Turkey Education Apps Market Size, Share, Trends and Forecast by Product Type, Operating System, End User, and Region, 2026-2034

Turkey Education Apps Market Size, Share, Trends & Forecast (2026-2034)

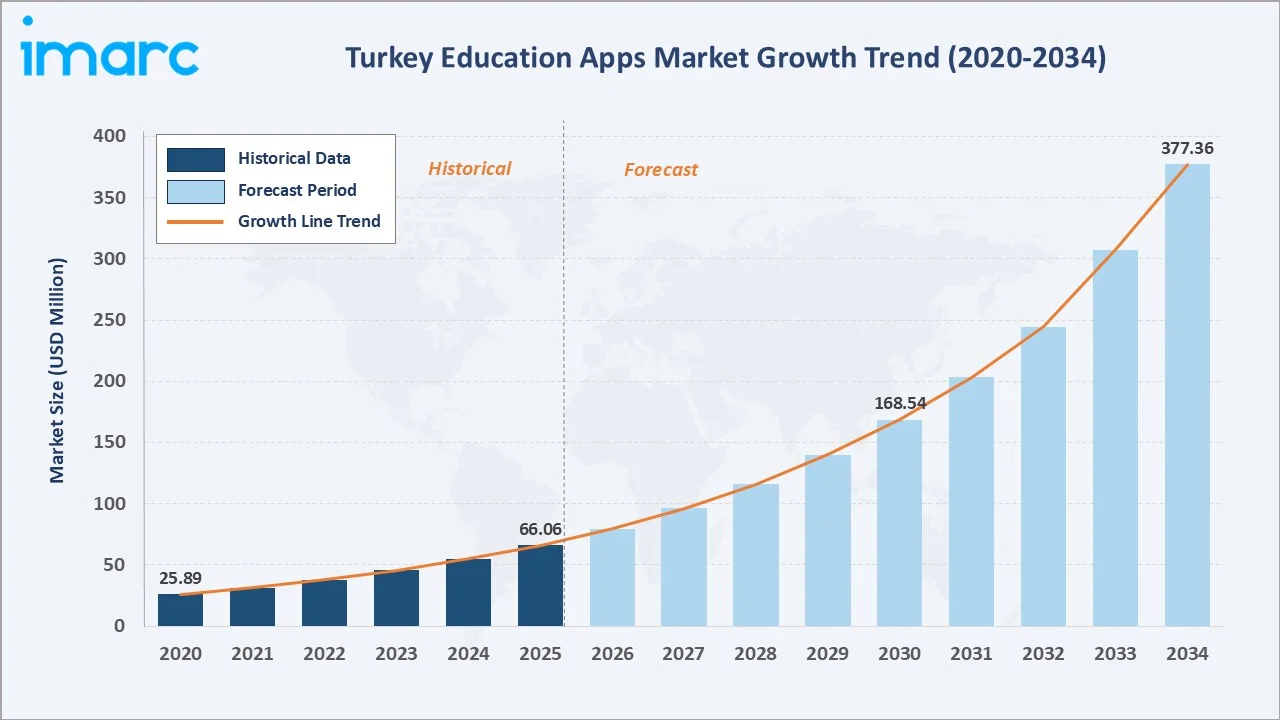

The Turkey education apps market was valued at USD 66.06 Million in 2025 and is projected to reach USD 377.36 Million by 2034, exhibiting a CAGR of 20.60% during 2026-2034. Rising smartphone adoption, government-backed digital education initiatives, an expanding young population, and increasing integration of AI-powered adaptive learning tools are the primary drivers shaping market growth.

