Tuberculosis Diagnostics Market Size, Share, Trends and Forecast by Disease Stage, Test Type, End-User, and Region, 2026-2034

Tuberculosis Diagnostics Market Size and Share:

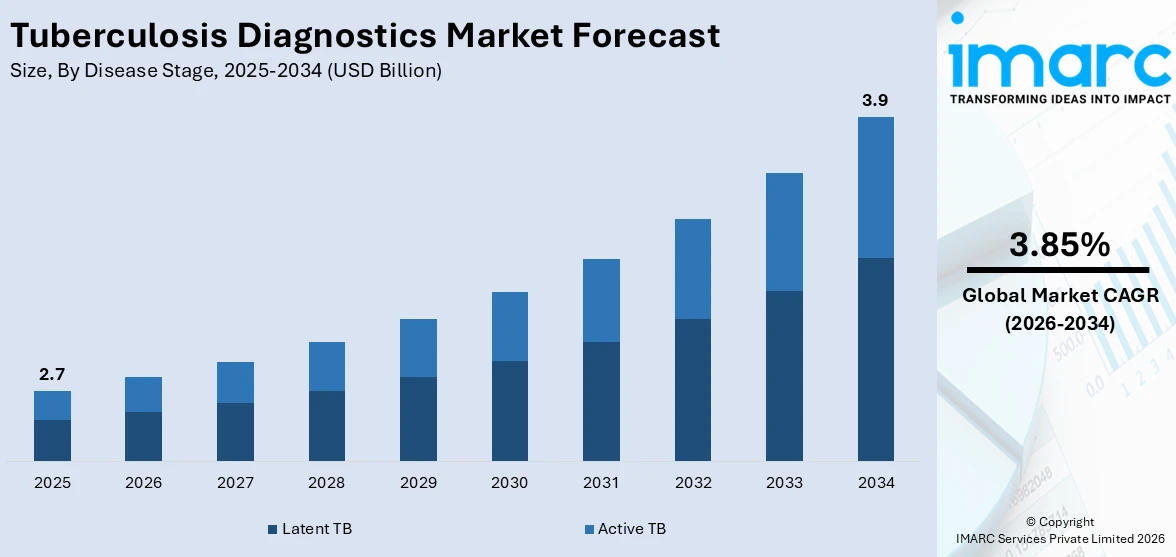

The global tuberculosis diagnostics market size was valued at USD 2.7 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 3.9 Billion by 2034, exhibiting a CAGR of 3.85% during 2026-2034. North America dominated the market, holding a significant market share of over 35.7% in 2025. Advanced healthcare, strong government support, high awareness, and technological innovation are some of the drivers contributing to the tuberculosis diagnostics market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 2.7 Billion |

|

Market Forecast in 2034

|

USD 3.9 Billion |

| Market Growth Rate 2026-2034 | 3.85% |

The market is primarily driven by the increasing global prevalence of TB, especially in developing regions. Advances in diagnostic technologies, such as molecular and nucleic acid amplification tests, have improved accuracy, speed, and sensitivity in detecting TB, which has boosted demand for innovative diagnostic solutions. Additionally, the rising emphasis on early and rapid diagnosis to control the spread of TB has led to the adoption of automated systems and digital platforms for faster results. Government initiatives, along with support from NGOs and global health organizations like the WHO, are increasing funding for TB control programs, further driving tuberculosis diagnostics market growth. Growing awareness about TB, the need for more efficient diagnostic tools, and the push for integrated healthcare solutions have all contributed to the expansion of the TB diagnostics market.

To get more information on this market Request Sample

In the United States, recent advancements in tuberculosis diagnostics focus on automating testing processes to increase efficiency. New FDA-approved platforms are improving lab throughput, delivering faster and more accurate results, and supporting global efforts to control latent tuberculosis. These innovations are streamlining workflows while ensuring precision in diagnostic procedures. For instance, in April 2025, Revvity secured FDA approval for its Auto-Pure 2400 platform integrated with the T-SPOT.TB test to automate and enhance latent tuberculosis diagnostics. The approved solution enables higher lab throughput with accurate results, aiding global tuberculosis control efforts.

