Track and Trace Solutions Market Size, Share, Trends and Forecast by Product, Technology, Application, End Use Industry, and Region, 2026-2034

Global Track and Trace Solutions Market Size, Share, Trends & Forecast (2026-2034)

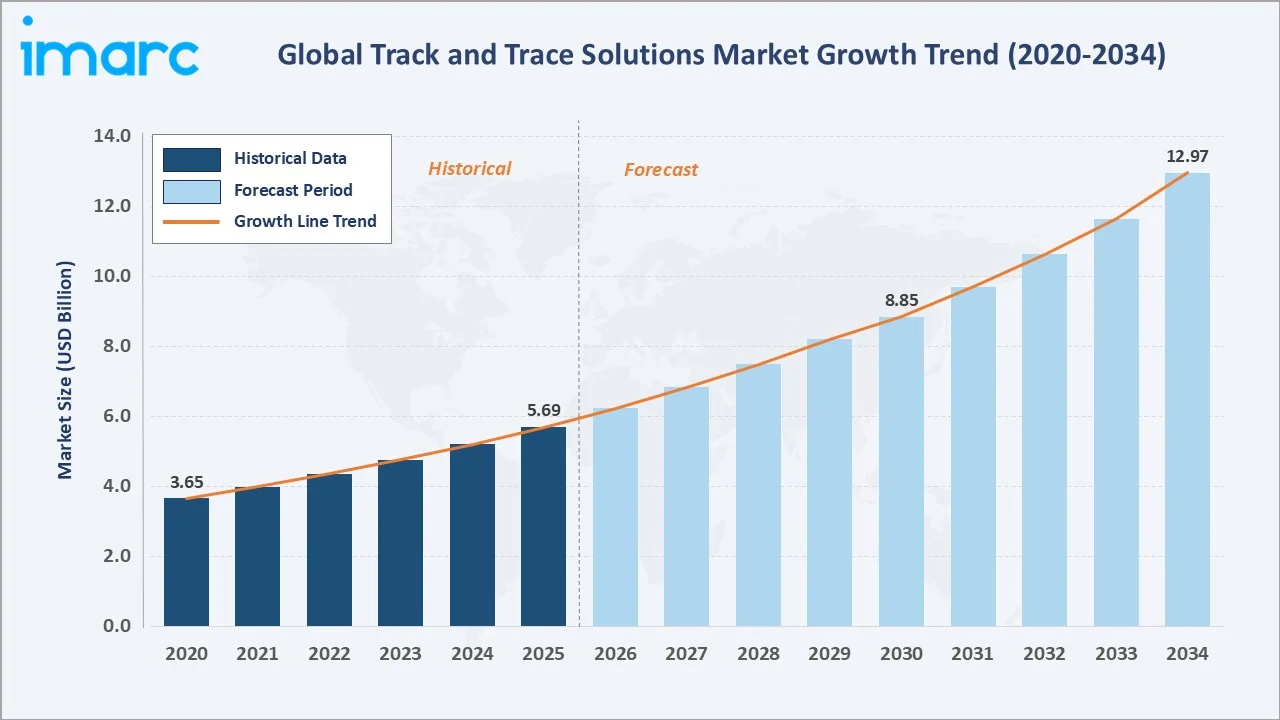

The global track and trace solutions market size was valued at USD 5.69 Billion in 2025 and is projected to reach USD 12.97 Billion by 2034, exhibiting a CAGR of 9.25% during 2026-2034. Key growth drivers include rising anti-counterfeit regulations, expanding e-commerce logistics, IoT-enabled supply chain visibility, and escalating pharmaceutical compliance requirements across global markets.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.69 Billion |

