Transplant Diagnostics Market Report Size, Share, Trends and Forecast by Component, Technology, Organ Type, Application, End User, and Region, 2026-2034

Transplant Diagnostics Market Size and Share:

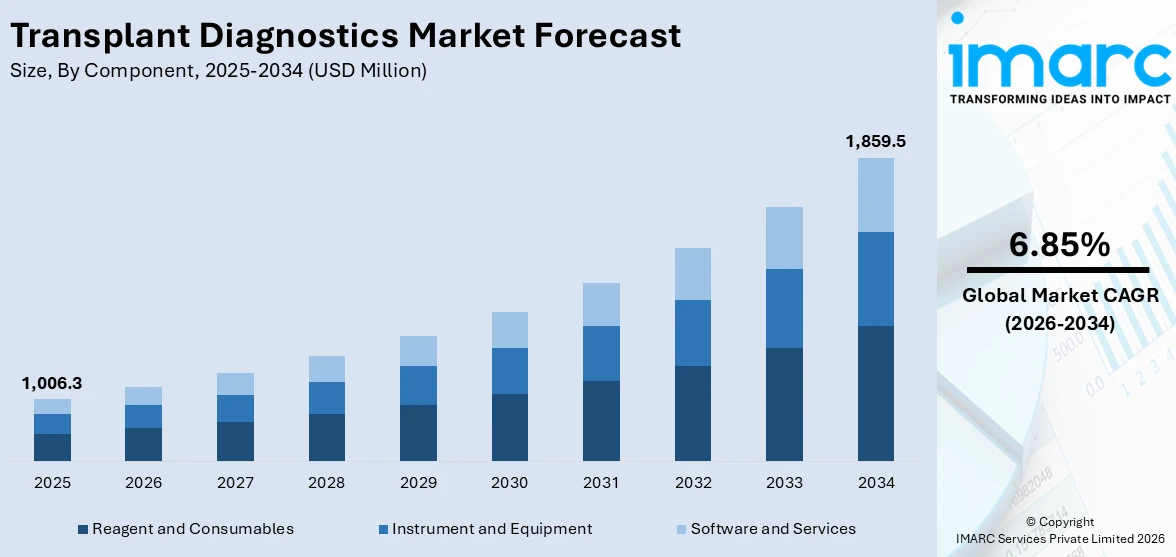

The global transplant diagnostics market size was valued at USD 1,006.3 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 1,859.5 Million by 2034, exhibiting a CAGR of 6.85% during 2026-2034. North America currently dominates the market, holding a significant market share of around 34.6% in 2025. The market is fueled by the increasing incidences of organ transplants and increasing demand for precise, fast, and non-invasive diagnostic systems to verify transplant compatibility and track post-transplant status. Furthermore, advances in molecular diagnostics, next-generation sequencing, and bioinformatics are facilitating enhanced detection of donor-recipient compatibility, risk of rejection, and infection tracking. Besides that, rising healthcare spending and supportive government programs are further augmenting the transplant diagnostics market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1,006.3 Million |

|

Market Forecast in 2034

|

USD 1,859.5 Million |

| Market Growth Rate 2026-2034 | 6.85% |

The market is propelled by advancements in non-invasive testing methods, increasing adoption of personalized medicine, and growing investments in healthcare infrastructure. Furthermore, the rising government spending on healthcare across numerous nations is driving market expansion. According to an industry report, global healthcare spending hit an all-time high of USD 9.8 Trillion in 2021, representing 10.3% of the global GDP. Besides this, rising awareness about organ donation, coupled with supportive policies from international health organizations, is fostering broader access to transplantation procedures. Additionally, the integration of artificial intelligence in diagnostic workflows is enhancing predictive accuracy for rejection risks. Also, strategic collaborations between diagnostic companies and healthcare providers are further accelerating innovation, ensuring the availability of precise, cost-efficient, and scalable testing solutions for global transplant programs.

