Travel Insurance Market Size, Share, Trends and Forecast by Insurance Type, Coverage, Distribution Channel, End User, and Region, 2026-2034

Travel Insurance Market Size, Share, Trends & Forecast (2026-2034)

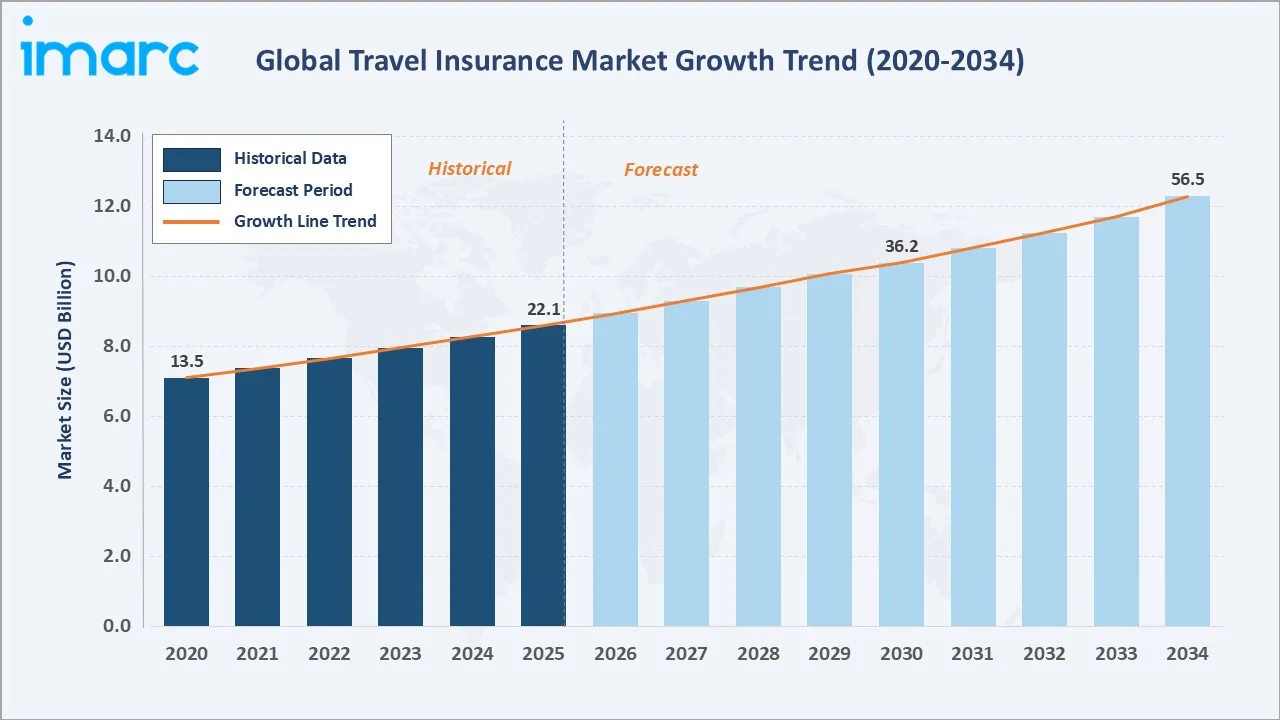

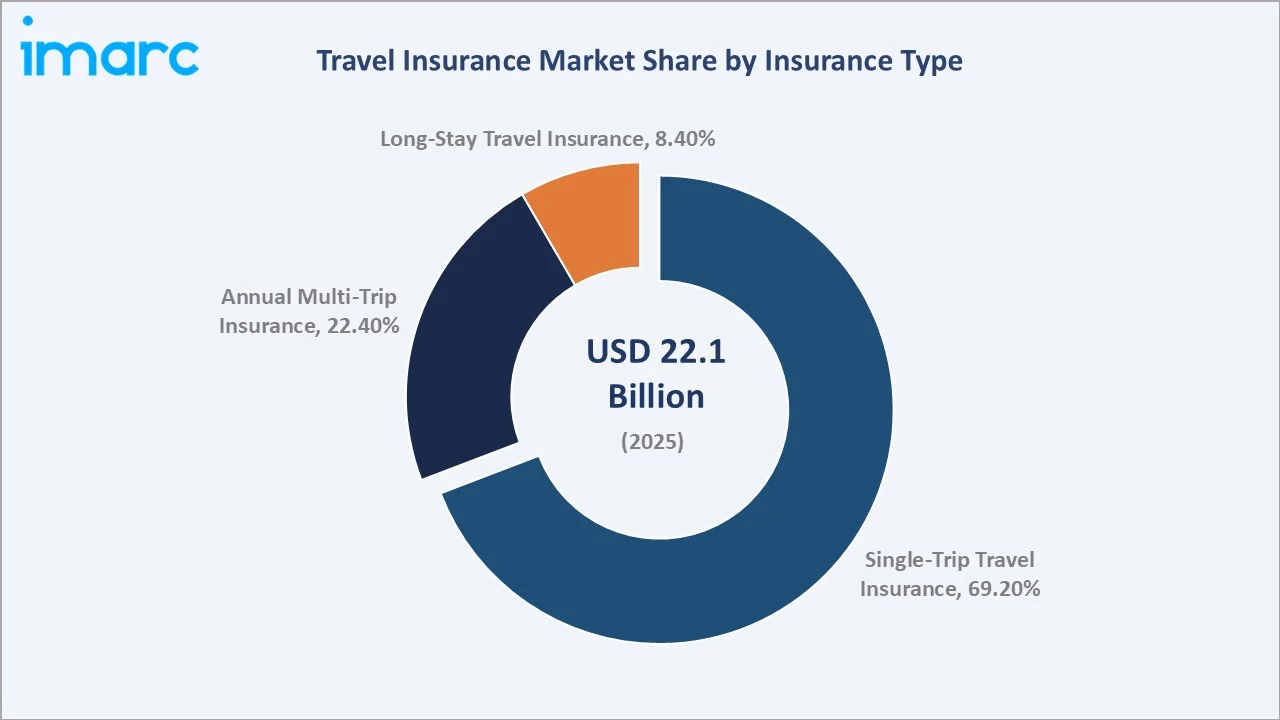

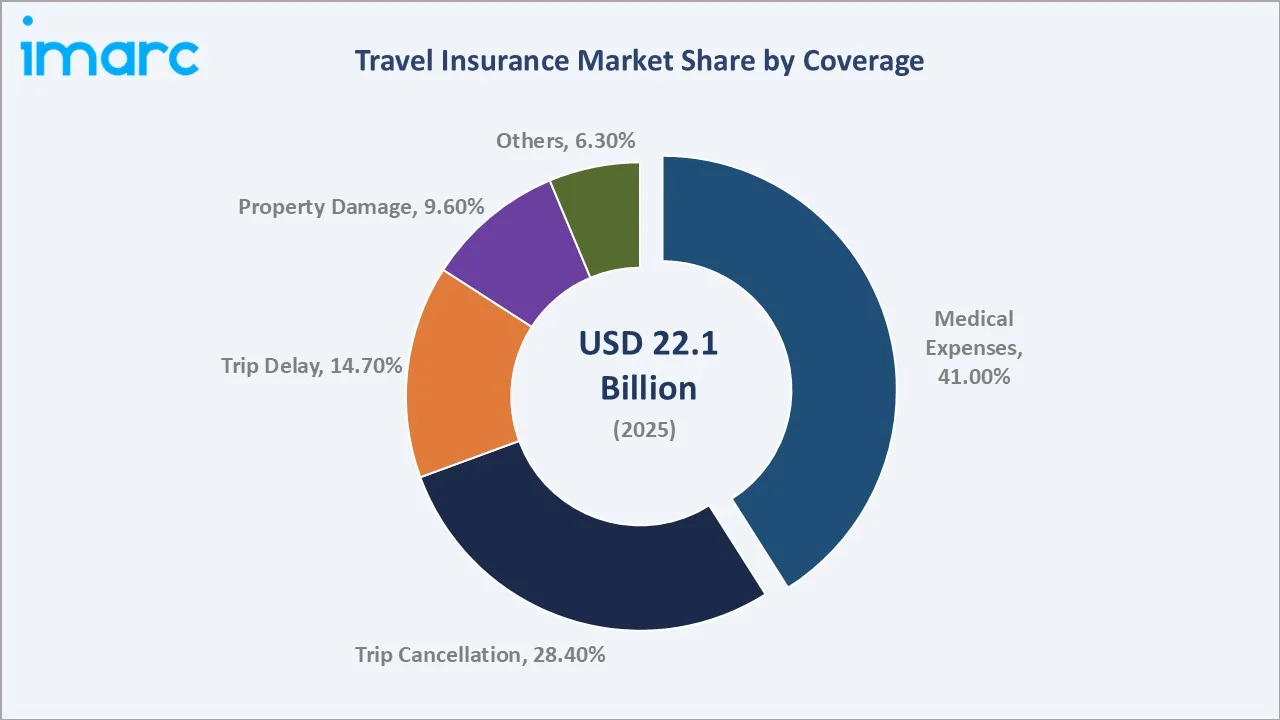

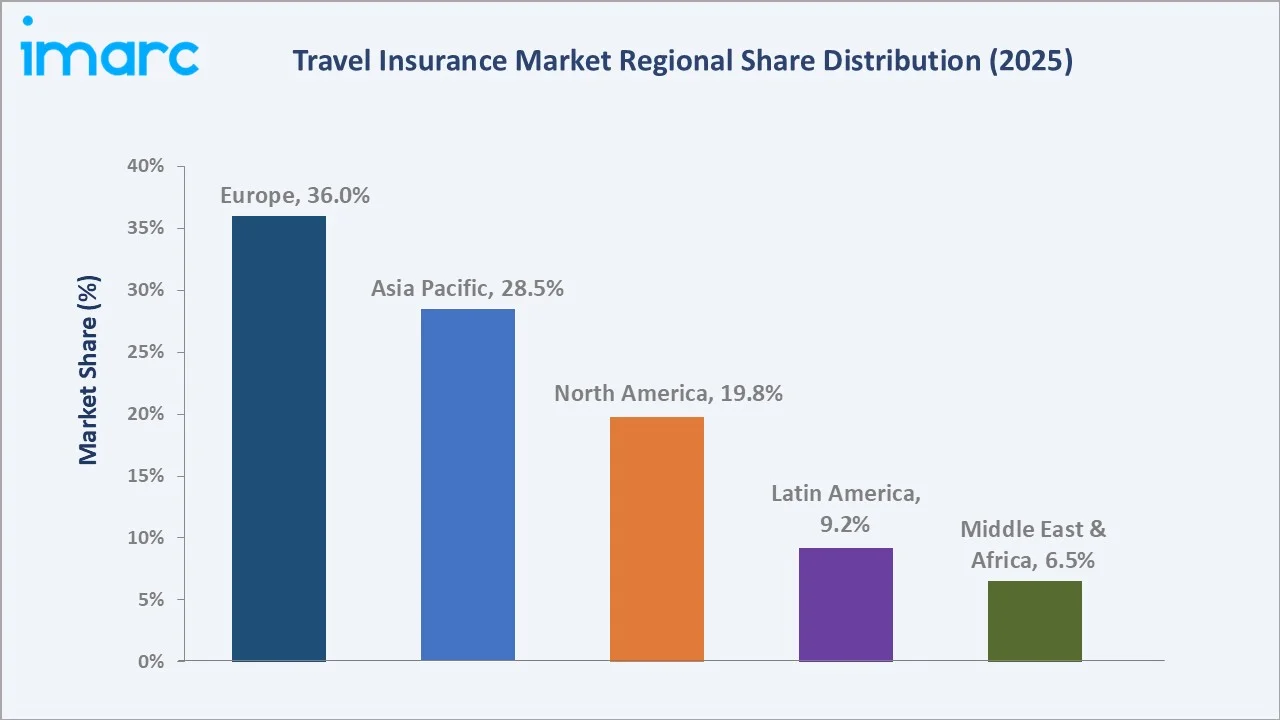

The global travel insurance market size reached USD 22.1 Billion in 2025 and is projected to reach USD 56.5 Billion by 2034, expanding at a CAGR of 10.40% during the forecast period. Growth is propelled by accelerating international tourism, rising traveler awareness of financial risks, and rapid digitalization of insurance distribution. Europe leads with a 36.0% regional share in 2025, while Asia Pacific emerges as the fastest-growing region. Single-trip travel insurance dominates at 69.2% by insurance type, while medical expenses coverage leads at 41.0% by coverage type. Key market participants include Allianz SE, AXA SA, Zurich Insurance Group, Generali Global Assistance, and Berkshire Hathaway Specialty Insurance.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 22.1 Billion |

|

Forecast Market Size (2034) |

USD 56.5 Billion |

|

CAGR (2026-2034) |

10.40% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (36.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