|

Forecast Market Size (2034) |

USD 12.97 Billion |

|

CAGR (2026-2034) |

9.25% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

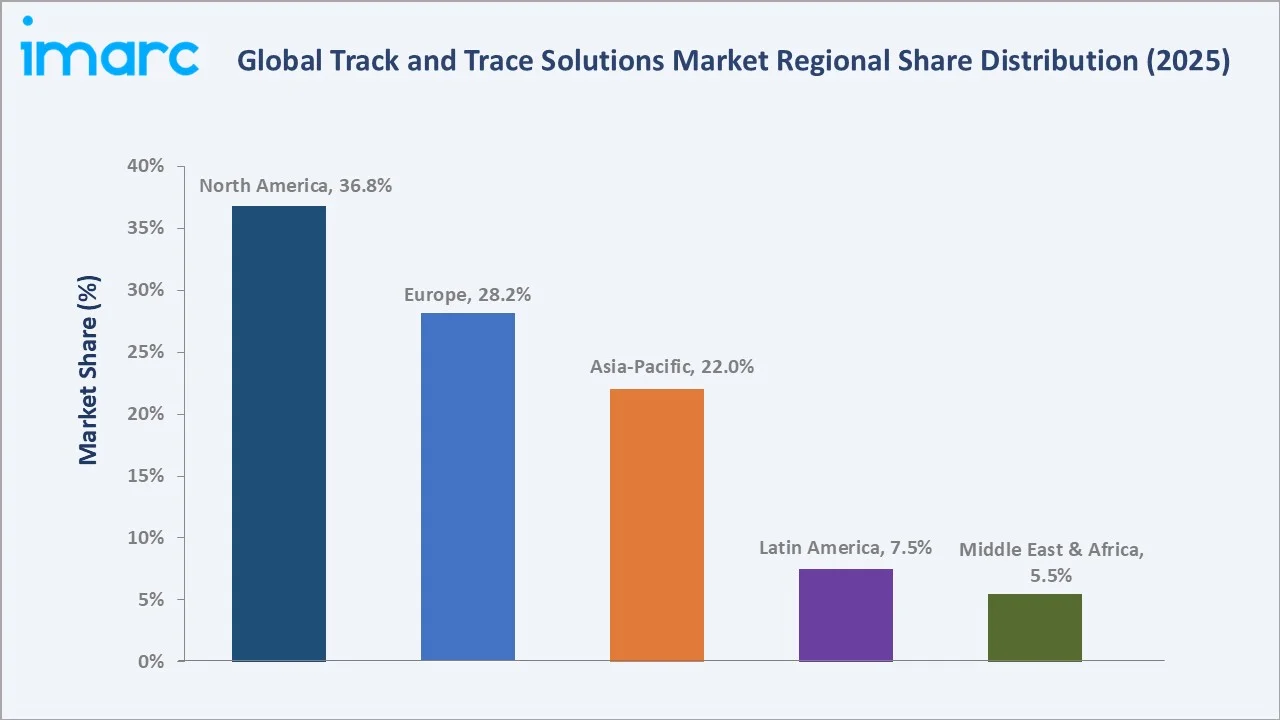

North America (36.8%) |

|

Fastest Growing Region |

Asia-Pacific |

|

Largest Product |

Software (58%, 2025) |

|

Largest Technology |

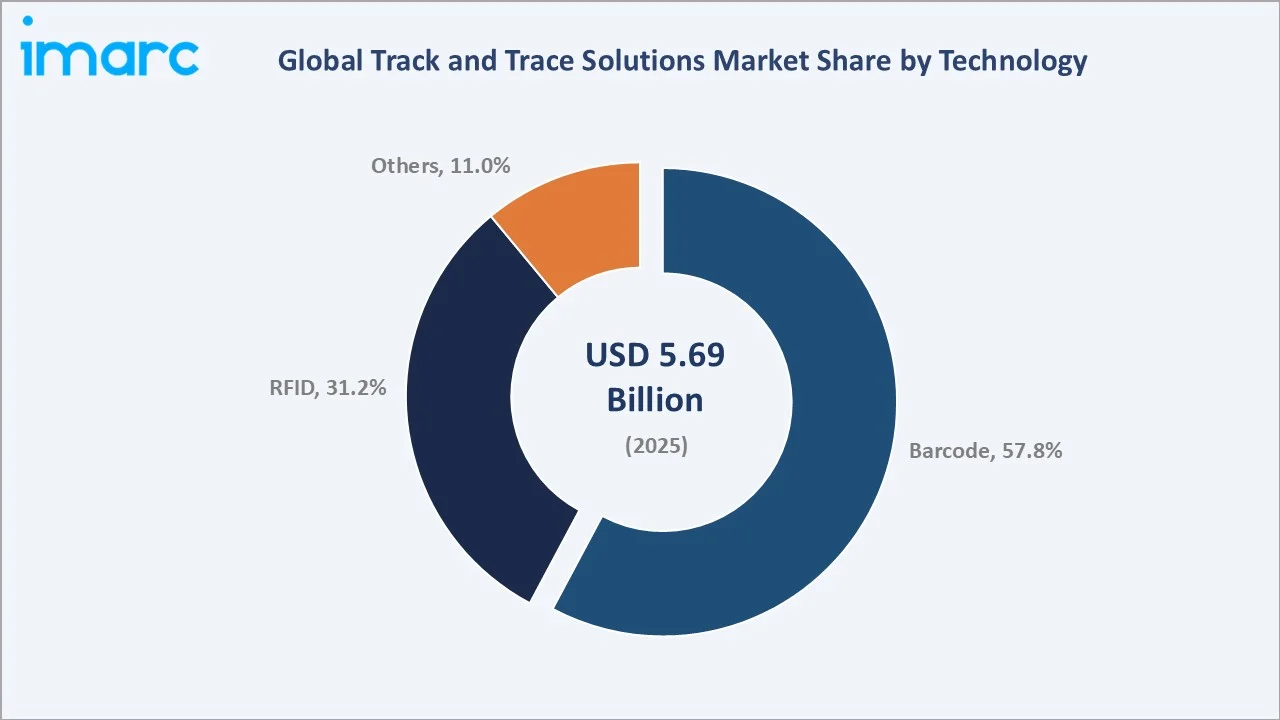

Barcode (57.8%, 2025) |

The global Track and Trace Solutions market show a steep, technology-driven growth trajectory from 2020 through 2034, transitioning from early-stage digital serialization adoption into a fully integrated, AI- and IoT-enabled supply chain intelligence ecosystem.