To get more information on this market Request Sample

In the United States, the market is driven by a strong regulatory framework, high healthcare spending, and extensive adoption of cutting-edge diagnostic technologies. Moreover, the presence of specialized transplant centers with advanced laboratory capabilities facilitates rapid and reliable compatibility testing. One of the emerging transplant diagnostics market trends is the expansion of favorable insurance coverage and reimbursement policies, which encourage the use of high-value molecular and genomic assays. Apart from this, supportive initiatives and models promoting organ donation are supporting market development. For instance, in November 2024, the Centers for Medicare & Medicaid Services (CMS) finalized the six-year mandatory Increasing Organ Transplant Access (IOTA) Model, aimed at improving access to kidney transplants, enhancing quality of care, optimizing care coordination, reducing disparities, and lowering Medicare costs. Scheduled to begin on July 1, 2025, the model will involve 103 kidney transplant hospitals and will employ performance-based financial incentives and penalties to encourage increased transplant volumes, faster and more efficient organ offer acceptance, and improved graft survival rates.

Transplant Diagnostics Market Trends:

Expanding Geriatric Population

The global rise in the geriatric population is creating substantial growth opportunities for the market. Older patients are at higher risk of degenerative age-related conditions and chronic diseases like cardiovascular disease, renal failure, and liver disease, which often require transplantation of organs. According to an industry report, approximately 93% of adults aged 65 years and over suffer from at least one chronic illness. Approximately 79% suffer from two or more. Moreover, improved surgical methods and care after surgery have made transplantation increasingly possible for older patients, increasing the pool of potential candidates. The older immune system poses special challenges, with accurate and sophisticated diagnostics needed to determine compatibility and effectively control rejection risks. Additionally, pre- and post-transplant molecular testing and biomarker-directed monitoring are especially important in this population to achieve optimal therapy. With the increasing longevity of people worldwide, healthcare systems have been experiencing increased demand for organ transplantation among the elderly population, directly driving up the demand for accurate, effective, and speedy transplant diagnostic solutions compatible with the intricacies of geriatric patient management.

Rising Chronic Diseases

The growing prevalence of acute and chronic diseases on account of the increasing consumption of processed food products and the escalating number of individuals who smoke tobacco products and consume alcohol is causing a significant rise in the number of organ failure cases. This, in turn, is positively impacting the transplant diagnostics market outlook. According to reports, the burden of chronic diseases is projected to reach approximately USD 47 Trillion by 2030. Moreover, diseases like chronic kidney disease, cirrhosis, and heart failure tend to advance to end-stage organ failure, where transplantation is the most viable treatment option. This increased prevalence of chronic diseases correlates with lifestyle choices, such as poor nutrition, lack of activity, and overweight/obesity, and the increase in diabetes and hypertension. Every transplant process entails extensive pre- and post-transplant diagnostic evaluation, such as HLA typing, crossmatching, and immune monitoring, to provide the best possible outcomes for patients. The escalating chronic disease burden is not only increasing the number of transplant candidates but also leading to the implementation of sophisticated molecular and serological testing technologies in order to enhance compatibility testing, minimize chances of organ rejection, and maximize long-term graft survival rates for different types of organs.

Escalating Number of Severe Road Accidents

The rising incidence of severe road accidents is indirectly contributing to the transplant diagnostics market growth by increasing the availability of organs from deceased donors. As per industry reports, around 1.19 Million people lose their lives each year worldwide as a result of road accidents. Traumatic brain injuries and fatal accidents often result in viable organ donations, which are vital to meeting the growing demand for transplants. The availability of donor organs from such cases triggers the immediate need for fast and reliable diagnostic testing to determine donor-recipient compatibility within tight timeframes. Furthermore, technologies like real-time PCR, next-generation sequencing, and advanced crossmatching assays play a crucial role in ensuring accurate matching and reducing rejection risks. Besides this, regions with high accident rates often have robust organ procurement systems in place, further accelerating the use of transplant diagnostics. As organ shortages remain a global challenge, the unfortunate rise in fatal accidents is inadvertently sustaining the demand for rapid, high-precision diagnostic tools in transplant medicine.

