Tourism Vehicle Rental Market Size, Share, Trends and Forecast by Vehicle Type, Booking Mode, End User, and Region 2026-2034

Tourism Vehicle Rental Market Size, Share, Trends & Forecast (2026-2034)

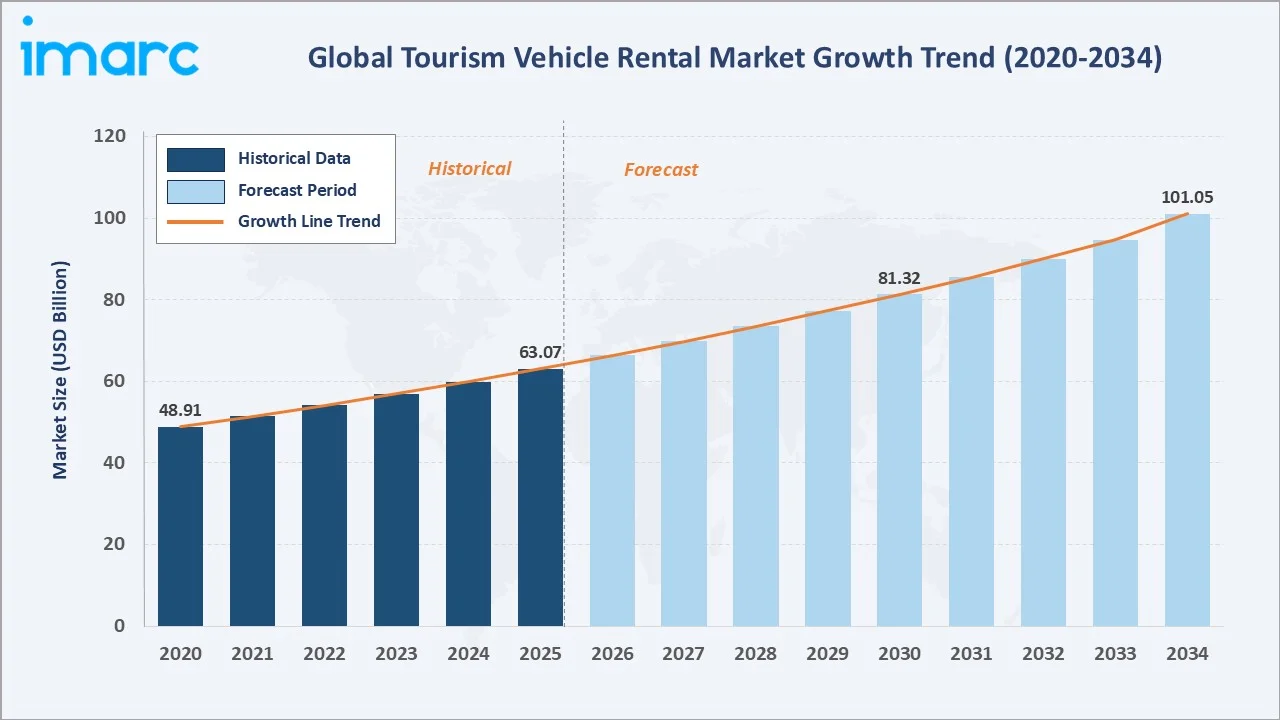

The global tourism vehicle rental market reached USD 63.07 Billion in 2025 and is projected to reach USD 101.05 Billion by 2034, growing at a CAGR of 5.22% during 2026-2034. The market is driven by expanding global tourism activity, rapid digitalization of booking platforms, rising preference for flexible transportation, and increasing adoption of electric and eco-friendly rental fleets.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 63.07 Billion |