Tuberculosis Diagnostics Market Trends:

Advancements in TB Genome Sequencing for Enhanced Diagnostics

Recent advancements in genome sequencing of Mycobacterium tuberculosis isolates are significantly enhancing the tuberculosis diagnostics market. This initiative aims to accelerate resistance profiling, enabling faster and more accurate diagnostic methods. By identifying genetic markers, the sequencing efforts improve clinical decision-making and allow for more personalized treatment strategies. The expanded use of genome sequencing in TB surveillance will provide a deeper understanding of regional TB variations and drug resistance patterns. These molecular insights are expected to refine diagnostic tools, enabling quicker detection and more effective management of TB. The ongoing developments in genome sequencing are set to revolutionize TB diagnostics, supporting efforts to improve treatment outcomes and meet global TB elimination targets. For example, as of March 2025, India has completed genome sequencing of 10,000 Mycobacterium tuberculosis isolates as part of the Dare2eraD TB program, aiming to eliminate tuberculosis ahead of the WHO’s 2030 targets. This breakthrough will enhance TB diagnostics, speed up resistance profiling, and improve treatment outcomes. The initiative, led by DBT, CSIR, and ICMR, is set to sequence over 32,000 isolates, revolutionizing TB surveillance and clinical decision-making.

Rising Concern of Multidrug-Resistant TB Driving Diagnostic Innovation

The increasing prevalence of multidrug-resistant tuberculosis (MDR-TB) and rifampicin-resistant tuberculosis (RR-TB) is significantly impacting the tuberculosis diagnostics market outlook. As these drug-resistant strains continue to cause a high number of global deaths, there is an urgent need for advanced diagnostic solutions to identify these infections quickly and accurately. The challenge posed by MDR-TB, which resists treatment with key antimicrobial drugs like isoniazid and rifampicin, highlights the importance of rapid resistance detection and profiling. This need for early and precise identification of resistant strains is driving demand for more sophisticated diagnostic tools, such as molecular and genomic testing, that can detect resistance patterns and guide treatment strategies. The rise of resistant TB strains is pushing the development of better, faster diagnostic methods to improve treatment outcomes and reduce mortality rates. According to WHO, multidrug-resistant tuberculosis (MDR-TB) and rifampicin-resistant tuberculosis (RR-TB) caused an estimated 150,000 deaths globally in 2023. MDR tuberculosis is caused by bacteria that are resistant to isoniazid and rifampicin, which are considered to be among the most potent antimicrobial drugs for TB.

National TB Elimination Campaign Boosting Diagnostic Demand

The launch of a nationwide TB elimination campaign under India’s National TB Elimination Programme (NTEP) is significantly impacting the tuberculosis diagnostics industry. The initiative, covering numerous districts across the country, aims to enhance TB detection and treatment through widespread screening efforts. This large-scale campaign increases the demand for rapid and accurate diagnostic tools that can identify both latent and active TB cases efficiently. As the program focuses on early diagnosis and reducing TB transmission, the need for advanced diagnostic solutions, such as molecular and rapid testing methods, has risen. Tuberculosis diagnostics market forecast suggests that the expansion of testing infrastructure and focus on timely intervention will further drive the adoption of innovative TB diagnostics technologies, ultimately contributing to improved TB control and faster treatment response. For instance, in December 2024, a 100-Day TB Elimination Campaign was launched under the National TB Elimination Programme (NTEP) in India, spanning across spanning 347 districts across 33 states and union territories.

Tuberculosis Diagnostics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global tuberculosis diagnostics market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on disease stage, test type, and end-user.

Analysis by Disease Stage:

- Latent TB

- Active TB

Latent TB refers to individuals who have the bacteria in their body but are not showing symptoms, and while they are not contagious, they have a higher risk of developing active TB later. As awareness about the potential progression from latent to active TB increases, there is a growing demand for diagnostic tools that can detect latent infections early. This push for early detection through screening programs, especially in high-risk populations, is fueling the market's growth. Active TB, characterized by symptoms and infectiousness, requires immediate detection and treatment to curb its spread. With the global rise in TB cases, there is a significant demand for rapid diagnostic solutions, such as molecular tests, PCR-based diagnostics, and culture methods, that can quickly and accurately identify active infections. These advancements in TB diagnostics are supporting the market’s expansion.