To get more information on this market, Request Sample

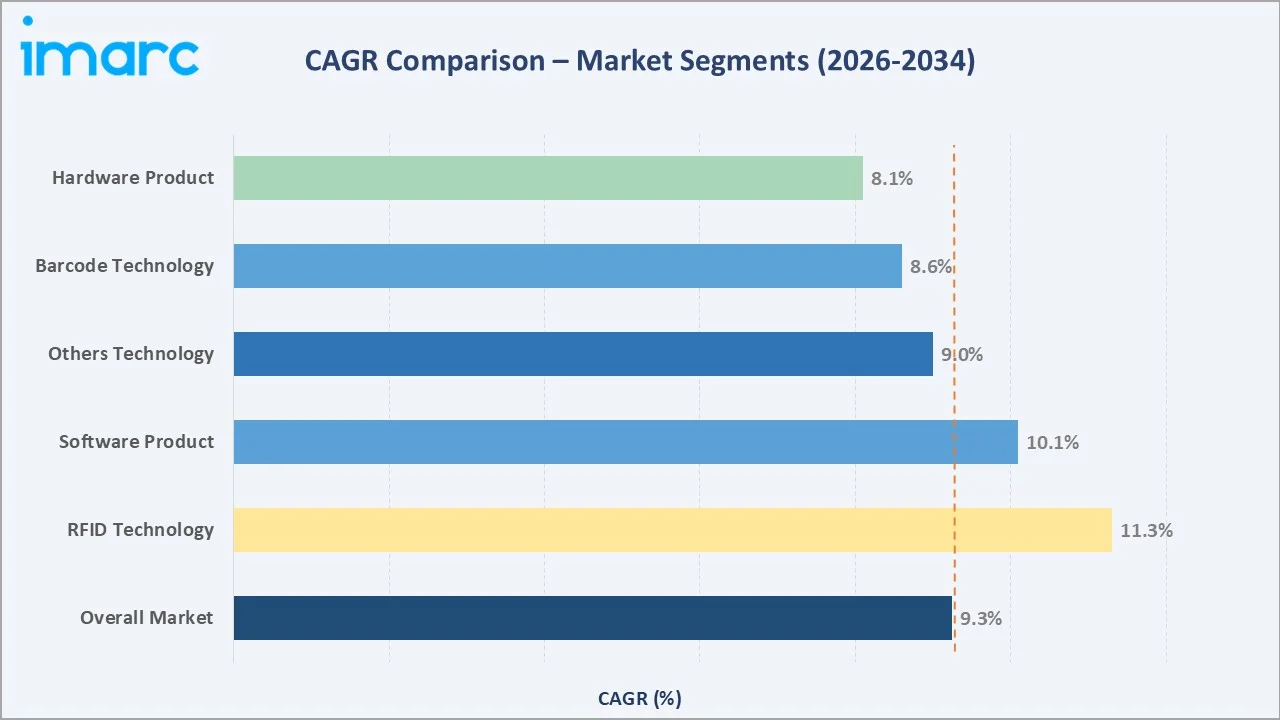

The Global Track & Trace Solutions Market demonstrates a strongly differentiated segment-level growth trajectory through 2034, with clear divergence between mature compliance-driven segments.

Executive Summary

The global track and trace solutions market reached USD 5.69 Billion in 2025, supported by growing regulatory mandates, supply chain digitization, and a sharp rise in counterfeit incidents across high-value industries. The market is forecast to expand to USD 12.97 Billion by 2034, driven by a steadyb over the period 2026-2034. Pharmaceutical serialization requirements - including DSCSA in the United States, FMD in Europe, and similar mandates across Asia - remain the single largest catalyst for adoption.

Software solutions, representing 58.0% of the market in 2025, dominate the product landscape as enterprises shift to cloud-based serialization platforms, digital compliance engines, and advanced analytics dashboards. Barcode technology holds a commanding 57.8% technology share, while RFID is the fastest-growing sub-segment, expected to expand at 11.3% CAGR through 2034 owing to its growing application in medical device tagging, pallet-level logistics, and retail inventory management.

North America leads regional markets with a 36.8% share in 2025, followed by Europe at 28.2% and Asia-Pacific at 22.0%. Asia-Pacific is forecasted to record the fastest regional growth, propelled by pharmaceutical export regulations in India and China, expanding e-commerce infrastructure, and increasing government investments in digital supply chain infrastructure. The competitive landscape is moderately consolidated, with Zebra Technologies, Honeywell, and Cognex holding significant positions alongside emerging specialized players.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Software – 58.0% (2025) |

|

Largest Technology Segment |

Barcode – 57.8% (2025) |

|

Leading Region |

North America – 36.8% (2025) |

|

Fastest Growing Region |

Asia-Pacific – High single-digit CAGR |

|

Fastest Growing Technology |

RFID – ~11.3% CAGR (2026-2034) |

|

Key End-Use Industry |

Pharmaceutical – Largest adopter globally |

|

Top Companies |

Zebra Technologies Corp., Honeywell International Inc, Cognex, SATO Corporation, ANTARES VISION S.p.A, TraceLink Inc, Optel Group |

|

Market Opportunity |

USD 7.28 Billion incremental value by 2034 |

Key Analytical Observations Supporting The Above Data:

- Software dominated the product segment at 58.0% in 2025, driven by enterprise demand for cloud-based compliance platforms, real-time serialization dashboards, and AI-powered audit trail management across pharmaceutical and food sectors.

- Barcode technology commanded 57.8% of the technology segment in 2025, underpinned by widespread infrastructure, low implementation cost, and universal compatibility with global supply chain standards including GS1 and ISO.

- RFID is the fastest-growing technology, projected to grow at ~11.3% CAGR through 2034, fueled by pharmaceutical unit-level tracking requirements, cold chain applications, and rapid deployment across retail and logistics warehouses.

- North America holds the largest regional share at 36.8% in 2025 due to the DSCSA Drug Supply Chain Security Act mandate, strong healthcare infrastructure, and high adoption of advanced track and trace software platforms.

- Asia-Pacific is the fastest-growing region, with China, India, and South Korea accelerating pharmaceutical serialization rollouts, boosting demand for both hardware scanning equipment and compliance software solutions.

- The pharmaceutical industry remains the primary end-use vertical globally, accounting for the majority of track and trace spending as companies invest in DSCSA, EU FMD, and China's drug traceability system compliance infrastructure.