To get more information on this market, Request Sample

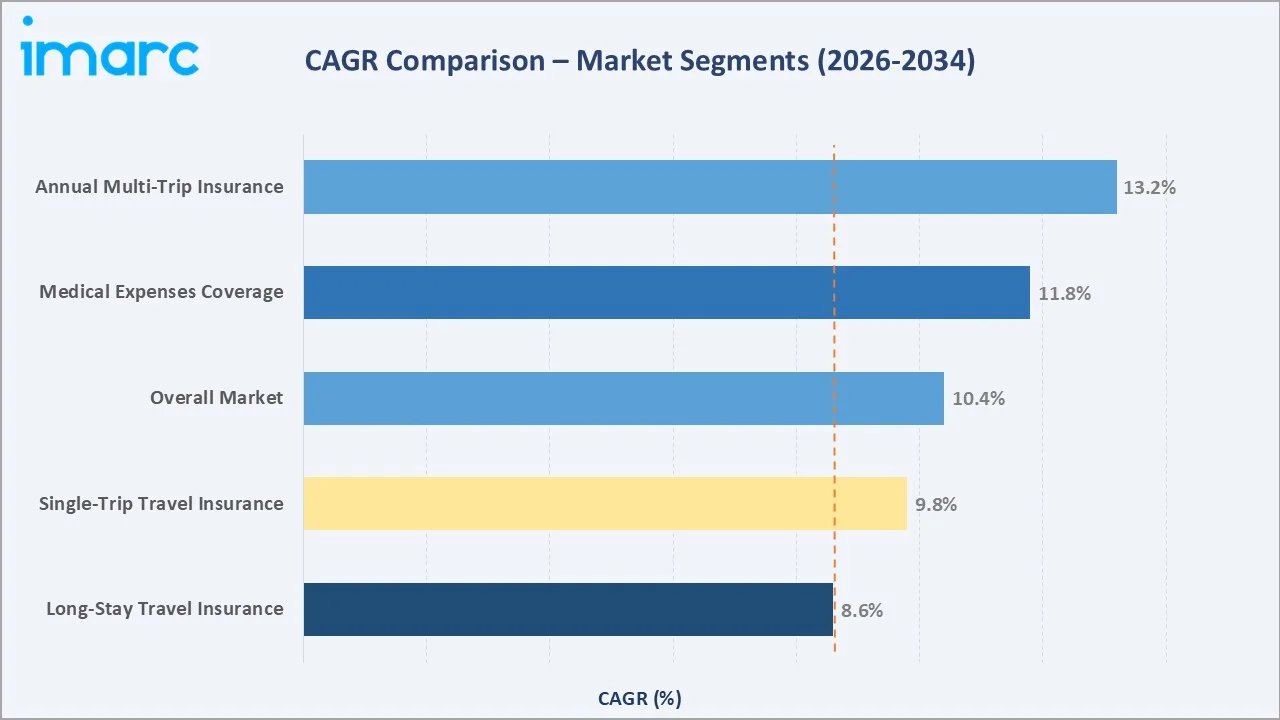

Segment-level CAGR comparisons highlight Asia Pacific and annual multi-trip insurance sub-categories as the fastest-growing areas within the global avocado processing industry through 2034.

Executive Summary

The global travel insurance market continues to demonstrate robust expansion, underpinned by rising international travel volumes, heightened traveler risk awareness post-COVID-19, and accelerating digital transformation of insurance distribution. Valued at USD 22.1 Billion in 2025, the market is forecasted to reach USD 56.5 Billion by 2034 at a CAGR of 10.40%. The proliferation of embedded insurance models - wherein coverage is offered seamlessly at the point of travel booking on OTA platforms - has significantly broadened consumer access and driven notable volume growth across both leisure and corporate travel segments.

Among the key growth drivers, the increasing focus on financial protection during overseas travel - particularly for medical emergencies, trip cancellations, and baggage loss - remains a primary catalyst. Medical expenses coverage alone represented 41.0% of total market revenue in 2025, reflecting the high financial exposure from overseas hospitalization. The single-trip insurance segment commands 69.2% of the market, while annual multi-trip policies gain traction among frequent travelers at 22.4%. Digital-first insurers and InsurTech entrants are intensifying competition through AI-powered underwriting and real-time claims platforms.

Europe retains market leadership with a 36.0% share (2025), supported by Schengen visa requirements mandating minimum EUR 30,000 medical travel coverage. Asia Pacific, at 28.5%, is the fastest-growing region driven by expanding middle-class outbound travel from China and India. North America contributes 19.8%, anchored by high per-capita travel expenditure and corporate travel demand. Leading insurers are investing in product innovation, digital infrastructure, and emerging market expansion - all key areas reshaping the competitive landscape through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Insurance Type) |

Single-Trip Travel Insurance - 69.2% share (2025) |

|

Largest Segment (Coverage) |

Medical Expenses - 41.0% share (2025) |

|

Leading Region |

Europe - 36.0% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~12.5%, 2026-2034) |

|

Top Companies |

Allianz SE, AXA SA, Zurich Insurance, Generali, Berkshire Hathaway |

|

Market Opportunity |

Digital/embedded insurance channel projected at USD 18+ Billion by 2034 |

Key Analytical Observations Supporting The Above Data:

- Single-trip travel insurance dominates with a 69.2% share (2025), driven by the global prevalence of one-off leisure travelers. These policies offer cost-efficient, trip-specific coverage, making them the default choice for infrequent international travelers across all income groups and geographies.

- Medical expenses coverage leads all coverage types at 41.0% (2025). Overseas hospitalization in the United States can exceed USD 30,000 per incident, making medical coverage the primary purchase motivator - especially for travelers visiting high-cost healthcare destinations such as the U.S., Switzerland, and Japan.

- Europe accounts for 36.0% of global revenues (2025). The Schengen Area's mandatory minimum travel insurance requirement of EUR 30,000 medical coverage directly stimulates baseline demand across all 27 EU member states, creating a structurally resilient demand foundation.

- Annual multi-trip insurance holds 22.4% market share (2025) and is expanding at an accelerating pace as frequent business travelers and senior frequent fliers seek a cost advantage over equivalent per-trip policies.

- Asia Pacific, representing 28.5% of the market in 2025, is forecast to post the highest regional CAGR through 2034, supported by projected 4.6% annual outbound travel growth from China and India and rapid digital insurance adoption through smartphone platforms.

Global Travel Insurance Market Overview

Travel insurance constitutes a specialized segment within the broader non-life insurance sector, providing policyholders with financial protection against losses incurred during domestic and international travel. Coverage categories encompass medical emergencies, trip cancellations, baggage loss, flight delays, and personal liability. The ecosystem spans reinsurers, specialty insurers, travel assistance providers, distribution intermediaries - including travel agents, OTAs, and airlines - and end consumers ranging from leisure tourists and business travelers to students, expatriates, and senior citizens.

Macroeconomic tailwinds - including rising disposable incomes, expanding middle-class populations in emerging markets, and the normalization of international travel following the COVID-19 disruption - are structurally supporting long-term market growth. Global tourism receipts reached USD 1.6 trillion in 2023 per UNWTO, with full recovery to pre-2019 travel levels achieved by 2024. Schengen visa mandates, corporate travel risk policies, and growing awareness of uninsured healthcare exposure collectively sustain the structural demand foundation for travel insurance globally.

The technological transformation of the industry - through AI-based underwriting, mobile-first policy management, parametric trigger-based products, and real-time digital claims processing - is expanding product accessibility and improving customer retention. By 2034, travel insurance is expected to be embedded in the majority of premium travel bookings globally, reflecting its growing status as an indispensable travel service rather than an optional purchase.