Transplant Diagnostics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global transplant diagnostics market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on component, technology, organ type, application, and end user.

Analysis by Component:

- Instrument and Equipment

- Reagent and Consumables

- Software and Services

Reagent and consumables lead the market in 2025. The segment constitutes the foundation of laboratory testing protocols. They are test kits, assay reagents, buffers, and disposable lab supplies utilized for HLA typing, crossmatching, and detection of antibodies. Their continual demand arises from the fact that every diagnostic test demands fresh and accurate materials for guaranteed accurate and reliable results, which have a direct bearing on transplant compatibility tests. As organ transplant success is highly dependent on reducing the risks of rejection, the quality and availability of such consumables are critical. Moreover, the increasing rate of transplant procedures being performed globally, along with the development of molecular and serological testing technology, fuels consistent market growth for these products. Suppliers are aided by a repeat business model, as the labs need to constantly restock, and the reagents and consumables are not only critical to clinical pathways but also a big revenue division in the market.

Analysis by Technology:

- Non-Molecular Assay

- Serological Assay

- Mixed Lymphocyte Culture

- Molecular Assay

- PC-based

- Sequencing-based

Molecular assay leads the market with around 42.6% of market share in 2025. They are precise, fast, and can identify genetic differences at a detailed level. Such tests, involving PCR-based techniques and next-generation sequencing (NGS), are extensively applied to HLA typing, donor-specific antibody detection, and monitoring post-transplant immune status. By confirming gene compatibility among donors and recipients with precise accuracy, molecular tests decrease organ rejection risk and enhance long-term graft survival. Their use is increasing as healthcare systems move toward more individualized and streamlined transplant evaluation processes. The technology's capability to rapidly handle complex genetic information aids in making timely decisions, important in transplant situations in which time sensitivity can determine patient outcomes. With ongoing developments, molecular assays are transforming the future of transplant diagnostics, rendering them invaluable in pre-transplant screening and post-transplant monitoring.

Analysis by Organ Type:

- Kidney

- Liver

- Heart

- Lung

- Pancreas

- Others

Kidney leads the market in 2025 due to the large prevalence of end-stage renal failure and chronic kidney disease globally. Timely and accurate diagnostics in this segment are critical to avoid incompatibility between the donor and recipient, minimize rejection risk, and maximize graft survival rates. These include tests like HLA typing, crossmatching, and detection of donor-specific antibodies, which are applied on a routine basis prior to and after kidney transplants, making diagnosis a part of the treatment process. Transplant diagnostics in kidney transplants are also bolstered by increased numbers of live and cadaveric donor transplants, as well as technology developed in molecular diagnostics that can furnish quicker and more accurate results. Since kidney transplants continue to be the most prevalent solid organ transplant, they are still a driving force for revenue and innovation in the market.