Global Track and Trace Solutions Market Overview

Track and trace solutions encompass a suite of hardware and software tools designed to monitor, record, and authenticate the movement of products through supply chains. These systems assign unique identifiers - via barcodes, RFID tags, or QR codes - to individual units, enabling end-to-end visibility from manufacturing to the consumer. The ecosystem spans raw material suppliers, component manufacturers, OEM solution providers, system integrators, and end-use industries including pharmaceuticals, food and beverages, cosmetics, and logistics.

Macroeconomic tailwinds such as global trade expansion, tightening regulatory environments, and the surge in e-commerce-related logistics complexity have elevated track and trace from a compliance function to a strategic supply chain imperative. The integration of IoT sensors, cloud computing, and blockchain into these platforms is transforming the sector into a connected intelligence layer across industries.

Market Dynamics

To evaluate market opportunities, Request Sample

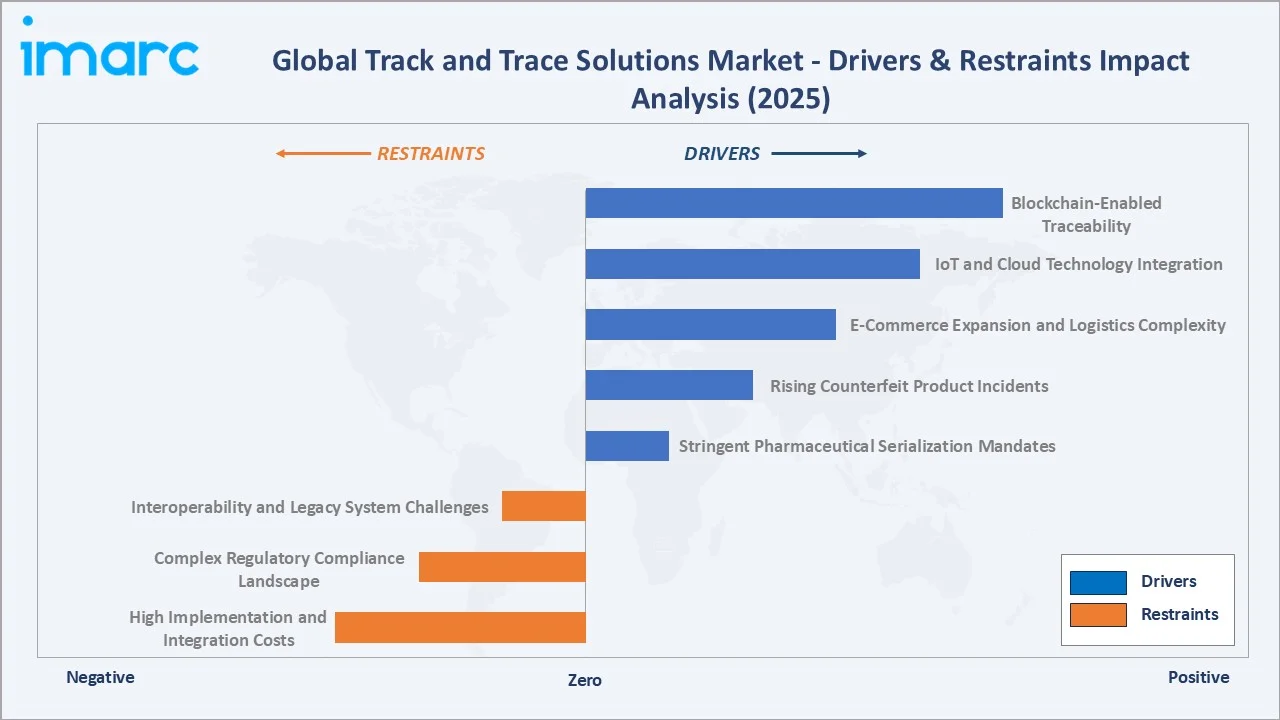

Market Drivers

- Stringent Pharmaceutical Serialization Mandates: Regulations such as the US DSCSA (effective 2023), EU Falsified Medicines Directive, and China's National Drug Administration guidelines have made unit-level serialization mandatory, compelling over 85% of pharmaceutical manufacturers globally to invest in track and trace infrastructure.

- Rising Counterfeit Product Incidents: The World Health Organization highlights that counterfeit medical products remain a significant global concern, which has driven the urgent adoption of track and trace systems across pharmaceuticals, cosmetics, and electronics, thereby strengthening overall market demand since 2020.

- E-Commerce Expansion and Logistics Complexity: Global B2C ecommerce revenue is expected to grow to USD 5.5 trillion by 2027 at a steady 14.4% compound annual growth rate, creating complex, multi-node supply chains requiring granular shipment visibility. This has accelerated adoption of barcode and RFID-based tracking across last-mile logistics providers.

- IoT and Cloud Technology Integration: The convergence of IoT-enabled smart labels, cloud-based serialization engines, and AI analytics platforms has significantly improved operational efficiency in track and trace systems since 2021, reducing total cost barriers and accelerating adoption among mid-market manufacturers.

Market Restraints

- High Implementation and Integration Costs: Large-scale serialization deployments in pharmaceutical manufacturing require substantial capital investment per production line, creating notable entry barriers for small and medium-sized enterprises operating in cost-sensitive markets.

- Complex Regulatory Compliance Landscape: With a large number of countries maintaining distinct or evolving serialization requirements, multinational companies face significant regulatory fragmentation, requiring customized solutions across jurisdictions and increasing overall compliance complexity and expenditure.

- Interoperability and Legacy System Challenges: A significant portion of manufacturing facilities continues to operate on legacy ERP or MES systems that lack native compatibility with modern track and trace platforms, creating integration challenges and extending deployment timelines across global industries.