Market Dynamics

To evaluate market opportunities, Request Sample

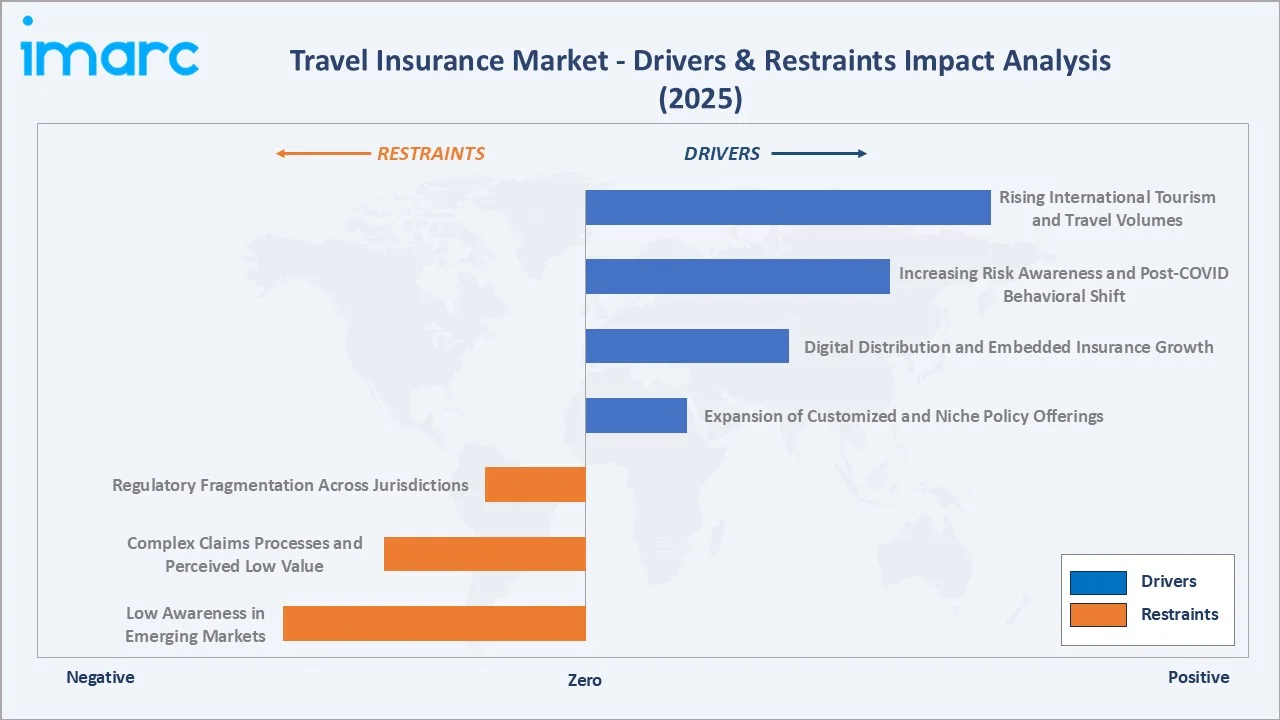

Market Drivers

- Rising International Tourism and Travel Volumes: Global international tourist arrivals rebounded to 1.4 billion in 2024 and are projected to surpass 1.8 billion by 2030 per the UNWTO. Higher travel frequency directly expands the addressable base for travel insurance, particularly in high-risk long-haul corridors connecting Asia, Europe, and the Americas.

- Increasing Risk Awareness and Post-COVID Behavioral Shift: Post-pandemic sensitivity to travel disruptions has structurally increased. A 2024 USTIA survey found 47% of American travelers purchased trip insurance - up from 34% in 2019 - reflecting a sustained behavioral change in how consumers perceive and manage travel-related financial risk.

- Digital Distribution and Embedded Insurance Growth: Integration of travel insurance into OTA booking flows via platforms like Expedia and Booking.com has significantly reduced purchase friction.

- Expansion of Customized and Niche Policy Offerings: Insurers are introducing hyper-personalized products addressing adventure travel, medical tourism, senior travelers, and digital nomad scenarios. Niche product development is broadening the purchaser demographic and increasing attachment rates at travel booking checkouts globally.

These drivers collectively reinforce a virtuous cycle of market expansion - rising travel frequency amplifies risk exposure, which drives insurance demand, which attracts digital platform investment, enabling broader product accessibility and higher attach rates across all consumer segments.

Market Restraints

- Low Awareness in Emerging Markets: Insurance penetration among outbound travelers from Southeast Asia and Sub-Saharan Africa remains below 20%, constrained by limited financial literacy, low trust in insurance products, and insufficient distribution infrastructure in underserved geographies.

- Complex Claims Processes and Perceived Low Value: According to J.D. Power, delays in claims settlement timelines are a major source of customer dissatisfaction, with satisfaction levels dropping as the time taken to settle claims increases - highlighting the critical need for claims experience improvement across the industry.

- Regulatory Fragmentation Across Jurisdictions: Divergent regulatory frameworks across Southeast Asia and Latin America complicate policy standardization and cross-border product distribution, increasing compliance costs for global insurers seeking to scale in multiple markets simultaneously.

Market Opportunities

- Untapped Emerging Market Potential: Asia Pacific, Latin America, and the Middle East collectively represent hundreds of millions of under-insured travelers. OECD analysis shows that around 1.2 billion people joined the middle class in developing countries over recent decades, underscoring the rapid expansion of middle-income populations and the structural opportunity this creates for insurers to localize products and digital distribution.

- AI-Driven Personalization and Parametric Insurance: AI enables real-time risk assessment and on-demand parametric products triggering automatic payouts upon pre-defined events (e.g., flight delays exceeding two hours).

- Strategic Insurer-Airline and OTA Partnerships: Embedded, co-branded insurance partnerships with leading airlines such as Emirates, Singapore Airlines, and Delta Air Lines offer highly scalable distribution, with industry benchmarks suggesting attach rates of ~10–20% per booking in well-optimized digital journeys.

Market Challenges

- Pricing Pressure and Commoditization: Proliferation of price comparison websites has intensified premium competition, compressing underwriting margins. Average premium per policy fell approximately 4.2% between 2021 and 2024 in the European market due to heightened platform-based price transparency.

- Cybersecurity and Data Privacy Risks: As digital distribution grows, travel insurers handle increasingly sensitive personal and financial data. GDPR compliance and analogous Asia Pacific frameworks require ongoing cybersecurity investment, raising operational costs for all market participants.

- Climate Change and Increased Catastrophe Exposure: Rising frequency of extreme weather events is expanding claims liability for trip cancellation and interruption coverage.