| Forecast Market Size (2034) | USD 101.05 Billion |

| CAGR (2026-2034) | 5.22% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

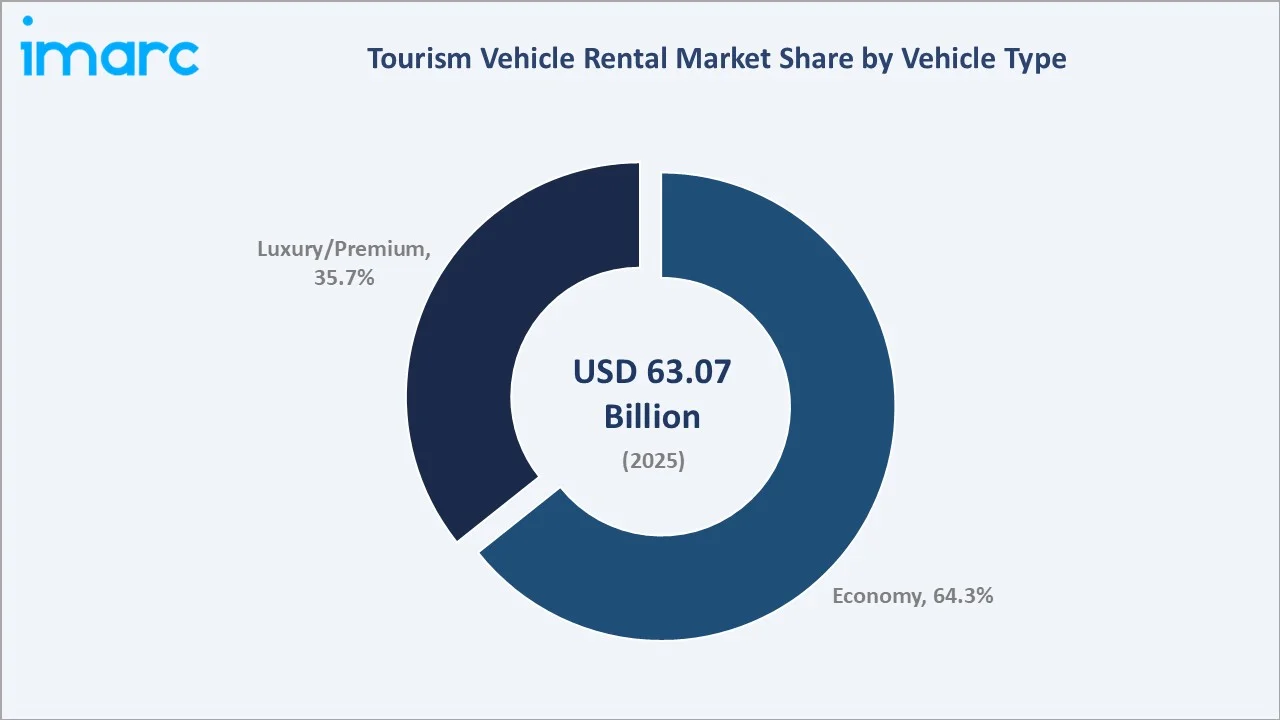

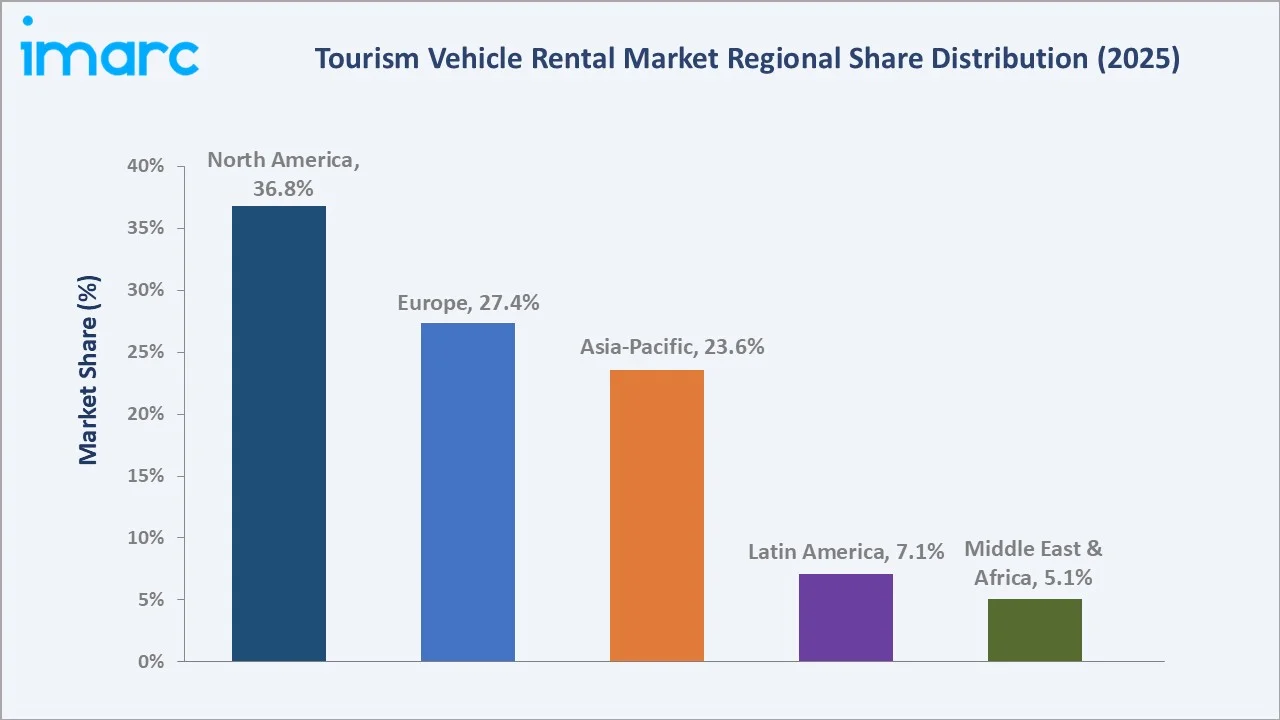

North America leads regionally with a 36.8% share in 2025, underpinned by a robust tourism ecosystem, high per-capita vehicle usage, extensive airport-adjacent rental networks, and early adoption of contactless and mobile-first booking experiences. The economy vehicle type commands a dominant 64.3% share of the vehicle type breakdown, anchored by cost-conscious leisure and business travelers seeking affordability.

To get more information on this market, Request Sample

Tourism vehicle rental demand is structurally supported by three forces: the sustained recovery of international tourism post-pandemic, a digitally empowered traveler base that values on-demand mobility, and aggressive fleet electrification by leading operators seeking sustainability credentials.

Executive Summary

The global tourism vehicle rental market is undergoing sustained expansion, supported by a confluence of rising international travel volumes, digital transformation of booking ecosystems, and shifting consumer preferences toward flexible, self-driven mobility. From USD 63.07 Billion in 2025, the market is forecast to reach USD 101.05 Billion by 2034, growing at a 5.22% CAGR from 2026 to 2034.