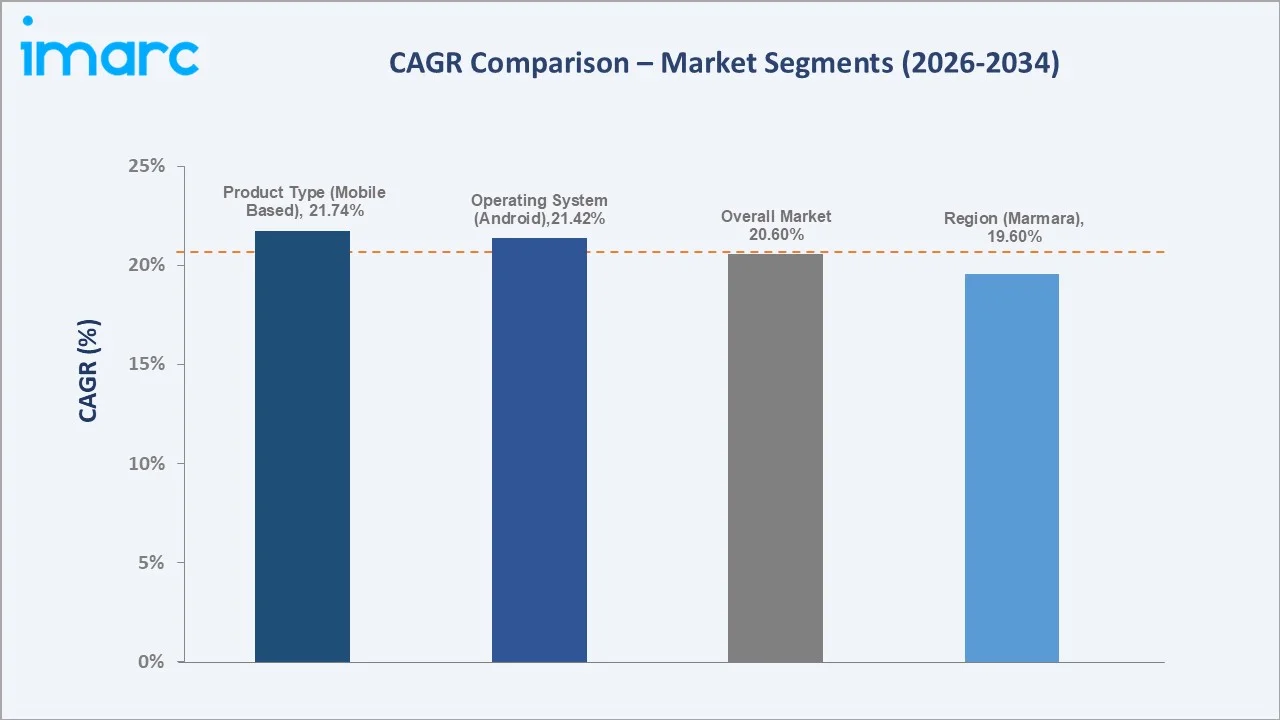

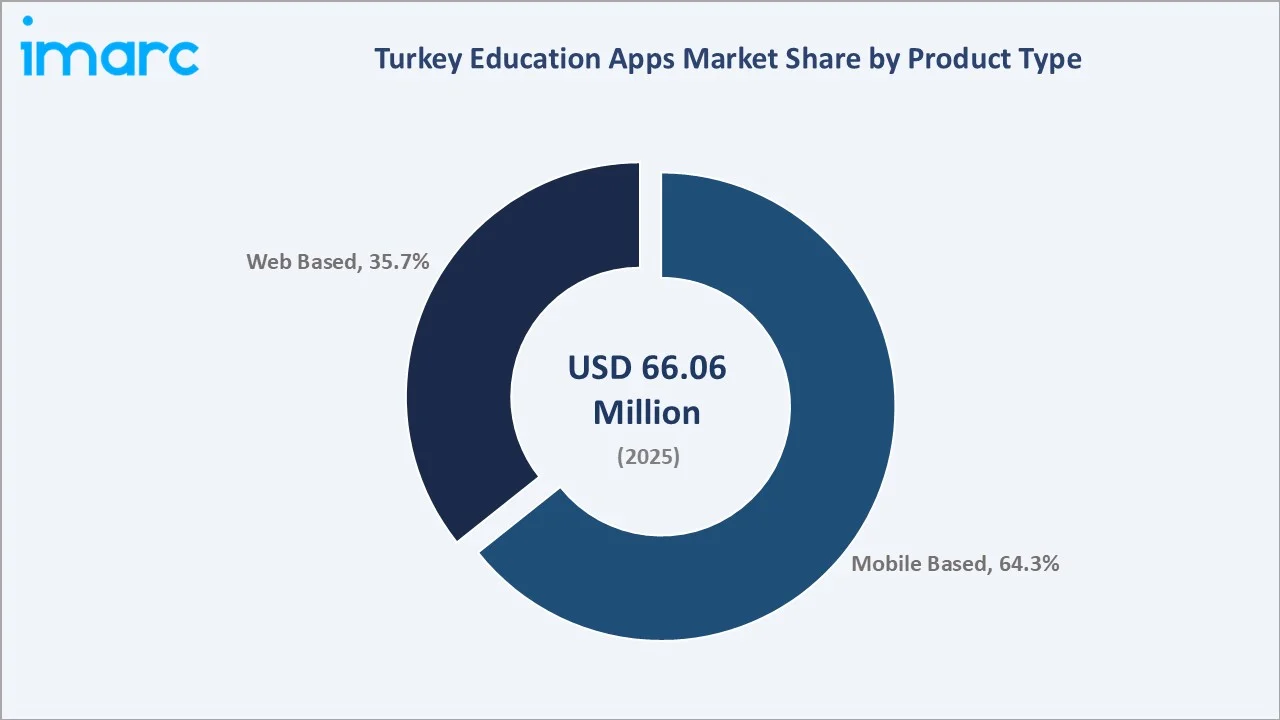

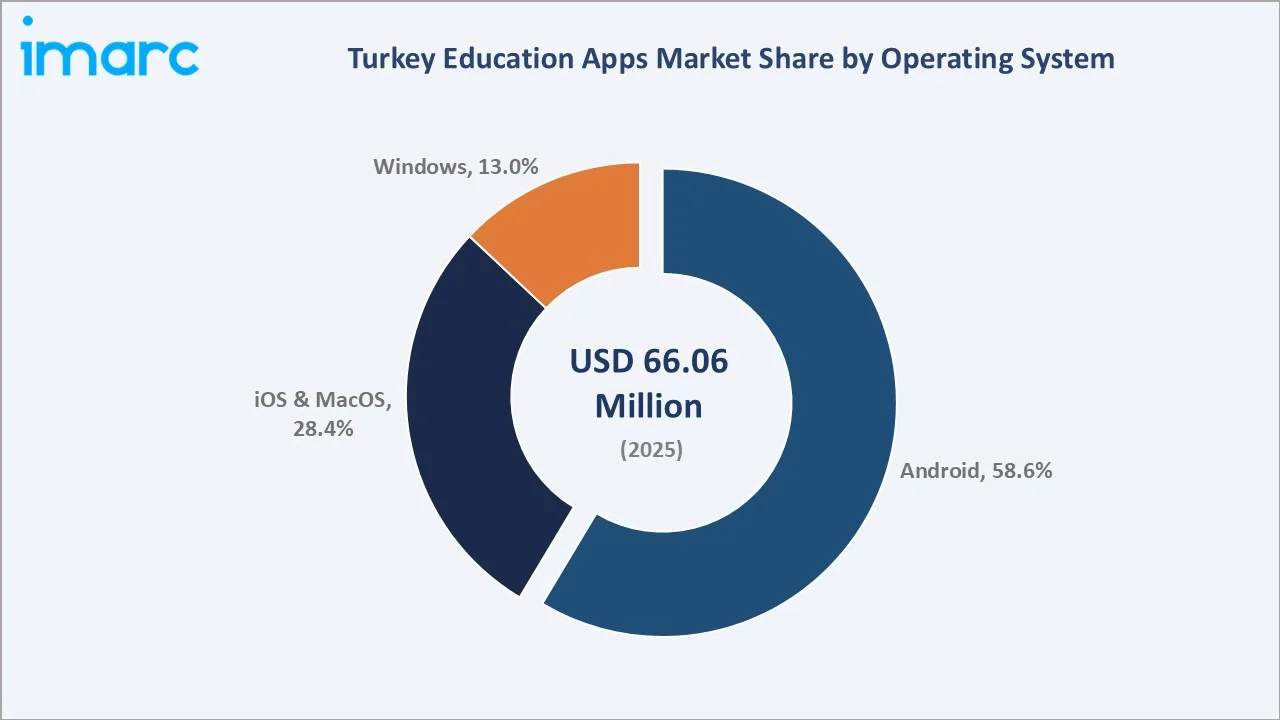

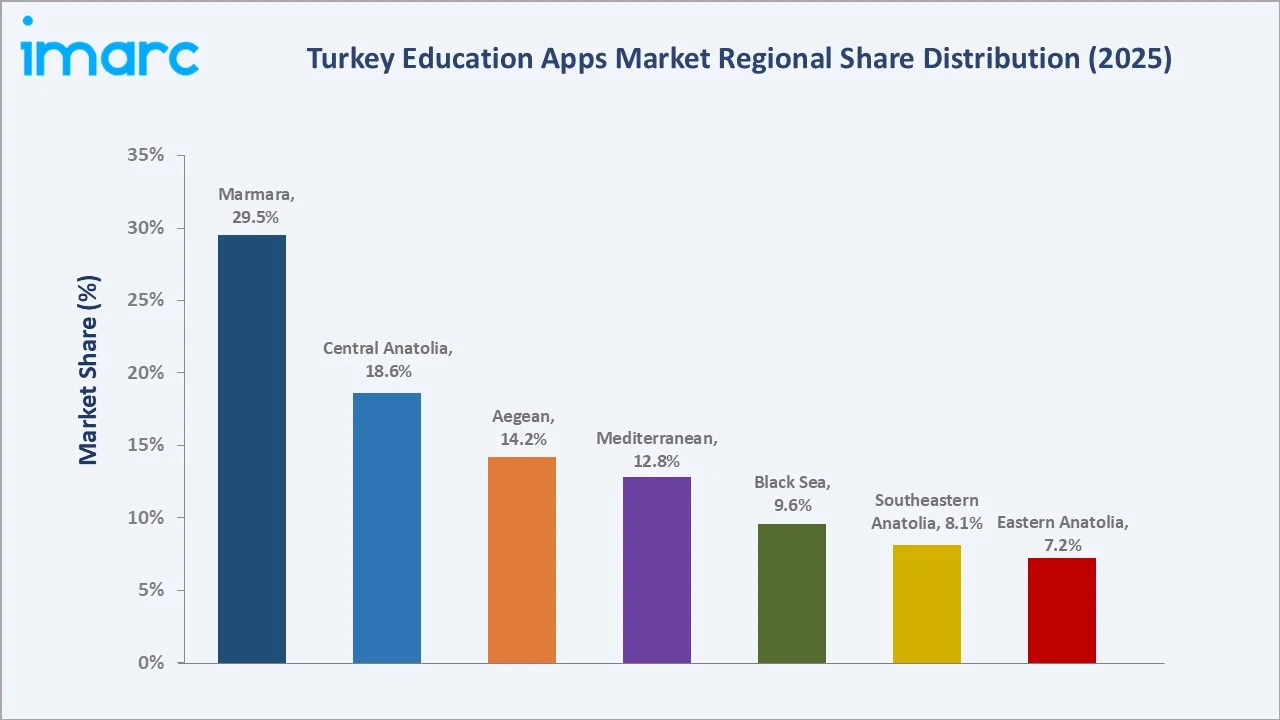

Mobile based leads the product type segment at 64.3%, Android commands 58.6% of the operating system segment, and Marmara holds 29.5% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 66.06 Million |

|

Forecast Market Size (2034) |

USD 377.36 Million |

|

CAGR (2026-2034) |

20.60% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Marmara (29.5%, 2025) |

|

Second Largest Region |

Central Anatolia (18.6%, 2025) |

|

Leading Product Type |

Mobile Based (64.3%, 2025) |

|

Leading Operating System |

Android (58.6%, 2025) |

The Turkey education apps market expanded from USD 25.89 Million in 2020 to USD 66.06 Million in 2025, driven by accelerating digital transformation in schools, the growth of mobile internet usage, and rapidly rising demand for test-prep and language learning applications across K-12, higher education, and professional segments. Anchored at USD 168.54 Million in 2030, the forecast to USD 377.36 Million by 2034 is supported by deepening AI integration, expanding corporate e-learning adoption, and continued government investment in digital education infrastructure.

To get more information on this market, Request Sample

CAGR trajectories across product type and operating system sub-segments show mobile based and Android expanding faster than the overall 20.60% market CAGR, driven by the widespread availability of affordable Android smartphones, expanding 4G and 5G connectivity, and strong consumer preference for on-demand, anytime-anywhere learning experiences.

Executive Summary

The Turkey education apps market is on a robust growth trajectory from USD 25.89 Million in 2020 to USD 377.36 Million by 2034. The segment has transitioned from basic instructional tools to comprehensive AI-powered, curriculum-aligned platforms serving K-12 students, university learners, and corporate training segments. Increasing smartphone ownership, affordable mobile data, and strong government support for digital education have laid the infrastructure for sustained market expansion.