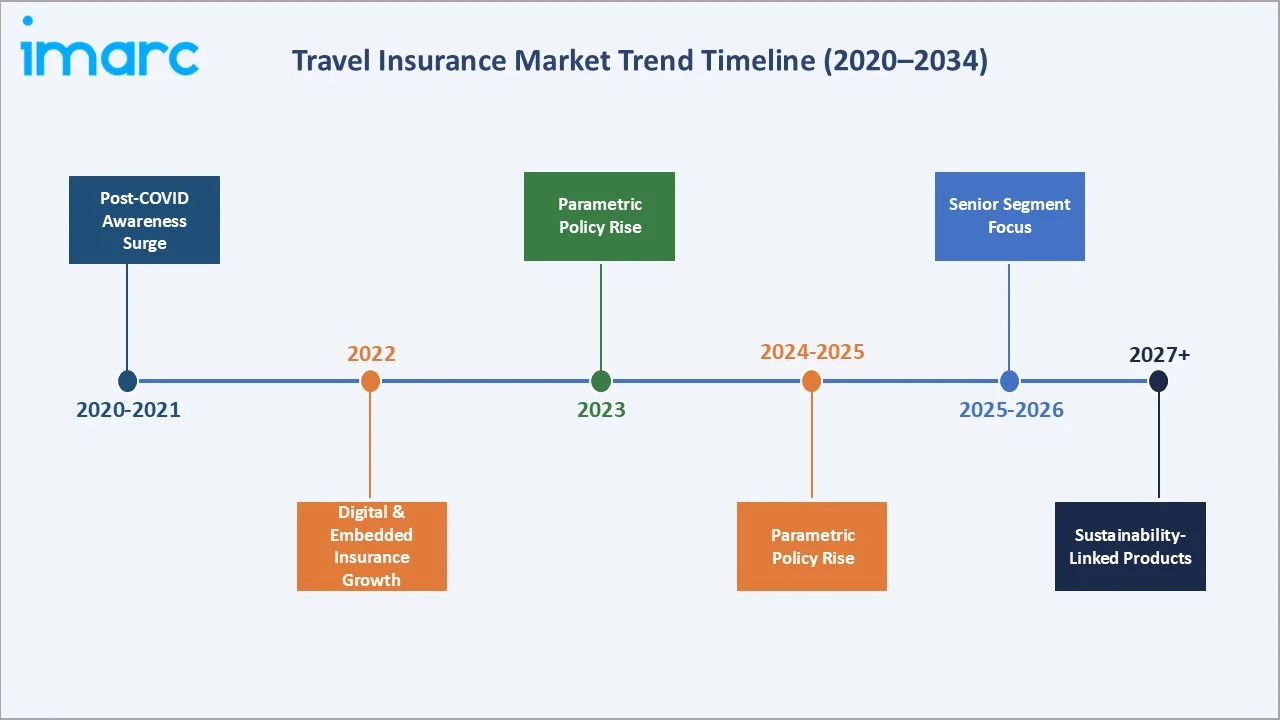

Emerging Market Trends

1. Digitalization and Embedded Insurance

The shift toward fully digital insurance journeys - from quote to claims - is the most transformative trend reshaping the market. Leading insurers such as Allianz and AXA have made significant multi-year investments in digital platforms and technology transformation initiatives, focusing on improving customer experience, operational efficiency, and embedded insurance capabilities.

2. AI-Driven Underwriting and Claims Automation

Machine learning algorithms now process real-time traveler profiles, destination risk indices, and weather forecasts to generate dynamic pricing within milliseconds. Automated claims platforms are significantly reducing settlement times—from days or weeks to, in some cases, hours—while materially improving customer satisfaction and Net Promoter Scores, ultimately strengthening policyholder retention.

3. Parametric and On-Demand Travel Insurance

Parametric products - triggered automatically upon objectively verified events such as flight cancellations or declared natural disasters - are gaining rapid market acceptance.

4. Growth of Senior Traveler and Medical Tourism Segments

Senior travelers (aged 60+) account for 31.0% of end-user share in 2025 and represent the fastest-growing demographic within the travel insurance buyer universe. This cohort demands higher medical coverage limits and pre-existing condition waivers. This is further driving demand for health-and-travel crossover policies.

5. Sustainability-Linked Insurance Products

Environmental consciousness is emerging as a product differentiator in mature markets. European insurers are increasingly incorporating sustainability features into travel insurance offerings, including carbon offset options and ESG-aligned products, while consumer surveys indicate growing preference for eco-conscious travel and insurance choices.

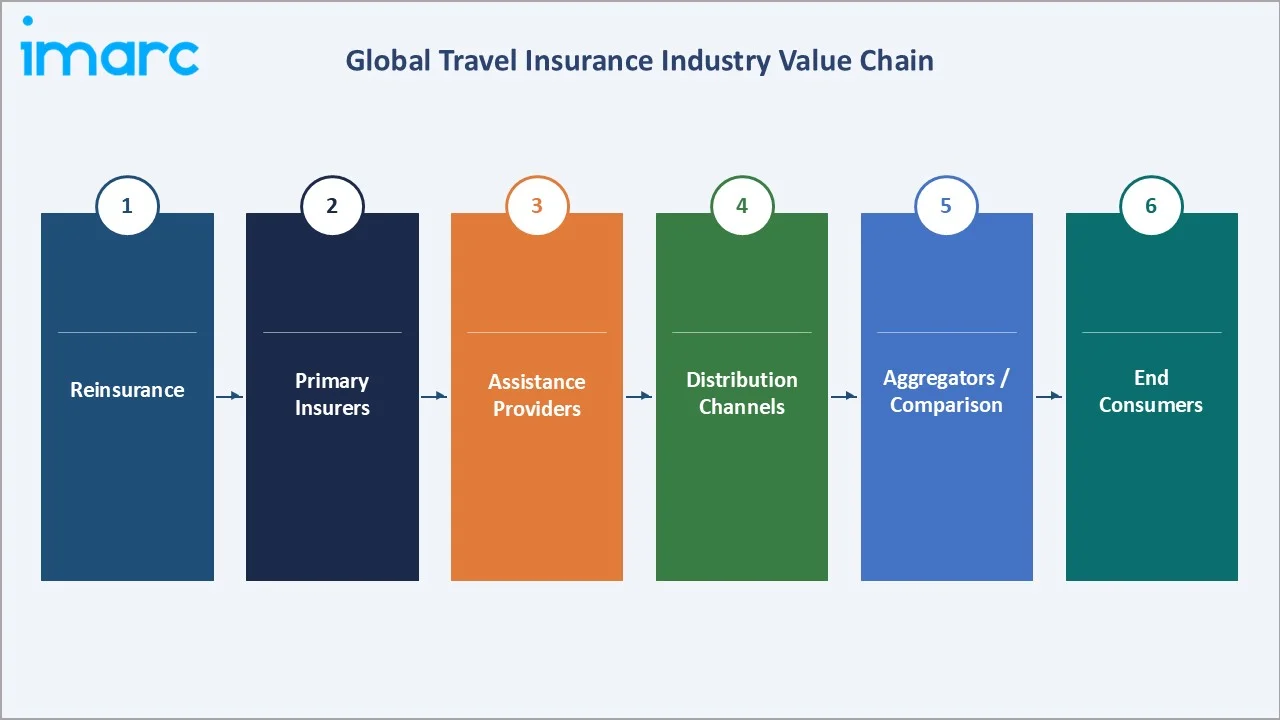

Industry Value Chain Analysis

The travel insurance value chain encompasses multiple interconnected stages, from risk capacity provision to end consumer policy delivery. Each stage is populated by specialized operators whose performance directly influences product pricing, coverage quality, claims efficiency, and market accessibility across global geographies.