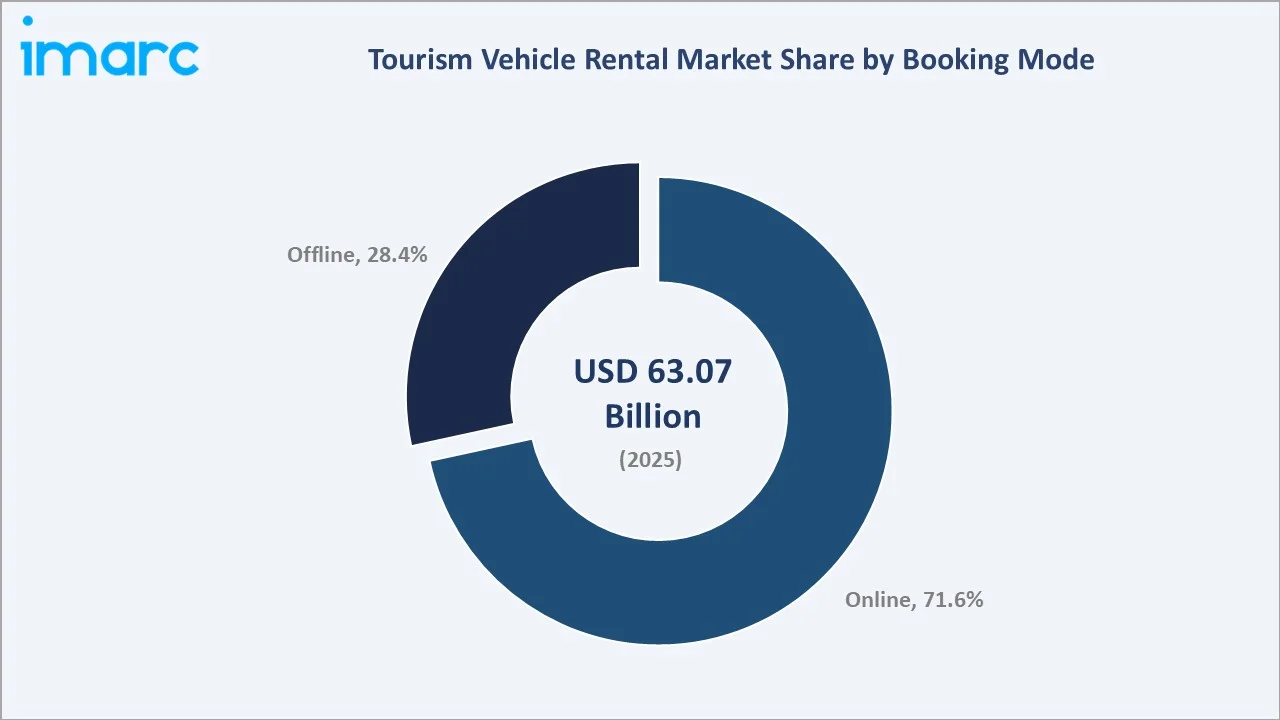

The economy vehicle type leads with a 64.3% share in 2025, driven by budget-conscious travelers and corporate clients seeking cost-effective mobility. Online booking mode dominates at 71.6%, reflecting deep penetration of OTA platforms, car-sharing apps, and direct digital channels. North America holds the largest regional position (36.8%), followed by Europe (27.4%) and Asia-Pacific (23.6%).

Key players including Enterprise Mobility, The Hertz Corporation, Avis Budget Group, Inc., Sixt SE, and Green Mobility Holding S.A. collectively hold a significant share of global rental revenues, competing on fleet breadth, digital experience, loyalty programs, and geographic coverage.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Vehicle Type | Economy – 64.3% share (2025) |

| Fastest Growing Vehicle Type | Luxury/Premium – ~6.8% (2026-2034) |

| Largest Booking Mode | Online – 71.6% share (2025) |

| Fastest Growing Booking Mode | Online – ~6.5% (2026-2034) |

| Leading Region | North America – 36.8% share (2025) |

| Top Companies | Enterprise Mobility, The Hertz Corporation, Avis Budget Group Inc., Sixt SE, and Green Mobility Holding S.A. |

Key Analytical Observations:

- Economy vehicles account for 64.3% of the global tourism vehicle rental market in 2025. This dominance reflects the large base of budget and mid-scale travelers, corporate travel policies favoring economy class, and the operational efficiency advantages for fleet operators.

- Online booking at 71.6% (2025) reflects the maturity of digital travel infrastructure. OTA integrations, loyalty program apps, and contactless pick-up capabilities have made online channels the default for both leisure and business travelers globally.

- Luxury/Premium vehicles, despite a 35.7% share (2025), are fastest growing, driven by affluent millennial travelers, destination wedding tourism, and corporate executive travel policies across North America, Europe, and the Gulf region.

- North America's 36.8% dominance is rooted in the US and Canada's high vehicle usage culture, extensive inter-city road networks, dense airport rental infrastructure, and mature fleet management ecosystems operated by global OEM-aligned rental brands.

Tourism Vehicle Rental Market Overview

Tourism vehicle rental encompasses short-term and medium-term rental of passenger cars, SUVs, vans, minibuses, and specialty vehicles to tourists, corporate travelers, and leisure customers. The market spans economy, mid-size, full-size, SUV, and luxury vehicle categories, delivered through airport counters, city locations, and increasingly via fully digital, contactless channels.

The market is underpinned by structural demand from international arrivals, as the first World Tourism Barometer of the year reported approximately 1.52 billion international tourist arrivals in 2025, an increase of nearly 60 million compared to 2024, coupled with the growth of domestic road tourism in North America, Europe, and Asia-Pacific.

Market Dynamics

To evaluate market opportunities, Request Sample

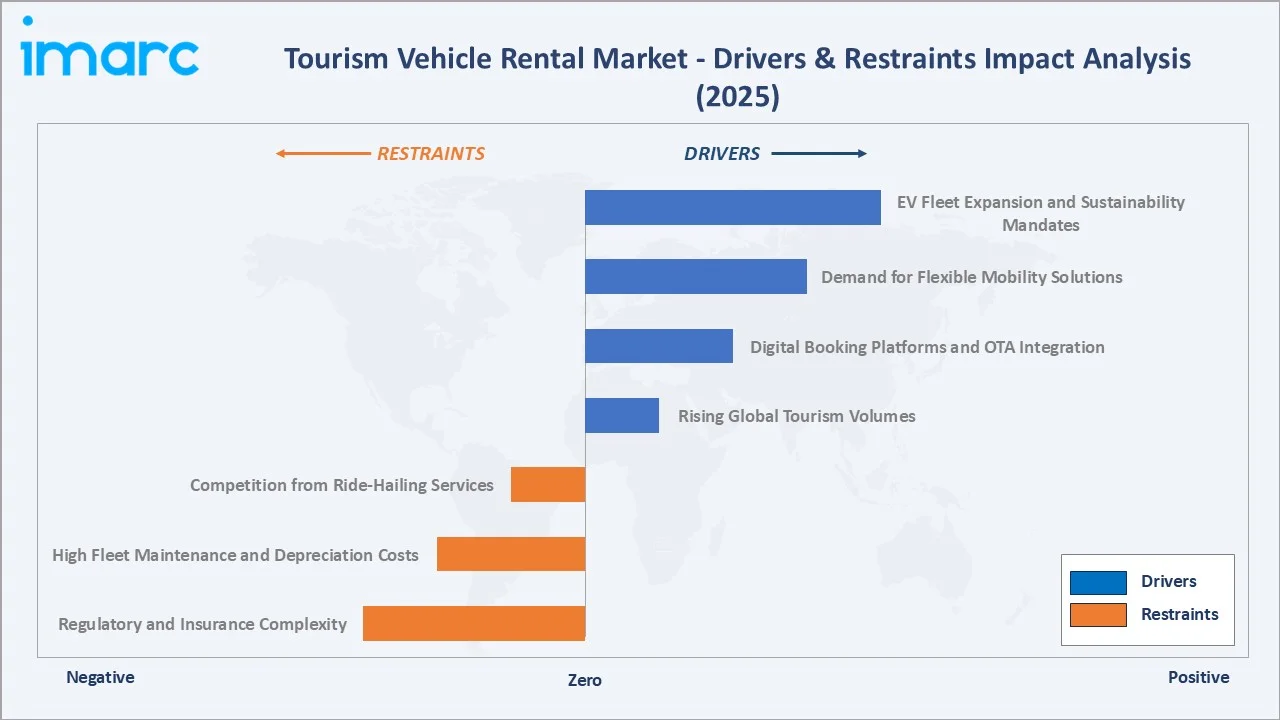

Market Drivers

- Rising Global Tourism Volumes: According to WTTC’s latest Economic Impact Research (EIR), the travel & tourism sector contributed a record USD 11.6 trillion to global GDP in 2025, representing 9.8% of the world economy. This growth in travel & tourism activity translates directly into rental demand across airport hubs and urban destinations.

