Turkey Biosimilar Market Size, Share, Trends and Forecast by Molecule, Indication, Manufacturing Type, and Region, 2026-2034

Turkey Biosimilar Market Overview:

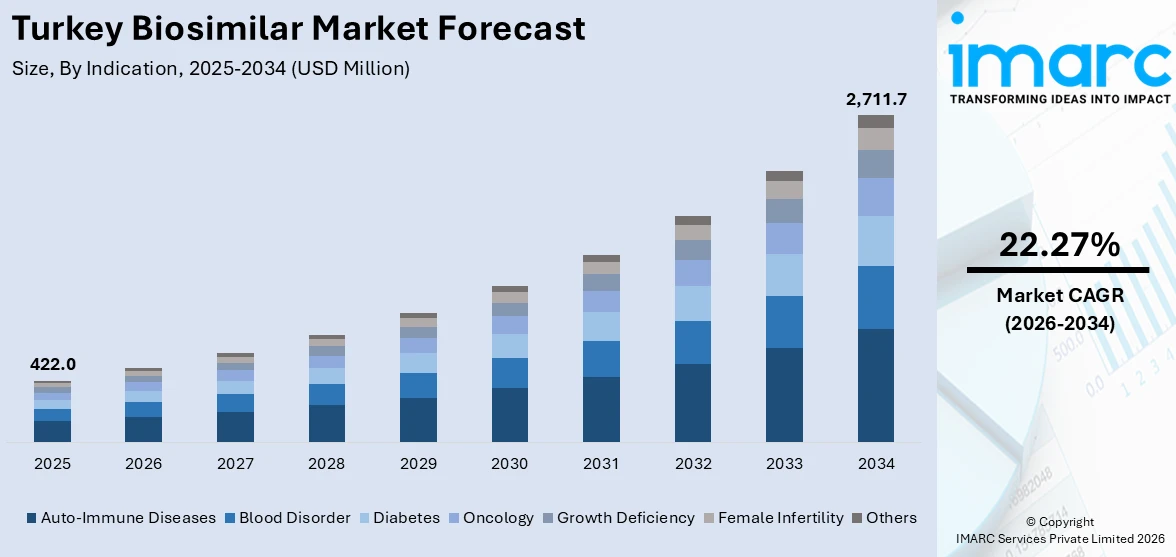

The Turkey biosimilar market size reached USD 422.0 Million in 2025. The market is projected to reach USD 2,711.7 Million by 2034, exhibiting a growth rate (CAGR) of 22.27% during 2026-2034. The market is expanding as demand grows for affordable treatments in therapeutic areas such as oncology and autoimmune diseases. Regional pharmaceuticals are shifting their focus to research, development, and sophisticated manufacturing to address increasing healthcare needs. Greater activity in clinical trials and collaborations is providing better product availability and quality. As businesses build up their strengths and diversify their portfolios, they are also targeting regional and international presence, which is further fueling the growth of the Turkey biosimilar market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 422.0 Million |

| Market Forecast in 2034 | USD 2,711.7 Million |

| Market Growth Rate 2026-2034 | 22.27% |

Turkey Biosimilar Market Trends:

Regulatory Clarity Enhances Market Confidence

Turkey has made significant progress in shaping a more predictable regulatory path for biosimilars. In September 2024, the Turkish Medicines and Medical Devices Authority (TİTCK) introduced updates to its Guideline on Biosimilar Pharmaceuticals, offering greater clarity on data expectations, comparability protocols, and manufacturing adjustments. This update helps create a more transparent approval environment for biosimilar developers encouraging faster market entry and improved product consistency. With clearer regulatory signals, developers can more confidently allocate resources toward local registration and production efforts. The guideline aligns with global best practices, enhancing the Turkish biosimilar space more attractive for international collaboration and local investment. This regulatory progress is not just about compliance; it’s also about strengthening the industry’s infrastructure to better serve long-term health system sustainability. As more products transition from development to approval under these enhanced rules, both access and competition are expected to increase. Overall, these refinements represent a critical step forward in reinforcing regulatory trust and accelerating Turkey biosimilar market growth.