Market Opportunities

- Blockchain-Enabled Traceability: Less than a small share of global supply chains currently leverage blockchain-based traceability, but early pilot programs in pharmaceutical and food sectors are demonstrating proven value, highlighting strong future growth potential for software vendors offering blockchain-enabled traceability solutions.

- Emerging Market Pharmaceutical Expansion: India's pharmaceutical exports exceeded USD 28 Billion in 2025, with national drug traceability systems mandating compliance for all exporters by 2026. Similar regulatory rollouts in Latin America and Southeast Asia are creating significant cumulative addressable opportunities, expanding the global track and trace solutions market and supporting long-term compliance-driven demand growth.

- Smart Packaging and Active Labelling: The integration of NFC, temperature sensors, and smart labeling technologies into packaging is expected to create a new incremental sub-segment within the track and trace solutions market, driven by expanding cold chain pharmaceutical requirements and premium food and beverage applications.

Market Challenges

- Data Privacy and Cybersecurity Risks: Centralized serialization databases containing product movement data across entire supply chains represent high-value targets for cyberattacks, with an increasing number of supply chain technology firms reporting attempted security breaches in recent years, underscoring growing cybersecurity concerns in the track and trace ecosystem.

- Workforce Skill Gaps: Deployment of advanced track and trace systems requires skilled personnel for system integration, calibration, and ongoing management, and a global shortage of qualified supply chain technology specialists is slowing deployment timelines and broader adoption across industries.

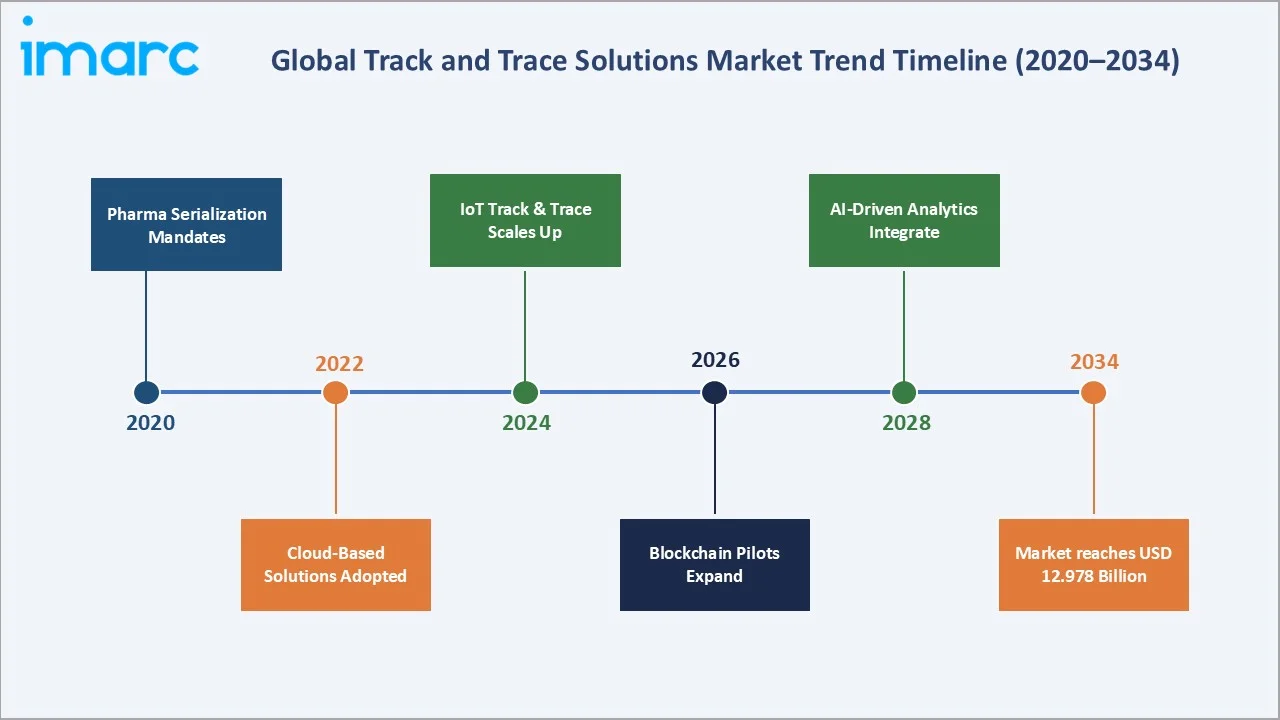

Emerging Market Trends

1. RFID Adoption Scaling Beyond Pharmaceuticals

RFID technology, historically concentrated in pharmaceutical unit-level tracking, is now expanding into retail, automotive, and logistics warehousing. The global shipment volume of RAIN UHF RFID tag chips has soared from roughly 34 billion units in 2022 to an impressive 52.8 billion in 2024—a staggering 54% increase. This volume-driven cost reduction in RFID technologies, with passive tags becoming significantly more affordable, is enabling broader adoption in previously cost-sensitive sectors.

2. Cloud-Native Serialization Platforms Replacing On-Premise Systems

Cloud-based track and trace platforms have grown at a strong double-digit rate in recent years, outpacing on-premise solutions, with a majority of new pharmaceutical serialization deployments increasingly shifting toward cloud-hosted and SaaS-based models due to faster regulatory updates and lower upfront infrastructure costs.

3. AI-Driven Supply Chain Analytics Integration

Advanced analytics modules embedded within track and trace platforms are enabling predictive capabilities such as diversion detection, counterfeit risk identification, and logistics bottleneck analysis. The AI-enhanced track and trace sub-segment is emerging as a high-growth area, driven by increasing demand for intelligent supply chain visibility and real-time decision support.