- Digital Booking Platforms and OTA Integration: The proliferation of travel apps and OTA platforms including Booking.com, Expedia, and Kayak has made vehicle comparison and reservation a frictionless, mobile-first experience, expanding the addressable customer base significantly.

- Demand for Flexible Mobility Solutions: Increasing traveler preference for self-driven tours, road trips, and itinerary flexibility over fixed public transport schedules is generating sustained rental demand, particularly in North America and Europe.

- EV Fleet Expansion and Sustainability Mandates: Major operators are committing to fleet electrification timelines. The Hertz Corporation's 100,000-vehicle EV order (October 2021) and Sixt's partnership to deploy 50 BMW iX3 EVs across Australia reflect a structural shift toward eco-friendly rentals, attracting sustainability-focused travelers.

Market Restraints

- Competition from Ride-Hailing Services: Uber, Lyft, Grab, and Bolt offer on-demand urban mobility without the need for a driving license, insurance, or fuel management, directly competing with short-duration rental use cases in dense city environments.

- High Fleet Maintenance and Depreciation Costs: Fleet ownership costs are primarily driven by depreciation/leasing (35–45%) and fuel/energy (25–35%), making them the largest contributors to total cost of ownership (TCO). Thus, managing large fleets across multiple countries requires significant capital investment, compressing margins for mid-tier operators.

- Regulatory and Insurance Complexity: Cross-border rental regulations, differing insurance mandates, and varying driver age restrictions across markets create operational complexity for international rental operators.

Market Opportunities

- Expansion in Asia-Pacific Emerging Markets: India, Vietnam, Indonesia, and the Philippines represent high-growth tourism corridors with underpenetrated vehicle rental ecosystems. Rising middle-class travel budgets and improving road infrastructure create greenfield rental opportunities.

- Subscription and Long-Term Rental Models: Monthly vehicle subscription services combining insurance, maintenance, and flexibility are gaining traction among digital nomads and long-stay business travelers, generating higher revenue-per-customer versus traditional daily rentals.

- Electric Vehicle Differentiation: Operators who build EV-first fleets in key markets gain premium pricing power, access to ESG-conscious corporate travel budgets, and qualification for government EV deployment incentives in the EU and North America.

Market Challenges

- Supply Chain Constraints for Vehicle Acquisition: Post-pandemic semiconductor shortages and OEM production disruptions have slowed fleet refresh cycles, inflating per-unit vehicle costs and constraining capacity in high-demand peak-season markets.

- Driver License and Age Restriction Variability: Inconsistent minimum age requirements (18–25 years) and license recognition policies across markets limit customer segments accessible to rental operators in cross-border tourism corridors.

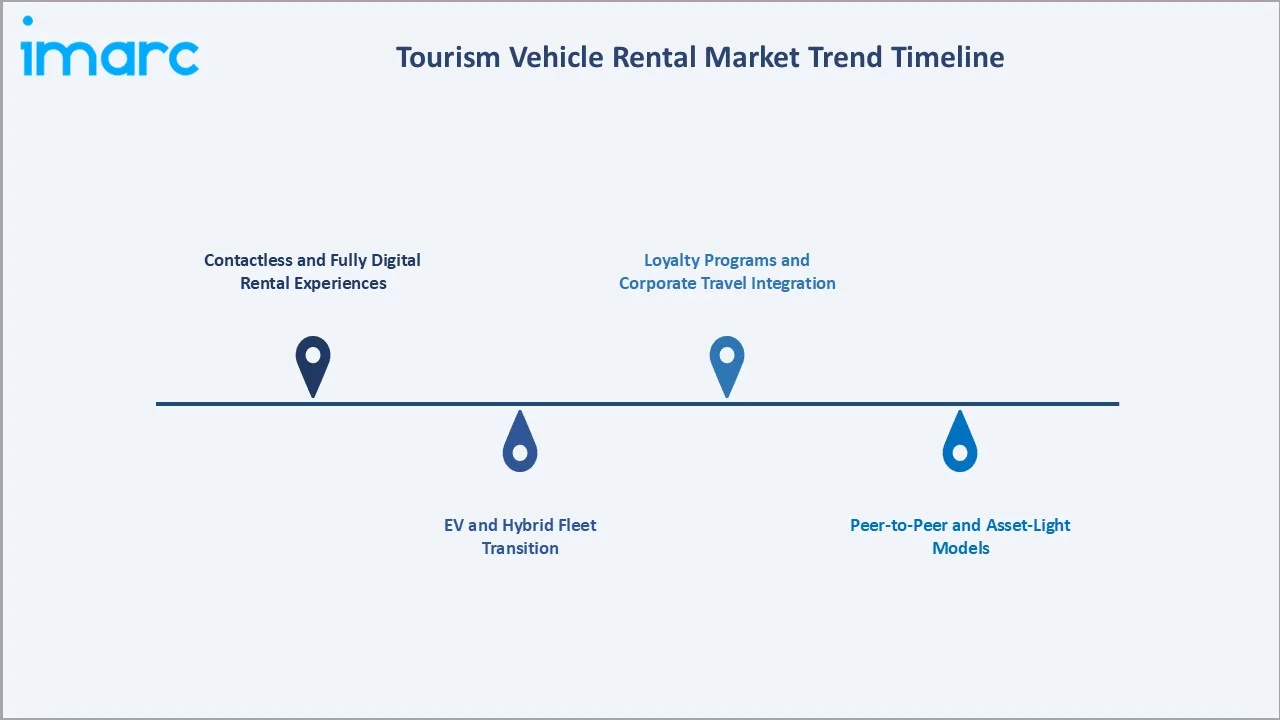

Emerging Market Trends

1. Contactless and Fully Digital Rental Experiences

In May 2025, Zoomcar and Wego partnered to let Wego users book 25,000+ self-drive cars across 99+ Indian cities, targeting global tourists seeking flexible and cost-effective travel. The tie-up highlights travel digitalization by integrating self-drive car booking directly into Wego’s website and app for a seamless mobility experience. Leading global rental companies including Enterprise, Hertz, and Sixt are also investing substantially in proprietary app experiences, loyalty program integration, and seamless digital check-in capabilities.