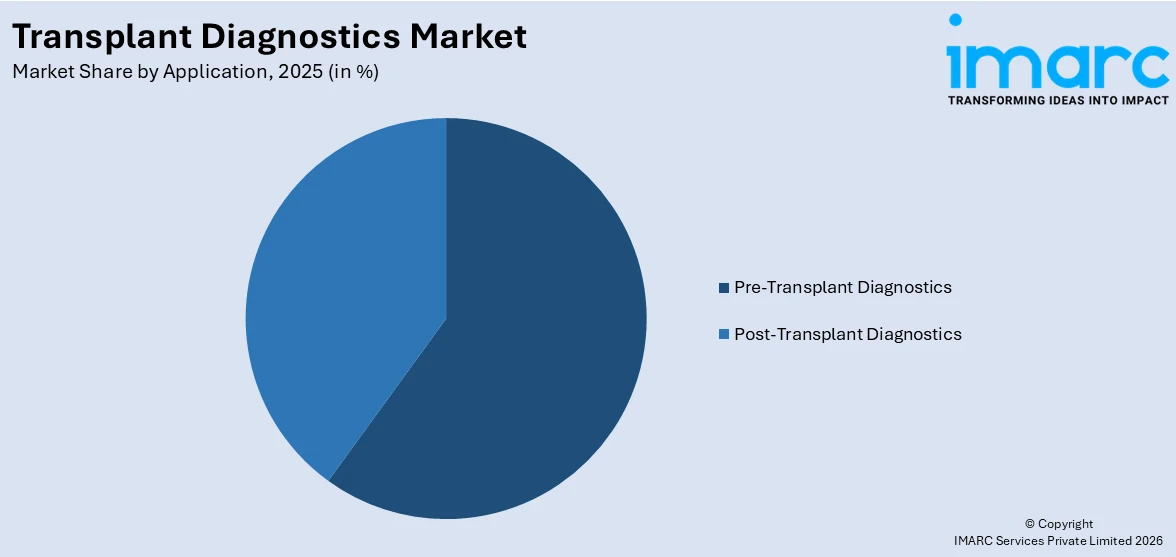

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Pre-Transplant Diagnostics

- Post-Transplant Diagnostics

Pre-transplant diagnostics are critical to assess donor-recipient compatibility and reduce the threat of graft rejection. Such tests comprise HLA typing, crossmatch, and donor-specific antibody screening, all of which identify the optimal match prior to surgery. Precise pre-transplant evaluation increases the success rate of transplants, minimizes complications, and facilitates improved long-term outcomes. Infectious disease workup is also done in addition to compatibility testing to avoid transmission of infection during transplantation. The increase in organ transplant demand and organ unavailability renders accurate and efficient pre-transplant diagnostics essential for making timely decisions. Advances in molecular tests and automation further increase test accuracy and efficiency, reinforcing their role as a cornerstone step in the process of transplantation.

Post-transplant diagnostics target the surveillance of the recipient's immune reaction to identify early indicators of rejection or infection. The tests involved are donor-specific antibody measurement, biomarker determination, and molecular testing to determine the function of the graft and immune activity. Continuous post-transplant monitoring enables clinicians to modulate immunosuppressive therapy early in the course of disease, averting irreversible transplanted organ damage. The increased uptake of non-invasive and quick testing technologies enhanced the comfort of patients and facilitated more regular monitoring, resulting in improved long-term graft survival rates. Since organ rejection may take months or years to be observed following surgery, demand for trusted post-transplant diagnosis continues to be robust. Ongoing innovation in this space is broadening the capacity for earlier detection of complications and is an essential part of integrated transplant medicine.

Analysis by End User:

- Hospitals and Transplant Centers

- Research Laboratories and Academic Institutes

- Commercial Service Providers

Hospitals and transplant centers are one of the key end users as they have direct responsibility for patient evaluation, surgery, and post-operative care. Transplant centers depend on sophisticated diagnostic instrumentation to do HLA typing, crossmatching, and immune monitoring, maximizing donor-recipient compatibility and minimizing rejection. With the increasing number of transplant procedures globally, hospitals are increasingly implementing fast and precise molecular and serological diagnostic testing methodologies to enhance patient outcomes. Most transplant centers also have specialized laboratories within their premises, allowing for quicker turnaround times for urgent diagnostic results. Their place is not just pivotal in clinical decision-making but also in managing multidisciplinary teams, thereby a prime driver for demand in the transplant diagnostics market.

Research institutes and academic institutions are involved in the market by adding innovation, method development, and validation of novel testing methods. They are engaged in developing molecular assays, discovery of biomarkers, and genomic technology to make transplants more successful and minimize complications. They are also significantly involved in clinical trials to evaluate new diagnostic tools before using them in hospitals and commercial applications. Cooperation among scientific centers and industry players serves to convert the results of research into applicable diagnostic solutions. Besides, these companies equip medical specialists and scientists with training, thereby providing the transplant community with a qualified workforce. Their efforts lead to ongoing improvement in diagnostic precision, sensitivity, and economic efficiency, which further consolidates their place in the overall transplant diagnostics system.