4. Blockchain for End-to-End Supply Chain Transparency

Distributed ledger technology is gaining traction as a secure and tamper-resistant foundation for serialization data. Commercial adoption is expected to accelerate in the coming years as scalability and integration challenges are progressively addressed.

5. Sustainability-Linked Traceability Requirements

ESG-driven traceability mandates—such as the EU Deforestation Regulation, emerging battery traceability requirements, and carbon footprint tracking initiatives—are creating new demand vectors for track and trace infrastructure beyond traditional pharmaceutical and food sectors, significantly expanding the market’s overall addressable opportunity by the end of the decade.

Industry Value Chain Analysis

The global track and trace solutions market value chain spans multiple integrated stages from component development through end-user deployment and data utilization. Each stage presents distinct competitive dynamics, cost structures, and technology investment requirements, shaping the overall market landscape across industries.

|

Stage |

Key Activities |

|

Raw Materials |

Ink, label substrates, RFID inlays, PCB components |

|

Component Manufacturing |

Thermal printheads, RFID chip fabrication, scanner optics |

|

OEM Manufacturing |

System assembly, firmware, hardware integration |

|

Software & Integration |

Serialization engines, cloud platforms, middleware |

|

Distribution Channels |

VARs, system integrators, direct sales, online platforms |

|

End Users |

Compliance deployment, ongoing operations, reporting |

Solution providers and platform integrators hold the highest strategic value by combining hardware, software, and analytics into end-to-end track and trace systems.

Technology Landscape in the Track and Trace Solutions Industry

Barcode Technology

Barcode technology remains the foundational layer within the track and trace solutions market, supported by widespread global adoption and compatibility across supply chains. Advances in 2D codes such as Data Matrix and QR, along with standards like GS1 Digital Link, have enhanced capabilities for unit-level serialization and high-speed processing, ensuring scalability and near-universal integration across industries.

RFID Technology

RFID accounted for 31.2% of market revenues in 2025 and is the fastest-growing technology segment. Ultra-Wideband (UWB) RFID and item-level passive UHF RFID are gaining traction for pharmaceutical unit-level tagging following US FDA guidance. RFID enables read rates of up to 1,000 items per second and eliminates line-of-sight requirements, offering significant advantages in warehouse and cold chain environments.

Smart Connectivity and IoT Integration

IoT-enabled track and trace infrastructure is increasingly integrating edge computing, real-time sensor data, and bi-directional connectivity with enterprise systems such as ERP and warehouse management platforms. This evolution is enabling capabilities like remote monitoring, predictive maintenance, and automated compliance reporting, driving greater efficiency and scalability across modern serialization deployments.

Emerging Technologies: Blockchain and AI

Blockchain enables a secure, immutable distributed ledger for serialization events, allowing multiple supply chain stakeholders to access tamper-proof product histories without relying on a central authority. At the same time, AI-powered inspection systems—including machine vision for label verification—are being integrated at the production line level, significantly enhancing accuracy, quality control, and overall system reliability in modern track and trace deployments.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Software | 58.0% | 2025 |

| Technology | Barcode | 57.8% | 2025 |

| Application | Serialization Solutions | 🔒 | 2025 |

| End Use Industry | Pharmaceutical | 26.8% | 2025 |

| Region | North America | 36.8% | 2025 |

By Product

The product segment is bifurcated into Software and Hardware, with Software leading at 58.0% of total revenues in 2025.

To access detailed market analysis, Request Sample

Software solutions are increasingly favored due to their ability to receive regulatory updates remotely, support multi-country compliance configurations, and integrate with broader enterprise platforms. Hardware remains essential as a physical interface layer, with demand for high-speed inkjet coders, laser markers, and handheld RFID readers growing alongside production capacity expansions in pharmaceuticals and food processing.

By Technology

Three primary technologies define this segment: Barcode (57.8%), RFID (31.2%), and Others including NFC, IoT sensor tags, and 2D codes (11.0%) in 2025. Barcode technology is widely adopted due to its cost-effectiveness, scalability, and compatibility with global standards, making it the preferred solution for unit-level serialization across pharmaceuticals, food, and consumer goods

Regional Market Insights

|

Region |

Market Share (2025) |

Key Drivers |

|

North America |

36.8% |

DSCSA compliance, pharma serialization, e-commerce logistics growth |

|

Europe |

28.2% |

EU FMD, EPCIS adoption, sustainability traceability mandates |

|

Asia-Pacific |

22.0% |

China NDA, India pharma exports, e-commerce warehouse RFID |

|

Latin America |

7.5% |

Brazil and Mexico pharma regulations, ANVISA compliance |

|

Middle East & Africa |

5.5% |

Gulf pharmaceutical serialization, food safety standards |

North America holds the largest regional share driven by the DSCSA requirements mandating unit-level pharmaceutical traceability across the entire US supply chain by 2023-2024. Europe follows closely at 28.2%, propelled by the EU Falsified Medicines Directive and emerging carbon footprint traceability requirements under the EU Green Deal framework.