Mobile based dominates the product type segment at 64.3% in 2025, supported by low-cost smartphone access, intuitive user interfaces, and the growing availability of offline-capable learning content. Mobile internet subscribers in Turkey reached 75.6 Million in the final quarter of 2024, creating one of the largest addressable user bases for mobile-delivered education services in the region. Android leads the operating system segment at 58.6%, fueled by the prevalence of mid-range Android devices across Turkey's broad consumer base. Marmara commands 29.5% of the regional share, led by Istanbul's large student population, concentration of private tutoring demand, and advanced digital infrastructure.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Mobile Based - 64.3% share (2025) |

|

Second Largest Product Type |

Web Based - 35.7% share (2025) |

|

Leading Operating System |

Android - 58.6% share (2025) |

|

Second Largest Operating System |

iOS & MacOS - 28.4% share (2025) |

|

Leading Region |

Marmara - 29.5% share (2025) |

|

Second Largest Region |

Central Anatolia - 18.6% share (2025) |

|

Top Companies |

Coursera Inc., Microsoft, Türk Telekom, Khan Academy |

Key Analytical Observations Expanding On The Data Above:

- Mobile based dominance at 64.3% is supported by widespread smartphone penetration, seamless app store distribution, and the flexibility of on-the-go learning experiences that align with the habits of Turkey's young, digitally active population.

- Web based at 35.7% remains relevant for desktop-centric learning environments, particularly in higher education institutions, corporate training setups, and government-administered digital education portals.

- Android leadership at 58.6% reflects the strong penetration of affordable mid-range Android smartphones across Turkish households, supported by competitive pricing from leading brands in the domestic market.