Analysis by Test Type:

Access the comprehensive market breakdown Request Sample

- Radiographic Test

- Laboratory Test

- Smear Microscopy

- Culture-based Test

- Nucleic Acid Testing

- Cytokine Detection Test

- Drug Resistance Test

- Others

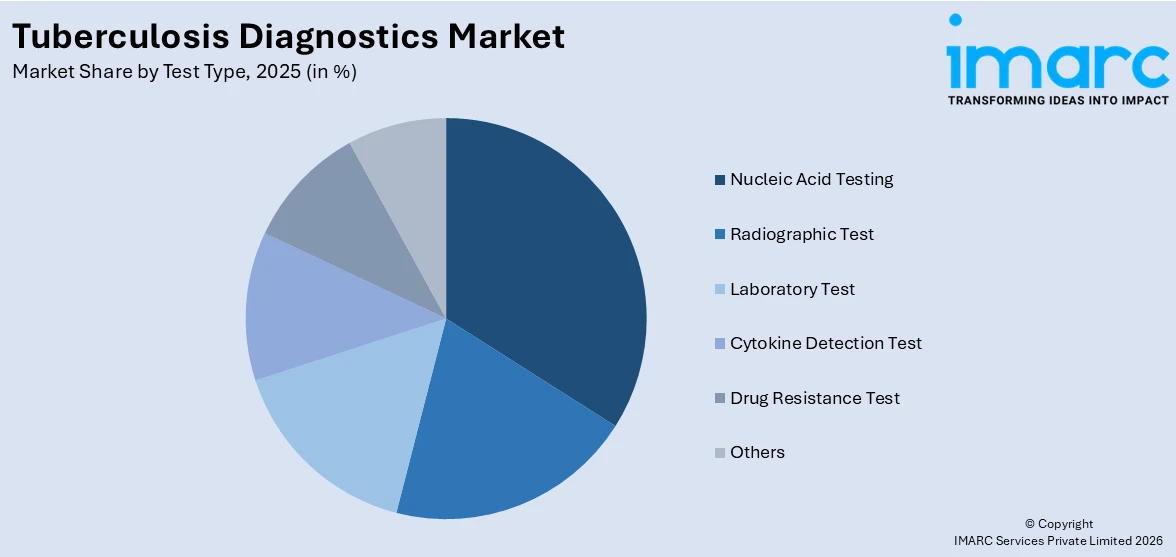

Nucleic acid testing led the market in 2025 due to its ability to provide rapid, accurate, and highly sensitive results. NAT, including polymerase chain reaction (PCR) and other molecular tests, allows for the detection of Mycobacterium tuberculosis DNA in patient samples, making it particularly effective for diagnosing both latent and active TB infections. The speed and precision of NAT reduce diagnostic delays, improving treatment outcomes and limiting the spread of TB. As the demand for quicker, more reliable diagnostic solutions grows, particularly in high-burden regions, NAT continues to gain traction. Furthermore, the ability to detect drug-resistant TB strains through NAT is increasingly crucial, driving further adoption and market growth in efforts to control TB more effectively.

Analysis by End-User:

- Hospitals and Clinics

- Diagnostics and Research Laboratories

- Others

Diagnostics and research laboratories led the market in 2025, holding around 53.2% of the market. These laboratories are central to the development and implementation of advanced diagnostic technologies, such as molecular tests, PCR, and culture-based methods. They provide critical infrastructure for accurate TB detection, offering a variety of testing services for both latent and active TB. With increasing research efforts to develop more efficient, faster, and cost-effective diagnostic tools, these laboratories are at the forefront of innovation in the TB diagnostics market. Additionally, as the demand for accurate and timely diagnosis grows, particularly in TB-endemic regions, the expansion of diagnostics and research laboratories to meet these needs is driving market growth. The continuous advancements and high demand for testing solutions in these settings support the overall market expansion.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 35.7%, owing to its advanced healthcare infrastructure, which ensures widespread access to high-quality diagnostic tools and services. The region benefits from strong government support, with initiatives like the Centers for Disease Control and Prevention (CDC) working toward improving TB detection, treatment, and prevention. Increased awareness of TB and its risks among the population, coupled with substantial investment in healthcare research and development, contributes to the market's growth. Additionally, the presence of leading diagnostic companies and technological innovations, such as molecular diagnostics and automated systems, further enhances TB detection accuracy and speed. These factors combined position North America as a major player in the global TB diagnostics market.