Commercial service providers provide specialized transplant diagnostic tests on behalf of hospitals, transplant programs, and research institutions. These firms tend to have centralized labs with high-end technologies, allowing them to provide high-throughput and accurate testing services. With outsourcing to commercial vendors, healthcare facilities can obtain specialized knowledge and complex molecular tests without huge investments in infrastructure. This is highly beneficial for small centers with limited internal capabilities. Commercial vendors also help with quality assurance, compliance with regulations, and implementation of state-of-the-art technologies, including next-generation sequencing. Their efficiency, scalability, and capacity to work with numerous clients across regions make them a fundamental piece in bridging access to timely and reliable transplant diagnostics globally.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 34.6% driven by the region's robust healthcare infrastructure, intensive use of sophisticated diagnostic technologies, and significant presence of top industry players. Moreover, the high rate of organ transplant surgeries, fueled by increasing numbers of chronic illnesses like kidney and liver failure, provides a boost to the market. Transplant centers and hospitals in the US and Canada employ cutting-edge molecular assays, next-generation sequencing, and serological testing to provide precise donor-recipient matching as well as efficient post-transplant monitoring. Supportive reimbursement policies, government programs to encourage organ donation, and research collaborations continue to enhance the market. Furthermore, North America's emphasis on innovation and high clinical trial activity rate continues to fuel advances in transplant diagnostic techniques.

Key Regional Takeaways:

United States Transplant Diagnostics Market Analysis

In 2025, the United States holds a substantial share of around 88.70% of the transplant diagnostics share in North America. The market driven by a sharp rise in chronic diseases, particularly kidney failure, diabetes, heart conditions, and liver diseases, which is increasing the demand for organ transplants in top-tier medical centers nationwide. According to an industry report published in 2024, in the United States, an estimated 129 million individuals are affected by at least one major chronic illness, such as heart disease. Moreover, 42% suffer from two or more, while 12% suffer from as many as 5. Additionally, advancements in molecular diagnostics, particularly in the areas of human leukocyte antigen (HLA) typing and next-generation sequencing, have significantly improved donor-recipient matching and transplant outcomes, increasing the adoption of sophisticated diagnostic tools. Furthermore, growing awareness among healthcare professionals and patients about the importance of early and accurate diagnostic testing in transplantation is fueling market growth. The expansion of organ transplant programs and supportive government initiatives to improve transplant infrastructure have further heightened the need for reliable diagnostic systems. The presence of technologically advanced healthcare facilities and a favorable reimbursement environment are also contributing to increased diagnostic testing. Other than this, increased investments in research and development (R&D) by key market players are resulting in more accurate, faster, and cost-effective diagnostic tools.

Asia-Pacific Transplant Diagnostics Market Analysis

In Asia‑Pacific, the market is expanding due to the rapid expansion of healthcare infrastructure and transplant programs across the region, which is increasing access to crucial diagnostic testing. For instance, in March 2023, India’s healthcare infrastructure comprises a total of 1,69,615 Sub-Centres (SCs), 31,882 Primary Health Centres (PHCs), 6,359 Community Health Centres (CHCs), 1,340 Sub-Divisional/District Hospitals (SDHs), 714 District Hospitals (DHs), and 362 Medical Colleges (MCs), spanning both urban and rural regions. Moreover, the increasing adoption of digital health technologies and laboratory automation, which enhance the efficiency and accuracy of diagnostic workflows, is also supporting industry expansion. The integration of artificial intelligence (AI) and machine learning (ML) in diagnostic platforms is also contributing to improved interpretation of complex genetic data, supporting more informed clinical decisions. Besides this, government support for transplant initiatives and favorable reimbursement policies in key nations are also encouraging the adoption of sophisticated testing systems.