|

Stage |

Key Players / Examples |

|

Reinsurance |

Swiss Re, Munich Re, Hannover Re, Gen Re |

|

Primary Underwriting |

Allianz SE, AXA SA, Zurich Insurance Group, Generali, Berkshire Hathaway Specialty |

|

Assistance Services |

International SOS, Europ Assistance, Global Excel Management |

|

Direct Distribution |

Insurer websites, mobile apps (e.g., Allianz Travel app, AXA Travel app) |

|

Indirect Distribution |

Travel agents, brokers, airlines, OTAs (Expedia, Booking.com, MakeMyTrip) |

|

Aggregators / Comparison |

InsureMyTrip, Squaremouth, MoneySuperMarket, PolicyBazaar |

|

End Consumers |

Leisure travelers, business travelers, senior citizens, students, expatriates |

.webp)

Technology Landscape in the Travel Insurance Industry

AI and Machine Learning Underwriting

AI-powered underwriting engines enable real-time, granular risk assessment at the individual traveler level. Algorithms integrate destination health risk indices, historical claims data, traveler age profiles, and trip itinerary complexity to generate dynamically priced quotes within seconds. Early adopters, including Allianz and AXA, have reported 8-12% improvement in loss ratios from AI deployment between 2022 and 2024.

Digital Claims Processing and Automation

Automated digital claims platforms are transforming the post-purchase customer experience. Straight-through processing rates for low-complexity claims reached 78% at leading insurers in 2024. InsurTech firms, including Cover Genius and Faye, have demonstrated average claim settlement timelines of under 48 hours through app-based claims submission and instant digital wallet disbursements.

Parametric Insurance and IoT Integration

Parametric products leveraging real-time flight data, weather APIs, and natural disaster alert systems are creating an entirely new product paradigm. IoT-enabled wearables are beginning to provide live health data feeds for medical emergency response optimization. The global parametric insurance market, inclusive of travel applications, is forecast to grow at 18.5% CAGR through 2034.

Mobile Platforms and Super-App Integration

Mobile-first insurance purchasing is now the primary acquisition channel across the Asia Pacific. Integration of travel insurance into super-app ecosystems - including WeChat, Grab, and Paytm - has unlocked mass market distribution at near-zero marginal acquisition cost. Mobile app–based insurance purchases are growing rapidly across Southeast Asia, driven by the rise of super-app ecosystems such as Grab and Gojek, highlighting the transformative potential of embedded, mobile-first insurance distribution.

Market Segmentation Analysis

By Insurance Type

The single-trip travel insurance sub-segment dominates the market with a 69.2% share (2025), driven by the global prevalence of one-off leisure and family travel. These policies provide cost-efficient, trip-specific coverage with minimal commitment, making them the default choice for the large majority of international travelers. Annual multi-trip insurance accounts for 22.4% of revenues, particularly among frequent business and senior travelers, offering meaningful cost savings compared to repeated single-trip purchases and increasing convenience through year-round coverage.

To access detailed market analysis, Request Sample

Long-stay travel insurance commands an 8.4% share in 2025, gaining traction from the rising digital nomad population, gap-year travelers, and medical tourism participants requiring extended international coverage beyond 60-90 days. Over 35 million people globally self-identify as digital nomads as of 2024, representing a fast-growing long-stay insurance segment across North America, Europe, and Southeast Asia.

By Coverage

Medical expenses coverage leads all coverage types with a 41.0% share (2025), reflecting the primacy of health risk as the core purchase motivator for travel insurance globally. Overseas medical care costs have escalated significantly - Emergency medical treatment in the United States can cost tens of thousands of dollars for uninsured foreign visitors, with hospitalization expenses often ranging between USD 25,000 and USD 50,000 per incident, according to insurer and healthcare cost estimates. Trip cancellation coverage holds a 28.4% share, driven by growing consumer awareness of non-refundable travel bookings, with purchase rates rising approximately 38% between 2019 and 2024 following the COVID-19 experience.

Trip delay (14.7%), property damage (9.6%), and other coverage types (6.3%) collectively address diverse traveler risk profiles spanning baggage protection, personal liability, and adventure sports coverage. The adventure sports coverage sub-segment is growing at above-market rates, driven by the rising popularity of adventure tourism - a global market estimated at USD 1.1 trillion by 2030.

Regional Market Insights

|

Region |

Share |

Key Growth Drivers |

Key Dynamics |

Major Companies |

|

Europe |

36.0% |

Schengen visa mandate, mature insurance culture, and high travel frequency |

Stable; digital channel growth |

Allianz, AXA, Zurich, Generali |

|

Asia Pacific |

28.5% |

Middle-class expansion, outbound travel growth, and digital adoption |

Fastest growing, super-app |

Tata AIG, AIA, AXA Asia |

|

North America |

19.8% |

High per-capita travel, corporate demand, and InsurTech innovation |

Mature; InsurTech disruption |

Berkshire Hathaway, Allianz Partners |

|

Latin America |

9.2% |

Rising middle class; digital payments; Brazil & Mexico outbound |

Emerging; mobile-led |

Mapfre, Allianz, AXA |

|

Middle East & Africa |

6.5% |

Hajj/Umrah travel; medical tourism; GCC outbound travel |

Nascent; high potential |

AXA Gulf, Salama, Allianz MENA |

Europe's market leadership (36.0%, 2025) is deeply entrenched. The Schengen Area's mandatory EUR 30,000 medical coverage requirement creates a structurally stable demand floor, with Germany, the UK, and France registering insurance attach rates above 40% per international trip. Despite market maturity, digital transformation and sustainability-linked product innovation are generating new growth vectors for established insurers.

Asia Pacific is the clear growth engine with China's outbound tourism market projected to reach 176.65 million departures by 2029. India's travel insurance market is expected to grow at approximately 15.2% CAGR through 2034, supported by rising disposable incomes and government-backed digitalization of financial services through the ONDC framework.