To get more information on this market Request Sample

Government Innovation Initiatives Fuel Momentum

Turkey is actively advancing its healthcare innovation agenda, and biosimilars are increasingly integrated into this strategy. Through national funding initiatives and supportive pricing frameworks, the country is creating a more accessible environment for biosimilar development. In March 2025, public agencies reinforced their commitment by expanding eligibility for state-backed R&D grants to include biosimilar projects, enabling academic and private-sector collaboration in early-stage development. This complements recent updates to pharmaceutical pricing policies, which aim to make biosimilar products more competitively positioned alongside originator biologics. Together, these measures are helping reduce barriers to entry while encouraging sustainable growth in domestic development. These changes also indicate a shift in policy focus from cost control alone to long-term capability building. By supporting biosimilar innovation both structurally and financially, Turkey is fostering an environment where market entry is more viable, and product diversity can flourish. This approach reflects a maturing ecosystem that recognizes the strategic importance of biosimilars in reducing healthcare costs and improving access. Such coordinated progress is emblematic of broader Turkey biosimilar market trends.

Strategic Expansion Through International Licensing

Turkey is strengthening its biosimilar ecosystem through strategic international licensing partnerships that support market entry and distribution. In January 2025, a licensing and commercialization agreement was signed, to introduce BAT2206, a biosimilar of ustekinumab (Stelara), into the Turkish market. Under the deal, World Medicine will manage registration, imports, and marketing in Turkey, while Bio‑Thera will handle commercial supply and manufacturing from its facilities abroad. This collaboration smartly leverages external production capacity while ensuring that biosimilar access in Turkey is both timely and efficiently managed. It also reflects how licensing agreements are becoming a key tool for introducing advanced biological treatments without waiting for local manufacturing to catch up. As Turkey’s healthcare sector continues to evolve, such collaborations help diversify the biosimilar pipeline and bring treatments to patients faster. The model supports access without compromising on quality or regulatory alignment, delivering both flexibility and scale. This approach underscores the growing sophistication of the country's biosimilar strategy and reinforces its position in the regional healthcare landscape.

Turkey Biosimilar Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on molecule, indication, and manufacturing type.

Molecule Insights:

- Infliximab

- Insulin Glargine

- Epoetin Alfa

- Etanercept

- Filgrastim

- Somatropin

- Rituximab

- Follitropin Alfa

- Adalimumab

- Pegfilgrastim

- Trastuzumab

- Bevacizumab

- Others

The report has provided a detailed breakup and analysis of the market based on the molecule. This includes infliximab, insulin glargine, epoetin alfa, etanercept, filgrastim, somatropin, rituximab, follitropin alfa, adalimumab, pegfilgrastim, trastuzumab, bevacizumab, and others.

Indication Insights:

- Auto-Immune Diseases

- Blood Disorder

- Diabetes

- Oncology

- Growth Deficiency

- Female Infertility

- Others

A detailed breakup and analysis of the market based on the indication have also been provided in the report. This includes auto-immune diseases, blood disorders, diabetes, oncology, growth deficiency, female infertility, and others.

Manufacturing Type Insights:

Access the comprehensive market breakdown Request Sample

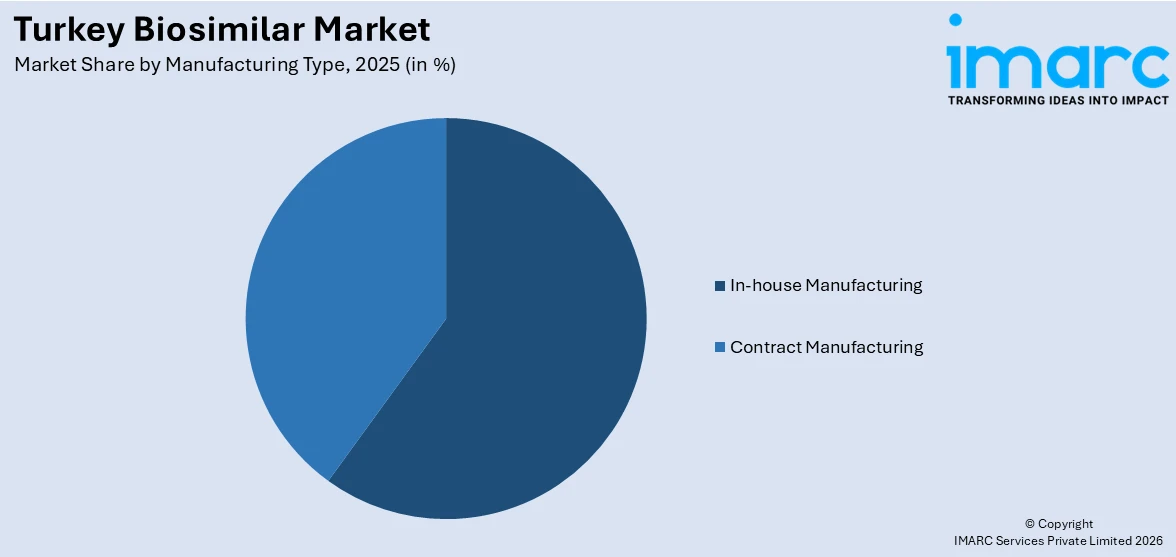

- In-house Manufacturing

- Contract Manufacturing

The report has provided a detailed breakup and analysis of the market based on the manufacturing type. This includes in-house manufacturing and contract manufacturing.

Regional Insights:

- Marmara

- Central Anatolia

- Mediterranean

- Aegean

- Southeastern Anatolia

- Black Sea

- Eastern Anatolia

The report has also provided a comprehensive analysis of all the major regional markets, which include Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, and Eastern Anatolia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Turkey Biosimilar Market News:

- January 2025: World Medicine, a leading Turkish pharmaceutical firm, has entered an exclusive license and commercialization agreement with China’s Bio‑Thera Solutions for BAT2206, a biosimilar version of Ustekinumab. Under the agreement, Bio‑Thera will manage manufacturing in its Guangzhou facility, while World Medicine handles regulatory approval, importation, and local marketing in Turkey. This strategic partnership positions the companies to deliver advanced treatment options for autoimmune conditions to patients in Turkey, reflecting World Medicine’s commitment to expanding its therapeutic portfolio and regional presence.

- March 2025: Yerlika Biopharma, a pioneering Turkish biotechnology firm, is advancing domestic biopharmaceutical manufacturing with its cutting-edge facility in Çerkezköy. By offering specialized CMO/CDMO capabilities, the company designs and manufactures a wide variety of biological products such as biosimilars, monoclonal antibodies, gene therapies, and vaccines under strict GMP conditions. By bringing production closer to home and providing end-to-end development and commercialization support, Yerlika fortifies Turkey's biopharm capabilities and solidifies its position as a globally competitive biotech partner.

Turkey Biosimilar Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Molecules Covered | Infliximab, Insulin Glargine, Epoetin Alfa, Etanercept, Filgrastim, Somatropin, Rituximab, Follitropin Alfa, Adalimumab, Pegfilgrastim, Trastuzumab, Bevacizumab, Others |

| Indications Covered | Auto-Immune Diseases, Blood Disorder, Diabetes, Oncology, Growth Deficiency, Female Infertility, Others |

| Manufacturing Types Covered | In-house Manufacturing, Contract Manufacturing |

| Regions Covered | Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, Eastern Anatolia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Turkey biosimilar market performed so far and how will it perform in the coming years?

- What is the breakup of the Turkey biosimilar market on the basis of molecule?

- What is the breakup of the Turkey biosimilar market on the basis of indication?

- What is the breakup of the Turkey biosimilar market on the basis of manufacturing type?

- What is the breakup of the Turkey biosimilar market on the basis of region?

- What are the various stages in the value chain of the Turkey biosimilar market?

- What are the key driving factors and challenges in the Turkey biosimilar market?

- What is the structure of the Turkey biosimilar market and who are the key players?

- What is the degree of competition in the Turkey biosimilar market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Turkey biosimilar market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Turkey biosimilar market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Turkey biosimilar industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)