- iOS and MacOS share at 28.4% captures premium learner segments, particularly among urban university students and professionals who prefer Apple-ecosystem devices for their seamless cross-device learning experiences.

- Marmara at 29.5% dominates regional share, anchored by Istanbul's large K-12 and university student population, high concentration of private tutoring demand in the country, and strong digital adoption across both public and private schools. In 2024, the overall number of students in Istanbul's universities surpassed 1.25 Million, distributed among 57 public and private institutions.

Turkey Education Apps Market Overview

Education apps refer to mobile and web-based software applications designed to deliver academic content, skill development modules, language learning tools, test preparation resources, and corporate training programs through digital platforms. These applications serve a broad spectrum of users, including K-12 students, higher education learners, corporate employees, and self-directed adult learners, across multiple subjects and competency areas.

The Turkish ecosystem integrates content developers, technology platform providers, mobile app developers, school and university networks, government education bodies, corporate training departments, app distribution platforms, and end users. Together they enable the delivery of structured digital learning experiences aligned with national curricula and professional development needs.

Market Dynamics

To evaluate market opportunities, Request Sample

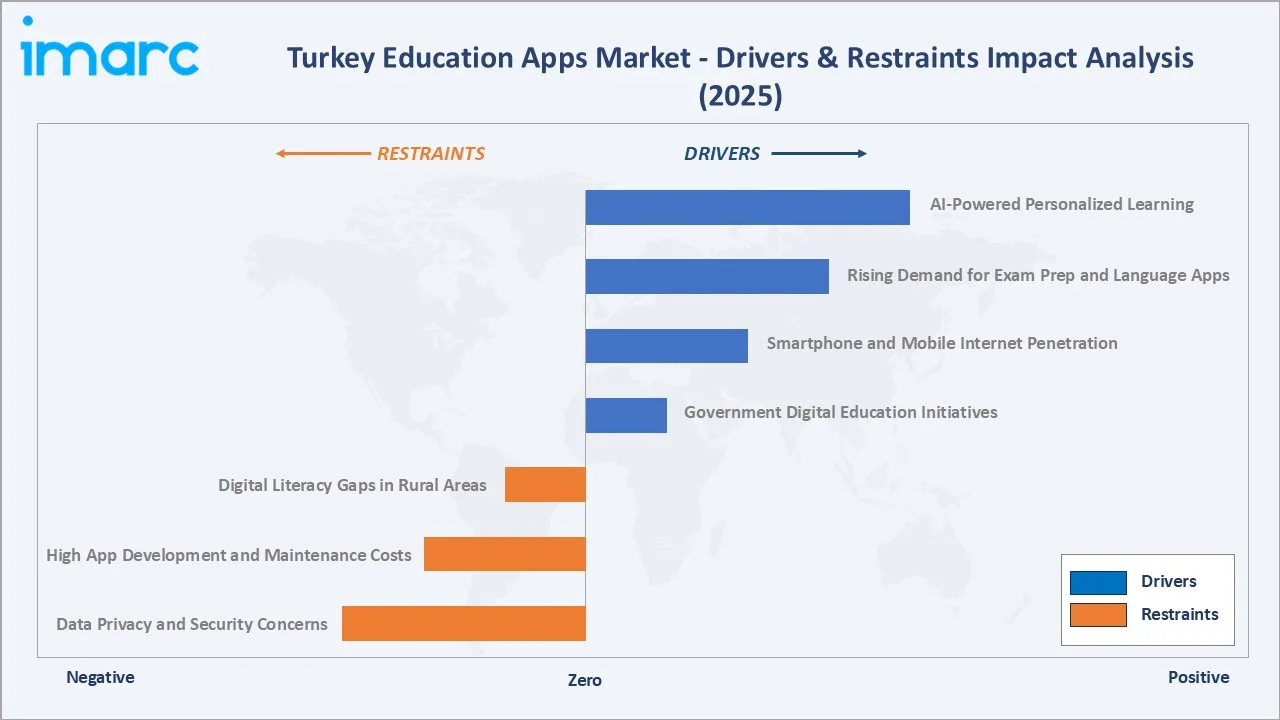

Market Drivers

- Government Digital Education Initiatives: National digital learning initiatives and online education platforms have fostered a structured digital education ecosystem by distributing learning devices to students and integrating curriculum-aligned digital content into classrooms, thereby accelerating the adoption of educational technology solutions.

- Smartphone and Mobile Internet Penetration: Rapid expansion of 4G and 5G networks and growing availability of affordable smartphones are bringing first-time digital learners from tier-2 and tier-3 cities into mobile-based education platforms. As of April 2026, Turkey boasted over 32 Million 5G-compatible devices, and approximately 21 Million subscribers started to utilize 5G services as the technology was progressively introduced in all 81 provinces.

- Rising Demand for Exam Preparation and Language Learning: High-stakes national university entrance examinations (YKS) and growing demand for English language proficiency in Turkey's competitive job market are driving consistent, year-round demand for test-prep and language learning applications among students and young professionals.

- AI-Powered Personalized Learning: Increasing integration of AI and machine learning (ML) algorithms into education platforms enables adaptive learning paths, intelligent tutoring systems, and personalized content recommendations that improve learning outcomes and user retention across apps.

Market Restraints

- Digital Literacy Gaps in Rural and Underserved Areas: Despite government investment in digital education infrastructure, significant digital literacy gaps persist in rural and low-income regions of Turkey, limiting the effective adoption of education apps among students and teachers in these areas.

- High App Development and Maintenance Costs: The cost of developing, updating, and maintaining high-quality, curriculum-aligned education apps with interactive features, AI capabilities, and multi-platform compatibility represents a significant financial barrier, particularly for smaller domestic EdTech startups in the market.

- Data Privacy and Security Concerns: Growing awareness of data protection issues and Turkey's Personal Data Protection Law (KVKK) compliance requirements create operational complexity for education app providers, particularly those collecting sensitive data from minors across school and consumer segments.

Market Opportunities

- Expansion of Corporate E-Learning: Growing demand for upskilling and reskilling programs among Turkey's workforce, driven by digital transformation across sectors such as banking, manufacturing, and retail, presents a significant opportunity for enterprise-focused education app providers.