Europe Transplant Diagnostics Market Analysis

The growth of the market in Europe is largely propelled by technological innovations and evolving healthcare policies. An increasing geriatric population and rising incidence of chronic conditions such as kidney disease, liver failure, and cardiometabolic disorders have heightened the demand for organ transplantation and associated diagnostics. According to reports, the number of individuals aged 65 years and older in the European Union accounted for 21.6% of the population of the region in January 2024. In parallel, breakthroughs in immunogenetics, advanced tissue‑typing platforms, and non-invasive biomarker assays are enabling more precise donor matching, early rejection detection, and optimal long‑term graft health. Increased awareness among clinicians and patients about the critical role of timely and accurate diagnostics in transplantation processes is also fueling uptake. Moreover, cross‑border healthcare initiatives and funding under pan‑European health programs are strengthening transplant networks, harmonizing diagnostic standards, and improving access across countries. A supportive reimbursement environment and alignment with personalized medicine strategies are also encouraging hospitals and laboratories to invest in sophisticated testing systems. Additionally, collaborative research efforts among academic institutions, biotech firms, and diagnostic companies are accelerating the commercialization of next‑generation assays tailored to European regulatory frameworks. The growing emphasis on quality metrics, audit compliance, and real‑world patient outcomes is further driving the adoption of standardized, high‑sensitivity diagnostic solutions.

Latin America Transplant Diagnostics Market Analysis

In Latin America, the market is significantly influenced by a growing focus on improving transplant success rates through personalized medicine and precision diagnostics. As healthcare systems strive to reduce post-transplant complications and improve long-term patient outcomes, there is an increasing demand for advanced immunological monitoring and molecular diagnostic tools. The gradual adoption of digital health and data integration technologies is also enhancing clinical decision-making and streamlining diagnostic processes. For instance, the digital health market in Brazil reached USD 10.66 Billion in 2024 and is projected to reach USD 40.85 Billion by 2033, growing at a CAGR of 16.10% during 2025-2033. Besides this, gradual enhancements in healthcare financing, insurance coverage, and reimbursement policies are making sophisticated transplantation diagnostics more accessible, supporting market growth.

Middle East and Africa Transplant Diagnostics Market Analysis

The market in the Middle East and Africa is experiencing robust growth due to the expansion of specialty healthcare facilities and the establishment of regional transplant centers catering to growing patient demand. Increasing investment in modern clinical laboratories is enabling access to advanced diagnostic methods such as immunogenetic profiling and multiplex biomarker assays. Governments in the region are also progressively prioritizing organ transplantation as part of national healthcare strategies, leading to improved funding and support for transplant-related services, including diagnostics. Additionally, the rising burden of non-communicable diseases, such as diabetes and hypertension, is leading to increased cases of organ failure and transplant need. An industry report indicates that the Middle East and North Africa region currently has 85 Million people living with diabetes, which is projected to rise to 163 million by 2050.

Competitive Landscape:

The market is characterized by intense innovations, led by the growing need for effective, timely, and non-invasive diagnostic products that can enhance patient outcomes in organ transplantation. Market players compete based on advancements in molecular diagnostics, next-generation sequencing (NGS), and polymerase chain reaction (PCR) technologies to deliver improvements in donor-recipient matching and post-transplant monitoring. Moreover, strategic partnerships with healthcare centers and research institutions are not uncommon, facilitating access to cutting-edge technology and increased global presence. In addition, regulatory compliance, quality control, and the capacity to deliver cost-efficient test solutions are foremost determinants of competitiveness. According to the transplant diagnostics market forecast, increasing transplant volumes, increasing knowledge of graft rejection detection in the early stage, and the incorporation of AI-powered data analytics are expected to sharpen competition between market players. Besides this, the emphasis on creating multiplex assays and custom testing solutions is opening new paths for differentiation, while regional growth strategies are being pursued to leverage emerging healthcare markets.

