaging tools |

|

Marco |

AT-8/9 Applanation Tonometers, NT-510 Non-Contact Tonometer, Tonoref II ARK with Tonometry |

Emerging |

Diagnostic tonometers for clinical and refractive care |

The competitive positioning across global market presence and strategic investment dimensions for 2025.

Key Company Profiles

Haag-Streit Group

Haag-Streit Group, headquartered in Koeniz, Switzerland, is the world's leading manufacturer of ophthalmic diagnostic equipment, with the Goldmann Applanation Tonometer as its flagship product.

- Product Portfolio: The company offers Applanation Tonometer 900 & 870, Tonosafe, Perkins MK3

- Recent Developments: In December 2024, Haag-Streit UK relaunched the Perkins Mk 3 hand-held applanation tonometer.

- Strategic Focus: Haag-Streit's strategy centers on maintaining applanation gold-standard clinical authority while digitizing its instruments to generate recurring software, calibration, and maintenance service revenue - transitioning from pure hardware to an instrument-plus-service model that improves margin retention and customer lock-in.

Topcon Corporation

Topcon Corporation, headquartered in Tokyo, Japan, is a global leader in precision ophthalmic diagnostic instruments. Topcon's tonometer portfolio spans non-contact automated platforms to combined fundus camera-tonometer systems.

- Product Portfolio: The company offers CT-80 and OMNIA tonometers.

- Recent Developments: In November 2025, Topcon announced the simultaneous FDA 510(k) clearance and U.S. commercial launch of OMNIA auto kerato-refracto tonometer.

- Strategic Focus: Topcon's strategy integrates AI and cloud connectivity into its hardware platforms, positioning the company to generate SaaS diagnostic platform revenue alongside device sales. The Microsoft collaboration specifically targets population health screening, where AI-augmented tonometry enables cost-efficient mass IOP screening without full specialist involvement.

Reichert Technologies (Ametek, Inc.)

Reichert Technologies, a subsidiary of Ametek, Inc., is headquartered in New York, and is the US market's leading tonometer manufacturer. Reichert's 7CR Auto Tonometer has been the top-selling non-contact tonometer in North America for over a decade.

- Product Portfolio: The company offers Tono-Vera Tonometer, Tono-Pen AVIA Tonometer, CT210 Contact Tonometer

- Recent Developments: In May 2024, Reichert Technologies announced the availability of Tono-Vera Tonometer with ActiView Positioning System in the United States.

- Strategic Focus: Reichert's strategy leverages its dominant US distribution network and brand authority to expand from institutional clinical platforms into the fast-growing portable and home-care segment - targeting both institutional outreach ophthalmology and the emerging patient self-monitoring market enabled by teleophthalmology reimbursement expansion.

iCare Finland Oy

iCare Finland Oy, a subsidiary of Revenio Group, is the global pioneer and market leader in home-use rebound tonometry. iCare's HOME and HOME2 platforms, cleared by the FDA and CE-marked, are the only rebound tonometers specifically designed for unsupervised patient self-monitoring.

- Product Portfolio: The company offers iCare ST500, iCare HOME2 tonometers.

- Recent Developments: In September 2024, iCare launched the iCare ST500, a slit-lamp-based tonometer that brings the features of iCare’s rebound tonometry technology into a modern design.

- Strategic Focus: iCare's strategy is to own the patient self-monitoring tonometry segment globally, building a recurring SaaS revenue model through iCare CLINIC platform subscriptions layered over hardware sales, while expanding clinical professional use of its platform in ophthalmic clinics and optometry practices as an anesthesia-free alternative to Goldmann for patient-comfort-sensitive examinations.

Market Concentration Analysis

The top 5 players collectively hold approximately 62-78% of global tonometer revenue in 2025. Haag-Streit and Topcon maintain structural dominance through deep hospital system relationships and clinical guideline alignment. The market's moderate concentration is challenged from below by iCare's differentiated home-care niche and from technology disruption by AI-integrated platform strategies from both Topcon and emerging medtech startups.

Private equity consolidation in ophthalmic diagnostics, exemplified by Ametek's Reichert ownership, is ongoing. Further consolidation among Tier 2 and Tier 3 players is expected between 2026 and 2030 as scale economics in AI software development favor larger, better-capitalized manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

Home-use tonometry at ~8.4% CAGR and portable clinical devices at ~7.2% CAGR are the two highest-return investment areas through 2034. Investment in FDA-cleared home rebound tonometer platforms with EHR connectivity and HIPAA-compliant cloud data storage captures both hardware and recurring SaaS revenue in the most-rapidly-expanding market sub-segment.

Emerging Markets

Asia-Pacific, at ~5.6% CAGR, is the highest-growth regional investment. Local assembly partnerships with Indian medical device manufacturers offer market access at competitive INR price points that imported premium devices cannot match for government tender volumes. China's 14th Five-Year Health Plan for county-level hospital ophthalmic diagnostics through 2025, creating government-tendered procurement opportunities for tonometer OEMs with established China distribution networks.