- AI Tutoring and Adaptive Assessment Tools: The rising adoption of AI-powered tutoring apps, automated grading tools, and adaptive assessment platforms creates new product differentiation opportunities for both domestic and international education app providers targeting Turkey's exam-intensive education system.

- Rural and Tier-2 City Penetration: Government broadband expansion initiatives and declining mobile data costs are opening new user acquisition opportunities in underserved regions, where demand for affordable, accessible digital education solutions is rising rapidly.

Market Challenges

- Monetization in a Price-Sensitive Market: Turkey's price-sensitive consumer base and strong preference for free or freemium content models create challenges for education app providers seeking to convert free users to paid subscriptions, compressing revenue per user compared to more mature markets.

- Intense Competition from Global Platforms: Dominant global education apps operate with significant scale advantages, strong brand recognition, and large content libraries, creating intense competitive pressure for smaller domestic Turkish education app providers.

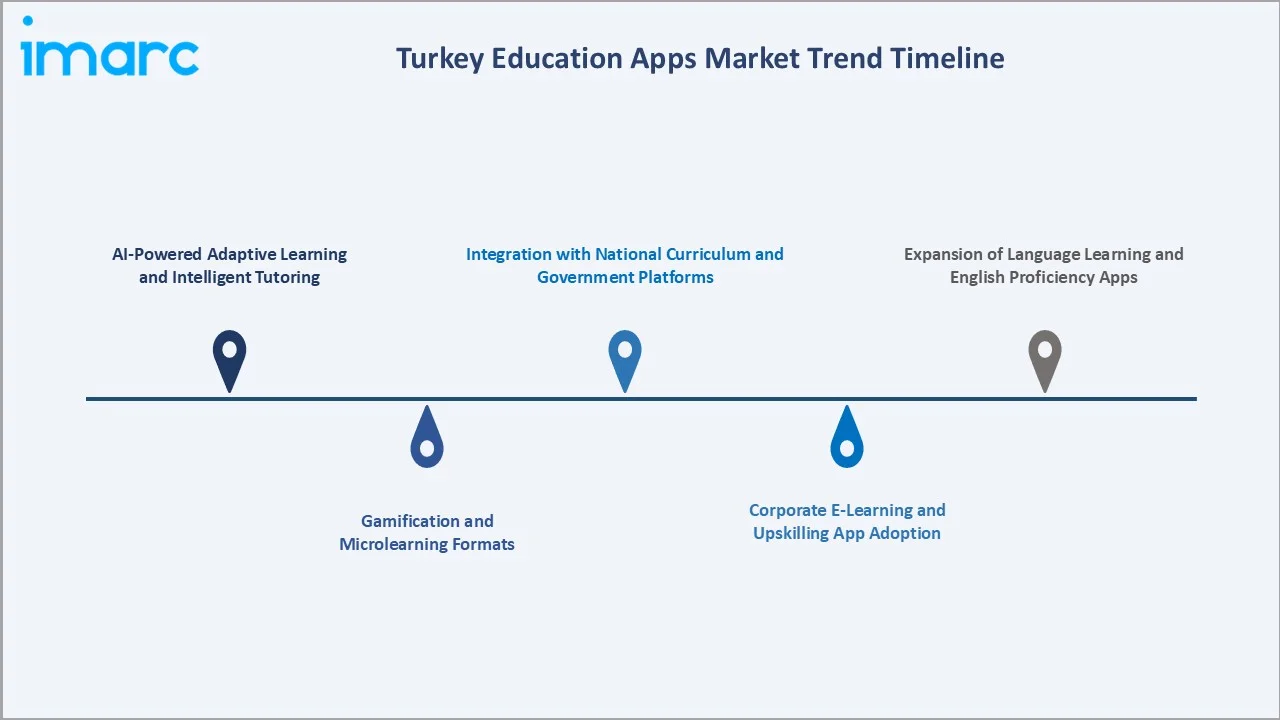

Emerging Market Trends

1. AI-Powered Adaptive Learning and Intelligent Tutoring

Education app providers in Turkey are increasingly deploying AI and ML algorithms to deliver personalized learning experiences, adaptive content sequencing, and intelligent tutoring systems. These tools analyze individual learning patterns, identify knowledge gaps, and adjust content difficulty in real time, significantly improving student engagement and learning outcomes across K-12 and exam preparation segments.

2. Gamification and Microlearning Formats

Short-form, gamified learning modules are rapidly gaining traction across Turkey's education app landscape, particularly among younger learners seeking engaging alternatives to traditional study methods. Platforms integrating points systems, achievement badges, leaderboards, and bite-sized lesson formats are reporting higher daily active user rates and longer average session durations, driving better retention metrics and stronger subscription conversion in the competitive Turkish education app market.

3. Integration with National Curriculum and Government Platforms

A growing number of education app developers are aligning their content with Turkey's Ministry of National Education curriculum standards and integrating with government-operated platforms. This alignment enables apps to position themselves as official supplementary learning tools, access school distribution channels, and build credibility with parents and educators, accelerating user acquisition across both public and private school segments.

4. Corporate E-Learning and Upskilling App Adoption

The rapid digital transformation of Turkish enterprises across the banking, manufacturing, retail, and technology sectors is driving accelerating adoption of mobile-first corporate learning apps. Companies are deploying education apps for onboarding, compliance training, and technical upskilling programs, with mobile delivery enabling employees in distributed locations to access training content on-demand.

5. Expansion of Language Learning and English Proficiency Apps

Strong demand for English language proficiency among Turkish students and professionals is fueling significant growth in language learning app adoption. The emphasis on English skills in Turkey's university entrance system and corporate hiring criteria is sustaining year-round user engagement with language learning platforms, supporting consistent revenue generation for providers operating in this segment.