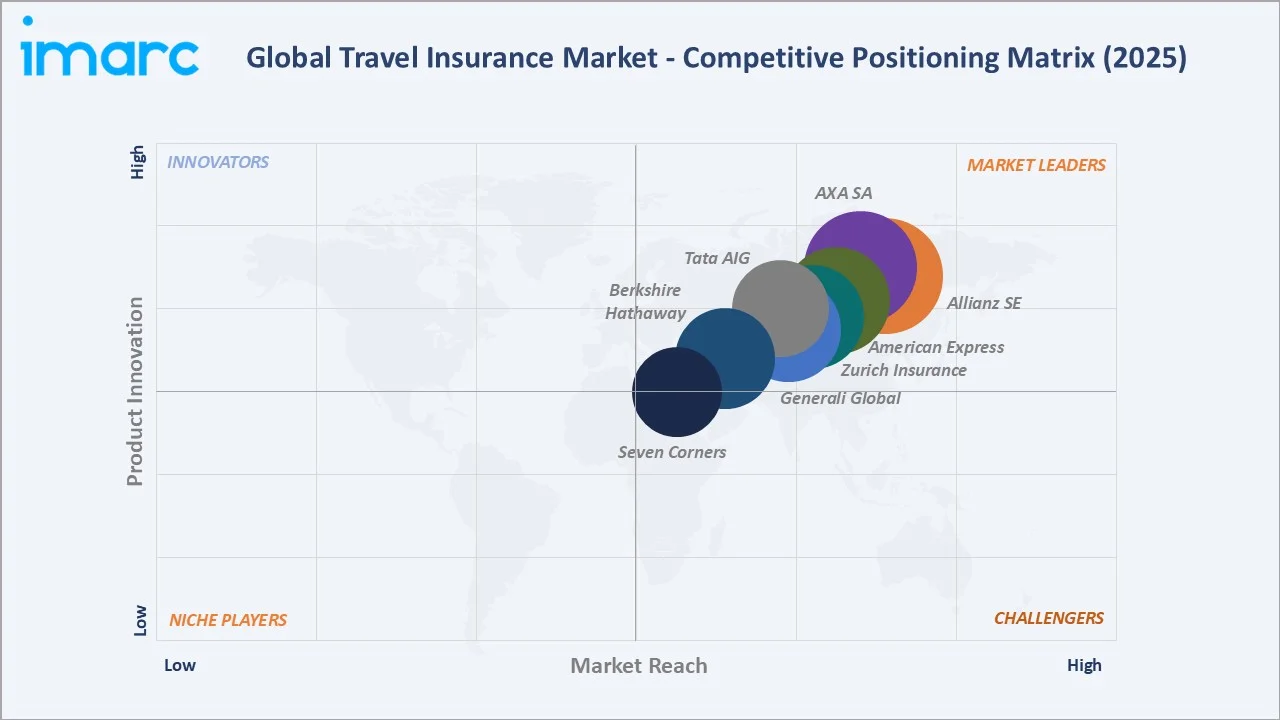

Competitive Landscape

The global travel insurance market exhibits moderate consolidation, with the top five players - Allianz SE, AXA SA, Zurich Insurance Group, Generali Global Assistance, and Berkshire Hathaway Specialty Insurance - collectively accounting for approximately 45-50% of global premiums in 2024. Competition is intensifying across three dimensions: AI-driven product innovation, digital platform investment depth, and distribution partnership breadth with airlines, OTAs, and financial institutions.

|

Company Name |

Headquarters |

Market Position |

Core Strength |

|

Allianz SE |

Munich, Germany |

Market Leader |

Global scale; digital claims automation; airline co-brand partnerships |

|

AXA SA |

Paris, France |

Market Leader |

AI underwriting; embedded distribution; Asia Pacific expansion focus |

|

Zurich Insurance Group |

Zurich, Switzerland |

Strong Challenger |

Corporate travel; SME expertise; ESG-linked product innovation |

|

Generali Global Assistance |

Trieste, Italy |

Strong Challenger |

Assistance services integration; MedEvac specialization; European depth |

|

Berkshire Hathaway Specialty |

Omaha, USA |

Specialty Leader |

High-net-worth travelers; specialty risk; capacity provision |

|

American Express |

New York, USA |

Niche Premium |

Cardholder bundling; premium concierge travel; loyalty integration |

|

Tata AIG General Insurance |

Mumbai, India |

Regional Leader |

Digital-first India distribution; competitive pricing; APAC focus |

|

Seven Corners Inc. |

Carmel, USA |

Niche Specialist |

International student, missionary, and expatriate segment expertise |

Key Company Profiles

Allianz SE

Allianz is the world's largest travel insurer by premium volume, operating across 70+ countries. The Allianz Partners division serves tens of millions of travelers annually and generates several billion dollars in revenue from travel-related insurance and assistance services.

- Product Portfolio: Single-trip, multi-trip, long-stay, and business travel policies; medical evacuation; cancel-for-any-reason variants.

- Recent Developments: Launched AI-based instant claims settlement platform in 2024; expanded embedded insurance partnership with Lufthansa Group and multiple European OTAs.

- Strategic Focus: Digital platform investment, airline co-brand partnerships, and sustainable travel insurance product development for ESG-aligned consumers.

AXA SA

AXA, through its AXA Partners division, offers travel insurance solutions across multiple global markets, leveraging its broad international footprint. The company has been a frontrunner in AI-driven underwriting and claims automation globally.

- Product Portfolio: Comprehensive travel, medical-only, business travel, adventure sports, and student insurance across retail and B2B channels in key global markets.

- Recent Developments: Launched parametric flight delay product in Europe in 2023; partnered with Booking.com for embedded travel insurance distribution in Asia Pacific in 2024.

- Strategic Focus: Embedded distribution deepening, Asia Pacific market expansion, and AI-powered personalized pricing capability development.

Zurich Insurance Group

Zurich's travel insurance operations focus on corporate travel, SME segments, and high-net-worth individual travelers. The company reported insurance revenues of approximately USD 44.8 billion in 2024.

- Product Portfolio: Corporate travel programs, business travel insurance, leisure individual and group policies, and specialized expatriate coverage products.

- Recent Developments: Introduced ESG-linked travel policies in Europe in 2024 with premium credits for sustainable travel choices; enhanced digital claims mobile app capabilities in 2023.

- Strategic Focus: Corporate segment deepening, sustainability product leadership, and digital service enhancement for business and high-net-worth traveler segments.

Generali Global Assistance

Generali is a leading European travel insurer with strong global assistance service capabilities, serving over 80 million travel insurance policyholders across 150 countries with approximately USD 1.7 billion in annual operating revenues in 2024.

- Product Portfolio: Travel medical, trip cancellation, annual multi-trip, specialty adventure, and embedded OTA insurance products across European and emerging markets.

- Recent Developments: Expanded 24/7 AI-assisted travel assistance helpline in 2024; launched cyber travel protection add-on product for corporate and premium leisure travelers globally.

- Strategic Focus: Assistance service integration, digital-first product delivery, and MedEvac specialization for high-risk destination travelers.

Market Concentration Analysis

The global travel insurance market exhibits moderate concentration at the top end, with the leading five players holding approximately 45-50% of global premiums in 2024. The remaining share is distributed among hundreds of regional specialists, niche InsurTech firms, and white-label underwriters serving OTA and airline distribution partners across global markets.