2. EV and Hybrid Fleet Transition

Major operators including Hertz, Enterprise, and Sixt have announced multi-year EV fleet expansion commitments, with Hertz's partnership with Tesla in October 2021 representing the most visible EV fleet transition in the industry. Moreover, the Goa Government (India) mandated that all new rent-a-cabs and rent-a-bikes registered from January 2024 must be electric vehicles.

3. Peer-to-Peer and Asset-Light Models

Turo, Getaround, and similar peer-to-peer (P2P) platforms are disrupting traditional fleet operators by enabling private vehicle owners to monetize idle assets. The P2P car rental market segment is growing at an estimated 12–15% CAGR, attracting younger, cost-sensitive travelers who value unique vehicle options and local pricing.

4. Loyalty Programs and Corporate Travel Integration

National Car Rental's Emerald Club, Enterprise Plus, Hertz Gold Plus Rewards, and Avis Preferred have deepened customer lifetime value. Corporate Travel Management Company (TMC) integrations with SAP Concur and TravelPerk further lock in enterprise accounts, stabilizing recurring B2B revenue streams for leading operators.

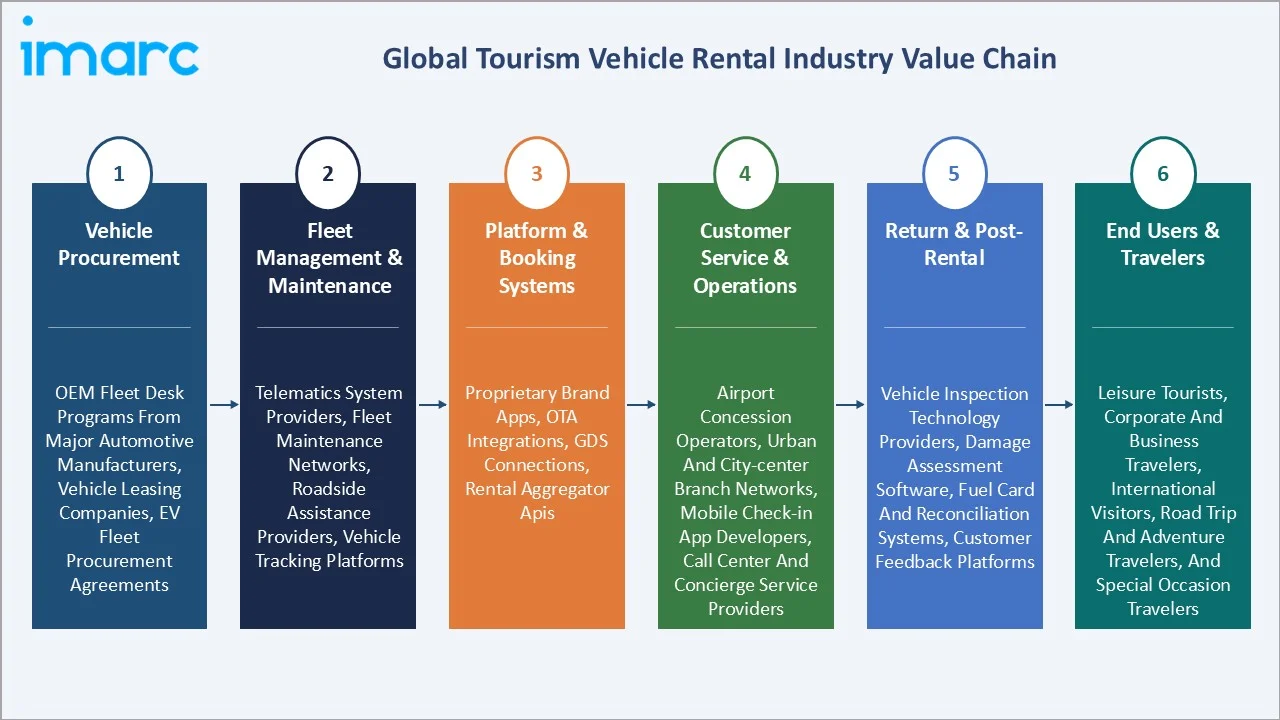

Industry Value Chain Analysis

The tourism vehicle rental value chain spans vehicle manufacturing through end-user mobility delivery, with each stage contributing specialized capabilities that determine fleet quality, cost competitiveness, and customer satisfaction.

| Stage | Key Players / Examples |

|---|---|

| Vehicle Procurement | OEM fleet desk programs from major automotive manufacturers, vehicle leasing companies, EV fleet procurement agreements |

| Fleet Management & Maintenance | Telematics system providers, fleet maintenance networks, roadside assistance providers, vehicle tracking platforms |

| Platform & Booking Systems | Proprietary brand apps, OTA integrations, GDS connections, rental aggregator APIs |

| Customer Service & Operations | Airport concession operators, urban and city-center branch networks, mobile check-in app developers, call center and concierge service providers |

| Return & Post-Rental | Vehicle inspection technology providers, damage assessment software, fuel card and reconciliation systems, customer feedback platforms |

| End Users & Travelers | Leisure tourists, corporate and business travelers, international visitors, road trip and adventure travelers, and special occasion travelers |

Technology Landscape in the Tourism Vehicle Rental Industry

Digital Booking and Mobile Platform Technology

Leading operators are investing in proprietary apps featuring keyless vehicle access, digital check-in bypassing airport counters, real-time vehicle location sharing, in-app roadside assistance activation, and integrated loyalty point management. The integration of rental apps with airline, hotel, and OTA booking platforms through API partnerships is enabling seamless multi-component travel package assembly that drives incremental rental attachment rates and customer lifetime value for global rental brands.