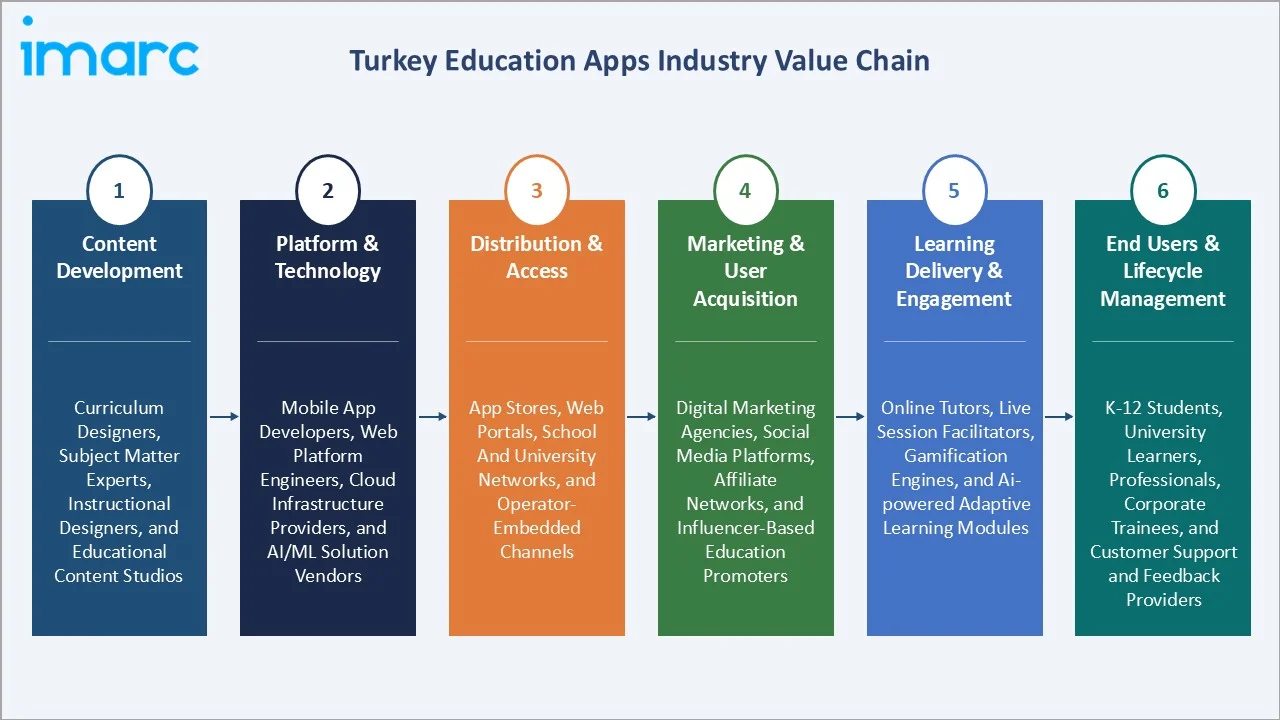

Industry Value Chain Analysis

The Turkey education apps value chain spans six stages from content creation through end user engagement and lifecycle management. Platform development, AI integration, and user acquisition capture the highest value-add, while curriculum alignment and government partnerships increasingly determine competitive position in this regulated and academically oriented category.

|

Stage |

Key Players / Examples |

|

Content Development |

Curriculum designers, subject matter experts, instructional designers, and educational content studios |

|

Platform & Technology |

Mobile app developers, web platform engineers, cloud infrastructure providers, and AI/ML solution vendors |

|

Distribution & Access |

App stores, web portals, school and university networks, and operator-embedded channels |

|

Marketing & User Acquisition |

Digital marketing agencies, social media platforms, affiliate networks, and influencer-based education promoters |

|

Learning Delivery & Engagement |

Online tutors, live session facilitators, gamification engines, and AI-powered adaptive learning modules |

|

End Users & Lifecycle Management |

K-12 students, university learners, professionals, corporate trainees, and customer support and feedback providers |

Vertically integrated players that own proprietary content libraries, AI-powered adaptive learning engines, and direct user acquisition channels are positioned to capture greater value than those reliant on third-party content or platform infrastructure.

Technology Landscape in the Turkey Education Apps Industry

AI and Adaptive Learning Engines

Education app providers in Turkey are deploying AI-powered adaptive learning systems that analyze student performance data to personalize content delivery, adjust difficulty levels, and generate targeted practice sets. These systems leverage natural language processing for intelligent tutoring interactions and computer vision for handwriting recognition in math and science applications.

Cloud Infrastructure and Content Delivery Networks

Scalable cloud platforms are enabling Turkish education app operators to deliver high-quality video lessons, interactive simulations, and live tutoring sessions with low latency across the country. Content delivery networks optimized for Turkish geography ensure reliable access for users in both metropolitan and regional locations.

Data Analytics and Learning Management Systems

Advanced data analytics dashboards integrated into education apps are enabling teachers, parents, and corporate training managers to track learner progress, identify performance gaps, and optimize instructional interventions. Learning management system integrations allow apps to connect with institutional platforms used by Turkish universities and enterprises for centralized training administration.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Mobile Based |

64.3% |

2025 |

|

Operating System |

Android |

58.6% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Marmara |

29.5% |

2025 |

By Product Type

Mobile based commands a 64.3% majority share in 2025, driven by the widespread availability of affordable smartphones across Turkey, seamless app store distribution, and strong consumer preference for flexible, on-the-go learning formats. The segment benefits from low barriers to discovery, app store algorithm-driven user acquisition, and the ability to deliver push notifications that drive high daily engagement.

To access detailed market analysis, Request Sample

Web based at 35.7% in 2025 remains significant for desktop and laptop-centric learning environments, particularly in higher education institutions, corporate training departments, and government-administered platforms. Web delivery supports richer interactive content, collaborative learning tools, and integration with institutional learning management systems.

By Operating System

Android dominates the operating system segment with a 58.6% share in 2025, reflecting the strong penetration of mid-range Android smartphones across Turkish households. The availability of affordable devices makes Android-based education apps accessible across a broad income spectrum, supporting strong volume-driven growth.

iOS and MacOS at 28.4% capture premium learner segments, particularly urban university students and professionals using Apple devices. Their strong presence in higher-income demographics supports demand for advanced learning applications, subscription-based educational content, and productivity-focused digital learning tools.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Marmara |

29.5% |

High urban concentration in Istanbul, strong digital infrastructure, large student and professional population, and high smartphone adoption |

|

Central Anatolia |

18.6% |

Government-backed digital education programs, Ankara-based academic institutions, and rising demand for university and exam preparation apps |

|

Aegean |

14.2% |

Growing tech ecosystem, expanding higher education enrollment, and increasing adoption of English language learning apps |

|

Mediterranean |

12.8% |

Rising youth population, expanding vocational training needs, and growing use of mobile-based skill development applications |

|

Black Sea |

9.6% |

Increasing internet penetration in smaller cities, growing demand for remote learning solutions, and rising awareness of digital education tools |

|

Southeastern Anatolia |

8.1% |

Government-led digital inclusion initiatives, growing school-age population, and expanding mobile internet coverage in underserved areas |

|

Eastern Anatolia |

7.2% |

Rural digitization programs, expanding mobile connectivity, and increasing youth engagement with accessible online learning platforms |

Marmara at 29.5% in 2025 leads the regional landscape, anchored by Istanbul's large and diverse student population, high concentration of private tutoring demand in Turkey, and strong digital adoption across both public and private school networks.