The report provides a comprehensive analysis of the competitive landscape in the transplant diagnostics market with detailed profiles of all major companies, including:

- Abbott Laboratories

- Becton Dickinson and Company

- bioMérieux SA

- Bio-Rad Laboratories Inc.

- F. Hoffmann-La Roche AG

- Hologic Inc.

- Illumina Inc.

- Immucor Inc. (IVD Holdings Inc.)

- Merck KGaA

- Qiagen N.V.

- Thermo Fisher Scientific Inc.

Latest News and Developments:

- July 2025: Plexision disclosed that it secured USD 365,000 in financing from the Richard King Mellon Foundation. The investment will be utilized to expedite the implementation of AI and ML capabilities across Plexision's range of cell-based blood tests in order to greatly increase the predicted accuracy for complex organ transplant outcomes.

- July 2025: Pirche AG established a partnership with the Mayo Clinic for the development of a novel digital risk prediction program to guide biomarker monitoring and organ transplant immunosuppression approaches. As part of this agreement, the Mayo Clinic will contribute its clinical expertise and scientific data to help develop the product, while Pirche will utilize its experience in transplant bioinformatics solutions to create and market the new Outcomes Prediction Module as a part of its TxPredictor platform.

- February 2025: Researchers at Mass General Brigham successfully developed a urine test for the non-invasive detection of kidney transplant rejection. The ExoTRU™ test, licensed by Thermo Fisher, is presently awaiting FDA authorization and can predict kidney transplant rejection years before it happens.

- February 2025: Pirche AG established a partnership with Devyser AB, a prominent provider of transplant diagnostics solutions. The collaboration intends to showcase how Pirche's TxPredictor Platform, an AI-based tool that supports clinical decision-making by offering superior immune profiling and risk prediction features, can provide more individualized monitoring with a suite of innovative biomarkers created by Devyser.

Transplant Diagnostics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Segment Coverage |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Instrument and Equipment, Reagent and Consumables, Software and Services |

| Technologies Covered |

|

| Organ Types Covered | Kidney, Liver, Heart, Lung, Pancreas, Others |

| Applications Covered | Pre-Transplant Diagnostics, Post-Transplant Diagnostics |

| End Users Covered | Hospitals and Transplant Centers, Research Laboratories and Academic Institutes, Commercial Service Providers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, Becton Dickinson and Company, bioMérieux SA, Bio-Rad Laboratories Inc., F. Hoffmann-La Roche AG, Hologic Inc, Illumina Inc., Immucor Inc. (IVD Holdings Inc.), Merck KGaA, Qiagen N.V. and Thermo Fisher Scientific Inc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the transplant diagnostics market from 2020-2034.

- The transplant diagnostics market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the transplant diagnostics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Transplant Diagnostics Market Report

The transplant diagnostics market was valued at USD 1,006.3 Million in 2025.

The transplant diagnostics market is projected to exhibit a CAGR 6.85% of during 2026-2034, reaching a value of USD 1,859.5 Million by 2034.

The market is driven by the increasing number of organ transplants, growing demand for precise donor-recipient matching, and rising adoption of advanced molecular diagnostic tools. Technological innovations, supportive government programs, and heightened awareness about early detection of transplant rejection are further propelling market growth across healthcare facilities and research organizations.

North America currently dominates the transplant diagnostics market with a market share of around 34.6%. The dominance is fueled by the region’s advanced healthcare infrastructure, high adoption of innovative diagnostic technologies, significant healthcare spending, and the presence of leading industry players, alongside strong regulatory support for transplant-related diagnostic advancements.

Some of the major players in the transplant diagnostics market include Abbott Laboratories, Becton Dickinson and Company, bioMérieux SA, Bio-Rad Laboratories Inc., F. Hoffmann-La Roche AG, Hologic Inc, Illumina Inc., Immucor Inc. (IVD Holdings Inc.), Merck KGaA, Qiagen N.V., and Thermo Fisher Scientific Inc., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)