Connected Fleet and IoT-Enabled Fleet Management Technology

Telematics and Internet of Things connectivity embedded in rental fleet vehicles enable real-time vehicle location tracking, driving behavior monitoring, predictive maintenance diagnostics, and automated return mileage and fuel reconciliation. Rental operators leverage connected fleet data to optimize vehicle repositioning across high-demand locations, identify maintenance needs before breakdown occurrence, and generate driving behavior reports used in damage liability assessment.

Electric Vehicle Fleet Integration Technology

EV fleet management technology for tourism rental operations encompasses charging infrastructure integration, range management advisory tools, and real-time charge level monitoring capabilities that address the primary operational complexity of EV rental versus internal combustion vehicle fleets. Fleet management platforms integrating EV-specific capabilities are enabling rental operators to manage mixed EV and ICE fleets from unified dashboards and optimize charging scheduling across depot and public charging points.

AI-Driven Dynamic Pricing and Demand Analytics

Revenue management systems powered by machine learning and AI are enabling rental operators to implement yield management approaches comparable to airline and hotel revenue optimization, dynamically adjusting prices across vehicle categories, locations, and date combinations in response to real-time demand signals. These systems analyze search query volumes, booking lead times, competitor rate changes, local event calendars, and historical occupancy patterns to generate revenue-maximizing price points at each decision interval.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Vehicle Type | Economy | 64.3% | 2025 |

| Booking Mode | Online | 71.6% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | North America | 36.8% | 2025 |

By Vehicle Type

The economy vehicle type dominates with a 64.3% share in 2025. This segment encompasses compact cars, sedans, and hatchbacks priced for value-conscious travelers. Economy vehicles are preferred by budget travelers, students, and corporate clients with standard travel policies. Their lower daily rates, wide availability across global operators, and fuel efficiency make them the default choice for short-to-medium duration rentals.

To access detailed market analysis, Request Sample

Luxury/premium vehicle types represent 35.7% of the market in 2025. This segment encompasses SUVs, premium sedans, sports cars, and specialty vehicles catering to high-net-worth travelers, honeymooners, and executive corporate clients. Luxury rental pricing commands a 2.5–4× premium over economy rates, delivering disproportionate revenue contribution relative to fleet share.

By Booking Mode

Online booking mode commands a 71.6% share in 2025, driven by OTA integrations, mobile-first rental apps, and corporate booking platform adoption. Contactless and app-based reservation systems have significantly lowered booking friction, enabling last-minute rentals and dynamic pricing strategies that maximize fleet utilization across peak and off-peak demand cycles.

Offline channels retain a 28.4% share in 2025, predominantly through airport counter walk-ins, hotel concierge referrals, and travel agency packages. Offline bookings remain prevalent in markets with lower digital penetration and among older traveler segments who prefer in-person service.

Regional Market Insights

North America leads global tourism vehicle rental with a 36.8% market share in 2025. The region's dominance reflects its high vehicle-per-capita ownership culture, extensive inter-city highway infrastructure, dominant airport rental networks, and the strong presence of global operators headquartered in the US.

Europe's 27.4% share represents a mature but evolving market. The transition toward EV rentals is most advanced in Europe, with Germany, France, and the UK leading fleet electrification. Asia-Pacific at 23.6% is the fastest-growing region, anchored by expanding outbound tourism from China, Korea, and India, combined with rapid improvement of rental infrastructure in Thailand, Japan, and Vietnam.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| North America | 36.8% | Largest global rental fleet operators, high-frequency domestic tourism, strong corporate travel spending, and mature digital booking infrastructure. |

| Europe | 27.4% | Cross-border road tourism via the Schengen zone, strong inbound international arrivals, and accelerating EV fleet adoption driven by EU sustainability mandates. |

| Asia-Pacific | 23.6% | Rapid growth of outbound tourism from China, India, and Southeast Asia; expanding road tourism; improving rental infrastructure in emerging markets. |

| Latin America | 7.1% | Rising domestic tourism in Brazil and Mexico, growing middle-class travel budgets, and expanding rental networks in key tourist destinations. |

| Middle East & Africa | 5.1% | Gulf tourism growth via Vision 2030 and UAE initiatives, luxury vehicle demand in GCC markets, and nascent rental market development in Africa. |