Key Regional Takeaways:

United States Tuberculosis Diagnostics Market Analysis

In 2025, the United States accounted for 88.7% of the market share in North America. The United States is witnessing increased tuberculosis diagnostics adoption due to the rising prevalence of multi-drug resistant (MDR) tuberculosis. For instance, during 2023, at the time of initial diagnosis, 589 (8.5%) tuberculosis cases in the United States were found to have resistance to at least isoniazid, including 100 (1.4%) cases of multidrug-resistant tuberculosis (MDR TB). The growing burden of MDR strains is compelling healthcare providers to implement more robust and early-stage diagnostic solutions. Enhanced government support, coupled with an expanding network of diagnostic laboratories, is contributing to the prioritization of efficient tuberculosis detection. The focus on MDR tuberculosis is prompting strategic investments in molecular and culture-based diagnostics. In addition, public health campaigns are raising awareness, leading to increased screening rates across high-risk populations. Technological advancements and ongoing clinical research for rapid MDR identification further accelerate the demand for accurate tuberculosis diagnostics.

Asia Pacific Tuberculosis Diagnostics Market Analysis

Asia Pacific is experiencing growing tuberculosis diagnostics adoption driven by expanding diagnostics facilities across the region. For instance, industry experts estimate that, as of February 2025, there are around 3,00,000 labs across India, and this number is growing. With national healthcare systems scaling their capabilities, there is greater access to modern diagnostic tools, enabling early identification and management of tuberculosis cases. The proliferation of public-private partnerships is boosting diagnostic infrastructure in both urban and rural areas. Government initiatives to strengthen infectious disease detection are encouraging hospitals and clinics to adopt updated tuberculosis diagnostics. Expanding laboratory networks, integration of automated testing systems, and capacity building for healthcare professionals are key contributors to this trend. In addition, rising health awareness among populations and improved patient outreach have enhanced participation in tuberculosis screening programs. The increase in diagnostic facilities supports timely intervention and reduces transmission risks, underscoring the importance of structured healthcare delivery in tuberculosis management across Asia Pacific.

Europe Tuberculosis Diagnostics Market Analysis

Europe is seeing heightened tuberculosis diagnostics adoption influenced by the rising geriatric population. In the WHO European Region, in 2023, more than 172,000 individuals with new and relapsed tuberculosis were reported, reflecting numbers similar to those seen in 2022. As older adults are more susceptible to infectious diseases due to weakened immunity, tuberculosis screening and diagnostic measures are becoming essential in elderly care. Healthcare systems are incorporating tuberculosis testing into routine evaluations for seniors, particularly in long-term care settings. With aging populations concentrated in urban centers, diagnostic services are being tailored to accommodate this demographic. Innovations in non-invasive testing and mobile diagnostic units are facilitating access for older patients. The growing burden of age-related comorbidities increases the demand for precise and early detection tools. Policymakers are integrating tuberculosis diagnostics into geriatric health strategies, emphasizing preventative care.

Latin America Tuberculosis Diagnostics Market Analysis

Latin America is witnessing increased tuberculosis diagnostics adoption due to the expansion of healthcare facilities and privatization. The Brazilian Federation of Hospitals (FBH) and the National Confederation of Health (CNSaúde) report that 62% of Brazil's 7,191 hospitals are privately owned. The region is investing in modern medical infrastructure, resulting in enhanced diagnostic capabilities. Privatized healthcare models are introducing competitive, patient-centric services that prioritize accurate tuberculosis detection. New diagnostic centers and private clinics are improving access and efficiency in early-stage tuberculosis testing.

Middle East and Africa Tuberculosis Diagnostics Market Analysis

The Middle East and Africa are recording growth in tuberculosis diagnostics adoption driven by increasing healthcare expenditure. For instance, in 2021, the overall prevalence of latent tuberculosis infection (LTBI) in the MENA region was determined to be 41.78%. In gender-specific subgroup analyses, the LTBI prevalence was 33.12% in males and 32.65% in females. The government and private sectors are investing heavily in healthcare infrastructure, leading to greater availability of diagnostic tools. Rising financial commitment is enabling the procurement of advanced equipment and training of professionals in tuberculosis testing.