Competitive Landscape

|

Company Name |

Brand / Division |

Market Position |

Key Strength |

|

Zebra Technologies Corp. |

Zebra |

Leader |

Broad hardware + software portfolio, global reach |

|

Honeywell International Inc. |

Honeywell Intelligrated |

Leader |

Industrial scanning, RFID, enterprise integration |

|

Cognex |

Cognex |

Leader |

Machine vision, barcode verification at line speed |

|

SATO Corporation |

SATO |

Challenger |

Healthcare-grade printers, Asia-Pacific dominance |

|

ANTARES VISION S.p.A |

DIAMIND, rfxcel |

Challenger |

End-to-end pharma serialization, EU FMD expertise |

|

TraceLink Inc |

OPUS |

Emerging |

Cloud-native serialization network, DSCSA specialist |

|

Optel Group |

Optel |

Emerging |

Vision-based track and trace, full-line solutions |

The global track and trace solutions market’s competitive landscape is moderately fragmented, with established technology providers competing alongside specialized software vendors and regional system integrators. Key players in the market include Zebra Technologies Corp., Honeywell International Inc., Cognex Corporation, SATO Corporation, Antares Vision S.p.A., TraceLink Inc., and OPTEL Group, all of which focus on enhancing digital traceability ecosystems across pharmaceutical, food, and industrial supply chains.

Key Company Profiles

Zebra Technologies Corp.

Zebra Technologies Corp. is a leading American multinational technology company specializing in data capture, asset tracking, and enterprise visibility solutions. Headquartered in Lincolnshire, Illinois, the company has evolved into a key provider of hardware, software, and automation systems that enable real-time tracking and intelligent decision-making across supply chains.

- Product Portfolio: ZT Series industrial printers, ZQ mobile printers, FX RFID fixed readers, DS series barcode scanners, Zebra DNA software suite, Savanna data intelligence platform.

- Recent Developments: In 2023, Zebra Technologies Corporation introduced new capabilities in its Zebra DNA Cloud platform, enhancing device management and supply chain visibility. The update enables flexible deployment with or without EMM systems and supports remote configuration and real-time device control, strengthening track and trace operations .

- Strategic Focus: Expanding software-as-a-service revenues, deepening healthcare vertical integration, and investing in AI-powered analytics capabilities within its enterprise platforms.

Honeywell International Inc.

Honeywell International Inc. is a leading American multinational conglomerate headquartered in Charlotte, North Carolina. Honeywell has a strong global footprint, serving customers worldwide with a workforce of over 100,000 employees and a presence across major industrial and emerging markets.

- Product Portfolio: Xenon barcode scanners, CN80 mobile computers, Vocollect voice-directed solutions, Honeywell Connected Worker platform, RFID-enabled mobile devices.

- Recent Developments: In 2026, Honeywell International Inc. launched its new Performance+ for Guided Work solution, combining voice-enabled workflows with advanced analytics to deliver real-time insights and improve supply chain visibility. The platform enhances workforce productivity, streamlines operations, and supports more efficient tracking and monitoring across logistics and warehouse environments—strengthening next-generation track and trace capabilities .

- Strategic Focus: Growing its Connected Worker and supply chain intelligence software portfolio, targeting the pharmaceutical and food & beverage verticals for cloud-based serialization deployments.

Cognex

Cognex is the world's leading provider of machine vision systems and barcode readers for industrial automation. Headquartered in Natick, with significant exposure to the pharmaceutical packaging and electronics manufacturing sectors.

- Product Portfolio: DataMan barcode readers, In-Sight vision systems, VisionPro software, Deep Learning-based inspection tools, line-speed 2D matrix readers for pharmaceutical serialization.

- Recent Developments: In 2022, Cognex Corporation introduced the DataMan 280 series of fixed-mount barcode readers, designed to enhance high-speed and accurate code reading in manufacturing and logistics. The solution supports reliable decoding of complex 1D, 2D, and DPM codes while integrating with Industry 4.0 platforms, improving production efficiency and strengthening track and trace capabilities across supply chains.

- Strategic Focus: Expanding AI-enhanced inspection capabilities, deepening pharmaceutical and medical device vertical penetration, and growing its developer ecosystem through Cognex Designer software tools.

Market Concentration Analysis

The global track and trace solutions market exhibits moderate consolidation, with the top five players - Zebra Technologies Corp., Honeywell International Inc, Cognex, SATO Corporation, ANTARES VISION S.p.A - collectively accounting for an estimated 45-50% of total market revenues in 2025.

The remaining 50-55% of the market is served by a fragmented long tail of regional specialists, niche software vendors, system integrators, and local hardware distributors. This fragmentation is especially pronounced in Asia-Pacific and Latin America, where local compliance requirements and language considerations provide regional players with competitive insulation from global vendors.

Consolidation trends are evident, with 12 notable M&A transactions recorded in the track and trace solutions sector between 2022-2025. Key deals include Antares Vision's acquisition of rfxcel to expand its cloud-native portfolio, and several RFID specialist acquisitions by Zebra Technologies. This trend is expected to continue as larger players seek to complete their end-to-end solution portfolios and accelerate software revenue growth.

Investment & Growth Opportunities

Fastest Growing Segments

- RFID Technology: The RFID sub-segment is projected at ~11.3% CAGR through 2034. Unit-level pharmaceutical serialization mandates across major markets, combined with expanding retail inventory management applications, are creating significant incremental growth opportunities for the track and trace solutions market over the forecast period.

- Cloud-Native Software Platforms: SaaS-based serialization and compliance platforms represent the fastest-growing software category, as enterprises increasingly migrate from legacy on-premise systems to cloud-based solutions, driving strong adoption and accelerating deployment across global track and trace operations.

- Asia-Pacific Market Entry: With pharmaceutical export regulations tightening across India and Southeast Asia, and e-commerce penetration accelerating warehouse RFID adoption, Asia-Pacific offers the highest risk-adjusted growth opportunity for both hardware and software vendors through 2034.

Emerging Markets

- India Pharmaceutical Serialization: India’s drug export serialization mandates are driving widespread adoption of track and trace systems across a large base of pharmaceutical exporters, creating strong demand for integrated hardware and software solutions to ensure global regulatory compliance and seamless cross-border supply chain visibility.