Concentration is notably higher in the direct-to-consumer segment, where brand recognition and digital platform investment create significant competitive moats. In the embedded B2B2C channel, concentration is lower as smaller specialist insurers competitively underwrite white-label products distributed through high-volume OTA and airline platforms, leveraging niche pricing advantages.

Consolidation activity has accelerated since 2021, driven by InsurTech acquisitions and digital capability build-outs. The market is expected to see 8-12 significant M&A transactions annually through 2034, primarily targeting InsurTech platforms with AI underwriting capabilities, parametric product expertise, and established digital distribution partnerships in high-growth emerging markets.

Investment & Growth Opportunities

Fastest Growing Segments

Annual multi-trip insurance (CAGR ~13.2%), parametric and on-demand products (CAGR ~18.5%), and senior traveler-specific policies represent the three highest-growth investment vectors in the global travel insurance market through 2034. These segments collectively address a total addressable market of approximately USD 28 billion by 2034, with particularly strong upside in digital-first distribution channels.

Emerging Market Expansion

Asia Pacific and Latin America present the most compelling geographic investment opportunities. India's travel insurance market is expected to grow at approximately 15.2% CAGR through 2034, representing an incremental USD 6+ billion opportunity. Entry via mobile-first digital platforms, OTA partnerships, and co-branded airline products is the preferred scaling strategy in high-growth emerging markets.

Venture Investment Trends

Venture capital investment in InsurTech platforms with travel insurance applications reached approximately USD 2.4 billion globally in 2023. Key investment themes include parametric product platforms, AI claims automation, super-app insurance integration, and senior traveler digital-native products targeting Asia Pacific and Latin America markets.

- Key growth bets: parametric product technology, AI personalization engines, and embedded OTA distribution platforms targeting Asia Pacific expansion.

- ESG-aligned investors are increasingly targeting sustainability-linked travel insurance products and low-carbon travel protection innovations.

- Institutional PE interest in multi-market travel InsurTech roll-ups is elevated, particularly targeting South and Southeast Asia and the GCC region.

Future Market Outlook (2026-2034)

The global travel insurance market is poised for sustained, broad-based growth through 2034, anchored by digital transformation, product innovation, and geographic expansion into high-growth emerging markets. From a base of USD 22.1 Billion in 2025, the market is forecast to reach USD 56.5 Billion by 2034, representing absolute incremental value addition of USD 34.4 Billion over the forecast decade at a CAGR of 10.40%.

Technological disruptions - including AI-powered dynamic pricing, real-time parametric claim triggers, mobile-first embedded distribution, and blockchain-based cross-border claims processing - are expected to materially reshape operational economics across the value chain. Insurers achieving 20-30% cost efficiency improvements through automation will gain decisive competitive advantage by 2028-2030 in key growth markets.

The next decade will witness a fundamental shift in consumer expectations. Personalization, instant service delivery, and sustainability will transition from niche differentiators to baseline requirements. Brands that embed these values into core product strategy will capture disproportionate market share among millennial and Gen-Z travelers, expected to represent 35%+ of global travel insurance spend by 2034.

Research Methodology

Primary Research

Primary research for this report included structured interviews conducted with over 150 industry participants in 2024-2025, comprising travel insurance executives, underwriting managers, digital distribution specialists, and end consumers across Europe, Asia Pacific, and North America. Key opinion leaders and senior industry professionals provided qualitative market intelligence.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, trade publications including Insurance Journal and Business Insurance, industry databases, UNWTO international tourism data, and publicly available financial disclosures. Over 200 secondary sources were reviewed, cross-validated, and synthesized for this report.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating international tourism growth indices, insurance penetration rates by region, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was conducted to address macroeconomic uncertainty through 2034.

Travel Insurance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Insurance Types Covered | Single-Trip Travel Insurance, Annual Multi-Trip Insurance, Long-Stay Travel Insurance |

| Coverages Covered | Medical Expenses, Trip Cancellation, Trip Delay, Property Damage, Others |

| Distribution Channels Covered | Insurance Intermediaries, Banks, Insurance Companies, Insurance Aggregators, Insurance Brokers, Others |

| End Users Covered | Senior Citizens, Education Travelers, Business Travelers, Family Travelers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Allianz SE, AXA SA, Zurich Insurance Group, Generali Global Assistance, Berkshire Hathaway Specialty, American Express, Tata AIG General Insurance, Seven Corners Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the travel insurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global travel insurance market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the travel insurance industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Travel Insurance Market Report

The global travel insurance market size reached USD 22.1 Billion in 2025 and is projected to reach USD 56.5 Billion by 2034, growing at a CAGR of 10.40% during the forecast period from 2025 to 2034.

The market is expected to grow at a CAGR of 10.40% during the forecast period, reflecting strong demand across both leisure and corporate travel segments and accelerating digital distribution growth globally.

Europe is the dominant region, accounting for 36.0% of global travel insurance revenues in 2025, driven by Schengen visa requirements, a mature insurance culture, and high international travel frequency among European residents.

Asia Pacific is the fastest-growing region, led by expanding middle-class outbound travel from China and India, rapid digital insurance adoption, and improving distribution infrastructure across Southeast Asian markets.

Key drivers include rising international tourism volumes, increasing risk awareness post-COVID-19, digital distribution growth through embedded OTA insurance, expanding customized policy offerings, and favorable demographics among frequent traveler segments.

Single-trip travel insurance is the largest segment with a 69.2% market share (2025), driven by its cost-efficiency, flexibility, and suitability for the large majority of one-off leisure and family international travelers globally.

Medical expenses coverage leads with a 41.0% share (2025), reflecting high traveler concern over overseas healthcare costs. U.S. emergency medical treatment for foreign visitors can exceed USD 30,000 per incident, making it the primary purchase motivator.

Leading companies include Allianz SE, AXA SA, Zurich Insurance Group, Generali Global Assistance, Berkshire Hathaway Specialty Insurance, American Express, Tata AIG General Insurance, and Seven Corners Inc.

Key trends include digitalization and embedded insurance, AI-driven underwriting and claims automation, parametric and on-demand insurance products, senior traveler segment growth, and sustainability-linked insurance product development.

High-growth opportunities exist in parametric product platforms, AI underwriting technology, Asia Pacific digital distribution, senior traveler-specific products, and embedded OTA insurance partnerships - collectively representing over USD 20 billion in addressable market opportunity by 2034.

Key challenges include commodity and claims cost inflation, regulatory fragmentation across jurisdictions, cybersecurity and data privacy risks, and climate change-driven increases in catastrophe-related trip cancellation claims exposure.

Technology is reshaping the market through AI-powered underwriting, automated digital claims platforms, parametric trigger-based products, and mobile super-app distribution - enabling faster service delivery, lower acquisition costs, and improved policyholder retention across all markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)