Competitive Landscape:

The tuberculosis diagnostics market is witnessing significant advancements through various avenues, including product launches, partnerships, funding, government initiatives, and research and development. Companies are focusing on introducing innovative diagnostic tools, while collaborations between organizations aim to enhance treatment and diagnostic capabilities. Increased funding is being directed toward the development of advanced diagnostics, particularly for drug-resistant strains. Government initiatives, such as national programs and free diagnostics, are crucial for broadening access to care. Research efforts are geared toward improving and standardizing diagnostic technologies. Currently, government initiatives and partnerships are the most common practices, reflecting a collaborative approach to tackling tuberculosis through better diagnostic solutions.

The report provides a comprehensive analysis of the competitive landscape in the tuberculosis diagnostics market with detailed profiles of all major companies, including:

- Abbott Laboratories

- Alere Inc.

- Becton Dickinson and Company

- BioMérieux

- Cepheid Inc.

- Epistem Ltd.

- Roche Holding AG

- Hain Lifescience GmbH

- Hologic Inc.

- QIAGEN GmbH

- Siemens

- Thermo Fisher Scientific Inc.

Latest News and Developments:

- May 2025: Thakurganj TB Joint Hospital in Lucknow, India, launched 24-hour laboratory services to ease access to essential diagnostics, including for tuberculosis. Patients earlier faced delays as samples had to be sent to other hospitals due to a lack of round-the-clock testing.

- April 2025: The Punjab government in India launched an advanced diagnostic van equipped with a handheld X-ray machine and a fluorescent microscope to enhance early TB detection. This initiative, supported by Indian Oil Corporation Limited and the People-to-People Health Foundation, aims to strengthen diagnostic capabilities in Sangrur and Malerkotla districts.

- March 2025: The Kalakkode Community Health Centre (CHC) in Kerala enhanced its tuberculosis diagnostic capabilities by installing a new Truenat machine. This advanced molecular diagnostic tool enables rapid and accurate detection of TB and rifampicin resistance, facilitating early intervention.

- February 2025: The Stop TB Partnership's Global Drug Facility announced a 38% price reduction for the BPaLM regimen, a six-month treatment for drug-resistant tuberculosis. Now priced at USD 364 per course, this decrease enhances affordability and access in high-burden countries. Additionally, new drug-sensitivity tests for bedaquiline were introduced to help prevent resistance and ensure effective treatment.

Tuberculosis Diagnostics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Disease Stages Covered | Latent TB, Active TB |

| Test Types Covered | Radiographic Test, Laboratory Test, Nucleic Acid Testing, Cytokine Detection Test, Drug Resistance Test, Others |

| End-Users Covered | Hospitals and Clinics, Diagnostics and Research Laboratories, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, Alere Inc., Becton Dickinson and Company, BioMérieux, Cepheid Inc., Epistem Ltd., Roche Holding AG, Hain Lifescience GmbH, Hologic Inc., QIAGEN GmbH, Siemens, Thermo Fisher Scientific Inc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the tuberculosis diagnostics market from 2020-2034.

- The tuberculosis diagnostics market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the tuberculosis diagnostics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Tuberculosis Diagnostics Market Report

The tuberculosis diagnostics market was valued at USD 2.7 Billion in 2025.

The tuberculosis diagnostics market is projected to exhibit a CAGR of 3.85% during 2026-2034, reaching a value of USD 3.9 Billion by 2034.

The tuberculosis diagnostics market is driven by factors such as rising global TB prevalence, advancements in diagnostic technologies (like molecular tests and digital platforms), increased government and NGO funding, growing awareness, and the need for rapid, accurate TB detection to support treatment and control efforts worldwide.

North America dominated the tuberculosis diagnostics market in 2025, holding around 35.7% due to advanced healthcare infrastructure, high disease awareness, strong research and development capabilities, and government initiatives promoting early detection and effective treatment solutions.

Some of the major players in the tuberculosis diagnostics market include Abbott Laboratories, Alere Inc., Becton Dickinson and Company, BioMérieux, Cepheid Inc., Epistem Ltd., Roche Holding AG, Hain Lifescience GmbH, Hologic Inc., QIAGEN GmbH, Siemens, and Thermo Fisher Scientific Inc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)