Venture and Strategic Investment Trends

Strategic M&A in tonometry, including Ametek's Reichert ownership and Revenio's iCare subsidiary structure, demonstrates private equity interest in medical device platforms with recurring consumables and software subscription revenue streams. The convergence of tonometry with AI and telemedicine creates an investable medtech category that commands 4-6x EV/Revenue valuations for companies with FDA-cleared home monitoring platforms and cloud data management capabilities.

Future Market Outlook (2026-2034)

The global tonometer market is projected to expand from USD 391.8 Million in 2025 to USD 579.8 Million by 2034 at a CAGR of 4.3%, adding USD 188.0 Million in incremental value. Three structural shifts will define this growth. Technological disruptions will center on AI-powered tonometry, wearable IOP sensors, and smartphone-compatible probes enabling continuous and minimally invasive monitoring.

Demographic tailwinds from a rapidly aging global population, combined with the escalating burden of diabetes-related eye disease, ensure structural demand growth across all major regions. The shift toward value-based and preventive care models in North America and Europe will favor subscription-based tonometry services and long-term patient monitoring solutions.

The competitive landscape will witness further consolidation as leading multinationals pursue M&A to integrate tonometry into broader ophthalmic diagnostics portfolios, while niche innovators in rebound and AI-enabled tonometry continue to reshape clinical protocols and expand the total addressable market.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews in 2024-2025 with ophthalmic device executives, glaucoma specialist ophthalmologists, ophthalmic device distributors in North America, Germany, Japan, and India; and ophthalmic device equity analysts at leading investment banks.

Secondary Research

Key secondary sources include WHO Global Glaucoma Prevalence Update (2025), FDA 510(k) device clearance database, European Glaucoma Society (EGS) Guidelines 2023, American Academy of Ophthalmology (AAO) Preferred Practice Patterns, NPCB India Annual Report, China Health Statistics Yearbook, Revenio Group Annual Reports (FY2022-2024), Ametek Inc. Annual Reports, ISO 10939 Ophthalmic Instruments standards documentation, and trade publications including Ophthalmology Times, Review of Ophthalmology, and EuroTimes.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Tonometer Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Direct, Indirect |

| Technologies Covered | Applanation Tonometry, Indentation Tonometry, Rebound Tonometer, Others |

| Portabilities Covered | Desktop, Handheld |

| End Users Covered | Hospitals, Ophthalmic Centers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Haag-Streit Group, Topcon Corporation, Reichert Technologies (Ametek), NIDEK CO. LTD., iCare Finland Oy, Keeler, Tomey Corporation, Marco, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the tonometer market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global tonometer market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the tonometer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Tonometer Market Report

The global tonometer market reached USD 391.8 Million in 2025, driven by rising glaucoma prevalence affecting over 80 million people worldwide and expanding ophthalmic screening programs.

The market is projected to reach USD 579.8 Million by 2034, growing at a CAGR of 4.3% during 2026-2034, driven by portable device adoption, AI integration, and home-use monitoring expansion.

Indirect tonometers lead with 64.6% market share in 2025. Non-contact air-puff designs eliminate anesthesia and reduce cross-contamination risk, enabling high-throughput use in ophthalmic screening clinics.

Applanation tonometry dominates at 51.4% in 2025. Goldmann Applanation Tonometry is the ISO-recognized clinical reference standard embedded in all major ophthalmology guidelines globally.

North America leads with 39.6% share in 2025, supported by CMS glaucoma screening coverage for high-risk Medicare beneficiaries, strong FDA 510(k) device pipelines, and high ophthalmologist density.

Key drivers include rising global glaucoma prevalence, aging demographics, AI-integrated diagnostic platforms, and expanding ophthalmic infrastructure in Asia-Pacific and Latin America.

Key players include Haag-Streit Group, Topcon Corporation, Reichert Technologies (Ametek), NIDEK CO. LTD., iCare Finland Oy, Keeler, Tomey Corporation, and Marco.

Rebound tonometry is the fastest-growing technology at ~5.8% CAGR. Its no-touch, no-anesthesia design drives adoption in pediatric care, home monitoring, and primary care screening settings.

Topcon Healthcare's Microsoft Azure partnership (May 2024) deploys AI to analyze IOP data alongside retinal imaging for systemic disease pre-screening. AI reduces specialist dependency and expands screening accessibility.

Reichert launched the Tono-Vera in the US in May 2024. It features the patented ActiView automated alignment and Bluetooth connectivity, delivering rebound IOP measurements comparable to Goldmann tonometry.

Home-use tonometry is growing at ~8.4% CAGR - the fastest end-user segment. CMS added remote IOP monitoring reimbursement codes in 2023, and iCare HOME2 enables FDA-cleared patient self-monitoring with EHR data integration.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)