Central Anatolia at 18.6% is supported by Ankara's dense academic and government institutional base. The region benefits from strong adoption of digital learning platforms among university students and professional learners.

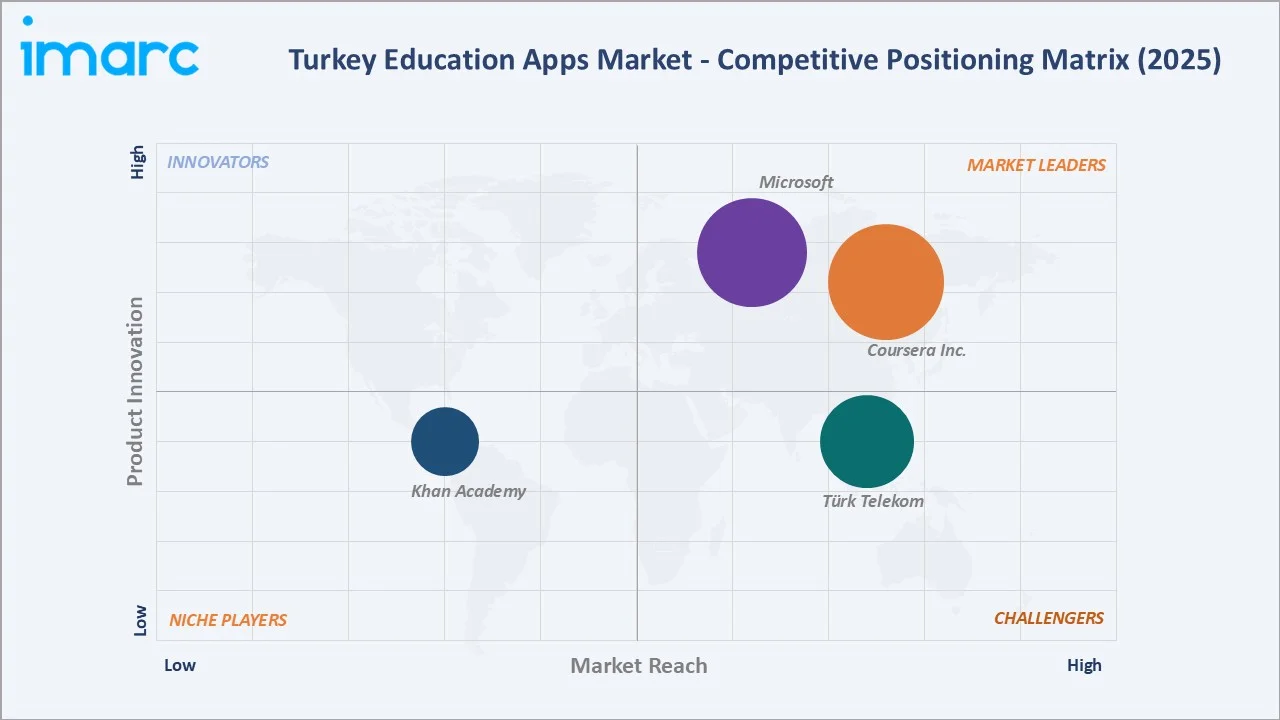

Competitive Landscape

The Turkey education apps market is moderately fragmented, with established global platforms leading user reach and product depth while domestic players compete on curriculum alignment, Turkish language content, and local institutional partnerships. Brand recognition, AI-powered personalization, curriculum compliance, and pricing strategy form the key competitive differentiators in the Turkish market.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Coursera Inc. |

Coursera and Udemy |

Leader |

Combined platform serving millions of learners; expanding university, enterprise, and skills-based learning globally |

|

Microsoft |

Microsoft Education |

Leader |

Collaboration and hybrid learning solutions for schools and universities |

|

Türk Telekom |

Vitamin LGS |

Challenger |

Domestic K-12 curriculum-aligned content and AI-powered adaptive learning |

|

Khan Academy |

Khan Academy |

Niche Player |

Free personalized learning for students across core academic subjects globally |

Key players include Coursera Inc., Microsoft, Türk Telekom, and Khan Academy, among others.

Key Company Profiles

Coursera Inc.

Coursera Inc. is a leading online learning platform headquartered in Mountain View, California, offering a broad range of digital education products, including online courses, professional certificates, and degree programs, developed in partnership with universities and industry organizations worldwide. The platform serves individual learners, enterprises, and government institutions across multiple countries, including Turkey.

- Product Portfolio: Platforms offering online courses, professional certificates, specializations, and degree programs across technology, business, data science, healthcare, and social sciences, with multi-language interface support, including Turkish.

- Recent Development: Coursera completed its combination with Udemy in May 2026, creating a combined platform with more than USD 1.5 Billion in annual pro-forma revenue in 2025.

- Strategic Focus: Expanding enterprise and university learning partnerships, scaling AI-powered personalized learning tools, and broadening access to internationally recognized credentials for learners in emerging markets.

Microsoft

Microsoft is a global technology company offering a comprehensive suite of education-focused products and services under the Microsoft Education brand. Its education solutions are deployed across schools, universities, and corporate training environments in Turkey and internationally, supporting digital learning through cloud-based collaboration and productivity tools.

- Product Portfolio: Microsoft Education suite including Microsoft Teams for Education, Microsoft 365 Education, and AI-powered learning tools.

- Recent Developments: Microsoft has been expanding its AI-powered Copilot features across the Microsoft 365 Education suite, enabling AI-assisted lesson planning, personalized feedback, and inclusive learning tools for students and educators in schools and universities globally.