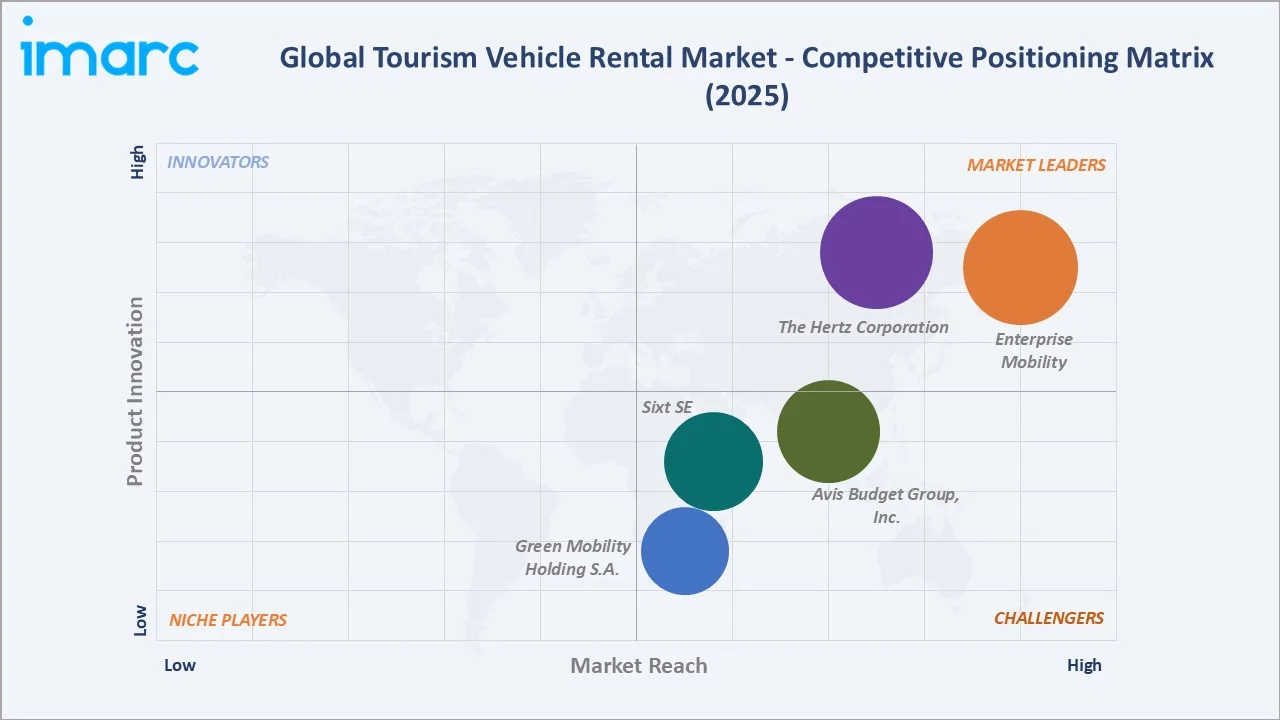

Competitive Landscape

The global tourism vehicle rental market is moderately concentrated. The top operators, Enterprise Mobility, The Hertz Corporation, Avis Budget Group, Inc., Sixt SE, and Green Mobility Holding S.A., collectively account for approximately 55–60% of global revenues in 2025. Competition centers on fleet breadth, geographic coverage, digital experience quality, and loyalty program differentiation.

| Company Name | Brand Name | Market Position | Core Strength |

|---|---|---|---|

| Enterprise Mobility | Enterprise, National, Alamo | Market Leader | One of the largest global fleets, airport and neighborhood presence, strong corporate accounts |

| The Hertz Corporation | Hertz, Dollar, Thrifty | Market Leader | Airport dominance, EV fleet leadership, global loyalty program |

| Avis Budget Group, Inc. | Avis, Budget, Zipcar, Payless, among others | Strong Challenger | Business traveler focus, subscription models, Zipcar car-sharing integration |

| Sixt SE | SIXT rent, SIXT+, SIXT share | Strong Challenger | Premium positioning, strong European presence, tech-forward app experience |

| Green Mobility Holding S.A. | Europcar, Goldcar, Fox Rent A Car, Euromobil | Challenger | Pan-European footprint, Green Mobility EV program, leisure segment strength |

The companies are focusing on fleet expansion, strategic partnerships with travel platforms, contactless rental experiences, and the growing integration of electric and low-emission vehicles. Competition is further intensifying as companies leverage mobile applications, real-time vehicle availability, flexible rental models, and sustainable mobility solutions to cater to the evolving needs of domestic and international tourists.

Key Company Profiles

Enterprise Mobility

Enterprise Mobility is the world's largest vehicle rental company by fleet size and revenue. The company operates Enterprise Rent-A-Car, National Car Rental, and Alamo Rent A Car brands worldwide.

- Product Portfolio: Economy to full-size SUVs under Enterprise; premium traveler-focused vehicles under National; and leisure & value segment under Alamo.

- Recent Developments: In April 2026, Enterprise Mobility partnered with Eurokars Leasing to introduce its Enterprise, National, and Alamo brands in Singapore, with two locations scheduled to open in October 2026.

- Strategic Focus: Fleet electrification, loyalty program expansion, corporate account growth, and technology-driven customer experience enhancement.

The Hertz Corporation

The Hertz Corporation is a leading international vehicle rental company operating under the Hertz, Dollar, and Thrifty brands. Hertz serves airports, urban locations, and off-airport sites.

- Product Portfolio: Full vehicle spectrum from economy sedans to luxury SUVs under Hertz; value-focused offerings under Dollar and Thrifty; Tesla and EV fleet available at premium tier.

- Recent Developments: In May 2026, Aeroplan partnered with The Hertz Corporation, including Hertz, Dollar, and Thrifty, to enable members to earn up to 5 points per dollar spent on car rentals, along with Status Qualifying Credits and premium loyalty benefits.

- Strategic Focus: Premium EV positioning, fleet efficiency optimization, Hertz Gold digital experience, and airport network densification in high-traffic hub markets.

Sixt SE

Sixt SE is a premium vehicle rental and mobility services company known for its technology-forward app experience and premium vehicle positioning. Sixt targets business and leisure travelers seeking a differentiated rental experience.

- Product Portfolio: Premium, luxury, and business vehicle categories; one-way rental services; Sixt+ subscription mobility; SIXT share car-sharing platform.

- Recent Developments: In November 2025, Sixt SE expanded into five new markets, including Mexico, Chile, the Cayman Islands, El Salvador, and Nicaragua. This is aimed at extending its car rental presence to 26 countries across Latin America and the Caribbean.

- Strategic Focus: US market penetration, luxury segment leadership, Sixt+ subscription growth, and app-based contactless experience differentiation.

Market Concentration Analysis

The global tourism vehicle rental market exhibits moderate to high concentration, with the top operators capturing approximately 55–60% of global revenue in 2025. Below the top tier, a fragmented mid-market includes 50+ regional operators, peer-to-peer platforms, and local rental businesses serving niche geographies and vehicle categories.

Regional and specialty operators and various national operators serve distinct domestic markets with limited geographic overlap with global brands. The market's moderate to high concentration reflects the capital-intensive nature of fleet management, the brand recognition required for tourist customer acquisition, and the airport concession relationships that gate access to the highest-volume rental locations globally.