- ESG-Linked Traceability: Rising ESG-driven requirements, including sustainability reporting, ethical sourcing, and carbon footprint tracking, are accelerating the adoption of advanced traceability solutions across industries, creating new growth avenues for track and trace providers beyond traditional pharmaceutical applications.

Venture and Strategic Investment Trends

- Venture capital investment in track and trace software companies has seen strong momentum globally, particularly in areas such as blockchain-based traceability, AI-powered inspection, and supply chain visibility platforms targeting pharmaceutical and food sectors.

- Strategic acquirers are focusing on platform completeness - combining hardware, cloud software, and network connectivity to offer end-to-end serialization-as-a-service offerings, reducing customer complexity and increasing recurring revenue capture.

Future Market Outlook (2026-2034)

The global track and trace solutions market is positioned for sustained, broad-based growth through 2034. The market is projected to grow from USD 5.69 Billion in 2025 to USD 8.85 Billion by 2030 and further expand to USD 12.97 Billion by 2034, compounding at 9.25% annually. This trajectory is underpinned by an expanding base of regulatory mandates, technology-driven cost reductions, and the emergence of traceability as a strategic competitive differentiator.

Technological disruptions are expected to significantly reshape the competitive landscape through 2034. Declining RFID costs will enable broader item-level tracking across fast-moving consumer goods, apparel, and agricultural produce—segments that currently have limited penetration. At the same time, AI-integrated inspection systems are set to replace manual quality control at serialization lines, while blockchain-based supply chain networks will support real-time, multi-party traceability without reliance on centralized infrastructure.

Industry transformation will be driven by three converging forces: regulatory expansion beyond pharmaceuticals into new verticals (batteries, cosmetics, agricultural inputs), the maturation of connected packaging as a consumer-facing traceability tool, and the emergence of data monetization models where supply chain intelligence becomes a revenue-generating asset for manufacturers and retailers. By 2034, track and trace solutions are expected to evolve from compliance tools into comprehensive supply chain intelligence platforms, redefining the role of traceability in global commerce.

Research Methodology

Primary Research

IMARC Group's primary research involved structured interviews with over 120 industry stakeholders across the track and trace solutions value chain, including solution providers, pharmaceutical manufacturers, food and beverage companies, regulatory compliance specialists, and third-party logistics providers. Interviews covered technology adoption trends, pricing dynamics, competitive assessments, and regional market conditions.

Secondary Research

Secondary research incorporated analysis of regulatory filings, company annual reports, industry association publications (GS1, HDMA, PDA), patent databases, trade publications, and publicly available market data. Regulatory documents from the US FDA, EMA, NMPA (China), CDSCO (India), and ANVISA (Brazil) provided the compliance mandate landscape underpinning demand projections.

Forecasting Models

Market sizing and forecasting employed a combined bottom-up and top-down methodology. Bottom-up modeling aggregated demand from individual end-use industries and geographies using installation base data, compliance mandate timelines, and technology replacement cycles. Top-down validation cross-referenced aggregate estimates against vendor revenue disclosures and industry association market size estimates. CAGR projections incorporate scenario analysis across base, optimistic, and conservative regulatory and technology adoption pathways.

Track and Trace Solutions Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Technologies Covered | Barcode, RFID, Others |

| Applications Covered |

|

| End Use Industries Covered | Pharmaceutical, Medical Device, Food and Beverages, Cosmetics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Zebra Technologies Corp., Honeywell International Inc., Cognex, SATO Corporation, ANTARES VISION S.p.A, TraceLink Inc, Optel Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the track and trace solutions market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global track and trace solutions market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the track and trace solutions industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Track And Trace Solutions Market Report

The global track and trace solutions market size was valued at USD 5.69 Billion in 2025, driven by pharmaceutical serialization mandates and rising anti-counterfeit demand worldwide

The market is projected to reach USD 12.97 Billion by 2034, expanding at a CAGR of 9.25% during 2026-2034, supported by expanding regulatory requirements and technology adoption

North America dominates with a 36.8% share in 2025, primarily due to DSCSA pharmaceutical serialization mandates, strong healthcare infrastructure, and high enterprise software adoption rates.

Software leads the product segment with a 58.0% share in 2025, reflecting the shift to cloud-based compliance platforms, serialization dashboards, and enterprise integration tools.

Barcode technology commands a 57.8% share in 2025, owing to its universal compatibility, established GS1 standards, and widespread installed base across global supply chains.

RFID is the fastest-growing technology, projected at approximately 11.3% CAGR through 2034, driven by pharmaceutical unit-level tracking mandates and expanding warehouse automation.

Key drivers include pharmaceutical serialization regulations (DSCSA, EU FMD), rising counterfeit product incidents, e-commerce logistics complexity, and IoT/cloud technology integration.

Pharmaceuticals lead adoption, followed by medical devices, food and beverages, cosmetics, and logistics. Pharma alone accounts for approximately 42% of market revenues in 2025.

Asia-Pacific is the fastest-growing region, driven by China's National Drug Administration traceability mandate, India's pharmaceutical export serialization requirements, and e-commerce expansion.

Key players include Zebra Technologies Corp., Honeywell International Inc., Cognex, SATO Corporation, ANTARES VISION S.p.A, TraceLink Inc, and Optel Group.

The global track and trace solutions market is estimated at USD 8.85 Billion in 2030, representing significant growth from the USD 5.69 Billion recorded in 2025.

Blockchain enables immutable and tamper-proof serialization records that can be securely shared across multiple supply chain stakeholders.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)