- Strategic Focus: Integrating AI capabilities across education products, expanding cloud-based digital learning infrastructure in schools and universities, and supporting educator development through programs.

Khan Academy

Khan Academy is a non-profit educational organization that provides free, high-quality digital learning content through a mobile and web-based platform available in multiple languages, including Turkish. The platform supports learners across K-12 subjects, test preparation, and core academic skills, and is accessible to students and teachers in Turkey.

- Product Portfolio: Khan Academy free learning platform covering K-12 mathematics, science, computing, humanities, and test preparation, with Turkish-language content available through the localized platform and AI-powered tutoring support through Khanmigo.

- Recent Development: Khan Academy has been expanding its AI-powered tutoring assistant Khanmigo across its platform, providing personalized learning guidance and interactive problem-solving support for students across core academic subjects globally.

- Strategic Focus: Expanding free access to quality education for underserved learner populations, deepening Turkish-language content offerings, and scaling AI-powered personalized learning tools to support student outcomes across K-12 subjects.

Market Concentration Analysis

The Turkey education apps market is moderately fragmented, with major international technology and online learning platforms maintaining broad user reach across multiple educational segments. At the same time, regional and domestic providers hold strong positions in curriculum-aligned K–12 learning solutions, test preparation applications, language learning platforms, and corporate e-learning services.

Barriers to entry include high content development costs for curriculum-aligned Turkish materials, compliance requirements, the need for Ministry of National Education accreditation for school-facing apps, and the scale advantages held by global platforms in AI capability development and brand recognition.

Consolidation is gradually occurring as international platforms acquire local content providers and domestic players seek strategic partnerships with global technology companies. The growing emphasis on AI-powered personalization, adaptive learning, and data analytics is further reinforcing competitive moats for well-capitalized incumbents with established user bases.

Investment & Growth Opportunities

Fastest-Growing Segments

Mobile based is expanding the fastest among product type segments, driven by Turkey's surging smartphone penetration and the growing preference for flexible, on-demand learning among students and professionals.

Emerging Markets

Central Anatolia is among the fastest-growing regions, supported by Ankara's academic density and strong government digital education programs. Southeastern Anatolia and Eastern Anatolia represent significant untapped opportunities for education app providers able to deliver affordable, offline-capable, Turkish-language content tailored to the specific curriculum needs and infrastructure constraints of these emerging digital markets.

Venture & Investment Trends

Investment is concentrated in AI-powered tutoring platforms, adaptive assessment tools, and language learning applications. Capital is also flowing into corporate e-learning solutions, mobile-first exam preparation apps, and EdTech startups developing Turkish-language content aligned with the university entrance examination system. Strategic partnerships between international platforms and domestic content developers represent a growing investment theme.

Future Market Outlook (2026-2034)

The Turkey education apps market is forecast to expand from USD 66.06 Million in 2025 to USD 377.36 Million by 2034 at a CAGR of 20.60%, adding approximately USD 311.30 Million in incremental annual market value over the forecast period, passing through USD 168.54 Million in 2030.

Four forces will shape the market through 2034: continued government investment in digital education infrastructure and curriculum digitization; the rapid integration of AI-powered adaptive learning and intelligent tutoring systems; expanding corporate e-learning adoption driven by workforce digital transformation across Turkish industries; and increasing demand from Turkey's large youth population for exam preparation, language learning, and skills development applications.

By 2034, the Turkey education apps market is expected to be defined by AI-personalized, mobile-first learning experiences tightly integrated with national curriculum standards, with exam preparation and language learning segments collectively accounting for a significantly higher share of overall market activity. Regulatory alignment with Turkey's data protection framework and deeper integration with government education platforms are expected to further shape the competitive dynamics of the market.

Research Methodology

Primary Research

Primary research included structured interviews with education app platform executives, Ministry of National Education digital education program managers, school and university IT administrators, corporate training managers, and consumer research participants across major Turkish cities, validating market sizing, regional demand patterns, segment mix, and technology adoption trends.

Secondary Research

Secondary sources included Turkey's Ministry of National Education publications, Turkish Statistical Institute (TurkStat) digital economy and education statistics, annual reports and investor presentations from listed education technology companies, and app store performance data for the Turkey market.

Forecasting Models

Market forecasts used top-down and bottom-up models combining digital device penetration data, education app download and revenue trends, operating system market share data, regional demographic variables, and government digital education investment projections. Scenario analysis addressed curriculum digitization pace, AI adoption rates, and changes in data protection regulation.

Turkey Education Apps Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Web Based, Mobile Based |

| Operating Systems Covered | IOS and MacOS, Android, Windows |

| End Users Covered | K-12 Education, Higher Education, Business Institutions |

| Regions Covered | Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, Eastern Anatolia |

| Companies Covered | Coursera Inc., Microsoft, Türk Telekom, Khan Academy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Turkey education apps market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Turkey education apps market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Turkey education apps industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Turkey Education Apps Market Report

The Turkey education apps market was valued at USD 66.06 Million in 2025, driven by government digital education initiatives, rising smartphone adoption, and growing demand for exam preparation and language learning applications.

The market is projected to grow at a CAGR of 20.60% from 2026 to 2034, reaching USD 377.36 Million, supported by AI integration, expanding mobile internet access, and rising corporate e-learning adoption.

Mobile based apps lead at 64.3% in 2025, driven by widespread smartphone penetration, seamless app store distribution, and strong consumer preference for flexible, on-demand learning experiences.

Android dominates at 58.6% in 2025, reflecting strong penetration of affordable mid-range Android smartphones across Turkish households from leading brands.

Marmara commands 29.5% in 2025, led by Istanbul's large student population, high private tutoring demand, and advanced digital infrastructure across the region.

Leading players include Coursera Inc., Microsoft, Türk Telekom, and Khan Academy, among others.

AI enables adaptive learning paths, intelligent tutoring, personalized content recommendations, and automated assessment tools, significantly improving student engagement and learning outcomes across K-12 and exam preparation app segments in Turkey.

Key challenges include monetization in a price-sensitive market, intense competition from global platforms, compliance with Turkey's KVKK data protection law, and persistent digital literacy gaps in rural and underserved regions limiting effective app adoption.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)