Investment & Growth Opportunities

Fastest Growing Segments

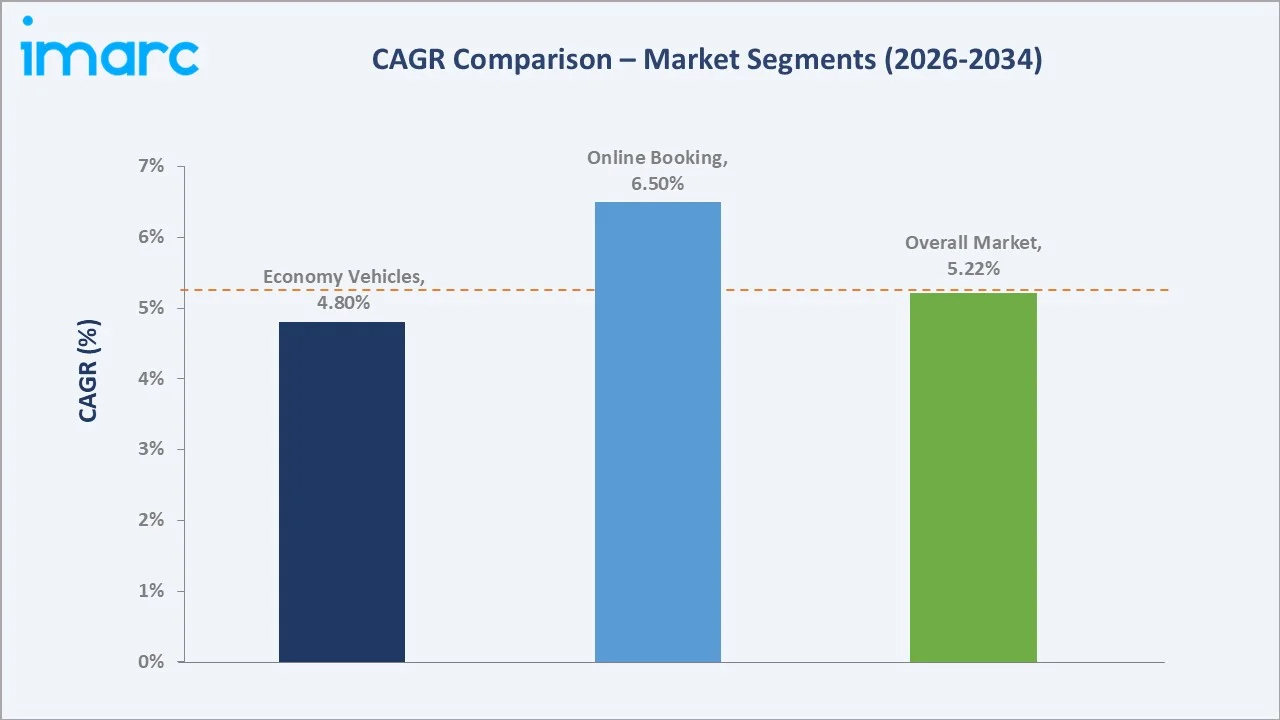

Online booking (~6.5% CAGR), luxury/premium vehicle rentals (~6.8% CAGR), EV-specific rental fleets (~18% CAGR), and subscription-based rental models (~12% CAGR) represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined incremental addressable market of approximately USD 25 Billion by 2034.

Emerging Market Expansion

India, Vietnam, Saudi Arabia, and Nigeria collectively represent an incremental USD 8+ Billion rental opportunity by 2034, as expanding tourism infrastructure and rising middle-class travel budgets attract global operators. Entry strategies include franchise partnerships, OTA channel agreements, and airport concession bids tied to new international terminal developments.

Venture and Institutional Investment Trends

- Private equity investment in fleet-light, platform-driven rental models is accelerating. Turo's USD 250 Million+ venture funding trajectory signals institutional confidence in P2P disruption.

- OEM-rental operator partnerships for EV supply chain integration are enabling operators to secure preferential fleet pricing and charging infrastructure co-development agreements.

- Subscription mobility services are attracting SaaS-style revenue multiple valuations from institutional investors, commanding 30–50% revenue premium over traditional per-day rental models.

Future Market Outlook (2026-2034)

The global tourism vehicle rental market is positioned for steady, broad-based expansion through 2034. From USD 63.07 Billion in 2025, the market will reach USD 101.05 Billion by 2034, representing total incremental value creation of USD 37.98 Billion at a CAGR of 5.22%. This trajectory is underpinned by the sustained global tourism growth arc and the deepening preference for flexible, on-demand mobility.

The technology transition toward fully digital, app-native rental experiences will define the market's competitive structure by 2034. Operators that build seamless mobile-first platforms, integrate AI-based pricing and fleet allocation, and deploy EV-dominant fleets in high-demand corridors will capture disproportionate market share growth. Offline rental channels are projected to decline to below 20% of bookings by 2034 as digital adoption reaches full maturity.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 80 industry participants in 2024–2025, including vehicle rental operators, fleet management professionals, OTA platform executives, corporate travel managers, and institutional investors across North America, Europe, and Asia-Pacific. Expert input validated market sizing, digital adoption rates, and fleet electrification trends.

Secondary Research

Secondary research encompassed operator annual reports, UNWTO tourism statistics, IATA travel data, OTA market disclosures, auto industry fleet procurement data, trade publications (Business Travel News, Auto Rental News, Phocuswire), and government tourism authority statistics.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting, incorporating tourist arrival volumes, rental penetration rates, average revenue per rental day, fleet utilization rates, and operator revenue disclosures. A base-case CAGR of 5.22% reflects consensus validated against booking platform data and operator fleet investment commitments for 2026–2034.

Tourism Vehicle Rental Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Economy, Luxury/Premium |

| Booking Modes Covered | Online, Offline |

| End Users Covered | Self-driven, Rental Agencies |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Enterprise Mobility, The Hertz Corporation, Avis Budget Group Inc., Sixt SE, Green Mobility Holding S.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the tourism vehicle rental market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global tourism vehicle rental market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the tourism vehicle rental industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Tourism Vehicle Rental Market Report

The global tourism vehicle rental market reached USD 63.07 Billion in 2025.

The market is projected to grow at a CAGR of 5.22%, reaching USD 101.05 Billion by 2034.

Key drivers include rising global tourism and travel recovery, digital platform and online booking adoption, growing traveler preference for self-drive and independent travel, and growth of luxury and experiential tourism consumption.

Economy vehicles dominate with a 64.3% share in 2025, reflecting the volume-driven demand from budget-conscious leisure tourists and domestic travelers globally.

Luxury/Premium vehicles are the fastest-growing type at approximately ~6.8% CAGR during 2026–2034, driven by experiential tourism growth, premium leisure travel trends, and aspirational vehicle rental consumption.

Online booking leads with a 71.6% share in 2025, reflecting the structural shift of rental transactions to digital platforms, mobile apps, OTA channels, and metasearch aggregators.

North America leads with 36.8% global share in 2025, anchored by the United States' dominant car rental market and extensive airport concession network.

Major players include Enterprise Mobility, The Hertz Corporation, Avis Budget Group, Inc., Sixt SE, and Green Mobility Holding S.A.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)